Key Insights

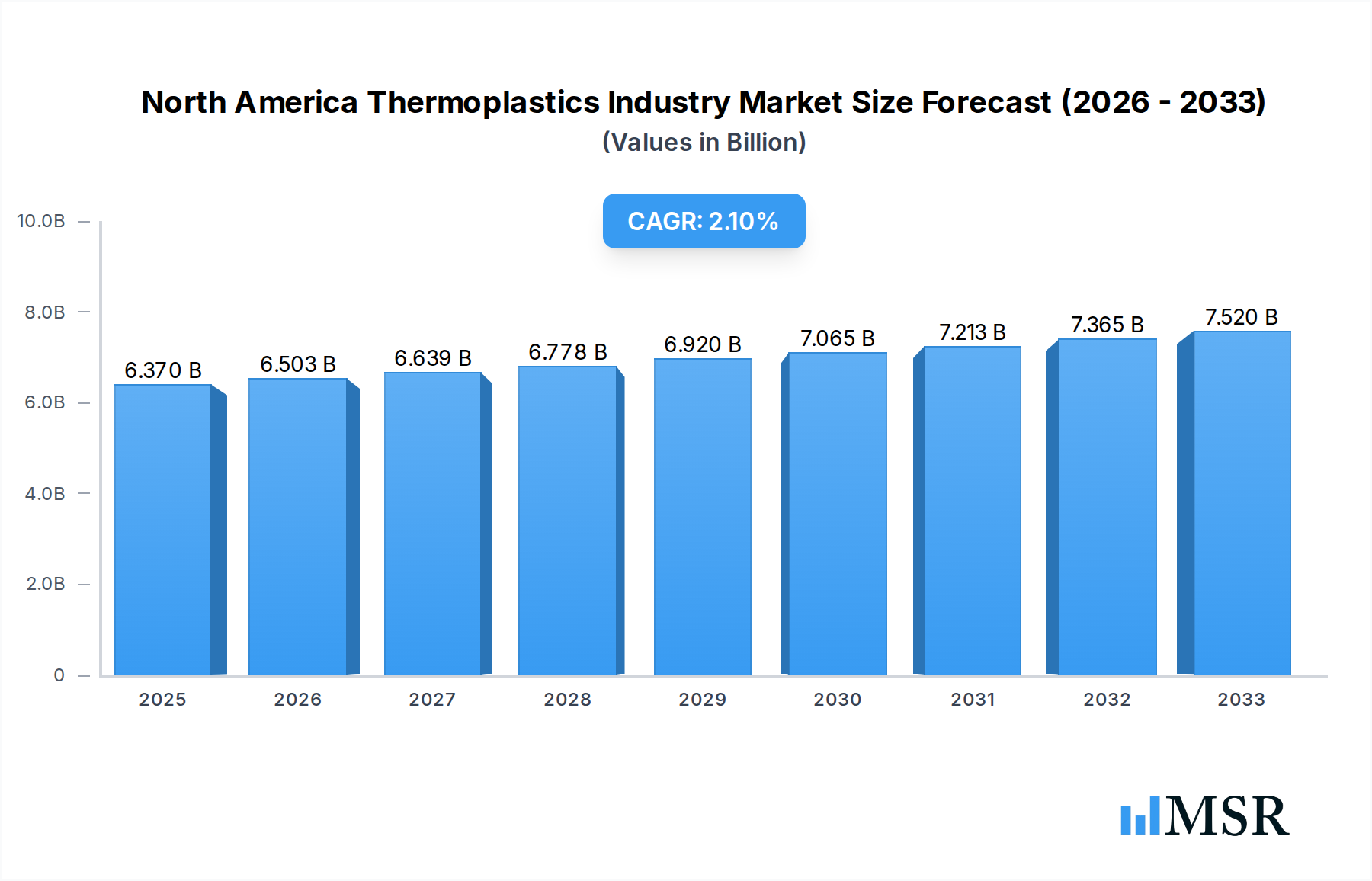

The North American thermoplastics market is poised for steady growth, reaching an estimated $6.37 billion in 2025, with a projected Compound Annual Growth Rate (CAGR) of 2.1% over the forecast period of 2025-2033. This expansion is primarily driven by increasing demand from key end-user industries such as packaging, automotive and transportation, and electrical and electronics. The packaging sector, in particular, continues to be a significant consumer of thermoplastics, fueled by rising e-commerce activities and the need for durable, lightweight, and cost-effective packaging solutions. The automotive industry's ongoing shift towards lightweight materials to improve fuel efficiency and reduce emissions further bolsters demand for engineering and high-performance thermoplastics. Furthermore, the burgeoning electrical and electronics sector, with its constant innovation and demand for advanced materials with superior insulating and mechanical properties, will act as a substantial growth catalyst. Technological advancements in thermoplastic processing, leading to enhanced material performance and sustainability, also contribute positively to market dynamics.

North America Thermoplastics Industry Market Size (In Billion)

However, the market faces certain restraints, including volatile raw material prices, which can impact profitability and product pricing strategies. Stringent environmental regulations concerning plastic waste and disposal also present challenges, pushing manufacturers to invest in sustainable alternatives and recycling technologies. Despite these hurdles, the market is witnessing significant trends such as the growing adoption of bio-based and recycled thermoplastics, driven by environmental consciousness and regulatory pressures. Innovations in high-performance thermoplastics, offering exceptional thermal stability, chemical resistance, and mechanical strength, are opening up new application areas in demanding sectors like aerospace and medical devices. The geographical landscape of the North American market is dominated by the United States, followed by Canada and Mexico, each contributing to the overall market size with distinct regional demands and manufacturing capabilities. Key players are actively investing in research and development to innovate and meet the evolving needs of diverse end-user industries.

North America Thermoplastics Industry Company Market Share

Unveiling the Future: North America Thermoplastics Industry Market Report (2019-2033)

Gain unparalleled insights into the dynamic North America thermoplastics market with this comprehensive industry report. Covering a critical study period from 2019 to 2033, with a base year of 2025 and a detailed forecast for 2025-2033, this analysis delivers actionable intelligence for stakeholders navigating this multi-billion dollar sector. Discover key market concentration, innovation drivers, regulatory landscapes, and emerging opportunities across diverse product types, end-user industries, and geographical regions including the United States, Canada, and Mexico.

North America Thermoplastics Industry Market Concentration & Dynamics

The North America thermoplastics market exhibits a moderate to high concentration, with a significant portion of market share held by a few dominant players, alongside a growing number of agile mid-sized and specialized firms. Innovation ecosystems are flourishing, driven by substantial R&D investments in material science and sustainable solutions. Regulatory frameworks, particularly concerning environmental impact and recycling, are evolving, influencing product development and manufacturing processes. Substitute products, primarily from advanced composites and traditional materials, present ongoing competitive pressure. End-user trends are rapidly shifting towards lightweight, durable, and recyclable materials, fueled by sustainability mandates and consumer demand. Merger and acquisition (M&A) activities are prevalent as companies seek to expand their product portfolios, geographical reach, and technological capabilities. The market is characterized by strategic consolidations to achieve economies of scale and enhance competitive positioning.

- Market Share Snapshot: Key players command a substantial collective market share, with the top 10 entities accounting for over 60% of the total market value.

- M&A Activity: The historical period saw over 50 significant M&A transactions, with an estimated market value exceeding $15 billion, aimed at market consolidation and technology acquisition.

- Regulatory Impact: Stringent environmental regulations, particularly in the United States and Canada, are driving innovation in bio-based and recycled thermoplastics.

North America Thermoplastics Industry Industry Insights & Trends

The North America thermoplastics industry is poised for robust growth, projected to reach an estimated market size of over $XXX billion by 2025, with a compound annual growth rate (CAGR) of XX% during the forecast period of 2025–2033. This expansion is propelled by a confluence of factors including escalating demand from the automotive and transportation sector for lightweight materials to improve fuel efficiency, a burgeoning packaging industry driven by e-commerce and convenience, and the expanding electrical and electronics market. Technological disruptions, such as advancements in polymer synthesis, additive manufacturing (3D printing), and recycling technologies, are reshaping product capabilities and market penetration. Evolving consumer behaviors, with a heightened emphasis on sustainability, recyclability, and product lifespan, are also significant drivers. The industry is witnessing a surge in demand for high-performance engineering thermoplastics and specialty polymers that offer superior mechanical, thermal, and chemical resistance properties, catering to increasingly sophisticated applications. Furthermore, the growing adoption of circular economy principles is spurring innovation in advanced recycling techniques and the development of bio-based and biodegradable thermoplastics. The push for electrification in vehicles and the demand for advanced materials in renewable energy infrastructure also contribute to the upward trajectory of the market.

- Market Size: Estimated market value of over $XXX billion by 2025, projected to exceed $XXX billion by 2033.

- CAGR: An anticipated CAGR of XX% during the forecast period of 2025–2033.

- Key Growth Catalysts: Demand from automotive lightweighting, sustainable packaging solutions, and advanced electronics.

- Technological Advancements: Innovations in 3D printing, bio-polymers, and enhanced recycling processes.

Key Markets & Segments Leading North America Thermoplastics Industry

The United States stands as the dominant geographical market within North America for thermoplastics, driven by its vast industrial base, significant manufacturing output, and high consumer spending. Canada and Mexico also represent substantial and growing markets, each contributing to the overall regional demand.

Product Type Dominance:

- Commodity Thermoplastics: Polyethylene (PE) and Polypropylene (PP) continue to lead the market due to their widespread application in Packaging (films, bottles, containers) and Building and Construction (pipes, insulation). The economic growth in these sectors directly translates to sustained demand for these versatile and cost-effective materials.

- Engineering Thermoplastics: Polyamide (PA) and Polycarbonate (PC) are witnessing robust growth, particularly in the Automotive and Transportation sector, where they are utilized for their strength, durability, and lightweight properties in components like engine parts, interior trim, and exterior panels. The Electrical and Electronics industry also relies heavily on these for insulation and housing.

- High-performance Engineering Thermoplastics: While a smaller segment, Polyether Ether Ketone (PEEK) and Polytetrafluoroethylene (PTFE) are critical for specialized applications in Medical devices, aerospace, and harsh industrial environments, demanding exceptional thermal and chemical resistance. Their growth is driven by niche but high-value applications.

End-user Industry Dominance:

- Packaging: This segment remains the largest consumer of thermoplastics, propelled by the growth of the food and beverage, pharmaceutical, and e-commerce industries. The demand for flexible and rigid packaging solutions, often incorporating PE and PP, is immense.

- Automotive and Transportation: With the industry's focus on lightweighting for fuel efficiency and the transition to electric vehicles, the demand for high-strength, low-weight engineering thermoplastics like PA and PC is soaring.

- Building and Construction: The ongoing need for durable, cost-effective, and weather-resistant materials for infrastructure projects, residential and commercial construction, solidifies the demand for PVC and PE.

- Electrical and Electronics: The relentless innovation in consumer electronics, telecommunications, and the growing adoption of smart technologies are driving demand for thermoplastics with excellent dielectric properties and flame retardancy.

North America Thermoplastics Industry Product Developments

Product innovations in the North America thermoplastics industry are increasingly focused on sustainability, enhanced performance, and novel applications. This includes the development of advanced bio-based and recycled thermoplastics that offer comparable or superior properties to their virgin counterparts, addressing the growing demand for eco-friendly solutions. Research is also concentrated on creating specialized polymers with improved thermal stability, chemical resistance, and mechanical strength for demanding applications in automotive, aerospace, and medical sectors. Furthermore, advancements in polymer compounding and blending are leading to materials with customized properties for additive manufacturing (3D printing), opening new avenues for product design and rapid prototyping.

Challenges in the North America Thermoplastics Industry Market

The North America thermoplastics industry faces several significant challenges. Stringent environmental regulations and growing public pressure for sustainability are creating hurdles related to waste management and the lifecycle impact of plastics. Fluctuations in raw material prices, particularly those derived from petrochemicals, can impact profitability and market stability. Intense competition from both domestic and international players, coupled with the emergence of alternative materials, necessitates continuous innovation and cost optimization. Supply chain disruptions, as witnessed in recent years, can lead to production delays and increased operational costs.

- Regulatory Compliance: Adapting to evolving environmental standards and waste reduction mandates.

- Raw Material Volatility: Managing price fluctuations of petrochemical feedstocks.

- Competitive Landscape: Navigating competition from alternative materials and international suppliers.

- Supply Chain Resilience: Mitigating risks associated with global supply chain disruptions.

Forces Driving North America Thermoplastics Industry Growth

Several key forces are propelling the growth of the North America thermoplastics industry. Technological advancements in material science, leading to the development of lighter, stronger, and more sustainable thermoplastics, are expanding their applicability across various sectors. The increasing focus on lightweighting in the automotive and aerospace industries to improve fuel efficiency and reduce emissions is a major growth driver. The burgeoning e-commerce sector is fueling demand for innovative and resilient packaging solutions. Furthermore, the transition towards renewable energy sources, such as wind and solar, is creating new markets for specialized thermoplastics with high performance and durability requirements. Supportive government initiatives promoting domestic manufacturing and the adoption of circular economy principles also contribute significantly to market expansion.

- Lightweighting Initiatives: Demand from automotive and aerospace for fuel efficiency.

- E-commerce Boom: Growth in demand for advanced packaging materials.

- Renewable Energy Sector: Expansion of applications in solar and wind power infrastructure.

- Sustainable Material Demand: Growing consumer and industry preference for eco-friendly options.

Challenges in the North America Thermoplastics Industry Market

Long-term growth catalysts for the North America thermoplastics industry are rooted in continued innovation and strategic market expansion. The development of novel bio-based and biodegradable thermoplastics will be crucial in addressing environmental concerns and tapping into growing consumer demand for sustainable products. Advancements in recycling technologies, including chemical recycling, offer the potential to create a truly circular economy for plastics, reducing reliance on virgin feedstocks. Strategic partnerships and collaborations between material manufacturers, end-users, and research institutions can accelerate the development and adoption of advanced thermoplastic solutions. Furthermore, exploring emerging applications in sectors like advanced healthcare, smart infrastructure, and space exploration will unlock new revenue streams and foster sustained growth.

- Circular Economy Adoption: Advancements in recycling and upcycling technologies.

- Bio-based Material Development: Innovation in sustainable and biodegradable alternatives.

- Inter-industry Collaboration: Partnerships to drive adoption in niche and emerging sectors.

- Emerging Market Penetration: Exploring applications in healthcare, aerospace, and smart infrastructure.

Emerging Opportunities in North America Thermoplastics Industry

Emerging opportunities in the North America thermoplastics industry are driven by a confluence of technological advancements and evolving societal needs. The increasing adoption of 3D printing (additive manufacturing) is creating a demand for specialized thermoplastic filaments with tailored properties for rapid prototyping and on-demand production across diverse industries. The push for electrification in the automotive sector presents significant opportunities for lightweight, high-performance thermoplastics in battery components, charging infrastructure, and vehicle interiors. Furthermore, the growing demand for sustainable and circular solutions is opening avenues for companies investing in advanced recycling technologies and the development of bio-based and recycled thermoplastic compounds. The medical industry's continuous innovation in implantable devices, diagnostics, and drug delivery systems also presents lucrative avenues for high-purity, biocompatible engineering thermoplastics.

- 3D Printing Applications: Development of advanced thermoplastic filaments for additive manufacturing.

- Electric Vehicle Components: Growth in demand for lightweight, high-performance materials for EV batteries and structural parts.

- Sustainable & Circular Solutions: Opportunities in bio-based polymers and advanced recycling technologies.

- Medical Device Innovation: Demand for biocompatible and high-purity thermoplastics in healthcare.

Leading Players in the North America Thermoplastics Industry Sector

- 3M (incl Dyneon LLC)

- Arkema

- Asahi Kasei Corporation

- BASF SE

- Celanese Corporation

- Chevron Phillips Chemical Company

- Covestro AG

- Daicel Corporation

- DSM

- DuPont

- Eastman Chemical Company

- Evonik Industries AG

- INEOS AG

- LANXESS

- LG Chem

- LyondellBasell Industries Holdings B V (incl A Schulman Inc )

- Mitsubishi Engineering-Plastics Corporation

- Polyplastics Co Ltd

- Röchling

- SABIC

- Solvay

- TEIJIN LIMITED

Key Milestones in North America Thermoplastics Industry Industry

- 2019: Launch of new bio-based polymer grades by several key players, responding to increasing sustainability demands.

- 2020: Significant investment in advanced recycling infrastructure across the United States and Canada.

- 2021: Increased adoption of high-performance thermoplastics in electric vehicle battery casings and components.

- 2022: Major mergers and acquisitions within the engineering thermoplastics segment to consolidate market share and expand product portfolios.

- 2023: Introduction of novel thermoplastic compounds designed for enhanced performance in 3D printing applications.

- 2024: Growth in the use of recycled content in packaging applications, driven by regulatory pressures and consumer preference.

Strategic Outlook for North America Thermoplastics Industry Market

The strategic outlook for the North America thermoplastics industry is characterized by a strong emphasis on innovation, sustainability, and market diversification. Companies are investing heavily in research and development to create advanced materials that offer enhanced performance, lighter weight, and improved recyclability, aligning with global environmental goals. The growing demand for circular economy solutions will necessitate further advancements in chemical and mechanical recycling technologies, creating new business models and opportunities. Strategic partnerships and collaborations will be crucial for navigating complex supply chains and accelerating the adoption of new thermoplastic applications, particularly in high-growth sectors like electric vehicles, renewable energy, and advanced healthcare. Companies that prioritize sustainable production practices, invest in digital transformation, and demonstrate agility in responding to evolving market demands are best positioned for long-term success.

North America Thermoplastics Industry Segmentation

-

1. Product Type

-

1.1. Commodity Thermoplastics

- 1.1.1. Polyethylene (PE)

- 1.1.2. Polypropylene (PP)

- 1.1.3. Polyvinyl Chloride (PVC)

- 1.1.4. Polystyrene (PS)

-

1.2. Engineering Thermoplastics

- 1.2.1. Polyamide (PA)

- 1.2.2. Polycarbonates (PC)

- 1.2.3. Polymethyl Methacrylate (PMMA)

- 1.2.4. Polyoxymethylene (POM)

- 1.2.5. Polyethylene Terephthalate (PET)

- 1.2.6. Polybutylene Terephthalate (PBT)

- 1.2.7. Acryloni

-

1.3. High-performance Engineering Thermoplastics

- 1.3.1. Polyether Ether Ketone (PEEK)

- 1.3.2. Liquid Crystal Polymer (LCP)

- 1.3.3. Polytetrafluoroethylene (PTFE)

- 1.3.4. Polyimide (PI)

- 1.4. Other Pr

-

1.1. Commodity Thermoplastics

-

2. End-user Industry

- 2.1. Packaging

- 2.2. Building and Construction

- 2.3. Automotive and Transportation

- 2.4. Electrical and Electronics

- 2.5. Sports and Leisure

- 2.6. Furniture and Bedding

- 2.7. Agriculture

- 2.8. Medical

- 2.9. Other End-user Industries

-

3. Geography

- 3.1. United States

- 3.2. Canada

- 3.3. Mexico

North America Thermoplastics Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Mexico

North America Thermoplastics Industry Regional Market Share

Geographic Coverage of North America Thermoplastics Industry

North America Thermoplastics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.07% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Commodity Thermoplastics

- 5.1.1.1. Polyethylene (PE)

- 5.1.1.2. Polypropylene (PP)

- 5.1.1.3. Polyvinyl Chloride (PVC)

- 5.1.1.4. Polystyrene (PS)

- 5.1.2. Engineering Thermoplastics

- 5.1.2.1. Polyamide (PA)

- 5.1.2.2. Polycarbonates (PC)

- 5.1.2.3. Polymethyl Methacrylate (PMMA)

- 5.1.2.4. Polyoxymethylene (POM)

- 5.1.2.5. Polyethylene Terephthalate (PET)

- 5.1.2.6. Polybutylene Terephthalate (PBT)

- 5.1.2.7. Acryloni

- 5.1.3. High-performance Engineering Thermoplastics

- 5.1.3.1. Polyether Ether Ketone (PEEK)

- 5.1.3.2. Liquid Crystal Polymer (LCP)

- 5.1.3.3. Polytetrafluoroethylene (PTFE)

- 5.1.3.4. Polyimide (PI)

- 5.1.4. Other Pr

- 5.1.1. Commodity Thermoplastics

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Packaging

- 5.2.2. Building and Construction

- 5.2.3. Automotive and Transportation

- 5.2.4. Electrical and Electronics

- 5.2.5. Sports and Leisure

- 5.2.6. Furniture and Bedding

- 5.2.7. Agriculture

- 5.2.8. Medical

- 5.2.9. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United States

- 5.3.2. Canada

- 5.3.3. Mexico

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Mexico

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global North America Thermoplastics Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Commodity Thermoplastics

- 6.1.1.1. Polyethylene (PE)

- 6.1.1.2. Polypropylene (PP)

- 6.1.1.3. Polyvinyl Chloride (PVC)

- 6.1.1.4. Polystyrene (PS)

- 6.1.2. Engineering Thermoplastics

- 6.1.2.1. Polyamide (PA)

- 6.1.2.2. Polycarbonates (PC)

- 6.1.2.3. Polymethyl Methacrylate (PMMA)

- 6.1.2.4. Polyoxymethylene (POM)

- 6.1.2.5. Polyethylene Terephthalate (PET)

- 6.1.2.6. Polybutylene Terephthalate (PBT)

- 6.1.2.7. Acryloni

- 6.1.3. High-performance Engineering Thermoplastics

- 6.1.3.1. Polyether Ether Ketone (PEEK)

- 6.1.3.2. Liquid Crystal Polymer (LCP)

- 6.1.3.3. Polytetrafluoroethylene (PTFE)

- 6.1.3.4. Polyimide (PI)

- 6.1.4. Other Pr

- 6.1.1. Commodity Thermoplastics

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Packaging

- 6.2.2. Building and Construction

- 6.2.3. Automotive and Transportation

- 6.2.4. Electrical and Electronics

- 6.2.5. Sports and Leisure

- 6.2.6. Furniture and Bedding

- 6.2.7. Agriculture

- 6.2.8. Medical

- 6.2.9. Other End-user Industries

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United States

- 6.3.2. Canada

- 6.3.3. Mexico

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. United States North America Thermoplastics Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Commodity Thermoplastics

- 7.1.1.1. Polyethylene (PE)

- 7.1.1.2. Polypropylene (PP)

- 7.1.1.3. Polyvinyl Chloride (PVC)

- 7.1.1.4. Polystyrene (PS)

- 7.1.2. Engineering Thermoplastics

- 7.1.2.1. Polyamide (PA)

- 7.1.2.2. Polycarbonates (PC)

- 7.1.2.3. Polymethyl Methacrylate (PMMA)

- 7.1.2.4. Polyoxymethylene (POM)

- 7.1.2.5. Polyethylene Terephthalate (PET)

- 7.1.2.6. Polybutylene Terephthalate (PBT)

- 7.1.2.7. Acryloni

- 7.1.3. High-performance Engineering Thermoplastics

- 7.1.3.1. Polyether Ether Ketone (PEEK)

- 7.1.3.2. Liquid Crystal Polymer (LCP)

- 7.1.3.3. Polytetrafluoroethylene (PTFE)

- 7.1.3.4. Polyimide (PI)

- 7.1.4. Other Pr

- 7.1.1. Commodity Thermoplastics

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Packaging

- 7.2.2. Building and Construction

- 7.2.3. Automotive and Transportation

- 7.2.4. Electrical and Electronics

- 7.2.5. Sports and Leisure

- 7.2.6. Furniture and Bedding

- 7.2.7. Agriculture

- 7.2.8. Medical

- 7.2.9. Other End-user Industries

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United States

- 7.3.2. Canada

- 7.3.3. Mexico

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Canada North America Thermoplastics Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Commodity Thermoplastics

- 8.1.1.1. Polyethylene (PE)

- 8.1.1.2. Polypropylene (PP)

- 8.1.1.3. Polyvinyl Chloride (PVC)

- 8.1.1.4. Polystyrene (PS)

- 8.1.2. Engineering Thermoplastics

- 8.1.2.1. Polyamide (PA)

- 8.1.2.2. Polycarbonates (PC)

- 8.1.2.3. Polymethyl Methacrylate (PMMA)

- 8.1.2.4. Polyoxymethylene (POM)

- 8.1.2.5. Polyethylene Terephthalate (PET)

- 8.1.2.6. Polybutylene Terephthalate (PBT)

- 8.1.2.7. Acryloni

- 8.1.3. High-performance Engineering Thermoplastics

- 8.1.3.1. Polyether Ether Ketone (PEEK)

- 8.1.3.2. Liquid Crystal Polymer (LCP)

- 8.1.3.3. Polytetrafluoroethylene (PTFE)

- 8.1.3.4. Polyimide (PI)

- 8.1.4. Other Pr

- 8.1.1. Commodity Thermoplastics

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Packaging

- 8.2.2. Building and Construction

- 8.2.3. Automotive and Transportation

- 8.2.4. Electrical and Electronics

- 8.2.5. Sports and Leisure

- 8.2.6. Furniture and Bedding

- 8.2.7. Agriculture

- 8.2.8. Medical

- 8.2.9. Other End-user Industries

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. United States

- 8.3.2. Canada

- 8.3.3. Mexico

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Mexico North America Thermoplastics Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Commodity Thermoplastics

- 9.1.1.1. Polyethylene (PE)

- 9.1.1.2. Polypropylene (PP)

- 9.1.1.3. Polyvinyl Chloride (PVC)

- 9.1.1.4. Polystyrene (PS)

- 9.1.2. Engineering Thermoplastics

- 9.1.2.1. Polyamide (PA)

- 9.1.2.2. Polycarbonates (PC)

- 9.1.2.3. Polymethyl Methacrylate (PMMA)

- 9.1.2.4. Polyoxymethylene (POM)

- 9.1.2.5. Polyethylene Terephthalate (PET)

- 9.1.2.6. Polybutylene Terephthalate (PBT)

- 9.1.2.7. Acryloni

- 9.1.3. High-performance Engineering Thermoplastics

- 9.1.3.1. Polyether Ether Ketone (PEEK)

- 9.1.3.2. Liquid Crystal Polymer (LCP)

- 9.1.3.3. Polytetrafluoroethylene (PTFE)

- 9.1.3.4. Polyimide (PI)

- 9.1.4. Other Pr

- 9.1.1. Commodity Thermoplastics

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Packaging

- 9.2.2. Building and Construction

- 9.2.3. Automotive and Transportation

- 9.2.4. Electrical and Electronics

- 9.2.5. Sports and Leisure

- 9.2.6. Furniture and Bedding

- 9.2.7. Agriculture

- 9.2.8. Medical

- 9.2.9. Other End-user Industries

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. United States

- 9.3.2. Canada

- 9.3.3. Mexico

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 3M (incl Dyneon LLC)

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Arkema

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Asahi Kasei Corporation

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 BASF SE

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 Celanese Corporation

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 Chevron Phillips Chemical Company

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 Covestro AG

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Daicel Corporation

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 DSM

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.10 DuPont

- 10.1.10.1. Company Overview

- 10.1.10.2. Products

- 10.1.10.3. Company Financials

- 10.1.10.4. SWOT Analysis

- 10.1.11 Eastman Chemical Company

- 10.1.11.1. Company Overview

- 10.1.11.2. Products

- 10.1.11.3. Company Financials

- 10.1.11.4. SWOT Analysis

- 10.1.12 Evonik Industries AG

- 10.1.12.1. Company Overview

- 10.1.12.2. Products

- 10.1.12.3. Company Financials

- 10.1.12.4. SWOT Analysis

- 10.1.13 INEOS AG

- 10.1.13.1. Company Overview

- 10.1.13.2. Products

- 10.1.13.3. Company Financials

- 10.1.13.4. SWOT Analysis

- 10.1.14 LANXESS

- 10.1.14.1. Company Overview

- 10.1.14.2. Products

- 10.1.14.3. Company Financials

- 10.1.14.4. SWOT Analysis

- 10.1.15 LG Chem

- 10.1.15.1. Company Overview

- 10.1.15.2. Products

- 10.1.15.3. Company Financials

- 10.1.15.4. SWOT Analysis

- 10.1.16 LyondellBasell Industries Holdings B V (incl A Schulman Inc )

- 10.1.16.1. Company Overview

- 10.1.16.2. Products

- 10.1.16.3. Company Financials

- 10.1.16.4. SWOT Analysis

- 10.1.17 Mitsubishi Engineering-Plastics Corporation

- 10.1.17.1. Company Overview

- 10.1.17.2. Products

- 10.1.17.3. Company Financials

- 10.1.17.4. SWOT Analysis

- 10.1.18 Polyplastics Co Ltd

- 10.1.18.1. Company Overview

- 10.1.18.2. Products

- 10.1.18.3. Company Financials

- 10.1.18.4. SWOT Analysis

- 10.1.19 Röchling

- 10.1.19.1. Company Overview

- 10.1.19.2. Products

- 10.1.19.3. Company Financials

- 10.1.19.4. SWOT Analysis

- 10.1.20 SABIC

- 10.1.20.1. Company Overview

- 10.1.20.2. Products

- 10.1.20.3. Company Financials

- 10.1.20.4. SWOT Analysis

- 10.1.21 Solvay

- 10.1.21.1. Company Overview

- 10.1.21.2. Products

- 10.1.21.3. Company Financials

- 10.1.21.4. SWOT Analysis

- 10.1.22 TEIJIN LIMITED*List Not Exhaustive

- 10.1.22.1. Company Overview

- 10.1.22.2. Products

- 10.1.22.3. Company Financials

- 10.1.22.4. SWOT Analysis

- 10.1.1 3M (incl Dyneon LLC)

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: Global North America Thermoplastics Industry Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: United States North America Thermoplastics Industry Revenue (million), by Product Type 2025 & 2033

- Figure 3: United States North America Thermoplastics Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 4: United States North America Thermoplastics Industry Revenue (million), by End-user Industry 2025 & 2033

- Figure 5: United States North America Thermoplastics Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 6: United States North America Thermoplastics Industry Revenue (million), by Geography 2025 & 2033

- Figure 7: United States North America Thermoplastics Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 8: United States North America Thermoplastics Industry Revenue (million), by Country 2025 & 2033

- Figure 9: United States North America Thermoplastics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Canada North America Thermoplastics Industry Revenue (million), by Product Type 2025 & 2033

- Figure 11: Canada North America Thermoplastics Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 12: Canada North America Thermoplastics Industry Revenue (million), by End-user Industry 2025 & 2033

- Figure 13: Canada North America Thermoplastics Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 14: Canada North America Thermoplastics Industry Revenue (million), by Geography 2025 & 2033

- Figure 15: Canada North America Thermoplastics Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 16: Canada North America Thermoplastics Industry Revenue (million), by Country 2025 & 2033

- Figure 17: Canada North America Thermoplastics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Mexico North America Thermoplastics Industry Revenue (million), by Product Type 2025 & 2033

- Figure 19: Mexico North America Thermoplastics Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 20: Mexico North America Thermoplastics Industry Revenue (million), by End-user Industry 2025 & 2033

- Figure 21: Mexico North America Thermoplastics Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 22: Mexico North America Thermoplastics Industry Revenue (million), by Geography 2025 & 2033

- Figure 23: Mexico North America Thermoplastics Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 24: Mexico North America Thermoplastics Industry Revenue (million), by Country 2025 & 2033

- Figure 25: Mexico North America Thermoplastics Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global North America Thermoplastics Industry Revenue million Forecast, by Product Type 2020 & 2033

- Table 2: Global North America Thermoplastics Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 3: Global North America Thermoplastics Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 4: Global North America Thermoplastics Industry Revenue million Forecast, by Region 2020 & 2033

- Table 5: Global North America Thermoplastics Industry Revenue million Forecast, by Product Type 2020 & 2033

- Table 6: Global North America Thermoplastics Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 7: Global North America Thermoplastics Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 8: Global North America Thermoplastics Industry Revenue million Forecast, by Country 2020 & 2033

- Table 9: Global North America Thermoplastics Industry Revenue million Forecast, by Product Type 2020 & 2033

- Table 10: Global North America Thermoplastics Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 11: Global North America Thermoplastics Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 12: Global North America Thermoplastics Industry Revenue million Forecast, by Country 2020 & 2033

- Table 13: Global North America Thermoplastics Industry Revenue million Forecast, by Product Type 2020 & 2033

- Table 14: Global North America Thermoplastics Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 15: Global North America Thermoplastics Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 16: Global North America Thermoplastics Industry Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Thermoplastics Industry?

The projected CAGR is approximately 4.07%.

2. Which companies are prominent players in the North America Thermoplastics Industry?

Key companies in the market include 3M (incl Dyneon LLC), Arkema, Asahi Kasei Corporation, BASF SE, Celanese Corporation, Chevron Phillips Chemical Company, Covestro AG, Daicel Corporation, DSM, DuPont, Eastman Chemical Company, Evonik Industries AG, INEOS AG, LANXESS, LG Chem, LyondellBasell Industries Holdings B V (incl A Schulman Inc ), Mitsubishi Engineering-Plastics Corporation, Polyplastics Co Ltd, Röchling, SABIC, Solvay, TEIJIN LIMITED*List Not Exhaustive.

3. What are the main segments of the North America Thermoplastics Industry?

The market segments include Product Type, End-user Industry, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 65 million as of 2022.

5. What are some drivers contributing to market growth?

; Growing Demand from Various End-user Industries; Other Drivers.

6. What are the notable trends driving market growth?

Packaging Industry to Dominate the Market.

7. Are there any restraints impacting market growth?

; Growing Demand from Various End-user Industries; Other Drivers.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Thermoplastics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Thermoplastics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Thermoplastics Industry?

To stay informed about further developments, trends, and reports in the North America Thermoplastics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence