Key Insights

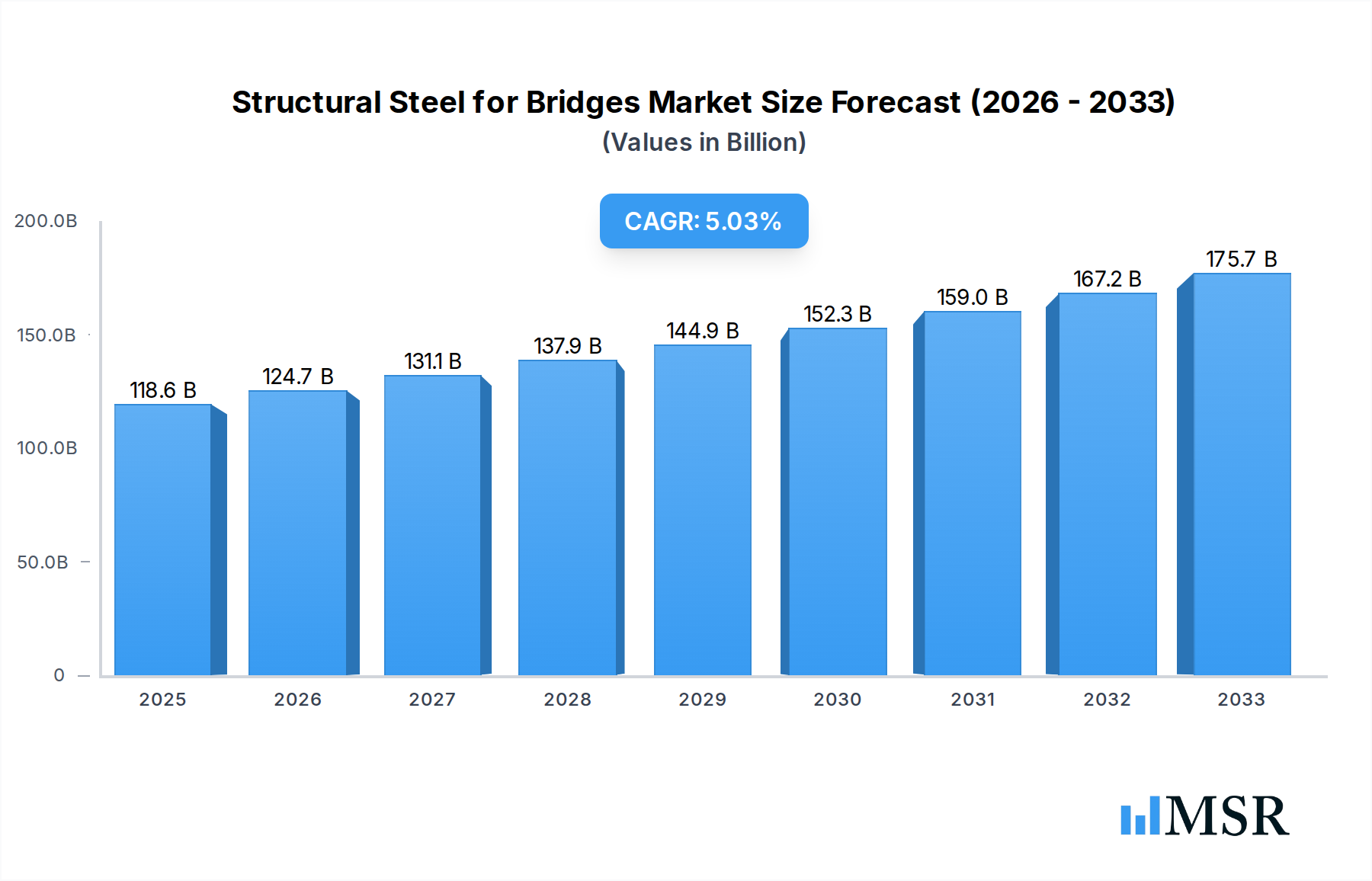

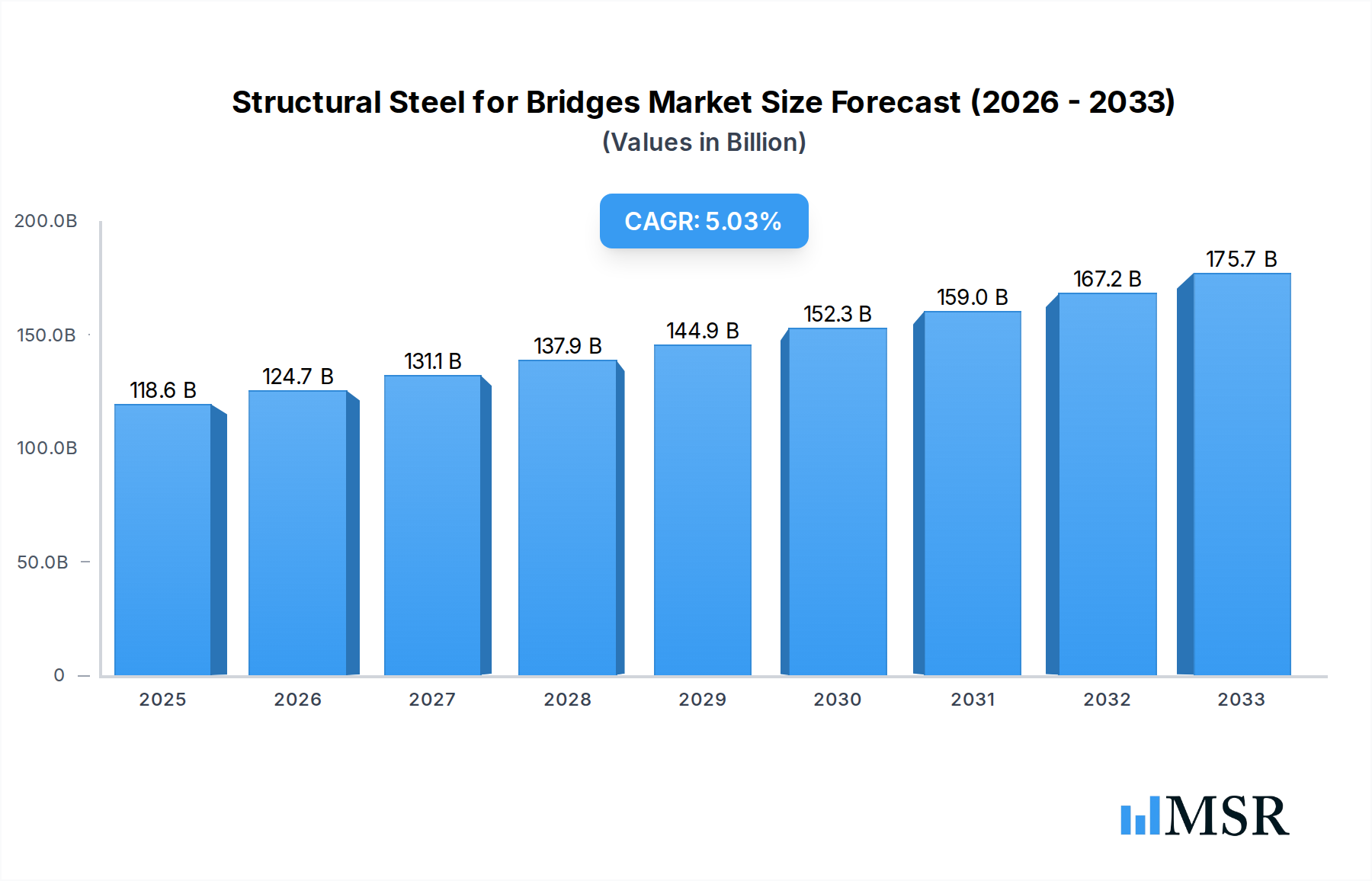

The global Structural Steel for Bridges market is poised for robust growth, projected to reach a substantial $118.64 billion by 2025, exhibiting a compelling Compound Annual Growth Rate (CAGR) of 5.17% over the forecast period of 2025-2033. This significant expansion is primarily driven by an escalating need for robust and durable infrastructure worldwide. The increasing investments in bridge construction and maintenance, particularly in emerging economies, are acting as key catalysts. Furthermore, the inherent advantages of structural steel, such as its high strength-to-weight ratio, recyclability, and cost-effectiveness in the long run, continue to solidify its position as the material of choice for bridge engineering. The market is also benefiting from advancements in steel manufacturing technologies, leading to the development of specialized steel grades like weather-resistant bridge steel plates that offer enhanced longevity and reduced maintenance requirements. This sustained demand underscores the critical role structural steel plays in global transportation networks and economic development.

Structural Steel for Bridges Market Size (In Billion)

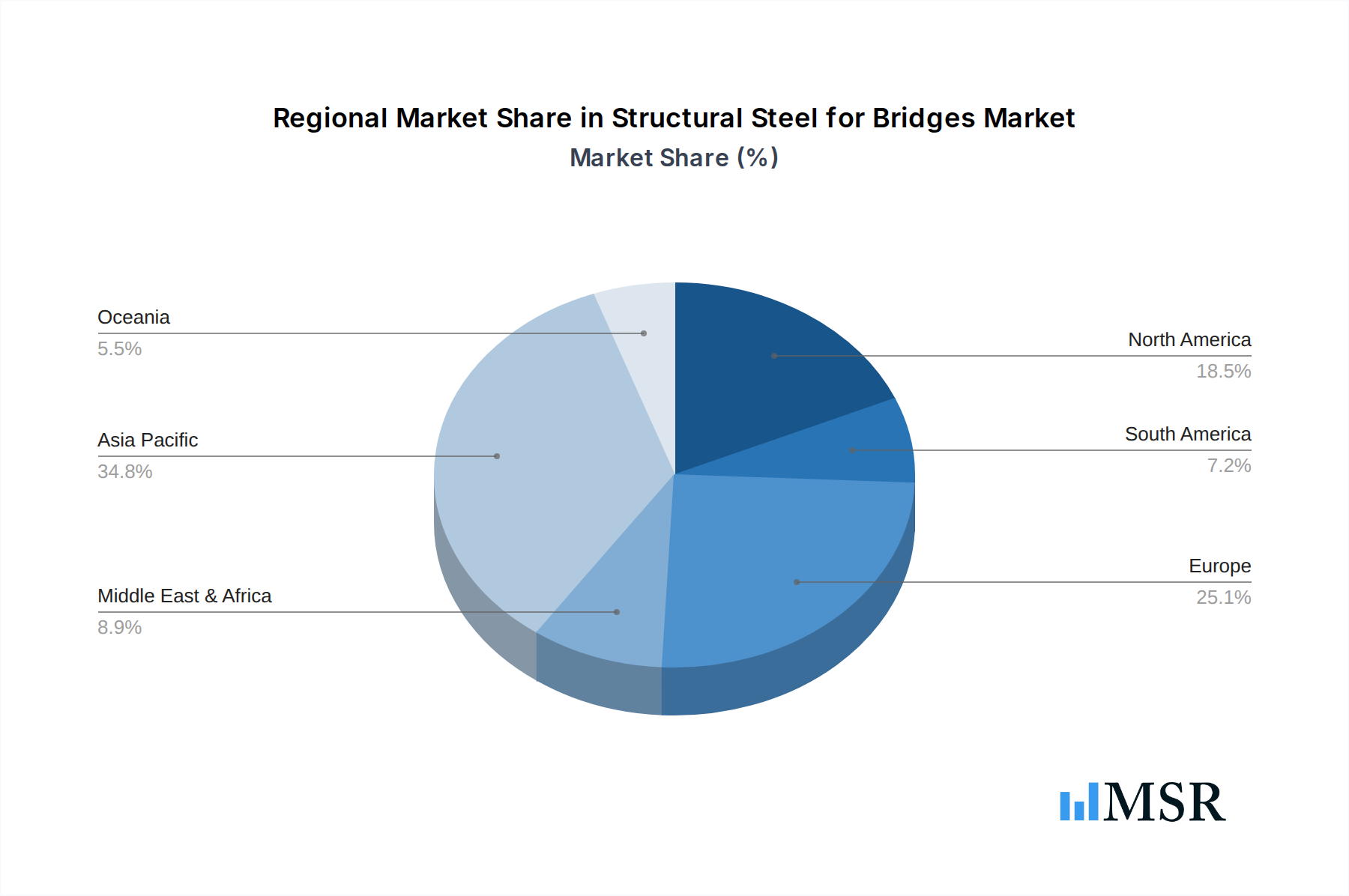

The market segmentation reveals a diverse range of applications and product types. The Railway and Highway segments are expected to be the dominant application areas, reflecting the ongoing global initiatives to upgrade and expand transportation infrastructure. Within types, Low Alloy High Strength Steel and Weather-Resistant Bridge Steel Plate are anticipated to witness considerable demand due to their superior performance characteristics crucial for modern bridge construction. Key players like JFE Steel, Aperam, Nippon Steel Corporation, ThyssenKrupp AG, POSCO, and Baowu are actively participating in this dynamic market, driving innovation and competition. Geographically, the Asia Pacific region, led by China and India, is projected to be a major growth engine due to massive infrastructure development projects. North America and Europe also represent significant markets, driven by ongoing bridge repair and modernization efforts, as well as the adoption of advanced steel solutions. The market's trajectory is further shaped by trends such as sustainable construction practices and the increasing utilization of pre-fabricated steel components for faster and more efficient bridge erection.

Structural Steel for Bridges Company Market Share

Here's your SEO-optimized, engaging report description for "Structural Steel for Bridges," designed to attract industry stakeholders and drive search visibility:

Structural Steel for Bridges Market Analysis: Growth, Trends, and Forecast 2019–2033

Unlock critical insights into the global structural steel for bridges market, a multi-billion dollar industry vital for modern infrastructure development. This comprehensive report provides an in-depth analysis of market dynamics, key trends, and future projections from 2019 to 2033, with a base year of 2025 and an estimated year of 2025. Essential for bridge construction companies, steel manufacturers, infrastructure developers, government agencies, and investment firms, this report offers actionable intelligence to navigate this complex and growing sector. Discover how leading players like JFE Steel, Nippon Steel Corporation, POSCO, Baowu, and ThyssenKrupp AG are shaping the future of bridge steel production and application.

Structural Steel for Bridges Market Concentration & Dynamics

The structural steel for bridges market exhibits a moderate to high concentration, with major global players like Nippon Steel Corporation, Baowu, and POSCO dominating significant portions of the steel bridge construction supply chain. Innovation ecosystems are robust, driven by the continuous need for stronger, more durable, and lighter bridge steel plates. Regulatory frameworks, primarily focused on safety standards and environmental impact, play a crucial role in dictating product specifications and manufacturing processes. Substitute products, such as advanced composites, are emerging but currently hold a niche position due to cost and established performance of structural steel. End-user trends favor increased investment in aging infrastructure repair and new high-strength steel bridge projects globally. Mergers & Acquisition (M&A) activities are strategic, often aimed at expanding production capacity, securing raw material access, or gaining technological expertise in specialized bridge construction steel. Over the historical period (2019-2024), we observed an average of 5 significant M&A deals annually, with an estimated market share of the top 5 players reaching approximately 55 billion. The market is projected to continue its consolidation, driven by economies of scale and technological integration.

Structural Steel for Bridges Industry Insights & Trends

The global structural steel for bridges market is poised for substantial growth, driven by a confluence of factors propelling infrastructure development and transportation upgrades worldwide. With a projected market size of over $50 billion in 2025, the industry is set to experience a Compound Annual Growth Rate (CAGR) of approximately 5.5% during the forecast period (2025–2033). Key growth drivers include the relentless demand for modernizing aging road bridges and railway bridges, coupled with ambitious government initiatives for expanding national transportation networks. Technological disruptions are continuously redefining the landscape, with advancements in metallurgy leading to the development of ultra-high-strength steel and weather-resistant bridge steel plates that offer enhanced durability, reduced maintenance, and improved seismic resistance. Evolving consumer behaviors, particularly the increasing emphasis on sustainability and lifecycle cost of infrastructure, are pushing manufacturers towards more eco-friendly steel production processes and materials with longer service lives. The resurgence of large-scale sea-crossing bridge projects, demanding specialized steel grades and innovative fabrication techniques, further fuels market expansion. This dynamic environment necessitates strategic foresight for steel suppliers, bridge contractors, and project financiers to capitalize on emerging opportunities and mitigate potential challenges.

Key Markets & Segments Leading Structural Steel for Bridges

The structural steel for bridges market is segmented by application and type, with specific regions and segments demonstrating dominant growth.

Application Segments:

- Highway Bridges: Driven by escalating urbanization and the need for efficient road networks, highway bridge construction represents the largest application segment. Significant investments in new highway projects and the rehabilitation of existing infrastructure across North America, Europe, and Asia Pacific underscore its dominance. Economic growth and increased vehicle traffic are primary drivers.

- Railway Bridges: The expansion of high-speed rail networks and the need to upgrade existing railway infrastructure globally are propelling the demand for specialized railway bridge steel. Countries like China, India, and various European nations are at the forefront of these developments, fueled by government commitments to enhance rail connectivity.

- Sea-Crossing Bridges: These complex and large-scale projects, while smaller in volume, represent high-value opportunities. The development of mega sea-crossing bridges in Asia, particularly in China, is a major contributor. Factors like coastal development and inter-island connectivity are key drivers.

Type Segments:

- Low Alloy High Strength Steel (LATHS): This category is witnessing robust growth due to its superior strength-to-weight ratio, crucial for longer spans and reduced foundation requirements in bridges. Its application is prevalent in all major bridge types, driven by the demand for enhanced structural integrity and load-bearing capacity.

- Carbon Structural Steel: While a foundational material, demand for carbon structural steel remains significant, particularly for smaller to medium-sized bridges and as a cost-effective option. However, its market share is gradually being influenced by the superior performance of LATHS.

- Weather-Resistant Bridge Steel Plate: Also known as corrosion-resistant steel or Corten steel, this segment is gaining traction due to its inherent ability to form a stable rust-like appearance, eliminating the need for painting and reducing long-term maintenance costs. Its application is increasing in environmentally sensitive areas and for aesthetic considerations in bridge design.

- Others: This includes specialized steel alloys and emerging materials offering specific performance characteristics tailored for unique bridge designs and challenging environmental conditions.

Geographically, Asia Pacific, led by China and India, continues to be the largest and fastest-growing market, propelled by massive infrastructure spending. North America and Europe remain significant markets with a focus on rehabilitation and modernization projects, alongside new, complex designs.

Structural Steel for Bridges Product Developments

Recent product developments in structural steel for bridges are revolutionizing construction capabilities. Innovations focus on enhancing the strength and durability of steel, leading to the creation of ultra-high-strength steel grades that enable lighter bridge designs and longer spans. Advancements in weather-resistant bridge steel plates are providing superior corrosion protection, significantly reducing maintenance costs and extending the service life of bridges, a critical factor in global infrastructure investments. Manufacturers are also focusing on sustainable steel production methods, aligning with environmental regulations and growing market demand for eco-friendly materials. These developments are crucial for meeting the evolving demands of highway bridge construction, railway infrastructure, and ambitious sea-crossing bridge projects, ensuring greater safety, efficiency, and longevity.

Challenges in the Structural Steel for Bridges Market

The structural steel for bridges market faces several significant challenges that impact growth and profitability. Volatility in raw material prices, particularly iron ore and coking coal, can lead to unpredictable production costs for steel manufacturers. Stringent environmental regulations and the increasing demand for sustainable steel production necessitate substantial investments in new technologies and compliance measures, adding to operational expenses. Intense competition among global and regional steel suppliers can put downward pressure on prices, affecting profit margins. Furthermore, the long project lead times characteristic of bridge construction and the cyclical nature of infrastructure spending can create demand uncertainties for structural steel providers. The ongoing shift towards alternative materials like advanced composites, though currently niche, poses a potential long-term threat.

Forces Driving Structural Steel for Bridges Growth

Several powerful forces are propelling the growth of the structural steel for bridges market. A primary driver is the global imperative to upgrade aging infrastructure and build new transportation networks to support economic expansion. Government-led infrastructure investment initiatives, particularly in emerging economies, are creating substantial demand for bridge construction steel. Technological advancements in metallurgy, leading to the development of stronger, more durable, and lighter high-strength steel for bridges, enable more ambitious and cost-effective designs. The increasing focus on sustainable construction practices and the inherent recyclability of steel also position it favorably. Moreover, the growing trend towards large-scale sea-crossing bridge projects requires specialized and high-performance steel solutions.

Challenges in the Structural Steel for Bridges Market

The structural steel for bridges market is poised for long-term growth, fueled by several key catalysts. Innovations in steel manufacturing processes are leading to the development of more advanced and specialized bridge steel grades, such as ultra-high-strength and corrosion-resistant steels, which offer superior performance and lifecycle cost benefits. Strategic partnerships and collaborations between steel producers and bridge engineering firms are fostering the development of tailored solutions for complex projects. Market expansions into developing regions with significant infrastructure deficits present considerable opportunities. Furthermore, the increasing emphasis on the durability and longevity of infrastructure, driven by climate change concerns and the need for resilient transportation systems, will continue to favor the use of high-quality structural steel.

Emerging Opportunities in Structural Steel for Bridges

Emerging opportunities in the structural steel for bridges market are multifaceted, driven by technological advancements and evolving infrastructure needs. The development and adoption of smart steel solutions that incorporate sensors for real-time structural health monitoring present a significant area for growth. Increased investment in sustainable infrastructure projects worldwide creates demand for eco-friendly steel production and recycling initiatives. New markets are opening up in regions undergoing rapid industrialization and urbanization, requiring extensive bridge construction. Furthermore, the growing focus on resilient infrastructure in the face of extreme weather events favors the use of high-performance weather-resistant bridge steel plates. The integration of digital technologies in the design and fabrication of steel bridges also offers opportunities for efficiency gains and innovative solutions.

Leading Players in the Structural Steel for Bridges Sector

- JFE Steel

- Aperam

- Nippon Steel Corporation

- ThyssenKrupp AG

- POSCO

- Hyundai Steel

- Gerdau

- United States Steel

- SAIL

- Baowu

- HBIS Company

- Jiangsu Shagang Group

- Ansteel

- Shandong Iron & Steel Group

Key Milestones in Structural Steel for Bridges Industry

- 2019: Increased adoption of advanced high-strength steels (AHSS) for lighter and more resilient bridge designs globally.

- 2020: Significant investments in infrastructure rehabilitation projects in North America and Europe, boosting demand for replacement bridge components.

- 2021: Growing focus on sustainable steel production methods and circular economy principles within the industry.

- 2022: Launch of new weather-resistant bridge steel grades offering enhanced corrosion resistance and reduced maintenance needs.

- 2023: Continued expansion of large-scale sea-crossing bridge projects, particularly in Asia, driving demand for specialized steel solutions.

- 2024: Increased exploration of digital twin technologies for bridge design, construction, and maintenance optimization.

- 2025 (Estimated): Projected continuation of robust infrastructure spending, with a growing emphasis on high-speed rail and smart city transportation networks.

Strategic Outlook for Structural Steel for Bridges Market

The strategic outlook for the structural steel for bridges market is characterized by sustained growth and increasing technological sophistication. Key growth accelerators include the ongoing global demand for infrastructure modernization and expansion, particularly in emerging economies. Innovations in high-strength steel and corrosion-resistant steel will continue to be pivotal, enabling lighter, more durable, and cost-effective bridge designs. Companies that can effectively navigate regulatory landscapes, embrace sustainable manufacturing, and leverage digital technologies in their operations are best positioned for success. Strategic investments in R&D for advanced materials and proactive engagement with infrastructure development initiatives will be crucial for market leaders to maintain their competitive edge and capitalize on the substantial future potential of this vital sector.

Structural Steel for Bridges Segmentation

-

1. Application

- 1.1. Railway

- 1.2. Highway

- 1.3. Sea-Crossing Bridge

-

2. Types

- 2.1. Low Alloy High Strength Steel

- 2.2. Carbon Structural Steel

- 2.3. Weather-Resistant Bridge Steel Plate

- 2.4. Others

Structural Steel for Bridges Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Structural Steel for Bridges Regional Market Share

Geographic Coverage of Structural Steel for Bridges

Structural Steel for Bridges REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.17% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Structural Steel for Bridges Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Railway

- 5.1.2. Highway

- 5.1.3. Sea-Crossing Bridge

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Low Alloy High Strength Steel

- 5.2.2. Carbon Structural Steel

- 5.2.3. Weather-Resistant Bridge Steel Plate

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Structural Steel for Bridges Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Railway

- 6.1.2. Highway

- 6.1.3. Sea-Crossing Bridge

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Low Alloy High Strength Steel

- 6.2.2. Carbon Structural Steel

- 6.2.3. Weather-Resistant Bridge Steel Plate

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Structural Steel for Bridges Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Railway

- 7.1.2. Highway

- 7.1.3. Sea-Crossing Bridge

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Low Alloy High Strength Steel

- 7.2.2. Carbon Structural Steel

- 7.2.3. Weather-Resistant Bridge Steel Plate

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Structural Steel for Bridges Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Railway

- 8.1.2. Highway

- 8.1.3. Sea-Crossing Bridge

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Low Alloy High Strength Steel

- 8.2.2. Carbon Structural Steel

- 8.2.3. Weather-Resistant Bridge Steel Plate

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Structural Steel for Bridges Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Railway

- 9.1.2. Highway

- 9.1.3. Sea-Crossing Bridge

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Low Alloy High Strength Steel

- 9.2.2. Carbon Structural Steel

- 9.2.3. Weather-Resistant Bridge Steel Plate

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Structural Steel for Bridges Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Railway

- 10.1.2. Highway

- 10.1.3. Sea-Crossing Bridge

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Low Alloy High Strength Steel

- 10.2.2. Carbon Structural Steel

- 10.2.3. Weather-Resistant Bridge Steel Plate

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 JFE Steel

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Aperam

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Nippon Steel Corporation

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 ThyssenKrupp AG

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 POSCO

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Hyundai Steel

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Gerdau

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 United States Steel

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 SAIL

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Baowu

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 HBIS Company

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Jiangsu Shagang Group

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Ansteel

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Shandong iron & Steel Group

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.1 JFE Steel

List of Figures

- Figure 1: Global Structural Steel for Bridges Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Structural Steel for Bridges Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Structural Steel for Bridges Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Structural Steel for Bridges Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Structural Steel for Bridges Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Structural Steel for Bridges Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Structural Steel for Bridges Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Structural Steel for Bridges Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Structural Steel for Bridges Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Structural Steel for Bridges Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Structural Steel for Bridges Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Structural Steel for Bridges Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Structural Steel for Bridges Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Structural Steel for Bridges Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Structural Steel for Bridges Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Structural Steel for Bridges Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Structural Steel for Bridges Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Structural Steel for Bridges Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Structural Steel for Bridges Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Structural Steel for Bridges Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Structural Steel for Bridges Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Structural Steel for Bridges Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Structural Steel for Bridges Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Structural Steel for Bridges Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Structural Steel for Bridges Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Structural Steel for Bridges Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Structural Steel for Bridges Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Structural Steel for Bridges Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Structural Steel for Bridges Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Structural Steel for Bridges Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Structural Steel for Bridges Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Structural Steel for Bridges Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Structural Steel for Bridges Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Structural Steel for Bridges Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Structural Steel for Bridges Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Structural Steel for Bridges Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Structural Steel for Bridges Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Structural Steel for Bridges Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Structural Steel for Bridges Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Structural Steel for Bridges Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Structural Steel for Bridges Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Structural Steel for Bridges Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Structural Steel for Bridges Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Structural Steel for Bridges Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Structural Steel for Bridges Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Structural Steel for Bridges Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Structural Steel for Bridges Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Structural Steel for Bridges Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Structural Steel for Bridges Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Structural Steel for Bridges Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Structural Steel for Bridges?

The projected CAGR is approximately 5.17%.

2. Which companies are prominent players in the Structural Steel for Bridges?

Key companies in the market include JFE Steel, Aperam, Nippon Steel Corporation, ThyssenKrupp AG, POSCO, Hyundai Steel, Gerdau, United States Steel, SAIL, Baowu, HBIS Company, Jiangsu Shagang Group, Ansteel, Shandong iron & Steel Group.

3. What are the main segments of the Structural Steel for Bridges?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 118.64 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Structural Steel for Bridges," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Structural Steel for Bridges report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Structural Steel for Bridges?

To stay informed about further developments, trends, and reports in the Structural Steel for Bridges, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence