Key Insights

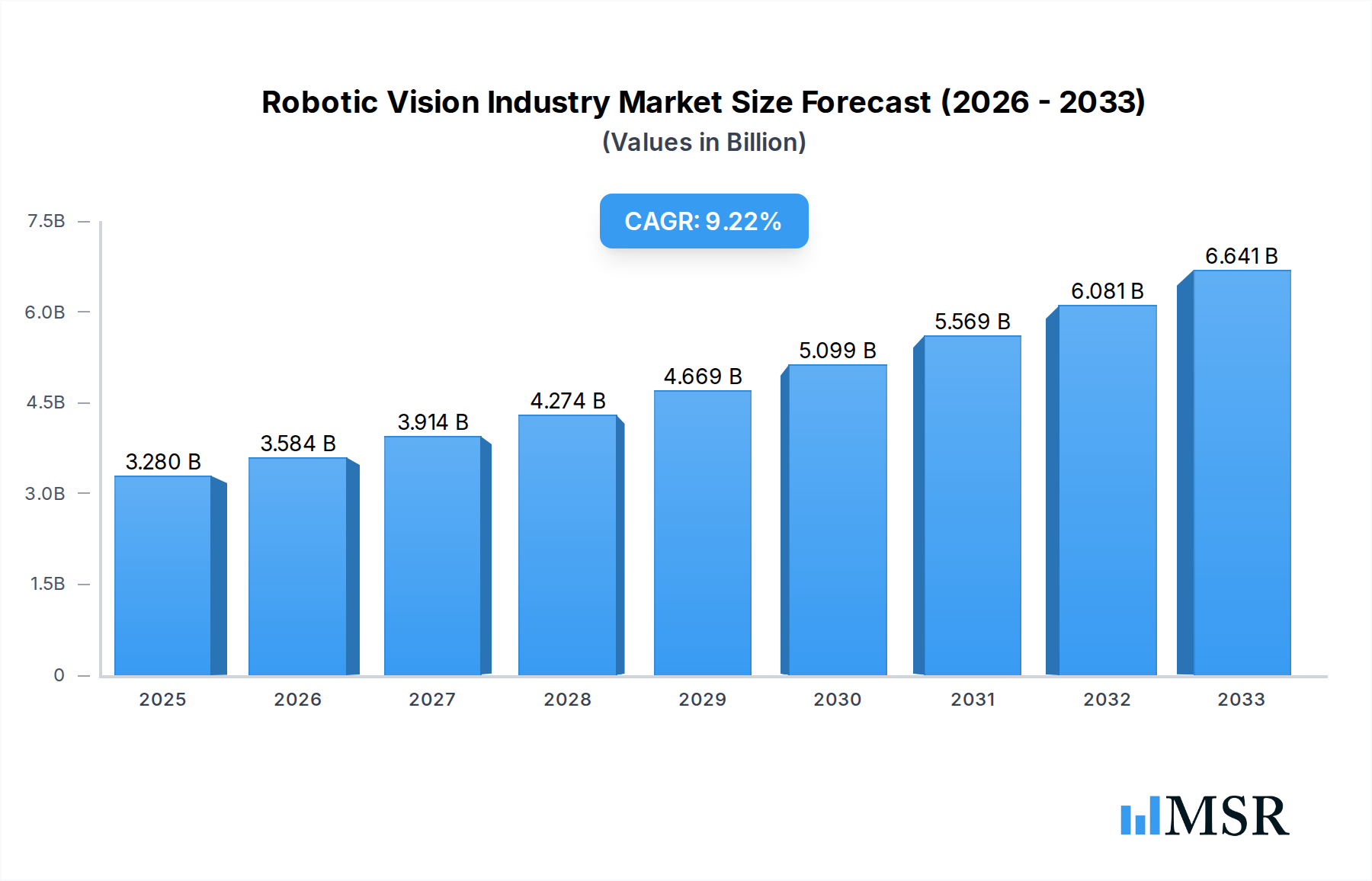

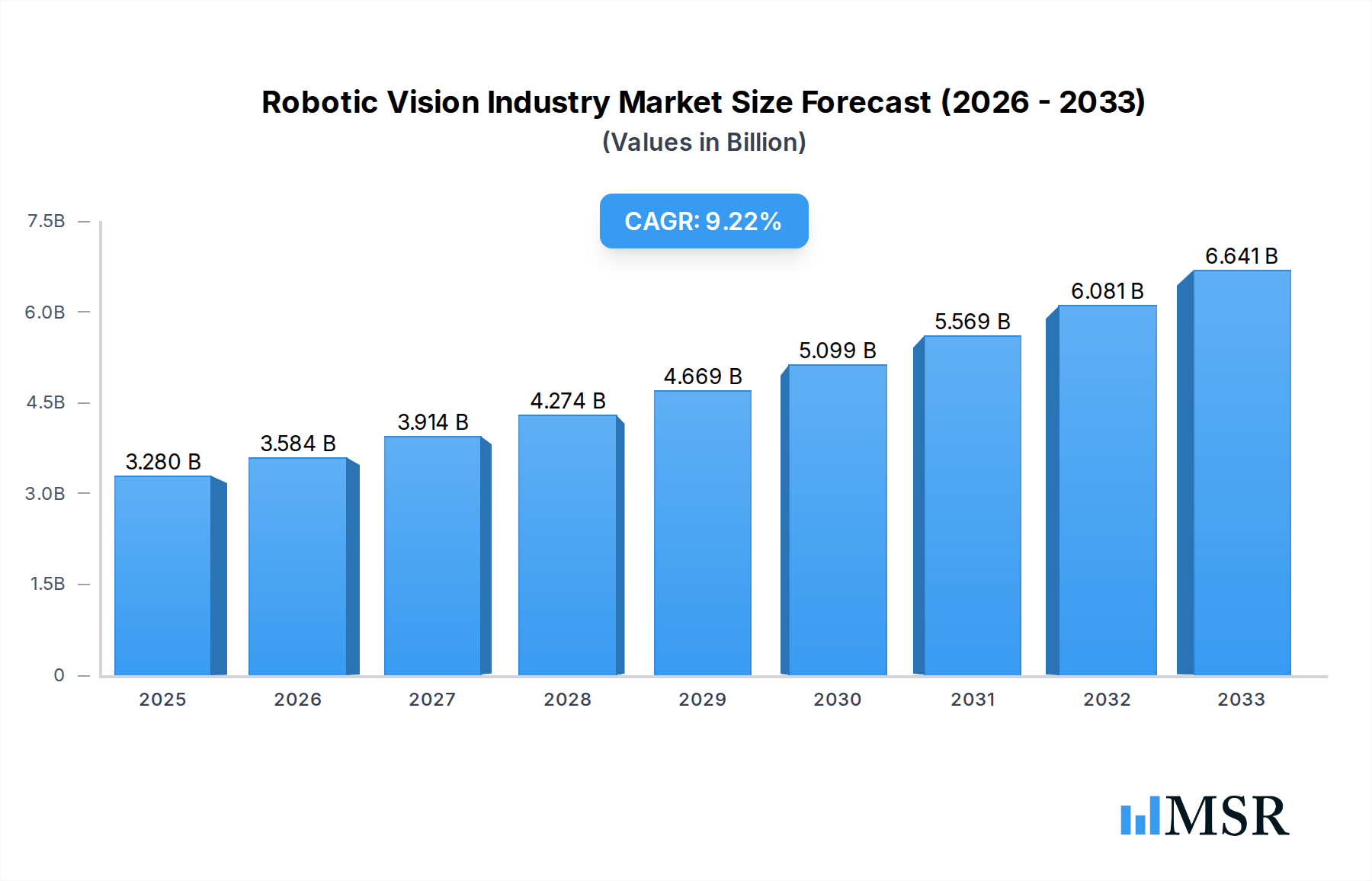

The global Robotic Vision market is poised for significant expansion, projected to reach USD 3.28 billion in 2025 and grow at a robust CAGR of 9.67% through 2033. This impressive growth is fueled by the escalating adoption of automation across diverse industries, driven by the need for enhanced productivity, improved quality control, and greater operational efficiency. The increasing sophistication of artificial intelligence and machine learning algorithms, coupled with advancements in sensor technology and processing power, are enabling robots to perform more complex tasks with greater precision. This, in turn, is expanding the application scope of robotic vision systems beyond traditional manufacturing, into sectors like logistics, healthcare, and agriculture. The automotive and electronics industries are leading the charge, leveraging robotic vision for critical applications such as assembly, inspection, and quality assurance, thereby driving substantial market demand.

Robotic Vision Industry Market Size (In Billion)

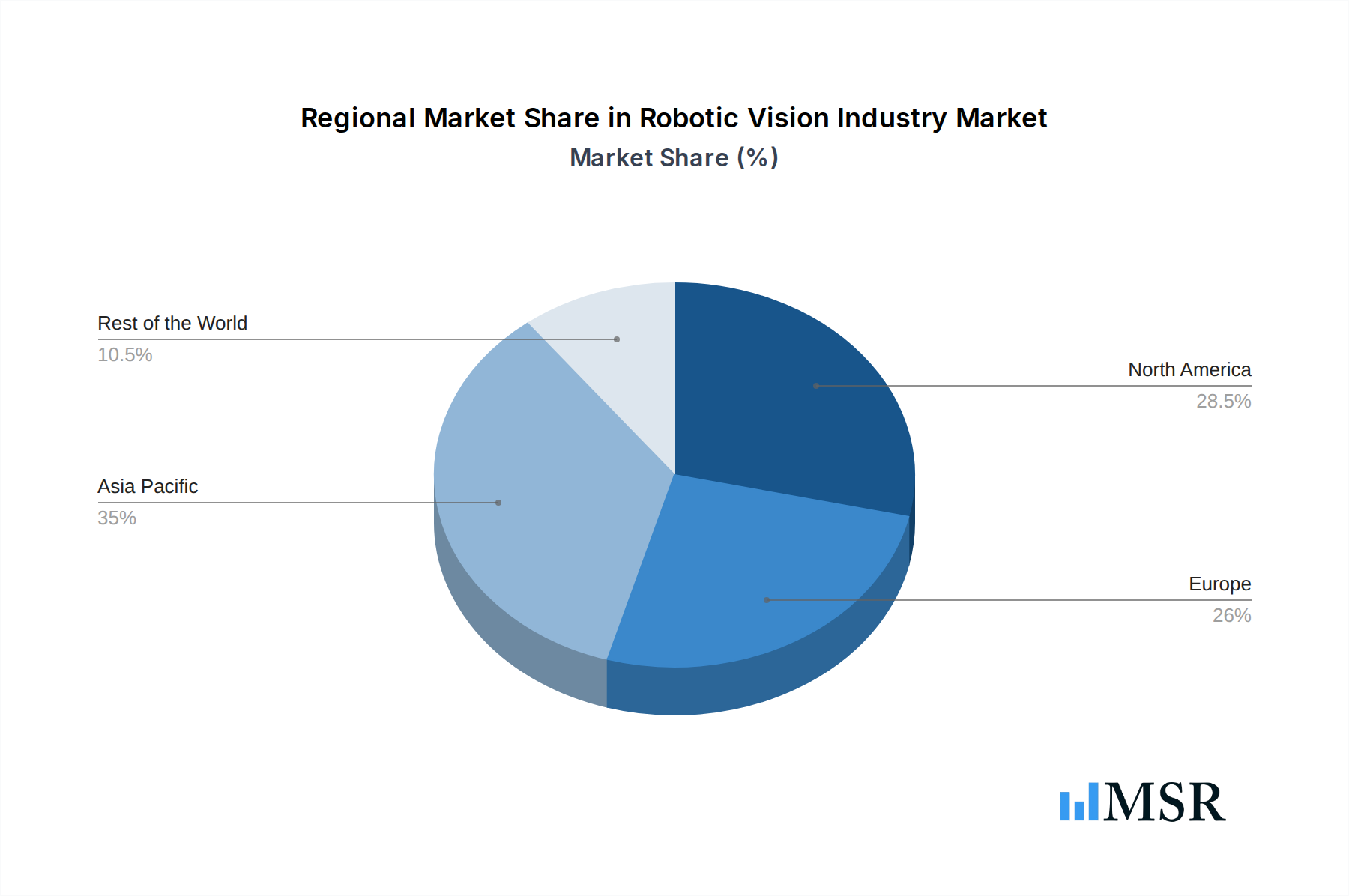

Further propelling the market are innovations in 2D and 3D vision technologies, offering enhanced depth perception and more detailed environmental understanding for robots. Emerging trends include the integration of AI-powered analytics for predictive maintenance and real-time defect detection, as well as the development of more compact and cost-effective vision solutions. While the high initial investment costs and the need for skilled personnel to implement and manage these systems present certain restraints, the long-term benefits of increased throughput and reduced errors are compelling organizations to overcome these challenges. Asia Pacific is expected to emerge as a dominant region, driven by its strong manufacturing base and increasing investments in Industry 4.0 initiatives, while North America and Europe continue to be crucial markets due to their advanced technological infrastructure and early adoption of automation.

Robotic Vision Industry Company Market Share

Robotic Vision Industry: Comprehensive Market Analysis & Growth Projections (2019–2033)

Unlock the future of industrial automation with this in-depth report on the Robotic Vision Industry. This comprehensive analysis delves into market dynamics, technological advancements, and growth opportunities within the rapidly evolving field of machine vision for robotics. Covering the historical period (2019–2024), base year (2025), and extending to 2033, this report provides actionable insights for stakeholders seeking to capitalize on the projected global market size and Compound Annual Growth Rate (CAGR). Discover key players, emerging trends, and strategic imperatives shaping the robotics and automation landscape.

Robotic Vision Industry Market Concentration & Dynamics

The Robotic Vision Industry exhibits a moderate to high market concentration, driven by a handful of dominant players and a growing ecosystem of innovative technology providers. Key companies like Keyence Corporation, FANUC Corporation, Cognex Corporation, and ABB Group hold significant market share, leveraging their extensive product portfolios and global reach. The innovation ecosystem is vibrant, with continuous advancements in AI, deep learning, and sensor technology fueling new applications. Regulatory frameworks, while evolving, generally support the adoption of automation to enhance safety and efficiency. Substitute products, such as traditional inspection methods, are increasingly being displaced by the superior precision and speed offered by robotic vision. End-user trends highlight a strong demand for automation across industries, driven by labor shortages and the pursuit of operational excellence. Mergers and acquisitions (M&A) activities are notable, with companies strategically acquiring complementary technologies and market access. Recent M&A deal counts indicate a consolidating yet expanding market.

Robotic Vision Industry Industry Insights & Trends

The Robotic Vision Industry is poised for substantial growth, propelled by an escalating demand for automation and intelligent manufacturing solutions. The global market size for robotic vision is projected to reach hundreds of billions by 2025, with a compelling CAGR expected throughout the forecast period. This surge is primarily attributed to the increasing adoption of robots across diverse end-user industries, including Automotive, Electronics, Aerospace, Food and Beverage, and Pharmaceutical. Technological disruptions are at the forefront, with breakthroughs in 3D Vision and advanced sensor fusion enhancing robotic capabilities for complex tasks. Evolving consumer behaviors, such as the demand for customized products and faster delivery times, are pushing manufacturers to adopt more agile and efficient production processes, directly benefiting the robotic vision market. The integration of AI and machine learning further amplifies the capabilities of robotic vision systems, enabling them to perform intricate inspections, quality control, and assembly operations with unprecedented accuracy and speed.

Key Markets & Segments Leading Robotic Vision Industry

The Robotic Vision Industry is experiencing significant expansion across several key markets and segments, with particular dominance observed in the Automotive and Electronics sectors. These industries are at the forefront of adopting advanced automation to meet stringent quality standards and high production volumes.

Technology Segments Driving Growth:

- 3D Vision: This segment is witnessing rapid growth due to its ability to provide depth perception and detailed spatial information, crucial for complex pick-and-place operations, precise assembly, and comprehensive quality inspection in intricate product manufacturing.

- 2D Vision: While a mature technology, 2D vision continues to be a foundational element, essential for a wide range of inspection, guidance, and identification tasks across all industries, offering cost-effectiveness and reliability for simpler applications.

End User Industries Fueling Demand:

- Automotive: The automotive industry is a primary driver, heavily investing in robotic vision for assembly line automation, defect detection in components, and quality assurance of finished vehicles. The push for electric vehicles (EVs) and advanced driver-assistance systems (ADAS) further accelerates this adoption.

- Electronics: The high-volume, precision-oriented nature of electronics manufacturing makes it a prime candidate for robotic vision. Applications include component inspection, soldering verification, circuit board assembly, and packaging.

- Aerospace: The aerospace sector leverages robotic vision for critical inspection tasks, ensuring the highest safety and quality standards for aircraft components and assemblies.

- Food and Beverage: Increasing automation for packaging, inspection of food products for contaminants or defects, and quality control throughout the production line is driving adoption in this sector.

- Pharmaceutical: Strict regulatory requirements and the need for precision in drug manufacturing and packaging make robotic vision indispensable for tasks like pill inspection, vial sealing verification, and traceability.

- Other End User Industries: Growth is also observed in logistics, e-commerce fulfillment, metal fabrication, and general manufacturing, where robotic vision enhances efficiency and productivity.

Economic growth and robust infrastructure development in emerging economies are also significant factors contributing to the broader adoption of robotic vision solutions globally.

Robotic Vision Industry Product Developments

Recent product developments in the Robotic Vision Industry are characterized by enhanced intelligence and integration. Innovations focus on more sophisticated AI algorithms for improved object recognition, defect detection, and adaptive learning capabilities. Advancements in sensor technology, including higher resolution cameras, faster frame rates, and new 3D sensing modalities, are enabling robots to perform more complex tasks with greater accuracy and speed. The market relevance of these developments lies in their ability to address evolving industry needs for increased automation, precision, and flexibility, thereby providing competitive advantages to adopting companies.

Challenges in the Robotic Vision Industry Market

The Robotic Vision Industry faces several challenges that could impact its growth trajectory. High initial investment costs for sophisticated robotic vision systems remain a barrier for some small and medium-sized enterprises (SMEs). The integration complexity of these systems with existing manufacturing infrastructure requires specialized expertise, leading to potential implementation delays and increased operational costs. Furthermore, a shortage of skilled personnel capable of designing, deploying, and maintaining these advanced systems presents a significant bottleneck. Cybersecurity concerns related to connected robotic vision systems and the need for robust data protection also require careful consideration.

Forces Driving Robotic Vision Industry Growth

Several key forces are propelling the growth of the Robotic Vision Industry. The relentless pursuit of increased productivity and operational efficiency by manufacturers globally is a primary driver. The rising demand for high-quality, defect-free products across all sectors necessitates the precision and consistency that robotic vision provides. Furthermore, the growing labor shortage in many industrial regions compels companies to automate tasks previously performed by humans. Advancements in artificial intelligence and machine learning are continuously enhancing the capabilities of robotic vision systems, making them more intelligent and adaptable to complex tasks. Government initiatives promoting Industry 4.0 and smart manufacturing also contribute significantly to market expansion.

Challenges in the Robotic Vision Industry Market

While growth is robust, the Robotic Vision Industry also encounters enduring challenges. The significant capital expenditure required for advanced robotic vision systems can be a deterrent for smaller businesses, impacting widespread adoption. The continuous need for software and hardware updates to keep pace with technological advancements adds to the total cost of ownership. Moreover, establishing universal standards for interoperability between different robotic vision components and systems remains an ongoing challenge. The skilled workforce gap, particularly in areas like AI integration and advanced sensor calibration, continues to limit the full potential of these technologies in certain regions.

Emerging Opportunities in Robotic Vision Industry

The Robotic Vision Industry is ripe with emerging opportunities driven by evolving technological frontiers and market demands. The increasing adoption of collaborative robots (cobots) presents a significant opportunity for vision systems that can enable safe and efficient human-robot interaction. The expansion of e-commerce and the need for automated logistics and fulfillment centers are creating substantial demand for robotic vision solutions in warehousing and material handling. Furthermore, the integration of AI and deep learning algorithms is opening doors for more sophisticated applications in predictive maintenance, anomaly detection, and real-time process optimization, moving beyond traditional inspection tasks. The growing focus on sustainability and circular economy principles also presents opportunities for robotic vision in advanced recycling and material sorting processes.

Leading Players in the Robotic Vision Industry Sector

- Keyence Corporation

- FANUC Corporation

- National Instruments Corporation

- Cognex Corporation

- Teledyne Dalsa Inc

- Sick AG

- ABB Group

- Qualcomm Technologies Inc

- Hexagon AB

- Omron Adept Technology Inc

Key Milestones in Robotic Vision Industry Industry

- September 2022: Following the 2021 acquisition of mobile robot company ASTI Mobile Robotics, ABB has launched its first line of branded Autonomous Mobile Robots (AMRs). ABB has a fully integrated offering of robots, AMRs, and machine automation solutions. ABB, which already provides AMR solutions for client projects, has collaborated with crucial partner Expert Technology Group in the UK to develop a complete assembly line based on AMRs for a technology startup creating breakthrough parts for EV vehicle drive trains. ABB's automation system uses ABB robots, vision function packages, and AMRs to transport products between robotic automation cells and human assembly stations.

- August 2022: Visionary.ai, a software-based image signal processor (ISP) technology developer, and Innoviz, one of the providers of high-performance, automotive-grade LiDAR sensors, and perception software, announced a new partnership to combine Visionary.ai's imaging technology with Innoviz's LiDAR sensors and perception software. The two technologies, when combined, offer to improve 3D machine vision performance for a variety of applications, including robots and drones.

Strategic Outlook for Robotic Vision Industry Market

The strategic outlook for the Robotic Vision Industry is exceptionally strong, driven by continuous technological innovation and increasing global demand for automation. Future growth will be accelerated by the deeper integration of AI and machine learning, enabling more autonomous and intelligent robotic systems. Strategic partnerships between hardware manufacturers, software developers, and end-users will be crucial for developing tailored solutions that address specific industry challenges. The expansion into emerging markets and the development of more accessible and user-friendly robotic vision solutions will also unlock new revenue streams and market segments, solidifying its position as a cornerstone of future industrial development.

Robotic Vision Industry Segmentation

-

1. Technology

- 1.1. 2D Vision

- 1.2. 3D Vision

-

2. End User Industry

- 2.1. Automotive

- 2.2. Electronics

- 2.3. Aerospace

- 2.4. Food and Beverage

- 2.5. Pharmaceutical

- 2.6. Other End User Industries

Robotic Vision Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Rest of the World

Robotic Vision Industry Regional Market Share

Geographic Coverage of Robotic Vision Industry

Robotic Vision Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 5.1.1. 2D Vision

- 5.1.2. 3D Vision

- 5.2. Market Analysis, Insights and Forecast - by End User Industry

- 5.2.1. Automotive

- 5.2.2. Electronics

- 5.2.3. Aerospace

- 5.2.4. Food and Beverage

- 5.2.5. Pharmaceutical

- 5.2.6. Other End User Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 6. Global Robotic Vision Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 6.1.1. 2D Vision

- 6.1.2. 3D Vision

- 6.2. Market Analysis, Insights and Forecast - by End User Industry

- 6.2.1. Automotive

- 6.2.2. Electronics

- 6.2.3. Aerospace

- 6.2.4. Food and Beverage

- 6.2.5. Pharmaceutical

- 6.2.6. Other End User Industries

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 7. North America Robotic Vision Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Technology

- 7.1.1. 2D Vision

- 7.1.2. 3D Vision

- 7.2. Market Analysis, Insights and Forecast - by End User Industry

- 7.2.1. Automotive

- 7.2.2. Electronics

- 7.2.3. Aerospace

- 7.2.4. Food and Beverage

- 7.2.5. Pharmaceutical

- 7.2.6. Other End User Industries

- 7.1. Market Analysis, Insights and Forecast - by Technology

- 8. Europe Robotic Vision Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Technology

- 8.1.1. 2D Vision

- 8.1.2. 3D Vision

- 8.2. Market Analysis, Insights and Forecast - by End User Industry

- 8.2.1. Automotive

- 8.2.2. Electronics

- 8.2.3. Aerospace

- 8.2.4. Food and Beverage

- 8.2.5. Pharmaceutical

- 8.2.6. Other End User Industries

- 8.1. Market Analysis, Insights and Forecast - by Technology

- 9. Asia Pacific Robotic Vision Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Technology

- 9.1.1. 2D Vision

- 9.1.2. 3D Vision

- 9.2. Market Analysis, Insights and Forecast - by End User Industry

- 9.2.1. Automotive

- 9.2.2. Electronics

- 9.2.3. Aerospace

- 9.2.4. Food and Beverage

- 9.2.5. Pharmaceutical

- 9.2.6. Other End User Industries

- 9.1. Market Analysis, Insights and Forecast - by Technology

- 10. Rest of the World Robotic Vision Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Technology

- 10.1.1. 2D Vision

- 10.1.2. 3D Vision

- 10.2. Market Analysis, Insights and Forecast - by End User Industry

- 10.2.1. Automotive

- 10.2.2. Electronics

- 10.2.3. Aerospace

- 10.2.4. Food and Beverage

- 10.2.5. Pharmaceutical

- 10.2.6. Other End User Industries

- 10.1. Market Analysis, Insights and Forecast - by Technology

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Keyence Corporation

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 FANUC Corporation

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 National Instruments Corporation

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Cognex Corporation

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Teledyne Dalsa Inc

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Sick AG

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 ABB Group

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Qualcomm Technologies Inc

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Hexagon A

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Omron Adept Technology Inc

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.1 Keyence Corporation

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Robotic Vision Industry Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Robotic Vision Industry Revenue (undefined), by Technology 2025 & 2033

- Figure 3: North America Robotic Vision Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 4: North America Robotic Vision Industry Revenue (undefined), by End User Industry 2025 & 2033

- Figure 5: North America Robotic Vision Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 6: North America Robotic Vision Industry Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Robotic Vision Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Robotic Vision Industry Revenue (undefined), by Technology 2025 & 2033

- Figure 9: Europe Robotic Vision Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 10: Europe Robotic Vision Industry Revenue (undefined), by End User Industry 2025 & 2033

- Figure 11: Europe Robotic Vision Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 12: Europe Robotic Vision Industry Revenue (undefined), by Country 2025 & 2033

- Figure 13: Europe Robotic Vision Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Robotic Vision Industry Revenue (undefined), by Technology 2025 & 2033

- Figure 15: Asia Pacific Robotic Vision Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 16: Asia Pacific Robotic Vision Industry Revenue (undefined), by End User Industry 2025 & 2033

- Figure 17: Asia Pacific Robotic Vision Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 18: Asia Pacific Robotic Vision Industry Revenue (undefined), by Country 2025 & 2033

- Figure 19: Asia Pacific Robotic Vision Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Rest of the World Robotic Vision Industry Revenue (undefined), by Technology 2025 & 2033

- Figure 21: Rest of the World Robotic Vision Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 22: Rest of the World Robotic Vision Industry Revenue (undefined), by End User Industry 2025 & 2033

- Figure 23: Rest of the World Robotic Vision Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 24: Rest of the World Robotic Vision Industry Revenue (undefined), by Country 2025 & 2033

- Figure 25: Rest of the World Robotic Vision Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Robotic Vision Industry Revenue undefined Forecast, by Technology 2020 & 2033

- Table 2: Global Robotic Vision Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 3: Global Robotic Vision Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Robotic Vision Industry Revenue undefined Forecast, by Technology 2020 & 2033

- Table 5: Global Robotic Vision Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 6: Global Robotic Vision Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: Global Robotic Vision Industry Revenue undefined Forecast, by Technology 2020 & 2033

- Table 8: Global Robotic Vision Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 9: Global Robotic Vision Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 10: Global Robotic Vision Industry Revenue undefined Forecast, by Technology 2020 & 2033

- Table 11: Global Robotic Vision Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 12: Global Robotic Vision Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Global Robotic Vision Industry Revenue undefined Forecast, by Technology 2020 & 2033

- Table 14: Global Robotic Vision Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 15: Global Robotic Vision Industry Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Robotic Vision Industry?

The projected CAGR is approximately 8.7%.

2. Which companies are prominent players in the Robotic Vision Industry?

Key companies in the market include Keyence Corporation, FANUC Corporation, National Instruments Corporation, Cognex Corporation, Teledyne Dalsa Inc, Sick AG, ABB Group, Qualcomm Technologies Inc, Hexagon A, Omron Adept Technology Inc.

3. What are the main segments of the Robotic Vision Industry?

The market segments include Technology, End User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

Increased Adoption of Cognitive Humanoid Robots; Growing Demand from End - User Segments like Automotive Industry.

6. What are the notable trends driving market growth?

Growing Demand from End-User Segments like Automotive Industry Drives the Market Growth.

7. Are there any restraints impacting market growth?

High Investments.

8. Can you provide examples of recent developments in the market?

September 2022 - Following the 2021 acquisition of mobile robot company ASTI Mobile Robotics, ABB has launched its first line of branded Autonomous Mobile Robots (AMRs). ABB has a fully integrated offering of robots, AMRs, and machine automation solutions. ABB, which already provides AMR solutions for client projects, has collaborated with crucial partner Expert Technology Group in the UK to develop a complete assembly line based on AMRs for a technology startup creating breakthrough parts for EV vehicle drive trains. ABB's automation system uses ABB robots, vision function packages, and AMRs to transport products between robotic automation cells and human assembly stations.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Robotic Vision Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Robotic Vision Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Robotic Vision Industry?

To stay informed about further developments, trends, and reports in the Robotic Vision Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence