Key Insights

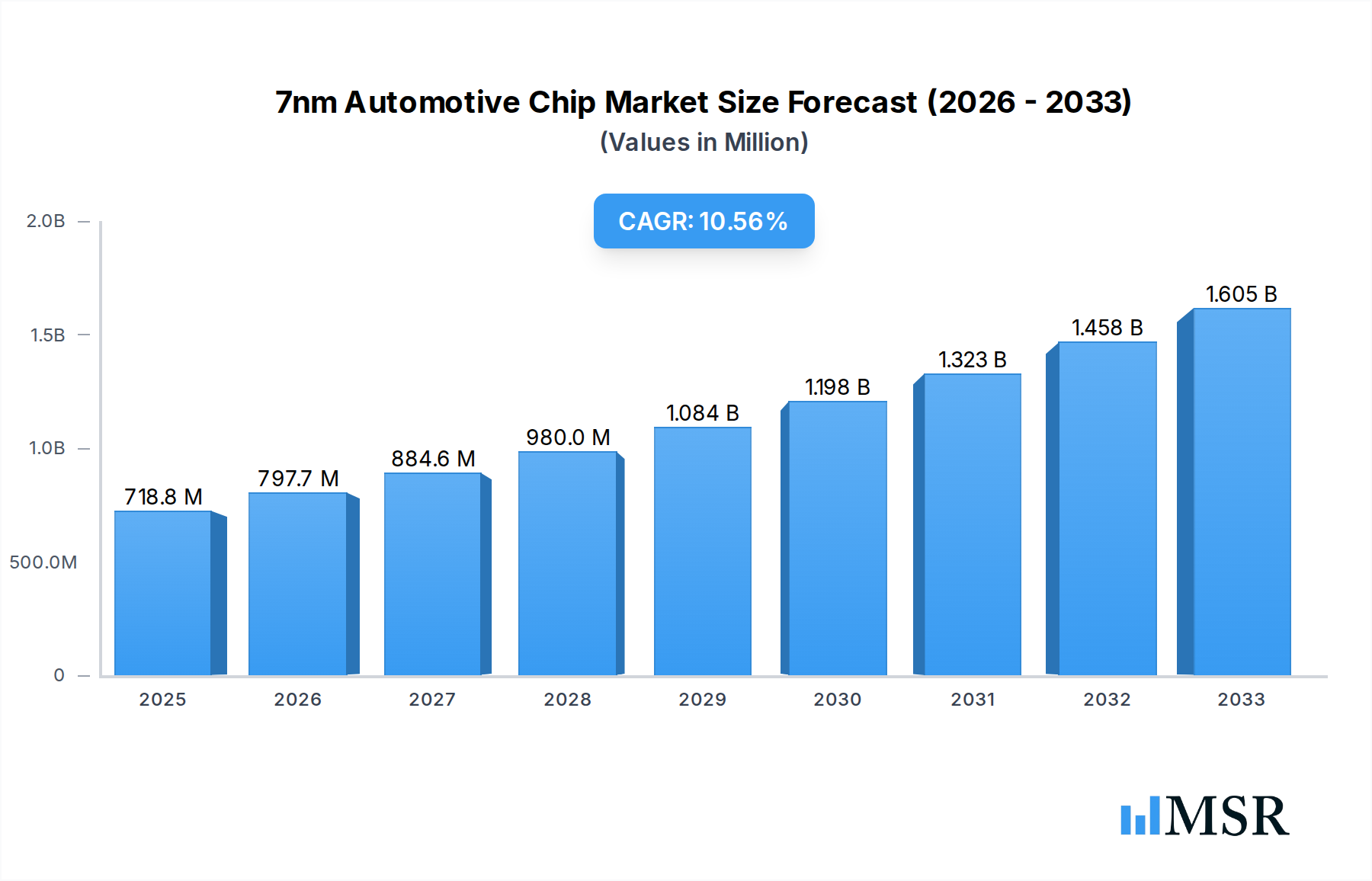

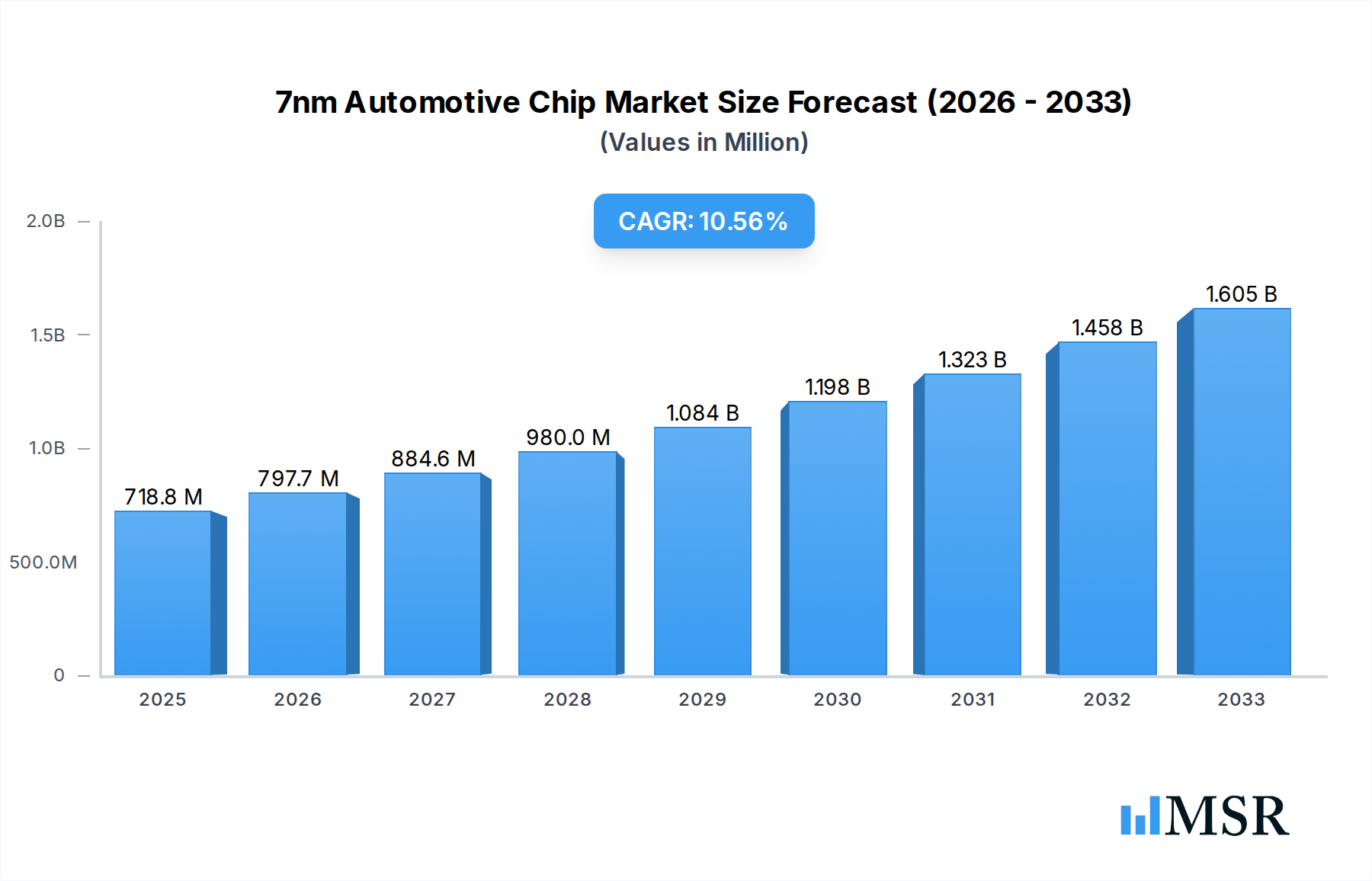

The 7nm automotive chip market is poised for remarkable expansion, driven by the escalating demand for advanced in-car technologies and the rapid integration of Artificial Intelligence (AI) in vehicles. With a projected market size of $718.84 billion in 2025 and an impressive Compound Annual Growth Rate (CAGR) of 10.66%, this sector is set to witness significant value creation throughout the forecast period of 2025-2033. The primary drivers fueling this growth are the increasing sophistication of autonomous driving systems, the proliferation of connected car features, and the burgeoning adoption of electric vehicles (EVs), all of which necessitate powerful and energy-efficient semiconductor solutions. The increasing complexity of infotainment systems and advanced driver-assistance systems (ADAS) further amplifies the need for cutting-edge chip technology.

7nm Automotive Chip Market Size (In Million)

The market's robust growth trajectory is further underscored by prevailing trends such as the transition towards smart cockpits that offer personalized and immersive user experiences, and the continuous miniaturization and performance enhancement of semiconductor manufacturing processes. While the benefits are substantial, the market does face certain restraints, including the high costs associated with advanced semiconductor fabrication and the stringent regulatory landscape governing automotive electronics. Nonetheless, the strategic importance of 7nm chips in enabling next-generation automotive functionalities, from enhanced safety features to advanced connectivity, ensures their central role in shaping the future of mobility. Key players like Qualcomm, Tesla, Huawei, and TSMC are at the forefront, innovating to meet the evolving demands of the automotive industry across critical segments like Commercial Vehicles and Passenger Vehicles.

7nm Automotive Chip Company Market Share

Here is an SEO-optimized, engaging report description for the 7nm Automotive Chip market, incorporating your specified details and structure.

7nm Automotive Chip Market Concentration & Dynamics

The 7nm automotive chip market exhibits a dynamic concentration, driven by a sophisticated innovation ecosystem heavily influenced by Qualcomm, TSMC, and Samsung. These semiconductor manufacturers are at the forefront of advanced node technology, enabling the production of high-performance chips crucial for autonomous driving, smart cockpit systems, and advanced driver-assistance systems (ADAS). Intel and Arm also play pivotal roles, with Arm providing the foundational architecture for many automotive processors. The regulatory framework, though evolving, is increasingly focused on automotive safety standards and data security, impacting chip design and validation. Substitute products, primarily older node chips or alternative processing solutions, are gradually being phased out as the demand for power efficiency and computational power intensifies for electric vehicles (EVs) and connected cars. End-user trends clearly favor integrated, intelligent solutions, pushing manufacturers like Tesla, Huawei, Geely Automobile, and ECARX to invest heavily in next-generation automotive silicon. Merger and acquisition (M&A) activities, though not as prevalent as in broader semiconductor markets, are strategically focused on acquiring specialized IP and talent. Over the study period of 2019–2033, expect a steady increase in M&A deals aimed at consolidating expertise in AI, cybersecurity, and high-performance computing for automotive applications. The market share is currently dominated by a few key players, with TSMC holding a significant portion of the foundry market for 7nm automotive chips.

- Key Players in Foundry: TSMC, Samsung

- Key Players in Chip Design: Qualcomm, Arm, Intel, Huawei

- Key Automotive OEMs Integrating 7nm Chips: Tesla, Geely Automobile, ECARX

- Dominant Application Areas: Smart Cockpit Chip, Autonomous Driving Systems

- Study Period: 2019–2033

- Base Year: 2025

7nm Automotive Chip Industry Insights & Trends

The 7nm automotive chip industry is poised for substantial growth, fueled by an unprecedented surge in demand for advanced computing power within vehicles. The market size is projected to reach billions in the coming years, with a significant Compound Annual Growth Rate (CAGR) anticipated throughout the forecast period of 2025–2033. This growth is primarily driven by the accelerating adoption of connected car technologies, the development of Level 3 and Level 4 autonomous driving capabilities, and the increasing sophistication of in-car infotainment systems and smart cockpits. The transition towards electric vehicles (EVs) also presents a powerful growth catalyst, as EVs often require more complex silicon for battery management, powertrain control, and integrated digital experiences. Technological disruptions, such as the advancement of AI and machine learning algorithms for real-time decision-making in vehicles, are necessitating the use of cutting-edge semiconductor nodes like 7nm to achieve the required performance and power efficiency. Consumer behaviors are rapidly evolving, with buyers expecting a seamless, smartphone-like experience within their vehicles, encompassing advanced navigation, personalized entertainment, and robust connectivity. This evolving demand is pushing automotive manufacturers to differentiate their offerings through superior in-car technology, directly impacting the need for high-performance 7nm automotive chips. Furthermore, the increasing integration of over-the-air (OTA) updates for software and feature enhancements necessitates powerful processors capable of handling complex data processing and management. The synergy between automotive OEMs and semiconductor giants like Qualcomm, TSMC, and Samsung will be crucial in navigating these trends and delivering innovative solutions. The historical period (2019–2024) has laid the groundwork, with early adoption and technological maturation, setting the stage for the explosive growth projected from the base year 2025 onwards. The continuous innovation in chip architectures and manufacturing processes, including advancements in heterogeneous computing and specialized AI accelerators, will further propel the market. The market size for 7nm automotive chips is expected to climb from billions in 2025 to trillions by 2033, underscoring the transformative impact of this technology on the future of mobility.

Key Markets & Segments Leading 7nm Automotive Chip

The Passenger Vehicle segment is currently the dominant force driving the 7nm automotive chip market, with the Smart Cockpit Chip type leading the charge. This dominance is underpinned by several critical factors. Firstly, the sheer volume of passenger vehicles manufactured globally, coupled with an increasing consumer demand for premium in-car experiences, creates a massive market for advanced processing capabilities. The economic growth in key automotive markets, particularly in Asia-Pacific and North America, directly translates into higher disposable incomes and a greater willingness among consumers to invest in vehicles equipped with cutting-edge technology. Infrastructure development, while more directly impacting ADAS and autonomous driving, indirectly supports the smart cockpit trend by enabling seamless connectivity and data transfer necessary for advanced infotainment.

The proliferation of connected car features, such as advanced navigation, high-definition streaming, personalized climate control, and sophisticated voice assistants, all rely heavily on the computational power and efficiency offered by 7nm automotive chips. Smart Cockpit Chip solutions are becoming a key differentiator for automotive brands like Tesla, Geely Automobile, and ECARX, allowing them to offer intuitive user interfaces, immersive digital dashboards, and integrated productivity tools. The Passenger Vehicle segment's adoption of these technologies is further amplified by the fierce competition among OEMs to provide superior user experiences.

Beyond the smart cockpit, the increasing integration of ADAS features in passenger vehicles, even in non-luxury segments, contributes significantly. Features like adaptive cruise control, lane-keeping assist, and automatic emergency braking, while not always requiring the highest-end 7nm processors, benefit from the improved power efficiency and smaller form factors that 7nm nodes enable, allowing for more integrated and less intrusive sensor and processing units. The Commercial Vehicle segment, while a growing area for 7nm chip adoption, particularly for fleet management, telematics, and driver monitoring, is still catching up to the rapid pace of integration seen in passenger cars. The sheer volume and consumer-driven innovation cycle in passenger vehicles, however, firmly establish it as the primary market leading the 7nm automotive chip revolution from 2025 onwards.

- Dominant Segment: Passenger Vehicle

- Leading Chip Type: Smart Cockpit Chip

- Drivers for Passenger Vehicle Dominance:

- High vehicle production volumes

- Strong consumer demand for advanced infotainment and connectivity

- Competitive differentiation through in-car technology

- Increasing adoption of ADAS features

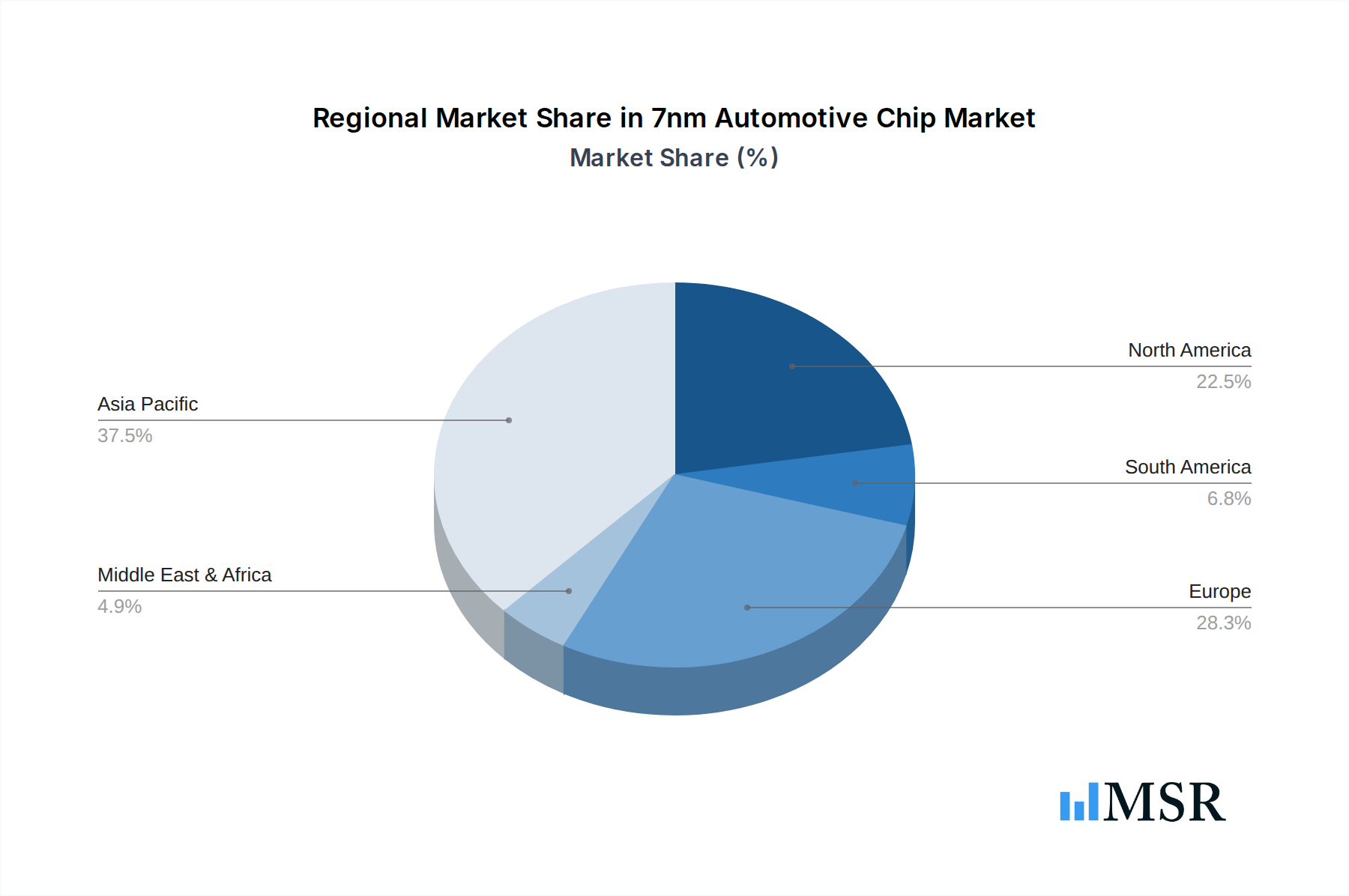

- Key Regions Driving Demand: Asia-Pacific, North America, Europe

- Forecast Period: 2025–2033

7nm Automotive Chip Product Developments

The 7nm automotive chip landscape is characterized by rapid product innovation, driven by the relentless pursuit of enhanced performance, power efficiency, and specialized functionalities. Companies like Qualcomm, Arm, and Intel are consistently rolling out new architectures optimized for automotive workloads. These advancements include integrated AI accelerators for sophisticated machine learning tasks, high-bandwidth memory solutions for faster data processing, and heterogeneous computing platforms that combine CPU, GPU, and specialized processing units for complex algorithms. TSMC and Samsung, as leading foundries, are instrumental in enabling these innovations by providing cutting-edge manufacturing processes that allow for higher transistor density and reduced power consumption. The market relevance of these products lies in their ability to power next-generation autonomous driving systems, advanced driver-assistance systems (ADAS), sophisticated infotainment interfaces, and seamless connectivity solutions, directly contributing to safer, more comfortable, and more intelligent vehicles. These chips are crucial for meeting the increasing demands of connected cars and electric vehicles (EVs).

Challenges in the 7nm Automotive Chip Market

The 7nm automotive chip market faces several significant challenges that could temper its growth trajectory. High development and manufacturing costs associated with leading-edge semiconductor nodes are a primary concern, impacting the profitability of chip manufacturers and potentially leading to higher costs for automotive OEMs. Furthermore, the stringent automotive safety standards and long validation cycles inherent in the automotive industry create a bottleneck for rapid product deployment, extending time-to-market. Supply chain disruptions, exacerbated by geopolitical factors and the inherent complexity of semiconductor manufacturing, pose a continuous risk to production volumes and lead times. Competitive pressures from established players and emerging technologies also necessitate constant innovation and investment, creating a challenging environment for smaller entities. The estimated impact of these challenges can lead to a delay in full market penetration by up to 2 years for certain advanced functionalities.

Forces Driving 7nm Automotive Chip Growth

Several powerful forces are propelling the growth of the 7nm automotive chip market. The exponential rise in vehicle electrification is a primary driver, as EVs often require more sophisticated silicon for battery management, power electronics, and integrated digital experiences. The relentless progress in autonomous driving technology and advanced driver-assistance systems (ADAS) necessitates high-performance computing and AI capabilities that are best delivered by 7nm chips. Increasing consumer demand for enhanced in-car connectivity and immersive smart cockpit experiences is also a significant catalyst. Furthermore, government initiatives and regulatory frameworks promoting vehicle safety and sustainability are indirectly pushing the adoption of advanced automotive electronics. The semiconductor industry's ongoing innovation in advanced node technologies, exemplified by companies like TSMC and Samsung, ensures the availability of powerful and efficient processing solutions.

Long-Term Growth Catalysts for 7nm Automotive Chip Market

Long-term growth for the 7nm automotive chip market will be significantly fueled by continued advancements in artificial intelligence (AI) and machine learning (ML) for autonomous driving, enabling vehicles to interpret complex environments and make real-time decisions. The ongoing evolution of the connected car ecosystem, with its demand for robust data processing and secure communication, will necessitate increasingly powerful silicon. Market expansions into emerging economies and the development of more affordable yet capable 7nm solutions for mainstream vehicles will unlock new customer segments. Strategic partnerships between automotive OEMs, Tier-1 suppliers, and semiconductor manufacturers like Qualcomm and Arm will accelerate innovation and streamline product integration. Furthermore, the development of specialized automotive processors tailored for specific functions, such as advanced sensor fusion or in-cabin sensing, will drive continued demand.

Emerging Opportunities in 7nm Automotive Chip

Emerging opportunities in the 7nm automotive chip market are abundant, driven by the confluence of technological innovation and evolving consumer preferences. The burgeoning market for software-defined vehicles (SDVs) presents a massive opportunity, as these vehicles rely heavily on powerful, upgradeable processors to enable a wide range of functionalities through software. The increasing demand for personalized in-car experiences, extending beyond infotainment to include health monitoring and productivity tools, opens avenues for specialized chip designs. The development of highly integrated domain controllers that consolidate multiple ECUs onto a single powerful chip, enabled by 7nm technology, offers significant cost and efficiency benefits for automotive manufacturers. Furthermore, the potential for edge computing within vehicles to process vast amounts of data locally, reducing reliance on cloud connectivity and enhancing real-time responsiveness, is a key emerging trend. The integration of next-generation communication technologies, such as 5G and beyond, within automotive platforms will also require advanced processing capabilities.

Leading Players in the 7nm Automotive Chip Sector

- Qualcomm

- Tesla

- Huawei

- Geely Automobile

- Arm

- ECARX

- TSMC

- Samsung

- Intel

Key Milestones in 7nm Automotive Chip Industry

- 2019: Qualcomm announces its Snapdragon Ride platform, designed for advanced driver-assistance systems, leveraging 7nm technology.

- 2020: TSMC begins mass production of 7nm chips for automotive applications, significantly boosting supply capabilities.

- 2021: Tesla's FSD (Full Self-Driving) computer, reportedly utilizing custom silicon manufactured on advanced nodes, demonstrates increasing computational demands.

- 2022: Arm launches its next-generation automotive IP portfolio, optimized for high-performance computing on advanced process nodes like 7nm.

- 2023: ECARX, a joint venture between Geely and Baidu, reveals plans to integrate 7nm processors for its intelligent cockpit solutions.

- 2024: Samsung announces significant advancements in its automotive chip foundry services, targeting 7nm and below for future vehicle designs.

Strategic Outlook for 7nm Automotive Chip Market

The strategic outlook for the 7nm automotive chip market is exceptionally positive, driven by the fundamental shift towards intelligent, connected, and increasingly autonomous vehicles. Key growth accelerators include the continued demand for high-performance computing to support advanced driver-assistance systems (ADAS) and autonomous driving, alongside the proliferation of sophisticated smart cockpit functionalities and in-car entertainment. The ongoing transition to electric vehicles (EVs) further amplifies the need for efficient and powerful silicon. Strategic opportunities lie in deepening collaborations between semiconductor manufacturers and automotive OEMs to co-develop customized solutions that meet specific performance and power efficiency targets. The market is poised for significant expansion as 7nm technology becomes more accessible and cost-effective for a wider range of vehicle segments, promising a future of enhanced safety, comfort, and personalized mobility.

7nm Automotive Chip Segmentation

-

1. Application

- 1.1. Commercial Vehicle

- 1.2. Passenger Vehicle

-

2. Type

- 2.1. Smart Cockpit Chip

- 2.2. Others

7nm Automotive Chip Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

7nm Automotive Chip Regional Market Share

Geographic Coverage of 7nm Automotive Chip

7nm Automotive Chip REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.66% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global 7nm Automotive Chip Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Commercial Vehicle

- 5.1.2. Passenger Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Smart Cockpit Chip

- 5.2.2. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America 7nm Automotive Chip Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Commercial Vehicle

- 6.1.2. Passenger Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Smart Cockpit Chip

- 6.2.2. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America 7nm Automotive Chip Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Commercial Vehicle

- 7.1.2. Passenger Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Smart Cockpit Chip

- 7.2.2. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe 7nm Automotive Chip Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Commercial Vehicle

- 8.1.2. Passenger Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Smart Cockpit Chip

- 8.2.2. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa 7nm Automotive Chip Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Commercial Vehicle

- 9.1.2. Passenger Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Smart Cockpit Chip

- 9.2.2. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific 7nm Automotive Chip Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Commercial Vehicle

- 10.1.2. Passenger Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Smart Cockpit Chip

- 10.2.2. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Qualcomm

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Tesla

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Huawei

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Geely Automobile

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Arm

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 ECARX

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 TSMC

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Samsung

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Intel

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 Qualcomm

List of Figures

- Figure 1: Global 7nm Automotive Chip Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global 7nm Automotive Chip Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America 7nm Automotive Chip Revenue (undefined), by Application 2025 & 2033

- Figure 4: North America 7nm Automotive Chip Volume (K), by Application 2025 & 2033

- Figure 5: North America 7nm Automotive Chip Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America 7nm Automotive Chip Volume Share (%), by Application 2025 & 2033

- Figure 7: North America 7nm Automotive Chip Revenue (undefined), by Type 2025 & 2033

- Figure 8: North America 7nm Automotive Chip Volume (K), by Type 2025 & 2033

- Figure 9: North America 7nm Automotive Chip Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America 7nm Automotive Chip Volume Share (%), by Type 2025 & 2033

- Figure 11: North America 7nm Automotive Chip Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America 7nm Automotive Chip Volume (K), by Country 2025 & 2033

- Figure 13: North America 7nm Automotive Chip Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America 7nm Automotive Chip Volume Share (%), by Country 2025 & 2033

- Figure 15: South America 7nm Automotive Chip Revenue (undefined), by Application 2025 & 2033

- Figure 16: South America 7nm Automotive Chip Volume (K), by Application 2025 & 2033

- Figure 17: South America 7nm Automotive Chip Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America 7nm Automotive Chip Volume Share (%), by Application 2025 & 2033

- Figure 19: South America 7nm Automotive Chip Revenue (undefined), by Type 2025 & 2033

- Figure 20: South America 7nm Automotive Chip Volume (K), by Type 2025 & 2033

- Figure 21: South America 7nm Automotive Chip Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America 7nm Automotive Chip Volume Share (%), by Type 2025 & 2033

- Figure 23: South America 7nm Automotive Chip Revenue (undefined), by Country 2025 & 2033

- Figure 24: South America 7nm Automotive Chip Volume (K), by Country 2025 & 2033

- Figure 25: South America 7nm Automotive Chip Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America 7nm Automotive Chip Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe 7nm Automotive Chip Revenue (undefined), by Application 2025 & 2033

- Figure 28: Europe 7nm Automotive Chip Volume (K), by Application 2025 & 2033

- Figure 29: Europe 7nm Automotive Chip Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe 7nm Automotive Chip Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe 7nm Automotive Chip Revenue (undefined), by Type 2025 & 2033

- Figure 32: Europe 7nm Automotive Chip Volume (K), by Type 2025 & 2033

- Figure 33: Europe 7nm Automotive Chip Revenue Share (%), by Type 2025 & 2033

- Figure 34: Europe 7nm Automotive Chip Volume Share (%), by Type 2025 & 2033

- Figure 35: Europe 7nm Automotive Chip Revenue (undefined), by Country 2025 & 2033

- Figure 36: Europe 7nm Automotive Chip Volume (K), by Country 2025 & 2033

- Figure 37: Europe 7nm Automotive Chip Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe 7nm Automotive Chip Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa 7nm Automotive Chip Revenue (undefined), by Application 2025 & 2033

- Figure 40: Middle East & Africa 7nm Automotive Chip Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa 7nm Automotive Chip Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa 7nm Automotive Chip Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa 7nm Automotive Chip Revenue (undefined), by Type 2025 & 2033

- Figure 44: Middle East & Africa 7nm Automotive Chip Volume (K), by Type 2025 & 2033

- Figure 45: Middle East & Africa 7nm Automotive Chip Revenue Share (%), by Type 2025 & 2033

- Figure 46: Middle East & Africa 7nm Automotive Chip Volume Share (%), by Type 2025 & 2033

- Figure 47: Middle East & Africa 7nm Automotive Chip Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East & Africa 7nm Automotive Chip Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa 7nm Automotive Chip Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa 7nm Automotive Chip Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific 7nm Automotive Chip Revenue (undefined), by Application 2025 & 2033

- Figure 52: Asia Pacific 7nm Automotive Chip Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific 7nm Automotive Chip Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific 7nm Automotive Chip Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific 7nm Automotive Chip Revenue (undefined), by Type 2025 & 2033

- Figure 56: Asia Pacific 7nm Automotive Chip Volume (K), by Type 2025 & 2033

- Figure 57: Asia Pacific 7nm Automotive Chip Revenue Share (%), by Type 2025 & 2033

- Figure 58: Asia Pacific 7nm Automotive Chip Volume Share (%), by Type 2025 & 2033

- Figure 59: Asia Pacific 7nm Automotive Chip Revenue (undefined), by Country 2025 & 2033

- Figure 60: Asia Pacific 7nm Automotive Chip Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific 7nm Automotive Chip Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific 7nm Automotive Chip Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global 7nm Automotive Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global 7nm Automotive Chip Volume K Forecast, by Application 2020 & 2033

- Table 3: Global 7nm Automotive Chip Revenue undefined Forecast, by Type 2020 & 2033

- Table 4: Global 7nm Automotive Chip Volume K Forecast, by Type 2020 & 2033

- Table 5: Global 7nm Automotive Chip Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Global 7nm Automotive Chip Volume K Forecast, by Region 2020 & 2033

- Table 7: Global 7nm Automotive Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: Global 7nm Automotive Chip Volume K Forecast, by Application 2020 & 2033

- Table 9: Global 7nm Automotive Chip Revenue undefined Forecast, by Type 2020 & 2033

- Table 10: Global 7nm Automotive Chip Volume K Forecast, by Type 2020 & 2033

- Table 11: Global 7nm Automotive Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Global 7nm Automotive Chip Volume K Forecast, by Country 2020 & 2033

- Table 13: United States 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United States 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Mexico 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global 7nm Automotive Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 20: Global 7nm Automotive Chip Volume K Forecast, by Application 2020 & 2033

- Table 21: Global 7nm Automotive Chip Revenue undefined Forecast, by Type 2020 & 2033

- Table 22: Global 7nm Automotive Chip Volume K Forecast, by Type 2020 & 2033

- Table 23: Global 7nm Automotive Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: Global 7nm Automotive Chip Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Brazil 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Argentina 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global 7nm Automotive Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 32: Global 7nm Automotive Chip Volume K Forecast, by Application 2020 & 2033

- Table 33: Global 7nm Automotive Chip Revenue undefined Forecast, by Type 2020 & 2033

- Table 34: Global 7nm Automotive Chip Volume K Forecast, by Type 2020 & 2033

- Table 35: Global 7nm Automotive Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 36: Global 7nm Automotive Chip Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 40: Germany 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: France 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: Italy 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Spain 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: Russia 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Benelux 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: Nordics 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global 7nm Automotive Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 56: Global 7nm Automotive Chip Volume K Forecast, by Application 2020 & 2033

- Table 57: Global 7nm Automotive Chip Revenue undefined Forecast, by Type 2020 & 2033

- Table 58: Global 7nm Automotive Chip Volume K Forecast, by Type 2020 & 2033

- Table 59: Global 7nm Automotive Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: Global 7nm Automotive Chip Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 62: Turkey 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 64: Israel 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 66: GCC 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 68: North Africa 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 70: South Africa 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global 7nm Automotive Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 74: Global 7nm Automotive Chip Volume K Forecast, by Application 2020 & 2033

- Table 75: Global 7nm Automotive Chip Revenue undefined Forecast, by Type 2020 & 2033

- Table 76: Global 7nm Automotive Chip Volume K Forecast, by Type 2020 & 2033

- Table 77: Global 7nm Automotive Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 78: Global 7nm Automotive Chip Volume K Forecast, by Country 2020 & 2033

- Table 79: China 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 80: China 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 82: India 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 84: Japan 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 86: South Korea 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 88: ASEAN 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 90: Oceania 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific 7nm Automotive Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific 7nm Automotive Chip Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the 7nm Automotive Chip?

The projected CAGR is approximately 10.66%.

2. Which companies are prominent players in the 7nm Automotive Chip?

Key companies in the market include Qualcomm, Tesla, Huawei, Geely Automobile, Arm, ECARX, TSMC, Samsung, Intel.

3. What are the main segments of the 7nm Automotive Chip?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "7nm Automotive Chip," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the 7nm Automotive Chip report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the 7nm Automotive Chip?

To stay informed about further developments, trends, and reports in the 7nm Automotive Chip, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence