Key Insights

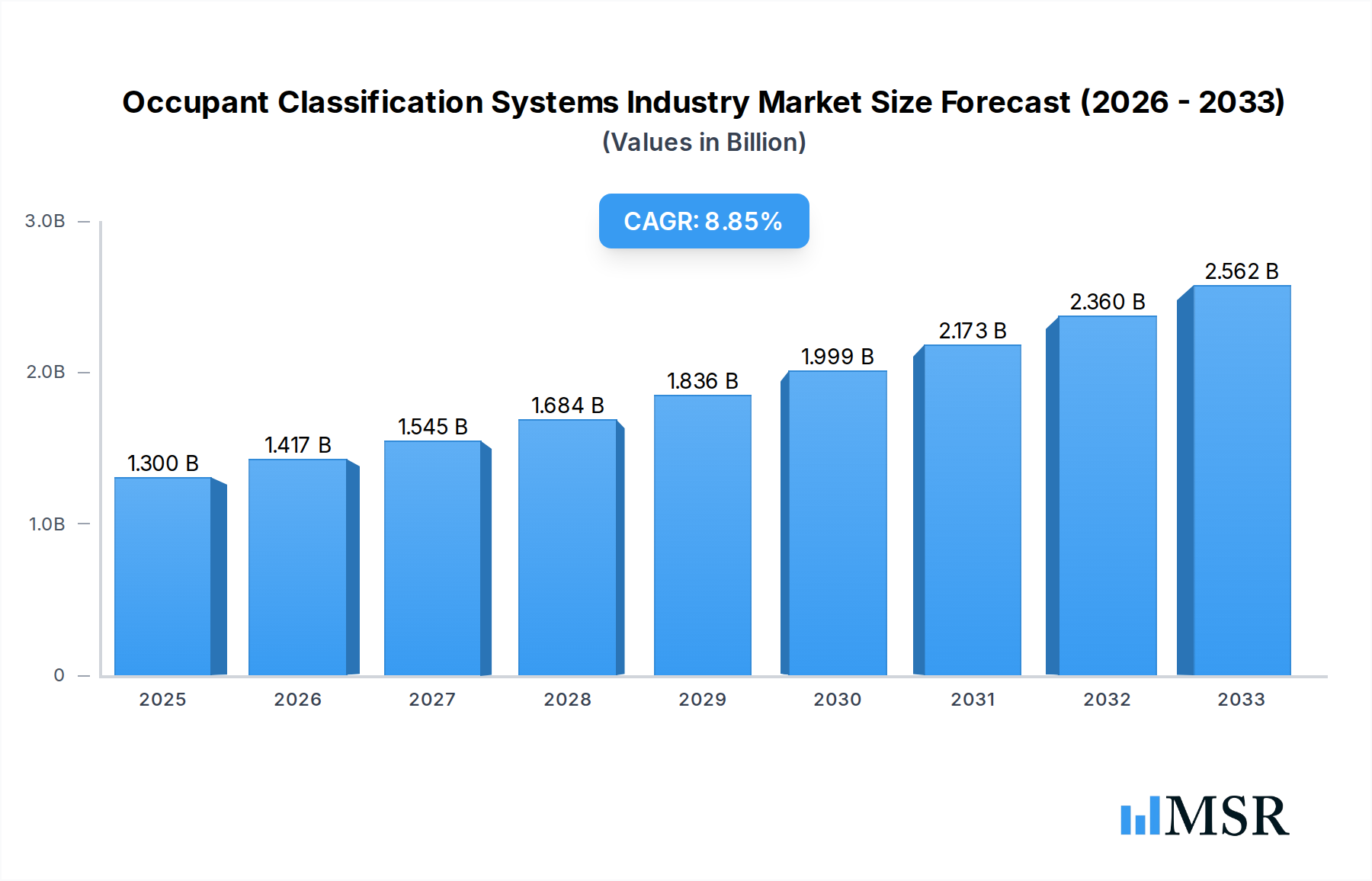

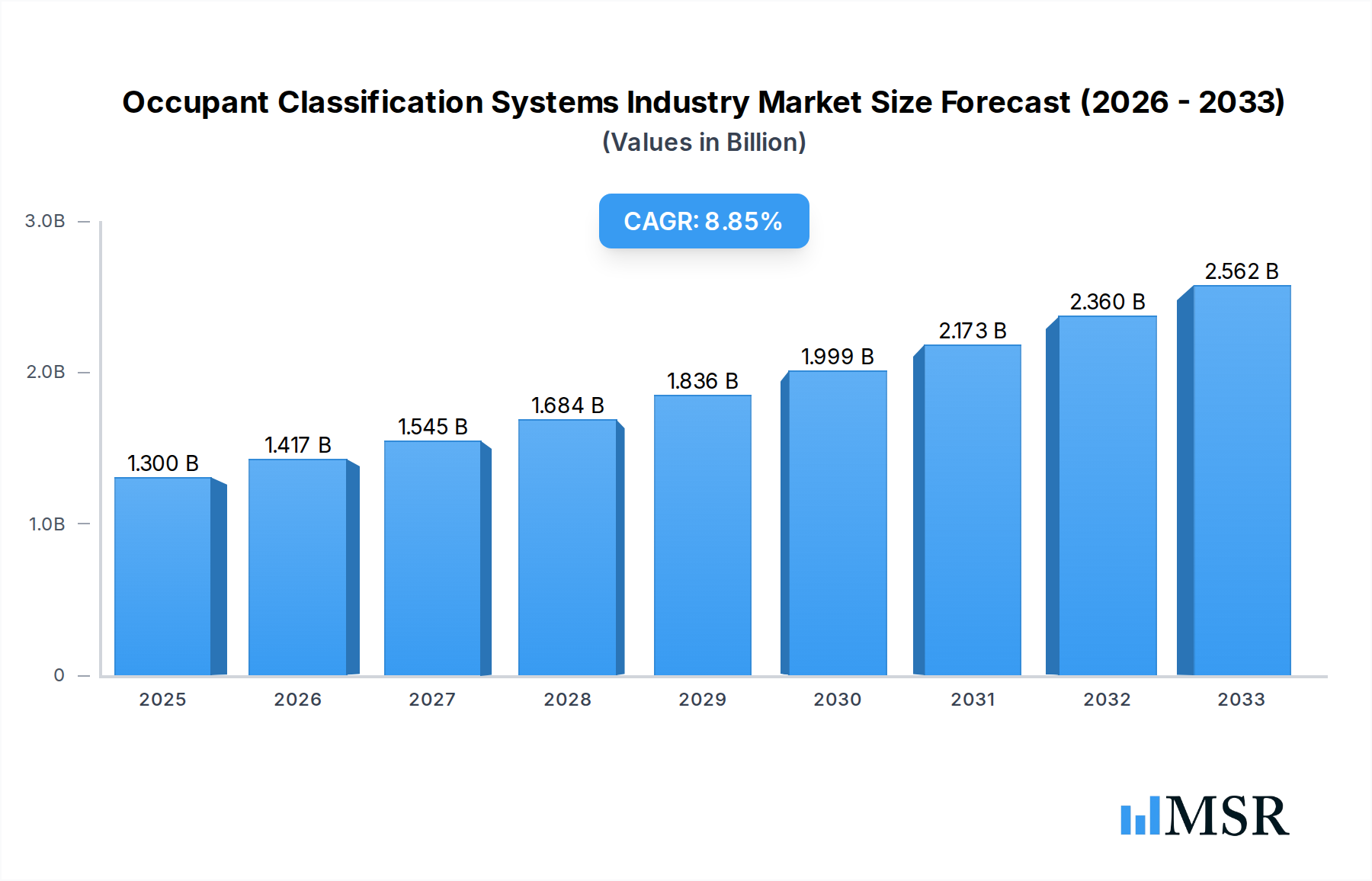

The Occupant Classification Systems (OCS) market is poised for robust expansion, driven by escalating safety regulations and the increasing adoption of advanced driver-assistance systems (ADAS) in vehicles worldwide. The market is projected to reach a substantial $1.3 billion in 2025, with a compelling Compound Annual Growth Rate (CAGR) of 9% through the forecast period of 2025-2033. This growth is fundamentally underpinned by the critical role OCS plays in enabling sophisticated airbag deployment strategies, which are becoming mandatory across various vehicle segments. The increasing sophistication of vehicle interiors, including the integration of diverse seating materials and advanced sensor technologies, further fuels the demand for highly accurate and adaptable OCS. Furthermore, the burgeoning automotive industry in emerging economies and the growing consumer awareness regarding vehicle safety are significant catalysts for market expansion.

Occupant Classification Systems Industry Market Size (In Billion)

Key trends shaping the OCS market include the miniaturization and enhanced sensitivity of pressure sensors and seat belt tension sensors, leading to more precise occupant detection and weight classification. The integration of OCS with other ADAS features, such as adaptive cruise control and automatic emergency braking, is another significant development, creating a more holistic and intelligent safety ecosystem within vehicles. The rising popularity of electric vehicles (EVs), which often feature novel interior designs and materials, presents unique opportunities and challenges for OCS development, driving innovation in sensor placement and algorithm development. While the market is experiencing strong growth, potential restraints could emerge from the high initial cost of advanced OCS integration and the ongoing need for continuous software updates to maintain optimal performance against evolving safety standards and vehicle architectures. Nonetheless, the overarching commitment to enhancing automotive safety ensures a dynamic and promising future for the Occupant Classification Systems industry.

Occupant Classification Systems Industry Company Market Share

Here's an SEO-optimized, engaging report description for the Occupant Classification Systems Industry, designed for high search visibility and to attract industry stakeholders, without requiring further modification:

This comprehensive market research report offers an in-depth analysis of the global Occupant Classification Systems (OCS) industry. Covering a detailed study period from 2019 to 2033, with a base and estimated year of 2025 and a forecast period from 2025 to 2033, this report provides critical insights into market dynamics, key trends, and future growth trajectories. The report delves into the intricate workings of OCS, crucial for enhancing vehicle safety by accurately classifying occupants for optimal airbag deployment and restraint system activation. With the automotive industry experiencing rapid evolution driven by advancements in autonomous driving and electrification, the demand for sophisticated OCS is set to surge. This report is an indispensable resource for automotive manufacturers, Tier-1 suppliers, technology providers, investors, and regulatory bodies seeking to navigate and capitalize on the burgeoning OCS market.

Occupant Classification Systems Industry Market Concentration & Dynamics

The Occupant Classification Systems (OCS) industry exhibits a moderate to high level of market concentration, with a handful of major global automotive suppliers dominating the landscape. Key players like Robert Bosch GmbH, Continental AG, Denso Corporation, ZF Group, and Aptiv Corporation command significant market share, driven by their extensive R&D capabilities, established supply chains, and long-standing relationships with automotive OEMs. Innovation ecosystems are vibrant, characterized by continuous advancements in sensor technology, AI-powered algorithms for occupant detection and classification, and integration with advanced driver-assistance systems (ADAS). Regulatory frameworks, particularly stringent safety standards mandated by bodies such as NHTSA in the US and Euro NCAP in Europe, are a primary driver of innovation and adoption. The threat of substitute products is minimal for core OCS functions, as their role in passive safety is irreplaceable. End-user trends are heavily influenced by the increasing demand for advanced safety features, the growing adoption of electric vehicles (EVs), and the push towards autonomous driving. Merger and acquisition (M&A) activities, while not at an extremely high volume, are strategic, focusing on acquiring niche technologies or consolidating market presence. For instance, recent M&A activities have seen consolidation in the sensor manufacturing segment, with an estimated 5-10 significant deals in the past five years, impacting market shares by up to 5-10% for acquiring entities.

Occupant Classification Systems Industry Industry Insights & Trends

The Occupant Classification Systems (OCS) industry is poised for substantial growth, driven by a confluence of technological advancements, evolving consumer preferences, and increasingly stringent global safety regulations. The global OCS market size is estimated to be valued at approximately $5.0 billion in the base year of 2025, projected to grow at a robust Compound Annual Growth Rate (CAGR) of around 7.5% during the forecast period of 2025–2033. A primary growth driver is the escalating demand for enhanced vehicle safety, with consumers actively seeking vehicles equipped with the latest occupant protection technologies. This trend is further amplified by government mandates and safety rating programs that incentivize or require the implementation of advanced passive safety systems, including sophisticated OCS. The proliferation of electric vehicles (EVs) also presents a significant opportunity. EVs, often designed with novel interior architectures and incorporating advanced battery management systems, require OCS solutions that can adapt to these unique configurations, ensuring optimal safety for all occupants. Furthermore, the development and gradual introduction of higher levels of autonomous driving are expected to reshape interior cabin designs, necessitating OCS that can accurately classify occupants in diverse seating arrangements and potentially in different states of engagement with the driving task. Technological disruptions are primarily centered around advancements in sensor fusion, the integration of multiple sensor types (e.g., pressure sensors, seat belt tension sensors, cameras, radar) to achieve higher accuracy and reliability in occupant detection and classification. Artificial intelligence (AI) and machine learning (ML) algorithms are increasingly being employed to analyze complex occupant data, enabling personalized and adaptive safety responses. The evolution of consumer behavior towards prioritizing safety as a key purchasing criterion, coupled with increased awareness of the benefits of advanced occupant protection systems, is a significant market influencer. The historical period from 2019–2024 witnessed steady growth, with the market size growing from an estimated $3.5 billion in 2019 to approximately $4.8 billion by 2024, demonstrating a sustained upward trajectory that sets the stage for accelerated expansion in the coming years. This growth is underpinned by the continuous investment in R&D by leading automotive suppliers and OEMs to meet and exceed evolving safety standards and consumer expectations.

Key Markets & Segments Leading Occupant Classification Systems Industry

The Occupant Classification Systems (OCS) industry is witnessing dominant growth and adoption across several key markets and segments, driven by a combination of economic factors, technological readiness, and regulatory impetus.

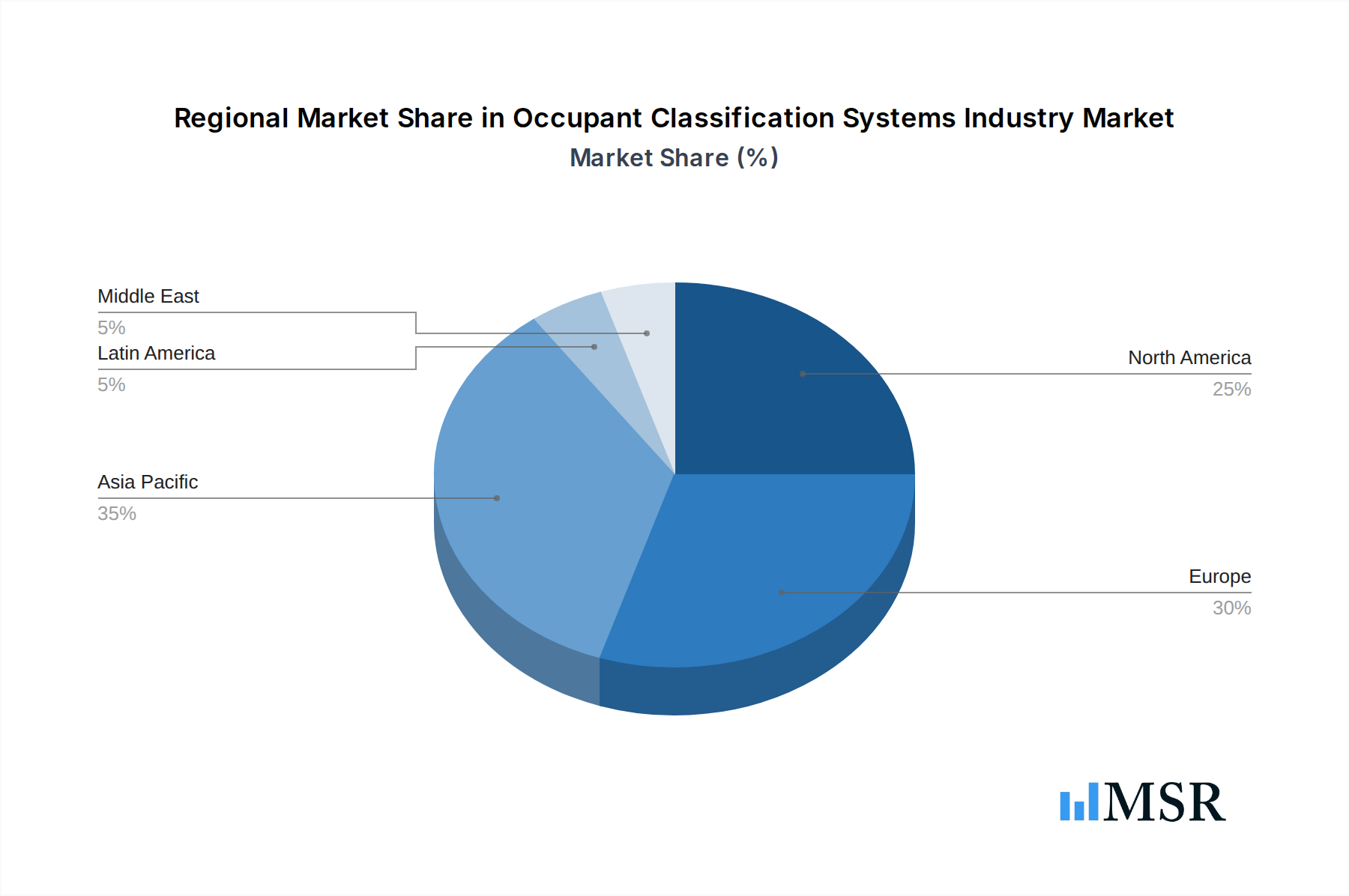

Dominant Regions and Countries

- North America (USA, Canada): This region is a significant market due to stringent safety regulations enforced by the National Highway Traffic Safety Administration (NHTSA) and a high consumer preference for advanced safety features. The substantial presence of major automotive manufacturers and a strong aftermarket for safety upgrades further bolster its leadership. Economic growth in this region consistently supports the adoption of new automotive technologies.

- Europe (Germany, France, UK): European countries, particularly Germany, are at the forefront of automotive innovation and safety standards. The European New Car Assessment Programme (Euro NCAP) plays a crucial role in driving the demand for advanced OCS. High vehicle penetration rates and a strong emphasis on passenger safety contribute to Europe's leading position.

- Asia-Pacific (China, Japan, South Korea): China's massive automotive market, coupled with rapidly evolving safety standards and increasing consumer disposable income, makes it a rapidly growing powerhouse. Japan and South Korea, with their highly advanced automotive industries and strong focus on technological integration, are also key contributors to this segment.

Dominant Component Segments

- Sensors (Pressure Sensor, Seat Belt Tension Sensor): The sensor segment, encompassing pressure sensors for seat occupancy detection and seat belt tension sensors for monitoring occupant restraint, forms the bedrock of OCS. The demand for these components is directly proportional to vehicle production volumes and the increasing sophistication of OCS. Advances in MEMS (Micro-Electro-Mechanical Systems) technology are leading to smaller, more accurate, and cost-effective sensors. The market for advanced pressure sensors alone is projected to exceed $1.5 billion by 2025.

- Airbag Control Unit (ACU): The ACU is the central processing unit for airbag systems, and its functionality is intrinsically linked to the OCS data. As OCS become more complex, the ACU must be capable of processing more information to make precise deployment decisions. The integration of OCS data with ACUs is a continuous area of development, driving demand for advanced ACUs.

Dominant Vehicle Types

- Light Vehicles (Passenger Cars, SUVs, Pickup Trucks): This segment constitutes the largest share of the OCS market due to its sheer volume. The continuous demand for enhanced safety features in everyday vehicles, coupled with regulatory mandates, ensures sustained growth for OCS in light vehicles. The market size for OCS in light vehicles is estimated to be around $4.0 billion in 2025.

- Electric Vehicles (EVs): The rapid growth of the EV market presents a substantial and expanding opportunity for OCS. EVs often feature unique interior designs and space utilization, requiring specialized OCS solutions. The integration of OCS with advanced battery management systems and overall vehicle safety architectures in EVs is a key trend. The EV segment's share of the OCS market is projected to grow from approximately 15% in 2025 to over 30% by 2033.

Occupant Classification Systems Industry Product Developments

Product innovations in the Occupant Classification Systems (OCS) industry are primarily focused on enhancing accuracy, reducing cost, and improving integration capabilities. Advancements include the development of highly sensitive multi-zone pressure sensors that can accurately detect the presence, weight, and even posture of occupants, including children and adults. Furthermore, the integration of AI-powered vision-based systems and radar-based sensors with traditional pressure and seat belt sensors is creating a more robust and comprehensive OCS. These integrated systems can differentiate between children and adults, detect rear-seat occupants, and even identify unbuckled passengers, leading to more intelligent airbag deployment and restraint system adjustments. The market relevance is amplified as OEMs strive to meet evolving safety regulations and consumer expectations for unparalleled passenger protection, especially in the rapidly growing electric vehicle segment.

Challenges in the Occupant Classification Systems Industry Market

The Occupant Classification Systems (OCS) industry faces several challenges that can impact its growth trajectory. Regulatory hurdles, while driving adoption, can also be complex to navigate, requiring significant investment in compliance testing and validation. Supply chain issues, particularly concerning the availability of specialized electronic components and raw materials, can lead to production delays and increased costs, with potential impacts of 5-10% on manufacturing timelines. Competitive pressures from established players and emerging technology providers necessitate continuous innovation and cost optimization. The high cost of advanced OCS, especially those incorporating multiple sensor technologies and AI, can also be a barrier to adoption in lower-segment vehicles, potentially limiting market penetration by 10-15% in certain price-sensitive segments. Furthermore, the integration of OCS with complex vehicle architectures and the need for robust cybersecurity measures to protect sensitive occupant data present ongoing technical challenges.

Forces Driving Occupant Classification Systems Industry Growth

Several key forces are driving the growth of the Occupant Classification Systems (OCS) industry. The paramount driver is the unwavering global focus on vehicle safety, with increasingly stringent regulations from bodies like NHTSA and Euro NCAP mandating advanced occupant protection systems. Consumer demand for enhanced safety features as a differentiator in vehicle purchasing decisions is also a significant catalyst. The rapid proliferation of electric vehicles (EVs), which often require tailored safety solutions due to their unique designs, creates new avenues for OCS adoption. Technological advancements, such as the miniaturization of sensors, improvements in AI and machine learning for occupant recognition, and the development of sensor fusion techniques, are making OCS more accurate, reliable, and cost-effective. Economic factors, including rising disposable incomes in developing markets and sustained automotive sales growth, further support market expansion.

Challenges in the Occupant Classification Systems Industry Market

Long-term growth catalysts for the Occupant Classification Systems (OCS) industry are deeply rooted in continued technological innovation and strategic market expansion. The relentless pursuit of higher safety standards will necessitate the evolution of OCS to handle increasingly complex scenarios, such as the detection of occupants in various postures, the identification of children and infants, and adaptation to multi-seat configurations in autonomous vehicles. Partnerships between OCS suppliers and automotive OEMs are crucial for co-development and seamless integration of these advanced systems. Furthermore, market expansion into emerging economies, where safety regulations are progressively tightening and consumer awareness is growing, presents a substantial long-term opportunity. The development of more cost-effective and scalable OCS solutions will also be key to unlocking wider market penetration across all vehicle segments, thereby ensuring sustained growth.

Emerging Opportunities in Occupant Classification Systems Industry

Emerging opportunities in the Occupant Classification Systems (OCS) industry are being shaped by advancements in vehicle technology and evolving consumer expectations. The rise of highly automated and autonomous driving is creating a demand for OCS that can monitor occupant status and engagement, providing critical safety data for transition between different driving modes. The integration of OCS with in-cabin sensing technologies for driver monitoring systems (DMS) and passenger well-being applications presents a significant growth area. The development of "smart cabin" concepts, where OCS plays a role in personalized climate control, seat adjustments, and even in-car entertainment based on occupant recognition, is another burgeoning trend. Furthermore, the increasing focus on sustainability in the automotive sector is driving the development of lighter and more energy-efficient OCS components.

Leading Players in the Occupant Classification Systems Industry Sector

- Denso Corporation

- ON Semiconductor Corporation

- ZF Group

- Aisin Seiki Co Ltd

- Continental AG

- Autoliv Inc

- Aptiv Corporation

- Robert Bosch GmbH

- TE Connectivity Limited

- IEE SENSING

Key Milestones in Occupant Classification Systems Industry Industry

- 2019: Introduction of advanced multi-zone pressure sensing technology for enhanced occupant weight and presence detection.

- 2020: Increased integration of OCS data with advanced driver-assistance systems (ADAS) for more intelligent safety interventions.

- 2021: Significant advancements in AI algorithms for improved accuracy in occupant classification, including differentiating between adult and child occupants.

- 2022: Emergence of vision-based and radar-based OCS solutions, offering complementary data to traditional sensors.

- 2023: Growing adoption of OCS in electric vehicles (EVs) to accommodate unique interior designs and safety architectures.

- 2024: Developments in sensor fusion techniques to create more robust and reliable OCS across diverse environmental conditions.

Strategic Outlook for Occupant Classification Systems Industry Market

The strategic outlook for the Occupant Classification Systems (OCS) industry is overwhelmingly positive, driven by a sustained demand for enhanced vehicle safety and the relentless pace of automotive innovation. Growth accelerators include the increasing stringency of global safety regulations, which will continue to mandate advanced OCS features. The rapid electrification of the automotive fleet will necessitate tailored OCS solutions, presenting substantial market potential. Furthermore, the ongoing development of autonomous driving technologies will require sophisticated OCS for monitoring occupant status and ensuring safe transitions. Strategic opportunities lie in fostering deeper collaborations between OCS suppliers and automotive OEMs for integrated system development, as well as expanding into rapidly growing emerging markets. The continuous evolution of sensor technology, coupled with advancements in AI and machine learning, will further drive product innovation and market penetration.

Occupant Classification Systems Industry Segmentation

-

1. Component

- 1.1. Airbag Control Unit (ACU)

-

1.2. Sensors

- 1.2.1. Pressure Sensor

- 1.2.2. Seat Belt Tension Sensor

-

2. Vehicle Type

- 2.1. Light Vehicles

- 2.2. Electric Vehicles

Occupant Classification Systems Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East

Occupant Classification Systems Industry Regional Market Share

Geographic Coverage of Occupant Classification Systems Industry

Occupant Classification Systems Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Airbag Control Unit (ACU)

- 5.1.2. Sensors

- 5.1.2.1. Pressure Sensor

- 5.1.2.2. Seat Belt Tension Sensor

- 5.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.2.1. Light Vehicles

- 5.2.2. Electric Vehicles

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. Global Occupant Classification Systems Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Airbag Control Unit (ACU)

- 6.1.2. Sensors

- 6.1.2.1. Pressure Sensor

- 6.1.2.2. Seat Belt Tension Sensor

- 6.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.2.1. Light Vehicles

- 6.2.2. Electric Vehicles

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. North America Occupant Classification Systems Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Component

- 7.1.1. Airbag Control Unit (ACU)

- 7.1.2. Sensors

- 7.1.2.1. Pressure Sensor

- 7.1.2.2. Seat Belt Tension Sensor

- 7.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.2.1. Light Vehicles

- 7.2.2. Electric Vehicles

- 7.1. Market Analysis, Insights and Forecast - by Component

- 8. Europe Occupant Classification Systems Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Component

- 8.1.1. Airbag Control Unit (ACU)

- 8.1.2. Sensors

- 8.1.2.1. Pressure Sensor

- 8.1.2.2. Seat Belt Tension Sensor

- 8.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.2.1. Light Vehicles

- 8.2.2. Electric Vehicles

- 8.1. Market Analysis, Insights and Forecast - by Component

- 9. Asia Pacific Occupant Classification Systems Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Component

- 9.1.1. Airbag Control Unit (ACU)

- 9.1.2. Sensors

- 9.1.2.1. Pressure Sensor

- 9.1.2.2. Seat Belt Tension Sensor

- 9.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 9.2.1. Light Vehicles

- 9.2.2. Electric Vehicles

- 9.1. Market Analysis, Insights and Forecast - by Component

- 10. Latin America Occupant Classification Systems Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Component

- 10.1.1. Airbag Control Unit (ACU)

- 10.1.2. Sensors

- 10.1.2.1. Pressure Sensor

- 10.1.2.2. Seat Belt Tension Sensor

- 10.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 10.2.1. Light Vehicles

- 10.2.2. Electric Vehicles

- 10.1. Market Analysis, Insights and Forecast - by Component

- 11. Middle East Occupant Classification Systems Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Component

- 11.1.1. Airbag Control Unit (ACU)

- 11.1.2. Sensors

- 11.1.2.1. Pressure Sensor

- 11.1.2.2. Seat Belt Tension Sensor

- 11.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 11.2.1. Light Vehicles

- 11.2.2. Electric Vehicles

- 11.1. Market Analysis, Insights and Forecast - by Component

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Denso Corporation

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 ON Semiconductor Corporation*List Not Exhaustive

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 ZF Group

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Aisin Seiki Co Ltd

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Continental AG

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Autoliv Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Aptiv Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Robert Bosch GmbH

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 TE Connectivity Limited

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 IEE SENSING

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Denso Corporation

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Occupant Classification Systems Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Occupant Classification Systems Industry Revenue (billion), by Component 2025 & 2033

- Figure 3: North America Occupant Classification Systems Industry Revenue Share (%), by Component 2025 & 2033

- Figure 4: North America Occupant Classification Systems Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 5: North America Occupant Classification Systems Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 6: North America Occupant Classification Systems Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Occupant Classification Systems Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Occupant Classification Systems Industry Revenue (billion), by Component 2025 & 2033

- Figure 9: Europe Occupant Classification Systems Industry Revenue Share (%), by Component 2025 & 2033

- Figure 10: Europe Occupant Classification Systems Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 11: Europe Occupant Classification Systems Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 12: Europe Occupant Classification Systems Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Occupant Classification Systems Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Occupant Classification Systems Industry Revenue (billion), by Component 2025 & 2033

- Figure 15: Asia Pacific Occupant Classification Systems Industry Revenue Share (%), by Component 2025 & 2033

- Figure 16: Asia Pacific Occupant Classification Systems Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 17: Asia Pacific Occupant Classification Systems Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 18: Asia Pacific Occupant Classification Systems Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Occupant Classification Systems Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Occupant Classification Systems Industry Revenue (billion), by Component 2025 & 2033

- Figure 21: Latin America Occupant Classification Systems Industry Revenue Share (%), by Component 2025 & 2033

- Figure 22: Latin America Occupant Classification Systems Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 23: Latin America Occupant Classification Systems Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 24: Latin America Occupant Classification Systems Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Latin America Occupant Classification Systems Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East Occupant Classification Systems Industry Revenue (billion), by Component 2025 & 2033

- Figure 27: Middle East Occupant Classification Systems Industry Revenue Share (%), by Component 2025 & 2033

- Figure 28: Middle East Occupant Classification Systems Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 29: Middle East Occupant Classification Systems Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 30: Middle East Occupant Classification Systems Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East Occupant Classification Systems Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Occupant Classification Systems Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 2: Global Occupant Classification Systems Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 3: Global Occupant Classification Systems Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Occupant Classification Systems Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 5: Global Occupant Classification Systems Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 6: Global Occupant Classification Systems Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Occupant Classification Systems Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 8: Global Occupant Classification Systems Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 9: Global Occupant Classification Systems Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Global Occupant Classification Systems Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 11: Global Occupant Classification Systems Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 12: Global Occupant Classification Systems Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Occupant Classification Systems Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 14: Global Occupant Classification Systems Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 15: Global Occupant Classification Systems Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global Occupant Classification Systems Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 17: Global Occupant Classification Systems Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 18: Global Occupant Classification Systems Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Occupant Classification Systems Industry?

The projected CAGR is approximately 9%.

2. Which companies are prominent players in the Occupant Classification Systems Industry?

Key companies in the market include Denso Corporation, ON Semiconductor Corporation*List Not Exhaustive, ZF Group, Aisin Seiki Co Ltd, Continental AG, Autoliv Inc, Aptiv Corporation, Robert Bosch GmbH, TE Connectivity Limited, IEE SENSING.

3. What are the main segments of the Occupant Classification Systems Industry?

The market segments include Component, Vehicle Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.3 billion as of 2022.

5. What are some drivers contributing to market growth?

; Emergence of MEMS Technology; Passenger Safety and Security Regulations and Increased Focus on compliance.

6. What are the notable trends driving market growth?

Passenger Safety and security Regulations and Increased Focus on Compliances to Drive the Market.

7. Are there any restraints impacting market growth?

; Integration Drift Error.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Occupant Classification Systems Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Occupant Classification Systems Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Occupant Classification Systems Industry?

To stay informed about further developments, trends, and reports in the Occupant Classification Systems Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence