Key Insights

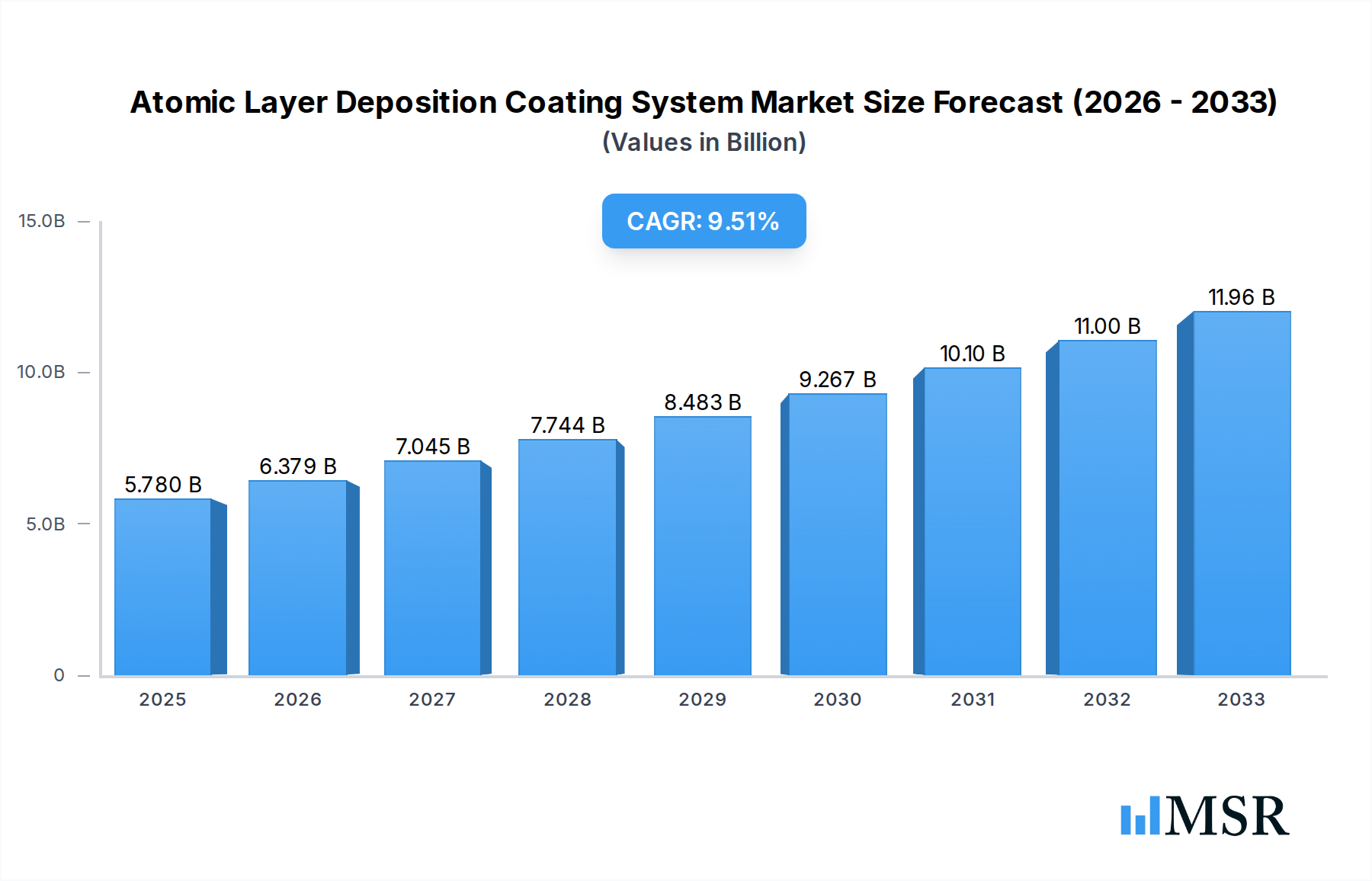

The global Atomic Layer Deposition (ALD) Coating System market is poised for significant expansion, projected to reach an estimated USD 5.78 billion by 2025, driven by a robust Compound Annual Growth Rate (CAGR) of 10.41%. This growth trajectory underscores the increasing demand for ALD technology across a multitude of high-tech industries. The inherent precision and conformality of ALD coatings are crucial for advancements in optical instruments, where they enhance anti-reflective properties and durability. In the medical sector, ALD is indispensable for creating biocompatible and functionalized surfaces on implants and diagnostic devices. The semiconductor wafer industry, a cornerstone of modern electronics, relies heavily on ALD for depositing ultra-thin, high-quality films essential for fabricating advanced microchips with improved performance and reduced power consumption. Emerging applications in other niche areas are also contributing to this burgeoning market.

Atomic Layer Deposition Coating System Market Size (In Billion)

The market's momentum is further fueled by continuous innovation in ALD system types. Thermal Atomic Layer Deposition (TALD) systems offer established reliability, while Plasma Enhanced Atomic Layer Deposition (PEALD) systems provide enhanced control and lower deposition temperatures, opening doors for new material combinations and sensitive substrates. The development of Power-Atomic Layer Deposition (Power-ALD) systems suggests a push towards higher throughput and scalability, catering to mass production needs. Key industry players are actively investing in research and development to refine these technologies and expand their application portfolios. While the ALD market benefits from strong demand, potential restraints such as the high initial capital investment for advanced systems and the need for skilled operators could moderate the pace of adoption in certain segments. However, the undeniable benefits of ALD in enabling next-generation technologies are expected to outweigh these challenges, ensuring sustained and strong market growth.

Atomic Layer Deposition Coating System Company Market Share

Atomic Layer Deposition Coating System Market: Comprehensive Analysis and Future Outlook (2019-2033)

This in-depth report provides a definitive analysis of the global Atomic Layer Deposition (ALD) Coating System market, examining its dynamics, key segments, product innovations, challenges, and future trajectory. Covering the historical period from 2019 to 2024, the base year of 2025, and a robust forecast period extending to 2033, this report offers actionable insights for industry stakeholders, including manufacturers, researchers, investors, and end-users. We delve into critical aspects such as market concentration, technological advancements, regulatory landscapes, and emerging opportunities within this rapidly evolving sector. The report utilizes billion for all monetary values and provides specific, quantifiable data where available.

Atomic Layer Deposition Coating System Market Concentration & Dynamics

The Atomic Layer Deposition (ALD) Coating System market exhibits a moderate to high concentration, with a few prominent players dominating a significant portion of the global market share. Leading companies like Beneq, Picosun, and Oxford Instruments have established strong footholds through continuous innovation and strategic market penetration. The innovation ecosystem is vibrant, characterized by significant R&D investments aimed at enhancing ALD process control, precursor compatibility, and throughput. Key metrics indicate that the top five companies command approximately 60% of the market share, with Forge Nano and Veeco also holding substantial positions. Regulatory frameworks, particularly concerning environmental impact and safety standards for precursor materials, are becoming increasingly stringent, influencing manufacturing processes and product development. Substitute products, such as Chemical Vapor Deposition (CVD) systems, offer a competitive challenge, but ALD’s superior conformality and precise thickness control for ultra-thin films secure its niche. End-user trends are heavily influenced by the booming semiconductor and medical device industries, driving demand for high-performance coatings. Merger and acquisition (M&A) activities, though not extremely frequent, are strategic, with a reported 15 M&A deals in the last five years, primarily focused on acquiring niche technological capabilities or expanding geographical reach.

Atomic Layer Deposition Coating System Industry Insights & Trends

The global Atomic Layer Deposition (ALD) Coating System market is poised for substantial growth, driven by an escalating demand for advanced thin-film coatings across diverse high-technology sectors. The market size is projected to reach approximately $20 billion by the end of the forecast period in 2033, exhibiting a compound annual growth rate (CAGR) of around 15%. This robust expansion is fueled by the unparalleled ability of ALD to deposit ultra-thin, highly conformal, and precisely controlled films at the atomic level. Technological disruptions are continuously reshaping the ALD landscape, with advancements in plasma-enhanced atomic layer deposition (PEALD) and spatial ALD (SALD) offering higher throughput and lower operating costs, making ALD more accessible for a wider range of applications. Evolving consumer behaviors, particularly the insatiable demand for miniaturized and high-performance electronic devices, wearables, and advanced medical implants, directly translate into increased reliance on ALD for critical component fabrication. The burgeoning semiconductor industry, with its relentless pursuit of smaller transistors and more complex architectures, is a primary growth engine. Similarly, the medical sector's need for biocompatible, anti-microbial, and drug-eluting coatings on implants and surgical instruments is a significant market driver. Furthermore, the aerospace and energy sectors are increasingly adopting ALD for protective coatings, corrosion resistance, and enhanced material properties. The development of new, environmentally friendly precursors and innovative reactor designs capable of handling larger substrate sizes are also key trends shaping the market's future. The increasing complexity of device manufacturing necessitates precise atomic-level control, a domain where ALD excels, thus underpinning its continuous market ascendancy.

Key Markets & Segments Leading Atomic Layer Deposition Coating System

The Semiconductor Wafer segment unequivocally leads the global Atomic Layer Deposition (ALD) Coating System market, driven by the insatiable demand for advanced microelectronics. This dominance is underpinned by several factors, including the relentless pursuit of Moore's Law, requiring increasingly sophisticated thin-film deposition for transistors, memory devices, and logic gates. The economic growth in developed and emerging economies, coupled with massive investments in semiconductor fabrication facilities worldwide, further fuels this segment's expansion.

Within the Application spectrum, the Semiconductor Wafer application commands an estimated 75% of the total market share, projected to reach $15 billion by 2033. Key drivers for this segment's leadership include:

- Miniaturization and Performance Enhancement: ALD's capability to deposit ultra-thin, conformal films is crucial for fabricating next-generation semiconductor devices with smaller feature sizes and enhanced electrical performance.

- Advanced Manufacturing Processes: High-k dielectrics, barrier layers, and passivation films essential for advanced chip manufacturing rely heavily on ALD techniques.

- Global Semiconductor Demand: The ever-increasing demand for smartphones, AI processors, data centers, and automotive electronics directly translates into higher ALD system adoption in wafer fabrication.

In terms of Types, the Plasma Enhanced Atomic Layer Deposition System (PEALD) segment is experiencing the most rapid growth and is projected to capture a significant market share, estimated at 55% of the total market by 2033, with a market value expected to reach $11 billion. This surge is attributable to:

- Lower Deposition Temperatures: PEALD enables the deposition of sensitive materials at lower temperatures, crucial for complex device architectures where thermal budget is a concern.

- Higher Deposition Rates: Compared to Thermal ALD, PEALD generally offers higher deposition rates, leading to increased throughput and reduced manufacturing costs.

- Wider Material Compatibility: PEALD allows for the deposition of a broader range of materials, including complex oxides and nitrides, which are vital for advanced semiconductor applications.

The Medical application segment, though smaller than semiconductors, is a rapidly growing area, projected to reach $2.5 billion by 2033. The demand for biocompatible coatings on implants, drug delivery systems, and biosensors is a key driver. The Optical Instrument segment, estimated at $1.5 billion by 2033, benefits from ALD's ability to create anti-reflective coatings, protective layers, and specialized optical filters. The Others segment, encompassing applications in energy, aerospace, and catalysis, is also showing promising growth, driven by the need for advanced protective and functional coatings.

Atomic Layer Deposition Coating System Product Developments

Product developments in the Atomic Layer Deposition (ALD) Coating System market are characterized by a relentless pursuit of enhanced precision, speed, and versatility. Companies are focusing on developing systems that can handle larger substrate sizes, reduce cycle times, and offer greater control over film stoichiometry and properties. Innovations in precursor delivery, plasma generation, and reactor design are leading to more efficient and cost-effective ALD processes. For instance, the development of spatial ALD (SALD) systems offers higher throughput for mass production, while advancements in PEALD cater to the deposition of a wider array of materials for demanding semiconductor and optoelectronic applications. These technological leaps are crucial for maintaining a competitive edge and meeting the evolving needs of industries like semiconductor manufacturing, medical devices, and advanced optics.

Challenges in the Atomic Layer Deposition Coating System Market

The Atomic Layer Deposition (ALD) Coating System market faces several challenges that can impact its growth trajectory. These include:

- High Capital Investment: ALD systems represent a significant upfront cost, which can be a barrier for smaller companies or those entering new application areas.

- Precursor Availability and Cost: The availability and cost of specialized ALD precursors can fluctuate, impacting the overall manufacturing economics.

- Process Complexity and Skill Requirements: Optimizing ALD processes and operating sophisticated systems requires highly skilled personnel, leading to a talent gap.

- Environmental Concerns: While ALD can be efficient, the use of certain precursors raises environmental and safety concerns, necessitating stricter regulations and the development of greener alternatives. The estimated impact of precursor cost volatility on market growth is approximately 5-10% annually.

Forces Driving Atomic Layer Deposition Coating System Growth

Several powerful forces are propelling the growth of the Atomic Layer Deposition (ALD) Coating System market. Technologically, the unrelenting demand for miniaturization and increased functionality in electronics, driven by advancements in semiconductors, fuels the need for ALD's atomic-level precision. Economically, the expansion of the semiconductor, medical device, and display industries, coupled with significant global investments in advanced manufacturing infrastructure, creates a robust market. Regulatory factors, such as stricter performance requirements for materials in critical applications, also indirectly benefit ALD by highlighting its superior capabilities. Furthermore, the growing adoption of ALD in emerging applications like quantum computing and advanced battery technologies represents a significant growth catalyst.

Challenges in the Atomic Layer Deposition Coating System Market

While the future is bright, the Atomic Layer Deposition (ALD) Coating System market must navigate certain long-term challenges. The ongoing need for process optimization to further reduce cycle times and increase throughput, especially for high-volume manufacturing, remains a critical area of focus. Developing ALD processes that are compatible with a wider range of substrate materials and complex 3D structures is also essential. Furthermore, the environmental sustainability of ALD processes, including the development of less toxic precursors and more energy-efficient systems, will become increasingly important as global environmental regulations tighten. Addressing these challenges through continued R&D and strategic partnerships will be key to unlocking the full potential of ALD technology.

Emerging Opportunities in Atomic Layer Deposition Coating System

Emerging opportunities in the Atomic Layer Deposition (ALD) Coating System market are vast and span across various innovative sectors. The burgeoning field of quantum computing, requiring precise atomic-level control for qubit fabrication, presents a significant untapped market. Advancements in flexible electronics and wearable devices demand ALD’s ability to deposit high-quality films on non-planar surfaces. The automotive industry's increasing electrification and demand for advanced sensors and battery components also represent substantial growth avenues. Furthermore, the development of novel ALD precursors and in-situ monitoring techniques offers opportunities for enhanced process control and new application development in areas like catalysis and advanced materials science. The market for ALD in flexible display technologies is projected to grow by over 20% annually.

Leading Players in the Atomic Layer Deposition Coating System Sector

- Forge Nano

- Beneq

- Oxford Instruments

- FHR Anlagenbau GmbH

- CVD Equipment Corporation

- SVT Associates

- Picosun

- Samco

- MLD Technologies

- Veeco

- Shenzhen Laplace Energy Technology

- Arradiance

- Alcadyne

- Denton Vacuum.

Key Milestones in Atomic Layer Deposition Coating System Industry

- 2019: Significant advancements in spatial ALD (SALD) technology leading to improved throughput for large-scale manufacturing.

- 2020: Introduction of new PEALD systems capable of depositing complex multi-layer stacks for advanced semiconductor nodes.

- 2021: Increased adoption of ALD for biocompatible coatings in the medical device industry, particularly for implants.

- 2022: Emergence of novel ALD precursor chemistries offering reduced toxicity and improved environmental profiles.

- 2023: Growing interest and R&D investment in ALD for applications in quantum computing and next-generation energy storage solutions.

- 2024: Further refinement of process control and automation in ALD systems, enabling higher yields and reduced manufacturing costs.

Strategic Outlook for Atomic Layer Deposition Coating System Market

The strategic outlook for the Atomic Layer Deposition (ALD) Coating System market is exceptionally positive, driven by the increasing complexity and performance demands of high-technology sectors. Growth accelerators include the ongoing miniaturization in the semiconductor industry, the expanding use of ALD in medical applications for enhanced biocompatibility and functionality, and the emergence of novel applications in areas like quantum computing and advanced energy solutions. Strategic opportunities lie in developing more cost-effective and higher-throughput ALD systems, expanding the range of compatible precursors and materials, and fostering collaborations across industry and academia to drive innovation. The market is expected to witness continued investment in R&D, with a focus on enhancing process control, reducing environmental impact, and addressing the growing need for atomic-level precision across a diverse range of applications.

Atomic Layer Deposition Coating System Segmentation

-

1. Application

- 1.1. Optical Instrument

- 1.2. Medical

- 1.3. Semiconductor Wafer

- 1.4. Others

-

2. Types

- 2.1. Thermal Atomic Layer Deposition System (TALD)

- 2.2. Plasma Enhanced Atomic Layer Deposition System (PEALD)

- 2.3. Power-Atomic Layer Deposition System (Power-ALD)

Atomic Layer Deposition Coating System Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

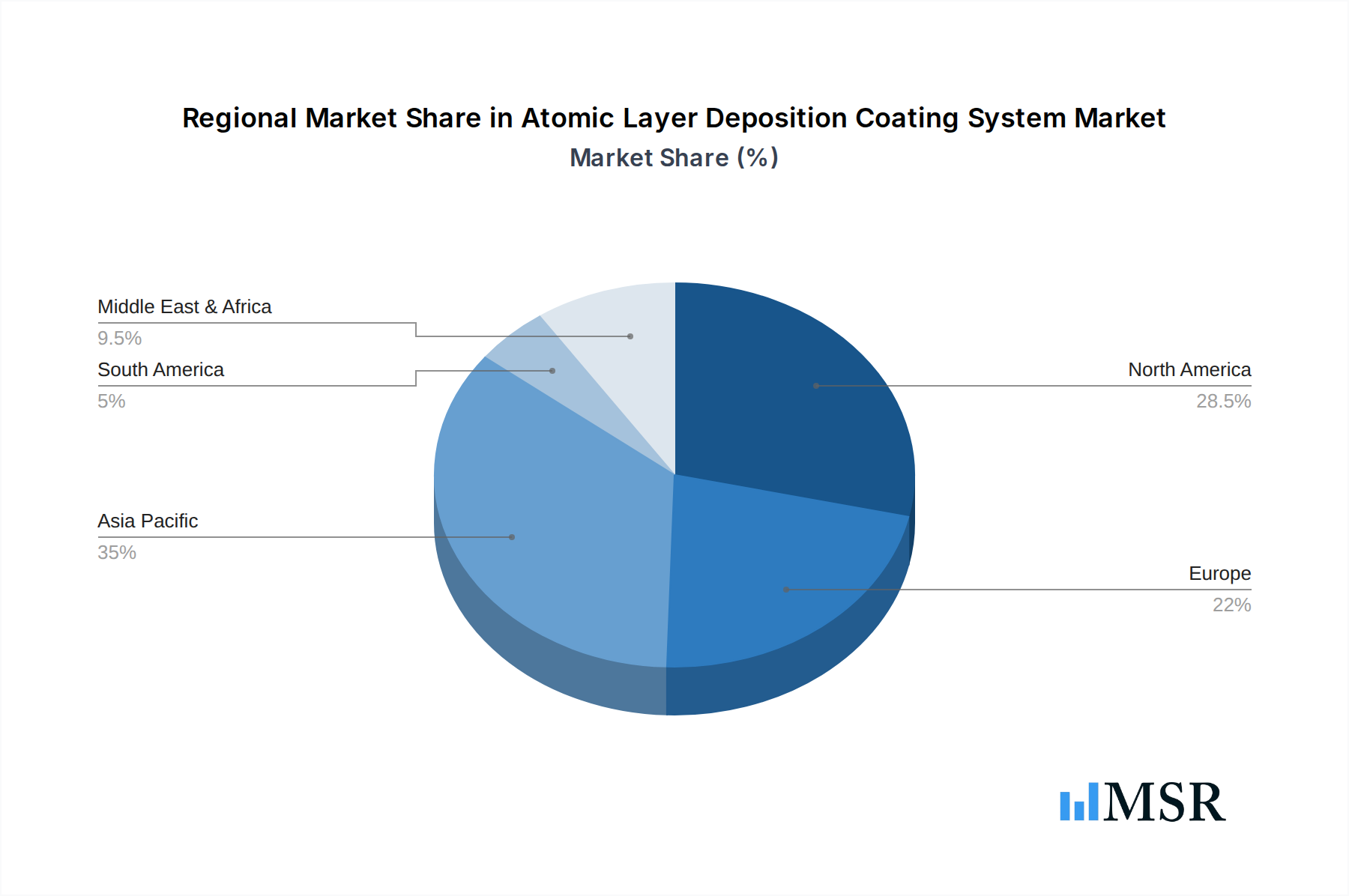

Atomic Layer Deposition Coating System Regional Market Share

Geographic Coverage of Atomic Layer Deposition Coating System

Atomic Layer Deposition Coating System REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.41% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Optical Instrument

- 5.1.2. Medical

- 5.1.3. Semiconductor Wafer

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Thermal Atomic Layer Deposition System (TALD)

- 5.2.2. Plasma Enhanced Atomic Layer Deposition System (PEALD)

- 5.2.3. Power-Atomic Layer Deposition System (Power-ALD)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Atomic Layer Deposition Coating System Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Optical Instrument

- 6.1.2. Medical

- 6.1.3. Semiconductor Wafer

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Thermal Atomic Layer Deposition System (TALD)

- 6.2.2. Plasma Enhanced Atomic Layer Deposition System (PEALD)

- 6.2.3. Power-Atomic Layer Deposition System (Power-ALD)

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Atomic Layer Deposition Coating System Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Optical Instrument

- 7.1.2. Medical

- 7.1.3. Semiconductor Wafer

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Thermal Atomic Layer Deposition System (TALD)

- 7.2.2. Plasma Enhanced Atomic Layer Deposition System (PEALD)

- 7.2.3. Power-Atomic Layer Deposition System (Power-ALD)

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Atomic Layer Deposition Coating System Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Optical Instrument

- 8.1.2. Medical

- 8.1.3. Semiconductor Wafer

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Thermal Atomic Layer Deposition System (TALD)

- 8.2.2. Plasma Enhanced Atomic Layer Deposition System (PEALD)

- 8.2.3. Power-Atomic Layer Deposition System (Power-ALD)

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Atomic Layer Deposition Coating System Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Optical Instrument

- 9.1.2. Medical

- 9.1.3. Semiconductor Wafer

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Thermal Atomic Layer Deposition System (TALD)

- 9.2.2. Plasma Enhanced Atomic Layer Deposition System (PEALD)

- 9.2.3. Power-Atomic Layer Deposition System (Power-ALD)

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Atomic Layer Deposition Coating System Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Optical Instrument

- 10.1.2. Medical

- 10.1.3. Semiconductor Wafer

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Thermal Atomic Layer Deposition System (TALD)

- 10.2.2. Plasma Enhanced Atomic Layer Deposition System (PEALD)

- 10.2.3. Power-Atomic Layer Deposition System (Power-ALD)

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Atomic Layer Deposition Coating System Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Optical Instrument

- 11.1.2. Medical

- 11.1.3. Semiconductor Wafer

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Thermal Atomic Layer Deposition System (TALD)

- 11.2.2. Plasma Enhanced Atomic Layer Deposition System (PEALD)

- 11.2.3. Power-Atomic Layer Deposition System (Power-ALD)

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Forge Nano

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Beneq

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Oxford Instruments

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 FHR Anlagenbau GmbH

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 CVD Equipment Corporation

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 SVT Associates

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Picosun

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Samco

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 MLD Technologies

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Veeco

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Shenzhen Laplace Energy Technology

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Arradiance

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Alcadyne

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Denton Vacuum.

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 Forge Nano

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Atomic Layer Deposition Coating System Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Atomic Layer Deposition Coating System Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Atomic Layer Deposition Coating System Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Atomic Layer Deposition Coating System Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Atomic Layer Deposition Coating System Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Atomic Layer Deposition Coating System Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Atomic Layer Deposition Coating System Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Atomic Layer Deposition Coating System Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Atomic Layer Deposition Coating System Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Atomic Layer Deposition Coating System Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Atomic Layer Deposition Coating System Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Atomic Layer Deposition Coating System Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Atomic Layer Deposition Coating System Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Atomic Layer Deposition Coating System Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Atomic Layer Deposition Coating System Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Atomic Layer Deposition Coating System Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Atomic Layer Deposition Coating System Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Atomic Layer Deposition Coating System Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Atomic Layer Deposition Coating System Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Atomic Layer Deposition Coating System Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Atomic Layer Deposition Coating System Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Atomic Layer Deposition Coating System Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Atomic Layer Deposition Coating System Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Atomic Layer Deposition Coating System Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Atomic Layer Deposition Coating System Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Atomic Layer Deposition Coating System Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Atomic Layer Deposition Coating System Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Atomic Layer Deposition Coating System Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Atomic Layer Deposition Coating System Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Atomic Layer Deposition Coating System Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Atomic Layer Deposition Coating System Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Atomic Layer Deposition Coating System Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Atomic Layer Deposition Coating System Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Atomic Layer Deposition Coating System Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Atomic Layer Deposition Coating System Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Atomic Layer Deposition Coating System Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Atomic Layer Deposition Coating System Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Atomic Layer Deposition Coating System Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Atomic Layer Deposition Coating System Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Atomic Layer Deposition Coating System Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Atomic Layer Deposition Coating System Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Atomic Layer Deposition Coating System Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Atomic Layer Deposition Coating System Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Atomic Layer Deposition Coating System Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Atomic Layer Deposition Coating System Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Atomic Layer Deposition Coating System Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Atomic Layer Deposition Coating System Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Atomic Layer Deposition Coating System Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Atomic Layer Deposition Coating System Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Atomic Layer Deposition Coating System Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Atomic Layer Deposition Coating System?

The projected CAGR is approximately 10.41%.

2. Which companies are prominent players in the Atomic Layer Deposition Coating System?

Key companies in the market include Forge Nano, Beneq, Oxford Instruments, FHR Anlagenbau GmbH, CVD Equipment Corporation, SVT Associates, Picosun, Samco, MLD Technologies, Veeco, Shenzhen Laplace Energy Technology, Arradiance, Alcadyne, Denton Vacuum..

3. What are the main segments of the Atomic Layer Deposition Coating System?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Atomic Layer Deposition Coating System," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Atomic Layer Deposition Coating System report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Atomic Layer Deposition Coating System?

To stay informed about further developments, trends, and reports in the Atomic Layer Deposition Coating System, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence