Key Insights

The European vibration sensor market, valued at approximately €1.5 billion in 2025, is projected to experience robust growth, driven by increasing automation across diverse industries and the burgeoning demand for predictive maintenance solutions. This growth is further fueled by technological advancements leading to more compact, sensitive, and cost-effective sensors. The automotive sector, a significant market segment, is adopting vibration sensors extensively for improved engine performance, safety systems, and driver-assistance features. The healthcare industry's reliance on precise diagnostics and the rise of sophisticated medical equipment are also substantial contributors to market expansion. Within Europe, Germany, France, and the United Kingdom represent the largest national markets, benefiting from strong industrial bases and technological innovation. The increasing integration of IoT (Internet of Things) technologies and the adoption of Industry 4.0 principles are expected to propel market growth further.

However, certain challenges exist. High initial investment costs associated with sensor implementation and integration can act as a restraint for smaller businesses. Furthermore, the market faces challenges related to the availability of skilled labor for sensor integration and data analysis. The market's competitive landscape is characterized by a mix of established players and emerging technology companies, driving innovation and price competition. To maintain growth, manufacturers are focusing on developing sensors with enhanced functionalities, improved durability, and lower energy consumption. The long-term outlook for the European vibration sensor market remains positive, particularly driven by sustained growth across automotive, healthcare, and industrial automation sectors. Expansion into emerging applications, such as smart infrastructure and robotics, will further contribute to market expansion throughout the forecast period (2025-2033).

Europe Vibration Sensors Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Europe vibration sensors industry, offering invaluable insights for stakeholders seeking to navigate this dynamic market. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report delivers a robust understanding of past performance, current trends, and future projections. The market is segmented by product (accelerometers, proximity probes, tachometers, others), industry (automotive, healthcare, aerospace & defense, consumer electronics, oil and gas, metals and mining, others), and country (United Kingdom, Germany, France, others). Key players analyzed include Honeywell International Inc, NXP Semiconductors N.V., SKF AB, National Instruments Corporation, Emerson Electric Co, TE Connectivity Ltd, Bosch Sensortec GmbH, Hansford Sensors Ltd, Texas Instruments Incorporated, Rockwell Automation Inc, and Analog Devices Inc. The total market size in 2025 is estimated at xx Million.

Europe Vibration Sensors Industry Market Concentration & Dynamics

The European vibration sensors market exhibits a moderately concentrated landscape, with several major players holding significant market share. However, the presence of numerous smaller, specialized companies fosters innovation and competition. The market is characterized by a dynamic interplay of factors, including technological advancements, evolving regulatory frameworks, and fluctuating end-user demands across various sectors. Mergers and acquisitions (M&A) activity plays a significant role in shaping market dynamics, with notable deals impacting market concentration and product offerings. For example, TE Connectivity Ltd's acquisition of First Sensor AG in March 2020 significantly expanded its product portfolio and market reach.

- Market Concentration: The top 5 players hold an estimated xx% market share in 2025.

- M&A Activity: A total of xx M&A deals were recorded between 2019 and 2024, indicative of significant industry consolidation.

- Innovation Ecosystems: Collaboration between sensor manufacturers, research institutions, and end-users drives continuous innovation in sensor technology and applications.

- Regulatory Frameworks: Compliance with stringent safety and environmental regulations influences product design and market access.

- Substitute Products: Technological advancements in alternative sensing technologies pose a moderate threat, requiring continuous innovation to maintain market share.

- End-User Trends: Growth in sectors like automotive, industrial automation, and healthcare is driving demand for sophisticated vibration sensors.

Europe Vibration Sensors Industry Industry Insights & Trends

The European vibration sensors market is experiencing robust growth, driven by increasing demand across diverse industrial sectors. Technological advancements, particularly in miniaturization, improved accuracy, and wireless connectivity, are fueling market expansion. The automotive industry, with its focus on advanced driver-assistance systems (ADAS) and electric vehicles, represents a significant growth driver. Similarly, the increasing adoption of industrial automation and the growth of the healthcare sector are propelling demand for high-performance vibration sensors. The market is expected to witness a Compound Annual Growth Rate (CAGR) of xx% from 2025 to 2033, reaching a projected value of xx Million by 2033. Consumer electronics and building automation also represent significant, albeit less rapidly growing, segments. Evolving consumer preferences for more advanced products with improved functionality and connectivity are positively impacting demand for these sensors.

Key Markets & Segments Leading Europe Vibration Sensors Industry

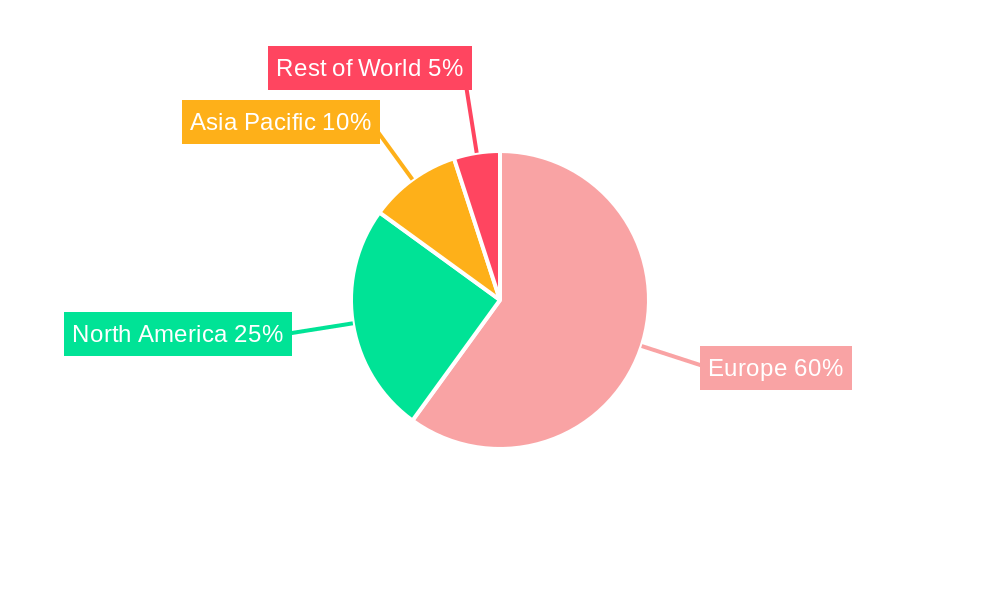

The automotive sector dominates the European vibration sensors market, driven by increasing demand for advanced driver-assistance systems (ADAS) and the rising adoption of electric and hybrid vehicles. Within the product segment, accelerometers hold the largest market share, owing to their widespread application across various industries. Germany and the United Kingdom are the leading national markets, benefiting from strong automotive and industrial manufacturing sectors.

- Dominant Region: Western Europe.

- Dominant Country: Germany.

- Dominant Product Segment: Accelerometers.

- Dominant Industry Segment: Automotive.

Drivers for Automotive Segment Growth:

- Strong growth in vehicle production and sales.

- Increasing demand for advanced driver-assistance systems (ADAS).

- Rise of electric and hybrid vehicles.

- Stringent regulations mandating improved safety features.

Drivers for Germany’s Market Dominance:

- Strong automotive manufacturing base.

- Presence of major automotive OEMs and suppliers.

- Robust industrial automation sector.

- Significant investment in research and development.

Europe Vibration Sensors Industry Product Developments

Recent advancements in vibration sensor technology include the development of smaller, more energy-efficient sensors with enhanced accuracy and improved wireless connectivity. The introduction of MEMS (Microelectromechanical Systems) based sensors has facilitated miniaturization and cost reduction, leading to wider adoption across various applications. Furthermore, innovations in signal processing algorithms have significantly improved the accuracy and reliability of vibration measurements. This technological progress is driving competitiveness and enabling the creation of advanced sensor solutions that meet evolving industry needs. For example, Hansford Sensors' launch of the HS-173I Accelerometer demonstrates advancements in ruggedized design for hazardous environments.

Challenges in the Europe Vibration Sensors Industry Market

The European vibration sensors market faces challenges including intense competition, stringent regulatory compliance requirements, and potential supply chain disruptions. The competitive landscape is characterized by a mix of large multinational corporations and smaller specialized firms, resulting in significant price pressure and a need for continuous innovation. Furthermore, meeting stringent regulatory requirements regarding safety and environmental compliance adds to the cost and complexity of product development and market entry. Supply chain vulnerabilities, particularly in sourcing critical components, pose a risk to production and delivery timelines, potentially impacting profitability.

Forces Driving Europe Vibration Sensors Industry Growth

Technological advancements, primarily in miniaturization, increased accuracy, and wireless capabilities, are driving market growth. The burgeoning demand across various industries, including automotive, healthcare, and industrial automation, is another major driver. Favorable government regulations and investments in infrastructure development further support industry expansion.

Long-Term Growth Catalysts in Europe Vibration Sensors Industry

Long-term growth will be driven by continued innovation in sensor technology, strategic partnerships between sensor manufacturers and technology providers, and expansion into new markets, especially in emerging economies. The adoption of Industry 4.0 initiatives will create substantial growth opportunities.

Emerging Opportunities in Europe Vibration Sensors Industry

Emerging trends indicate growing opportunities in the Internet of Things (IoT), smart cities, and predictive maintenance applications. The integration of vibration sensors into smart devices and infrastructure systems presents significant market potential. Furthermore, increasing demand for sophisticated vibration monitoring solutions in healthcare and environmental monitoring offer significant expansion possibilities.

Leading Players in the Europe Vibration Sensors Industry Sector

- Honeywell International Inc

- NXP Semiconductors N.V.

- SKF AB

- National Instruments Corporation

- Emerson Electric Co

- TE Connectivity Ltd

- Bosch Sensortec GmbH

- Hansford Sensors Ltd

- Texas Instruments Incorporated

- Rockwell Automation Inc

- Analog Devices Inc

Key Milestones in Europe Vibration Sensors Industry Industry

- March 2020: TE Connectivity Ltd completed its public takeover of First Sensor AG, significantly expanding its product portfolio and market reach.

- August 2020: Hansford Sensors Ltd launched the HS-173I Accelerometer, a premium intrinsically safe triaxial sensor designed for hazardous environments, expanding its product line and targeting a niche market.

Strategic Outlook for Europe Vibration Sensors Industry Market

The future of the European vibration sensors market appears promising, fueled by continued technological innovation, expanding applications across diverse sectors, and the growth of related industries. Strategic opportunities lie in developing advanced sensor solutions tailored to specific industry needs, fostering partnerships to enhance product offerings and market reach, and investing in research and development to maintain a competitive edge. The market's long-term potential is considerable, particularly in high-growth sectors such as automotive, healthcare, and industrial automation.

Europe Vibration Sensors Industry Segmentation

-

1. product

- 1.1. Accelerometers

- 1.2. Proximity Probes

- 1.3. Tachometers

- 1.4. Others

-

2. Industry

- 2.1. Automotive

- 2.2. Helathcare

- 2.3. Aerospace & Defence

- 2.4. Consumer Electronics

- 2.5. Oil And Gas

- 2.6. Metals and Mining

- 2.7. others

Europe Vibration Sensors Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Vibration Sensors Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 8.30% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 Increasing Need for Machine Monitoring and Maintenance; Longer Service Life

- 3.2.2 Self Generating Capability and Wide Range of Frequency of Vibration Sensors

- 3.3. Market Restrains

- 3.3.1. Compatibility With Old Machinery; Critical and Hazardous Implication on the Environment

- 3.4. Market Trends

- 3.4.1. Aerospace & Defense End User to Hold Significant Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Vibration Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by product

- 5.1.1. Accelerometers

- 5.1.2. Proximity Probes

- 5.1.3. Tachometers

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Industry

- 5.2.1. Automotive

- 5.2.2. Helathcare

- 5.2.3. Aerospace & Defence

- 5.2.4. Consumer Electronics

- 5.2.5. Oil And Gas

- 5.2.6. Metals and Mining

- 5.2.7. others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by product

- 6. Germany Europe Vibration Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 7. France Europe Vibration Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 8. Italy Europe Vibration Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 9. United Kingdom Europe Vibration Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 10. Netherlands Europe Vibration Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 11. Sweden Europe Vibration Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Europe Europe Vibration Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Honeywell International Inc

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 NXP Semiconductors N V

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 SKF AB

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 National Instruments Corporation

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Emerson Electric Co

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 TE Connectivity Ltd

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Bosch Sensortec GmbH (Robert Bosch GmbH

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Hansford Sensors Ltd

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Texas Instruments Incorporated

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Rockwell Automation Inc

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.11 Analog Devices Inc

- 13.2.11.1. Overview

- 13.2.11.2. Products

- 13.2.11.3. SWOT Analysis

- 13.2.11.4. Recent Developments

- 13.2.11.5. Financials (Based on Availability)

- 13.2.1 Honeywell International Inc

List of Figures

- Figure 1: Europe Vibration Sensors Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe Vibration Sensors Industry Share (%) by Company 2024

List of Tables

- Table 1: Europe Vibration Sensors Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe Vibration Sensors Industry Revenue Million Forecast, by product 2019 & 2032

- Table 3: Europe Vibration Sensors Industry Revenue Million Forecast, by Industry 2019 & 2032

- Table 4: Europe Vibration Sensors Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Europe Vibration Sensors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Germany Europe Vibration Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: France Europe Vibration Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Italy Europe Vibration Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: United Kingdom Europe Vibration Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Netherlands Europe Vibration Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Sweden Europe Vibration Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Rest of Europe Europe Vibration Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Europe Vibration Sensors Industry Revenue Million Forecast, by product 2019 & 2032

- Table 14: Europe Vibration Sensors Industry Revenue Million Forecast, by Industry 2019 & 2032

- Table 15: Europe Vibration Sensors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: United Kingdom Europe Vibration Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Germany Europe Vibration Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: France Europe Vibration Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Italy Europe Vibration Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Spain Europe Vibration Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Netherlands Europe Vibration Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Belgium Europe Vibration Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Sweden Europe Vibration Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Norway Europe Vibration Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Poland Europe Vibration Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Denmark Europe Vibration Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Vibration Sensors Industry?

The projected CAGR is approximately 8.30%.

2. Which companies are prominent players in the Europe Vibration Sensors Industry?

Key companies in the market include Honeywell International Inc, NXP Semiconductors N V, SKF AB, National Instruments Corporation, Emerson Electric Co, TE Connectivity Ltd, Bosch Sensortec GmbH (Robert Bosch GmbH, Hansford Sensors Ltd, Texas Instruments Incorporated, Rockwell Automation Inc, Analog Devices Inc.

3. What are the main segments of the Europe Vibration Sensors Industry?

The market segments include product, Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Need for Machine Monitoring and Maintenance; Longer Service Life. Self Generating Capability and Wide Range of Frequency of Vibration Sensors.

6. What are the notable trends driving market growth?

Aerospace & Defense End User to Hold Significant Share.

7. Are there any restraints impacting market growth?

Compatibility With Old Machinery; Critical and Hazardous Implication on the Environment.

8. Can you provide examples of recent developments in the market?

Mar 2020: TE Connectivity Ltd has completed its public takeover of First Sensor AG. TE now holds 71.87% shares of First Sensor. In combination with First Sensor and TE portfolios, TE will be able to offer a broader product base, including innovative sensors, connectors, and systems, that supports the growth strategy of TE's sensors business and TE Connectivity as a whole.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Vibration Sensors Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Vibration Sensors Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Vibration Sensors Industry?

To stay informed about further developments, trends, and reports in the Europe Vibration Sensors Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence