Key Insights

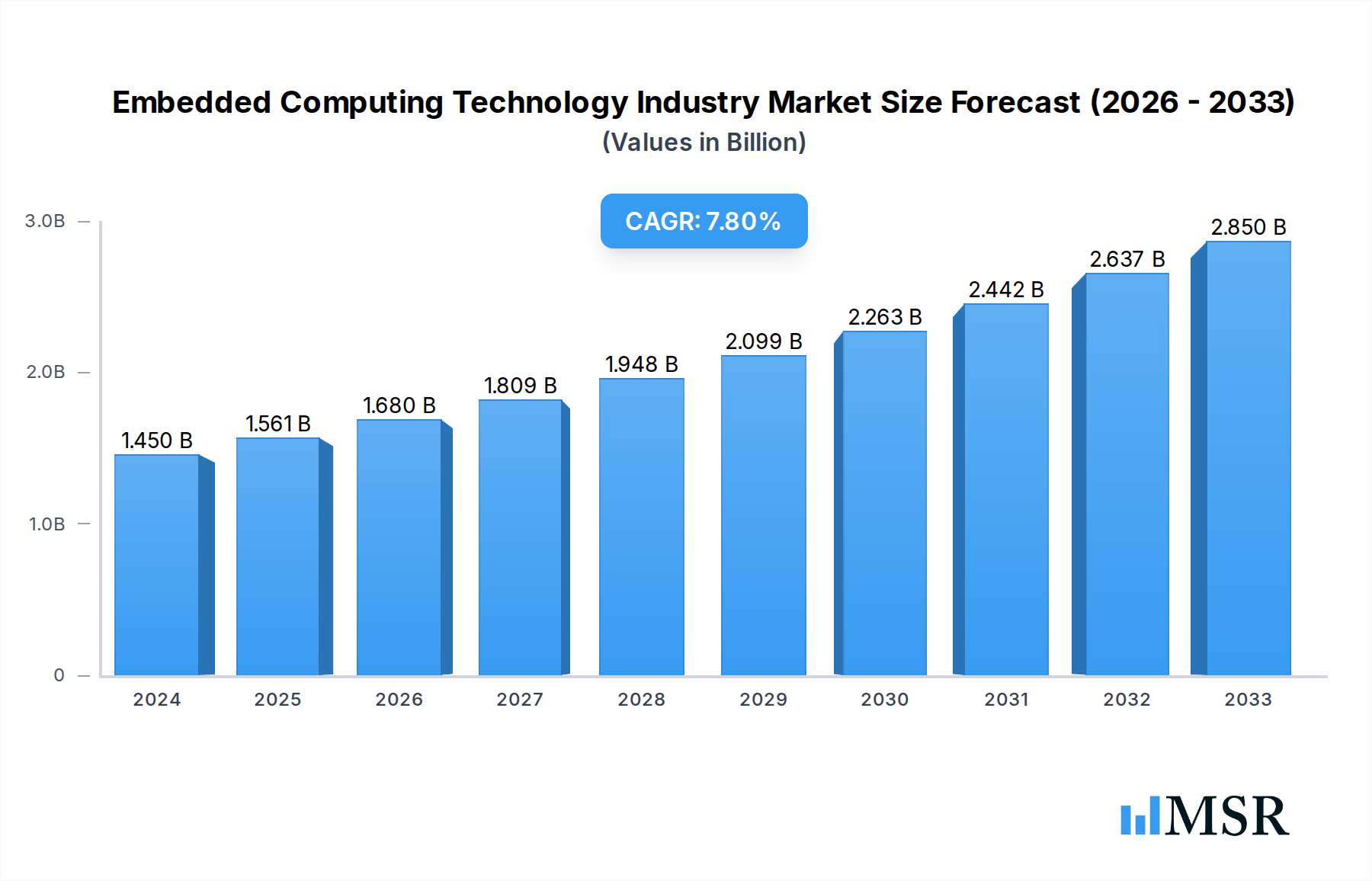

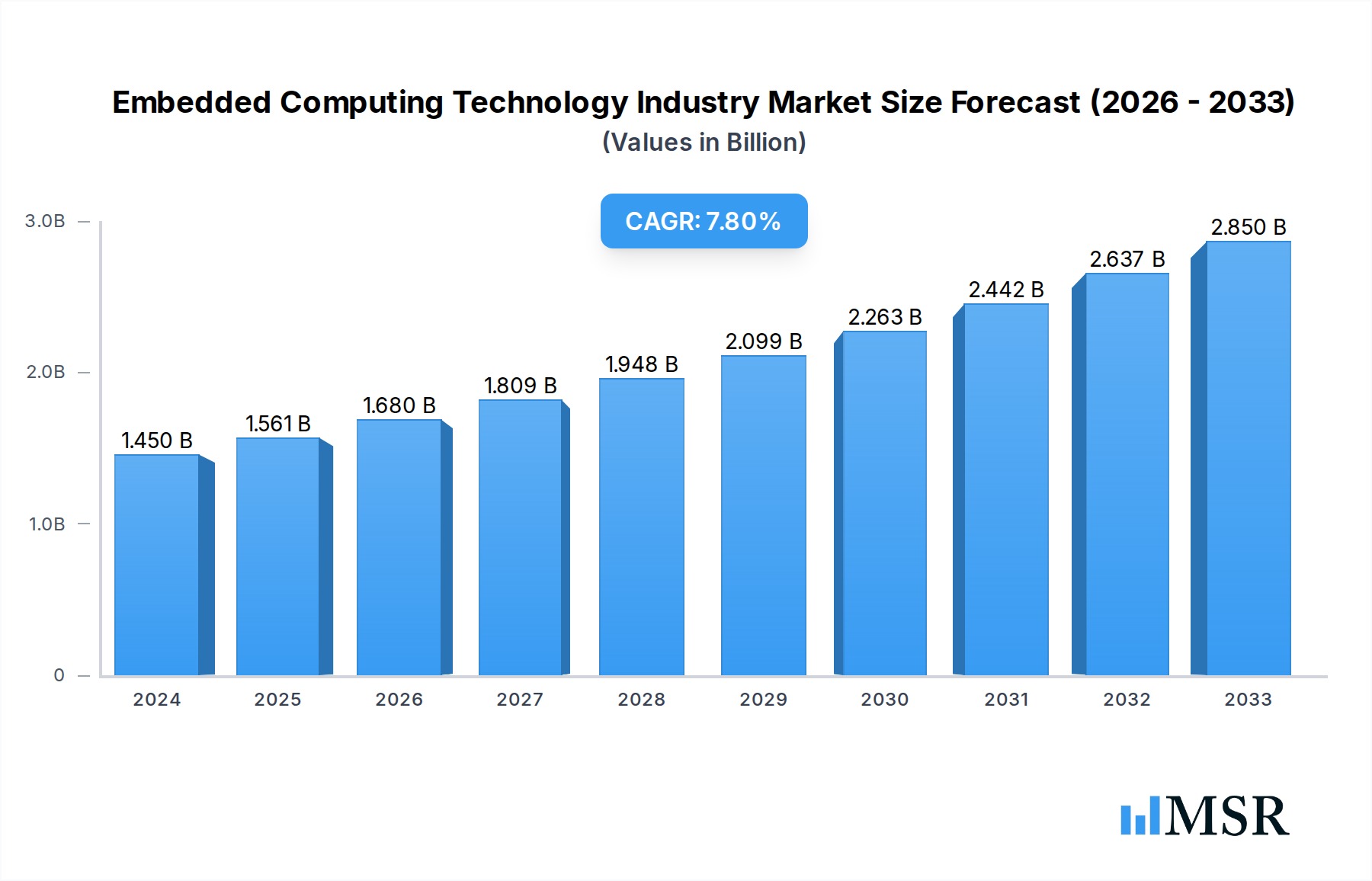

The Embedded Computing Technology Industry is poised for robust expansion, projected to reach a significant $1.45 billion valuation in 2024, with an impressive Compound Annual Growth Rate (CAGR) of 7.68% anticipated to drive its trajectory through 2033. This growth is primarily fueled by the escalating demand for smarter, more connected devices across a multitude of sectors. Key drivers include the pervasive adoption of Industrial IoT (IIoT) and the increasing complexity of automation solutions in manufacturing, where embedded systems are the backbone of operational efficiency and control. The automotive sector is another major contributor, with the proliferation of advanced driver-assistance systems (ADAS), infotainment, and the ongoing transition towards electric and autonomous vehicles necessitating sophisticated embedded computing capabilities. Furthermore, the burgeoning healthcare industry, with its growing reliance on real-time patient monitoring, diagnostic equipment, and telemedicine, is significantly boosting market demand. Consumer electronics, smart home devices, and retail solutions are also increasingly integrating advanced embedded systems to enhance user experience and streamline operations.

Embedded Computing Technology Industry Market Size (In Billion)

Despite this positive outlook, the market faces certain restraints that could temper growth. The increasing complexity and miniaturization of embedded systems can lead to higher manufacturing costs and longer development cycles. Additionally, the ongoing global semiconductor shortages, though showing signs of easing, can still pose challenges for supply chain stability and component availability, impacting production timelines and costs. The competitive landscape is characterized by the presence of both established technology giants and specialized embedded computing providers, fostering innovation but also intensifying pricing pressures. Emerging trends, such as the rise of edge computing, which brings processing closer to the data source, and the integration of artificial intelligence and machine learning directly into embedded devices, are set to revolutionize the industry by enabling faster decision-making and more localized intelligence. The market is segmented into Hardware (including Industrial PCs, HMIs, Edge Servers, and other specialized hardware), Software, and various End User segments like Automotive, Industrial Automation, Healthcare, Retail, and Consumer and Smart Home.

Embedded Computing Technology Industry Company Market Share

Unlock critical insights into the dynamic Embedded Computing Technology Industry, a rapidly expanding sector revolutionizing industries from Automotive to Industrial Automation and Healthcare. This in-depth report, spanning the Historical Period (2019–2024) and the Forecast Period (2025–2033) with a Base Year of 2025, delivers actionable intelligence for stakeholders seeking to capitalize on this multi-billion dollar market. Dive deep into market concentration, growth drivers, emerging trends, key segments, and leading players shaping the future of embedded systems.

Embedded Computing Technology Industry Market Concentration & Dynamics

The Embedded Computing Technology Industry exhibits a moderate to high market concentration, driven by the significant investments required for advanced R&D and manufacturing. Major players like Intel Corporation, Qualcomm Incorporated, and Microsoft Corporation hold substantial market share, influencing innovation and pricing dynamics. The innovation ecosystem is robust, fueled by collaborations between hardware providers such as Axiomtek Co Ltd, Congatec AG, and Super Micro Computer Inc, and software giants like Microsoft Corporation. Regulatory frameworks, particularly concerning data security and safety-critical applications in Automotive and Healthcare, are increasingly stringent, impacting product development and market entry. The threat of substitute products is low, given the specialized nature of embedded solutions, but advancements in cloud computing and IoT platforms continuously evolve the competitive landscape. End-user trends are shifting towards higher performance, lower power consumption, and enhanced connectivity, pushing for more sophisticated Edge Servers and intelligent Hardware solutions. Merger and Acquisition (M&A) activities are strategically focused on acquiring specialized technologies or expanding market reach. Historically, there have been over 50 significant M&A deals valued in the billions across the Embedded Computing Technology Industry from 2019 to 2024, indicating active consolidation and strategic maneuvering.

Embedded Computing Technology Industry Industry Insights & Trends

The Embedded Computing Technology Industry is projected to experience robust growth, with an estimated market size of over $150 billion in the Base Year of 2025, and is forecast to reach over $300 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 7.5% during the Forecast Period (2025–2033). This significant expansion is primarily fueled by the relentless demand for connected devices, the proliferation of the Internet of Things (IoT), and the accelerating adoption of Artificial Intelligence (AI) and Machine Learning (ML) at the edge. Technological disruptions are at the forefront, with advancements in processors, memory technologies, and specialized accelerators enabling more powerful and efficient embedded systems. The increasing complexity of applications in Industrial Automation, requiring real-time processing and robust connectivity, is a major market driver. Furthermore, the growth of smart cities, connected vehicles, and advanced medical devices underscores the pervasive influence of embedded computing. Evolving consumer behaviors, characterized by a demand for seamless user experiences and personalized services, are also pushing the boundaries of embedded intelligence. The rise of edge computing, enabling data processing closer to the source, is a key trend that significantly bolsters the market for Edge Servers and sophisticated Hardware components. Software advancements, including real-time operating systems (RTOS) and embedded AI frameworks, are crucial for unlocking the full potential of these hardware platforms, further driving market growth. The integration of 5G technology is poised to accelerate the adoption of embedded systems in real-time applications, creating unprecedented opportunities across various sectors.

Key Markets & Segments Leading Embedded Computing Technology Industry

The Embedded Computing Technology Industry is experiencing significant growth across multiple segments and end-user industries.

Component Type Dominance:

- Hardware is the dominant segment, projected to account for over 70% of the market share by 2025. This includes critical sub-segments:

- Industrial PC (IPC): Driven by the insatiable demand for robust and reliable computing in manufacturing, logistics, and automation, IPCs represent a substantial portion of the Hardware market. Economic growth and the push for Industry 4.0 initiatives worldwide are key drivers.

- HMI (Human-Machine Interface): Essential for intuitive interaction with complex machinery and systems, HMIs are experiencing strong demand, particularly in Industrial Automation and Retail. The need for user-friendly interfaces in diverse environments fuels this growth.

- Edge Servers: This rapidly expanding sub-segment is a direct consequence of the IoT revolution and the need for localized data processing and analytics. The increasing deployment of IoT devices across all end-user sectors is the primary driver.

- Other Hardware: Encompasses specialized embedded modules, processors, and components crucial for various niche applications, contributing to overall hardware dominance.

- Software: While smaller in market share compared to hardware, the embedded software segment is crucial for enabling functionality and is experiencing high growth rates. Embedded operating systems, middleware, and application software are vital for system performance and capabilities.

- Hardware is the dominant segment, projected to account for over 70% of the market share by 2025. This includes critical sub-segments:

End User Dominance:

- Industrial Automation: This sector consistently leads the Embedded Computing Technology Industry, driven by the global push for automation, efficiency, and smart manufacturing (Industry 4.0). Investments in robotics, AI-powered manufacturing, and predictive maintenance are significant growth accelerators. Economic growth, particularly in emerging economies investing heavily in industrial infrastructure, underpins this dominance.

- Automotive: The increasing integration of advanced driver-assistance systems (ADAS), in-car infotainment, and the impending rise of autonomous vehicles are making the automotive sector a powerhouse for embedded computing. The stringent safety and performance requirements in this sector demand highly sophisticated embedded solutions.

- Healthcare: The growing adoption of connected medical devices, remote patient monitoring, diagnostic imaging, and robotic surgery is propelling the healthcare segment. The need for reliable, secure, and high-performance embedded systems in critical medical applications is paramount.

- Consumer and Smart Home: The proliferation of smart home devices, wearables, and connected consumer electronics is a substantial contributor to market growth. The increasing consumer demand for convenience, energy efficiency, and integrated living experiences fuels this segment.

- Retail: Embedded systems are crucial for point-of-sale (POS) systems, inventory management, digital signage, and customer analytics, making retail a significant end-user market. The drive for enhanced customer experiences and operational efficiency fuels adoption.

- Other End Users: Includes segments like aerospace, defense, telecommunications, and energy, each with unique and growing demands for specialized embedded computing solutions.

Embedded Computing Technology Industry Product Developments

Product innovations in the Embedded Computing Technology Industry are characterized by an increased focus on performance, power efficiency, and connectivity. Companies are developing highly integrated System-on-Modules (SoMs) and compact industrial PCs capable of handling complex AI workloads at the edge. Advancements in edge AI hardware, including specialized neural processing units (NPUs) and GPUs, are enabling real-time inference for applications in vision systems, predictive maintenance, and autonomous navigation. The integration of secure boot mechanisms and hardware-based encryption is becoming standard to address growing cybersecurity concerns. Furthermore, the development of ruggedized and fanless embedded solutions designed to withstand harsh environmental conditions in Industrial Automation and outdoor applications is a key trend.

Challenges in the Embedded Computing Technology Industry Market

The Embedded Computing Technology Industry faces several significant challenges. Supply chain disruptions, particularly for critical semiconductor components, continue to pose a considerable risk, impacting production timelines and costs. The increasing complexity of embedded systems and the rapid pace of technological evolution require continuous and substantial investment in research and development, creating high entry barriers. Stringent regulatory compliance, especially in safety-critical sectors like Automotive and Healthcare, adds complexity and cost to product development and certification. Furthermore, the growing threat landscape for cybersecurity necessitates robust and continuously updated security measures, demanding significant resources. The competitive pressure from established players and emerging innovators also necessitates agile strategies and constant innovation.

Forces Driving Embedded Computing Technology Industry Growth

Several powerful forces are driving the exponential growth of the Embedded Computing Technology Industry. The pervasive adoption of the Internet of Things (IoT) across all sectors is a primary catalyst, creating an insatiable demand for connected devices with embedded intelligence. The ongoing digital transformation and the drive towards Industry 4.0 in manufacturing are necessitating more sophisticated automation and control systems. Advancements in Artificial Intelligence (AI) and Machine Learning (ML) are enabling embedded systems to perform complex data analysis and decision-making at the edge, unlocking new functionalities. The increasing demand for real-time data processing and reduced latency in applications like autonomous driving and smart grids is also a significant growth driver. Furthermore, government initiatives and investments in smart city development and infrastructure modernization are creating substantial market opportunities.

Challenges in the Embedded Computing Technology Industry Market

Long-term growth catalysts for the Embedded Computing Technology Industry are rooted in continued innovation and strategic market expansion. The ongoing miniaturization of components and the development of more power-efficient processors will enable a wider range of embedded applications. Breakthroughs in AI and neuromorphic computing will lead to even more intelligent and adaptive embedded systems. Strategic partnerships between hardware manufacturers, software developers, and system integrators will foster the creation of comprehensive solutions. Furthermore, the expansion of embedded computing into new and emerging markets, such as sustainable energy management and advanced agriculture, will provide sustained growth opportunities.

Emerging Opportunities in Embedded Computing Technology Industry

Emerging opportunities in the Embedded Computing Technology Industry are abundant and span across various technological frontiers. The continued expansion of 5G networks will unlock the full potential of real-time embedded applications, including industrial robotics, connected vehicles, and augmented reality. The growing demand for edge AI solutions for real-time analytics and decision-making in sectors like retail and smart cities presents a massive opportunity. The development of specialized embedded systems for quantum computing research and applications is also on the horizon. Furthermore, the increasing focus on sustainability and energy efficiency will drive the demand for intelligent embedded systems in renewable energy management, smart grids, and electric vehicle charging infrastructure. The need for robust cybersecurity solutions tailored for embedded devices will also create specialized market niches.

Leading Players in the Embedded Computing Technology Industry Sector

- SMART Embedded Computing

- IBM Corporation

- Interelectronix

- Axiomtek Co Ltd

- Congatec AG

- Super Micro Computer Inc

- Microsoft Corporation

- Dell Corporation

- Fujitsu Limited

- Qualcomm Incorporated

- Renesas Electronics Corporation

- Texas Instruments Incorporated

- Intel Corporation

Key Milestones in Embedded Computing Technology Industry Industry

- 2019: Significant advancements in ARM-based processors offering higher performance and power efficiency, impacting mobile and IoT embedded systems.

- 2020: Increased adoption of AI accelerators in embedded platforms, enabling on-device machine learning for various applications.

- 2021: Growing emphasis on supply chain resilience and diversification due to global component shortages, leading to increased strategic partnerships.

- 2022: Expansion of edge computing solutions with more powerful and compact edge servers and gateways.

- 2023: Enhanced security features and adoption of hardware-based security modules in embedded devices to combat rising cyber threats.

- 2024: Continued integration of 5G connectivity into embedded systems, enabling low-latency, high-bandwidth applications.

Strategic Outlook for Embedded Computing Technology Industry Market

The strategic outlook for the Embedded Computing Technology Industry market is exceptionally positive, fueled by sustained innovation and expanding application landscapes. The market will witness a continued convergence of hardware, software, and AI capabilities, leading to the development of increasingly intelligent and autonomous embedded systems. Companies that can effectively address the evolving demands for edge computing, cybersecurity, and power efficiency will be best positioned for success. Strategic investments in R&D, focus on vertical market specialization, and the formation of strong ecosystem partnerships will be crucial for capturing market share and driving future growth. The global push towards digital transformation and smart technologies across all industries ensures a robust and expanding future for embedded computing.

Embedded Computing Technology Industry Segmentation

-

1. Component Type

-

1.1. Hardware

- 1.1.1. Industrial PC

- 1.1.2. HMI

- 1.1.3. Edge Servers

- 1.1.4. Other Hardware

- 1.2. Software

-

1.1. Hardware

-

2. End User

- 2.1. Automotive

- 2.2. Industrial Automation

- 2.3. Healthcare

- 2.4. Retail

- 2.5. Consumer and Smart Home

- 2.6. Other End Users

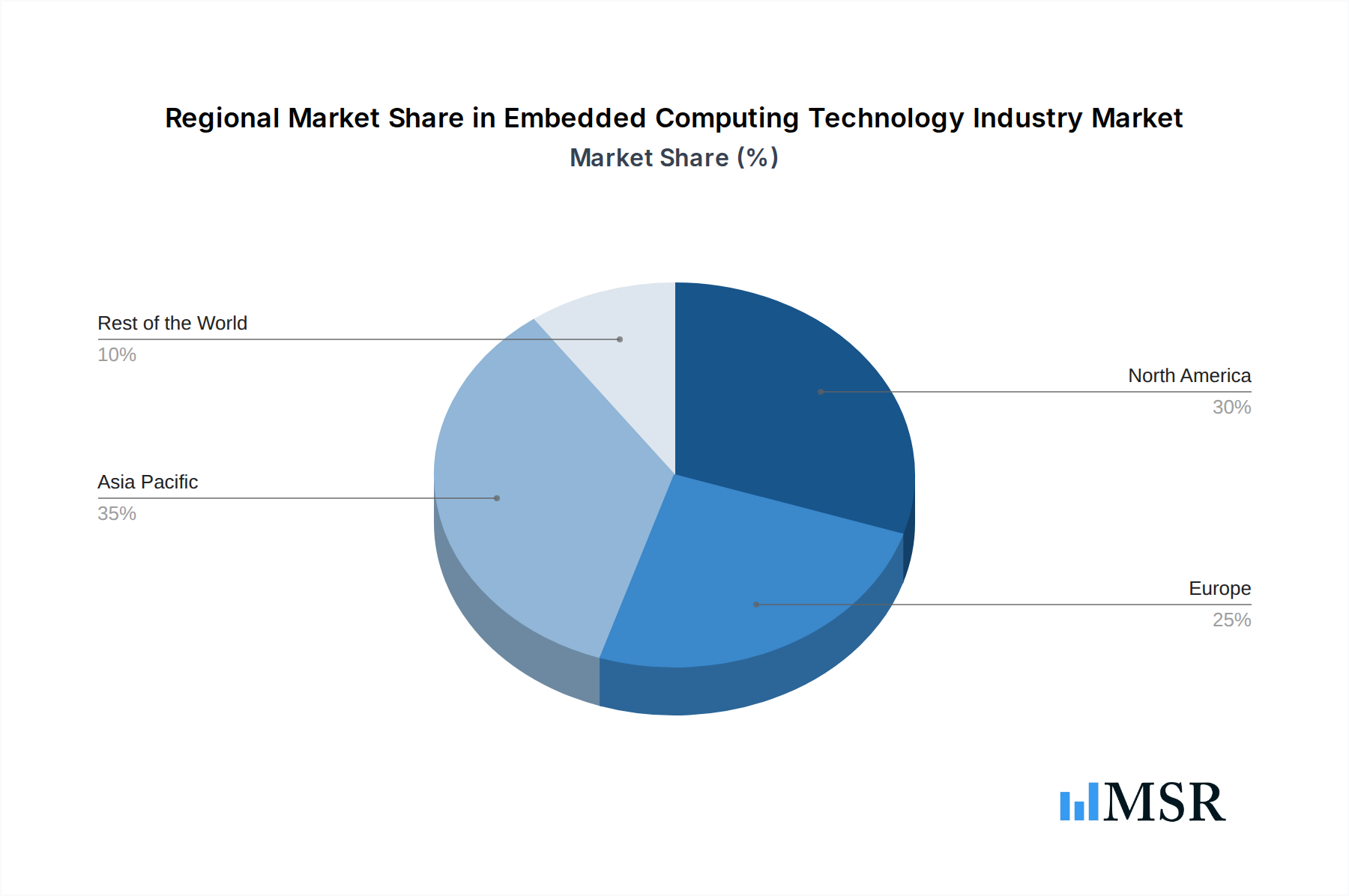

Embedded Computing Technology Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Rest of the World

Embedded Computing Technology Industry Regional Market Share

Geographic Coverage of Embedded Computing Technology Industry

Embedded Computing Technology Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.68% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Component Type

- 5.1.1. Hardware

- 5.1.1.1. Industrial PC

- 5.1.1.2. HMI

- 5.1.1.3. Edge Servers

- 5.1.1.4. Other Hardware

- 5.1.2. Software

- 5.1.1. Hardware

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Automotive

- 5.2.2. Industrial Automation

- 5.2.3. Healthcare

- 5.2.4. Retail

- 5.2.5. Consumer and Smart Home

- 5.2.6. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Component Type

- 6. Global Embedded Computing Technology Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Component Type

- 6.1.1. Hardware

- 6.1.1.1. Industrial PC

- 6.1.1.2. HMI

- 6.1.1.3. Edge Servers

- 6.1.1.4. Other Hardware

- 6.1.2. Software

- 6.1.1. Hardware

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Automotive

- 6.2.2. Industrial Automation

- 6.2.3. Healthcare

- 6.2.4. Retail

- 6.2.5. Consumer and Smart Home

- 6.2.6. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Component Type

- 7. North America Embedded Computing Technology Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Component Type

- 7.1.1. Hardware

- 7.1.1.1. Industrial PC

- 7.1.1.2. HMI

- 7.1.1.3. Edge Servers

- 7.1.1.4. Other Hardware

- 7.1.2. Software

- 7.1.1. Hardware

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Automotive

- 7.2.2. Industrial Automation

- 7.2.3. Healthcare

- 7.2.4. Retail

- 7.2.5. Consumer and Smart Home

- 7.2.6. Other End Users

- 7.1. Market Analysis, Insights and Forecast - by Component Type

- 8. Europe Embedded Computing Technology Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Component Type

- 8.1.1. Hardware

- 8.1.1.1. Industrial PC

- 8.1.1.2. HMI

- 8.1.1.3. Edge Servers

- 8.1.1.4. Other Hardware

- 8.1.2. Software

- 8.1.1. Hardware

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Automotive

- 8.2.2. Industrial Automation

- 8.2.3. Healthcare

- 8.2.4. Retail

- 8.2.5. Consumer and Smart Home

- 8.2.6. Other End Users

- 8.1. Market Analysis, Insights and Forecast - by Component Type

- 9. Asia Pacific Embedded Computing Technology Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Component Type

- 9.1.1. Hardware

- 9.1.1.1. Industrial PC

- 9.1.1.2. HMI

- 9.1.1.3. Edge Servers

- 9.1.1.4. Other Hardware

- 9.1.2. Software

- 9.1.1. Hardware

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Automotive

- 9.2.2. Industrial Automation

- 9.2.3. Healthcare

- 9.2.4. Retail

- 9.2.5. Consumer and Smart Home

- 9.2.6. Other End Users

- 9.1. Market Analysis, Insights and Forecast - by Component Type

- 10. Rest of the World Embedded Computing Technology Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Component Type

- 10.1.1. Hardware

- 10.1.1.1. Industrial PC

- 10.1.1.2. HMI

- 10.1.1.3. Edge Servers

- 10.1.1.4. Other Hardware

- 10.1.2. Software

- 10.1.1. Hardware

- 10.2. Market Analysis, Insights and Forecast - by End User

- 10.2.1. Automotive

- 10.2.2. Industrial Automation

- 10.2.3. Healthcare

- 10.2.4. Retail

- 10.2.5. Consumer and Smart Home

- 10.2.6. Other End Users

- 10.1. Market Analysis, Insights and Forecast - by Component Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 SMART Embedded Computing

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 IBM Corporation

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Interelectronix

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Axiomtek Co Ltd

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Congatec AG

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Super Micro Computer Inc

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Microsoft Corporation

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Dell Corporation

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Fujitsu Limited

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Qualcomm Incorporated

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 Renesas Electronics Corporation*List Not Exhaustive

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 Texas Instruments Incorporated

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.13 Intel Corporation

- 11.1.13.1. Company Overview

- 11.1.13.2. Products

- 11.1.13.3. Company Financials

- 11.1.13.4. SWOT Analysis

- 11.1.1 SMART Embedded Computing

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Embedded Computing Technology Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Embedded Computing Technology Industry Revenue (billion), by Component Type 2025 & 2033

- Figure 3: North America Embedded Computing Technology Industry Revenue Share (%), by Component Type 2025 & 2033

- Figure 4: North America Embedded Computing Technology Industry Revenue (billion), by End User 2025 & 2033

- Figure 5: North America Embedded Computing Technology Industry Revenue Share (%), by End User 2025 & 2033

- Figure 6: North America Embedded Computing Technology Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Embedded Computing Technology Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Embedded Computing Technology Industry Revenue (billion), by Component Type 2025 & 2033

- Figure 9: Europe Embedded Computing Technology Industry Revenue Share (%), by Component Type 2025 & 2033

- Figure 10: Europe Embedded Computing Technology Industry Revenue (billion), by End User 2025 & 2033

- Figure 11: Europe Embedded Computing Technology Industry Revenue Share (%), by End User 2025 & 2033

- Figure 12: Europe Embedded Computing Technology Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Embedded Computing Technology Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Embedded Computing Technology Industry Revenue (billion), by Component Type 2025 & 2033

- Figure 15: Asia Pacific Embedded Computing Technology Industry Revenue Share (%), by Component Type 2025 & 2033

- Figure 16: Asia Pacific Embedded Computing Technology Industry Revenue (billion), by End User 2025 & 2033

- Figure 17: Asia Pacific Embedded Computing Technology Industry Revenue Share (%), by End User 2025 & 2033

- Figure 18: Asia Pacific Embedded Computing Technology Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Embedded Computing Technology Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Rest of the World Embedded Computing Technology Industry Revenue (billion), by Component Type 2025 & 2033

- Figure 21: Rest of the World Embedded Computing Technology Industry Revenue Share (%), by Component Type 2025 & 2033

- Figure 22: Rest of the World Embedded Computing Technology Industry Revenue (billion), by End User 2025 & 2033

- Figure 23: Rest of the World Embedded Computing Technology Industry Revenue Share (%), by End User 2025 & 2033

- Figure 24: Rest of the World Embedded Computing Technology Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Rest of the World Embedded Computing Technology Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Embedded Computing Technology Industry Revenue billion Forecast, by Component Type 2020 & 2033

- Table 2: Global Embedded Computing Technology Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 3: Global Embedded Computing Technology Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Embedded Computing Technology Industry Revenue billion Forecast, by Component Type 2020 & 2033

- Table 5: Global Embedded Computing Technology Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 6: Global Embedded Computing Technology Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Embedded Computing Technology Industry Revenue billion Forecast, by Component Type 2020 & 2033

- Table 8: Global Embedded Computing Technology Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 9: Global Embedded Computing Technology Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Global Embedded Computing Technology Industry Revenue billion Forecast, by Component Type 2020 & 2033

- Table 11: Global Embedded Computing Technology Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 12: Global Embedded Computing Technology Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Embedded Computing Technology Industry Revenue billion Forecast, by Component Type 2020 & 2033

- Table 14: Global Embedded Computing Technology Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 15: Global Embedded Computing Technology Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Embedded Computing Technology Industry?

The projected CAGR is approximately 7.68%.

2. Which companies are prominent players in the Embedded Computing Technology Industry?

Key companies in the market include SMART Embedded Computing, IBM Corporation, Interelectronix, Axiomtek Co Ltd, Congatec AG, Super Micro Computer Inc, Microsoft Corporation, Dell Corporation, Fujitsu Limited, Qualcomm Incorporated, Renesas Electronics Corporation*List Not Exhaustive, Texas Instruments Incorporated, Intel Corporation.

3. What are the main segments of the Embedded Computing Technology Industry?

The market segments include Component Type, End User .

4. Can you provide details about the market size?

The market size is estimated to be USD 1.45 billion as of 2022.

5. What are some drivers contributing to market growth?

; Increasing Investments in Industrial Automation; Rising Demand in Consumer Electronics due to Size and Power Constraints.

6. What are the notable trends driving market growth?

Consumer Electronics to Witness Significant Growth.

7. Are there any restraints impacting market growth?

Low Skillset in Emerging Economies.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Embedded Computing Technology Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Embedded Computing Technology Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Embedded Computing Technology Industry?

To stay informed about further developments, trends, and reports in the Embedded Computing Technology Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence