Key Insights

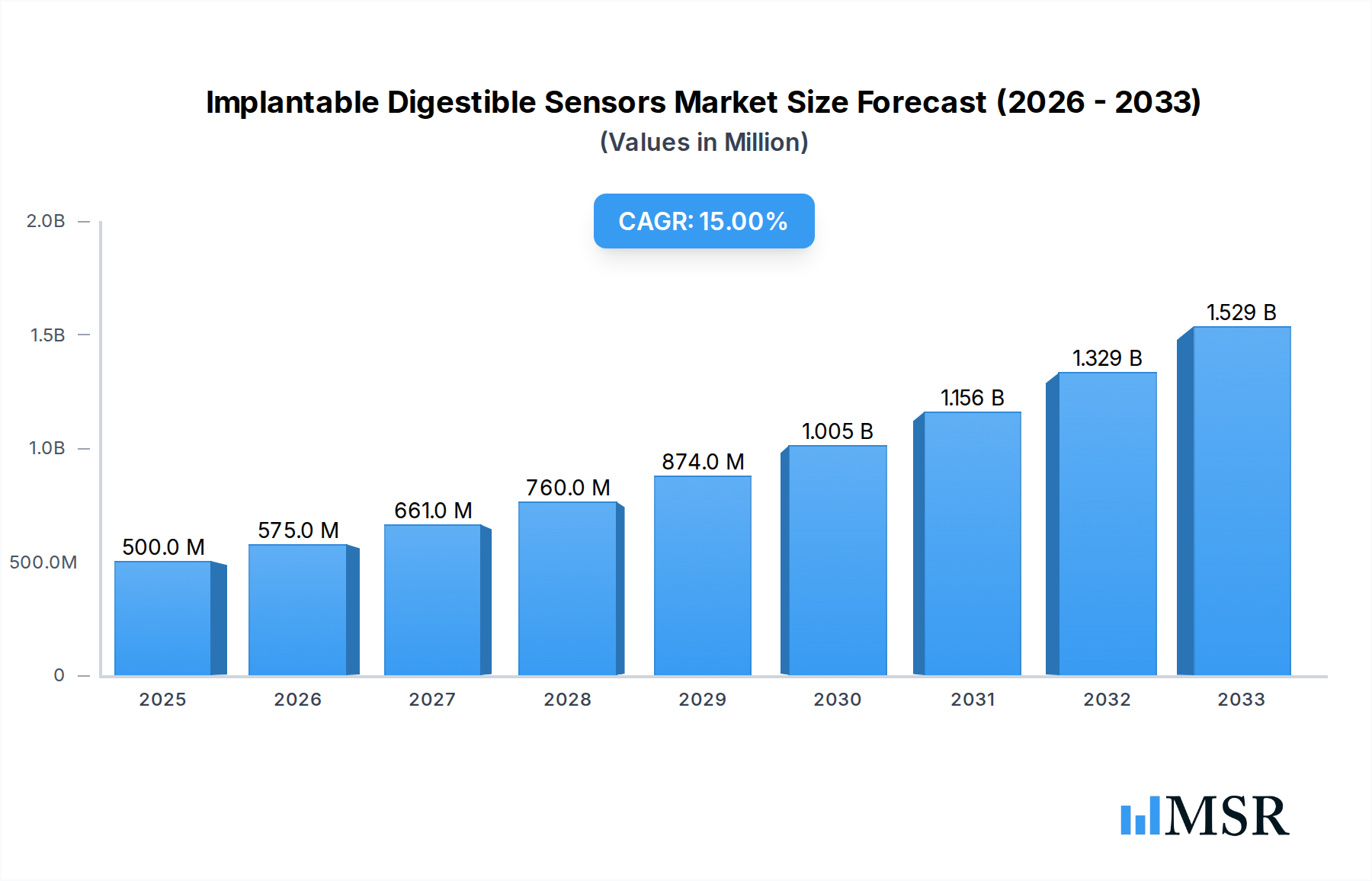

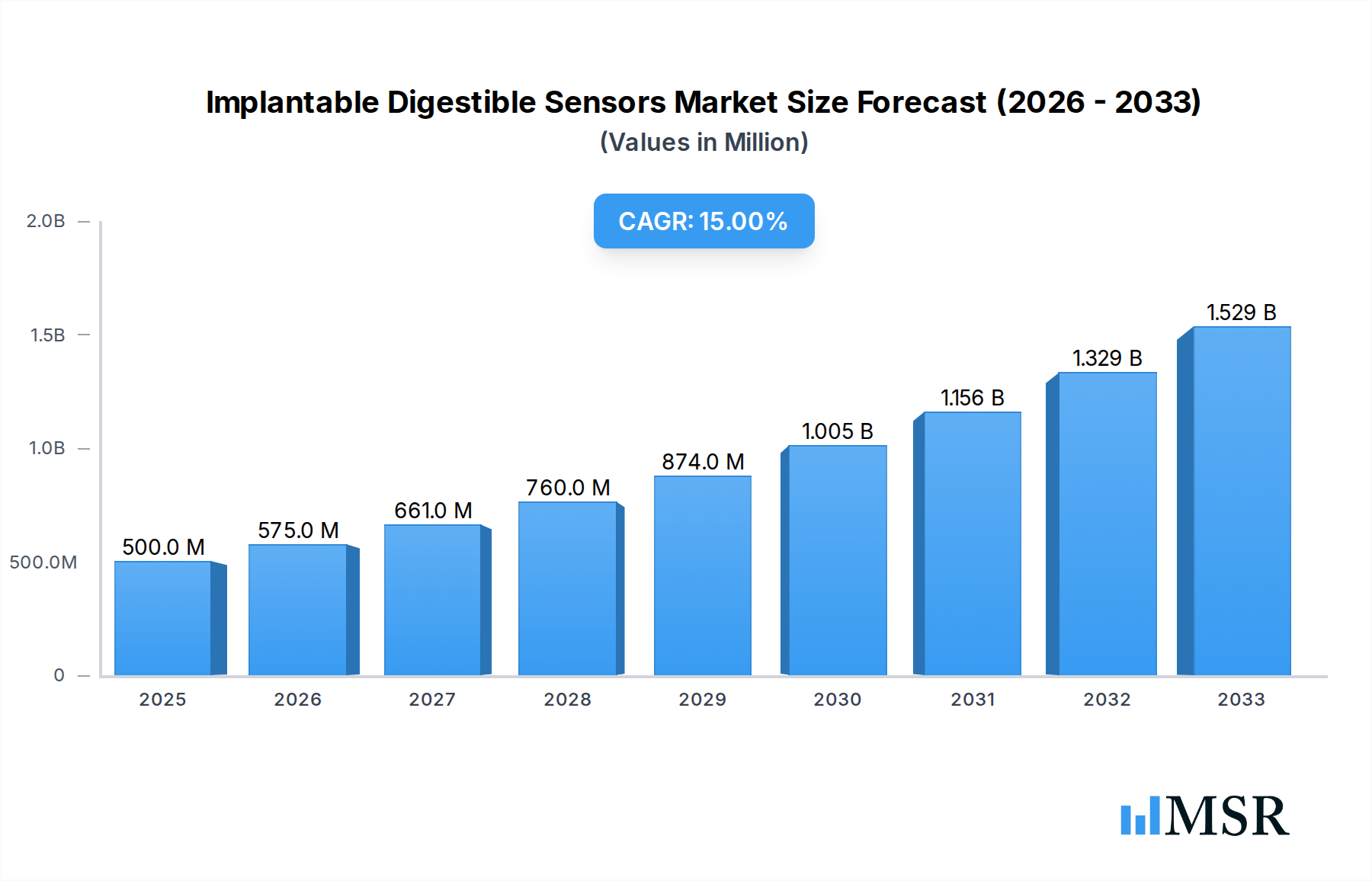

The Implantable Digestible Sensors market is poised for substantial growth, projected to reach $500 million by 2025, with a remarkable Compound Annual Growth Rate (CAGR) of 15% anticipated over the forecast period of 2025-2033. This robust expansion is primarily driven by the increasing prevalence of chronic diseases, the growing demand for personalized medicine, and the continuous advancements in miniaturization and wireless communication technologies. The diagnostic segment is expected to lead the market, fueled by the need for early detection and precise monitoring of various gastrointestinal conditions and systemic diseases. Technological innovation, particularly in image, temperature, and pressure sensing capabilities, is enabling more accurate and less invasive patient monitoring. The growing adoption of remote patient monitoring solutions further bolsters this segment, allowing healthcare providers to track patient health metrics effectively from a distance.

Implantable Digestible Sensors Market Size (In Million)

While the market presents significant opportunities, certain restraints could impact its trajectory. These include the high cost associated with research, development, and manufacturing of these sophisticated devices, as well as regulatory hurdles that may prolong product approval processes. Furthermore, patient and physician acceptance of implantable technologies, alongside concerns regarding data security and privacy, will play a crucial role in market penetration. However, the expanding application of implantable digestible sensors beyond diagnostics into therapeutic applications and the increasing focus on preventative healthcare are expected to counterbalance these challenges. Key players are actively investing in R&D to develop innovative solutions and expand their product portfolios, aiming to capture a significant share of this burgeoning market.

Implantable Digestible Sensors Company Market Share

Implantable Digestible Sensors Market: A Comprehensive 2033 Forecast

This in-depth report delivers a crucial analysis of the implantable digestible sensors market, forecasting its trajectory from 2019 to 2033, with a base year of 2025. Delve into the future of ingestible sensors and gain actionable intelligence on smart pills, diagnostic sensors, and monitoring devices. This research is essential for healthcare technology companies, biotech firms, pharmaceutical manufacturers, and investment firms seeking to understand the evolving landscape of minimally invasive medical diagnostics and therapeutics.

Implantable Digestible Sensors Market Concentration & Dynamics

The implantable digestible sensors market is characterized by a moderate to high level of concentration, driven by the significant R&D investment required for innovation and regulatory approvals. Key players like Medtronic, Sensirion AG, Honeywell International, Inc., TE Connectivity, Koninklijke Philips N.V, General Electric Company, and Proteus Healthcare are actively shaping the competitive environment through strategic acquisitions and internal product development. M&A activities, valued at over $500 million in the historical period (2019-2024), are expected to continue as larger entities seek to integrate advanced digital health solutions. The innovation ecosystem is robust, with a growing number of startups focusing on niche applications within gastrointestinal diagnostics and personalized medicine. Regulatory frameworks, particularly those overseen by the FDA and EMA, are becoming more defined, offering a clearer pathway for market entry but also demanding rigorous safety and efficacy testing. The emergence of smart ingestible devices is influencing end-user trends, with an increasing demand for non-invasive and convenient health monitoring solutions. Substitute products, while currently limited for highly specific internal sensing, are evolving, necessitating continuous innovation.

Implantable Digestible Sensors Industry Insights & Trends

The implantable digestible sensors market is poised for substantial growth, projected to reach an estimated market size of over $15,000 million by 2025 and expand significantly through the forecast period (2025-2033). The Compound Annual Growth Rate (CAGR) is anticipated to exceed 18%, fueled by a confluence of technological advancements, increasing healthcare expenditure, and a growing preference for patient-centric diagnostic solutions. The primary market growth drivers include the escalating prevalence of chronic diseases like inflammatory bowel disease (IBD) and gastrointestinal disorders, demanding continuous and accurate monitoring. Technological disruptions are at the forefront, with advancements in miniaturization, wireless communication protocols, and biodegradable materials enabling more sophisticated and less invasive ingestible sensors. The integration of artificial intelligence (AI) and machine learning (ML) with sensor data is revolutionizing disease management by enabling predictive analytics and personalized treatment plans. Evolving consumer behaviors, particularly the rising awareness and adoption of wearable technology and home-based healthcare solutions, are creating a receptive market for smart pill technology. The development of image technology sensors for internal visualization, alongside temperature technology and pressure technology sensors for precise physiological parameter tracking, are key trends expanding the application scope. The market is also witnessing a surge in research and development for other novel sensing modalities, promising a broader range of diagnostic capabilities.

Key Markets & Segments Leading Implantable Digestible Sensors

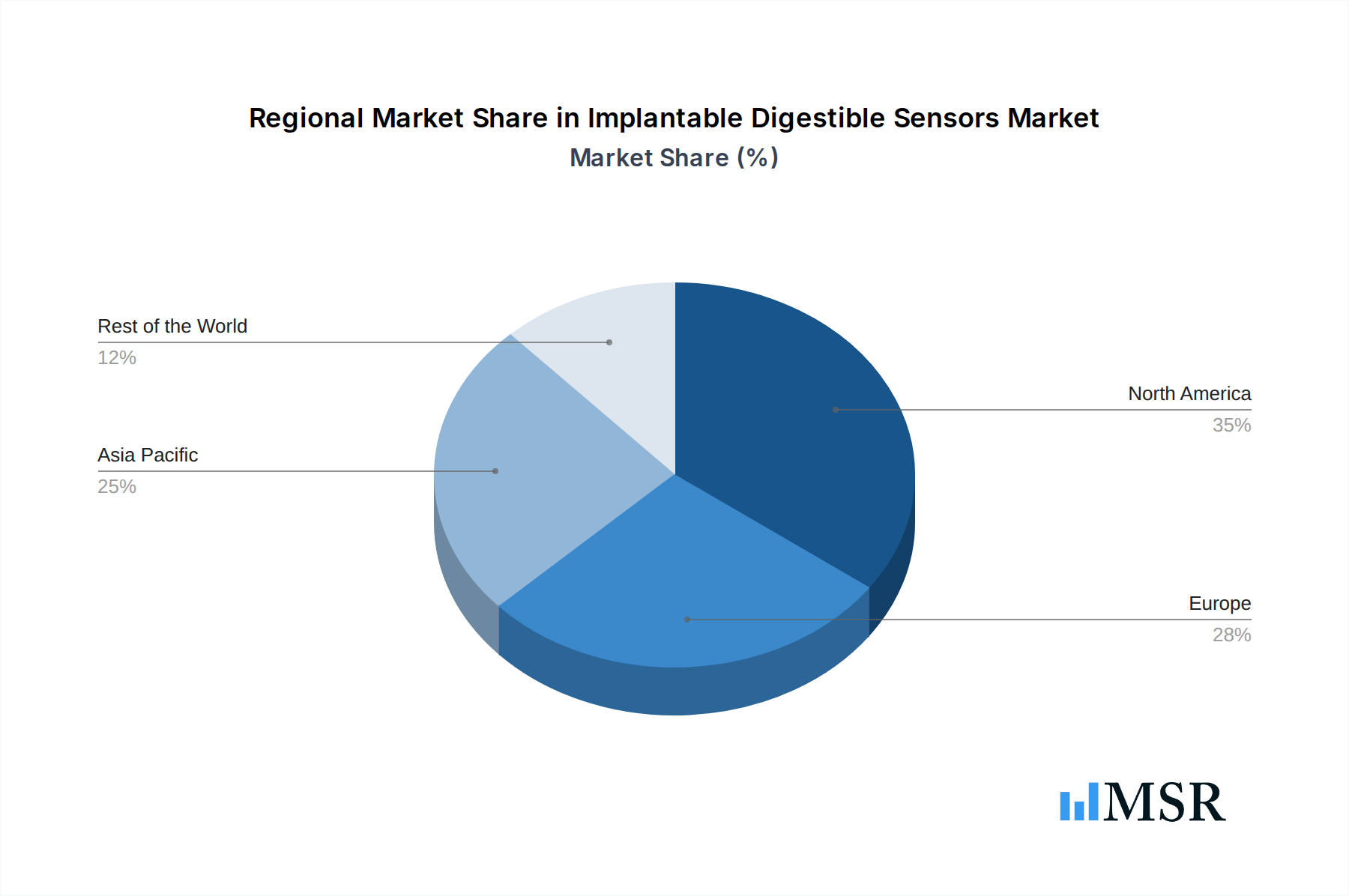

The implantable digestible sensors market is witnessing significant growth across various regions and applications. North America, particularly the United States, is expected to lead the market due to its advanced healthcare infrastructure, substantial R&D investment, and high adoption rates of innovative medical technologies. Economic growth and supportive government initiatives aimed at improving patient outcomes are also key drivers in this region.

Within the Application segment:

- Diagnostics: This segment is projected to dominate the market, driven by the increasing demand for early and accurate detection of gastrointestinal diseases, cancers, and infections. The ability of implantable sensors to provide real-time, in-situ diagnostic data is invaluable for clinicians.

- Drivers: Rising incidence of gastrointestinal cancers, increasing need for precise pathology, advancements in biosensing for disease markers.

- Monitoring: This segment is also experiencing robust growth, particularly for chronic disease management and post-operative patient surveillance. The continuous data stream from monitoring sensors allows for proactive intervention and personalized therapy adjustments.

- Drivers: Growing prevalence of chronic conditions like IBD, need for medication adherence tracking, advancements in remote patient monitoring.

Within the Type segment:

- Temperature Technology: This type of sensor is crucial for detecting fever, inflammation, and monitoring gastrointestinal tract conditions. Its relatively lower cost and straightforward implementation make it a widely adopted technology.

- Drivers: Ubiquitous need for temperature monitoring in various conditions, ease of integration into ingestible devices.

- Pressure Technology: Essential for understanding gastrointestinal motility, detecting blockages, and monitoring conditions like gastroparesis. Advancements in micro-electromechanical systems (MEMS) are enhancing the precision and sensitivity of these sensors.

- Drivers: Critical for diagnosing motility disorders, improving surgical outcomes through pressure mapping.

- Image Technology: While in its nascent stages for ingestible applications, this segment holds immense future potential for internal visualization, polyp detection, and detailed examination of the gastrointestinal lining.

- Drivers: Potential for non-invasive colonoscopy alternatives, early detection of mucosal abnormalities.

- Other: This encompasses a range of emerging technologies, including pH sensors, biochemical sensors for analyzing specific biomarkers, and electrical activity sensors, all contributing to a more comprehensive understanding of gastrointestinal health.

- Drivers: Development of highly specific biosensors, integration of multiple sensing modalities for holistic health assessment.

Implantable Digestible Sensors Product Developments

Product developments in implantable digestible sensors are characterized by increasing miniaturization, enhanced wireless connectivity, and improved biocompatibility. Innovations are focused on creating multi-functional sensors capable of simultaneously measuring temperature, pH, pressure, and even specific biochemical markers, revolutionizing gastrointestinal diagnostics. The integration of these sensors with advanced drug delivery systems is also a significant trend, leading to the development of smart pills that can both diagnose and treat conditions. Companies are emphasizing biodegradable materials to ensure safe and natural excretion, minimizing patient discomfort and risk. These technological advancements provide a significant competitive edge by offering more accurate, convenient, and personalized healthcare solutions.

Challenges in the Implantable Digestible Sensors Market

The implantable digestible sensors market faces several significant challenges that could impede its rapid growth. Regulatory hurdles remain a primary concern, with stringent approval processes from bodies like the FDA demanding extensive clinical trials and safety validation, leading to prolonged development timelines and increased costs, estimated to be in the tens of millions for each successful product. Supply chain complexities for highly specialized components and manufacturing processes can also lead to production bottlenecks and impact cost-effectiveness. Furthermore, patient acceptance and adoption rates, while improving, are still influenced by concerns regarding invasiveness, data security, and the perceived need for such advanced monitoring, potentially limiting initial market penetration by as much as 20%.

Forces Driving Implantable Digestible Sensors Growth

Several powerful forces are propelling the implantable digestible sensors market forward. Technological advancements in miniaturization, wireless communication, and biosensing are enabling the creation of smaller, more capable, and user-friendly devices. The escalating global burden of chronic diseases, particularly gastrointestinal disorders, is creating a substantial demand for effective diagnostic and monitoring solutions. Supportive government initiatives and increasing healthcare expenditure worldwide are fostering an environment conducive to the adoption of innovative medical technologies. Furthermore, the growing trend towards personalized medicine and preventive healthcare aligns perfectly with the capabilities of ingestible sensors, empowering individuals with greater control over their health.

Challenges in the Implantable Digestible Sensors Market

Long-term growth catalysts for the implantable digestible sensors market lie in continued innovation and strategic market expansion. The development of advanced AI-powered analytics to interpret complex sensor data will unlock deeper clinical insights and enhance predictive capabilities. Strategic partnerships between sensor manufacturers, pharmaceutical companies, and healthcare providers will accelerate the integration of these technologies into standard clinical practice. Furthermore, exploring new market segments, such as veterinary applications and remote healthcare in developing regions, presents significant untapped potential. The continuous improvement of sensor accuracy, battery life, and data transmission reliability will further solidify their position as indispensable tools in modern healthcare.

Emerging Opportunities in Implantable Digestible Sensors

Emerging opportunities within the implantable digestible sensors market are diverse and promising. The expansion of remote patient monitoring platforms, especially in underserved areas, offers a significant avenue for growth. The integration of these sensors with advanced digital therapeutics and personalized drug delivery systems creates a new paradigm for chronic disease management. Furthermore, the growing interest in proactive health and wellness tracking presents a substantial market for consumer-grade ingestible sensors. The development of biodegradable and self-dissolving sensors will address safety concerns and enhance patient comfort, paving the way for wider adoption. Exploring applications beyond the gastrointestinal tract, such as esophageal or pharyngeal monitoring, also presents novel growth prospects.

Leading Players in the Implantable Digestible Sensors Sector

- Medtronic

- Sensirion AG

- Honeywell International, Inc.

- TE Connectivity

- Koninklijke Philips N.V

- General Electric Company

- Proteus Healthcare

Key Milestones in Implantable Digestible Sensors Industry

- 2019: Proteus Discover digital medicine platform receives FDA clearance, marking a significant step for ingestible sensor technology in medication adherence.

- 2020: Continued advancements in microfabrication enable smaller and more integrated sensor components, reducing the size of potential ingestible devices.

- 2021: Increased investment in AI and machine learning for analyzing physiological data from ingestible sensors, leading to more sophisticated diagnostic capabilities.

- 2022: Focus on biodegradable materials gains momentum, addressing safety concerns and paving the way for more environmentally friendly ingestible sensor designs.

- 2023: Several pilot programs demonstrate the efficacy of ingestible sensors in managing chronic gastrointestinal conditions, increasing clinician confidence and adoption.

- 2024: Emergence of novel sensor types, including biochemical and image sensors, showcasing the expanding potential beyond basic physiological monitoring.

Strategic Outlook for Implantable Digestible Sensors Market

The strategic outlook for the implantable digestible sensors market is exceptionally positive, driven by a clear demand for more sophisticated and less invasive diagnostic and monitoring tools. Growth accelerators include the continued integration of AI and machine learning to enhance data interpretation, leading to predictive diagnostics and personalized treatment regimens. Strategic collaborations between key industry players and academic institutions will foster rapid innovation and accelerate the translation of research into viable products. Expansion into new therapeutic areas and geographical markets, coupled with a focus on user-centric design and affordability, will be crucial for market penetration. The development of multi-modal sensors and their integration into comprehensive digital health ecosystems will be a defining characteristic of future growth.

Implantable Digestible Sensors Segmentation

-

1. Application

- 1.1. Diagnostics

- 1.2. Monitoring

-

2. Type

- 2.1. Image Technology

- 2.2. Temperature Technology

- 2.3. Pressure Technology

- 2.4. Other

Implantable Digestible Sensors Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Implantable Digestible Sensors Regional Market Share

Geographic Coverage of Implantable Digestible Sensors

Implantable Digestible Sensors REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Diagnostics

- 5.1.2. Monitoring

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Image Technology

- 5.2.2. Temperature Technology

- 5.2.3. Pressure Technology

- 5.2.4. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Implantable Digestible Sensors Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Diagnostics

- 6.1.2. Monitoring

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Image Technology

- 6.2.2. Temperature Technology

- 6.2.3. Pressure Technology

- 6.2.4. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Implantable Digestible Sensors Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Diagnostics

- 7.1.2. Monitoring

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Image Technology

- 7.2.2. Temperature Technology

- 7.2.3. Pressure Technology

- 7.2.4. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Implantable Digestible Sensors Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Diagnostics

- 8.1.2. Monitoring

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Image Technology

- 8.2.2. Temperature Technology

- 8.2.3. Pressure Technology

- 8.2.4. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Implantable Digestible Sensors Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Diagnostics

- 9.1.2. Monitoring

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Image Technology

- 9.2.2. Temperature Technology

- 9.2.3. Pressure Technology

- 9.2.4. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Implantable Digestible Sensors Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Diagnostics

- 10.1.2. Monitoring

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Image Technology

- 10.2.2. Temperature Technology

- 10.2.3. Pressure Technology

- 10.2.4. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Implantable Digestible Sensors Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Diagnostics

- 11.1.2. Monitoring

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Image Technology

- 11.2.2. Temperature Technology

- 11.2.3. Pressure Technology

- 11.2.4. Other

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Medtronic

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Sensirion AG

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Honeywell International Inc.

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 TE Connectivity

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Koninklijke Philips N.V

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 General Electric Company

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Proteus Healthcare

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.1 Medtronic

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Implantable Digestible Sensors Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: Global Implantable Digestible Sensors Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Implantable Digestible Sensors Revenue (million), by Application 2025 & 2033

- Figure 4: North America Implantable Digestible Sensors Volume (K), by Application 2025 & 2033

- Figure 5: North America Implantable Digestible Sensors Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Implantable Digestible Sensors Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Implantable Digestible Sensors Revenue (million), by Type 2025 & 2033

- Figure 8: North America Implantable Digestible Sensors Volume (K), by Type 2025 & 2033

- Figure 9: North America Implantable Digestible Sensors Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Implantable Digestible Sensors Volume Share (%), by Type 2025 & 2033

- Figure 11: North America Implantable Digestible Sensors Revenue (million), by Country 2025 & 2033

- Figure 12: North America Implantable Digestible Sensors Volume (K), by Country 2025 & 2033

- Figure 13: North America Implantable Digestible Sensors Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Implantable Digestible Sensors Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Implantable Digestible Sensors Revenue (million), by Application 2025 & 2033

- Figure 16: South America Implantable Digestible Sensors Volume (K), by Application 2025 & 2033

- Figure 17: South America Implantable Digestible Sensors Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Implantable Digestible Sensors Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Implantable Digestible Sensors Revenue (million), by Type 2025 & 2033

- Figure 20: South America Implantable Digestible Sensors Volume (K), by Type 2025 & 2033

- Figure 21: South America Implantable Digestible Sensors Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America Implantable Digestible Sensors Volume Share (%), by Type 2025 & 2033

- Figure 23: South America Implantable Digestible Sensors Revenue (million), by Country 2025 & 2033

- Figure 24: South America Implantable Digestible Sensors Volume (K), by Country 2025 & 2033

- Figure 25: South America Implantable Digestible Sensors Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Implantable Digestible Sensors Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Implantable Digestible Sensors Revenue (million), by Application 2025 & 2033

- Figure 28: Europe Implantable Digestible Sensors Volume (K), by Application 2025 & 2033

- Figure 29: Europe Implantable Digestible Sensors Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Implantable Digestible Sensors Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Implantable Digestible Sensors Revenue (million), by Type 2025 & 2033

- Figure 32: Europe Implantable Digestible Sensors Volume (K), by Type 2025 & 2033

- Figure 33: Europe Implantable Digestible Sensors Revenue Share (%), by Type 2025 & 2033

- Figure 34: Europe Implantable Digestible Sensors Volume Share (%), by Type 2025 & 2033

- Figure 35: Europe Implantable Digestible Sensors Revenue (million), by Country 2025 & 2033

- Figure 36: Europe Implantable Digestible Sensors Volume (K), by Country 2025 & 2033

- Figure 37: Europe Implantable Digestible Sensors Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Implantable Digestible Sensors Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Implantable Digestible Sensors Revenue (million), by Application 2025 & 2033

- Figure 40: Middle East & Africa Implantable Digestible Sensors Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Implantable Digestible Sensors Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Implantable Digestible Sensors Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Implantable Digestible Sensors Revenue (million), by Type 2025 & 2033

- Figure 44: Middle East & Africa Implantable Digestible Sensors Volume (K), by Type 2025 & 2033

- Figure 45: Middle East & Africa Implantable Digestible Sensors Revenue Share (%), by Type 2025 & 2033

- Figure 46: Middle East & Africa Implantable Digestible Sensors Volume Share (%), by Type 2025 & 2033

- Figure 47: Middle East & Africa Implantable Digestible Sensors Revenue (million), by Country 2025 & 2033

- Figure 48: Middle East & Africa Implantable Digestible Sensors Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Implantable Digestible Sensors Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Implantable Digestible Sensors Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Implantable Digestible Sensors Revenue (million), by Application 2025 & 2033

- Figure 52: Asia Pacific Implantable Digestible Sensors Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Implantable Digestible Sensors Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Implantable Digestible Sensors Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Implantable Digestible Sensors Revenue (million), by Type 2025 & 2033

- Figure 56: Asia Pacific Implantable Digestible Sensors Volume (K), by Type 2025 & 2033

- Figure 57: Asia Pacific Implantable Digestible Sensors Revenue Share (%), by Type 2025 & 2033

- Figure 58: Asia Pacific Implantable Digestible Sensors Volume Share (%), by Type 2025 & 2033

- Figure 59: Asia Pacific Implantable Digestible Sensors Revenue (million), by Country 2025 & 2033

- Figure 60: Asia Pacific Implantable Digestible Sensors Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Implantable Digestible Sensors Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Implantable Digestible Sensors Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Implantable Digestible Sensors Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Implantable Digestible Sensors Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Implantable Digestible Sensors Revenue million Forecast, by Type 2020 & 2033

- Table 4: Global Implantable Digestible Sensors Volume K Forecast, by Type 2020 & 2033

- Table 5: Global Implantable Digestible Sensors Revenue million Forecast, by Region 2020 & 2033

- Table 6: Global Implantable Digestible Sensors Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Implantable Digestible Sensors Revenue million Forecast, by Application 2020 & 2033

- Table 8: Global Implantable Digestible Sensors Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Implantable Digestible Sensors Revenue million Forecast, by Type 2020 & 2033

- Table 10: Global Implantable Digestible Sensors Volume K Forecast, by Type 2020 & 2033

- Table 11: Global Implantable Digestible Sensors Revenue million Forecast, by Country 2020 & 2033

- Table 12: Global Implantable Digestible Sensors Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: United States Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Canada Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 18: Mexico Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Implantable Digestible Sensors Revenue million Forecast, by Application 2020 & 2033

- Table 20: Global Implantable Digestible Sensors Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Implantable Digestible Sensors Revenue million Forecast, by Type 2020 & 2033

- Table 22: Global Implantable Digestible Sensors Volume K Forecast, by Type 2020 & 2033

- Table 23: Global Implantable Digestible Sensors Revenue million Forecast, by Country 2020 & 2033

- Table 24: Global Implantable Digestible Sensors Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Brazil Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Argentina Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Implantable Digestible Sensors Revenue million Forecast, by Application 2020 & 2033

- Table 32: Global Implantable Digestible Sensors Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Implantable Digestible Sensors Revenue million Forecast, by Type 2020 & 2033

- Table 34: Global Implantable Digestible Sensors Volume K Forecast, by Type 2020 & 2033

- Table 35: Global Implantable Digestible Sensors Revenue million Forecast, by Country 2020 & 2033

- Table 36: Global Implantable Digestible Sensors Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 40: Germany Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: France Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: Italy Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Spain Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 48: Russia Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 50: Benelux Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 52: Nordics Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Implantable Digestible Sensors Revenue million Forecast, by Application 2020 & 2033

- Table 56: Global Implantable Digestible Sensors Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Implantable Digestible Sensors Revenue million Forecast, by Type 2020 & 2033

- Table 58: Global Implantable Digestible Sensors Volume K Forecast, by Type 2020 & 2033

- Table 59: Global Implantable Digestible Sensors Revenue million Forecast, by Country 2020 & 2033

- Table 60: Global Implantable Digestible Sensors Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 62: Turkey Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 64: Israel Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 66: GCC Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 68: North Africa Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 70: South Africa Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Implantable Digestible Sensors Revenue million Forecast, by Application 2020 & 2033

- Table 74: Global Implantable Digestible Sensors Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Implantable Digestible Sensors Revenue million Forecast, by Type 2020 & 2033

- Table 76: Global Implantable Digestible Sensors Volume K Forecast, by Type 2020 & 2033

- Table 77: Global Implantable Digestible Sensors Revenue million Forecast, by Country 2020 & 2033

- Table 78: Global Implantable Digestible Sensors Volume K Forecast, by Country 2020 & 2033

- Table 79: China Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 80: China Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 82: India Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 84: Japan Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 86: South Korea Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 90: Oceania Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Implantable Digestible Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Implantable Digestible Sensors Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Implantable Digestible Sensors?

The projected CAGR is approximately 15%.

2. Which companies are prominent players in the Implantable Digestible Sensors?

Key companies in the market include Medtronic, Sensirion AG, Honeywell International, Inc., TE Connectivity, Koninklijke Philips N.V, General Electric Company, Proteus Healthcare.

3. What are the main segments of the Implantable Digestible Sensors?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 500 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Implantable Digestible Sensors," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Implantable Digestible Sensors report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Implantable Digestible Sensors?

To stay informed about further developments, trends, and reports in the Implantable Digestible Sensors, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence