Key Insights

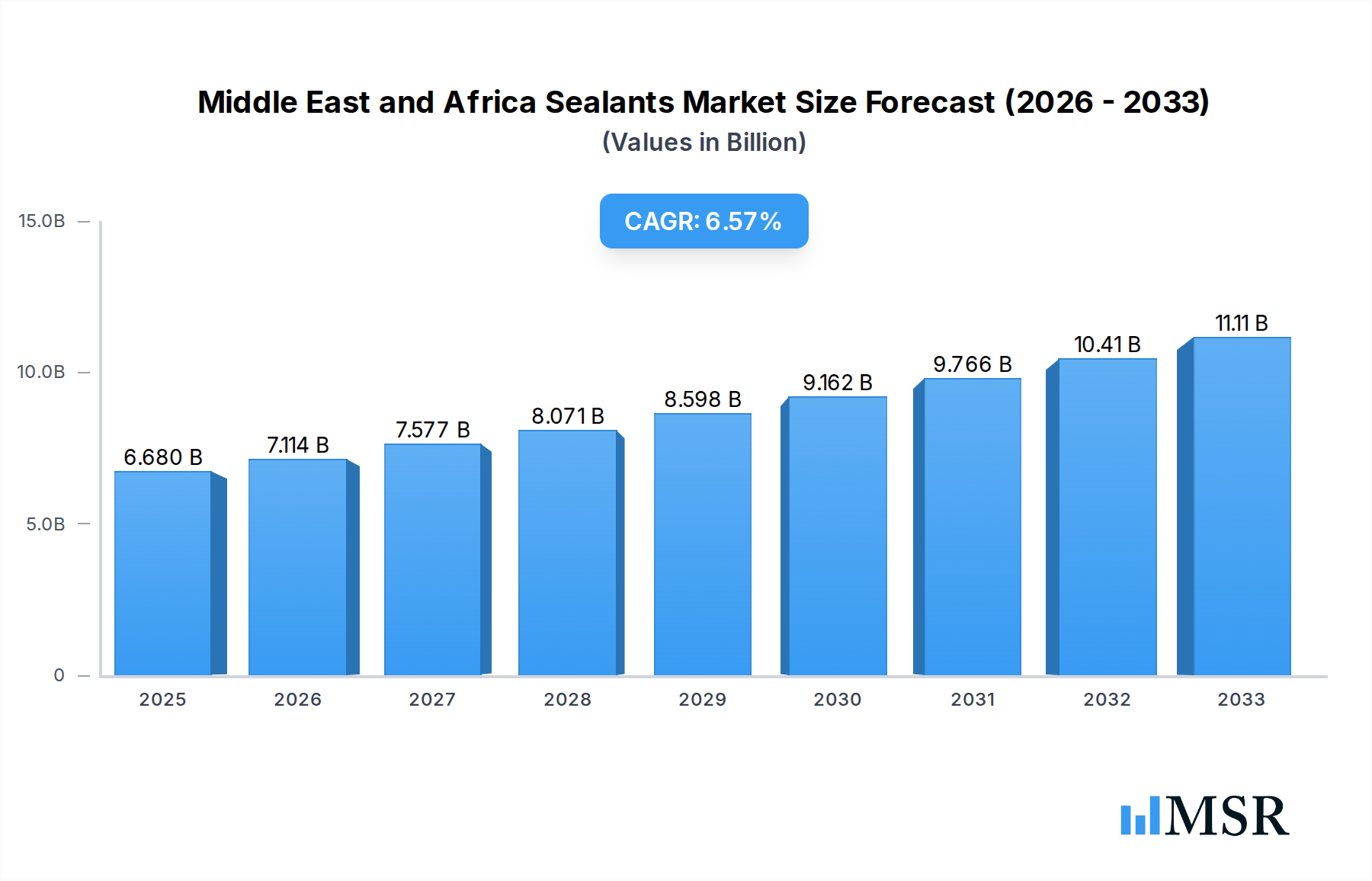

The Middle East and Africa (MEA) Sealants Market is poised for robust expansion, projected to reach USD 6.68 billion in 2025 and grow at a compelling Compound Annual Growth Rate (CAGR) of 6.5% through 2033. This significant growth is underpinned by a confluence of dynamic drivers and evolving market trends across the region. The increasing demand for advanced building and construction solutions, fueled by rapid urbanization and infrastructure development, particularly in emerging economies within MEA, is a primary catalyst. Furthermore, the automotive sector's resurgence and the growing adoption of lightweight materials in vehicle manufacturing are contributing to the uptake of specialized sealants. The aerospace industry's expansion and the healthcare sector's increasing reliance on high-performance sealing materials for medical devices and facilities also present substantial opportunities.

Middle East and Africa Sealants Market Market Size (In Billion)

The market's trajectory is further shaped by the increasing preference for sustainable and eco-friendly sealant formulations, aligning with global environmental initiatives. Innovations in resin technology, such as advanced acrylic, epoxy, and polyurethane formulations, are offering enhanced durability, flexibility, and chemical resistance, thereby broadening their application scope. While the market benefits from these drivers, potential restraints include volatile raw material prices and the availability of skilled labor for application. However, the strategic focus on developing and manufacturing these high-performance sealants within the MEA region, coupled with investments in research and development, is expected to mitigate these challenges and sustain the market's upward momentum. Key segments, including acrylic and epoxy resins, alongside the dominant end-user industries of building & construction and automotive, will continue to drive market value and volume.

Middle East and Africa Sealants Market Company Market Share

Discover critical insights into the burgeoning Middle East and Africa Sealants Market, valued at an estimated $7.2 billion in 2025 and projected to reach $12.5 billion by 2033, exhibiting a robust CAGR of 7.1% from 2025-2033. This comprehensive report delves into the intricate dynamics, key trends, and future trajectory of this vital sector. Analyze market size, growth drivers, competitive landscape, and strategic opportunities for stakeholders seeking to capitalize on the region's rapid development.

Middle East and Africa Sealants Market Market Concentration & Dynamics

The Middle East and Africa (MEA) sealants market demonstrates a moderate level of concentration, with a few dominant global players alongside a growing number of regional manufacturers. Innovation ecosystems are rapidly evolving, driven by increasing demand for advanced material solutions across diverse industries. Regulatory frameworks are becoming more defined, with a focus on environmental sustainability and product safety, influencing formulation and application. Substitute products, while present, face increasing competition from high-performance sealants offering superior durability and functionality. End-user trends are heavily influenced by infrastructure development, urbanization, and a growing automotive manufacturing base. Mergers and acquisitions (M&A) activities are anticipated to play a significant role in market consolidation and expansion, with approximately 15-20 significant M&A deals expected within the study period. Key players actively pursue strategic partnerships and expansions to strengthen their market share.

- Market Share: Dominated by leading global chemical companies and specialized sealant manufacturers.

- Innovation Ecosystems: Emerging R&D hubs focusing on sustainable and high-performance sealants.

- Regulatory Frameworks: Increasing emphasis on VOC reduction, durability standards, and safety certifications.

- Substitute Products: Emerging alternatives from bio-based materials and advanced polymer technologies.

- End-User Trends: Driven by construction boom, automotive production, and industrial maintenance.

- M&A Activities: Strategic acquisitions and partnerships to expand product portfolios and geographic reach.

Middle East and Africa Sealants Market Industry Insights & Trends

The Middle East and Africa sealants market is poised for substantial growth, projected to expand from an estimated $7.2 billion in 2025 to $12.5 billion by 2033, with a compound annual growth rate (CAGR) of 7.1% during the forecast period (2025–2033). This impressive expansion is fueled by a confluence of powerful market growth drivers, including rapid urbanization and large-scale infrastructure projects across the MEA region. Government initiatives focused on economic diversification and the development of smart cities are creating unprecedented demand for construction sealants, vital for enhancing building energy efficiency, structural integrity, and aesthetic appeal. The automotive sector's resurgence, with increasing local manufacturing and vehicle production, further bolsters the need for specialized automotive sealants that ensure safety, comfort, and durability. Technological disruptions are continuously shaping the industry, with a growing emphasis on the development and adoption of eco-friendly, low-VOC (Volatile Organic Compound) sealants, driven by stringent environmental regulations and increasing consumer awareness regarding health and sustainability. The shift towards advanced silicone and polyurethane-based sealants, offering superior adhesion, flexibility, and weather resistance, is a notable trend. Evolving consumer behaviors are also playing a critical role, with a greater demand for high-performance, long-lasting, and easy-to-apply sealant solutions across both industrial and DIY segments. The building and construction sector, representing the largest end-user industry, is expected to witness consistent growth due to ongoing residential, commercial, and industrial construction activities. The automotive sector follows, driven by both OEM and aftermarket applications. The report also details the market size and CAGR for various resin types and niche end-user industries, providing a granular understanding of the market's potential.

Key Markets & Segments Leading Middle East and Africa Sealants Market

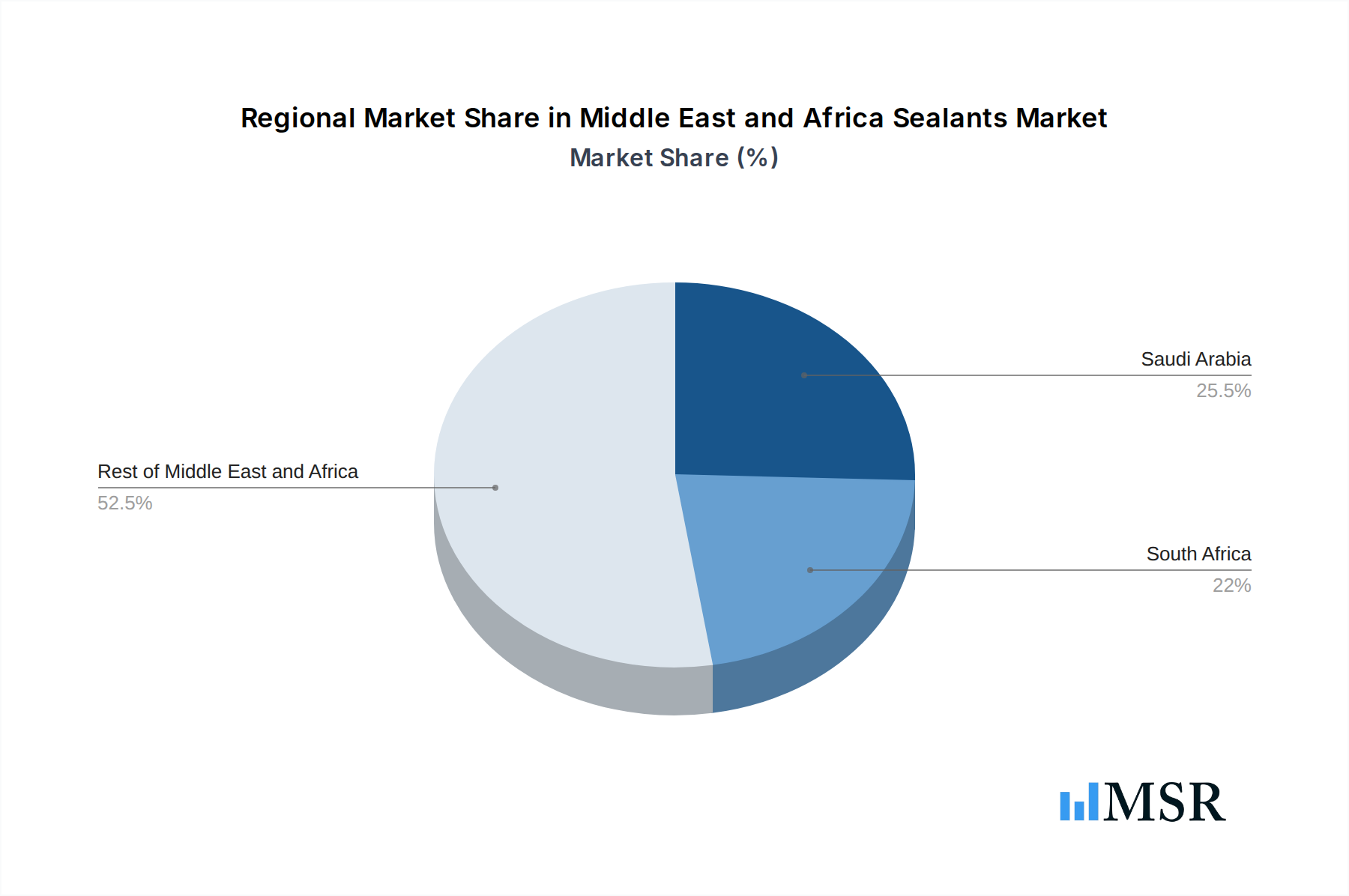

The Middle East and Africa sealants market is significantly driven by robust growth in the Building and Construction end-user industry. This segment is propelled by substantial government investments in infrastructure development, housing projects, and commercial complexes across key economies. Saudi Arabia, in particular, stands out as a dominant market due to its ambitious Vision 2030 plan, which encompasses mega-projects like NEOM and the Red Sea Project, requiring vast quantities of high-performance sealants for architectural, structural, and waterproofing applications. South Africa, with its established industrial base and ongoing urban renewal initiatives, also presents a significant market. The "Rest of Middle-East and Africa" segment, encompassing rapidly developing nations in the GCC and Sub-Saharan Africa, is characterized by high growth potential, fueled by increasing disposable incomes and a burgeoning middle class driving demand for modern housing and infrastructure.

Within the resin segments, Silicone sealants exhibit strong dominance due to their exceptional flexibility, UV resistance, and durability, making them ideal for façade sealing, window glazing, and weatherproofing in diverse climatic conditions prevalent in the region. Polyurethane sealants also hold a significant market share, valued for their strength, abrasion resistance, and excellent adhesion to various substrates, crucial for automotive and construction applications. Acrylic sealants cater to a broad range of interior and exterior applications, offering good performance and cost-effectiveness. Epoxy sealants are primarily used in industrial applications requiring high strength and chemical resistance.

- Dominant End-User Industry: Building and Construction, driven by extensive infrastructure projects and urbanization.

- Drivers: Government infrastructure spending, housing demand, commercial development, energy efficiency mandates.

- Saudi Arabia: Leading market due to Vision 2030 mega-projects and significant construction activity.

- South Africa: Established construction sector, urban renewal projects, and infrastructure upgrades.

- Rest of Middle-East and Africa: High growth potential from developing economies and increasing urbanization.

- Dominant Resin Segments:

- Silicone Sealants: Preferred for their superior weatherability, UV resistance, and flexibility in diverse climatic conditions.

- Polyurethane Sealants: Valued for high strength, abrasion resistance, and excellent adhesion in automotive and construction.

- Acrylic Sealants: Widely used for general-purpose interior and exterior applications due to cost-effectiveness and ease of use.

- Epoxy Sealants: Essential for industrial applications demanding high chemical and mechanical resistance.

Middle East and Africa Sealants Market Product Developments

Product innovation is a key differentiator in the MEA sealants market. Manufacturers are focusing on developing next-generation sealants that offer enhanced performance, sustainability, and ease of application. Recent advancements include the introduction of low-VOC and solvent-free formulations to meet stringent environmental regulations and cater to growing health consciousness. Innovations in silicone and polyurethane technologies are yielding sealants with improved adhesion to challenging substrates, greater flexibility for seismic resilience, and extended service life in harsh climatic conditions. The development of specialized sealants for emerging applications, such as advanced façade systems and electric vehicle assembly, further underscores the industry's dynamic nature and commitment to technological progress.

Challenges in the Middle East and Africa Sealants Market Market

The Middle East and Africa sealants market faces several challenges that impact its growth trajectory. Price sensitivity among certain end-users, particularly in developing economies, can lead to the preference for lower-cost, albeit less durable, alternatives. Supply chain disruptions and logistical complexities across vast and diverse geographical regions can lead to increased lead times and operational costs. Furthermore, fierce competition from both global giants and local players intensifies pricing pressures. Ensuring consistent product quality and adherence to varying regional building codes and standards also presents a significant hurdle for manufacturers aiming for widespread adoption.

Forces Driving Middle East and Africa Sealants Market Growth

Several key forces are propelling the growth of the Middle East and Africa sealants market. Foremost is the accelerated pace of construction and infrastructure development, fueled by government initiatives and economic diversification plans. The increasing focus on energy efficiency and sustainable building practices is driving demand for advanced sealants that improve building envelopes and reduce energy consumption. The growing automotive manufacturing sector across the region is another significant growth catalyst, necessitating high-performance sealants for vehicle assembly and repair. Furthermore, rising disposable incomes and urbanization are leading to increased demand for higher-quality housing and commercial spaces, where reliable sealants are paramount.

Challenges in the Middle East and Africa Sealants Market Market

Long-term growth catalysts for the Middle East and Africa sealants market lie in continued technological innovation and product diversification. The development of smart sealants with self-healing properties or embedded sensors represents a future frontier. Strategic partnerships and collaborations between raw material suppliers, sealant manufacturers, and construction companies will foster innovation and market penetration. Market expansion into untapped African nations, supported by improved infrastructure and economic stability, offers substantial untapped potential. A sustained focus on research and development for sustainable and bio-based sealants will align with global environmental trends and create a competitive advantage.

Emerging Opportunities in Middle East and Africa Sealants Market

Emerging opportunities in the MEA sealants market are abundant and diverse. The rapid growth of renewable energy infrastructure, such as solar farms and wind turbines, creates a demand for specialized sealants to protect these installations from harsh environmental elements. The booming tourism and hospitality sectors in many MEA countries are driving the construction of luxury resorts and hotels, requiring high-performance architectural sealants. The increasing adoption of modular and prefabricated construction techniques presents opportunities for specialized, fast-curing sealants. Furthermore, growing awareness and demand for DIY and home improvement solutions offer a significant untapped market for consumer-grade sealants.

Leading Players in the Middle East and Africa Sealants Market Sector

- Henkel AG & Co KGaA

- NATIONAL ADHESIVE INC

- 3M

- The Industrial Group Ltd

- Arkema Group

- Dow

- H B Fuller Company

- Soudal Holding N V

- MAPEI S p A

- Sika AG

- Wacker Chemie AG

- Permoseal (Pty) Ltd

Key Milestones in Middle East and Africa Sealants Market Industry

- January 2020: H.B. Fuller Company introduced a new range of Gorilla professional-grade adhesives and sealants for MRO industrial applications, expanding its product portfolio for industrial maintenance and repair sectors.

- December 2020: Wacker Chemie AG launched renewables-based silicone sealants, extending its portfolio with a focus on sustainability and eco-friendly solutions.

Strategic Outlook for Middle East and Africa Sealants Market Market

The strategic outlook for the Middle East and Africa sealants market is exceptionally positive, driven by robust economic development and significant investment in infrastructure. Key growth accelerators include the ongoing mega-projects in the GCC, the expanding automotive industry, and the increasing adoption of energy-efficient building solutions. Manufacturers who focus on developing innovative, sustainable, and high-performance sealants tailored to the region's specific climatic and application needs will be well-positioned for success. Strategic opportunities lie in expanding product portfolios to include specialized sealants for emerging sectors like renewable energy and modular construction, while also leveraging digital channels to enhance customer engagement and distribution networks across diverse geographies.

Middle East and Africa Sealants Market Segmentation

-

1. Resin

- 1.1. Acrylic

- 1.2. Epoxy

- 1.3. Polyurethane

- 1.4. Silicone

- 1.5. Other Resins

-

2. End-User Industry

- 2.1. Aerospace

- 2.2. Automotive

- 2.3. Building and Construction

- 2.4. Healthcare

- 2.5. Other End-user Industries

-

3. Geography

- 3.1. Saudi Arabia

- 3.2. South Africa

- 3.3. Rest of Middle-East and Africa

Middle East and Africa Sealants Market Segmentation By Geography

- 1. Saudi Arabia

- 2. South Africa

- 3. Rest of Middle East and Africa

Middle East and Africa Sealants Market Regional Market Share

Geographic Coverage of Middle East and Africa Sealants Market

Middle East and Africa Sealants Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Resin

- 5.1.1. Acrylic

- 5.1.2. Epoxy

- 5.1.3. Polyurethane

- 5.1.4. Silicone

- 5.1.5. Other Resins

- 5.2. Market Analysis, Insights and Forecast - by End-User Industry

- 5.2.1. Aerospace

- 5.2.2. Automotive

- 5.2.3. Building and Construction

- 5.2.4. Healthcare

- 5.2.5. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. Saudi Arabia

- 5.3.2. South Africa

- 5.3.3. Rest of Middle-East and Africa

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Saudi Arabia

- 5.4.2. South Africa

- 5.4.3. Rest of Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Resin

- 6. Middle East and Africa Sealants Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Resin

- 6.1.1. Acrylic

- 6.1.2. Epoxy

- 6.1.3. Polyurethane

- 6.1.4. Silicone

- 6.1.5. Other Resins

- 6.2. Market Analysis, Insights and Forecast - by End-User Industry

- 6.2.1. Aerospace

- 6.2.2. Automotive

- 6.2.3. Building and Construction

- 6.2.4. Healthcare

- 6.2.5. Other End-user Industries

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. Saudi Arabia

- 6.3.2. South Africa

- 6.3.3. Rest of Middle-East and Africa

- 6.1. Market Analysis, Insights and Forecast - by Resin

- 7. Saudi Arabia Middle East and Africa Sealants Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Resin

- 7.1.1. Acrylic

- 7.1.2. Epoxy

- 7.1.3. Polyurethane

- 7.1.4. Silicone

- 7.1.5. Other Resins

- 7.2. Market Analysis, Insights and Forecast - by End-User Industry

- 7.2.1. Aerospace

- 7.2.2. Automotive

- 7.2.3. Building and Construction

- 7.2.4. Healthcare

- 7.2.5. Other End-user Industries

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. Saudi Arabia

- 7.3.2. South Africa

- 7.3.3. Rest of Middle-East and Africa

- 7.1. Market Analysis, Insights and Forecast - by Resin

- 8. South Africa Middle East and Africa Sealants Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Resin

- 8.1.1. Acrylic

- 8.1.2. Epoxy

- 8.1.3. Polyurethane

- 8.1.4. Silicone

- 8.1.5. Other Resins

- 8.2. Market Analysis, Insights and Forecast - by End-User Industry

- 8.2.1. Aerospace

- 8.2.2. Automotive

- 8.2.3. Building and Construction

- 8.2.4. Healthcare

- 8.2.5. Other End-user Industries

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. Saudi Arabia

- 8.3.2. South Africa

- 8.3.3. Rest of Middle-East and Africa

- 8.1. Market Analysis, Insights and Forecast - by Resin

- 9. Rest of Middle East and Africa Middle East and Africa Sealants Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Resin

- 9.1.1. Acrylic

- 9.1.2. Epoxy

- 9.1.3. Polyurethane

- 9.1.4. Silicone

- 9.1.5. Other Resins

- 9.2. Market Analysis, Insights and Forecast - by End-User Industry

- 9.2.1. Aerospace

- 9.2.2. Automotive

- 9.2.3. Building and Construction

- 9.2.4. Healthcare

- 9.2.5. Other End-user Industries

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. Saudi Arabia

- 9.3.2. South Africa

- 9.3.3. Rest of Middle-East and Africa

- 9.1. Market Analysis, Insights and Forecast - by Resin

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Henkel AG & Co KGaA

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 NATIONAL ADHESIVE INC

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 3M

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 The Industrial Group Ltd

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 Arkema Group

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 Dow

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 H B Fuller Company

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Soudal Holding N V

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 MAPEI S p A

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.10 Sika AG

- 10.1.10.1. Company Overview

- 10.1.10.2. Products

- 10.1.10.3. Company Financials

- 10.1.10.4. SWOT Analysis

- 10.1.11 Wacker Chemie AG*List Not Exhaustive

- 10.1.11.1. Company Overview

- 10.1.11.2. Products

- 10.1.11.3. Company Financials

- 10.1.11.4. SWOT Analysis

- 10.1.12 Permoseal (Pty) Ltd

- 10.1.12.1. Company Overview

- 10.1.12.2. Products

- 10.1.12.3. Company Financials

- 10.1.12.4. SWOT Analysis

- 10.1.1 Henkel AG & Co KGaA

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: Middle East and Africa Sealants Market Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Middle East and Africa Sealants Market Share (%) by Company 2025

List of Tables

- Table 1: Middle East and Africa Sealants Market Revenue million Forecast, by Resin 2020 & 2033

- Table 2: Middle East and Africa Sealants Market Revenue million Forecast, by End-User Industry 2020 & 2033

- Table 3: Middle East and Africa Sealants Market Revenue million Forecast, by Geography 2020 & 2033

- Table 4: Middle East and Africa Sealants Market Revenue million Forecast, by Region 2020 & 2033

- Table 5: Middle East and Africa Sealants Market Revenue million Forecast, by Resin 2020 & 2033

- Table 6: Middle East and Africa Sealants Market Revenue million Forecast, by End-User Industry 2020 & 2033

- Table 7: Middle East and Africa Sealants Market Revenue million Forecast, by Geography 2020 & 2033

- Table 8: Middle East and Africa Sealants Market Revenue million Forecast, by Country 2020 & 2033

- Table 9: Middle East and Africa Sealants Market Revenue million Forecast, by Resin 2020 & 2033

- Table 10: Middle East and Africa Sealants Market Revenue million Forecast, by End-User Industry 2020 & 2033

- Table 11: Middle East and Africa Sealants Market Revenue million Forecast, by Geography 2020 & 2033

- Table 12: Middle East and Africa Sealants Market Revenue million Forecast, by Country 2020 & 2033

- Table 13: Middle East and Africa Sealants Market Revenue million Forecast, by Resin 2020 & 2033

- Table 14: Middle East and Africa Sealants Market Revenue million Forecast, by End-User Industry 2020 & 2033

- Table 15: Middle East and Africa Sealants Market Revenue million Forecast, by Geography 2020 & 2033

- Table 16: Middle East and Africa Sealants Market Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Middle East and Africa Sealants Market?

The projected CAGR is approximately 6.2%.

2. Which companies are prominent players in the Middle East and Africa Sealants Market?

Key companies in the market include Henkel AG & Co KGaA, NATIONAL ADHESIVE INC, 3M, The Industrial Group Ltd, Arkema Group, Dow, H B Fuller Company, Soudal Holding N V, MAPEI S p A, Sika AG, Wacker Chemie AG*List Not Exhaustive, Permoseal (Pty) Ltd.

3. What are the main segments of the Middle East and Africa Sealants Market?

The market segments include Resin, End-User Industry, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 808.49 million as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand from the Construction Industry in Saudi Arabia; Other Drivers.

6. What are the notable trends driving market growth?

The Construction End-User Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

; Impact of COVID-19 Pandemic on Global Economy.

8. Can you provide examples of recent developments in the market?

In Jan 2020, H.B. Fuller Company introduced a new range of Gorilla professional-grade adhesives and sealants for MRO industrial applications.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Middle East and Africa Sealants Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Middle East and Africa Sealants Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Middle East and Africa Sealants Market?

To stay informed about further developments, trends, and reports in the Middle East and Africa Sealants Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence