Key Insights

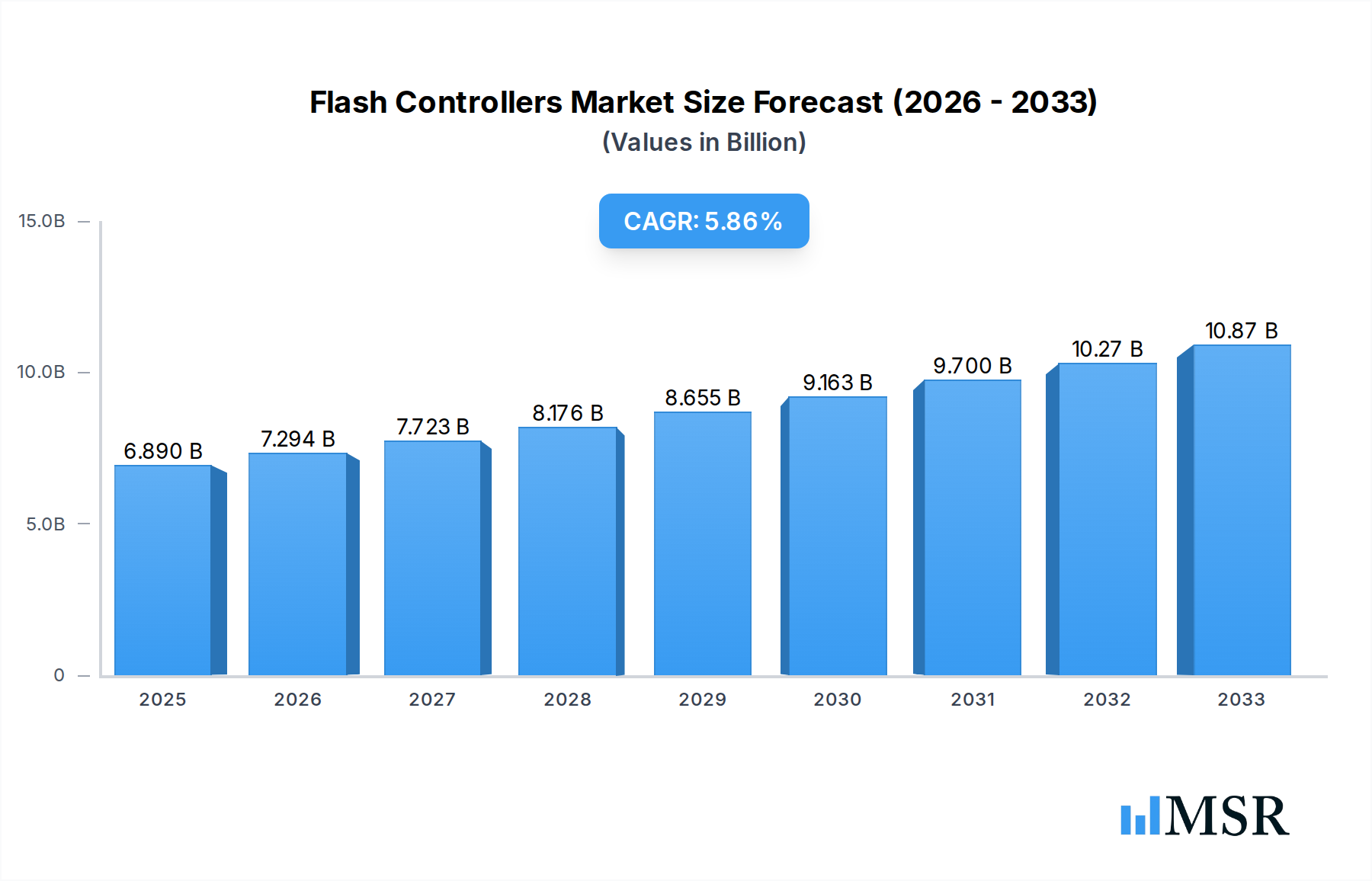

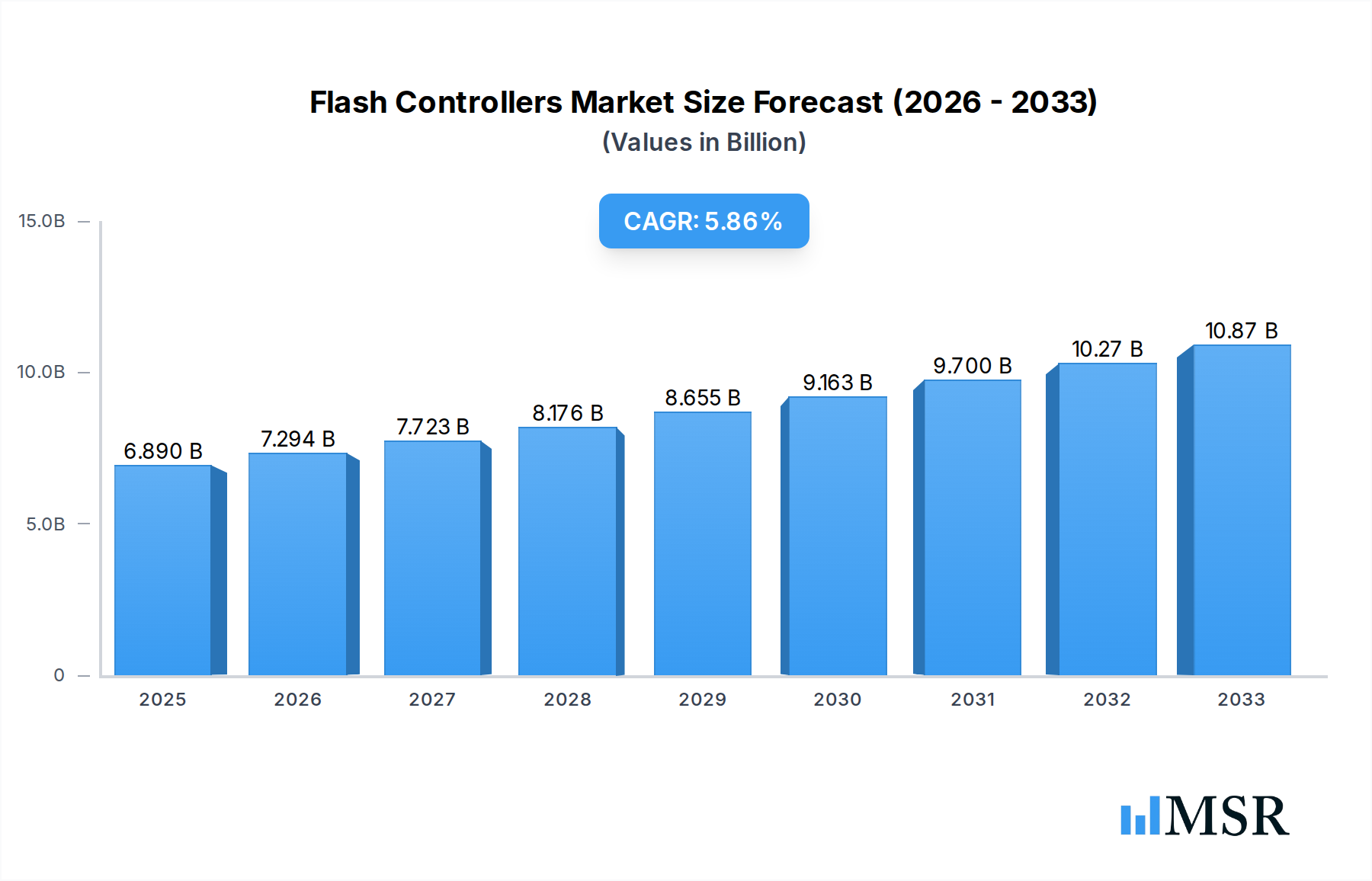

The global Flash Controllers market is poised for robust expansion, driven by the escalating demand for high-speed, high-capacity, and reliable data storage solutions across a myriad of applications. Valued at an estimated $6.89 billion in 2025, the market is projected to grow at a compelling Compound Annual Growth Rate (CAGR) of 5.87% from 2025 to 2033. This significant growth trajectory is primarily fueled by the pervasive digitalization across industries, the explosive growth of connected devices in the Internet of Things (IoT) ecosystem, and the increasing sophistication of automotive electronics, particularly in advanced driver-assistance systems (ADAS) and in-car infotainment. Furthermore, the relentless demand for faster data processing and storage in consumer electronics like smartphones, laptops, and gaming consoles, alongside the expanding requirements from cloud computing and industrial automation sectors, are major contributors to this upward trend. The market sees strong innovation in various types of controllers, including SD & eMMC, USB, SATA, and PCIe controllers, catering to diverse performance and interface needs.

Flash Controllers Market Size (In Billion)

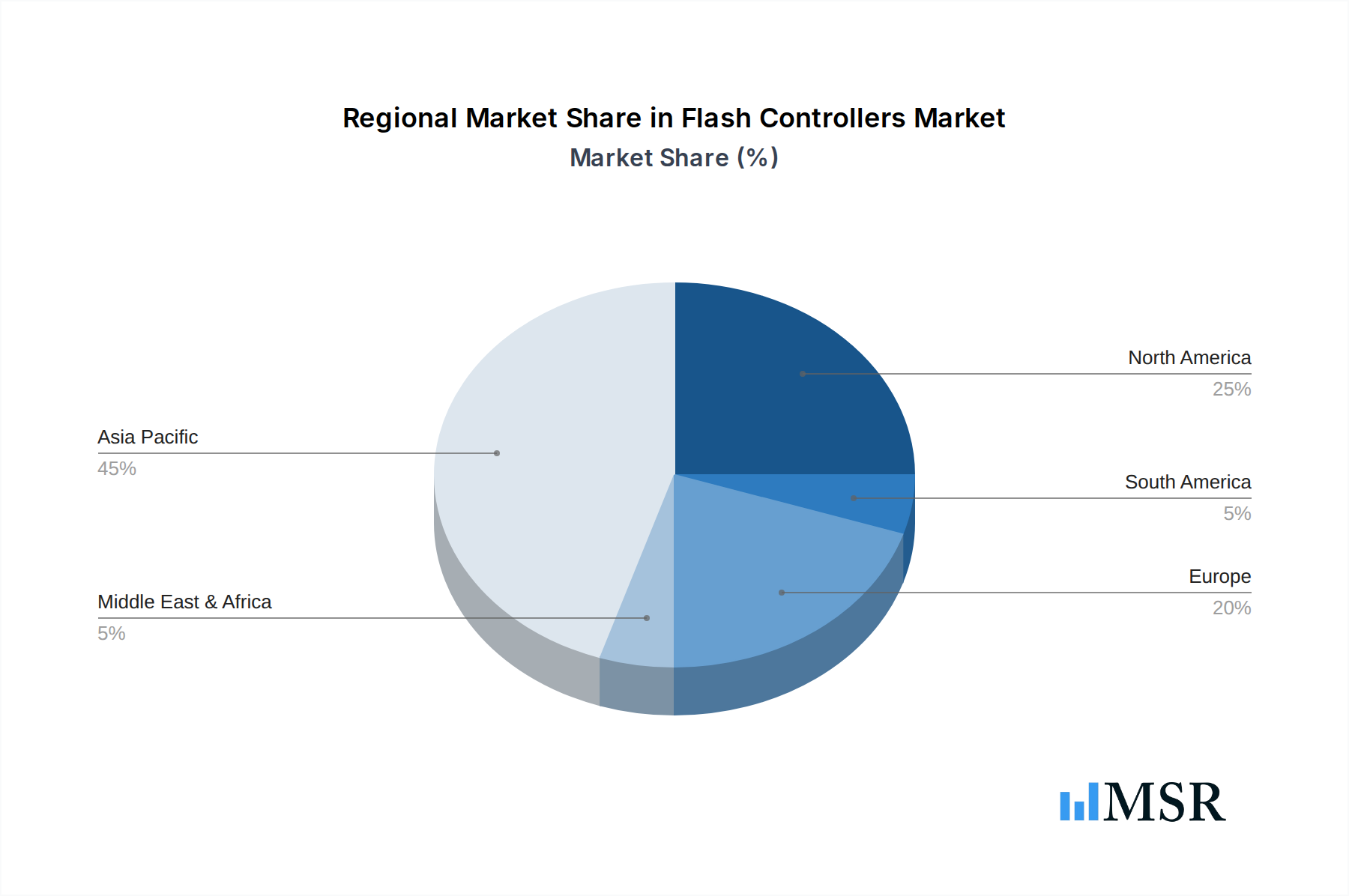

Key market trends include the continuous evolution of flash memory technologies, such as 3D NAND and QLC NAND, which necessitate more advanced and intelligent controllers to manage data integrity, endurance, and performance efficiently. There is a growing emphasis on high-performance interfaces, with a significant shift towards PCIe Gen4 and Gen5 controllers to meet the demanding speeds of next-generation SSDs and enterprise storage. Moreover, the integration of enhanced security features, robust error correction algorithms, and power-efficient designs are becoming paramount, especially for edge computing and automotive applications. Despite intense market competition and the rapid pace of technological obsolescence, leading players like Marvell, Silicon Motion, Phison, Realtek, JMicron, Hyperstone, Greenliant, InnoGrit, Sage Microelectronics Corp, and Maxio are continuously investing in R&D to deliver innovative flash controller solutions. Geographically, Asia Pacific is expected to maintain its dominance, propelled by its robust manufacturing base and burgeoning consumer electronics market, while North America and Europe demonstrate strong adoption in enterprise and automotive sectors.

Flash Controllers Company Market Share

Flash Controllers Market: Unlocking Future Storage Performance

Unleash unparalleled insights into the dynamic Flash Controllers Market with our definitive research report, meticulously crafted for industry leaders, investors, and technology strategists. This comprehensive study delves deep into the core of NAND Controllers, SSD Controllers, and Embedded Controllers, revealing critical trends shaping the future of data storage solutions. From high-performance storage for enterprise applications to low-power controllers for IoT devices, we provide an exhaustive analysis of the technological advancements and market forces at play.

Gain a strategic edge by understanding the intricate landscape of Flash Controllers, including key players like Marvell, Silicon Motion, Phison, and Realtek. Our report offers a granular examination of market segmentation across crucial applications such as Consumer Electronics, Internet of Things (IoT), Automotive, Industrial Automation, and Communication Application, alongside controller types including SD & eMMC Controllers, USB Controllers, CF Controllers, SATA Controllers, and PCIe Controllers.

Spanning a Study Period from 2019 to 2033, with a Base Year of 2025 and a Forecast Period extending to 2033, this report provides robust historical data (2019-2024) and forward-looking projections. Discover detailed market share analysis, growth drivers, technological disruptions, and emerging opportunities that will redefine the Flash Controllers ecosystem. Navigate regulatory frameworks, evaluate competitive pressures, and identify strategic growth accelerators to capitalize on a market projected to reach hundreds of billions of dollars. This is more than a report; it's your strategic roadmap to success in the evolving world of flash memory.

Flash Controllers Market Concentration & Dynamics

The Flash Controllers market exhibits a moderate to high level of concentration, with a few dominant players holding significant sway, particularly in high-growth segments like PCIe SSD controllers. Companies such as Silicon Motion, Phison, and Marvell command substantial market share, collectively exceeding xx billion dollars in annual revenue for flash controller shipments. This concentration is a result of decades of intellectual property development, intricate supply chain management, and deep partnerships with NAND flash manufacturers. Smaller, specialized firms and emerging players like InnoGrit and Sage Microelectronics Corp are carving out niches through innovative architectures and solutions for specific applications, contributing to a dynamic innovation ecosystem where continuous R&D is paramount. The average R&D expenditure for leading players often surpasses xx billion dollars annually, emphasizing the race for performance and power efficiency.

Regulatory frameworks, particularly those related to data security, privacy, and environmental standards (like WEEE and RoHS), are increasingly impacting controller design and manufacturing. Compliance costs and certification processes can be significant barriers to entry for new competitors. The threat of substitute products, while not immediately high for the core function of flash control, comes from evolving memory technologies like MRAM or RRAM, which could eventually reduce the reliance on traditional NAND and, by extension, current flash controller designs. However, the maturity and cost-effectiveness of NAND flash ensure its dominance for the foreseeable future.

End-user trends are rapidly shaping demand. The relentless pursuit of higher data throughput and lower latency in data centers and enterprise storage is driving the adoption of PCIe Gen5 and Gen6 controllers. Meanwhile, the proliferation of IoT devices and edge computing demands ultra-low power consumption and robust embedded controllers. The automotive sector, with its stringent reliability and extended temperature requirements, represents a burgeoning opportunity, pushing controller innovation in endurance and functional safety. Mergers and acquisitions (M&A) are a constant feature of this landscape, driven by the need to acquire new IP, expand market reach, or consolidate competitive positions. Over the historical period (2019-2024), there were an estimated xx M&A deals involving controller technology or related firms, with a cumulative deal value exceeding xx billion dollars, signifying strategic maneuvers to enhance technological capabilities and secure market leadership. These activities are crucial for companies to remain competitive and adapt to the fast-evolving memory and storage landscape.

Flash Controllers Industry Insights & Trends

The Flash Controllers industry is experiencing unprecedented growth, fueled by the insatiable global demand for data storage across virtually every sector. The market size, valued at an estimated xx billion dollars in 2025, is projected to expand significantly, demonstrating a robust Compound Annual Growth Rate (CAGR) of xx% over the forecast period of 2025-2033. This impressive trajectory is primarily driven by several pivotal factors. The exponential growth of data generated by digital transformation initiatives, cloud computing, artificial intelligence (AI), and machine learning (ML) applications necessitates increasingly sophisticated and efficient storage solutions. Flash controllers are at the heart of these solutions, managing the complex interactions between host systems and NAND flash memory to deliver high performance, reliability, and endurance.

Technological disruptions are constantly reshaping the flash controller landscape. The transition from SATA to PCIe interfaces, especially with the widespread adoption of PCIe Gen4 and the emergence of Gen5, has fundamentally altered performance expectations, delivering gigabytes per second of throughput and drastically reducing latency. This shift demands controllers with advanced error correction codes (ECC), sophisticated wear-leveling algorithms, and optimized firmware to maximize the lifespan and performance of denser QLC and PLC NAND flash. Furthermore, the integration of AI capabilities within controllers for predictive maintenance, intelligent data placement, and enhanced security is becoming a critical differentiator. Innovations in power management are also crucial, particularly for battery-powered devices in the IoT and mobile segments, where extending battery life without compromising performance is a key design goal.

Evolving consumer behaviors play a significant role in market expansion. The demand for instantaneous access to content, high-resolution media consumption, and real-time gaming on mobile devices and PCs drives the need for faster, more reliable embedded storage. The proliferation of smart homes, wearable technology, and connected vehicles creates a vast ecosystem of edge devices, each requiring efficient and robust flash storage managed by intelligent controllers. In the enterprise segment, the move towards disaggregated storage architectures and composable infrastructure, driven by hyperscale cloud providers and large enterprises, places immense pressure on controllers to support greater scalability, flexibility, and virtualization. Moreover, the increasing focus on data security mandates advanced encryption and secure boot functionalities integrated directly into the controller hardware, addressing growing concerns over cyber threats and data breaches. These intertwined trends collectively underscore the critical and evolving role of flash controllers as the intelligence layer for all forms of non-volatile storage.

Key Markets & Segments Leading Flash Controllers

Among the various application segments, Consumer Electronics currently dominates the Flash Controllers market, accounting for an estimated xx billion dollars in market value in 2025. This segment's leading position is primarily driven by the sheer volume of smartphones, tablets, laptops, and gaming consoles shipped globally each year. The continuous innovation in these devices, pushing for thinner designs, faster application loading, and seamless multimedia experiences, directly translates into a soaring demand for advanced SD & eMMC and PCIe controllers. Economic growth in developing regions, coupled with increasing disposable incomes, fuels the widespread adoption of these personal electronic devices, creating a massive installed base that requires flash memory. Infrastructure development, particularly in mobile broadband (5G) networks, further accelerates the demand for devices capable of handling larger data volumes, which in turn necessitates high-performance flash controllers.

- Drivers for Consumer Electronics Dominance:

- High Volume Shipments: Billions of smartphones, tablets, and laptops sold annually.

- Performance Demands: Consumers expect faster boot-up, quicker app loading, and seamless multitasking.

- Multimedia Consumption: Storage for high-resolution photos, videos, and gaming.

- Economic Growth: Rising disposable incomes globally, particularly in emerging economies.

- 5G Rollout: Increased data consumption and need for faster on-device storage.

Following Consumer Electronics, the Internet of Things (IoT) and Automotive segments are emerging as significant growth engines. IoT devices, ranging from smart sensors and industrial gateways to connected home appliances, require reliable, low-power, and often rugged flash controllers for embedded storage. The proliferation of billions of IoT endpoints creates a vast, fragmented, but rapidly expanding market for specialized embedded controllers. Similarly, the automotive sector is undergoing a profound transformation with the advent of advanced driver-assistance systems (ADAS), in-vehicle infotainment (IVI), and autonomous driving. These applications demand extremely high-endurance, high-reliability, and secure flash storage, primarily using PCIe and eMMC controllers, capable of operating in harsh environments and enduring billions of write cycles over a vehicle's lifespan. The increasing complexity of software and data logging in modern vehicles ensures a sustained and growing demand for automotive-grade flash controllers.

In terms of Type, PCIe Controllers are rapidly gaining prominence and are expected to be the fastest-growing segment, closely challenging the established dominance of SD & eMMC controllers. The enterprise and client SSD markets are almost entirely transitioning to PCIe-based NVMe interfaces due to their superior bandwidth and lower latency compared to SATA. Data centers, cloud computing environments, and high-performance computing (HPC) heavily rely on PCIe controllers to manage vast amounts of data at unparalleled speeds. While SD & eMMC Controllers will continue to hold a significant market share, especially in consumer and embedded devices where cost and power efficiency are paramount, the future growth trajectory is undeniably skewed towards PCIe for high-performance and enterprise-grade applications, driving innovation in controller architectures, firmware, and error correction technologies to handle the ever-increasing density and complexity of NAND flash.

Flash Controllers Product Developments

Recent product developments in Flash Controllers are primarily focused on pushing the boundaries of speed, efficiency, and reliability. Innovators like Marvell and Silicon Motion are leading the charge with next-generation PCIe Gen5 and even Gen6 NVMe controllers, designed to leverage the full potential of advanced NAND flash, offering sequential read/write speeds exceeding 14 gigabytes per second for enterprise and high-end consumer SSDs. These controllers integrate sophisticated error correction algorithms, such as LDPC (Low-Density Parity-Check), to extend the lifespan of increasingly dense QLC and PLC NAND. Another key area of innovation is the development of power-efficient controllers for IoT and edge computing, featuring lower core voltages and advanced power management states to maximize battery life in billions of connected devices. Furthermore, hardware-level encryption (e.g., AES 256-bit) and secure boot functionalities are becoming standard, enhancing data security and establishing a competitive edge in critical applications like automotive and industrial automation.

Challenges in the Flash Controllers Market

The Flash Controllers market faces several significant challenges. Regulatory hurdles, particularly around data privacy (e.g., GDPR, CCPA) and security standards, necessitate complex hardware and firmware designs, increasing development costs by an estimated xx billion dollars annually for leading players. Supply chain issues, exacerbated by geopolitical tensions and global events, lead to volatility in component availability (e.g., specific process nodes for controller ASICs) and can delay product launches by several months, impacting revenue by potentially billions of dollars. Intense competitive pressures force companies into aggressive pricing strategies, shrinking profit margins despite significant R&D investments. The rapid evolution of NAND flash technology, with increasing layers and new cell types, also demands constant controller redesign and validation, adding to development complexity and time-to-market pressures. Furthermore, managing the performance and endurance of denser NAND flash without compromising reliability remains a core technical hurdle for controller manufacturers.

Forces Driving Flash Controllers Growth

Several powerful forces are propelling the growth of the Flash Controllers market. Technologically, the relentless demand for faster storage in data centers, driven by AI, big data analytics, and cloud computing, is a primary catalyst, pushing the adoption of high-performance PCIe NVMe controllers. The widespread rollout of 5G networks is fueling the need for faster storage in edge devices and smartphones, directly boosting demand for eMMC and client PCIe controllers. Economically, the increasing affordability of NAND flash memory allows for greater storage capacities across all device categories, making SSDs and embedded flash storage more accessible to billions of consumers and enterprises. The digital transformation across industries, from healthcare to manufacturing, creates a massive wave of data generation, requiring robust and efficient flash storage solutions. Regulatory factors, such as government initiatives promoting digital infrastructure and data localization policies, indirectly stimulate the demand for local data storage, consequently increasing the need for flash controllers. The continued innovation in NAND flash technology itself, offering higher densities and lower costs, creates a perpetual need for advanced controllers to manage these complex memories effectively.

Long-Term Growth Catalysts in the Flash Controllers Market

The long-term growth of the Flash Controllers market is primarily catalyzed by a continuous wave of innovation in memory technology and interface standards. The progression towards higher PCIe generations (Gen6 and beyond) will unlock unprecedented data transfer speeds, necessitating entirely new controller architectures capable of handling terabytes per second of throughput. Strategic partnerships between controller manufacturers and NAND flash producers are crucial for co-developing optimized solutions that maximize the performance and longevity of next-generation flash, such as PLC (Penta-Level Cell) NAND. Market expansions into niche but high-value sectors, like automotive and industrial automation, where robust, long-life, and secure storage is paramount, will drive specialized controller development. Furthermore, the integration of advanced AI and machine learning directly into controller firmware for intelligent data management, predictive failure analysis, and enhanced security will be a significant differentiator, creating new revenue streams and extending the controllers' value proposition beyond basic data transfer, fostering sustained market growth over the next decade.

Emerging Opportunities in Flash Controllers

Emerging opportunities in the Flash Controllers market are abundant, driven by evolving technological landscapes and new application frontiers. One significant trend is the rise of computational storage drives (CSD), where flash controllers integrate processing capabilities to offload tasks from the host CPU, accelerating data-intensive workloads directly within the storage device. This presents a new market segment for highly intelligent controllers. Another opportunity lies in the burgeoning edge AI market, where billions of edge devices require compact, low-power, and secure embedded flash storage with controllers optimized for real-time inference and data logging. The expanding use of flash storage in AI training and inference servers also offers a lucrative avenue for high-performance, low-latency PCIe controllers specifically designed for large-scale parallel data access. Furthermore, the increasing focus on cybersecurity in storage will drive demand for controllers with advanced hardware-based security features, including quantum-resistant encryption and tamper detection, creating new market segments and competitive advantages for secure flash controller solutions.

Leading Players in the Flash Controllers Sector

- Marvell

- Silicon Motion

- Phison

- Realtek

- JMicron

- Hyperstone

- Greenliant

- InnoGrit

- Sage Microelectronics Corp

- Maxio

Key Milestones in Flash Controllers Industry

- Q3 2019: Adoption of PCIe Gen4 NVMe controllers gains significant traction in enterprise and high-end client SSDs, marking a major performance leap from Gen3.

- Q1 2020: Introduction of controllers optimized for 1xx-layer 3D NAND flash, improving density and cost-effectiveness for SSDs and embedded storage.

- Q4 2020: Launch of automotive-grade flash controllers with extended temperature ranges and enhanced reliability features, addressing stringent demands of ADAS and infotainment systems.

- Q2 2021: Major controller manufacturers begin shipping samples of PCIe Gen5 controllers, setting the stage for next-generation data center and enthusiast platforms.

- Q3 2022: Integration of advanced machine learning algorithms into controller firmware for improved wear-leveling and predictive maintenance, extending SSD lifespan.

- Q1 2023: Release of ultra-low-power flash controllers specifically designed for new generations of IoT devices and wearables, optimizing battery life.

- Q4 2023: Announcement of flash controllers with hardware-level support for CXL (Compute Express Link), enabling memory-semantic storage for next-gen servers.

- Q2 2024: Commercial availability of controllers fully compatible with 2xx-layer QLC NAND, driving down cost per gigabyte for high-capacity storage.

Strategic Outlook for Flash Controllers Market

The strategic outlook for the Flash Controllers market points towards sustained, robust growth driven by an accelerating digital economy. Key growth accelerators include the pervasive expansion of cloud infrastructure, the exponential rise of AI and machine learning workloads, and the continued proliferation of IoT and edge computing devices, all demanding more performant and intelligent storage. Strategic opportunities lie in the development of highly specialized controllers for emerging applications like computational storage, in-memory computing, and automotive-grade solutions that meet stringent safety and reliability standards. Companies that invest heavily in advanced R&D for next-generation PCIe standards, integrated AI capabilities, and robust security features within their controllers will capture significant market share. Forming strategic partnerships with NAND flash manufacturers and system integrators will be crucial for co-innovation and ensuring optimal compatibility, paving the way for controllers to unlock the full potential of future flash memory technologies and solidify their indispensable role in the global data ecosystem.

Flash Controllers Segmentation

-

1. Application

- 1.1. Consumer Electronics

- 1.2. Internet of Things

- 1.3. Automotive

- 1.4. Industrial Automation

- 1.5. Communication Application

- 1.6. Others

-

2. Type

- 2.1. SD & eMMC Controllers

- 2.2. USB Controllers

- 2.3. CF Controllers

- 2.4. SATA Controllers

- 2.5. PCIe Controllers

Flash Controllers Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Flash Controllers Regional Market Share

Geographic Coverage of Flash Controllers

Flash Controllers REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.87% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Consumer Electronics

- 5.1.2. Internet of Things

- 5.1.3. Automotive

- 5.1.4. Industrial Automation

- 5.1.5. Communication Application

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. SD & eMMC Controllers

- 5.2.2. USB Controllers

- 5.2.3. CF Controllers

- 5.2.4. SATA Controllers

- 5.2.5. PCIe Controllers

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Flash Controllers Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Consumer Electronics

- 6.1.2. Internet of Things

- 6.1.3. Automotive

- 6.1.4. Industrial Automation

- 6.1.5. Communication Application

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. SD & eMMC Controllers

- 6.2.2. USB Controllers

- 6.2.3. CF Controllers

- 6.2.4. SATA Controllers

- 6.2.5. PCIe Controllers

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Flash Controllers Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Consumer Electronics

- 7.1.2. Internet of Things

- 7.1.3. Automotive

- 7.1.4. Industrial Automation

- 7.1.5. Communication Application

- 7.1.6. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. SD & eMMC Controllers

- 7.2.2. USB Controllers

- 7.2.3. CF Controllers

- 7.2.4. SATA Controllers

- 7.2.5. PCIe Controllers

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Flash Controllers Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Consumer Electronics

- 8.1.2. Internet of Things

- 8.1.3. Automotive

- 8.1.4. Industrial Automation

- 8.1.5. Communication Application

- 8.1.6. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. SD & eMMC Controllers

- 8.2.2. USB Controllers

- 8.2.3. CF Controllers

- 8.2.4. SATA Controllers

- 8.2.5. PCIe Controllers

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Flash Controllers Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Consumer Electronics

- 9.1.2. Internet of Things

- 9.1.3. Automotive

- 9.1.4. Industrial Automation

- 9.1.5. Communication Application

- 9.1.6. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. SD & eMMC Controllers

- 9.2.2. USB Controllers

- 9.2.3. CF Controllers

- 9.2.4. SATA Controllers

- 9.2.5. PCIe Controllers

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Flash Controllers Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Consumer Electronics

- 10.1.2. Internet of Things

- 10.1.3. Automotive

- 10.1.4. Industrial Automation

- 10.1.5. Communication Application

- 10.1.6. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. SD & eMMC Controllers

- 10.2.2. USB Controllers

- 10.2.3. CF Controllers

- 10.2.4. SATA Controllers

- 10.2.5. PCIe Controllers

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Flash Controllers Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Consumer Electronics

- 11.1.2. Internet of Things

- 11.1.3. Automotive

- 11.1.4. Industrial Automation

- 11.1.5. Communication Application

- 11.1.6. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. SD & eMMC Controllers

- 11.2.2. USB Controllers

- 11.2.3. CF Controllers

- 11.2.4. SATA Controllers

- 11.2.5. PCIe Controllers

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Marvell

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Silicon Motion

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Phison

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Realtek

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 JMicron

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Hyperstone

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Greenliant

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 InnoGrit

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Sage Microelectronics Corp

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Maxio

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Marvell

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Flash Controllers Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Flash Controllers Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Flash Controllers Revenue (billion), by Application 2025 & 2033

- Figure 4: North America Flash Controllers Volume (K), by Application 2025 & 2033

- Figure 5: North America Flash Controllers Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Flash Controllers Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Flash Controllers Revenue (billion), by Type 2025 & 2033

- Figure 8: North America Flash Controllers Volume (K), by Type 2025 & 2033

- Figure 9: North America Flash Controllers Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Flash Controllers Volume Share (%), by Type 2025 & 2033

- Figure 11: North America Flash Controllers Revenue (billion), by Country 2025 & 2033

- Figure 12: North America Flash Controllers Volume (K), by Country 2025 & 2033

- Figure 13: North America Flash Controllers Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Flash Controllers Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Flash Controllers Revenue (billion), by Application 2025 & 2033

- Figure 16: South America Flash Controllers Volume (K), by Application 2025 & 2033

- Figure 17: South America Flash Controllers Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Flash Controllers Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Flash Controllers Revenue (billion), by Type 2025 & 2033

- Figure 20: South America Flash Controllers Volume (K), by Type 2025 & 2033

- Figure 21: South America Flash Controllers Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America Flash Controllers Volume Share (%), by Type 2025 & 2033

- Figure 23: South America Flash Controllers Revenue (billion), by Country 2025 & 2033

- Figure 24: South America Flash Controllers Volume (K), by Country 2025 & 2033

- Figure 25: South America Flash Controllers Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Flash Controllers Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Flash Controllers Revenue (billion), by Application 2025 & 2033

- Figure 28: Europe Flash Controllers Volume (K), by Application 2025 & 2033

- Figure 29: Europe Flash Controllers Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Flash Controllers Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Flash Controllers Revenue (billion), by Type 2025 & 2033

- Figure 32: Europe Flash Controllers Volume (K), by Type 2025 & 2033

- Figure 33: Europe Flash Controllers Revenue Share (%), by Type 2025 & 2033

- Figure 34: Europe Flash Controllers Volume Share (%), by Type 2025 & 2033

- Figure 35: Europe Flash Controllers Revenue (billion), by Country 2025 & 2033

- Figure 36: Europe Flash Controllers Volume (K), by Country 2025 & 2033

- Figure 37: Europe Flash Controllers Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Flash Controllers Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Flash Controllers Revenue (billion), by Application 2025 & 2033

- Figure 40: Middle East & Africa Flash Controllers Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Flash Controllers Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Flash Controllers Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Flash Controllers Revenue (billion), by Type 2025 & 2033

- Figure 44: Middle East & Africa Flash Controllers Volume (K), by Type 2025 & 2033

- Figure 45: Middle East & Africa Flash Controllers Revenue Share (%), by Type 2025 & 2033

- Figure 46: Middle East & Africa Flash Controllers Volume Share (%), by Type 2025 & 2033

- Figure 47: Middle East & Africa Flash Controllers Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East & Africa Flash Controllers Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Flash Controllers Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Flash Controllers Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Flash Controllers Revenue (billion), by Application 2025 & 2033

- Figure 52: Asia Pacific Flash Controllers Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Flash Controllers Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Flash Controllers Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Flash Controllers Revenue (billion), by Type 2025 & 2033

- Figure 56: Asia Pacific Flash Controllers Volume (K), by Type 2025 & 2033

- Figure 57: Asia Pacific Flash Controllers Revenue Share (%), by Type 2025 & 2033

- Figure 58: Asia Pacific Flash Controllers Volume Share (%), by Type 2025 & 2033

- Figure 59: Asia Pacific Flash Controllers Revenue (billion), by Country 2025 & 2033

- Figure 60: Asia Pacific Flash Controllers Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Flash Controllers Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Flash Controllers Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Flash Controllers Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Flash Controllers Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Flash Controllers Revenue billion Forecast, by Type 2020 & 2033

- Table 4: Global Flash Controllers Volume K Forecast, by Type 2020 & 2033

- Table 5: Global Flash Controllers Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Flash Controllers Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Flash Controllers Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global Flash Controllers Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Flash Controllers Revenue billion Forecast, by Type 2020 & 2033

- Table 10: Global Flash Controllers Volume K Forecast, by Type 2020 & 2033

- Table 11: Global Flash Controllers Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Flash Controllers Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Flash Controllers Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global Flash Controllers Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Flash Controllers Revenue billion Forecast, by Type 2020 & 2033

- Table 22: Global Flash Controllers Volume K Forecast, by Type 2020 & 2033

- Table 23: Global Flash Controllers Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global Flash Controllers Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Brazil Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Argentina Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Flash Controllers Revenue billion Forecast, by Application 2020 & 2033

- Table 32: Global Flash Controllers Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Flash Controllers Revenue billion Forecast, by Type 2020 & 2033

- Table 34: Global Flash Controllers Volume K Forecast, by Type 2020 & 2033

- Table 35: Global Flash Controllers Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global Flash Controllers Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Germany Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: France Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Italy Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Spain Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Russia Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Benelux Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Nordics Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Flash Controllers Revenue billion Forecast, by Application 2020 & 2033

- Table 56: Global Flash Controllers Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Flash Controllers Revenue billion Forecast, by Type 2020 & 2033

- Table 58: Global Flash Controllers Volume K Forecast, by Type 2020 & 2033

- Table 59: Global Flash Controllers Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global Flash Controllers Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Turkey Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Israel Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: GCC Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: North Africa Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: South Africa Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Flash Controllers Revenue billion Forecast, by Application 2020 & 2033

- Table 74: Global Flash Controllers Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Flash Controllers Revenue billion Forecast, by Type 2020 & 2033

- Table 76: Global Flash Controllers Volume K Forecast, by Type 2020 & 2033

- Table 77: Global Flash Controllers Revenue billion Forecast, by Country 2020 & 2033

- Table 78: Global Flash Controllers Volume K Forecast, by Country 2020 & 2033

- Table 79: China Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 80: China Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 82: India Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 84: Japan Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: South Korea Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Oceania Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Flash Controllers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Flash Controllers Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Flash Controllers?

The projected CAGR is approximately 5.87%.

2. Which companies are prominent players in the Flash Controllers?

Key companies in the market include Marvell, Silicon Motion, Phison, Realtek, JMicron, Hyperstone, Greenliant, InnoGrit, Sage Microelectronics Corp, Maxio.

3. What are the main segments of the Flash Controllers?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.89 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Flash Controllers," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Flash Controllers report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Flash Controllers?

To stay informed about further developments, trends, and reports in the Flash Controllers, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence