Key Insights

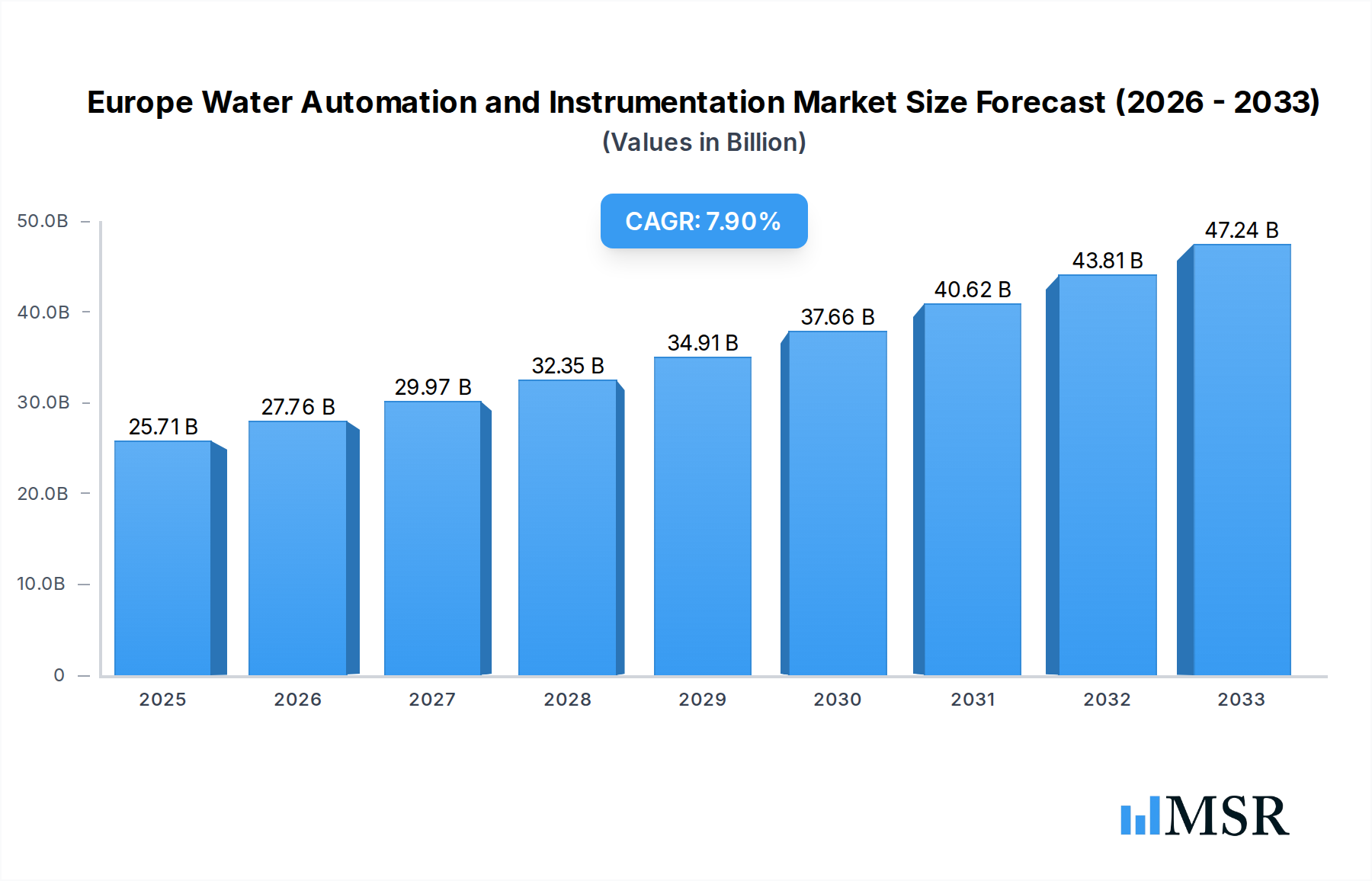

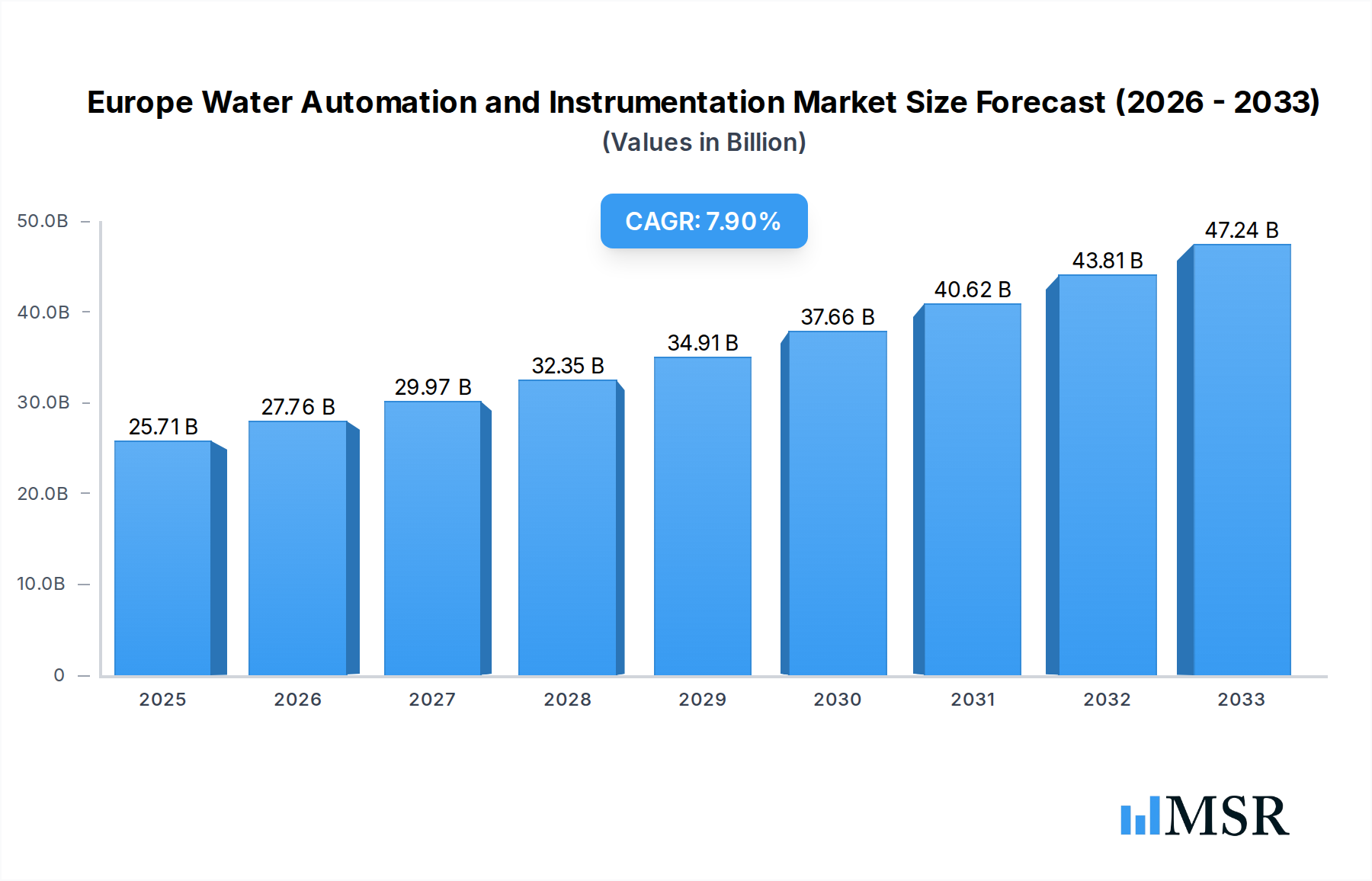

The Europe Water Automation and Instrumentation Market is poised for substantial growth, projected to reach USD 25.71 billion in 2025 and expand at a robust CAGR of 8.1% through 2033. This significant market expansion is driven by an increasing global emphasis on efficient water management, stringent environmental regulations, and the growing adoption of smart technologies across various end-user industries. The demand for advanced automation solutions, including Distributed Control Systems (DCS), Supervisory Control and Data Acquisition (SCADA), Programmable Logic Controllers (PLC), and Human-Machine Interfaces (HMI), is particularly strong. These technologies are crucial for optimizing water treatment processes, ensuring compliance, and enhancing operational efficiency in utilities, manufacturing, and chemical sectors. Furthermore, the burgeoning need for precise monitoring and control of water quality and quantity fuels the demand for sophisticated instrumentation such as pressure transmitters, level transmitters, temperature transmitters, liquid and gas analyzers, and flow sensors.

Europe Water Automation and Instrumentation Market Market Size (In Billion)

The market's growth trajectory is further bolstered by ongoing investments in upgrading aging water infrastructure and the increasing deployment of Industrial Internet of Things (IIoT) and AI-driven solutions for predictive maintenance and real-time data analysis. Leading companies are actively innovating to offer integrated solutions that address the complex challenges of water scarcity and pollution. While the market benefits from strong drivers, potential restraints such as high initial investment costs for advanced systems and the need for skilled personnel to operate and maintain these technologies may present some hurdles. However, the clear benefits of improved resource management, reduced operational costs, and enhanced sustainability are expected to outweigh these challenges, solidifying Europe's position as a key region in the global water automation and instrumentation landscape.

Europe Water Automation and Instrumentation Market Company Market Share

This in-depth report provides a detailed analysis of the Europe Water Automation and Instrumentation Market, a rapidly expanding sector driven by increasing demand for efficient water management solutions across diverse industries. Examining market dynamics, industry insights, key segments, technological advancements, and competitive landscapes, this report offers crucial intelligence for stakeholders seeking to capitalize on growth opportunities. The study period spans from 2019 to 2033, with a base year of 2025. The forecast period extends from 2025 to 2033, building upon historical data from 2019 to 2024. The Europe Water Automation and Instrumentation Market is projected to reach USD XX billion by 2025 and is expected to grow at a Compound Annual Growth Rate (CAGR) of XX% during the forecast period.

Europe Water Automation and Instrumentation Market Market Concentration & Dynamics

The Europe Water Automation and Instrumentation Market is characterized by a moderately consolidated landscape, with key players like Siemens AG, Schneider Electric SE, Emerson Electric, and ABB Group holding significant market share. Innovation is a critical driver, with companies investing heavily in research and development for advanced water treatment automation, smart water metering, and industrial IoT integration. Regulatory frameworks, particularly those focused on water quality standards and environmental protection, play a pivotal role in shaping market trends. The growing emphasis on sustainability and water scarcity is pushing for the adoption of sophisticated water management systems. Substitute products, such as manual control systems, are gradually being phased out in favor of automated and instrumented solutions. End-user trends highlight a strong preference for digital water solutions, real-time monitoring, and predictive maintenance capabilities across various sectors. Mergers and acquisitions (M&A) activity is a notable dynamic, with strategic consolidations aimed at expanding product portfolios and market reach. For instance, the acquisition of Suez by Veolia in April 2021 significantly reshaped the competitive landscape of the broader water sector, impacting associated automation and instrumentation markets. The M&A deal count is estimated to be around XX deals within the study period, reflecting a trend towards strategic alliances and market consolidation.

Europe Water Automation and Instrumentation Market Industry Insights & Trends

The Europe Water Automation and Instrumentation Market is experiencing robust growth, propelled by several interconnected factors. A primary driver is the escalating need for efficient water resource management, driven by increasing population, industrial expansion, and the growing threat of water scarcity across the continent. Governments and regulatory bodies are implementing stringent environmental policies and water quality standards, compelling industries to invest in advanced water purification automation and precise water quality monitoring instruments. The rise of the Industrial Internet of Things (IIoT) is revolutionizing the sector, enabling real-time data collection, analysis, and remote control of water treatment processes. This fosters operational efficiency, reduces water wastage, and optimizes resource allocation. The demand for smart water solutions, including smart metering and leakage detection systems, is surging, particularly from the utilities sector, to combat non-revenue water and improve infrastructure management. Technological advancements in sensors, actuators, and control systems are leading to more accurate, reliable, and cost-effective water automation solutions and water instrumentation solutions. The food and beverage and chemical industries, with their high water consumption and stringent quality requirements, are significant contributors to market expansion. Furthermore, the ongoing digital transformation across all industries is creating a strong appetite for integrated water management platforms and data analytics for water utilities. The market size for Europe Water Automation and Instrumentation Market was valued at approximately USD XX billion in 2024 and is projected to reach USD XX billion by 2033, exhibiting a CAGR of XX%. Key trends include the growing adoption of cloud-based platforms for data management and remote monitoring, the increasing sophistication of AI and machine learning for predictive analytics in water treatment, and the demand for integrated solutions that encompass both automation and instrumentation. The focus on energy-efficient water treatment processes also drives the demand for advanced instrumentation and control systems.

Key Markets & Segments Leading Europe Water Automation and Instrumentation Market

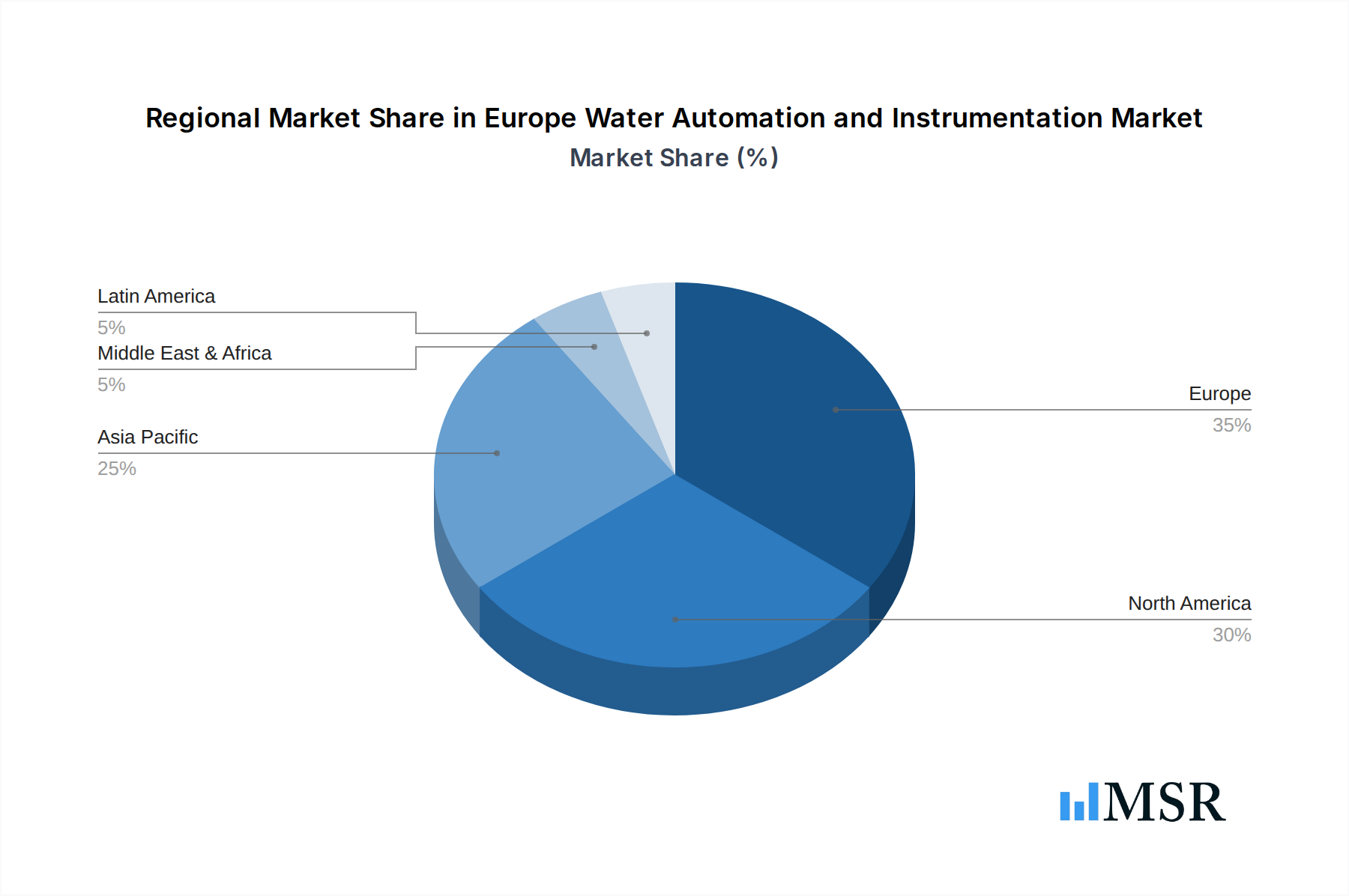

The Europe Water Automation and Instrumentation Market showcases dominant performance in key regions and segments, driven by robust industrial activity and stringent environmental regulations. Germany, the United Kingdom, France, and the Netherlands are leading markets, owing to their advanced industrial infrastructure and proactive approach to water resource management.

Water Automation Solutions:

- SCADA (Supervisory Control and Data Acquisition) systems are witnessing significant adoption due to their ability to monitor and control large-scale water distribution and treatment networks efficiently. The utilities sector heavily relies on SCADA for real-time operational oversight.

- DCS (Distributed Control Systems) are crucial for complex industrial processes, particularly in chemical and manufacturing sectors, where precise control over water treatment is paramount.

- PLC (Programmable Logic Controllers) are widely deployed for their flexibility and reliability in automating smaller-scale water treatment units and pump stations across various industries.

- HMI (Human-Machine Interface) solutions are integral for enabling operators to interact with automated systems, with increasing demand for user-friendly and intuitive interfaces.

- Other Water Automation Solutions, including advanced process control software and digital twins, are gaining traction for optimizing water treatment operations.

Water Instrumentation Solutions:

- Flow Sensors/Transmitters are essential for accurate measurement of water volumes, driving demand in utilities for billing and in industries for process control.

- Pressure Transmitters are critical for monitoring pressure in pipelines and treatment facilities, ensuring system integrity and preventing leaks.

- Level Transmitters are vital for managing water levels in reservoirs, tanks, and treatment basins.

- Liquid Analyzers are in high demand for monitoring water quality parameters like pH, turbidity, and conductivity, crucial for compliance and process efficiency, particularly in the food and beverage and chemical sectors.

- Leakage Detection Systems are experiencing substantial growth, driven by utilities' efforts to reduce water loss and improve infrastructure efficiency.

- Gas Analyzers are important in specific industrial applications where gas detection in water systems is critical for safety and process control.

End-User Industry Dominance:

- Utilities represent the largest end-user segment, driven by the need for efficient water supply, wastewater treatment, and infrastructure management, leading to significant investments in SCADA, leakage detection, and smart metering.

- Manufacturing industries, including automotive and electronics, are major consumers of water for various processes, necessitating advanced automation and instrumentation for quality control and resource optimization.

- Chemical and Pharmaceutical industries rely heavily on precise water quality control and automated treatment processes, making them key adopters of sophisticated instrumentation like liquid analyzers and DCS.

- Food and Beverages sector demands high standards of water purity and safety, driving the adoption of advanced liquid analyzers and automated disinfection systems.

- Paper and Pulp industries utilize vast amounts of water, requiring efficient automation for water recycling and treatment processes.

The growth in these segments is underpinned by factors such as increasing infrastructure investments, a rising focus on operational efficiency, and the imperative to comply with stringent environmental regulations.

Europe Water Automation and Instrumentation Market Product Developments

Recent product developments in the Europe Water Automation and Instrumentation Market focus on enhancing intelligence, connectivity, and efficiency. Manufacturers are introducing next-generation sensors with improved accuracy, faster response times, and greater resistance to harsh environments. The integration of AI and machine learning into water treatment automation software is enabling predictive maintenance and optimized process control, minimizing downtime and operational costs. The development of advanced digital water platforms allows for seamless data integration from various automation and instrumentation devices, providing a holistic view of water management operations. Innovations in wireless sensor technologies and IIoT connectivity are facilitating easier deployment and scalability of monitoring solutions, particularly for leakage detection and remote asset management. These advancements are crucial for meeting the evolving demands for sustainable and data-driven water management practices.

Challenges in the Europe Water Automation and Instrumentation Market Market

Despite significant growth, the Europe Water Automation and Instrumentation Market faces several challenges. High initial investment costs for advanced automation and instrumentation systems can be a barrier for smaller utilities and businesses. Cybersecurity concerns related to connected water infrastructure are a growing apprehension, necessitating robust security protocols. Interoperability issues between different vendor systems can hinder seamless integration, leading to fragmented solutions. The shortage of skilled personnel capable of installing, operating, and maintaining complex automation and instrumentation systems also poses a significant challenge. Furthermore, evolving regulatory landscapes can sometimes create compliance complexities, requiring continuous adaptation of systems and processes.

Forces Driving Europe Water Automation and Instrumentation Market Growth

The Europe Water Automation and Instrumentation Market is propelled by a confluence of powerful growth drivers. The increasing global focus on water scarcity and sustainability mandates efficient water management, thereby fueling demand for automation and instrumentation. Stringent environmental regulations and water quality standards set by European bodies necessitate advanced monitoring and control technologies. The ongoing digital transformation and the widespread adoption of Industrial Internet of Things (IIoT) are creating opportunities for smart water solutions, remote monitoring, and data-driven decision-making. Significant infrastructure upgrades and investments in water and wastewater treatment facilities across Europe are directly contributing to market expansion. Furthermore, the pursuit of operational efficiency and cost reduction by industries and utilities drives the adoption of automated systems that minimize manual intervention and optimize resource utilization.

Challenges in the Europe Water Automation and Instrumentation Market Market

Long-term growth catalysts for the Europe Water Automation and Instrumentation Market are rooted in innovation and strategic market expansion. The continuous development of smart water technologies, including AI-powered predictive analytics and advanced sensor networks, will drive increased adoption and value creation. Strategic partnerships and collaborations between automation providers, instrumentation manufacturers, and water utilities are crucial for developing integrated and customized solutions. The expansion of digital water platforms that offer comprehensive data management and operational insights will further accelerate market growth. Moreover, the increasing global demand for sustainable water management practices will open up new export opportunities and drive further innovation within the European market.

Emerging Opportunities in Europe Water Automation and Instrumentation Market

Emerging opportunities within the Europe Water Automation and Instrumentation Market are abundant and diverse. The growing adoption of smart city initiatives presents a significant avenue for deploying integrated water management systems, including intelligent water networks and smart metering solutions. The increasing focus on water reuse and recycling across industrial sectors is creating demand for advanced purification and monitoring technologies. The development of predictive maintenance solutions leveraging AI and machine learning for water infrastructure is a key trend, offering significant cost savings and operational improvements. Furthermore, the expanding market for decentralized water treatment systems and micro-grids presents opportunities for scalable and modular automation and instrumentation solutions. The integration of blockchain technology for enhanced data security and transparency in water management is another promising area.

Leading Players in the Europe Water Automation and Instrumentation Market Sector

- Emerson Electric

- ABB Group

- NALCO

- Phoenix Contact

- Rockwell Automation Inc

- Endress + Hauser Pvt Ltd

- Yokogawa Electric Corporation

- GE Corporation

- Mitsubishi Electric Corporation (Note: Mitsubishi Motors Corporation is an automotive company, Mitsubishi Electric Corporation is relevant here)

- Eurotek India

- KROHNE LT

- MJK Automation

- Siemens AG

- Schneider Electric SE

Key Milestones in Europe Water Automation and Instrumentation Market Industry

- April 2021: Veolia acquired its rival Suez, a significant consolidation event in the broader water industry that will indirectly impact the demand for automation and instrumentation solutions within the merged entity's vast operations.

- March 2021: The SUEZ and Schneider Electric groups formed a partnership in digital water, aiming to develop and market joint innovative digital solutions for water cycle management. This collaboration is expected to accelerate digital transformations for municipal water operators and industrial players by offering a comprehensive suite of software solutions for planning, operation, maintenance, and optimization of water treatment infrastructure.

Strategic Outlook for Europe Water Automation and Instrumentation Market Market

The strategic outlook for the Europe Water Automation and Instrumentation Market is highly positive, driven by continuous technological advancements and an unwavering commitment to sustainability. Future growth will be significantly accelerated by the widespread adoption of smart water technologies, including IoT-enabled sensors, AI-driven analytics, and cloud-based management platforms. Strategic investments in upgrading aging water infrastructure and developing resilient water systems will remain a key focus. The increasing demand for traceability and transparency in water quality management will further propel the adoption of advanced instrumentation and data logging solutions. Collaborative efforts between technology providers, regulatory bodies, and end-users will be crucial in addressing complex water challenges and unlocking new market potentials, solidifying Europe's position as a leader in innovative water management.

Europe Water Automation and Instrumentation Market Segmentation

-

1. Water Automation Solution

- 1.1. DCS

- 1.2. SCADA

- 1.3. PLC

- 1.4. HMI

- 1.5. Other Water Automation Solutions

-

2. Water Instrumentation Solution

- 2.1. Pressure Transmitter

- 2.2. Level Transmitter

- 2.3. Temperature Transmitter

- 2.4. Liquid Analyzers

- 2.5. Gas Analyzers

- 2.6. Leakage Detection Systems

- 2.7. Flow Sensors/Transmitters

- 2.8. Other Water Instrumentation Solutions

-

3. End-User Industry (Qualitative Analysis)

- 3.1. Chemical

- 3.2. Manufacturing

- 3.3. Food and Beverages

- 3.4. Utilities

- 3.5. Paper and Pulp

- 3.6. Other End-user Industries

Europe Water Automation and Instrumentation Market Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Water Automation and Instrumentation Market Regional Market Share

Geographic Coverage of Europe Water Automation and Instrumentation Market

Europe Water Automation and Instrumentation Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Water Automation Solution

- 5.1.1. DCS

- 5.1.2. SCADA

- 5.1.3. PLC

- 5.1.4. HMI

- 5.1.5. Other Water Automation Solutions

- 5.2. Market Analysis, Insights and Forecast - by Water Instrumentation Solution

- 5.2.1. Pressure Transmitter

- 5.2.2. Level Transmitter

- 5.2.3. Temperature Transmitter

- 5.2.4. Liquid Analyzers

- 5.2.5. Gas Analyzers

- 5.2.6. Leakage Detection Systems

- 5.2.7. Flow Sensors/Transmitters

- 5.2.8. Other Water Instrumentation Solutions

- 5.3. Market Analysis, Insights and Forecast - by End-User Industry (Qualitative Analysis)

- 5.3.1. Chemical

- 5.3.2. Manufacturing

- 5.3.3. Food and Beverages

- 5.3.4. Utilities

- 5.3.5. Paper and Pulp

- 5.3.6. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Water Automation Solution

- 6. Europe Water Automation and Instrumentation Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Water Automation Solution

- 6.1.1. DCS

- 6.1.2. SCADA

- 6.1.3. PLC

- 6.1.4. HMI

- 6.1.5. Other Water Automation Solutions

- 6.2. Market Analysis, Insights and Forecast - by Water Instrumentation Solution

- 6.2.1. Pressure Transmitter

- 6.2.2. Level Transmitter

- 6.2.3. Temperature Transmitter

- 6.2.4. Liquid Analyzers

- 6.2.5. Gas Analyzers

- 6.2.6. Leakage Detection Systems

- 6.2.7. Flow Sensors/Transmitters

- 6.2.8. Other Water Instrumentation Solutions

- 6.3. Market Analysis, Insights and Forecast - by End-User Industry (Qualitative Analysis)

- 6.3.1. Chemical

- 6.3.2. Manufacturing

- 6.3.3. Food and Beverages

- 6.3.4. Utilities

- 6.3.5. Paper and Pulp

- 6.3.6. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Water Automation Solution

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Emerson Electric

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 ABB Group

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 NALCO

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Phoenix Contact

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Rockwell Automation Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Endress + Hauser Pvt Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Yokogawa Electric Corporation

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 GE Corporation

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Mitsubishi Motors Corporation

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Eurotek India

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 KROHNE LT

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 MJK Automation

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Siemens AG

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Schneider Electric SE

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.1 Emerson Electric

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Water Automation and Instrumentation Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Water Automation and Instrumentation Market Share (%) by Company 2025

List of Tables

- Table 1: Europe Water Automation and Instrumentation Market Revenue billion Forecast, by Water Automation Solution 2020 & 2033

- Table 2: Europe Water Automation and Instrumentation Market Volume K Unit Forecast, by Water Automation Solution 2020 & 2033

- Table 3: Europe Water Automation and Instrumentation Market Revenue billion Forecast, by Water Instrumentation Solution 2020 & 2033

- Table 4: Europe Water Automation and Instrumentation Market Volume K Unit Forecast, by Water Instrumentation Solution 2020 & 2033

- Table 5: Europe Water Automation and Instrumentation Market Revenue billion Forecast, by End-User Industry (Qualitative Analysis) 2020 & 2033

- Table 6: Europe Water Automation and Instrumentation Market Volume K Unit Forecast, by End-User Industry (Qualitative Analysis) 2020 & 2033

- Table 7: Europe Water Automation and Instrumentation Market Revenue billion Forecast, by Region 2020 & 2033

- Table 8: Europe Water Automation and Instrumentation Market Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: Europe Water Automation and Instrumentation Market Revenue billion Forecast, by Water Automation Solution 2020 & 2033

- Table 10: Europe Water Automation and Instrumentation Market Volume K Unit Forecast, by Water Automation Solution 2020 & 2033

- Table 11: Europe Water Automation and Instrumentation Market Revenue billion Forecast, by Water Instrumentation Solution 2020 & 2033

- Table 12: Europe Water Automation and Instrumentation Market Volume K Unit Forecast, by Water Instrumentation Solution 2020 & 2033

- Table 13: Europe Water Automation and Instrumentation Market Revenue billion Forecast, by End-User Industry (Qualitative Analysis) 2020 & 2033

- Table 14: Europe Water Automation and Instrumentation Market Volume K Unit Forecast, by End-User Industry (Qualitative Analysis) 2020 & 2033

- Table 15: Europe Water Automation and Instrumentation Market Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Europe Water Automation and Instrumentation Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: United Kingdom Europe Water Automation and Instrumentation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: United Kingdom Europe Water Automation and Instrumentation Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Germany Europe Water Automation and Instrumentation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Europe Water Automation and Instrumentation Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: France Europe Water Automation and Instrumentation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: France Europe Water Automation and Instrumentation Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: Italy Europe Water Automation and Instrumentation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Italy Europe Water Automation and Instrumentation Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 25: Spain Europe Water Automation and Instrumentation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Spain Europe Water Automation and Instrumentation Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: Netherlands Europe Water Automation and Instrumentation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Netherlands Europe Water Automation and Instrumentation Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 29: Belgium Europe Water Automation and Instrumentation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Belgium Europe Water Automation and Instrumentation Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: Sweden Europe Water Automation and Instrumentation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Sweden Europe Water Automation and Instrumentation Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: Norway Europe Water Automation and Instrumentation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Norway Europe Water Automation and Instrumentation Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: Poland Europe Water Automation and Instrumentation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Poland Europe Water Automation and Instrumentation Market Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Denmark Europe Water Automation and Instrumentation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Denmark Europe Water Automation and Instrumentation Market Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Water Automation and Instrumentation Market?

The projected CAGR is approximately 8.1%.

2. Which companies are prominent players in the Europe Water Automation and Instrumentation Market?

Key companies in the market include Emerson Electric, ABB Group, NALCO, Phoenix Contact, Rockwell Automation Inc, Endress + Hauser Pvt Ltd, Yokogawa Electric Corporation, GE Corporation, Mitsubishi Motors Corporation, Eurotek India, KROHNE LT, MJK Automation, Siemens AG, Schneider Electric SE.

3. What are the main segments of the Europe Water Automation and Instrumentation Market?

The market segments include Water Automation Solution, Water Instrumentation Solution, End-User Industry (Qualitative Analysis).

4. Can you provide details about the market size?

The market size is estimated to be USD 25.71 billion as of 2022.

5. What are some drivers contributing to market growth?

Government Regulation to Save Water Resources and Energy; Increase in Adoption of Smart Water Technologies.

6. What are the notable trends driving market growth?

Demand from Food and Beverage Industry to Witness a Significant Growth Rate.

7. Are there any restraints impacting market growth?

High Investment Cost.

8. Can you provide examples of recent developments in the market?

April 2021 - Veolia has agreed to a deal to buy its rival Suez, ending a fraught takeover battle that merges the world's two largest water and wastewater companies. The company has agreed on a price of EUR 20.50 per Suez share.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Water Automation and Instrumentation Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Water Automation and Instrumentation Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Water Automation and Instrumentation Market?

To stay informed about further developments, trends, and reports in the Europe Water Automation and Instrumentation Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence