Key Insights for South Korea Mobile Payment Industry Market

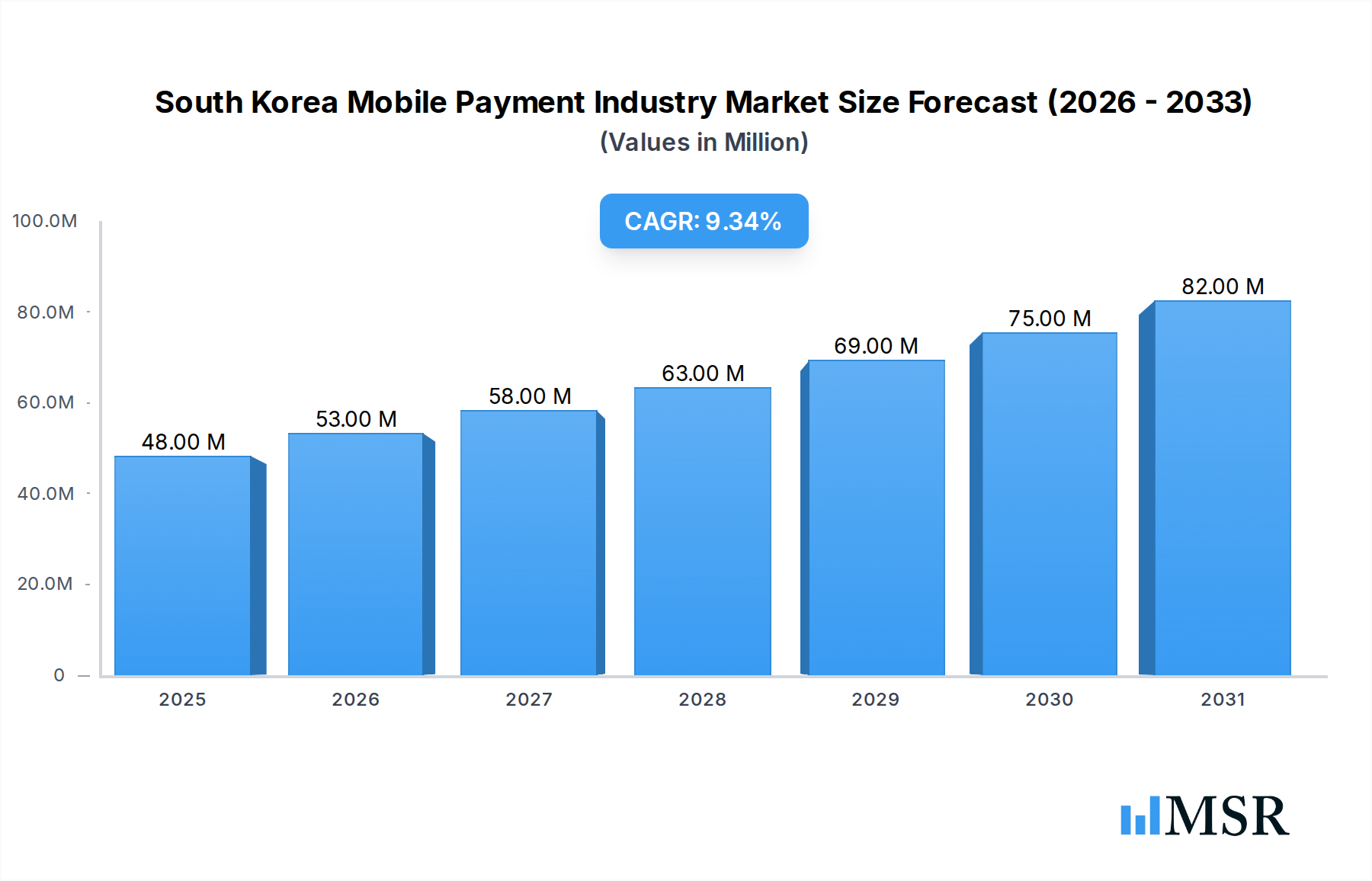

The South Korea Mobile Payment Industry Market is currently valued at $40.67 Million as of 2023, demonstrating robust growth catalyzed by advanced technological adoption and a pervasive digital-first consumer culture. Projections indicate a substantial expansion, with the market expected to reach approximately $74.52 Million by 2030, exhibiting a Compound Annual Growth Rate (CAGR) of 9.13% over the forecast period. This significant growth trajectory is primarily underpinned by the increasing adoption of mobile devices across the populace, coupled with a surging demand and inclination towards e-commerce and online shopping. The extensive penetration of smartphones and high-speed internet infrastructure provides a fertile ground for the proliferation of various mobile payment solutions, from Proximity Payment Market systems leveraging Near Field Communication (NFC) to Remote Payment Market solutions facilitating seamless online transactions.

South Korea Mobile Payment Industry Market Size (In Million)

Macroeconomic tailwinds include the government's initiatives to foster a cashless society, the continuous innovation by leading Fintech Market players, and the rapid digitalization across multiple industry verticals. The E-commerce Market acts as a pivotal growth engine, continually driving transaction volumes and encouraging the integration of sophisticated payment gateways. Consequently, the demand for secure and efficient Online Payment Gateway Market solutions is at an all-time high, crucial for both B2C and increasingly B2B payment types. However, this promising landscape is not without its challenges. The market faces significant restraints from growing cyber threats, which necessitate continuous investment in robust security protocols and stringent regulatory compliance to maintain consumer trust and prevent fraud. Despite these challenges, the prevailing trend indicates that the e-commerce industry will continue to be a primary catalyst for market growth, fostering innovation in Mobile Apps Market and advanced payment technologies.

South Korea Mobile Payment Industry Company Market Share

The competitive landscape is dominated by a few key domestic players, including Kakao Pay, Samsung Pay, and Naver Pay, who continuously innovate to capture larger market shares through enhanced user experience and diversified service offerings. The adoption of NFC Technology Market and QR Code Payment Market solutions is expanding rapidly, reflecting a preference for convenient and instantaneous transactions. The robust regulatory framework, coupled with high consumer digital literacy, supports the continued expansion of the overall Digital Payment Market in South Korea. The market is expected to witness further consolidation and strategic partnerships as companies vie for technological leadership and expanded merchant networks, ultimately leading to a more integrated and sophisticated mobile payment ecosystem.

Dominant Payment Mode Segment in South Korea Mobile Payment Industry Market

Within the South Korea Mobile Payment Industry Market, the Remote Payment Market segment currently holds a dominant position, primarily due to the overwhelming inclination of consumers towards e-commerce and online shopping. While Proximity Payment Market solutions, leveraging technologies such as Near Field Communication (NFC) and QR codes, have seen significant adoption in brick-and-mortar retail environments, the sheer volume and value of transactions processed remotely through various online channels significantly contribute to the remote payment segment's larger revenue share. This dominance is intrinsically linked to South Korea's highly developed e-commerce infrastructure and its digitally native population, where online purchases for goods, services, and digital content are commonplace.

The Remote Payment Market encompasses transactions made via mobile applications, mobile web browsers, and direct mobile billing, where the payer and payee are not physically present at the point of interaction. Key players like Kakao Pay and Naver Pay, deeply integrated with popular messaging and search platforms, respectively, have solidified their control over this segment. Their comprehensive ecosystems offer not only payment functionalities but also loyalty programs, remittances, and investment services, making them indispensable for millions of users engaging in online commercial activities. Mobile Apps Market solutions from these providers facilitate everything from ordering groceries to paying utility bills, blurring the lines between communication, commerce, and finance.

The market's structural evolution, driven by the E-commerce Market boom, has further entrenched remote payments. The convenience of one-click purchases, secure saved payment details, and seamless integration with online retail platforms have made remote transactions the default for a vast majority of digital interactions. While the QR Code Payment Market has gained traction for both proximity and remote payments, its impact is often more pronounced in remote scenarios for bill payments or specific online vendor interactions. The B2C payment type within the Remote Payment Market is particularly vibrant, driven by consumer goods, digital subscriptions, and entertainment services. The ongoing trend of digital transformation across industries, including media & entertainment and BFSI, ensures continued growth for remote payment solutions. Despite the rise of NFC Technology Market for in-store payments, the strategic advantage and established user base of remote payment platforms, coupled with the inherent flexibility they offer, ensure their continued leadership within the South Korea Mobile Payment Industry Market, with their market share expected to consolidate further as digital lifestyles become even more ingrained.

Key Market Drivers & Constraints in South Korea Mobile Payment Industry Market

The South Korea Mobile Payment Industry Market is propelled by several robust drivers, primarily the increasing adoption of mobile devices and the surging demand for e-commerce and online shopping. South Korea boasts one of the highest smartphone penetration rates globally, with over 95% of the population owning a smartphone, significantly exceeding the global average. This widespread availability of mobile devices forms the foundational infrastructure for mobile payment services, transforming how consumers interact with financial transactions. The ubiquity of smartphones directly correlates with higher engagement in Mobile Apps Market for financial activities, fueling the growth of the overall Digital Payment Market. This high penetration ensures a large potential user base for new payment solutions and facilitates the rapid rollout of updates and innovative features by Fintech Market players.

Complementing this, the growing demand and inclination towards e-commerce and online shopping provide a consistent stream of transaction volume for mobile payments. South Korea's E-commerce Market is one of the most developed globally, with annual online transaction values regularly setting new records. Consumers increasingly rely on online platforms for everything from daily necessities to luxury goods, leading to a profound shift from traditional payment methods to mobile-centric solutions. This trend has naturally amplified the demand for efficient and secure Online Payment Gateway Market services, making mobile payments an indispensable component of the online retail experience. Companies like Coupang and SSG.com Corp, major e-commerce players, integrate mobile payment solutions directly, driving user adoption.

Conversely, a significant constraint impeding the South Korea Mobile Payment Industry Market is the growing threat of cybercrime and data breaches. As the volume and value of mobile transactions increase, so does the attractiveness of these platforms for malicious actors. High-profile cyberattacks or data leaks can severely erode consumer trust, leading to hesitation in adopting or continuing to use mobile payment services. This necessitates continuous, substantial investment in cybersecurity infrastructure, advanced encryption protocols, and real-time fraud detection systems. Regulatory bodies and payment service providers face immense pressure to ensure the highest levels of security, as any perceived vulnerability could have a cascading negative impact on user adoption and market growth. The complexity of securing diverse payment technologies, from NFC Technology Market to QR codes, adds to this challenge, requiring a multi-layered security approach to protect sensitive financial data.

Competitive Ecosystem of South Korea Mobile Payment Industry Market

The South Korea Mobile Payment Industry Market is characterized by intense competition among several dominant domestic players and a dynamic landscape of emerging Fintech Market innovators. The absence of specific URLs in the provided data means company names are presented as plain text.

- Kakao Pay: A leading mobile payment service, integrated within the popular KakaoTalk messaging app, offering a wide array of financial services from payments and remittances to investments.

- Samsung Pay: Leveraging Samsung's widespread smartphone presence, this service utilizes NFC and MST (Magnetic Secure Transmission) technologies, providing broad acceptance at both traditional and modern POS terminals.

- Toss: Operated by Viva Republica, Toss is a rapidly growing fintech platform known for its user-friendly interface and diverse financial services, including peer-to-peer transfers, investment, and insurance.

- PayCo: A payment service from NHN Entertainment, primarily focused on online payments and integrated with various e-commerce and content platforms, offering loyalty programs and discounts.

- SK Group: While a conglomerate, SK Group's various subsidiaries, notably SK Telecom, contribute to the mobile payment ecosystem through services like T Pay, leveraging their extensive telecommunications infrastructure.

- L Pay: Operated by Lotte Group, L Pay is integrated across Lotte's vast retail empire, including department stores, supermarkets, and online malls, catering to a loyal customer base.

- ZeroPay Pvt. Ltd.: A QR code-based payment service supported by the Seoul Metropolitan Government and various financial institutions, designed to reduce merchant transaction fees, particularly for small businesses.

- Coupang: As a dominant e-commerce player, Coupang offers its proprietary payment solution, Coupay, providing seamless checkout experiences within its extensive online marketplace.

- SSG.com Corp: Affiliated with Shinsegae Group, SSG.com provides SSG Pay, a mobile payment service deeply integrated with Shinsegae's online and offline retail outlets, similar to L Pay.

- Naver Pay: Directly integrated with South Korea's most popular search engine, Naver, Naver Pay offers robust online payment, loyalty points, and a growing presence in offline transactions through QR code technology.

This ecosystem is marked by continuous innovation, strategic partnerships, and fierce competition to expand user bases and merchant networks, especially in the E-commerce Market and the burgeoning Digital Payment Market segments.

Recent Developments & Milestones in South Korea Mobile Payment Industry Market

The South Korea Mobile Payment Industry Market continues to evolve rapidly, marked by strategic alliances, service expansions, and technological integrations. These developments underscore the dynamic nature of the Digital Payment Market and the commitment of key players to innovation and market expansion.

February 2024: The TWQR mobile payment service officially launched in South Korea, marking a significant advancement in cross-border payment interoperability. This service, now accessible at 35,000 merchant locations across the East Asian nation, represents a collaborative effort between two prominent Taiwanese financial organizations and the South Korean financial services giant BC Card Co. The introduction of TWQR aims to facilitate seamless transactions for Taiwanese tourists and business travelers in South Korea, enhancing convenience and boosting the adoption of

QR Code Payment Marketsolutions in a cross-border context. This initiative not only strengthens bilateral economic ties but also sets a precedent for future international payment collaborations, driving the global accessibility of mobile payment systems.April 2023: Kakao Pay, a leading online payment service and a subsidiary of the South Korean messaging and internet conglomerate Kakao, announced a strategic move into the global financial markets by acquiring a minority stake in Siebert Financial. This New York-based brokerage firm received an investment of USD 17 million from Kakao Pay, resulting in the South Korean company securing a 19.9% stake. This acquisition is a testament to Kakao Pay's ambition to diversify its financial services portfolio beyond domestic mobile payments and remittances, venturing into the competitive US brokerage landscape. It signifies a broader trend among major

Fintech Marketplayers to expand their global footprint and offer a more comprehensive suite of financial products, potentially integrating brokerage services with their existingMobile Apps Marketpayment platforms.

Regional Market Breakdown for South Korea Mobile Payment Industry Market

While the scope of this report focuses specifically on the South Korea Mobile Payment Industry Market as a singular geographic entity, analysis of distinct dynamics within this national market can illuminate various "regional" nuances in adoption and growth. For the purpose of providing a comprehensive breakdown, we consider key economic zones and demographic segments within South Korea as distinct conceptual regions, each exhibiting unique characteristics influencing mobile payment penetration and usage patterns. This approach helps understand localized demand drivers and maturity levels, even without separate quantitative data for internal regions.

1. Seoul Metropolitan Area (SMA): This region, encompassing Seoul, Incheon, and Gyeonggi Province, represents the most mature and technologically advanced segment of the market. It exhibits the highest mobile payment adoption rates, driven by a dense urban population, high smartphone penetration, and a vast network of merchants supporting various Proximity Payment Market and Remote Payment Market solutions. The SMA acts as an innovation hub, quickly embracing new technologies like NFC Technology Market and advanced Mobile Apps Market for payments. Competition is fierce here, leading to continuous innovation and diversified services, including those from Kakao Pay and Naver Pay. Demand is primarily driven by convenience for daily commutes, high e-commerce activity, and sophisticated consumer preferences.

2. Busan-Ulsan-Gyeongnam Region (Southeast Coast): As a major industrial and port region, this area shows strong growth, particularly in B2B and logistics-related mobile payments. While slightly behind the SMA in early adoption, its growing younger population and increasing digital literacy are accelerating the uptake of consumer-facing mobile payment solutions. The E-commerce Market penetration is robust, and there's a steady shift from traditional banking to Digital Payment Market services. Demand drivers include a burgeoning middle class, industrial supply chain digitalization, and expanding tourism infrastructure, which fuels demand for efficient transaction processing.

3. Jeju Island (Tourism & Hospitality Focus): This unique "region" is characterized by its heavy reliance on tourism. Mobile payment adoption here is heavily influenced by the influx of domestic and international visitors. Solutions supporting QR Code Payment Market for simplified transactions, especially with diverse international visitors, are gaining traction. Local businesses are rapidly integrating mobile payment terminals to cater to a transient, digitally-savvy customer base. The primary demand driver is the need for seamless, multi-currency-friendly, and quick payment options in the hospitality, F&B, and retail sectors catering to tourists. This region often sees faster adoption of payment trends that enhance visitor experience.

4. Rural and Provincial Areas (Developing Adoption): These areas, outside major metropolitan and industrial zones, represent a more nascent segment of the South Korea Mobile Payment Industry Market. While smartphone penetration remains high, the pace of merchant adoption and consumer comfort with mobile payments can be slower due to cultural preferences for cash or traditional card payments, and potentially less robust internet infrastructure in very remote locations. However, government initiatives like ZeroPay, aimed at reducing merchant fees, are fostering growth. Demand drivers include increasing access to broadband, younger generations migrating back from urban areas, and the expanding reach of online grocery and retail services making Remote Payment Market solutions more necessary. This segment is considered to be the fastest-growing in percentage terms, albeit from a lower base, as digital inclusion initiatives bridge the technological gap.

South Korea Mobile Payment Industry Regional Market Share

Pricing Dynamics & Margin Pressure in South Korea Mobile Payment Industry Market

Pricing dynamics within the South Korea Mobile Payment Industry Market are complex, influenced by a combination of intense competition, regulatory oversight, and the evolving technological landscape. Average selling prices (ASPs) for payment services are not typically reflected in direct consumer fees but rather in transaction charges levied on merchants and, indirectly, through interchange fees between financial institutions. The robust competition, particularly among major players like Kakao Pay, Samsung Pay, and Naver Pay, exerts significant margin pressure across the value chain. These providers often engage in aggressive marketing, promotional offers, and loyalty programs to attract and retain both consumers and merchants, which can compress profitability.

Key cost levers for mobile payment providers include infrastructure development and maintenance (especially for NFC Technology Market and QR Code Payment Market deployment), cybersecurity investments to combat growing threats, and compliance with stringent financial regulations. Customer acquisition costs, particularly for small and medium-sized enterprises (SMEs), can also be substantial. Payment service providers typically earn revenue through a percentage of transaction value, subscription fees for premium services, and interest on stored value balances. The trend towards lower merchant discount rates, driven by government policies like ZeroPay aiming to support small businesses, directly impacts the margins of payment facilitators, pushing them to seek alternative revenue streams or increase transaction volumes to compensate.

Commodity cycles, particularly in areas like silicon for NFC chips or data center energy, can indirectly affect operational costs, but the primary pressure comes from competitive intensity within the Digital Payment Market and the broader Fintech Market. Companies are forced to differentiate not just on price but also on the breadth of services (e.g., integration with loyalty programs, remittances, micro-investments), user experience, and ecosystem integration. This drive for value-added services, while enhancing customer stickiness, also adds to development and operational expenditures, constantly reshaping the balance between pricing power and profitability for participants in the South Korea Mobile Payment Industry Market.

Customer Segmentation & Buying Behavior in South Korea Mobile Payment Industry Market

Customer segmentation in the South Korea Mobile Payment Industry Market reveals diverse buying behaviors influenced by demographics, technological fluency, and specific use-case requirements. Broadly, the end-user base can be segmented by age, income level, and primary transaction type, each exhibiting distinct purchasing criteria and price sensitivity. The pervasive adoption of the Mobile Apps Market for everyday activities has significantly shaped how these segments interact with payment solutions.

1. Young Adults & Millennials (18-39 years): This segment represents the early adopters and heaviest users of mobile payments. They prioritize convenience, speed, and seamless integration with social media and E-commerce Market platforms. Price sensitivity is lower for daily micro-transactions but higher for service fees on larger transfers. Their purchasing criteria often include comprehensive ecosystem benefits (e.g., loyalty points, discounts, bundled services), ease of peer-to-peer transfers, and robust security features. They are highly responsive to new features, QR Code Payment Market innovations, and gamified payment experiences, often preferring Remote Payment Market for online purchases and Proximity Payment Market via NFC Technology Market for in-store transactions.

2. Middle-Aged Adults (40-59 years): This segment values reliability, security, and integration with established financial institutions. While embracing mobile payments for convenience, they may exhibit higher price sensitivity towards transaction fees and prioritize services with strong brand trust (e.g., Samsung Pay linked to bank cards). Their primary procurement channels include direct bank integrations and trusted financial Mobile Apps Market. They use mobile payments for a mix of online and offline transactions, including bill payments and larger retail purchases. This group often evaluates mobile payment solutions based on practicality and direct utility rather than novelty.

3. Seniors (60+ years): This segment is gradually increasing its adoption, often driven by family influence or necessity for accessing digital services. They are typically the most price-sensitive and prioritize simplicity, ease of use, and strong customer support. Trust in the underlying financial institution is paramount. They tend to favor familiar Online Payment Gateway Market systems or basic Proximity Payment Market options requiring minimal technical interaction. Their procurement channel is often through recommendation or direct assistance, with less independent exploration of new Fintech Market offerings. Notable shifts include increased comfort with mobile banking apps, driven by a desire to avoid physical bank visits.

Overall, a notable shift in buyer preference is towards integrated super-apps that offer a holistic financial and lifestyle experience, blurring the lines between payments, shopping, and social interactions. This reduces the need for multiple apps and consolidates financial activity within a preferred digital ecosystem.

South Korea Mobile Payment Industry Segmentation

-

1. Mode

- 1.1. Proximity Payment

- 1.2. Remote Payment

-

2. Payment Type

- 2.1. B2B

- 2.2. B2C

- 2.3. B2G

-

3. Technology

- 3.1. Near Field Communication (NFC)

- 3.2. QR Code Payment

- 3.3. Mobile Web Payment

- 3.4. Direct Mobile Billing

- 3.5. Mobile Apps

- 3.6. Wireless Application Protocol (WAP)

- 3.7. Others

-

4. Industry Vertical

- 4.1. Media & Entertainment

- 4.2. Retail & E-commerce

- 4.3. BFSI

- 4.4. Automotive

- 4.5. Medical & Healthcare

- 4.6. Transportation

- 4.7. Consumer Electronics

- 4.8. Others

South Korea Mobile Payment Industry Segmentation By Geography

- 1. South Korea

South Korea Mobile Payment Industry Regional Market Share

Geographic Coverage of South Korea Mobile Payment Industry

South Korea Mobile Payment Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.13% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Mode

- 5.1.1. Proximity Payment

- 5.1.2. Remote Payment

- 5.2. Market Analysis, Insights and Forecast - by Payment Type

- 5.2.1. B2B

- 5.2.2. B2C

- 5.2.3. B2G

- 5.3. Market Analysis, Insights and Forecast - by Technology

- 5.3.1. Near Field Communication (NFC)

- 5.3.2. QR Code Payment

- 5.3.3. Mobile Web Payment

- 5.3.4. Direct Mobile Billing

- 5.3.5. Mobile Apps

- 5.3.6. Wireless Application Protocol (WAP)

- 5.3.7. Others

- 5.4. Market Analysis, Insights and Forecast - by Industry Vertical

- 5.4.1. Media & Entertainment

- 5.4.2. Retail & E-commerce

- 5.4.3. BFSI

- 5.4.4. Automotive

- 5.4.5. Medical & Healthcare

- 5.4.6. Transportation

- 5.4.7. Consumer Electronics

- 5.4.8. Others

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. South Korea

- 5.1. Market Analysis, Insights and Forecast - by Mode

- 6. South Korea Mobile Payment Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Mode

- 6.1.1. Proximity Payment

- 6.1.2. Remote Payment

- 6.2. Market Analysis, Insights and Forecast - by Payment Type

- 6.2.1. B2B

- 6.2.2. B2C

- 6.2.3. B2G

- 6.3. Market Analysis, Insights and Forecast - by Technology

- 6.3.1. Near Field Communication (NFC)

- 6.3.2. QR Code Payment

- 6.3.3. Mobile Web Payment

- 6.3.4. Direct Mobile Billing

- 6.3.5. Mobile Apps

- 6.3.6. Wireless Application Protocol (WAP)

- 6.3.7. Others

- 6.4. Market Analysis, Insights and Forecast - by Industry Vertical

- 6.4.1. Media & Entertainment

- 6.4.2. Retail & E-commerce

- 6.4.3. BFSI

- 6.4.4. Automotive

- 6.4.5. Medical & Healthcare

- 6.4.6. Transportation

- 6.4.7. Consumer Electronics

- 6.4.8. Others

- 6.1. Market Analysis, Insights and Forecast - by Mode

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Kakao Pay

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Samsung Pay

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Toss

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 PayCo

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 SK Group

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 L Pay

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 ZeroPay Pvt. Ltd.

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Coupang

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 SSG.com Corp

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Naver Pay

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Others

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 Kakao Pay

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: South Korea Mobile Payment Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: South Korea Mobile Payment Industry Share (%) by Company 2025

List of Tables

- Table 1: South Korea Mobile Payment Industry Revenue Million Forecast, by Mode 2020 & 2033

- Table 2: South Korea Mobile Payment Industry Revenue Million Forecast, by Payment Type 2020 & 2033

- Table 3: South Korea Mobile Payment Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 4: South Korea Mobile Payment Industry Revenue Million Forecast, by Industry Vertical 2020 & 2033

- Table 5: South Korea Mobile Payment Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: South Korea Mobile Payment Industry Revenue Million Forecast, by Mode 2020 & 2033

- Table 7: South Korea Mobile Payment Industry Revenue Million Forecast, by Payment Type 2020 & 2033

- Table 8: South Korea Mobile Payment Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 9: South Korea Mobile Payment Industry Revenue Million Forecast, by Industry Vertical 2020 & 2033

- Table 10: South Korea Mobile Payment Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South Korea Mobile Payment Industry?

The projected CAGR is approximately 9.13%.

2. Which companies are prominent players in the South Korea Mobile Payment Industry?

Key companies in the market include Kakao Pay, Samsung Pay, Toss, PayCo, SK Group, L Pay, ZeroPay Pvt. Ltd., Coupang, SSG.com Corp, Naver Pay, Others.

3. What are the main segments of the South Korea Mobile Payment Industry?

The market segments include Mode, Payment Type, Technology, Industry Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 40.67 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Adoption of Mobile Devices; The Growing Demand and Inclination Towards E-commerce and Online Shopping.

6. What are the notable trends driving market growth?

E-commerce Industry is expected to drive the growth of the market.

7. Are there any restraints impacting market growth?

Growing Cyber Threats in the region.

8. Can you provide examples of recent developments in the market?

Frebruary 2024 - TWQR mobile payment service launched in South Korea. The mobile payment service, available at 35,000 merchants in the East Asian country, is a collaboration between the two Taiwanese organizations and the South Korean financial services company BC Card Co, per the statement.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South Korea Mobile Payment Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South Korea Mobile Payment Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South Korea Mobile Payment Industry?

To stay informed about further developments, trends, and reports in the South Korea Mobile Payment Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence