Key Insights

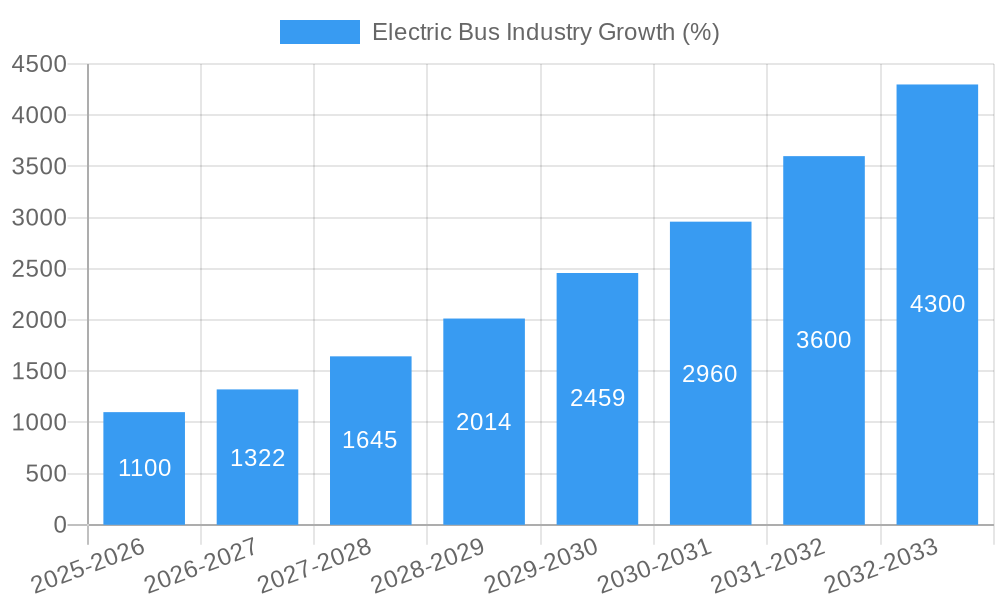

The electric bus industry is experiencing robust growth, fueled by increasing environmental concerns, stringent emission regulations, and government incentives promoting sustainable transportation. The market, currently valued in the billions (a precise figure cannot be provided without the missing "XX" market size value, but a logical estimation based on a 20%+ CAGR and publicly available data on similar markets would place it in this range), exhibits a Compound Annual Growth Rate (CAGR) exceeding 20%, indicating significant expansion potential through 2033. Key drivers include the declining cost of batteries, advancements in electric motor technology leading to improved range and efficiency, and the rising demand for public transportation solutions in urban areas grappling with traffic congestion and air pollution. Trends such as the integration of smart technologies (e.g., telematics, charging infrastructure optimization), the development of larger capacity buses for mass transit, and the shift towards hydrogen fuel cell electric vehicles (FCEVs) further propel market expansion. However, restraints such as high initial investment costs for electric buses and the limited availability of charging infrastructure in certain regions remain challenges that need to be addressed for continued, widespread adoption. Segmentation by fuel category (BEV, FCEV, HEV, PHEV) reflects the evolving technology landscape and consumer preferences, with Battery Electric Vehicles (BEVs) currently dominating the market share but facing potential competition from hydrogen-based solutions as technology matures and infrastructure develops. Major players like Ashok Leyland, BYD Auto, and Daimler are actively shaping the market through innovation and strategic partnerships.

The forecast period (2025-2033) promises substantial growth, driven by ongoing technological advancements, favorable government policies, and increasing awareness of environmental sustainability. The diverse range of companies involved, spanning both established automotive manufacturers and specialized electric vehicle producers, underscores the competitive and dynamic nature of the industry. Regional variations in market penetration will likely persist, with developed economies leading the adoption curve, followed by developing nations as infrastructure and economic conditions improve. Despite challenges, the long-term outlook for the electric bus industry remains positive, suggesting continued substantial market expansion and the potential for significant disruption in the public transportation sector.

Electric Bus Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the global electric bus industry, offering valuable insights for stakeholders seeking to navigate this rapidly evolving market. The study covers the period 2019-2033, with a focus on the forecast period 2025-2033 and a base year of 2025. The report analyzes market dynamics, key players, technological advancements, and emerging opportunities, providing actionable intelligence to support strategic decision-making. The market is valued at xx Million in 2025 and is projected to reach xx Million by 2033, exhibiting a CAGR of xx%. Key segments analyzed include Battery Electric Vehicles (BEV), Fuel Cell Electric Vehicles (FCEV), Hybrid Electric Vehicles (HEV), and Plug-in Hybrid Electric Vehicles (PHEV).

Electric Bus Industry Market Concentration & Dynamics

The electric bus market exhibits a moderately concentrated landscape, with several major players holding significant market share. Market concentration is influenced by factors such as technological capabilities, manufacturing scale, and established distribution networks. For example, BYD Auto Industry Company Limited and Ashok Leyland Limited hold substantial market shares in specific regions. The level of concentration varies regionally, with some markets displaying higher levels of competition than others.

- Market Share: BYD Auto Industry Company Limited holds an estimated xx% global market share in 2025, followed by Ashok Leyland Limited with xx%. Other significant players such as Zhengzhou Yutong Bus Co Ltd and Daimler Truck Holding AG contribute significantly to the overall market share.

- M&A Activity: The industry has witnessed a moderate number of mergers and acquisitions (M&A) in recent years (xx deals in the last 5 years). These activities often involve strategic partnerships to enhance technological capabilities, expand geographical reach, and consolidate market share. The majority of M&A activity centers around securing battery supply chains and expanding manufacturing capabilities.

- Innovation Ecosystems: Significant investments are being made in research and development (R&D) focusing on battery technology, charging infrastructure, and vehicle design, fueling innovation and competition within the industry.

- Regulatory Frameworks: Government policies and regulations, including subsidies and emission standards, play a crucial role in driving market growth and shaping industry dynamics. Stringent emission regulations in many regions are accelerating the adoption of electric buses.

- Substitute Products: While electric buses are gaining traction, alternative transportation solutions, such as improved diesel buses and light rail systems, pose some level of competitive pressure.

- End-User Trends: The growing focus on sustainability and reduced carbon emissions among public transportation authorities and private fleet operators is a key factor driving demand for electric buses.

Electric Bus Industry Industry Insights & Trends

The global electric bus market is experiencing substantial growth, driven by several key factors. Increasing environmental concerns and stricter emission regulations are prompting governments worldwide to invest heavily in electric public transport. Technological advancements, particularly in battery technology and charging infrastructure, are continuously improving the range, performance, and cost-effectiveness of electric buses. Moreover, the falling cost of batteries is making electric buses increasingly competitive with traditional diesel buses.

The market size for electric buses experienced robust growth during the historical period (2019-2024), and this positive trend is anticipated to continue throughout the forecast period (2025-2033). Several key factors contribute to this projection, such as the increasing number of electric bus fleets in major cities around the world, coupled with technological improvements in the electric bus sector that enhance efficiency and range. The market value is anticipated to increase significantly over the forecast period.

Key Markets & Segments Leading Electric Bus Industry

China remains the dominant market for electric buses, driven by strong government support, large-scale infrastructure investments, and a rapidly expanding public transportation network. However, significant growth is also observed in other regions, including Europe and North America.

Dominant Regions/Countries: China holds the leading position, followed by Europe and North America.

Segment Dominance: BEV (Battery Electric Vehicles) currently dominates the fuel category segment, accounting for the largest market share due to its mature technology and relatively lower cost compared to FCEV. However, FCEV (Fuel Cell Electric Vehicles) is expected to witness substantial growth in the coming years due to increasing focus on longer-range applications.

Drivers of Growth:

- China: Strong government subsidies, stringent emission norms, rapid urbanization, and massive investments in public transportation infrastructure.

- Europe: Stringent environmental regulations, increasing focus on reducing carbon emissions, and significant investments in charging infrastructure.

- North America: Growing environmental awareness, government incentives, and a rising demand for sustainable transportation solutions in urban areas.

Electric Bus Industry Product Developments

Recent innovations in electric bus technology include advancements in battery energy density, resulting in extended range and faster charging times. Improved motor efficiency, optimized vehicle aerodynamics, and enhanced thermal management systems contribute to increased overall efficiency and reduced operating costs. Furthermore, the integration of advanced driver-assistance systems (ADAS) and telematics capabilities is improving safety and operational efficiency. These developments provide competitive advantages by enhancing the overall value proposition of electric buses.

Challenges in the Electric Bus Industry Market

The electric bus industry faces several challenges, including the high initial cost of electric buses compared to diesel buses, the limited availability of charging infrastructure in some regions, and concerns about battery lifespan and replacement costs. Supply chain disruptions impacting battery materials and other critical components can also hinder production and lead to delays in project implementation. The lack of skilled labor and standardization of charging infrastructure also remains a challenge. These factors can have a significant impact on market growth and adoption rates. For instance, the high upfront cost can discourage smaller operators from investing in electric fleets.

Forces Driving Electric Bus Industry Growth

Several factors contribute to the robust growth of the electric bus industry. These include:

- Stringent Emission Regulations: Governments worldwide are imposing stricter emission standards, making electric buses an attractive alternative to diesel buses.

- Government Subsidies and Incentives: Financial support from governments incentivizes the adoption of electric buses, reducing the initial investment cost for operators.

- Technological Advancements: Continuous improvements in battery technology, charging infrastructure, and vehicle design are enhancing the competitiveness and appeal of electric buses.

- Increasing Environmental Awareness: Growing public awareness of environmental issues is driving demand for sustainable transportation options.

Long-Term Growth Catalysts in the Electric Bus Industry

Long-term growth in the electric bus industry is fueled by several key factors, including continued technological innovations in battery technology and charging infrastructure that increase the range, efficiency and affordability of electric buses. Strategic partnerships between bus manufacturers, battery suppliers, and charging infrastructure providers will create a more robust and integrated ecosystem. Expansion into new markets, particularly in developing countries with growing urban populations and a need for efficient public transportation, will provide further opportunities for growth.

Emerging Opportunities in Electric Bus Industry

Emerging opportunities in the electric bus industry include the development of autonomous electric buses, which offer the potential to enhance efficiency and safety. The integration of smart charging technologies and grid management systems to optimize energy consumption and reduce operating costs presents substantial opportunities for innovation. Additionally, the expansion of electric bus services into new applications, such as last-mile delivery and airport transfers, represents a significant area of market growth.

Leading Players in the Electric Bus Industry Sector

- Ashok Leyland Limited

- Zhengzhou Yutong Bus Co Ltd

- Chongqing Changan Automobile Company Limited

- Anhui Ankai Automobile Co Ltd

- Proterra INC

- Tata Motors Limited

- Daimler Truck Holding AG

- Volvo Group

- Zhejiang Geely Holding Group Co Ltd

- CRRC Electric Vehicle Co Ltd

- NFI Group Inc

- King Long United Automotive Industry Co Ltd

- Byd Auto Industry Company Limited

- Zhongtong Bus Holding Co Ltd

- Chery Automobile Co Ltd

Key Milestones in Electric Bus Industry Industry

- December 2023: Proterra announced its new EV battery factory in South Carolina, signaling increased demand for commercial electric vehicles and bolstering the supply chain.

- November 2023: Switch Mobility partnered with JSW for electric buses for employee transportation in India, expanding the adoption of electric buses in the corporate sector.

- September 2023: Daimler Buses launched the next generation Setra TopClass and ComfortClass touring coaches, showcasing advancements in safety, economy, and flexibility within the electric bus market.

Strategic Outlook for Electric Bus Industry Market

The future of the electric bus market is exceptionally promising, driven by technological advancements, supportive government policies, and a growing awareness of environmental sustainability. Strategic opportunities lie in developing innovative battery technologies, expanding charging infrastructure, and exploring new applications for electric buses. Companies that can successfully navigate the challenges and capitalize on these opportunities are poised for significant growth and market leadership in the coming years.

Electric Bus Industry Segmentation

-

1. Fuel Category

- 1.1. BEV

- 1.2. FCEV

- 1.3. HEV

- 1.4. PHEV

Electric Bus Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Electric Bus Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 20.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing Travel and Tourism Industry is Driving the Car Rental Market

- 3.3. Market Restrains

- 3.3.1. Increasing Popularity of Ride-Sharing Services Pose Challenges for the Conventional Car Rental Market

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Electric Bus Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Fuel Category

- 5.1.1. BEV

- 5.1.2. FCEV

- 5.1.3. HEV

- 5.1.4. PHEV

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. South America

- 5.2.3. Europe

- 5.2.4. Middle East & Africa

- 5.2.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Fuel Category

- 6. North America Electric Bus Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Fuel Category

- 6.1.1. BEV

- 6.1.2. FCEV

- 6.1.3. HEV

- 6.1.4. PHEV

- 6.1. Market Analysis, Insights and Forecast - by Fuel Category

- 7. South America Electric Bus Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Fuel Category

- 7.1.1. BEV

- 7.1.2. FCEV

- 7.1.3. HEV

- 7.1.4. PHEV

- 7.1. Market Analysis, Insights and Forecast - by Fuel Category

- 8. Europe Electric Bus Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Fuel Category

- 8.1.1. BEV

- 8.1.2. FCEV

- 8.1.3. HEV

- 8.1.4. PHEV

- 8.1. Market Analysis, Insights and Forecast - by Fuel Category

- 9. Middle East & Africa Electric Bus Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Fuel Category

- 9.1.1. BEV

- 9.1.2. FCEV

- 9.1.3. HEV

- 9.1.4. PHEV

- 9.1. Market Analysis, Insights and Forecast - by Fuel Category

- 10. Asia Pacific Electric Bus Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Fuel Category

- 10.1.1. BEV

- 10.1.2. FCEV

- 10.1.3. HEV

- 10.1.4. PHEV

- 10.1. Market Analysis, Insights and Forecast - by Fuel Category

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Ashok Leyland Limited

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Zhengzhou Yutong Bus Co Ltd

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Chongqing Changan Automobile Company Limited

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Anhui Ankai Automobile Co Ltd

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Proterra INC

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Tata Motors Limited

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Daimler Truck Holding AG

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Volvo Group

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Zhejiang Geely Holding Group Co Ltd

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 CRRC Electric Vehicle Co Ltd

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 NFI Group Inc

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 King Long United Automotive Industry Co Ltd

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Byd Auto Industry Company Limited

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Zhongtong Bus Holding Co Ltd

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Chery Automobile Co Ltd

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.1 Ashok Leyland Limited

List of Figures

- Figure 1: Global Electric Bus Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Electric Bus Industry Revenue (Million), by Fuel Category 2024 & 2032

- Figure 3: North America Electric Bus Industry Revenue Share (%), by Fuel Category 2024 & 2032

- Figure 4: North America Electric Bus Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: North America Electric Bus Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: South America Electric Bus Industry Revenue (Million), by Fuel Category 2024 & 2032

- Figure 7: South America Electric Bus Industry Revenue Share (%), by Fuel Category 2024 & 2032

- Figure 8: South America Electric Bus Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: South America Electric Bus Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: Europe Electric Bus Industry Revenue (Million), by Fuel Category 2024 & 2032

- Figure 11: Europe Electric Bus Industry Revenue Share (%), by Fuel Category 2024 & 2032

- Figure 12: Europe Electric Bus Industry Revenue (Million), by Country 2024 & 2032

- Figure 13: Europe Electric Bus Industry Revenue Share (%), by Country 2024 & 2032

- Figure 14: Middle East & Africa Electric Bus Industry Revenue (Million), by Fuel Category 2024 & 2032

- Figure 15: Middle East & Africa Electric Bus Industry Revenue Share (%), by Fuel Category 2024 & 2032

- Figure 16: Middle East & Africa Electric Bus Industry Revenue (Million), by Country 2024 & 2032

- Figure 17: Middle East & Africa Electric Bus Industry Revenue Share (%), by Country 2024 & 2032

- Figure 18: Asia Pacific Electric Bus Industry Revenue (Million), by Fuel Category 2024 & 2032

- Figure 19: Asia Pacific Electric Bus Industry Revenue Share (%), by Fuel Category 2024 & 2032

- Figure 20: Asia Pacific Electric Bus Industry Revenue (Million), by Country 2024 & 2032

- Figure 21: Asia Pacific Electric Bus Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Electric Bus Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Electric Bus Industry Revenue Million Forecast, by Fuel Category 2019 & 2032

- Table 3: Global Electric Bus Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 4: Global Electric Bus Industry Revenue Million Forecast, by Fuel Category 2019 & 2032

- Table 5: Global Electric Bus Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: United States Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Canada Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Mexico Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Global Electric Bus Industry Revenue Million Forecast, by Fuel Category 2019 & 2032

- Table 10: Global Electric Bus Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 11: Brazil Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Argentina Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Rest of South America Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Global Electric Bus Industry Revenue Million Forecast, by Fuel Category 2019 & 2032

- Table 15: Global Electric Bus Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: United Kingdom Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Germany Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: France Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Italy Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Spain Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Russia Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Benelux Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Nordics Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Rest of Europe Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Global Electric Bus Industry Revenue Million Forecast, by Fuel Category 2019 & 2032

- Table 26: Global Electric Bus Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 27: Turkey Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Israel Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: GCC Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: North Africa Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 31: South Africa Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 32: Rest of Middle East & Africa Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 33: Global Electric Bus Industry Revenue Million Forecast, by Fuel Category 2019 & 2032

- Table 34: Global Electric Bus Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 35: China Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: India Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 37: Japan Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: South Korea Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 39: ASEAN Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 40: Oceania Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 41: Rest of Asia Pacific Electric Bus Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Electric Bus Industry?

The projected CAGR is approximately > 20.00%.

2. Which companies are prominent players in the Electric Bus Industry?

Key companies in the market include Ashok Leyland Limited, Zhengzhou Yutong Bus Co Ltd, Chongqing Changan Automobile Company Limited, Anhui Ankai Automobile Co Ltd, Proterra INC, Tata Motors Limited, Daimler Truck Holding AG, Volvo Group, Zhejiang Geely Holding Group Co Ltd, CRRC Electric Vehicle Co Ltd, NFI Group Inc, King Long United Automotive Industry Co Ltd, Byd Auto Industry Company Limited, Zhongtong Bus Holding Co Ltd, Chery Automobile Co Ltd.

3. What are the main segments of the Electric Bus Industry?

The market segments include Fuel Category.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Travel and Tourism Industry is Driving the Car Rental Market.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Increasing Popularity of Ride-Sharing Services Pose Challenges for the Conventional Car Rental Market.

8. Can you provide examples of recent developments in the market?

December 2023: Proterra announced its new EV battery factory in South Carolina as demand for commercial electric vehicles increased.November 2023: Switch Mobilty partners with JSW for electric buses for employee transportation in India.September 2023: Daimler Buses launched the next generation Setra TopClass and ComfortClass touring coaches that meet the highest standards of safety, economy, and flexibility.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Electric Bus Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Electric Bus Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Electric Bus Industry?

To stay informed about further developments, trends, and reports in the Electric Bus Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence