Key Insights

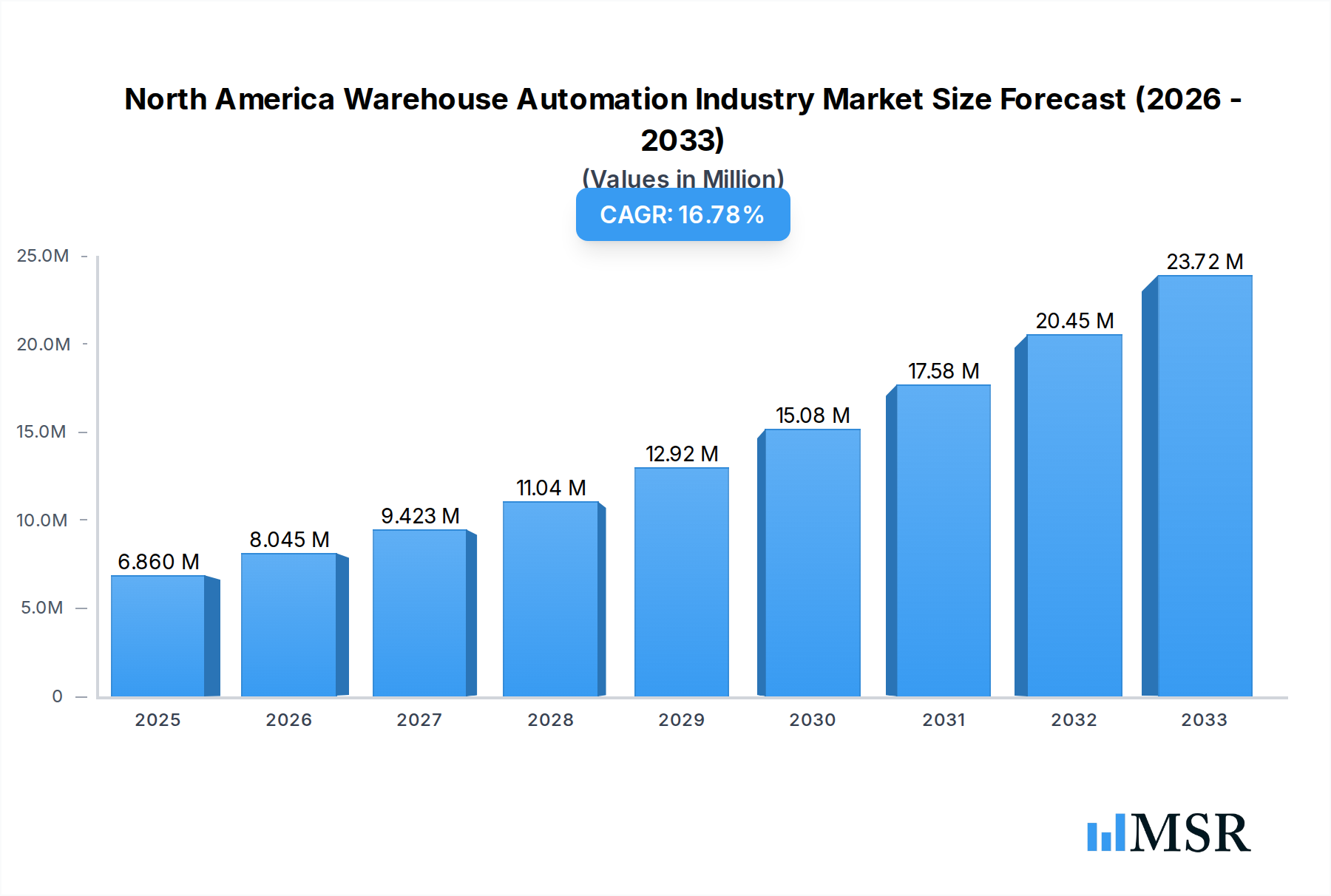

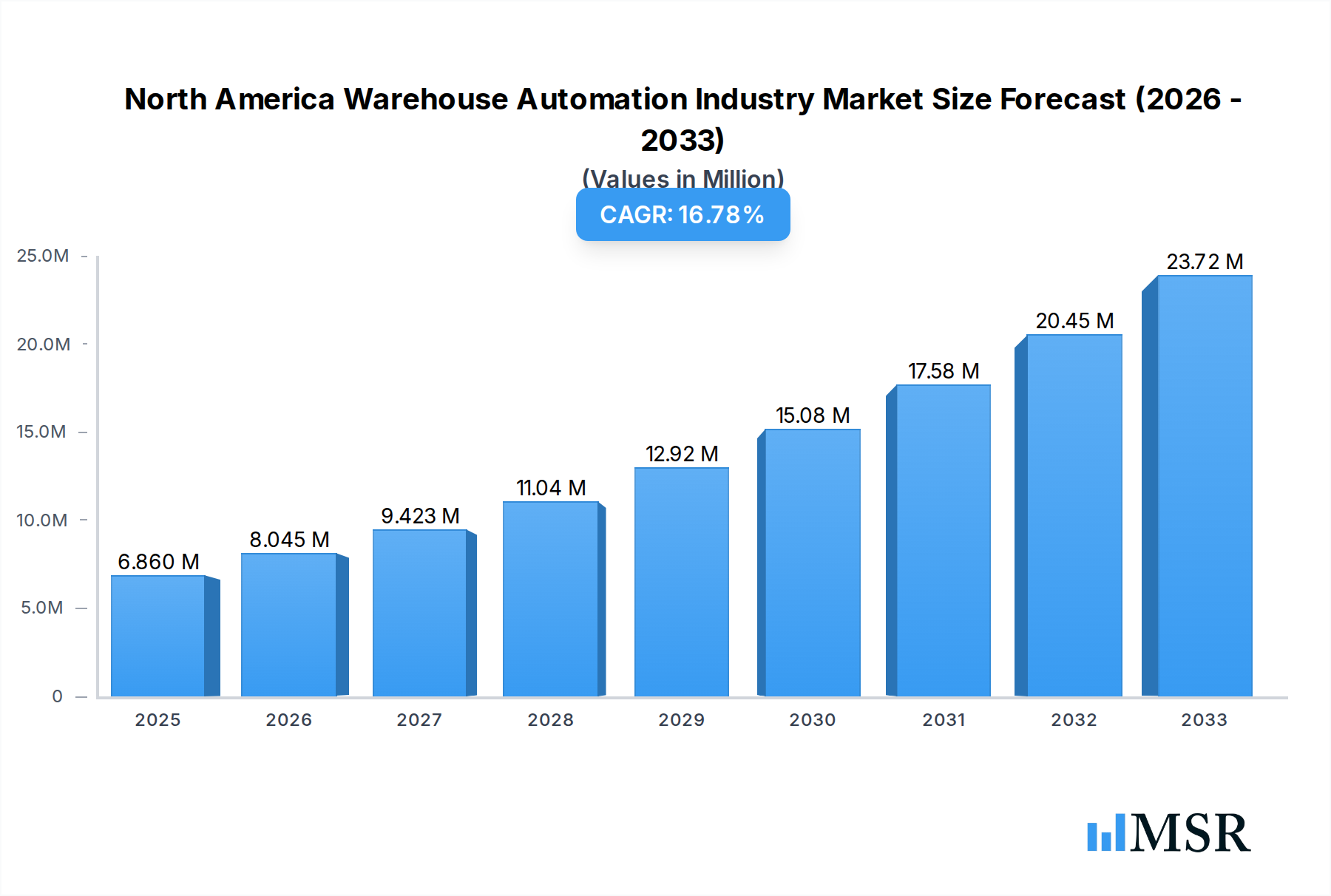

The North American warehouse automation market is poised for exceptional growth, projected to reach a substantial USD 6.86 million by 2025. This significant expansion is fueled by an impressive Compound Annual Growth Rate (CAGR) of 16.70% over the forecast period of 2025-2033. The escalating demand for faster order fulfillment, coupled with the persistent labor shortages across various industries, are the primary drivers propelling this market forward. E-commerce's continued dominance and the resulting surge in online order volumes necessitate advanced automation solutions to manage the complexities of modern warehousing. Furthermore, the drive for operational efficiency, cost reduction, and improved accuracy in inventory management are compelling businesses to invest in sophisticated technologies like mobile robots, automated storage and retrieval systems (AS/RS), and automated conveyor systems. The increasing adoption of these technologies by key end-user industries such as Food and Beverage, Post and Parcel, Groceries, and General Merchandise underscores the transformative impact of automation on supply chain operations.

North America Warehouse Automation Industry Market Size (In Million)

The market is characterized by a dynamic interplay of technological advancements and evolving industry needs. Innovations in Artificial Intelligence (AI) and Machine Learning (ML) are enhancing the capabilities of warehouse automation solutions, enabling more intelligent decision-making and predictive maintenance. The integration of robotics, particularly Autonomous Mobile Robots (AMRs) and Automated Guided Vehicles (AGVs), is revolutionizing material handling within warehouses, offering flexibility and scalability. While the high initial investment cost for some automation solutions and the need for skilled personnel to operate and maintain them present potential restraints, the long-term benefits in terms of productivity, safety, and reduced operational expenses are outweighing these challenges. Geographically, North America, with its robust e-commerce infrastructure and a strong manufacturing base, is a leading region for warehouse automation adoption, driven by significant investments from prominent companies like Locus Robotics, Omron Adept Technologies, and Honeywell Intelligrated.

North America Warehouse Automation Industry Company Market Share

Dive deep into the transformative North America warehouse automation industry with our comprehensive market analysis. This report offers unparalleled insights into the dynamic landscape of automated warehousing, covering key players, emerging technologies, and critical growth drivers. Essential for logistics managers, supply chain executives, technology providers, and investors, this study provides actionable intelligence to navigate the future of automated warehousing solutions in North America. Discover how mobile robots, AGVs, AMRs, AS/RS systems, and advanced warehouse management software are revolutionizing operations across diverse sectors.

North America Warehouse Automation Industry Market Concentration & Dynamics

The North America warehouse automation market is characterized by a moderate to high level of concentration, with a few dominant players and a growing number of innovative warehouse robotics companies and automation solution providers. Innovation ecosystems are flourishing, driven by significant R&D investments and strategic collaborations. Regulatory frameworks, while evolving, are generally supportive of automation adoption to address labor shortages and enhance productivity. Substitute products, such as manual labor and semi-automated systems, are gradually being displaced by more efficient and cost-effective automated solutions. End-user trends strongly favor automation, with an increasing demand for speed, accuracy, and cost reduction in fulfillment operations. Merger and acquisition (M&A) activities are prevalent, indicating consolidation and the strategic acquisition of innovative technologies. Notable M&A deals have been observed, further shaping the competitive landscape. The market share distribution indicates a significant presence of established industrial automation giants alongside agile, specialized robotics for logistics.

North America Warehouse Automation Industry Industry Insights & Trends

The North America warehouse automation industry is poised for substantial growth, driven by escalating e-commerce penetration, a persistent labor deficit, and the imperative for operational efficiency. Our analysis forecasts the market size to reach approximately $XX Billion in 2025, with an impressive Compound Annual Growth Rate (CAGR) of XX% projected through 2033. Technological disruptions, including advancements in AI-powered warehouse robots, sophisticated warehouse management systems (WMS), and the integration of the Internet of Things (IoT) for enhanced connectivity, are reshaping operational paradigms. Evolving consumer behaviors, such as the demand for faster delivery times and personalized services, are compelling businesses to invest heavily in automated fulfillment centers. The adoption of autonomous mobile robots (AMRs) for flexible material handling, alongside the deployment of advanced automated storage and retrieval systems (AS/RS) for optimized space utilization, are key trends. Furthermore, the integration of piece picking robots and de-palletizing/palletizing systems is significantly boosting throughput and reducing operational costs. The continuous innovation in warehouse automation software is enabling seamless integration and real-time data analytics, leading to smarter and more responsive supply chains.

Key Markets & Segments Leading North America Warehouse Automation Industry

The North America warehouse automation industry is currently dominated by the United States, owing to its advanced technological infrastructure, significant e-commerce volume, and proactive adoption of automation. Within the component segment, Hardware commands a substantial market share.

- Hardware Dominance:

- Mobile Robots (AGV, AMR): The rapid adoption of autonomous mobile robots (AMRs) and Automated Guided Vehicles (AGVs) is a primary driver. Their flexibility, scalability, and ability to navigate complex warehouse environments make them indispensable for picking, sorting, and transport tasks.

- Automated Storage and Retrieval Systems (AS/RS): Crucial for maximizing storage density and optimizing inventory management, AS/RS solutions are seeing increased demand, especially in industries requiring high throughput and precise inventory control.

- Automated Conveyor & Sorting Systems: These systems are fundamental for efficient material flow within warehouses, facilitating rapid movement of goods between different zones and processing stations.

- Piece Picking Robots: With the rise of e-commerce and the need for rapid order fulfillment, piece picking robots are gaining traction for their ability to handle individual items with speed and accuracy, reducing reliance on manual labor.

The Software segment is also experiencing robust growth, with advanced WMS and warehouse execution systems (WES) playing a pivotal role in orchestrating complex automation workflows and providing real-time visibility.

In terms of end-user industries, Food and Beverage, Post and Parcel, and General Merchandise are leading the adoption of warehouse automation.

- End-User Industry Leadership:

- Food and Beverage: Driven by stringent inventory management requirements, demand for cold chain logistics, and the need for rapid order fulfillment for perishable goods.

- Post and Parcel: Experiencing unprecedented growth in parcel volumes, necessitating highly efficient and scalable automation for sorting and delivery preparation.

- General Merchandise: Characterized by high SKU variety and fluctuating demand, requiring flexible and robust automation solutions for order picking and processing.

The Groceries sector is also rapidly embracing automation to meet evolving consumer expectations for faster, more convenient delivery options.

North America Warehouse Automation Industry Product Developments

Recent product developments in the North America warehouse automation industry are focused on enhancing robot intelligence, improving system integration, and expanding automation capabilities. Innovations in AI and machine learning are powering more sophisticated mobile robots capable of dynamic pathfinding and object recognition. Advances in piece picking robots are enabling them to handle a wider range of product types and sizes with greater dexterity. The integration of advanced sensors and vision systems is improving the accuracy and efficiency of automated storage and retrieval systems (AS/RS) and conveyor systems. Furthermore, the development of modular and scalable automation solutions allows businesses to adapt their operations more readily to changing demands, providing a significant competitive edge.

Challenges in the North America Warehouse Automation Industry Market

Despite robust growth, the North America warehouse automation industry faces several challenges. High upfront investment costs for implementing advanced automation systems remain a significant barrier for some businesses, particularly small and medium-sized enterprises (SMEs). Supply chain issues impacting the availability of critical automation components and skilled labor for installation and maintenance can lead to project delays. Furthermore, navigating complex regulatory frameworks and ensuring compliance with safety standards requires careful consideration. The integration of new automation technologies with existing legacy systems can also present technical hurdles.

Forces Driving North America Warehouse Automation Industry Growth

Several powerful forces are propelling the North America warehouse automation industry forward. The relentless growth of e-commerce is a primary driver, demanding faster order fulfillment and increased efficiency. The persistent labor shortage across North America is forcing businesses to seek automated solutions to maintain operational capacity. Advancements in robotics technology, including the development of more sophisticated AMRs and AGVs, are making automation more accessible and versatile. Government initiatives and incentives aimed at boosting industrial productivity and competitiveness also contribute to market expansion.

Challenges in the North America Warehouse Automation Industry Market

Long-term growth catalysts for the North America warehouse automation industry are rooted in continuous innovation and strategic market expansion. The ongoing evolution of AI and machine learning is expected to unlock new levels of autonomy and intelligence in warehouse operations, enabling predictive maintenance and optimized decision-making. Strategic partnerships between automation solution providers and end-users are crucial for tailoring solutions to specific industry needs. The expansion of automation into less traditional end-user industries and the development of more cost-effective and user-friendly warehouse automation solutions will further broaden market reach and adoption rates.

Emerging Opportunities in North America Warehouse Automation Industry

Emerging opportunities in the North America warehouse automation industry are abundant. The increasing demand for sustainable logistics is driving the development of energy-efficient automation solutions and robotics. The expansion of micro-fulfillment centers in urban areas presents a significant opportunity for compact and highly automated systems. Furthermore, the integration of automation with data analytics and artificial intelligence offers immense potential for predictive logistics, dynamic inventory management, and personalized customer experiences. The growing adoption of robotics-as-a-service (RaaS) models is also making advanced automation more accessible to a wider range of businesses.

Leading Players in the North America Warehouse Automation Industry Sector

- Locus Robotics

- Omron Adept Technologies

- Honeywell Intelligrated (Honeywell International Inc)

- Fetch Robotics Inc

- Invia Robotics Inc

- Dematic Group

- KUKA AG

- Daifuku Co Ltd

- Oracle Corporation

- One Network Enterprises Inc

Key Milestones in North America Warehouse Automation Industry Industry

- March 2022: Honeywell announced a strategic partnership with OTTO Motors, a division of Clearpath Robotics, giving warehouses and distribution centers throughout North America an automated option to handle some of the most labor-intensive roles in an increasingly scarce job market. The collaboration enables the company's customers to increase efficiency, reduce errors and improve safety by deploying OTTO's autonomous mobile robots (AMRs) in their facilities.

- March 2022: Addverb Technologies announced a North American partnership with Numina Group. The agreement expands the deployment of Addverb's innovative mobile robots for automation solutions to North American warehouses. It gives Numina Group customers access to innovative technology applications for faster and smarter warehouse order fulfillment automation.

Strategic Outlook for North America Warehouse Automation Industry Market

The strategic outlook for the North America warehouse automation industry remains exceptionally strong. Future market potential will be driven by the continued integration of cutting-edge technologies such as AI, IoT, and advanced robotics. Strategic opportunities lie in developing bespoke automation solutions for specialized industries and catering to the growing demand for flexible, scalable, and cost-effective automation. The focus will increasingly shift towards creating interconnected, intelligent, and highly efficient warehouse ecosystems that can adapt to dynamic market conditions and evolving consumer expectations. Collaboration and strategic alliances will be key to unlocking new markets and delivering comprehensive automation strategies.

North America Warehouse Automation Industry Segmentation

-

1. Component

-

1.1. Hardware

- 1.1.1. Mobile Robots (AGV, AMR)

- 1.1.2. Automated Storage and Retrieval Systems (AS/RS)

- 1.1.3. Automated Conveyor & Sorting Systems

- 1.1.4. De-palletizing/Palletizing Systems

- 1.1.5. Automatic Identification and Data Collection

- 1.1.6. Piece Picking Robots

- 1.2. Software

- 1.3. Services (Value Added Services, Maintenance, etc.)

-

1.1. Hardware

-

2. End-user Industry

- 2.1. Food and Beverage

- 2.2. Post and Parcel

- 2.3. Groceries

- 2.4. General Merchandise

- 2.5. Apparel

- 2.6. Manufacturing

- 2.7. Other End-User Industries

North America Warehouse Automation Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

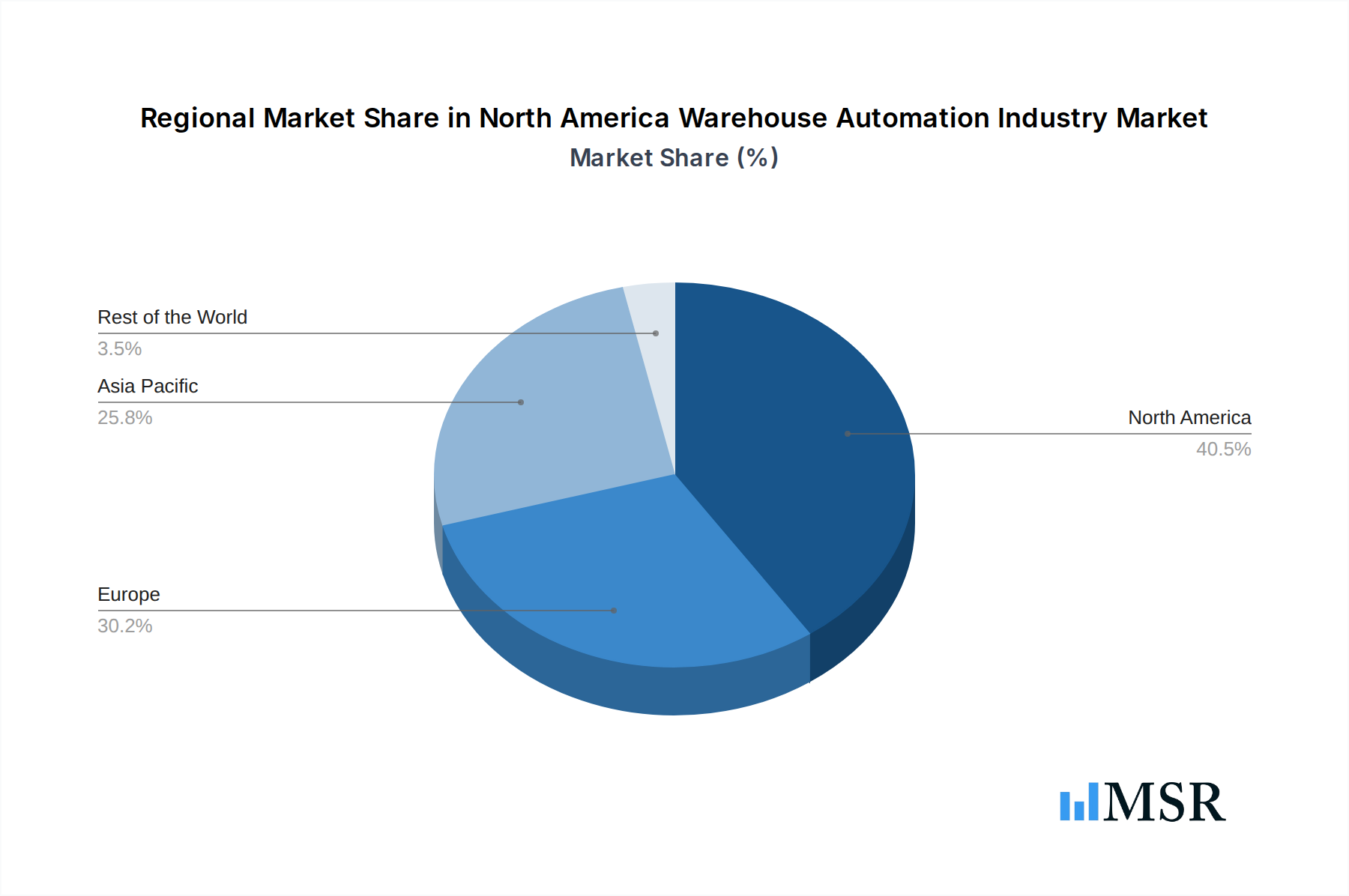

North America Warehouse Automation Industry Regional Market Share

Geographic Coverage of North America Warehouse Automation Industry

North America Warehouse Automation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16.70% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Hardware

- 5.1.1.1. Mobile Robots (AGV, AMR)

- 5.1.1.2. Automated Storage and Retrieval Systems (AS/RS)

- 5.1.1.3. Automated Conveyor & Sorting Systems

- 5.1.1.4. De-palletizing/Palletizing Systems

- 5.1.1.5. Automatic Identification and Data Collection

- 5.1.1.6. Piece Picking Robots

- 5.1.2. Software

- 5.1.3. Services (Value Added Services, Maintenance, etc.)

- 5.1.1. Hardware

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Food and Beverage

- 5.2.2. Post and Parcel

- 5.2.3. Groceries

- 5.2.4. General Merchandise

- 5.2.5. Apparel

- 5.2.6. Manufacturing

- 5.2.7. Other End-User Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. North America Warehouse Automation Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Hardware

- 6.1.1.1. Mobile Robots (AGV, AMR)

- 6.1.1.2. Automated Storage and Retrieval Systems (AS/RS)

- 6.1.1.3. Automated Conveyor & Sorting Systems

- 6.1.1.4. De-palletizing/Palletizing Systems

- 6.1.1.5. Automatic Identification and Data Collection

- 6.1.1.6. Piece Picking Robots

- 6.1.2. Software

- 6.1.3. Services (Value Added Services, Maintenance, etc.)

- 6.1.1. Hardware

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Food and Beverage

- 6.2.2. Post and Parcel

- 6.2.3. Groceries

- 6.2.4. General Merchandise

- 6.2.5. Apparel

- 6.2.6. Manufacturing

- 6.2.7. Other End-User Industries

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Locus Robotics

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Omron Adept Technologies

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Honeywell Intelligrated (Honeywell International Inc )

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Fetch Robotics Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Invia Robotics Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Dematic Group

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 KUKA AG

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Daifuku Co Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Oracle Corporation

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 One Network Enterprises Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Locus Robotics

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Warehouse Automation Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: North America Warehouse Automation Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Warehouse Automation Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 2: North America Warehouse Automation Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 3: North America Warehouse Automation Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: North America Warehouse Automation Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 5: North America Warehouse Automation Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 6: North America Warehouse Automation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States North America Warehouse Automation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada North America Warehouse Automation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Mexico North America Warehouse Automation Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Warehouse Automation Industry?

The projected CAGR is approximately 16.70%.

2. Which companies are prominent players in the North America Warehouse Automation Industry?

Key companies in the market include Locus Robotics, Omron Adept Technologies, Honeywell Intelligrated (Honeywell International Inc ), Fetch Robotics Inc , Invia Robotics Inc, Dematic Group, KUKA AG, Daifuku Co Ltd, Oracle Corporation, One Network Enterprises Inc.

3. What are the main segments of the North America Warehouse Automation Industry?

The market segments include Component, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.86 Million as of 2022.

5. What are some drivers contributing to market growth?

Growth in the e-commerce industry and SKUs proliferation.; Increase in technology innovations and availbility.

6. What are the notable trends driving market growth?

Increased Adoption of Robotics In The Warehouses Is Driving The Market.

7. Are there any restraints impacting market growth?

Optimizing Battery Life of Hearable Device.

8. Can you provide examples of recent developments in the market?

March 2022 - Honeywell announced a strategic partnership with OTTO Motors, a division of Clearpath Robotics, giving warehouses and distribution centers throughout North America an automated option to handle some of the most labor-intensive roles in an increasingly scarce job market. The collaboration enables the company's customers to increase efficiency, reduce errors and improve safety by deploying OTTO's autonomous mobile robots (AMRs) in their facilities.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Warehouse Automation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Warehouse Automation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Warehouse Automation Industry?

To stay informed about further developments, trends, and reports in the North America Warehouse Automation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence