Key Insights

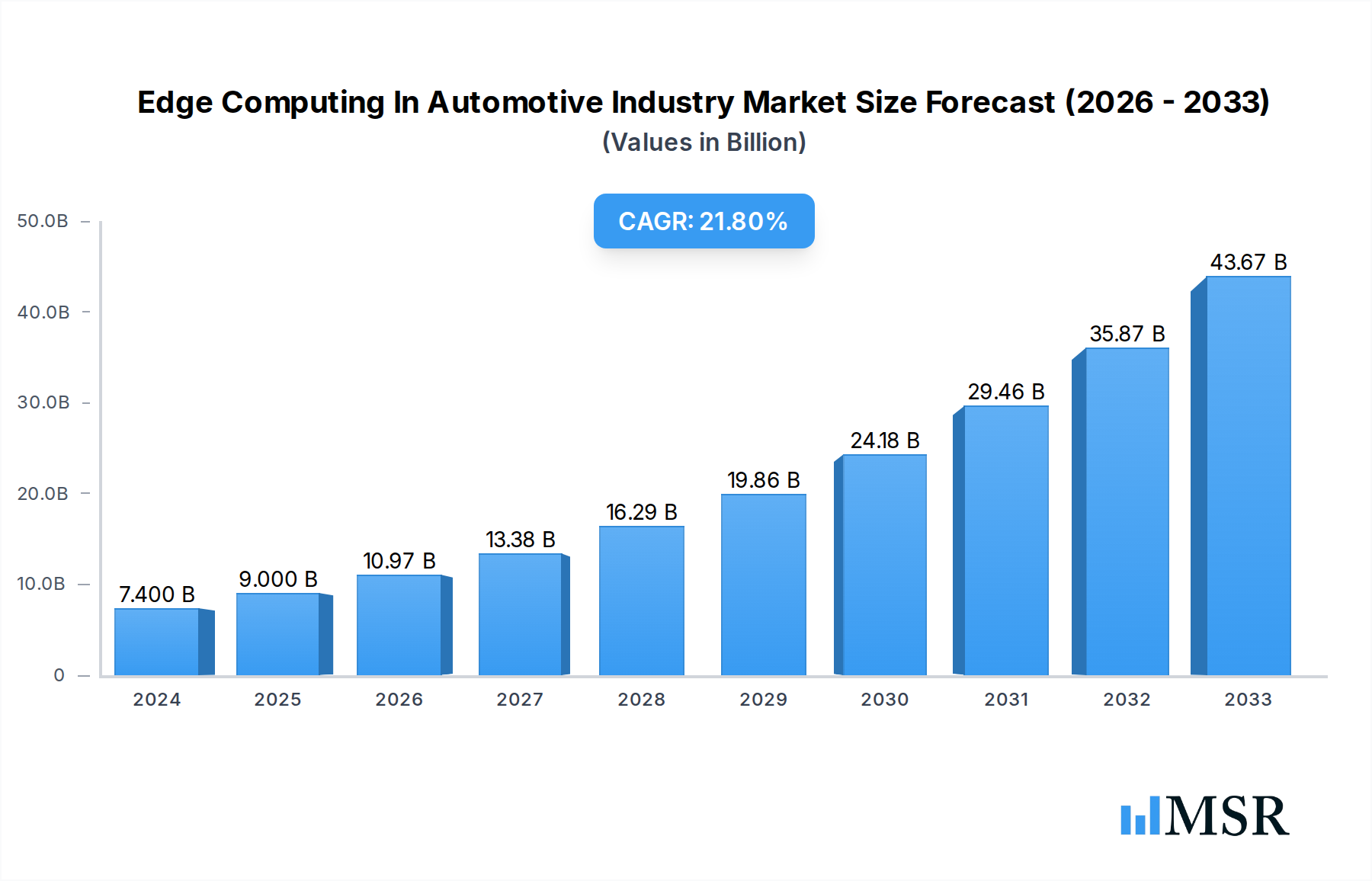

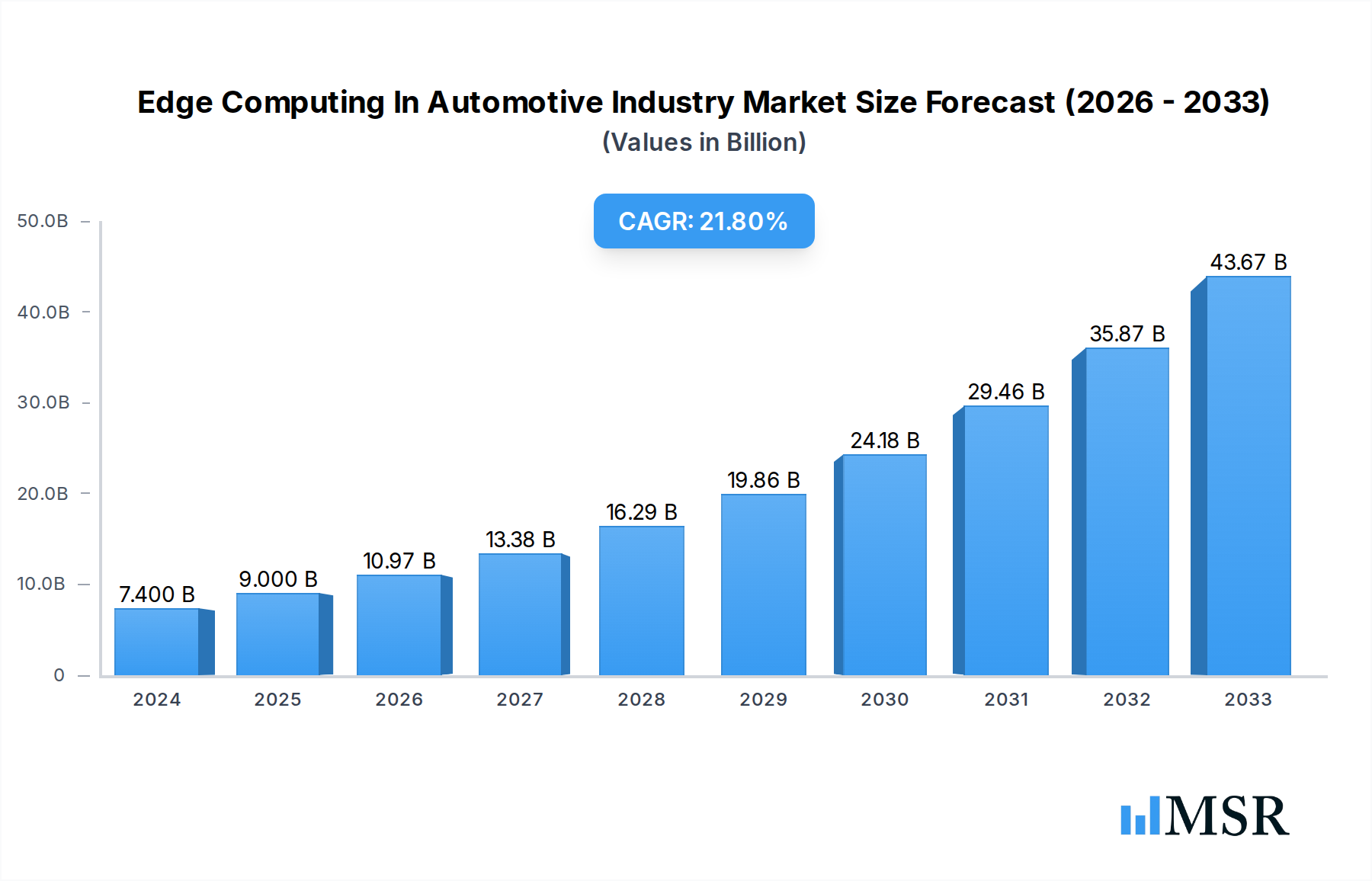

The Edge Computing in Automotive Industry is poised for remarkable expansion, with a market size of approximately $7.4 billion in 2024 and a projected Compound Annual Growth Rate (CAGR) of 21.7% during the forecast period of 2025-2033. This robust growth is primarily fueled by the accelerating adoption of connected car technologies, the critical need for real-time data processing for enhanced safety features like advanced driver-assistance systems (ADAS) and autonomous driving, and the burgeoning development of smart city initiatives. The integration of AI and machine learning at the edge is enabling faster decision-making, reduced latency, and improved operational efficiency across various automotive applications. Furthermore, the growing demand for sophisticated in-vehicle infotainment systems and the increasing deployment of vehicle-to-everything (V2X) communication are significant contributors to this upward trajectory. Key players are heavily investing in developing advanced edge solutions to cater to these evolving demands.

Edge Computing In Automotive Industry Market Size (In Billion)

The market is witnessing a significant shift towards distributed computing architectures, enabling data to be processed closer to its source, thus minimizing reliance on centralized cloud infrastructure. This trend is particularly vital for applications like real-time traffic management, optimizing transportation and logistics operations, and enhancing the overall efficiency of smart city ecosystems. While the rapid advancements in technology and increasing adoption of IoT devices within vehicles act as strong growth drivers, challenges such as cybersecurity concerns, standardization issues, and the high initial investment costs for edge infrastructure may present some restraining factors. However, the immense benefits offered by edge computing in terms of enhanced performance, improved safety, and greater connectivity are expected to outweigh these challenges, paving the way for widespread implementation across the automotive value chain.

Edge Computing In Automotive Industry Company Market Share

Report Description: Edge Computing in the Automotive Industry - Driving the Future of Mobility

Unlock the billion-dollar potential of edge computing in the automotive sector. This comprehensive report dives deep into the rapidly evolving landscape of edge computing for connected vehicles, autonomous driving, and smart transportation. Discover critical market insights, technological advancements, and strategic opportunities poised to reshape the automotive industry. With a study period spanning 2019–2033, a base year of 2025, and a forecast period of 2025–2033, this report offers unparalleled foresight into a market projected to reach billions in valuation. Explore how innovations in connected cars, traffic management, smart cities, and transportation & logistics are being powered by robust edge AI and 5G automotive solutions.

This report is an essential resource for automotive OEMs, Tier-1 suppliers, technology providers, fleet operators, urban planners, and investors seeking to capitalize on the transformative power of edge computing. Gain actionable intelligence on edge network security, automotive edge platforms, autonomous vehicle edge computing, and the strategic implications for digital transformation in automotive.

Edge Computing In Automotive Industry Market Concentration & Dynamics

The edge computing in the automotive industry exhibits a dynamic market concentration, characterized by a blend of established technology giants and agile startups vying for dominance. Innovation ecosystems are flourishing, driven by partnerships and intense R&D efforts, particularly in areas like AI for autonomous driving and IoT in automotive. Regulatory frameworks are slowly adapting to accommodate the complexities of connected car data security and vehicle-to-everything (V2X) communication standards. Substitute products, while present, are increasingly being outpaced by the superior latency and processing capabilities offered by edge solutions. End-user trends are heavily skewed towards enhanced safety, improved user experience, and the promise of autonomous mobility, all of which significantly boost demand for advanced edge capabilities. Merger and acquisition (M&A) activities have been instrumental in consolidating market share and acquiring critical technologies, with a growing number of deals valued in the billions. For instance, numerous acquisitions focus on enhancing edge AI hardware and automotive cybersecurity solutions.

- Market Share Dynamics: While a few dominant players hold significant market share, the landscape is fragmenting as new entrants introduce specialized edge solutions.

- M&A Activities: Billions are being invested in acquiring innovative edge computing companies and automotive software providers to accelerate product development and market penetration.

- Innovation Hubs: Key regions are emerging as centers for automotive edge development, fostering collaboration between research institutions and industry leaders.

Edge Computing In Automotive Industry Industry Insights & Trends

The edge computing in the automotive industry is experiencing exponential growth, driven by a convergence of technological advancements and escalating demand for real-time data processing. The market size is projected to surge into the billions, fueled by the increasing complexity of vehicles and the proliferation of intelligent transportation systems. Key growth drivers include the relentless pursuit of autonomous vehicle deployment, the necessity for enhanced in-car infotainment, and the critical need for efficient smart city infrastructure. Technological disruptions, such as the widespread adoption of 5G networks, advancements in edge AI algorithms, and the development of robust edge computing hardware for vehicles, are fundamentally reshaping the industry. Evolving consumer behaviors, characterized by a growing expectation for seamless connectivity, personalized experiences, and advanced safety features, are pushing OEMs and technology providers to invest heavily in edge solutions. The CAGR is anticipated to be substantial, reflecting the transformative impact of edge computing on every facet of the automotive ecosystem, from vehicle design and manufacturing to operational efficiency and user interaction. The ability of edge devices to process data locally, reducing reliance on cloud connectivity for critical functions, is a major trend. This includes the deployment of edge gateways for automotive and sophisticated edge analytics for transportation.

Key Markets & Segments Leading Edge Computing In Automotive Industry

The Connected Cars segment is emerging as a dominant force in the edge computing in the automotive industry, driving significant market value projected to reach billions. This dominance is fueled by the escalating demand for enhanced safety features, real-time diagnostics, over-the-air updates, and sophisticated infotainment systems. The proliferation of connected vehicle technologies necessitates powerful on-board processing capabilities, making edge computing indispensable. Furthermore, the Smart Cities segment is a crucial growth accelerator, leveraging edge computing for intelligent traffic management, public safety, and efficient resource allocation. The integration of connected vehicles with smart city infrastructure creates a synergistic environment where edge devices at the roadside and within vehicles can communicate and process data collaboratively.

Drivers for Connected Cars Dominance:

- Increasing adoption of advanced driver-assistance systems (ADAS).

- Consumer demand for personalized in-car digital experiences.

- Regulatory mandates for vehicle safety and communication capabilities.

- The growth of the automotive IoT ecosystem.

Drivers for Smart Cities Leadership:

- Urbanization and the need for intelligent infrastructure solutions.

- Government initiatives to improve urban mobility and sustainability.

- The potential for edge computing in traffic management to reduce congestion and emissions.

- The development of smart city platforms leveraging real-time data.

The Transportation & Logistics segment also presents significant opportunities, with edge computing enabling real-time fleet management, predictive maintenance, and optimized route planning, further contributing to market growth into the billions. While Traffic Management and Other Applications are crucial, the immediate impact and investment in Connected Cars and the foundational role in Smart Cities position them as the primary leaders in the current edge computing adoption cycle within the automotive sector.

Edge Computing In Automotive Industry Product Developments

Product innovations in edge computing for the automotive industry are rapidly expanding, focusing on miniaturization, power efficiency, and enhanced processing power for localized data analysis. Companies are developing specialized edge AI chips and integrated edge computing modules designed to withstand the harsh automotive environment. These advancements enable real-time processing of sensor data for features like advanced driver-assistance systems (ADAS), autonomous driving functions, and sophisticated in-cabin user experiences. The market relevance of these products is immense, offering competitive advantages through reduced latency, improved data security, and optimized bandwidth utilization, all critical for a trillion-dollar industry transformation.

Challenges in the Edge Computing In Automotive Industry Market

The edge computing in the automotive industry faces several significant challenges that can hinder its widespread adoption and growth into the billions. Regulatory hurdles surrounding data privacy and security for connected vehicle data remain a complex issue, requiring standardized frameworks and robust compliance measures. Supply chain disruptions, particularly for specialized semiconductor components needed for advanced edge processors, can impact production volumes and timelines. Competitive pressures from established players and emerging startups intensify the need for differentiation and cost-effectiveness in automotive edge solutions. Furthermore, the integration of disparate edge systems and the need for interoperability across different vehicle platforms and infrastructure pose technical complexities.

Forces Driving Edge Computing In Automotive Industry Growth

Several powerful forces are propelling the growth of edge computing in the automotive industry, pushing the market towards billions in valuation. The relentless advancement of autonomous driving technology is a primary driver, demanding ultra-low latency processing of sensor data that only edge computing can provide. The increasing sophistication of in-car electronics and the demand for immersive automotive infotainment systems necessitate localized processing power. Furthermore, the widespread deployment of 5G networks offers the high bandwidth and low latency required for seamless communication between edge devices and essential cloud services. Government initiatives promoting smart city development and intelligent transportation systems are also significant catalysts, encouraging the adoption of edge solutions for improved traffic flow, safety, and environmental sustainability. The economic benefits of reducing cloud data transfer costs and improving operational efficiency for fleet management also contribute substantially.

Challenges in the Edge Computing In Automotive Industry Market

The long-term growth of edge computing in the automotive industry, projected to reach billions, hinges on overcoming persistent challenges. Standardization of edge computing protocols and V2X communication standards is crucial for interoperability and seamless integration across diverse vehicle architectures and infrastructure. Developing robust edge AI cybersecurity solutions to protect sensitive vehicle and passenger data from evolving threats is paramount. The high initial investment required for implementing edge infrastructure, both within vehicles and for supporting roadside units, can be a significant barrier for smaller players. Furthermore, the ongoing need for continuous software updates and maintenance for distributed edge devices presents logistical and operational complexities. Addressing these challenges will be vital for unlocking the full potential of the edge in transforming the automotive landscape.

Emerging Opportunities in Edge Computing In Automotive Industry

Emerging opportunities in edge computing within the automotive industry are creating new avenues for innovation and market expansion, projected to contribute billions to the overall valuation. The burgeoning field of edge-enabled predictive maintenance for vehicles offers significant cost savings and improved vehicle uptime for fleet operators and individual owners. The integration of edge AI for enhanced driver monitoring systems presents opportunities to improve safety and personalize the driving experience. Furthermore, the development of edge computing solutions for last-mile delivery vehicles and the broader autonomous logistics sector is a rapidly growing market. The increasing consumer demand for highly personalized in-car experiences, powered by edge AI personalization engines, opens doors for new service offerings and revenue streams. The intersection of edge computing with augmented reality (AR) and virtual reality (VR) technologies for automotive AR HUDs and immersive navigation is another promising frontier.

Leading Players in the Edge Computing In Automotive Industry Sector

- Digi International Inc

- Belden Inc

- Amazon Web Services (AWS) Inc

- Azion Technologies Ltd

- Altran Inc

- Cisco Systems Inc

- Hewlett Packard Enterprise Development LP

- Litmus Automation

- Huawei Technologies Co Ltd

- General Electric Company

Key Milestones in Edge Computing In Automotive Industry Industry

- February 2023: Digi International announced The Digi IX10 cellular router, which launches at DistribuTECH 2023 and expands its portfolio of the private cellular network (PCN) solutions, offering much-needed connectivity for smart grid devices using the CBRS shared spectrum and Anterix Band 8 900 MHz licensed spectrum. This development signifies a crucial step in robust connectivity for distributed intelligent systems, impacting the broader IoT ecosystem that supports automotive applications.

- March 2022: Cisco announced a partnership with Verizon in a successful proof-of-concept demo in Las Vegas to demonstrate that cellular and mobile edge computing (MEC) technology can facilitate autonomous driving solutions without the use of expensive physical roadside units to extend the radio signal. This milestone validates the potential of MEC for autonomous vehicle connectivity and reduces reliance on costly physical infrastructure.

Strategic Outlook for Edge Computing In Automotive Industry Market

The strategic outlook for the edge computing in the automotive industry is exceptionally strong, with projected market growth into the billions. The increasing focus on autonomous driving, connected services, and smart mobility infrastructure will continue to fuel demand for sophisticated edge solutions. Key growth accelerators include strategic partnerships between automotive OEMs, technology providers, and telecommunications companies to develop integrated edge automotive platforms. Investments in edge AI hardware optimization for automotive applications will drive further innovation and cost efficiencies. The expansion of V2X communication deployments will create a more interconnected and intelligent transportation ecosystem. Furthermore, the development of standardized automotive edge security frameworks will build trust and encourage wider adoption. The long-term potential lies in creating a fully autonomous and highly connected mobility future, where edge computing is the foundational technology.

Edge Computing In Automotive Industry Segmentation

-

1. Application

- 1.1. Connected Cars

- 1.2. Traffic Management

- 1.3. Smart Cities

- 1.4. Transportation & Logistics

- 1.5. Other Applications

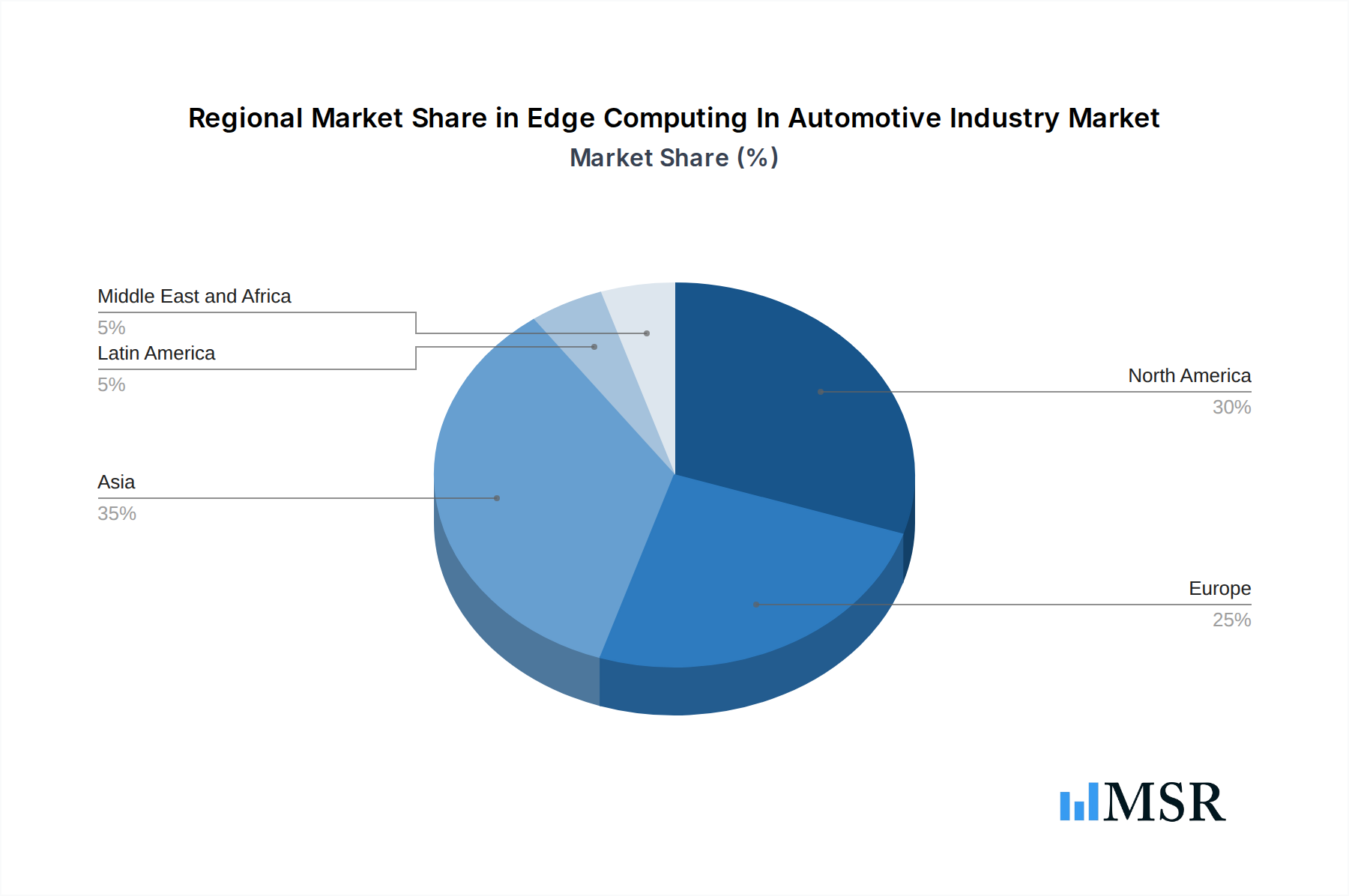

Edge Computing In Automotive Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Latin America

- 5. Middle East and Africa

Edge Computing In Automotive Industry Regional Market Share

Geographic Coverage of Edge Computing In Automotive Industry

Edge Computing In Automotive Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 21.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Connected Cars

- 5.1.2. Traffic Management

- 5.1.3. Smart Cities

- 5.1.4. Transportation & Logistics

- 5.1.5. Other Applications

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia

- 5.2.4. Latin America

- 5.2.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Edge Computing In Automotive Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Connected Cars

- 6.1.2. Traffic Management

- 6.1.3. Smart Cities

- 6.1.4. Transportation & Logistics

- 6.1.5. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Edge Computing In Automotive Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Connected Cars

- 7.1.2. Traffic Management

- 7.1.3. Smart Cities

- 7.1.4. Transportation & Logistics

- 7.1.5. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Edge Computing In Automotive Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Connected Cars

- 8.1.2. Traffic Management

- 8.1.3. Smart Cities

- 8.1.4. Transportation & Logistics

- 8.1.5. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Asia Edge Computing In Automotive Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Connected Cars

- 9.1.2. Traffic Management

- 9.1.3. Smart Cities

- 9.1.4. Transportation & Logistics

- 9.1.5. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Latin America Edge Computing In Automotive Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Connected Cars

- 10.1.2. Traffic Management

- 10.1.3. Smart Cities

- 10.1.4. Transportation & Logistics

- 10.1.5. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Middle East and Africa Edge Computing In Automotive Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Connected Cars

- 11.1.2. Traffic Management

- 11.1.3. Smart Cities

- 11.1.4. Transportation & Logistics

- 11.1.5. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Digi International Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Belden Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Amazon Web Services (AWS) Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Azion Technologies Ltd

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Altran Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Cisco Systems Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Hewlett Packard Enterprise Development LP

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Litmus Automation

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Huawei Technologies Co Ltd

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 General Electric Company

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Digi International Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Edge Computing In Automotive Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Edge Computing In Automotive Industry Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Edge Computing In Automotive Industry Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Edge Computing In Automotive Industry Revenue (billion), by Country 2025 & 2033

- Figure 5: North America Edge Computing In Automotive Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Edge Computing In Automotive Industry Revenue (billion), by Application 2025 & 2033

- Figure 7: Europe Edge Computing In Automotive Industry Revenue Share (%), by Application 2025 & 2033

- Figure 8: Europe Edge Computing In Automotive Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: Europe Edge Computing In Automotive Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Edge Computing In Automotive Industry Revenue (billion), by Application 2025 & 2033

- Figure 11: Asia Edge Computing In Automotive Industry Revenue Share (%), by Application 2025 & 2033

- Figure 12: Asia Edge Computing In Automotive Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Asia Edge Computing In Automotive Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Latin America Edge Computing In Automotive Industry Revenue (billion), by Application 2025 & 2033

- Figure 15: Latin America Edge Computing In Automotive Industry Revenue Share (%), by Application 2025 & 2033

- Figure 16: Latin America Edge Computing In Automotive Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Latin America Edge Computing In Automotive Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Middle East and Africa Edge Computing In Automotive Industry Revenue (billion), by Application 2025 & 2033

- Figure 19: Middle East and Africa Edge Computing In Automotive Industry Revenue Share (%), by Application 2025 & 2033

- Figure 20: Middle East and Africa Edge Computing In Automotive Industry Revenue (billion), by Country 2025 & 2033

- Figure 21: Middle East and Africa Edge Computing In Automotive Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Edge Computing In Automotive Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Edge Computing In Automotive Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Global Edge Computing In Automotive Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 4: Global Edge Computing In Automotive Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: Global Edge Computing In Automotive Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 6: Global Edge Computing In Automotive Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Edge Computing In Automotive Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global Edge Computing In Automotive Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Global Edge Computing In Automotive Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 10: Global Edge Computing In Automotive Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 11: Global Edge Computing In Automotive Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 12: Global Edge Computing In Automotive Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Edge Computing In Automotive Industry?

The projected CAGR is approximately 21.7%.

2. Which companies are prominent players in the Edge Computing In Automotive Industry?

Key companies in the market include Digi International Inc, Belden Inc, Amazon Web Services (AWS) Inc, Azion Technologies Ltd , Altran Inc, Cisco Systems Inc, Hewlett Packard Enterprise Development LP, Litmus Automation, Huawei Technologies Co Ltd, General Electric Company.

3. What are the main segments of the Edge Computing In Automotive Industry?

The market segments include Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.4 billion as of 2022.

5. What are some drivers contributing to market growth?

Rising Adoption of IOT; Exponentially Growing Data Volumes And Network Traffic.

6. What are the notable trends driving market growth?

Rising Adoption of IOT to Witness the Growth Edge Computing in Automotive Market.

7. Are there any restraints impacting market growth?

Initial Capital Expenditure For Infrastructure; Privacy and Security Concerns.

8. Can you provide examples of recent developments in the market?

February 2023: Digi International announced The Digi IX10 cellular router, which launches at DistribuTECH 2023 and expands its portfolio of the private cellular network (PCN) solutions, offering much-needed connectivity for smart grid devices using the CBRS shared spectrum and Anterix Band 8 900 MHz licensed spectrum.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Edge Computing In Automotive Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Edge Computing In Automotive Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Edge Computing In Automotive Industry?

To stay informed about further developments, trends, and reports in the Edge Computing In Automotive Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence