Key Insights

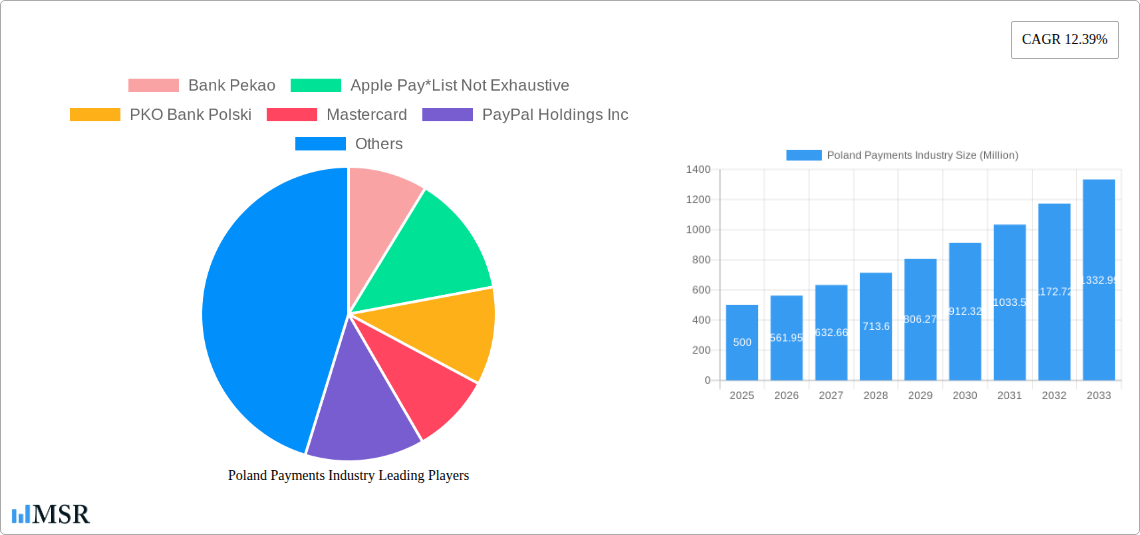

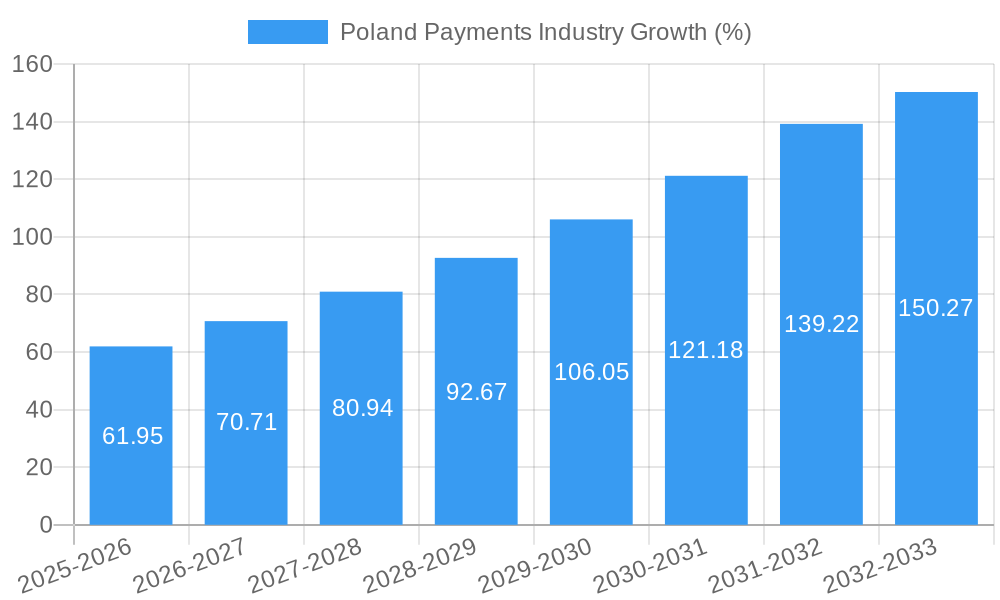

The Poland payments industry, currently experiencing robust growth, is projected to maintain a significant upward trajectory throughout the forecast period (2025-2033). A Compound Annual Growth Rate (CAGR) of 12.39% indicates a dynamic market driven by several key factors. The increasing adoption of digital technologies, particularly among younger demographics, fuels the expansion of online payment methods, surpassing traditional point-of-sale transactions in certain segments. Growth in e-commerce and the rise of mobile payment solutions like Apple Pay and Google Pay significantly contribute to this shift. Furthermore, the expansion of the Polish economy and increasing financial inclusion are driving greater transaction volumes across various sectors, including retail, entertainment, healthcare, and hospitality. While the precise market size in 2025 is unavailable, extrapolating from the provided CAGR and considering comparable European markets, a reasonable estimate would place the market value at around €500 million (or equivalent in local currency).

However, the industry also faces challenges. Competition among established players like Bank Pekao, PKO Bank Polski, Mastercard, and PayPal, alongside emerging fintech companies, is intense. Maintaining robust cybersecurity measures and adapting to evolving consumer preferences will be crucial for continued success. The regulatory landscape also plays a significant role, impacting the adoption and integration of new payment technologies. Despite these challenges, the overall outlook for the Poland payments industry remains positive, with sustained growth expected through 2033, driven by ongoing digitalization and economic development. The market segmentation by payment mode (point-of-sale vs. online) and end-user industry provides valuable insight into growth opportunities within specific niches. Understanding consumer behavior and technological advancements within each segment is vital for strategic planning and competitive advantage.

Poland Payments Industry Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Poland payments industry, covering market dynamics, key segments, leading players, and future growth prospects. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report offers invaluable insights for industry stakeholders, investors, and strategic decision-makers. The report leverages data from the historical period (2019-2024) and incorporates the latest industry developments to paint a clear picture of the evolving Polish payments landscape.

Poland Payments Industry Market Concentration & Dynamics

The Polish payments industry exhibits a dynamic landscape characterized by both established players and emerging fintech companies. Market concentration is moderate, with a few dominant banks like Bank Pekao and PKO Bank Polski holding significant market share, but facing increasing competition from international players such as Mastercard and PayPal Holdings Inc. The industry's innovation ecosystem is thriving, fueled by advancements in mobile payments, digital wallets, and open banking initiatives. The regulatory framework, while evolving, generally supports innovation. Substitute products, such as cash and alternative payment methods, still hold a share, although their usage is gradually declining. End-user trends show a strong preference for digital and contactless payments, driven by convenience and security concerns. M&A activity has been moderate in recent years, with approximately xx deals recorded between 2019 and 2024, reflecting consolidation and expansion strategies within the industry.

- Market Share (2024): Bank Pekao: xx%; PKO Bank Polski: xx%; Mastercard: xx%; Others: xx%

- M&A Deal Count (2019-2024): xx

- Key Regulatory Changes: (List specific relevant regulations and their impact)

Poland Payments Industry Industry Insights & Trends

The Polish payments industry is experiencing robust growth, driven by increasing digital adoption, rising e-commerce penetration, and a growing middle class. The market size reached approximately xx Million in 2024 and is projected to reach xx Million by 2025, exhibiting a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). Technological disruptions, particularly the rise of mobile payments and contactless transactions, are reshaping the industry. Evolving consumer behavior, characterized by a preference for speed, convenience, and security, further fuels the industry's growth. The increasing adoption of buy now, pay later (BNPL) services, as evidenced by PKO BP's recent announcement, signifies another significant trend. The growing popularity of digital wallets like Apple Pay and other mobile payment solutions significantly contributes to this growth. The expansion of online sales continues to be a key factor.

Key Markets & Segments Leading Poland Payments Industry

The Polish payments market is dominated by the Retail and Online Sale segments. Within the "By Mode of Payment" category, point-of-sale (POS) transactions maintain a significant share, although online sales are rapidly gaining ground. The Retail segment within "By End-user Industry" accounts for a substantial portion of the overall market volume, driven by strong consumer spending.

By Mode of Payment:

- Point of Sale: Drivers include rising retail sales, increased penetration of contactless POS terminals, and growing adoption of mobile payment solutions.

- Online Sales: Drivers include the exponential growth of e-commerce, rising internet and smartphone penetration, and increasing consumer preference for online shopping.

By End-user Industry:

- Retail: Dominant due to high consumer spending and widespread adoption of digital payment methods.

- Entertainment: Strong growth driven by online streaming, ticketing, and gaming.

- Healthcare: Steady growth driven by increased adoption of digital health services and online payments for medical expenses.

- Hospitality: Growing adoption of mobile and contactless payments in hotels, restaurants, and tourism.

- Other End-user Industries: This segment demonstrates moderate growth, driven by expanding digital payment adoption across various sectors.

Poland Payments Industry Product Developments

Recent product innovations include the expansion of contactless payment options at POS terminals and online, the introduction of new digital wallets and mobile payment applications, and the growing adoption of BNPL services. These advancements enhance the user experience, improve security, and cater to the evolving needs of Polish consumers. The introduction of advanced fraud detection systems and improved security measures further reinforces trust in the digital payment ecosystem.

Challenges in the Poland Payments Industry Market

The Polish payments industry faces challenges including regulatory complexities, potential cybersecurity threats, and maintaining the necessary infrastructure to support the growing volume of digital transactions. Competition from both domestic and international players further intensifies the challenges faced by industry participants. The need for ongoing investment in infrastructure and cybersecurity measures poses a significant financial hurdle for many companies.

Forces Driving Poland Payments Industry Growth

Key growth drivers include increasing digitalization, rising e-commerce adoption, and government support for financial technology innovation. The expansion of 4G/5G networks and growing smartphone penetration significantly contributes to the ease of mobile payments adoption. The growing acceptance of digital payments by businesses of all sizes is driving the adoption of modern POS technologies.

Long-Term Growth Catalysts in the Poland Payments Industry

Long-term growth will be fueled by continued investment in fintech innovation, strategic partnerships between banks and technology companies, and the expansion of financial inclusion across Poland. The development of new payment solutions, improved security protocols and expansion into new market segments will further accelerate growth.

Emerging Opportunities in Poland Payments Industry

Opportunities exist in the expansion of mobile payment solutions, the growth of BNPL services, and the development of innovative solutions for specific end-user industries. The untapped potential in underserved rural regions and among less digitally-savvy populations presents a substantial growth opportunity. Furthermore, the growing interest in cryptocurrency and other digital assets represents a potential new avenue for market expansion.

Leading Players in the Poland Payments Industry Sector

- Bank Pekao

- Apple Pay

- PKO Bank Polski

- Mastercard

- PayPal Holdings Inc

- PayU

- Santander Bank Polska

- DotPay

- American Express

- Tap2Pay me

Key Milestones in Poland Payments Industry Industry

- May 2022: Allegro launched a new cash-on-delivery payment option allowing card and smartphone contactless payments via couriers. This increases the accessibility and convenience of online shopping.

- May 2022: PKO BP announced the completion of its BNPL (Buy Now, Pay Later) solution, expanding the available payment options across numerous online shops in Poland. This move significantly increases the convenience for online consumers.

Strategic Outlook for Poland Payments Industry Market

The Polish payments industry is poised for substantial growth in the coming years, driven by the factors outlined above. Strategic opportunities exist for companies that can successfully navigate the challenges, innovate, and adapt to the evolving needs of the market. Focusing on enhanced security, user experience, and strategic partnerships will be key to success. The market's future potential is substantial, and companies with forward-thinking strategies are well-positioned to capture significant market share.

Poland Payments Industry Segmentation

-

1. Mode of Payment

-

1.1. Point of Sale

- 1.1.1. Card Pay

- 1.1.2. Digital Wallet (includes Mobile Wallets)

- 1.1.3. Cash

- 1.1.4. Others

-

1.2. Online Sale

- 1.2.1. Others (

-

1.1. Point of Sale

-

2. End-user Industry

- 2.1. Retail

- 2.2. Entertainment

- 2.3. Healthcare

- 2.4. Hospitality

- 2.5. Other End-user Industries

Poland Payments Industry Segmentation By Geography

- 1. Poland

Poland Payments Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 12.39% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Advancements in the Polish Payments Market; Initiatives by the Government to improve cashless payment methods

- 3.3. Market Restrains

- 3.3.1. Lack of a standard legislative policy remains especially in the case of cross-border transactions

- 3.4. Market Trends

- 3.4.1. Advancements in the Polish Payments Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Poland Payments Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 5.1.1. Point of Sale

- 5.1.1.1. Card Pay

- 5.1.1.2. Digital Wallet (includes Mobile Wallets)

- 5.1.1.3. Cash

- 5.1.1.4. Others

- 5.1.2. Online Sale

- 5.1.2.1. Others (

- 5.1.1. Point of Sale

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Retail

- 5.2.2. Entertainment

- 5.2.3. Healthcare

- 5.2.4. Hospitality

- 5.2.5. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Poland

- 5.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Bank Pekao

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Apple Pay*List Not Exhaustive

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 PKO Bank Polski

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Mastercard

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 PayPal Holdings Inc

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 PayU

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Santander Bank Polska

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 DotPay

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 American Express

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Tap2Pay me

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Bank Pekao

List of Figures

- Figure 1: Poland Payments Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Poland Payments Industry Share (%) by Company 2024

List of Tables

- Table 1: Poland Payments Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Poland Payments Industry Revenue Million Forecast, by Mode of Payment 2019 & 2032

- Table 3: Poland Payments Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 4: Poland Payments Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Poland Payments Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Poland Payments Industry Revenue Million Forecast, by Mode of Payment 2019 & 2032

- Table 7: Poland Payments Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 8: Poland Payments Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Poland Payments Industry?

The projected CAGR is approximately 12.39%.

2. Which companies are prominent players in the Poland Payments Industry?

Key companies in the market include Bank Pekao, Apple Pay*List Not Exhaustive, PKO Bank Polski, Mastercard, PayPal Holdings Inc, PayU, Santander Bank Polska, DotPay, American Express, Tap2Pay me.

3. What are the main segments of the Poland Payments Industry?

The market segments include Mode of Payment, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Advancements in the Polish Payments Market; Initiatives by the Government to improve cashless payment methods.

6. What are the notable trends driving market growth?

Advancements in the Polish Payments Market.

7. Are there any restraints impacting market growth?

Lack of a standard legislative policy remains especially in the case of cross-border transactions.

8. Can you provide examples of recent developments in the market?

May 2022 - Allegro announced a new service implemented in one of the platform's delivery methods - One Kurier. Customers using this method and paying for cash-on-delivery purchases can pay by card or smartphone using the contactless method on the courier's device used to manage shipments.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Poland Payments Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Poland Payments Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Poland Payments Industry?

To stay informed about further developments, trends, and reports in the Poland Payments Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence