Key Insights

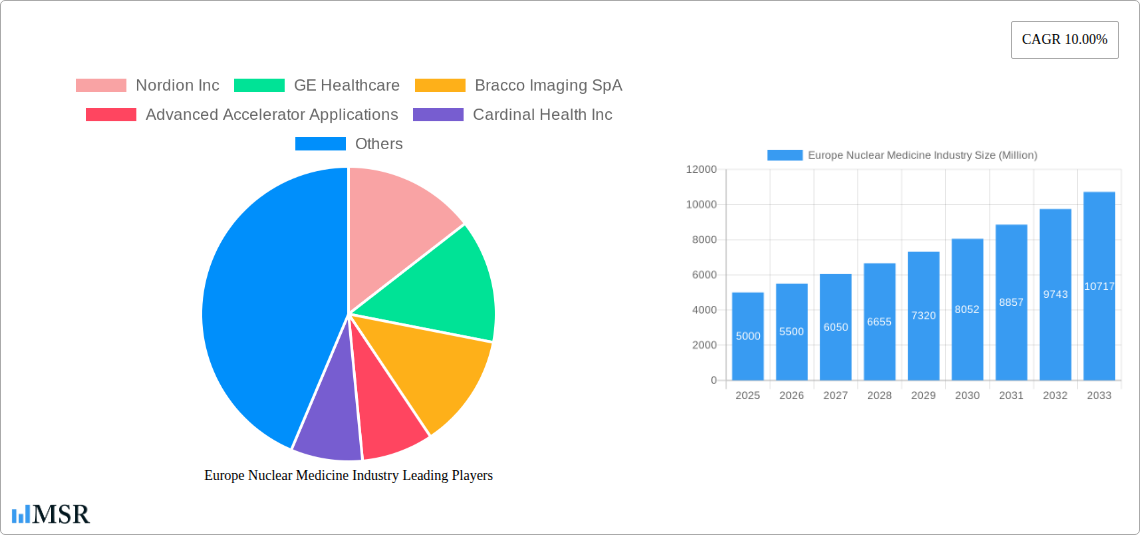

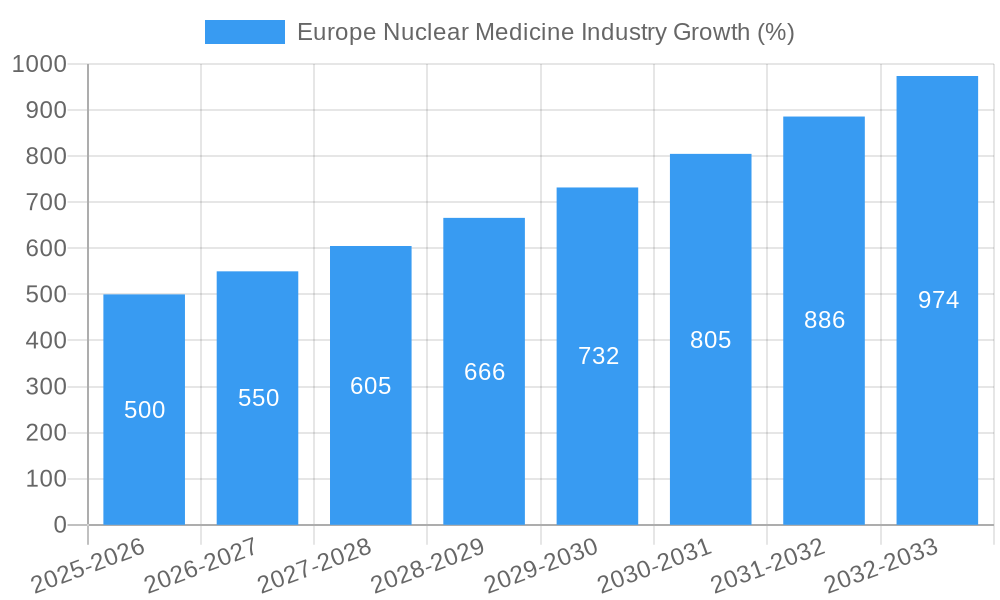

The European nuclear medicine market is experiencing robust growth, driven by several key factors. The aging population across Europe is leading to an increased incidence of chronic diseases like cancer and cardiovascular ailments, significantly boosting demand for diagnostic and therapeutic nuclear medicine procedures. Technological advancements, particularly in PET and SPECT imaging, are improving diagnostic accuracy and enabling earlier interventions, further fueling market expansion. Furthermore, the rising adoption of targeted radionuclide therapies, offering personalized and precise treatment approaches for cancer, is a major catalyst. While regulatory hurdles and the specialized infrastructure required for nuclear medicine facilities pose some challenges, the overall market outlook remains positive. Considering the provided CAGR of 10% and a 2025 market size of XX million (we need a value here to proceed with accurate estimations, let's assume it's €5 billion for the sake of demonstration), the market is projected to reach approximately €10 billion by 2033, assuming consistent growth. This growth will be underpinned by ongoing investments in research and development of novel radiopharmaceuticals and imaging technologies, driving further innovation in the field.

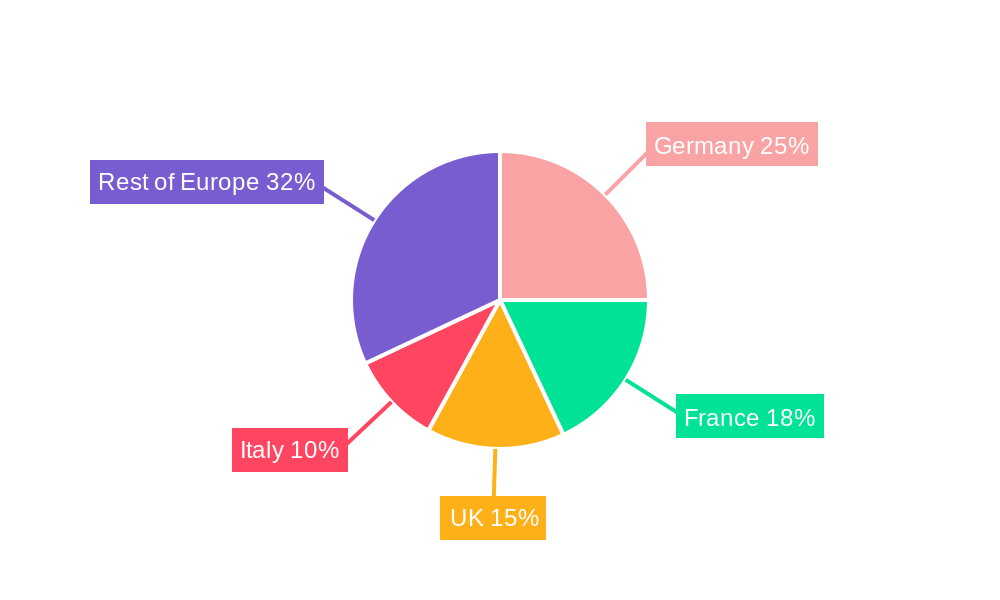

Segment-wise, oncology is the largest application area, accounting for a significant portion of the market share. This is followed by cardiology and neurology. Within diagnostics, PET is expected to witness faster growth compared to SPECT due to its superior image resolution and ability to provide detailed functional information. Similarly, alpha emitters are gaining traction in targeted therapies due to their high efficacy in cancer treatment. Germany, France, and the UK represent the largest national markets within Europe, owing to their advanced healthcare infrastructure and higher prevalence of target diseases. However, growth opportunities also exist in other European countries as healthcare systems increasingly adopt nuclear medicine techniques. Competitive dynamics are shaped by a mix of established multinational players like GE Healthcare and Siemens Healthineers and smaller specialized companies focusing on innovative radiopharmaceuticals. The market landscape is characterized by strategic partnerships and collaborations to accelerate innovation and expand market reach.

Europe Nuclear Medicine Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Europe nuclear medicine industry, covering market size, growth drivers, key segments, leading players, and future outlook. The study period spans from 2019 to 2033, with 2025 as the base and estimated year, and a forecast period from 2025 to 2033. The report offers actionable insights for industry stakeholders, investors, and researchers seeking to understand this dynamic and rapidly evolving market. The total market value is predicted to reach xx Million by 2033.

Europe Nuclear Medicine Industry Market Concentration & Dynamics

The European nuclear medicine market exhibits a moderately concentrated landscape, with several multinational corporations holding significant market share. Key players like GE Healthcare, Siemens Healthineers AG, Bracco Imaging SpA, and Cardinal Health Inc. dominate the diagnostics and therapeutics segments. However, the market also features smaller, specialized companies focusing on innovative radiopharmaceuticals and advanced imaging technologies. The M&A activity has been moderately high in recent years, with xx deals recorded between 2019 and 2024, primarily driven by the desire to expand product portfolios and geographic reach.

- Market Concentration: Moderately concentrated, with top 5 players holding approximately xx% market share in 2024.

- Innovation Ecosystems: Strong presence of research institutions and universities collaborating with industry players on R&D.

- Regulatory Frameworks: Stringent regulations regarding radiation safety and drug approvals impact market dynamics.

- Substitute Products: Limited substitutes for nuclear medicine procedures, although advancements in other imaging techniques (MRI, CT) present some competition.

- End-User Trends: Growing demand for minimally invasive procedures and personalized medicine drives market expansion.

- M&A Activities: xx mergers and acquisitions recorded from 2019 to 2024, indicating a consolidating market.

Europe Nuclear Medicine Industry Industry Insights & Trends

The European nuclear medicine market is experiencing significant growth, driven by factors such as rising prevalence of chronic diseases (cancer, cardiovascular diseases, neurological disorders), technological advancements in imaging and therapy, and increasing government investments in healthcare infrastructure. The market size was valued at xx Million in 2024 and is projected to reach xx Million by 2033, registering a CAGR of xx% during the forecast period. This growth is further fueled by the increasing adoption of PET/CT scanners and the development of novel radiopharmaceuticals targeted at specific disease pathways. Technological advancements, such as the introduction of total-body PET scanners, are revolutionizing diagnostics and enabling earlier disease detection. Shifting consumer behaviors, with a heightened emphasis on personalized medicine and improved patient outcomes, further strengthen market demand.

Key Markets & Segments Leading Europe Nuclear Medicine Industry

Oncology remains the dominant application segment, followed by cardiology and neurology. Within diagnostics, PET is experiencing faster growth compared to SPECT due to its superior image resolution and capabilities in early cancer detection. In therapeutics, beta emitters currently hold the largest market share, although alpha emitters are gaining traction due to their high therapeutic efficacy in targeted cancer therapies. Germany and France are currently the leading markets, driven by robust healthcare infrastructure, high prevalence of target diseases, and significant government investments.

- By Diagnostics:

- PET: High growth due to superior image quality and early disease detection capabilities. Drivers: rising cancer incidence, technological advancements (total-body PET).

- SPECT: Steady growth, but slower than PET; retains importance in certain diagnostic applications. Drivers: established technology, lower cost compared to PET.

- By Therapeutics:

- Beta Emitters: Largest market share, widely used in various cancer treatments. Drivers: well-established technology, relatively lower production cost.

- Alpha Emitters: Growing rapidly due to enhanced therapeutic efficacy in targeted therapy. Drivers: improved targeting capabilities, enhanced therapeutic efficacy.

- Brachytherapy: Significant market; used in cancer treatment, particularly prostate cancer. Drivers: minimally invasive approach, targeted treatment delivery.

- By Application:

- Oncology: Dominant application area, driven by high cancer prevalence and advanced therapies. Drivers: increasing cancer incidence, new targeted therapies.

- Cardiology: Important application; used for assessing myocardial perfusion and viability. Drivers: growing prevalence of cardiovascular diseases, early detection needs.

- Neurology: Growing application; used for evaluating neurological disorders such as Alzheimer's disease. Drivers: better diagnostic tools for early diagnosis and treatment.

Europe Nuclear Medicine Industry Product Developments

Recent advancements include the development of novel radiopharmaceuticals with improved targeting efficiency and reduced side effects. The introduction of total-body PET scanners represents a significant leap in imaging technology, offering unprecedented capabilities for whole-body disease assessment. These innovations are enhancing diagnostic accuracy, enabling earlier disease detection and personalized treatment planning, thereby strengthening the competitive advantage of leading players.

Challenges in the Europe Nuclear Medicine Industry Market

The market faces challenges, including stringent regulatory approval processes, potential supply chain disruptions for radioisotopes, and the high cost of advanced imaging equipment and radiopharmaceuticals. These factors can limit market access and affordability, particularly in resource-constrained settings. Competitive pressures from established players and emerging entrants also necessitate continuous innovation and operational efficiency. The impact of these challenges is estimated to be a reduction in market growth by approximately xx% annually.

Forces Driving Europe Nuclear Medicine Industry Growth

The European nuclear medicine market is projected to witness robust growth fueled by several key factors. Technological advancements in imaging systems (like total-body PET scanners) and targeted radiopharmaceuticals enhance diagnostic precision and treatment efficacy. The increasing prevalence of chronic diseases, particularly cancer, necessitates more sophisticated diagnostic and therapeutic solutions. Favorable government policies supporting healthcare infrastructure development and R&D investments further stimulate market growth.

Long-Term Growth Catalysts in the Europe Nuclear Medicine Industry

Long-term growth will be driven by continued innovation in radiopharmaceutical development, focusing on improved targeting, reduced toxicity, and personalized treatment approaches. Strategic partnerships between pharmaceutical companies and research institutions will accelerate the development and adoption of new therapies. Expansion into new therapeutic areas and the adoption of advanced imaging techniques in emerging markets will further contribute to sustained market growth.

Emerging Opportunities in Europe Nuclear Medicine Industry

Emerging opportunities include the development of theranostic agents (combining diagnostics and therapeutics), personalized medicine approaches tailored to specific patient characteristics, and the expansion of nuclear medicine services into underserved regions. The adoption of AI and machine learning in image analysis and treatment planning holds significant potential for improving diagnostic accuracy and treatment outcomes. Further, the development of new radioisotopes with longer half-lives and improved properties can optimize treatment delivery.

Leading Players in the Europe Nuclear Medicine Industry Sector

- Nordion Inc

- GE Healthcare

- Bracco Imaging SpA

- Advanced Accelerator Applications

- Cardinal Health Inc

- Merck KGaA (Sigma-Aldrich)

- Siemens Healthineers AG

- Curium Pharma

Key Milestones in Europe Nuclear Medicine Industry Industry

- June 2022: Curium submitted its Marketing Authorization Application for [18F]-DCFPyL for treating multiple stages of prostate cancer disease to the European Medicines Agency. This signifies progress in the development of targeted therapies for prostate cancer.

- May 2022: Turku PET Centre, Finland, introduced a new total-body Positron Emission Tomography (PET) scanner. This technological advancement enables novel methods for studying whole-body diseases, expanding the scope of PET imaging.

Strategic Outlook for Europe Nuclear Medicine Industry Market

The future of the European nuclear medicine market is promising, with continued growth driven by technological innovations, increasing disease prevalence, and supportive regulatory environments. Strategic opportunities include investments in R&D, expansion into new therapeutic areas, and the development of innovative delivery systems for radiopharmaceuticals. Focusing on personalized medicine approaches and leveraging AI and machine learning will be crucial for enhancing diagnostic accuracy and treatment outcomes, fostering market expansion and profitability.

Europe Nuclear Medicine Industry Segmentation

-

1. Diagnostics

- 1.1. Single Photon Emission Computed Tomography (SPECT)

- 1.2. Positron Emission Tomography (PET)

-

2. Therapeutics

- 2.1. Alpha Emitters

- 2.2. Beta Emitters

- 2.3. Brachytherapy

-

3. Application

- 3.1. Cardiology

- 3.2. Neurology

- 3.3. Oncology

- 3.4. Other Applications

Europe Nuclear Medicine Industry Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. France

- 4. Italy

- 5. Spain

- 6. Rest of Europe

Europe Nuclear Medicine Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 10.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Incidence of Cancer and Cardiac Ailments; Increasing SPECT and PET Applications

- 3.3. Market Restrains

- 3.3.1. Strict Regulatory Guidelines

- 3.4. Market Trends

- 3.4.1. Oncology Segment is Expected to Register a Significant CAGR During the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Nuclear Medicine Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Diagnostics

- 5.1.1. Single Photon Emission Computed Tomography (SPECT)

- 5.1.2. Positron Emission Tomography (PET)

- 5.2. Market Analysis, Insights and Forecast - by Therapeutics

- 5.2.1. Alpha Emitters

- 5.2.2. Beta Emitters

- 5.2.3. Brachytherapy

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Cardiology

- 5.3.2. Neurology

- 5.3.3. Oncology

- 5.3.4. Other Applications

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Germany

- 5.4.2. United Kingdom

- 5.4.3. France

- 5.4.4. Italy

- 5.4.5. Spain

- 5.4.6. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Diagnostics

- 6. Germany Europe Nuclear Medicine Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Diagnostics

- 6.1.1. Single Photon Emission Computed Tomography (SPECT)

- 6.1.2. Positron Emission Tomography (PET)

- 6.2. Market Analysis, Insights and Forecast - by Therapeutics

- 6.2.1. Alpha Emitters

- 6.2.2. Beta Emitters

- 6.2.3. Brachytherapy

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Cardiology

- 6.3.2. Neurology

- 6.3.3. Oncology

- 6.3.4. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Diagnostics

- 7. United Kingdom Europe Nuclear Medicine Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Diagnostics

- 7.1.1. Single Photon Emission Computed Tomography (SPECT)

- 7.1.2. Positron Emission Tomography (PET)

- 7.2. Market Analysis, Insights and Forecast - by Therapeutics

- 7.2.1. Alpha Emitters

- 7.2.2. Beta Emitters

- 7.2.3. Brachytherapy

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Cardiology

- 7.3.2. Neurology

- 7.3.3. Oncology

- 7.3.4. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Diagnostics

- 8. France Europe Nuclear Medicine Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Diagnostics

- 8.1.1. Single Photon Emission Computed Tomography (SPECT)

- 8.1.2. Positron Emission Tomography (PET)

- 8.2. Market Analysis, Insights and Forecast - by Therapeutics

- 8.2.1. Alpha Emitters

- 8.2.2. Beta Emitters

- 8.2.3. Brachytherapy

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Cardiology

- 8.3.2. Neurology

- 8.3.3. Oncology

- 8.3.4. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Diagnostics

- 9. Italy Europe Nuclear Medicine Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Diagnostics

- 9.1.1. Single Photon Emission Computed Tomography (SPECT)

- 9.1.2. Positron Emission Tomography (PET)

- 9.2. Market Analysis, Insights and Forecast - by Therapeutics

- 9.2.1. Alpha Emitters

- 9.2.2. Beta Emitters

- 9.2.3. Brachytherapy

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Cardiology

- 9.3.2. Neurology

- 9.3.3. Oncology

- 9.3.4. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Diagnostics

- 10. Spain Europe Nuclear Medicine Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Diagnostics

- 10.1.1. Single Photon Emission Computed Tomography (SPECT)

- 10.1.2. Positron Emission Tomography (PET)

- 10.2. Market Analysis, Insights and Forecast - by Therapeutics

- 10.2.1. Alpha Emitters

- 10.2.2. Beta Emitters

- 10.2.3. Brachytherapy

- 10.3. Market Analysis, Insights and Forecast - by Application

- 10.3.1. Cardiology

- 10.3.2. Neurology

- 10.3.3. Oncology

- 10.3.4. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Diagnostics

- 11. Rest of Europe Europe Nuclear Medicine Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - by Diagnostics

- 11.1.1. Single Photon Emission Computed Tomography (SPECT)

- 11.1.2. Positron Emission Tomography (PET)

- 11.2. Market Analysis, Insights and Forecast - by Therapeutics

- 11.2.1. Alpha Emitters

- 11.2.2. Beta Emitters

- 11.2.3. Brachytherapy

- 11.3. Market Analysis, Insights and Forecast - by Application

- 11.3.1. Cardiology

- 11.3.2. Neurology

- 11.3.3. Oncology

- 11.3.4. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by Diagnostics

- 12. Germany Europe Nuclear Medicine Industry Analysis, Insights and Forecast, 2019-2031

- 13. France Europe Nuclear Medicine Industry Analysis, Insights and Forecast, 2019-2031

- 14. Italy Europe Nuclear Medicine Industry Analysis, Insights and Forecast, 2019-2031

- 15. United Kingdom Europe Nuclear Medicine Industry Analysis, Insights and Forecast, 2019-2031

- 16. Netherlands Europe Nuclear Medicine Industry Analysis, Insights and Forecast, 2019-2031

- 17. Sweden Europe Nuclear Medicine Industry Analysis, Insights and Forecast, 2019-2031

- 18. Rest of Europe Europe Nuclear Medicine Industry Analysis, Insights and Forecast, 2019-2031

- 19. Competitive Analysis

- 19.1. Market Share Analysis 2024

- 19.2. Company Profiles

- 19.2.1 Nordion Inc

- 19.2.1.1. Overview

- 19.2.1.2. Products

- 19.2.1.3. SWOT Analysis

- 19.2.1.4. Recent Developments

- 19.2.1.5. Financials (Based on Availability)

- 19.2.2 GE Healthcare

- 19.2.2.1. Overview

- 19.2.2.2. Products

- 19.2.2.3. SWOT Analysis

- 19.2.2.4. Recent Developments

- 19.2.2.5. Financials (Based on Availability)

- 19.2.3 Bracco Imaging SpA

- 19.2.3.1. Overview

- 19.2.3.2. Products

- 19.2.3.3. SWOT Analysis

- 19.2.3.4. Recent Developments

- 19.2.3.5. Financials (Based on Availability)

- 19.2.4 Advanced Accelerator Applications

- 19.2.4.1. Overview

- 19.2.4.2. Products

- 19.2.4.3. SWOT Analysis

- 19.2.4.4. Recent Developments

- 19.2.4.5. Financials (Based on Availability)

- 19.2.5 Cardinal Health Inc

- 19.2.5.1. Overview

- 19.2.5.2. Products

- 19.2.5.3. SWOT Analysis

- 19.2.5.4. Recent Developments

- 19.2.5.5. Financials (Based on Availability)

- 19.2.6 Merck KGaA (Sigma-Aldrich)

- 19.2.6.1. Overview

- 19.2.6.2. Products

- 19.2.6.3. SWOT Analysis

- 19.2.6.4. Recent Developments

- 19.2.6.5. Financials (Based on Availability)

- 19.2.7 Siemens Healthineers AG*List Not Exhaustive

- 19.2.7.1. Overview

- 19.2.7.2. Products

- 19.2.7.3. SWOT Analysis

- 19.2.7.4. Recent Developments

- 19.2.7.5. Financials (Based on Availability)

- 19.2.8 Curium Pharma

- 19.2.8.1. Overview

- 19.2.8.2. Products

- 19.2.8.3. SWOT Analysis

- 19.2.8.4. Recent Developments

- 19.2.8.5. Financials (Based on Availability)

- 19.2.1 Nordion Inc

List of Figures

- Figure 1: Europe Nuclear Medicine Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe Nuclear Medicine Industry Share (%) by Company 2024

List of Tables

- Table 1: Europe Nuclear Medicine Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe Nuclear Medicine Industry Revenue Million Forecast, by Diagnostics 2019 & 2032

- Table 3: Europe Nuclear Medicine Industry Revenue Million Forecast, by Therapeutics 2019 & 2032

- Table 4: Europe Nuclear Medicine Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 5: Europe Nuclear Medicine Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Europe Nuclear Medicine Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Germany Europe Nuclear Medicine Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: France Europe Nuclear Medicine Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Italy Europe Nuclear Medicine Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: United Kingdom Europe Nuclear Medicine Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Netherlands Europe Nuclear Medicine Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Sweden Europe Nuclear Medicine Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Rest of Europe Europe Nuclear Medicine Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Europe Nuclear Medicine Industry Revenue Million Forecast, by Diagnostics 2019 & 2032

- Table 15: Europe Nuclear Medicine Industry Revenue Million Forecast, by Therapeutics 2019 & 2032

- Table 16: Europe Nuclear Medicine Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 17: Europe Nuclear Medicine Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: Europe Nuclear Medicine Industry Revenue Million Forecast, by Diagnostics 2019 & 2032

- Table 19: Europe Nuclear Medicine Industry Revenue Million Forecast, by Therapeutics 2019 & 2032

- Table 20: Europe Nuclear Medicine Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 21: Europe Nuclear Medicine Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 22: Europe Nuclear Medicine Industry Revenue Million Forecast, by Diagnostics 2019 & 2032

- Table 23: Europe Nuclear Medicine Industry Revenue Million Forecast, by Therapeutics 2019 & 2032

- Table 24: Europe Nuclear Medicine Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 25: Europe Nuclear Medicine Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 26: Europe Nuclear Medicine Industry Revenue Million Forecast, by Diagnostics 2019 & 2032

- Table 27: Europe Nuclear Medicine Industry Revenue Million Forecast, by Therapeutics 2019 & 2032

- Table 28: Europe Nuclear Medicine Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 29: Europe Nuclear Medicine Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 30: Europe Nuclear Medicine Industry Revenue Million Forecast, by Diagnostics 2019 & 2032

- Table 31: Europe Nuclear Medicine Industry Revenue Million Forecast, by Therapeutics 2019 & 2032

- Table 32: Europe Nuclear Medicine Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 33: Europe Nuclear Medicine Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 34: Europe Nuclear Medicine Industry Revenue Million Forecast, by Diagnostics 2019 & 2032

- Table 35: Europe Nuclear Medicine Industry Revenue Million Forecast, by Therapeutics 2019 & 2032

- Table 36: Europe Nuclear Medicine Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 37: Europe Nuclear Medicine Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Nuclear Medicine Industry?

The projected CAGR is approximately 10.00%.

2. Which companies are prominent players in the Europe Nuclear Medicine Industry?

Key companies in the market include Nordion Inc, GE Healthcare, Bracco Imaging SpA, Advanced Accelerator Applications, Cardinal Health Inc, Merck KGaA (Sigma-Aldrich), Siemens Healthineers AG*List Not Exhaustive, Curium Pharma.

3. What are the main segments of the Europe Nuclear Medicine Industry?

The market segments include Diagnostics, Therapeutics, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Incidence of Cancer and Cardiac Ailments; Increasing SPECT and PET Applications.

6. What are the notable trends driving market growth?

Oncology Segment is Expected to Register a Significant CAGR During the Forecast Period.

7. Are there any restraints impacting market growth?

Strict Regulatory Guidelines.

8. Can you provide examples of recent developments in the market?

In June 2022, Curium submitted its Marketing Authorization Application for [18F]-DCFPyL for treating multiple stages of prostate cancer disease to the European Medicines Agency.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Nuclear Medicine Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Nuclear Medicine Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Nuclear Medicine Industry?

To stay informed about further developments, trends, and reports in the Europe Nuclear Medicine Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence