Key Insights

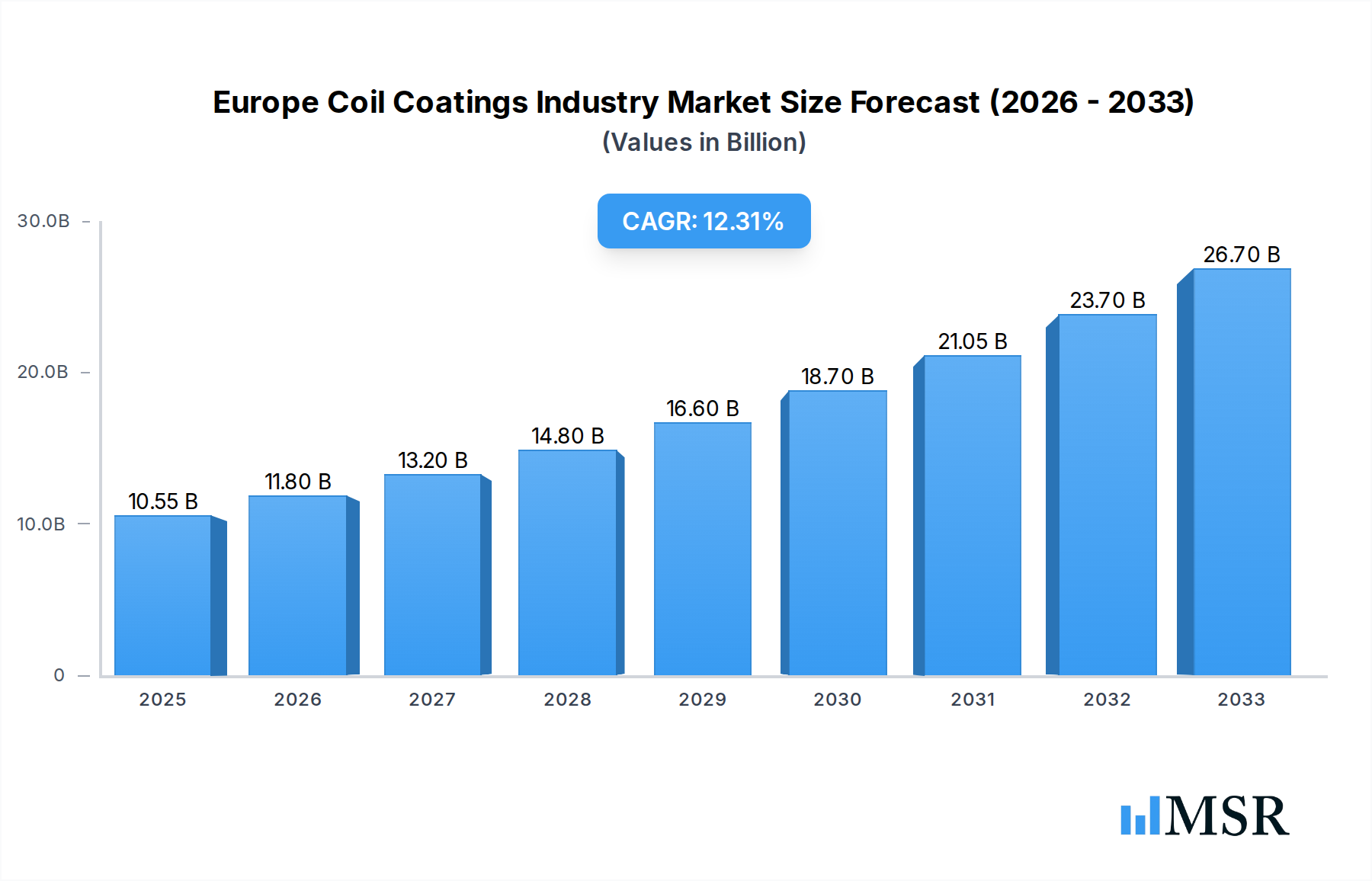

The Europe Coil Coatings market is poised for significant expansion, projecting a robust market size of $10.55 billion in 2025, with a compelling CAGR of 12.06% anticipated throughout the forecast period extending to 2033. This strong growth trajectory is fueled by escalating demand across key end-user industries. The building and construction sector remains a primary driver, benefiting from the increasing adoption of pre-painted metal for architectural facades, roofing, and interior components due to their aesthetic appeal, durability, and cost-effectiveness. The automotive industry is also a substantial contributor, with coil coatings playing a crucial role in enhancing vehicle aesthetics and providing essential corrosion protection for body panels. Furthermore, growing industrial and domestic appliance manufacturing, alongside the furniture sector's preference for durable and attractive finishes, further bolsters market demand. The HVAC segment also presents a steady demand for coil-coated materials.

Europe Coil Coatings Industry Market Size (In Billion)

The market's expansion is further propelled by ongoing technological advancements in coating formulations, leading to the development of more environmentally friendly and high-performance solutions, such as those based on Polyester and Polyvinylidene Fluorides (PVDF) resins. These advancements address stricter environmental regulations and meet the evolving needs for superior durability, UV resistance, and chemical inertness. While the market enjoys robust growth, certain factors could influence its pace. Restraints might include fluctuations in raw material prices, particularly for resins and pigments, and intense competition among established players, including prominent coil coaters, paint suppliers, and pretreatment resin manufacturers. However, the overall outlook for the Europe Coil Coatings market remains overwhelmingly positive, driven by innovation and the continuous integration of these coatings into a widening array of applications that prioritize both performance and visual appeal.

Europe Coil Coatings Industry Company Market Share

This comprehensive report provides an in-depth analysis of the Europe Coil Coatings Industry, a vital sector driving innovation and sustainability across numerous applications. Spanning from 2019 to 2033, with a base year of 2025 and a forecast period extending to 2033, this report offers critical insights into market dynamics, growth drivers, emerging trends, and competitive landscapes.

Europe Coil Coatings Industry Market Concentration & Dynamics

The Europe coil coatings market exhibits a moderately concentrated landscape, influenced by a blend of established global players and regional specialists. Key participants, including Coil Coaters like ArcelorMittal, Arconic, Alcoa Corporation, Norsk Hydro ASA, Novelis, Rautaruukki Corporation, Salzgitter Flachstahl GmbH, Tata Steel, and Thyssenkrupp, alongside Paint Suppliers such as AkzoNobel N V, Axalta Coatings Systems, Beckers Group, Kansai Paint Co Ltd, PPG Industries Inc, The Sherwin-Williams Company, NIPPONPAINT Co Ltd, Brillux GmbH & Co KG, and Hempel A/S, exert significant influence. Furthermore, Pretreatment Resins Pigments and Equipment providers like Wacker Chemie AG, Arkema Group, Bayer AG, BASF SE, Evonik Industries AG, Henkel AG & Co KGaA, and Solvay are integral to the ecosystem. The innovation ecosystem is robust, fueled by continuous R&D in low-VOC coatings and high-performance formulations. Regulatory frameworks, particularly those from the European Union concerning environmental impact and chemical safety, are shaping product development and market entry. Substitute products, such as powder coatings and liquid painting, present a competitive challenge, though coil coatings retain advantages in efficiency and consistency for large-scale applications. End-user trends lean towards sustainable building materials and enhanced durability in appliances. Mergers and acquisitions (M&A) activities have been notable, with an estimated XX M&A deal count between 2019-2024, contributing to market consolidation and strategic expansion. The market share of leading players is projected to shift as sustainability initiatives gain further traction.

Europe Coil Coatings Industry Industry Insights & Trends

The Europe Coil Coatings Industry is poised for significant expansion, driven by a confluence of escalating demand from key end-user sectors and a relentless pursuit of sustainable and advanced material solutions. The market size for Europe's coil coatings sector is estimated to reach approximately XX billion in 2025, with a projected Compound Annual Growth Rate (CAGR) of XX% from 2025 to 2033. This robust growth trajectory is underpinned by several critical factors. Firstly, the Building and Construction segment continues to be a primary demand generator, fueled by extensive infrastructure development projects across the continent, a growing emphasis on energy-efficient buildings, and the aesthetic appeal offered by pre-coated metal sheets for facades, roofing, and interior applications. The increasing adoption of green building standards further amplifies the demand for eco-friendly coil coating solutions. Secondly, the Industrial and Domestic Appliances sector is witnessing a surge in demand for durable, aesthetically pleasing, and scratch-resistant surfaces, making coil-coated metals an ideal choice for refrigerators, washing machines, ovens, and other white goods. Technological advancements in coil coating formulations are enabling manufacturers to achieve superior finishes and enhanced product lifespans.

The Automotive industry, while undergoing transformation, remains a significant contributor, with coil coatings utilized in vehicle bodies, interior components, and structural parts, offering corrosion resistance and aesthetic versatility. The push towards lightweight materials in automotive manufacturing also favors the use of pre-coated metal solutions. Furthermore, the Furniture and HVAC sectors are increasingly incorporating coil-coated metals for their durability, design flexibility, and cost-effectiveness. The ability of coil coatings to mimic various textures and finishes, coupled with their resistance to wear and tear, makes them attractive for furniture manufacturers and HVAC system components. Evolving consumer behaviors are also playing a crucial role, with a growing preference for products that are not only functional but also environmentally conscious and visually appealing. This trend encourages the development and adoption of low-VOC (Volatile Organic Compound) and VOC-free coil coatings, as well as those derived from renewable resources. Technological disruptions, such as advancements in curing technologies, digital printing on coated metals, and the development of self-cleaning or anti-microbial coatings, are further shaping the market, offering enhanced performance and novel functionalities. The overall market is characterized by a strong emphasis on product innovation, sustainability, and meeting the diverse needs of a dynamic European industrial landscape.

Key Markets & Segments Leading Europe Coil Coatings Industry

The Europe Coil Coatings Industry's dominance is significantly influenced by specific geographical regions and end-user segments, driven by economic vigor and evolving industrial demands.

Dominant Resin Type:

- Polyester: This resin type consistently holds a leading position due to its excellent balance of cost-effectiveness, durability, and flexibility. It finds widespread application in the Building and Construction sector for roofing and facade panels, and in Industrial and Domestic Appliances due to its good weatherability and wide color palette. Its adaptability to various finishing requirements makes it a preferred choice for mass-market applications.

- Polyvinylidene Fluorides (PVDF): While typically commanding a higher price point, PVDF resins are crucial for high-performance applications where exceptional UV resistance, chemical inertness, and long-term durability are paramount. The Building and Construction sector, particularly for premium facades and architectural elements, as well as the Automotive sector for exterior trim and components requiring superior weatherability, are key consumers. The extended lifespan and low maintenance offered by PVDF coatings justify their premium cost.

- Polyurethane (PU): PU coatings offer a good blend of flexibility, hardness, and chemical resistance, making them suitable for applications requiring a balance of performance and aesthetic appeal. They are widely used in Industrial and Domestic Appliances and Furniture where durability and a high-quality finish are desired.

- Plastisols: Known for their excellent formability, abrasion resistance, and impact absorption, Plastisols are particularly dominant in applications requiring robust protection and flexibility, such as in the roofing industry for membranes and in automotive underbody coatings.

Dominant End-user Industry:

- Building and Construction: This segment stands as the largest and most influential driver of the Europe Coil Coatings Industry. The ongoing urbanization, substantial infrastructure investments across European nations, and a growing demand for sustainable and aesthetically pleasing architectural solutions are fueling this dominance. The industry benefits from governmental incentives for energy-efficient buildings and renovations, which often favor materials utilizing advanced coil coatings for enhanced insulation and weather resistance. The resilience and longevity of coil-coated metal sheets for roofing, cladding, and interior elements contribute to their widespread adoption.

- Industrial and Domestic Appliances: This sector represents a significant and growing market for coil coatings. The demand for durable, scratch-resistant, and aesthetically appealing surfaces for white goods, kitchen appliances, and other household items directly translates into increased consumption of coil-coated metals. Manufacturers are leveraging coil coatings to achieve premium finishes, differentiate their products, and enhance the perceived value.

- Automotive: While subject to market fluctuations, the automotive sector remains a vital segment. Coil coatings are essential for vehicle bodies, providing corrosion protection and a base for paint finishes. The increasing use of pre-coated steel and aluminum in vehicle manufacturing for weight reduction and structural integrity continues to support demand.

- HVAC: The growing focus on energy efficiency and indoor air quality is driving demand for robust and durable HVAC components. Coil coatings offer the necessary protection against corrosion and provide a clean, aesthetically pleasing finish for air handling units, ductwork, and other system parts.

The market's leadership within these segments is driven by factors such as economic growth, favorable regulatory environments promoting sustainable construction, technological advancements in coating formulations, and the inherent performance benefits of coil-coated materials.

Europe Coil Coatings Industry Product Developments

Product innovations in the Europe Coil Coatings Industry are increasingly focused on enhancing sustainability, performance, and application efficiency. Developments include the introduction of low-VOC and VOC-free formulations to meet stringent environmental regulations, as well as coatings with improved scratch resistance, UV durability, and self-cleaning properties. Advanced resin technologies are enabling thinner yet more robust coatings, reducing material consumption. Furthermore, research into bio-based and recycled content in coatings is gaining traction, aligning with the circular economy principles. These innovations cater to the evolving demands of the Building and Construction, Automotive, and Appliances sectors, providing competitive advantages through enhanced aesthetics, extended product lifespans, and reduced environmental impact.

Challenges in the Europe Coil Coatings Industry Market

The Europe Coil Coatings Industry faces several significant challenges. Stringent environmental regulations regarding VOC emissions and the use of certain chemicals can increase compliance costs and necessitate reformulation efforts. Fluctuations in raw material prices, particularly for key resins and pigments, can impact profitability and pricing strategies. The growing competition from alternative coating technologies like powder coatings and advanced liquid paints, offering comparable performance in certain applications, also poses a threat. Supply chain disruptions, geopolitical uncertainties, and increasing energy costs can further exacerbate operational challenges and affect market stability. These factors collectively demand continuous innovation and strategic agility from market participants.

Forces Driving Europe Coil Coatings Industry Growth

The Europe Coil Coatings Industry is propelled by robust growth drivers that underscore its strategic importance. Significant investments in infrastructure development and the escalating demand for sustainable building materials in the Building and Construction sector are paramount. Furthermore, the trend towards aesthetically pleasing and durable finishes in Industrial and Domestic Appliances and Automotive applications continues to fuel market expansion. Technological advancements leading to the development of eco-friendly, high-performance coatings with enhanced durability and novel functionalities are also critical accelerators. Favorable regulatory landscapes that promote energy efficiency and sustainable manufacturing practices further incentivize the adoption of advanced coil coating solutions across various industries.

Challenges in the Europe Coil Coatings Industry Market

Long-term growth catalysts for the Europe Coil Coatings Industry lie in continuous innovation and strategic market adaptation. The development of next-generation coatings with superior performance characteristics, such as advanced corrosion resistance, self-healing capabilities, and antimicrobial properties, will be crucial. Partnerships and collaborations between coil coaters, paint suppliers, and equipment manufacturers are essential to drive research and development and bring innovative solutions to market. Expanding into emerging applications and niche markets, along with focusing on circular economy principles through the development of recyclable and bio-based coatings, will ensure sustained relevance and growth.

Emerging Opportunities in Europe Coil Coatings Industry

Emerging opportunities within the Europe Coil Coatings Industry are abundant, driven by evolving market demands and technological advancements. The increasing focus on sustainability presents a significant opportunity for the development and market penetration of eco-friendly coil coatings, including those with low-VOC content, bio-based resins, and those that enhance the recyclability of coated materials. The growth of the renewable energy sector, particularly solar panel manufacturing, is creating new avenues for specialized coil coatings. Furthermore, advancements in digital printing technologies on pre-coated metals open doors for customized aesthetics and innovative product designs across various end-user industries. The drive for enhanced durability and reduced maintenance in construction and automotive applications also presents opportunities for high-performance coating systems.

Leading Players in the Europe Coil Coatings Industry Sector

- ArcelorMittal

- Arconic

- Alcoa Corporation

- Norsk Hydro ASA

- Novelis

- Rautaruukki Corporation

- Salzgitter Flachstahl GmbH

- Tata Steel

- Thyssenkrupp

- AkzoNobel N V

- Axalta Coatings Systems

- Beckers Group

- Kansai Paint Co Ltd

- PPG Industries Inc

- The Sherwin-Williams Company

- NIPPONPAINT Co Ltd

- Brillux GmbH & Co KG

- Hempel A/S

- Wacker Chemie AG

- Arkema Group

- Bayer AG

- BASF SE

- Evonik Industries AG

- Henkel AG & Co KGaA

- Solvay

Key Milestones in Europe Coil Coatings Industry Industry

- 2019: Launch of advanced low-VOC polyester coatings by leading paint suppliers, responding to stricter EU environmental directives.

- 2020: Significant investments by coil coaters in R&D for sustainable coating formulations, including bio-based resins, driven by growing consumer and regulatory pressure.

- 2021: Mergers and acquisitions activity increased as larger players sought to consolidate market share and expand their product portfolios in specialty coatings.

- 2022: Introduction of enhanced UV-resistant PVDF coatings with extended warranty periods, targeting the premium building and construction segment.

- 2023: Increased adoption of digital printing technologies on coil-coated metal for personalized designs in furniture and appliance sectors.

- 2024: Growing emphasis on circular economy principles, with initiatives to improve the recyclability of coil-coated materials.

Strategic Outlook for Europe Coil Coatings Industry Market

The strategic outlook for the Europe Coil Coatings Industry remains exceptionally strong, driven by an intrinsic link to key growth sectors like sustainable construction and advanced manufacturing. Future growth accelerators will stem from continued innovation in eco-friendly and high-performance coating technologies, such as self-healing and smart coatings. Strategic partnerships between raw material suppliers, coating manufacturers, and end-users will be pivotal in developing tailor-made solutions that address specific industry challenges and capitalize on emerging trends. The industry's ability to adapt to evolving regulatory landscapes and integrate circular economy principles will further solidify its competitive position and unlock new market potential across Europe.

Europe Coil Coatings Industry Segmentation

-

1. Resin Type

- 1.1. Polyester

- 1.2. Polyvinylidene Fluorides (PVDF)

- 1.3. Polyurethane(PU)

- 1.4. Plastisols

- 1.5. Other Resin Types

-

2. End-user Industry

- 2.1. Building and Construction

- 2.2. Industrial and Domestic Appliances

- 2.3. Automotive

- 2.4. Furniture

- 2.5. HVAC

- 2.6. Other End-user Industries

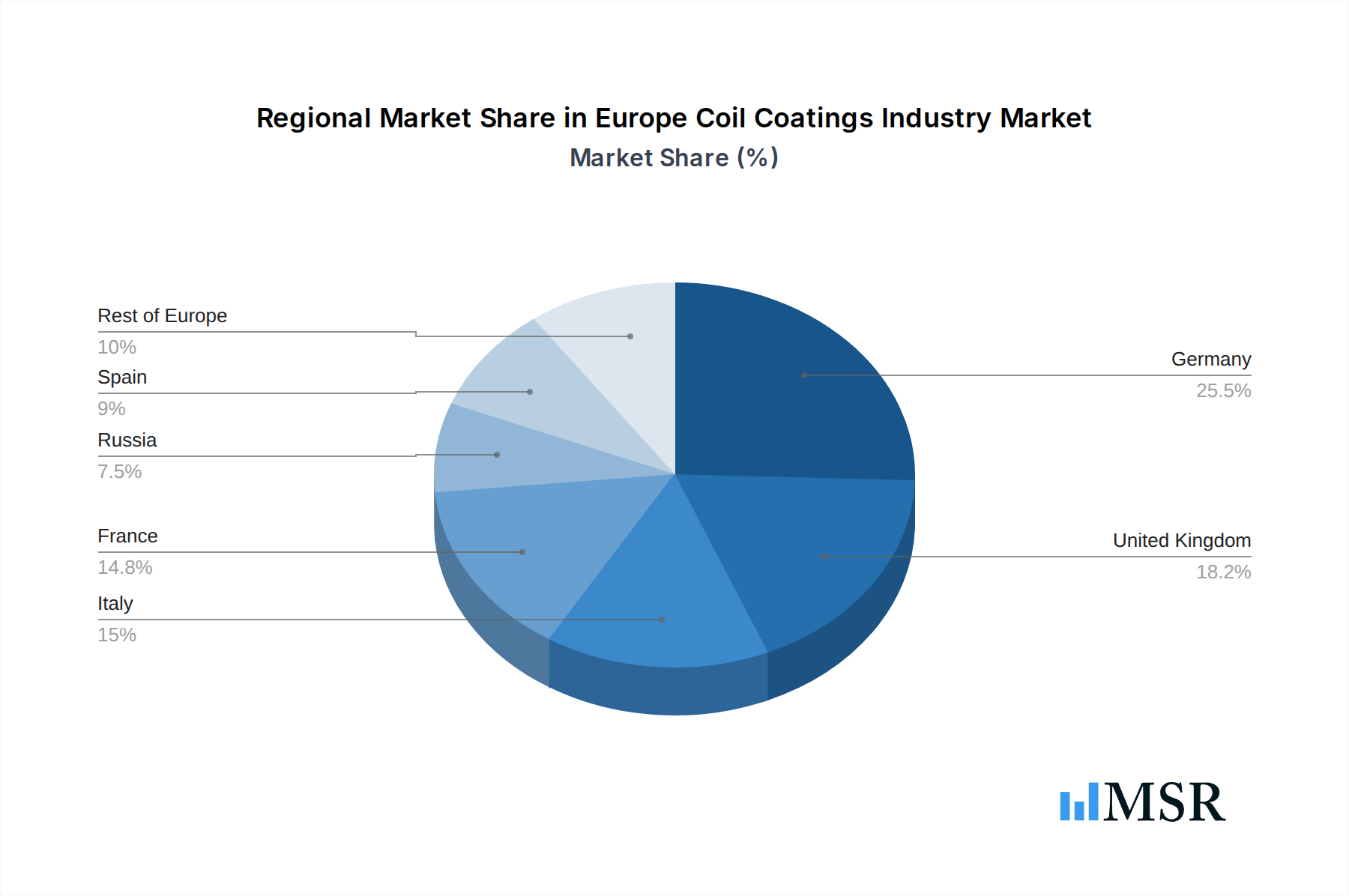

Europe Coil Coatings Industry Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. Italy

- 4. France

- 5. Russia

- 6. Spain

- 7. Rest of Europe

Europe Coil Coatings Industry Regional Market Share

Geographic Coverage of Europe Coil Coatings Industry

Europe Coil Coatings Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.06% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Resin Type

- 5.1.1. Polyester

- 5.1.2. Polyvinylidene Fluorides (PVDF)

- 5.1.3. Polyurethane(PU)

- 5.1.4. Plastisols

- 5.1.5. Other Resin Types

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Building and Construction

- 5.2.2. Industrial and Domestic Appliances

- 5.2.3. Automotive

- 5.2.4. Furniture

- 5.2.5. HVAC

- 5.2.6. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Germany

- 5.3.2. United Kingdom

- 5.3.3. Italy

- 5.3.4. France

- 5.3.5. Russia

- 5.3.6. Spain

- 5.3.7. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Resin Type

- 6. Global Europe Coil Coatings Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Resin Type

- 6.1.1. Polyester

- 6.1.2. Polyvinylidene Fluorides (PVDF)

- 6.1.3. Polyurethane(PU)

- 6.1.4. Plastisols

- 6.1.5. Other Resin Types

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Building and Construction

- 6.2.2. Industrial and Domestic Appliances

- 6.2.3. Automotive

- 6.2.4. Furniture

- 6.2.5. HVAC

- 6.2.6. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Resin Type

- 7. Germany Europe Coil Coatings Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Resin Type

- 7.1.1. Polyester

- 7.1.2. Polyvinylidene Fluorides (PVDF)

- 7.1.3. Polyurethane(PU)

- 7.1.4. Plastisols

- 7.1.5. Other Resin Types

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Building and Construction

- 7.2.2. Industrial and Domestic Appliances

- 7.2.3. Automotive

- 7.2.4. Furniture

- 7.2.5. HVAC

- 7.2.6. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Resin Type

- 8. United Kingdom Europe Coil Coatings Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Resin Type

- 8.1.1. Polyester

- 8.1.2. Polyvinylidene Fluorides (PVDF)

- 8.1.3. Polyurethane(PU)

- 8.1.4. Plastisols

- 8.1.5. Other Resin Types

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Building and Construction

- 8.2.2. Industrial and Domestic Appliances

- 8.2.3. Automotive

- 8.2.4. Furniture

- 8.2.5. HVAC

- 8.2.6. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Resin Type

- 9. Italy Europe Coil Coatings Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Resin Type

- 9.1.1. Polyester

- 9.1.2. Polyvinylidene Fluorides (PVDF)

- 9.1.3. Polyurethane(PU)

- 9.1.4. Plastisols

- 9.1.5. Other Resin Types

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Building and Construction

- 9.2.2. Industrial and Domestic Appliances

- 9.2.3. Automotive

- 9.2.4. Furniture

- 9.2.5. HVAC

- 9.2.6. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Resin Type

- 10. France Europe Coil Coatings Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Resin Type

- 10.1.1. Polyester

- 10.1.2. Polyvinylidene Fluorides (PVDF)

- 10.1.3. Polyurethane(PU)

- 10.1.4. Plastisols

- 10.1.5. Other Resin Types

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Building and Construction

- 10.2.2. Industrial and Domestic Appliances

- 10.2.3. Automotive

- 10.2.4. Furniture

- 10.2.5. HVAC

- 10.2.6. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Resin Type

- 11. Russia Europe Coil Coatings Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Resin Type

- 11.1.1. Polyester

- 11.1.2. Polyvinylidene Fluorides (PVDF)

- 11.1.3. Polyurethane(PU)

- 11.1.4. Plastisols

- 11.1.5. Other Resin Types

- 11.2. Market Analysis, Insights and Forecast - by End-user Industry

- 11.2.1. Building and Construction

- 11.2.2. Industrial and Domestic Appliances

- 11.2.3. Automotive

- 11.2.4. Furniture

- 11.2.5. HVAC

- 11.2.6. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Resin Type

- 12. Spain Europe Coil Coatings Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Resin Type

- 12.1.1. Polyester

- 12.1.2. Polyvinylidene Fluorides (PVDF)

- 12.1.3. Polyurethane(PU)

- 12.1.4. Plastisols

- 12.1.5. Other Resin Types

- 12.2. Market Analysis, Insights and Forecast - by End-user Industry

- 12.2.1. Building and Construction

- 12.2.2. Industrial and Domestic Appliances

- 12.2.3. Automotive

- 12.2.4. Furniture

- 12.2.5. HVAC

- 12.2.6. Other End-user Industries

- 12.1. Market Analysis, Insights and Forecast - by Resin Type

- 13. Rest of Europe Europe Coil Coatings Industry Analysis, Insights and Forecast, 2020-2032

- 13.1. Market Analysis, Insights and Forecast - by Resin Type

- 13.1.1. Polyester

- 13.1.2. Polyvinylidene Fluorides (PVDF)

- 13.1.3. Polyurethane(PU)

- 13.1.4. Plastisols

- 13.1.5. Other Resin Types

- 13.2. Market Analysis, Insights and Forecast - by End-user Industry

- 13.2.1. Building and Construction

- 13.2.2. Industrial and Domestic Appliances

- 13.2.3. Automotive

- 13.2.4. Furniture

- 13.2.5. HVAC

- 13.2.6. Other End-user Industries

- 13.1. Market Analysis, Insights and Forecast - by Resin Type

- 14. Competitive Analysis

- 14.1. Company Profiles

- 14.1.1 Coil Coaters

- 14.1.1.1. Company Overview

- 14.1.1.2. Products

- 14.1.1.3. Company Financials

- 14.1.1.4. SWOT Analysis

- 14.1.2 1 ArcelorMittal

- 14.1.2.1. Company Overview

- 14.1.2.2. Products

- 14.1.2.3. Company Financials

- 14.1.2.4. SWOT Analysis

- 14.1.3 2 Arconic

- 14.1.3.1. Company Overview

- 14.1.3.2. Products

- 14.1.3.3. Company Financials

- 14.1.3.4. SWOT Analysis

- 14.1.4 3 Alcoa Corporation

- 14.1.4.1. Company Overview

- 14.1.4.2. Products

- 14.1.4.3. Company Financials

- 14.1.4.4. SWOT Analysis

- 14.1.5 4 Norsk Hydro ASA

- 14.1.5.1. Company Overview

- 14.1.5.2. Products

- 14.1.5.3. Company Financials

- 14.1.5.4. SWOT Analysis

- 14.1.6 5 Novelis

- 14.1.6.1. Company Overview

- 14.1.6.2. Products

- 14.1.6.3. Company Financials

- 14.1.6.4. SWOT Analysis

- 14.1.7 6 Rautaruukki Corporation

- 14.1.7.1. Company Overview

- 14.1.7.2. Products

- 14.1.7.3. Company Financials

- 14.1.7.4. SWOT Analysis

- 14.1.8 7 Salzgitter Flachstahl GmbH

- 14.1.8.1. Company Overview

- 14.1.8.2. Products

- 14.1.8.3. Company Financials

- 14.1.8.4. SWOT Analysis

- 14.1.9 8 Tata Steel

- 14.1.9.1. Company Overview

- 14.1.9.2. Products

- 14.1.9.3. Company Financials

- 14.1.9.4. SWOT Analysis

- 14.1.10 9 Thyssenkrupp

- 14.1.10.1. Company Overview

- 14.1.10.2. Products

- 14.1.10.3. Company Financials

- 14.1.10.4. SWOT Analysis

- 14.1.11 Paint Suppliers

- 14.1.11.1. Company Overview

- 14.1.11.2. Products

- 14.1.11.3. Company Financials

- 14.1.11.4. SWOT Analysis

- 14.1.12 1 AkzoNobel N V

- 14.1.12.1. Company Overview

- 14.1.12.2. Products

- 14.1.12.3. Company Financials

- 14.1.12.4. SWOT Analysis

- 14.1.13 2 Axalta Coatings Systems

- 14.1.13.1. Company Overview

- 14.1.13.2. Products

- 14.1.13.3. Company Financials

- 14.1.13.4. SWOT Analysis

- 14.1.14 3 Beckers Group

- 14.1.14.1. Company Overview

- 14.1.14.2. Products

- 14.1.14.3. Company Financials

- 14.1.14.4. SWOT Analysis

- 14.1.15 4 Kansai Paint Co Ltd

- 14.1.15.1. Company Overview

- 14.1.15.2. Products

- 14.1.15.3. Company Financials

- 14.1.15.4. SWOT Analysis

- 14.1.16 5 PPG Industries Inc

- 14.1.16.1. Company Overview

- 14.1.16.2. Products

- 14.1.16.3. Company Financials

- 14.1.16.4. SWOT Analysis

- 14.1.17 6 The Sherwin-Williams Company

- 14.1.17.1. Company Overview

- 14.1.17.2. Products

- 14.1.17.3. Company Financials

- 14.1.17.4. SWOT Analysis

- 14.1.18 7 NIPPONPAINT Co Ltd

- 14.1.18.1. Company Overview

- 14.1.18.2. Products

- 14.1.18.3. Company Financials

- 14.1.18.4. SWOT Analysis

- 14.1.19 8 Brillux GmbH & Co KG

- 14.1.19.1. Company Overview

- 14.1.19.2. Products

- 14.1.19.3. Company Financials

- 14.1.19.4. SWOT Analysis

- 14.1.20 9 Hempel A/S

- 14.1.20.1. Company Overview

- 14.1.20.2. Products

- 14.1.20.3. Company Financials

- 14.1.20.4. SWOT Analysis

- 14.1.21 Pretreatment Resins Pigments and Equipment

- 14.1.21.1. Company Overview

- 14.1.21.2. Products

- 14.1.21.3. Company Financials

- 14.1.21.4. SWOT Analysis

- 14.1.22 1 Wacker Chemie AG

- 14.1.22.1. Company Overview

- 14.1.22.2. Products

- 14.1.22.3. Company Financials

- 14.1.22.4. SWOT Analysis

- 14.1.23 2 Arkema Group

- 14.1.23.1. Company Overview

- 14.1.23.2. Products

- 14.1.23.3. Company Financials

- 14.1.23.4. SWOT Analysis

- 14.1.24 3 Bayer AG

- 14.1.24.1. Company Overview

- 14.1.24.2. Products

- 14.1.24.3. Company Financials

- 14.1.24.4. SWOT Analysis

- 14.1.25 4 BASF SE

- 14.1.25.1. Company Overview

- 14.1.25.2. Products

- 14.1.25.3. Company Financials

- 14.1.25.4. SWOT Analysis

- 14.1.26 5 Evonik Industries AG

- 14.1.26.1. Company Overview

- 14.1.26.2. Products

- 14.1.26.3. Company Financials

- 14.1.26.4. SWOT Analysis

- 14.1.27 6 Henkel AG & Co KGaA

- 14.1.27.1. Company Overview

- 14.1.27.2. Products

- 14.1.27.3. Company Financials

- 14.1.27.4. SWOT Analysis

- 14.1.28 7 Solvay*List Not Exhaustive

- 14.1.28.1. Company Overview

- 14.1.28.2. Products

- 14.1.28.3. Company Financials

- 14.1.28.4. SWOT Analysis

- 14.1.1 Coil Coaters

- 14.2. Market Entropy

- 14.2.1 Company's Key Areas Served

- 14.2.2 Recent Developments

- 14.3. Company Market Share Analysis 2025

- 14.3.1 Top 5 Companies Market Share Analysis

- 14.3.2 Top 3 Companies Market Share Analysis

- 14.4. List of Potential Customers

- 15. Research Methodology

List of Figures

- Figure 1: Global Europe Coil Coatings Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Germany Europe Coil Coatings Industry Revenue (billion), by Resin Type 2025 & 2033

- Figure 3: Germany Europe Coil Coatings Industry Revenue Share (%), by Resin Type 2025 & 2033

- Figure 4: Germany Europe Coil Coatings Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 5: Germany Europe Coil Coatings Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 6: Germany Europe Coil Coatings Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: Germany Europe Coil Coatings Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: United Kingdom Europe Coil Coatings Industry Revenue (billion), by Resin Type 2025 & 2033

- Figure 9: United Kingdom Europe Coil Coatings Industry Revenue Share (%), by Resin Type 2025 & 2033

- Figure 10: United Kingdom Europe Coil Coatings Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 11: United Kingdom Europe Coil Coatings Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 12: United Kingdom Europe Coil Coatings Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: United Kingdom Europe Coil Coatings Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Italy Europe Coil Coatings Industry Revenue (billion), by Resin Type 2025 & 2033

- Figure 15: Italy Europe Coil Coatings Industry Revenue Share (%), by Resin Type 2025 & 2033

- Figure 16: Italy Europe Coil Coatings Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 17: Italy Europe Coil Coatings Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 18: Italy Europe Coil Coatings Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Italy Europe Coil Coatings Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: France Europe Coil Coatings Industry Revenue (billion), by Resin Type 2025 & 2033

- Figure 21: France Europe Coil Coatings Industry Revenue Share (%), by Resin Type 2025 & 2033

- Figure 22: France Europe Coil Coatings Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 23: France Europe Coil Coatings Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: France Europe Coil Coatings Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: France Europe Coil Coatings Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Russia Europe Coil Coatings Industry Revenue (billion), by Resin Type 2025 & 2033

- Figure 27: Russia Europe Coil Coatings Industry Revenue Share (%), by Resin Type 2025 & 2033

- Figure 28: Russia Europe Coil Coatings Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 29: Russia Europe Coil Coatings Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: Russia Europe Coil Coatings Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Russia Europe Coil Coatings Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Spain Europe Coil Coatings Industry Revenue (billion), by Resin Type 2025 & 2033

- Figure 33: Spain Europe Coil Coatings Industry Revenue Share (%), by Resin Type 2025 & 2033

- Figure 34: Spain Europe Coil Coatings Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 35: Spain Europe Coil Coatings Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 36: Spain Europe Coil Coatings Industry Revenue (billion), by Country 2025 & 2033

- Figure 37: Spain Europe Coil Coatings Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Rest of Europe Europe Coil Coatings Industry Revenue (billion), by Resin Type 2025 & 2033

- Figure 39: Rest of Europe Europe Coil Coatings Industry Revenue Share (%), by Resin Type 2025 & 2033

- Figure 40: Rest of Europe Europe Coil Coatings Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 41: Rest of Europe Europe Coil Coatings Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 42: Rest of Europe Europe Coil Coatings Industry Revenue (billion), by Country 2025 & 2033

- Figure 43: Rest of Europe Europe Coil Coatings Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Europe Coil Coatings Industry Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 2: Global Europe Coil Coatings Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 3: Global Europe Coil Coatings Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Europe Coil Coatings Industry Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 5: Global Europe Coil Coatings Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 6: Global Europe Coil Coatings Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Europe Coil Coatings Industry Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 8: Global Europe Coil Coatings Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 9: Global Europe Coil Coatings Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Global Europe Coil Coatings Industry Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 11: Global Europe Coil Coatings Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 12: Global Europe Coil Coatings Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Europe Coil Coatings Industry Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 14: Global Europe Coil Coatings Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 15: Global Europe Coil Coatings Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global Europe Coil Coatings Industry Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 17: Global Europe Coil Coatings Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 18: Global Europe Coil Coatings Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: Global Europe Coil Coatings Industry Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 20: Global Europe Coil Coatings Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 21: Global Europe Coil Coatings Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 22: Global Europe Coil Coatings Industry Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 23: Global Europe Coil Coatings Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 24: Global Europe Coil Coatings Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Coil Coatings Industry?

The projected CAGR is approximately 12.06%.

2. Which companies are prominent players in the Europe Coil Coatings Industry?

Key companies in the market include Coil Coaters, 1 ArcelorMittal, 2 Arconic, 3 Alcoa Corporation, 4 Norsk Hydro ASA, 5 Novelis, 6 Rautaruukki Corporation, 7 Salzgitter Flachstahl GmbH, 8 Tata Steel, 9 Thyssenkrupp, Paint Suppliers, 1 AkzoNobel N V, 2 Axalta Coatings Systems, 3 Beckers Group, 4 Kansai Paint Co Ltd, 5 PPG Industries Inc, 6 The Sherwin-Williams Company, 7 NIPPONPAINT Co Ltd, 8 Brillux GmbH & Co KG, 9 Hempel A/S, Pretreatment Resins Pigments and Equipment, 1 Wacker Chemie AG, 2 Arkema Group, 3 Bayer AG, 4 BASF SE, 5 Evonik Industries AG, 6 Henkel AG & Co KGaA, 7 Solvay*List Not Exhaustive.

3. What are the main segments of the Europe Coil Coatings Industry?

The market segments include Resin Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 10.55 billion as of 2022.

5. What are some drivers contributing to market growth?

; Increasing Demand from the Building and Construction Industry; Stringent Environmental Regulations for Conventional Products.

6. What are the notable trends driving market growth?

Rising Demand from the Building and Construction Industry.

7. Are there any restraints impacting market growth?

; Increasing Demand from the Building and Construction Industry; Stringent Environmental Regulations for Conventional Products.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Coil Coatings Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Coil Coatings Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Coil Coatings Industry?

To stay informed about further developments, trends, and reports in the Europe Coil Coatings Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence