Key Insights

The OpenStack Services market is poised for extraordinary expansion, projected to reach USD 22.81 Million by 2033, driven by a remarkable 32.01% CAGR. This robust growth signifies a significant shift towards open-source cloud infrastructure solutions. The primary catalysts for this surge include the increasing demand for cost-effective and flexible cloud deployments, the growing adoption of hybrid and multi-cloud strategies by enterprises, and the continuous evolution of OpenStack's capabilities to support advanced workloads like AI/ML and big data analytics. Furthermore, the inherent advantages of OpenStack, such as vendor neutrality, extensive community support, and the ability to customize solutions, are compelling businesses to leverage its power. The market is segmented by deployment models, with On-Cloud solutions expected to dominate due to their scalability and accessibility, while On-Premise deployments will continue to cater to organizations with specific security and regulatory compliance needs. Key end-user industries such as Information Technology, Telecommunication, and Banking & Financial Services are leading the charge in OpenStack adoption, recognizing its potential to enhance operational efficiency and drive innovation.

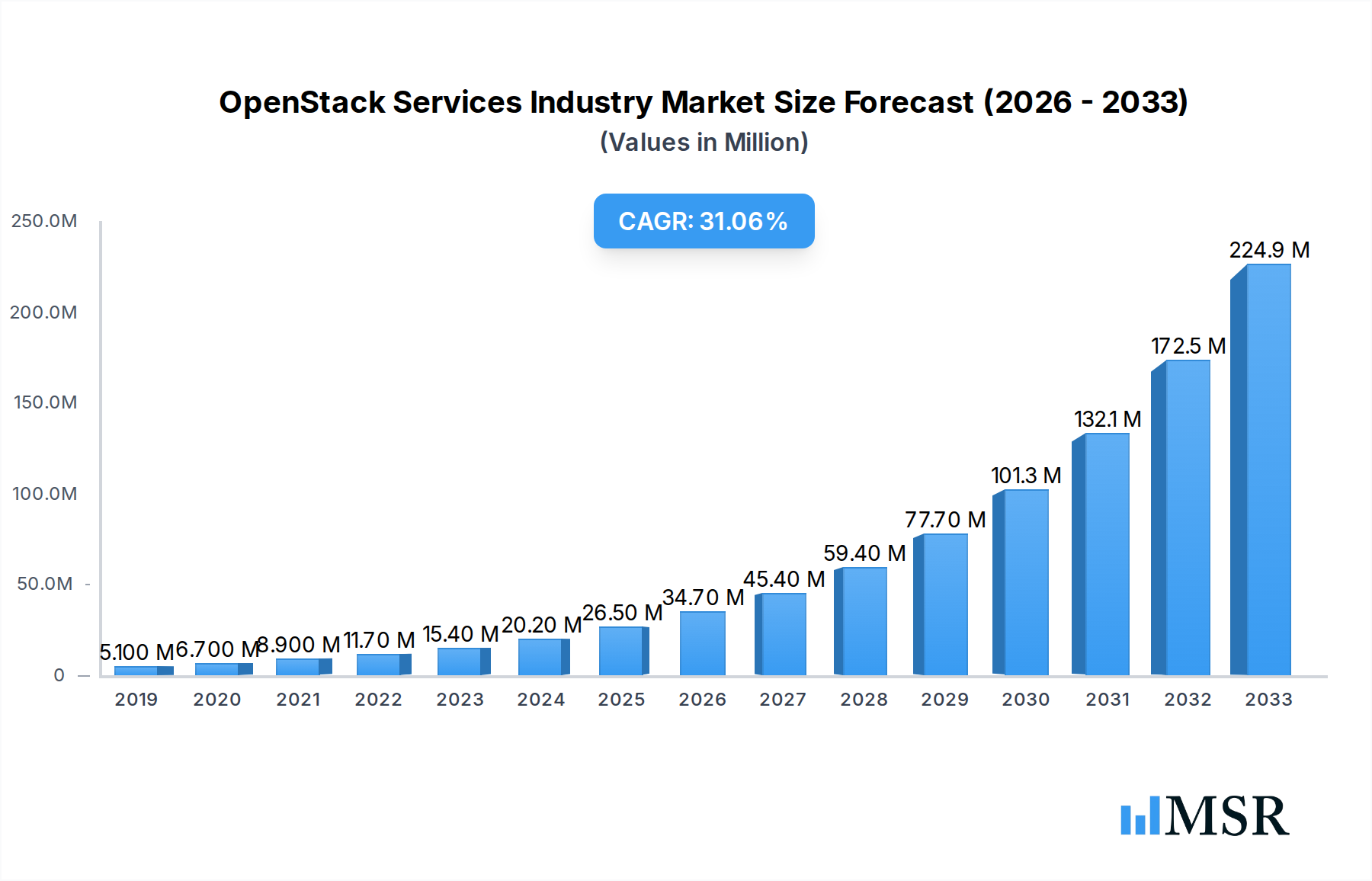

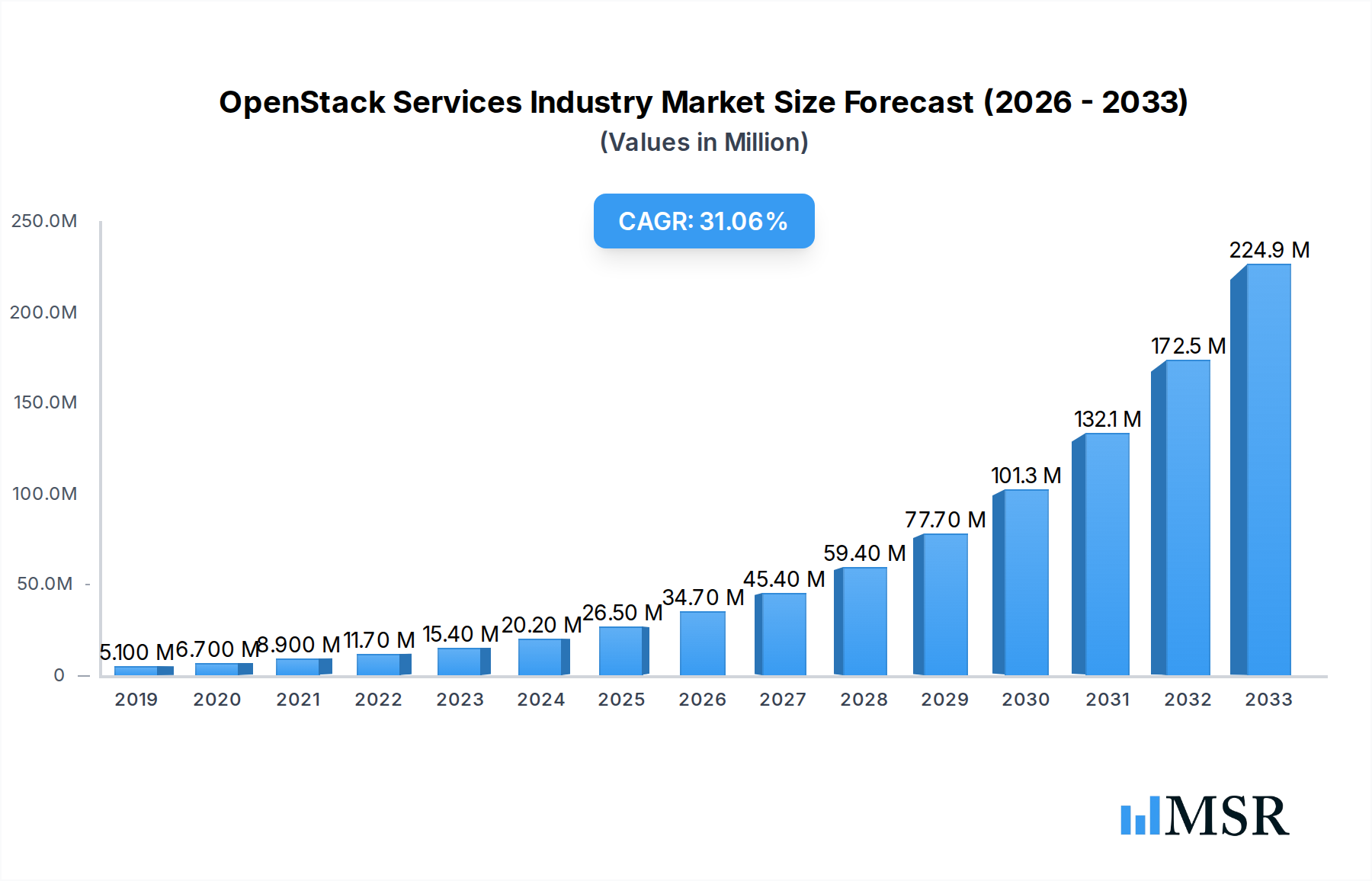

OpenStack Services Industry Market Size (In Million)

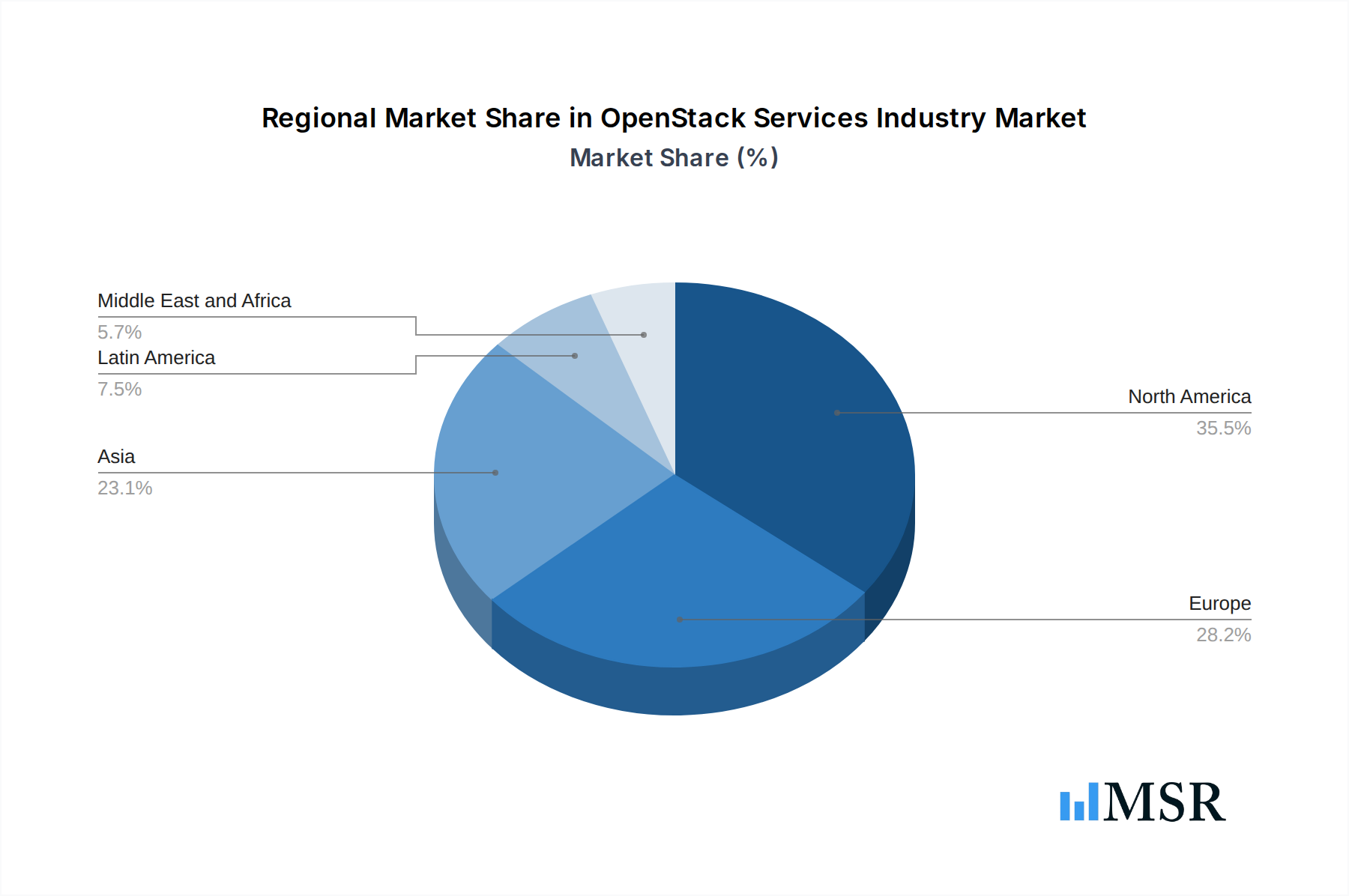

The competitive landscape for OpenStack Services is dynamic, with major technology players like Mirantis Inc., Canonical Ltd., NetApp Inc., Cisco Systems Inc., Rackspace US Inc., Hewlett Packard Enterprise Development LP, Red Hat Inc., Dell Inc., Huawei Technologies Co Ltd, and VMware Inc. actively contributing to market growth through their comprehensive service offerings and ongoing development efforts. Emerging trends include the increasing integration of OpenStack with container orchestration platforms like Kubernetes, the rise of managed OpenStack services for simplified deployment and management, and the focus on security enhancements and automation to address enterprise concerns. While the market is experiencing a strong upward trajectory, potential restraints could include the complexity of OpenStack deployments and the need for skilled personnel, as well as the ongoing competition from established proprietary cloud providers. However, the overwhelming benefits of open-source flexibility and cost savings are expected to outweigh these challenges, paving the way for sustained and significant market growth across all major regions, with North America and Europe currently leading in adoption.

OpenStack Services Industry Company Market Share

Unlock critical insights into the dynamic OpenStack Services Industry with this comprehensive report. Covering the historical period of 2019–2024 and projecting growth through 2033, this analysis provides an in-depth understanding of market concentration, key trends, leading segments, and future opportunities. Dive into actionable data, including market size estimations for the base year 2025, projected to reach XX Million by 2025 and XX Million by 2033, with a Compound Annual Growth Rate (CAGR) of XX% during the forecast period 2025–2033. This report is your essential guide to navigating the evolving landscape of private cloud and infrastructure-as-a-service (IaaS) solutions.

OpenStack Services Industry Market Concentration & Dynamics

The OpenStack Services Industry is characterized by a moderate to high market concentration, with a few dominant players shaping its trajectory. Innovation ecosystems are vibrant, driven by open-source collaboration and continuous feature development, fostering an environment where cloud orchestration and private cloud solutions are paramount. Regulatory frameworks, while generally permissive for open-source technologies, can influence adoption in highly regulated sectors like banking and financial services. Substitute products, primarily public cloud offerings and competing private cloud solutions, present a constant competitive pressure. End-user trends highlight a growing demand for hybrid cloud and multi-cloud strategies, with a significant push towards enhanced data security and cost optimization. Merger and acquisition (M&A) activities, while not as rampant as in some tech sectors, are strategic, focusing on acquiring specialized skills or expanding service portfolios. For instance, XX M&A deals were recorded within the historical period, indicating consolidation and strategic partnerships aimed at strengthening market positions within the enterprise cloud domain. The market share distribution sees key players like Red Hat Inc. and Canonical Ltd. holding substantial portions, especially in enterprise and telecommunication deployments, while companies like Mirantis Inc. focus on managed OpenStack services and VEXXHOST Inc. on deployment tools.

OpenStack Services Industry Industry Insights & Trends

The OpenStack Services Industry is experiencing robust growth, propelled by the increasing need for flexible, scalable, and cost-effective private cloud infrastructure. The market size was estimated at XX Million in 2025, with projections indicating a significant expansion to XX Million by 2033. This growth is underpinned by a Compound Annual Growth Rate (CAGR) of XX% during the forecast period of 2025–2033. Technological disruptions, such as the evolution of containerization technologies and the rise of AI/ML workloads, are driving the demand for sophisticated orchestration and management platforms like OpenStack. Evolving consumer behaviors, particularly the shift towards greater data sovereignty, enhanced security protocols, and a preference for open-source solutions that offer flexibility and avoid vendor lock-in, are significantly impacting market dynamics. The increasing adoption of virtualization technologies and the continuous development of new OpenStack features, including advanced networking, storage, and compute management capabilities, are key growth drivers. Furthermore, the growing complexity of IT environments necessitates comprehensive cloud management services and managed OpenStack solutions to ensure optimal performance and cost efficiency. The demand for secure private cloud environments within government and enterprise sectors, driven by data privacy regulations and the need for dedicated resources, is a major catalyst for the OpenStack Services Industry.

Key Markets & Segments Leading OpenStack Services Industry

The Information Technology (IT) sector and Telecommunication industries are currently the dominant markets for OpenStack Services, significantly influencing the global market size and growth trajectory. The demand for robust, scalable, and secure private cloud infrastructure within these sectors is unparalleled, driving substantial investment in OpenStack deployments.

Information Technology (IT): This segment is a powerhouse for OpenStack adoption.

- Drivers: The inherent need for agile development, efficient resource allocation, and the ability to rapidly deploy and manage complex IT infrastructures fuels demand. Organizations are increasingly leveraging OpenStack for building private clouds that support their application development lifecycle, data analytics platforms, and internal IT operations, contributing an estimated XX% to the market share.

- Dominance Analysis: Large enterprises within the IT sector utilize OpenStack to create highly customized and secure private cloud environments, reducing reliance on public cloud services for sensitive workloads and gaining greater control over their infrastructure.

Telecommunication: The telecommunications industry is a rapidly growing segment for OpenStack.

- Drivers: The evolution towards 5G networks, edge computing, and the need for NFV (Network Functions Virtualization) infrastructure are primary drivers. OpenStack provides the foundational layer for building these agile and scalable network infrastructures.

- Dominance Analysis: Telecom operators are increasingly adopting OpenStack to virtualize their network functions, enabling faster service deployment, improved network efficiency, and reduced operational costs. The push for network cloudification makes OpenStack a crucial component for modern telecommunication services.

Banking and Financial Services: While traditionally more cautious due to stringent regulatory requirements, this sector is witnessing increased OpenStack adoption for specific use cases.

- Drivers: Demand for enhanced security, data sovereignty, and cost-effective private cloud solutions for non-core banking applications.

- Dominance Analysis: Financial institutions are increasingly exploring OpenStack for building private clouds that offer greater control over sensitive financial data and compliance with regulations like GDPR and CCPA.

Academic: Educational institutions are leveraging OpenStack for research computing, cloud infrastructure for students, and internal IT modernization.

- Drivers: Cost-effectiveness and the flexibility to experiment with cutting-edge cloud technologies.

- Dominance Analysis: Universities are using OpenStack to create large-scale computing clusters for research and to provide students with hands-on experience in cloud environments.

Retail/E-Commerce: This segment is adopting OpenStack for building scalable e-commerce platforms and managing customer data securely.

- Drivers: The need for highly available and scalable infrastructure to handle peak traffic loads and the increasing importance of personalized customer experiences driven by data analytics.

- Dominance Analysis: Retailers are using OpenStack to power their online storefronts, inventory management systems, and customer relationship management tools, ensuring a seamless and secure online shopping experience.

OpenStack Services Industry Product Developments

The OpenStack Services Industry is continuously evolving with significant product developments enhancing its capabilities and market relevance. Recent innovations include the launch of Atmosphere by VEXXHOST Inc., an open-source tool designed to deploy fully integrated OpenStack environments, simplifying cloud deployment and improving accessibility. Furthermore, advancements in Red Hat's OpenStack platform have tightened its integration with cloud-native technologies like OpenShift, enabling seamless hybrid cloud solutions and better support for telecom operator specific needs. These developments underscore a strong focus on ease of use, interoperability, and tailored solutions for specific industry verticals, positioning OpenStack as a resilient and adaptable infrastructure-as-a-service (IaaS) platform.

Challenges in the OpenStack Services Industry Market

Despite its strengths, the OpenStack Services Industry faces several challenges. One significant barrier is the complexity of deployment and management, which can deter smaller organizations or those with limited IT expertise, demanding specialized OpenStack support services. Integration with legacy systems remains a hurdle for many enterprises seeking to transition to a cloud-native environment. Furthermore, the perception of competition from hyperscale public cloud providers can sometimes overshadow the benefits of private and hybrid cloud solutions. Talent acquisition for skilled OpenStack engineers and administrators also presents a challenge, impacting implementation and ongoing operational efficiency. Quantifiable impacts include an estimated XX% delay in project timelines due to integration complexities and a XX% increase in operational costs when lacking skilled personnel.

Forces Driving OpenStack Services Industry Growth

Several key forces are driving the growth of the OpenStack Services Industry. The relentless demand for cost-effective cloud solutions and the desire for greater data control and sovereignty are paramount. Technological advancements in areas like container orchestration and AI/ML infrastructure require flexible and scalable private cloud environments that OpenStack excels at providing. Furthermore, the growing adoption of hybrid and multi-cloud strategies positions OpenStack as a crucial component for managing diverse IT landscapes. The inherent flexibility and customization offered by open-source solutions also attract organizations looking to avoid vendor lock-in and optimize their IT investments.

Challenges in the OpenStack Services Industry Market

Long-term growth catalysts for the OpenStack Services Industry are deeply rooted in continuous innovation and strategic market expansions. The increasing maturity of the OpenStack ecosystem, with a focus on simplifying deployment and management through tools like VEXXHOST's Atmosphere, is a significant catalyst. Partnerships, such as the one between UNICC and Canonical for secure private cloud environments, highlight the growing trust and adoption in critical sectors. Furthermore, the ongoing development of advanced features, including enhanced security protocols and AI/ML support, ensures OpenStack remains relevant in the face of evolving technological demands. Market expansions into new verticals and geographies, coupled with the increasing adoption of managed OpenStack services, will continue to fuel long-term growth.

Emerging Opportunities in OpenStack Services Industry

Emerging opportunities in the OpenStack Services Industry lie in the growing demand for specialized solutions and integrated platforms. The rise of edge computing presents a significant opportunity for OpenStack to power distributed infrastructure. The increasing adoption of AI and machine learning workloads necessitates powerful and customizable private cloud environments, a niche where OpenStack can excel. Furthermore, the demand for secure, sovereign cloud solutions for government and sensitive data industries is expanding, with OpenStack's private cloud capabilities being a strong fit. The development of managed OpenStack services and consulting expertise continues to create new avenues for service providers to cater to organizations seeking to leverage OpenStack without extensive in-house expertise.

Leading Players in the OpenStack Services Industry Sector

- Mirantis Inc

- Canonical Ltd

- NetApp Inc

- Cisco Systems Inc

- Rackspace US Inc

- Hewlett Packard Enterprise Development LP

- Red Hat Inc

- Dell Inc

- Huawei Technologies Co Ltd

- VMware Inc

Key Milestones in OpenStack Services Industry Industry

- October 2023: UNICC partnered with Canonical to build and deliver secure private cloud environments for the UN system, emphasizing advanced security and data sovereignty for sensitive UN data and software applications.

- September 2022: Red Hat released updated OpenStack platform capabilities focused on telecom operators, strengthening its integration with the cloud-native OpenShift platform.

- June 2022: VEXXHOST Inc. launched Atmosphere, an open-source tool for deploying fully integrated OpenStack environments, enhancing accessibility and user benefit for the IaaS platform.

Strategic Outlook for OpenStack Services Industry Market

The strategic outlook for the OpenStack Services Industry is positive, driven by a persistent demand for flexible, secure, and cost-effective private and hybrid cloud solutions. Growth accelerators include the increasing adoption of OpenStack for mission-critical workloads in sectors like telecommunications and finance, alongside its growing relevance in powering AI/ML and edge computing initiatives. The continuous evolution of the OpenStack ecosystem, with a focus on simplified deployment and enhanced integration capabilities, will further bolster its market position. Strategic opportunities lie in the expansion of managed services, specialized consulting, and tailored solutions for emerging technologies, ensuring OpenStack remains a vital component of modern enterprise IT infrastructure.

OpenStack Services Industry Segmentation

-

1. Deployment Model

- 1.1. On-Cloud

- 1.2. On-Premise

-

2. End-user Industry

- 2.1. Information Technology

- 2.2. Telecommunication

- 2.3. Banking and Financial Services

- 2.4. Academic

- 2.5. Retail/E-Commerce

OpenStack Services Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Latin America

- 5. Middle East and Africa

OpenStack Services Industry Regional Market Share

Geographic Coverage of OpenStack Services Industry

OpenStack Services Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 32.01% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Deployment Model

- 5.1.1. On-Cloud

- 5.1.2. On-Premise

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Information Technology

- 5.2.2. Telecommunication

- 5.2.3. Banking and Financial Services

- 5.2.4. Academic

- 5.2.5. Retail/E-Commerce

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Deployment Model

- 6. Global OpenStack Services Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Deployment Model

- 6.1.1. On-Cloud

- 6.1.2. On-Premise

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Information Technology

- 6.2.2. Telecommunication

- 6.2.3. Banking and Financial Services

- 6.2.4. Academic

- 6.2.5. Retail/E-Commerce

- 6.1. Market Analysis, Insights and Forecast - by Deployment Model

- 7. North America OpenStack Services Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Deployment Model

- 7.1.1. On-Cloud

- 7.1.2. On-Premise

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Information Technology

- 7.2.2. Telecommunication

- 7.2.3. Banking and Financial Services

- 7.2.4. Academic

- 7.2.5. Retail/E-Commerce

- 7.1. Market Analysis, Insights and Forecast - by Deployment Model

- 8. Europe OpenStack Services Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Deployment Model

- 8.1.1. On-Cloud

- 8.1.2. On-Premise

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Information Technology

- 8.2.2. Telecommunication

- 8.2.3. Banking and Financial Services

- 8.2.4. Academic

- 8.2.5. Retail/E-Commerce

- 8.1. Market Analysis, Insights and Forecast - by Deployment Model

- 9. Asia OpenStack Services Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Deployment Model

- 9.1.1. On-Cloud

- 9.1.2. On-Premise

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Information Technology

- 9.2.2. Telecommunication

- 9.2.3. Banking and Financial Services

- 9.2.4. Academic

- 9.2.5. Retail/E-Commerce

- 9.1. Market Analysis, Insights and Forecast - by Deployment Model

- 10. Latin America OpenStack Services Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Deployment Model

- 10.1.1. On-Cloud

- 10.1.2. On-Premise

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Information Technology

- 10.2.2. Telecommunication

- 10.2.3. Banking and Financial Services

- 10.2.4. Academic

- 10.2.5. Retail/E-Commerce

- 10.1. Market Analysis, Insights and Forecast - by Deployment Model

- 11. Middle East and Africa OpenStack Services Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Deployment Model

- 11.1.1. On-Cloud

- 11.1.2. On-Premise

- 11.2. Market Analysis, Insights and Forecast - by End-user Industry

- 11.2.1. Information Technology

- 11.2.2. Telecommunication

- 11.2.3. Banking and Financial Services

- 11.2.4. Academic

- 11.2.5. Retail/E-Commerce

- 11.1. Market Analysis, Insights and Forecast - by Deployment Model

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Mirantis Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Canonical Ltd

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 NetApp Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Cisco Systems Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Rackspace US Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Hewlett Packard Enterprise Development LP

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Red Hat Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Dell Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Huawei Technologies Co Ltd

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 VMware Inc

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Mirantis Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global OpenStack Services Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America OpenStack Services Industry Revenue (Million), by Deployment Model 2025 & 2033

- Figure 3: North America OpenStack Services Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 4: North America OpenStack Services Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 5: North America OpenStack Services Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 6: North America OpenStack Services Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America OpenStack Services Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe OpenStack Services Industry Revenue (Million), by Deployment Model 2025 & 2033

- Figure 9: Europe OpenStack Services Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 10: Europe OpenStack Services Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 11: Europe OpenStack Services Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 12: Europe OpenStack Services Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe OpenStack Services Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia OpenStack Services Industry Revenue (Million), by Deployment Model 2025 & 2033

- Figure 15: Asia OpenStack Services Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 16: Asia OpenStack Services Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 17: Asia OpenStack Services Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 18: Asia OpenStack Services Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia OpenStack Services Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America OpenStack Services Industry Revenue (Million), by Deployment Model 2025 & 2033

- Figure 21: Latin America OpenStack Services Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 22: Latin America OpenStack Services Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 23: Latin America OpenStack Services Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: Latin America OpenStack Services Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Latin America OpenStack Services Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa OpenStack Services Industry Revenue (Million), by Deployment Model 2025 & 2033

- Figure 27: Middle East and Africa OpenStack Services Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 28: Middle East and Africa OpenStack Services Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 29: Middle East and Africa OpenStack Services Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: Middle East and Africa OpenStack Services Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Middle East and Africa OpenStack Services Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global OpenStack Services Industry Revenue Million Forecast, by Deployment Model 2020 & 2033

- Table 2: Global OpenStack Services Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 3: Global OpenStack Services Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global OpenStack Services Industry Revenue Million Forecast, by Deployment Model 2020 & 2033

- Table 5: Global OpenStack Services Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 6: Global OpenStack Services Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Global OpenStack Services Industry Revenue Million Forecast, by Deployment Model 2020 & 2033

- Table 8: Global OpenStack Services Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 9: Global OpenStack Services Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Global OpenStack Services Industry Revenue Million Forecast, by Deployment Model 2020 & 2033

- Table 11: Global OpenStack Services Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 12: Global OpenStack Services Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global OpenStack Services Industry Revenue Million Forecast, by Deployment Model 2020 & 2033

- Table 14: Global OpenStack Services Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 15: Global OpenStack Services Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global OpenStack Services Industry Revenue Million Forecast, by Deployment Model 2020 & 2033

- Table 17: Global OpenStack Services Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 18: Global OpenStack Services Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the OpenStack Services Industry?

The projected CAGR is approximately 32.01%.

2. Which companies are prominent players in the OpenStack Services Industry?

Key companies in the market include Mirantis Inc, Canonical Ltd, NetApp Inc, Cisco Systems Inc, Rackspace US Inc, Hewlett Packard Enterprise Development LP, Red Hat Inc, Dell Inc, Huawei Technologies Co Ltd, VMware Inc.

3. What are the main segments of the OpenStack Services Industry?

The market segments include Deployment Model, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 22.81 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Need for Organizations to Improve Their Business Agility and Efficiency; OpenStack Being Open Source Provides the Flexibility for Customized Solution; Increasing use of OpenStack Services in Telecommunication Sector.

6. What are the notable trends driving market growth?

Increasing use of OpenStack Services in Telecommunication Sector is Driving the Market.

7. Are there any restraints impacting market growth?

Lack of Robustness that Enterprises Desire for Their Data Centers. Including IT Management Features. Such as Availability and Security.

8. Can you provide examples of recent developments in the market?

October 2023 - UNICC is Partnered with Canonical, the publisher of Ubuntu and provider of open-source security, support and services, to build and deliver the secure private cloud environment for the UN system, offering advanced security and data sovereignty for the UN’s most sensitive data and software applications.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "OpenStack Services Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the OpenStack Services Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the OpenStack Services Industry?

To stay informed about further developments, trends, and reports in the OpenStack Services Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence