Key Insights

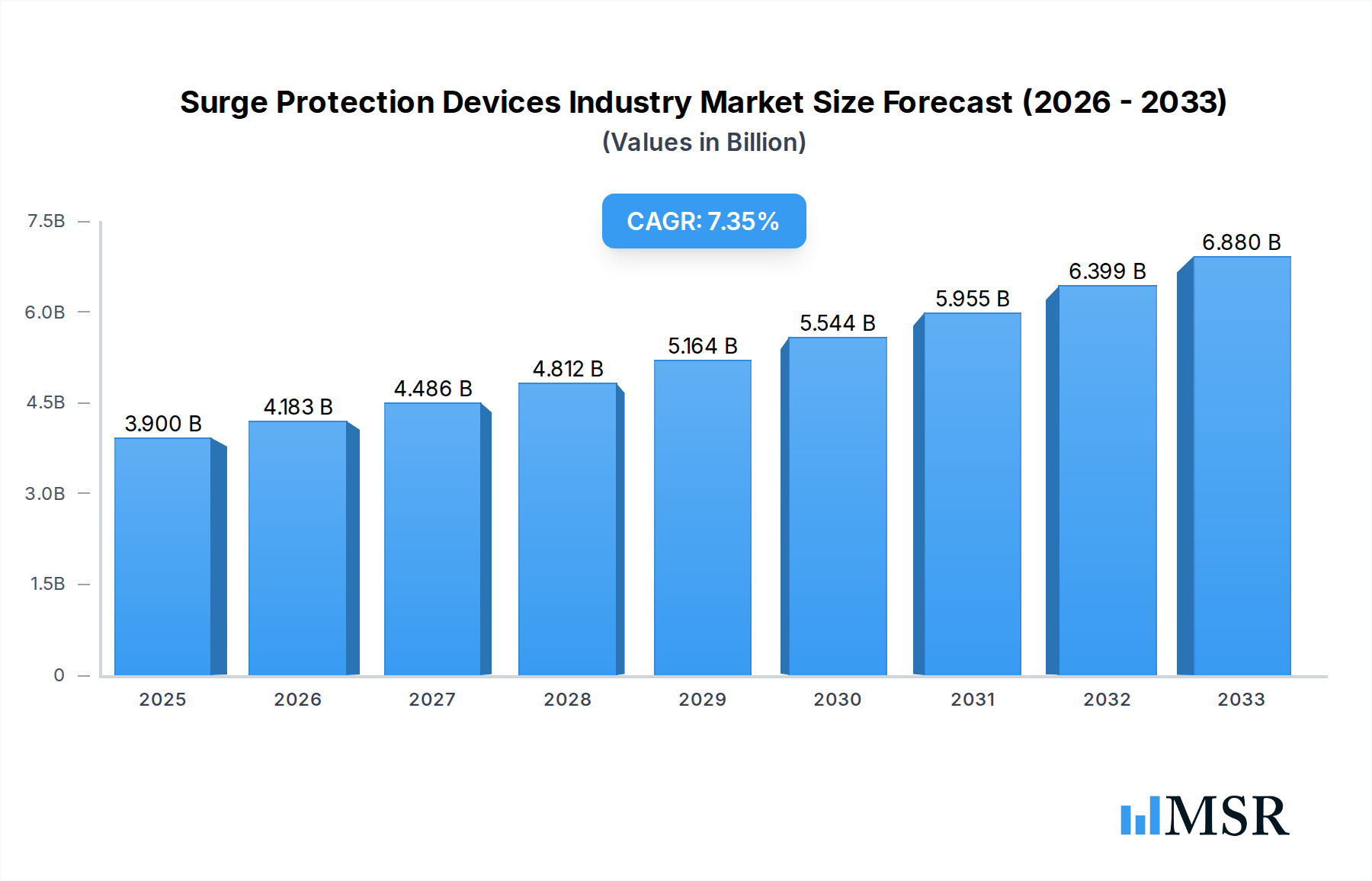

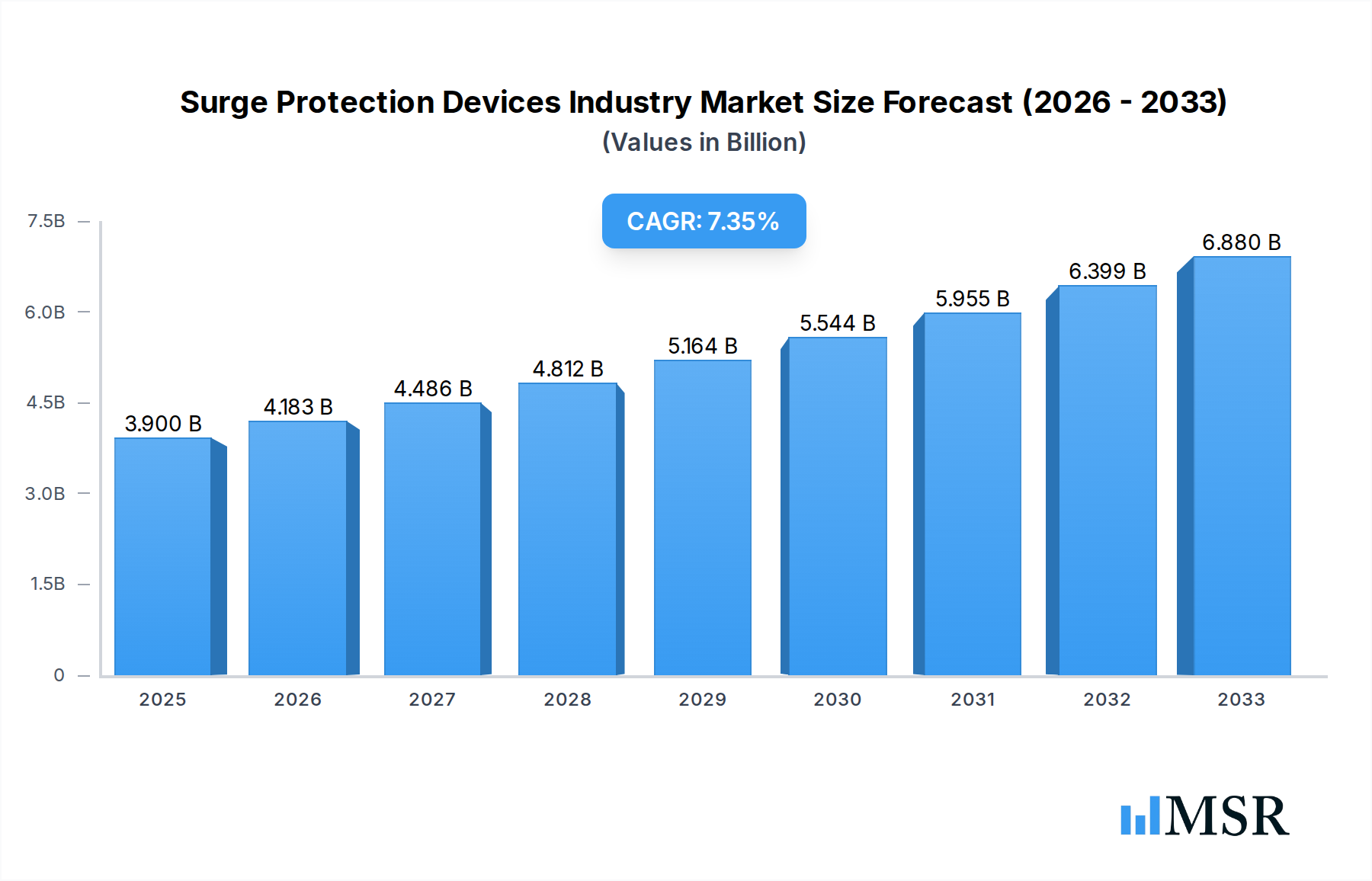

The global Surge Protection Devices (SPD) market is poised for significant expansion, projected to reach an estimated $3.9 billion in 2025, with a robust Compound Annual Growth Rate (CAGR) of 7.1% expected from 2025 to 2033. This substantial growth is propelled by an increasing reliance on electronic devices across all sectors, coupled with the rising threat of power surges due to unstable power grids and an escalating adoption of renewable energy sources, which can introduce transient voltage fluctuations. The industrial sector is a key driver, demanding high-capacity SPDs to safeguard sensitive machinery and critical infrastructure from costly damage and downtime. Similarly, the commercial segment, encompassing data centers, telecommunications, and retail, is experiencing heightened demand for reliable surge protection to ensure operational continuity and data integrity. The residential segment also contributes, driven by the proliferation of smart home technology and the need to protect increasingly sophisticated consumer electronics.

Surge Protection Devices Industry Market Size (In Billion)

The market is characterized by distinct segmentation, with "Hard-Wired" surge protectors dominating due to their permanent integration in industrial and commercial settings, offering superior protection. In terms of discharge current, the "10KA-25KA" segment is anticipated to witness considerable growth as higher levels of protection become standard. Key market trends include the integration of smart surge protection features, offering remote monitoring and control capabilities, and the development of more compact and efficient SPD designs. However, challenges such as the high initial cost of advanced SPD systems and a lack of widespread awareness regarding the importance of surge protection in certain regions could temper growth. Leading companies like ABB Ltd, Schneider Electric SE, and Eaton Corporation Plc are actively innovating and expanding their product portfolios to capture market share, further shaping the competitive landscape.

Surge Protection Devices Industry Company Market Share

This in-depth report provides an indispensable analysis of the global Surge Protection Devices (SPD) industry, covering the historical period (2019-2024), the base year (2025), and a detailed forecast period (2025-2033). We offer actionable insights for industry stakeholders, including manufacturers, suppliers, investors, and end-users, by examining market dynamics, key segments, emerging trends, and strategic opportunities. The global surge protection devices market is projected to reach a valuation of over $7 billion by 2025, with projected growth to exceed over $10 billion by 2033, driven by a CAGR of approximately 4.5% during the forecast period.

Surge Protection Devices Industry Market Concentration & Dynamics

The surge protection devices industry exhibits a moderately concentrated market landscape, with leading players such as ABB Ltd, Tripp Lite, Leviton Manufacturing Company Inc, Schneider Electric SE, Littelfuse Inc, Belkin International, Hubbell Incorporated, Emerson Electric Co, Legrand, and Eaton Corporation Plc holding significant market shares. Innovation ecosystems are driven by ongoing research and development focused on enhanced surge suppression capabilities, miniaturization, and smart SPD integration for IoT applications. Regulatory frameworks, including IEC and UL standards, play a crucial role in dictating product quality and safety, influencing market entry and competitive positioning. While substitute products like fuses and circuit breakers offer basic overcurrent protection, they lack the specific transient voltage suppression capabilities of SPDs, limiting their substitutability in critical applications. End-user trends indicate a growing demand for reliable protection in residential, commercial, and industrial sectors, fueled by increasing digitization and reliance on sensitive electronic equipment. Merger and acquisition activities are observed as key strategies for market expansion, technology acquisition, and consolidating market presence, with an estimated over 50 M&A deals recorded over the historical period.

Surge Protection Devices Industry Industry Insights & Trends

The global surge protection devices market is experiencing robust growth, propelled by several key drivers. The increasing proliferation of sensitive electronic devices across residential, commercial, and industrial sectors necessitates reliable surge protection to prevent costly damage and downtime. The escalating frequency and intensity of lightning strikes, exacerbated by climate change, further amplify the demand for effective surge arresters. Advancements in technology, such as the development of hybrid surge protection devices and smart SPDs with remote monitoring capabilities, are creating new market opportunities. The growing adoption of renewable energy sources like solar photovoltaic (PV) systems and battery energy storage systems (BESS), which are inherently vulnerable to power surges, is a significant growth catalyst. Furthermore, the rapid expansion of electric vehicle (EV) charging infrastructure, demanding robust protection for charging stations and vehicles, is contributing to market expansion. The market size for surge protection devices was estimated to be over $6.5 billion in 2024 and is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 4.5% through 2033. The increasing focus on cybersecurity and data integrity also indirectly drives demand for surge protection, as power surges can disrupt or damage critical network infrastructure. The evolving consumer behavior towards valuing device longevity and data security is pushing individuals and businesses to invest in preventative measures like surge protection.

Key Markets & Segments Leading Surge Protection Devices Industry

The Industrial end-user segment is a dominant force in the surge protection devices industry, driven by the critical need to protect expensive and sensitive machinery, control systems, and data networks in manufacturing facilities, power plants, and data centers. Economic growth and infrastructure development in regions like North America and Asia Pacific further fuel this demand.

- End User - Industrial:

- Drivers: High concentration of sensitive industrial electronics, stringent safety regulations, and the high cost of equipment failure.

- Dominance Analysis: Industrial operations often involve large-scale power distribution and highly complex electronic systems, making them particularly susceptible to surge events. The implementation of stringent safety standards and the direct correlation between downtime and significant financial losses make robust surge protection a non-negotiable requirement for industrial facilities. The continuous operation demands of these sectors necessitate investment in reliable SPD solutions.

The Commercial segment is also experiencing significant growth, propelled by the increasing reliance on electronic infrastructure in offices, retail spaces, and healthcare facilities. Growing awareness of the potential for data loss and equipment damage from power surges is driving adoption.

- End User - Commercial:

- Drivers: Proliferation of IT equipment, data centers, and the need for business continuity.

- Dominance Analysis: Modern commercial enterprises are heavily dependent on technology for daily operations. From servers and workstations to point-of-sale systems and security equipment, these devices are vulnerable to surge damage. The imperative to maintain business continuity and prevent data loss makes surge protection a crucial investment for commercial entities.

The Residential segment, while historically smaller, is witnessing substantial growth due to the increasing number of electronic devices in homes and growing consumer awareness of surge protection benefits.

- End User - Residential:

- Drivers: High density of home electronics, smart home adoption, and rising consumer awareness.

- Dominance Analysis: The average home now contains a multitude of electronic devices, from televisions and computers to gaming consoles and smart home appliances. These devices, often connected to the internet, are susceptible to surges originating from both external events like lightning and internal power fluctuations. The rising adoption of smart home technologies, which rely on interconnected electronic devices, further accentuates the need for comprehensive surge protection.

In terms of Type, Hard-Wired surge protection devices dominate the industrial and commercial sectors due to their permanent installation and higher surge current handling capabilities. Plug-In surge protectors are prevalent in residential and smaller commercial applications. For Discharge Current, categories like 10KA-25KA and Above 25KA are crucial for industrial applications, while Upto 10KA is common in residential and light commercial use.

Surge Protection Devices Industry Product Developments

Product developments in the surge protection devices industry are focused on enhancing performance, intelligence, and application-specific solutions. Manufacturers are introducing advanced hybrid SPD technologies that combine metal oxide varistor (MOV) and gas discharge tube (GDT) technologies for superior surge suppression and longevity. The integration of IoT capabilities allows for remote monitoring, diagnostics, and predictive maintenance of SPDs, enabling proactive identification of potential failures. Innovations are also geared towards developing compact and modular SPD solutions for easier integration into existing systems, particularly for emerging applications like electric vehicle charging stations and battery energy storage systems. The development of SPDs with higher discharge current ratings and enhanced thermal management is crucial for industrial and high-power applications, ensuring reliability and safety.

Challenges in the Surge Protection Devices Industry Market

The surge protection devices industry faces several challenges that can hinder its growth trajectory.

- Regulatory Hurdles: Navigating diverse and evolving international safety standards and certification processes can be complex and costly for manufacturers, especially for smaller players.

- Supply Chain Disruptions: Global supply chain vulnerabilities, as experienced in recent years, can impact the availability and cost of critical components required for SPD manufacturing.

- Competitive Pressures: Intense competition from established players and new entrants, particularly in the cost-sensitive residential segment, can lead to price erosion and reduced profit margins.

- Lack of Consumer Awareness: Despite advancements, a significant portion of the end-user market, especially in residential sectors, remains unaware of the critical need for surge protection, leading to a slower adoption rate than potential.

Forces Driving Surge Protection Devices Industry Growth

Several key forces are propelling the growth of the surge protection devices industry.

- Technological Advancements: Continuous innovation in SPD technology, including the development of smarter, more efficient, and application-specific devices, is a primary growth driver.

- Increasing Digitization: The pervasive integration of sensitive electronic devices across all sectors, from homes and offices to factories and critical infrastructure, creates an escalating need for protection against transient overvoltages.

- Growing Awareness of Power Quality: An increasing understanding among consumers and businesses about the detrimental effects of power quality issues, including surges, on electronic equipment, data integrity, and operational continuity is fostering demand.

- Climate Change Impact: The rise in the frequency and severity of extreme weather events, such as lightning storms, directly contributes to the demand for enhanced surge protection solutions.

- Government Regulations and Standards: Evolving safety standards and increasing mandates for surge protection in critical infrastructure and new technology deployments are acting as significant market accelerators.

Long-Term Growth Catalysts in the Surge Protection Devices Industry Market

Long-term growth in the surge protection devices market will be significantly influenced by continued innovation and strategic market expansion. The development of advanced SPD solutions tailored for emerging technologies like 5G infrastructure, artificial intelligence (AI) hardware, and quantum computing will open new revenue streams. Furthermore, the increasing focus on grid modernization and the integration of distributed energy resources will drive demand for sophisticated surge protection at various points in the power distribution network. Partnerships and collaborations between SPD manufacturers and manufacturers of electronic equipment, as well as smart home technology providers, will foster greater product integration and wider market penetration. Expansion into developing economies, where infrastructure is being rapidly modernized and the adoption of electronics is on the rise, presents substantial untapped growth potential.

Emerging Opportunities in Surge Protection Devices Industry

Emerging opportunities in the surge protection devices industry are predominantly linked to new technological frontiers and evolving consumer preferences. The rapid growth of the Internet of Things (IoT) ecosystem, with its vast network of connected devices, creates a substantial demand for localized and intelligent surge protection. The burgeoning electric vehicle (EV) market necessitates robust surge protection solutions for charging infrastructure, vehicle on-board chargers, and battery management systems. The increasing deployment of renewable energy systems, particularly solar and wind farms, and the integration of battery energy storage systems (BESS), which are highly susceptible to surge events, present a significant opportunity for specialized SPD solutions. Furthermore, the trend towards smart grids and smart cities will require advanced, network-connected surge protection devices for enhanced grid reliability and resilience.

Leading Players in the Surge Protection Devices Industry Sector

- ABB Ltd

- Tripp Lite

- Leviton Manufacturing Company Inc

- Schneider Electric SE

- Littelfuse Inc

- Belkin International

- Hubbell Incorporated

- Emerson Electric Co

- Legrand

- Eaton Corporation Plc

Key Milestones in Surge Protection Devices Industry Industry

- April 2022: Raycap showcased its latest advancements in surge protection for photovoltaic systems, battery energy storage, and e-car charging stations at The smarter E Europe.

- September 2021: Toshiba Energy Systems & Solutions Corporation announced its intention to nearly triple its production capacity of polymer-housed surge arresters by April 2022 to meet growing demand for overvoltage protection in power transmission and distribution equipment.

Strategic Outlook for Surge Protection Devices Industry Market

The strategic outlook for the surge protection devices industry market is highly positive, driven by persistent technological innovation and increasing global demand. Key growth accelerators include the ongoing expansion of industrial automation, the widespread adoption of smart home technologies, and the critical need to protect advanced infrastructure in sectors like telecommunications and renewable energy. Manufacturers are expected to focus on developing next-generation SPDs with enhanced cybersecurity features, integrated diagnostics, and improved energy efficiency. Strategic partnerships with infrastructure developers and electronic device manufacturers will be crucial for market penetration. Furthermore, the increasing regulatory emphasis on grid resilience and the protection of critical infrastructure will create sustained demand for high-performance surge protection solutions. The market is poised for continued robust growth, offering significant opportunities for both established players and innovative newcomers.

Surge Protection Devices Industry Segmentation

-

1. Type

- 1.1. Hard-Wired

- 1.2. Plug-In

- 1.3. Line Cord

-

2. Discharge Current

- 2.1. Upto 10KA

- 2.2. 10KA-25KA

- 2.3. Above 25KA

-

3. End User

- 3.1. Industrial

- 3.2. Commercial

- 3.3. Residential

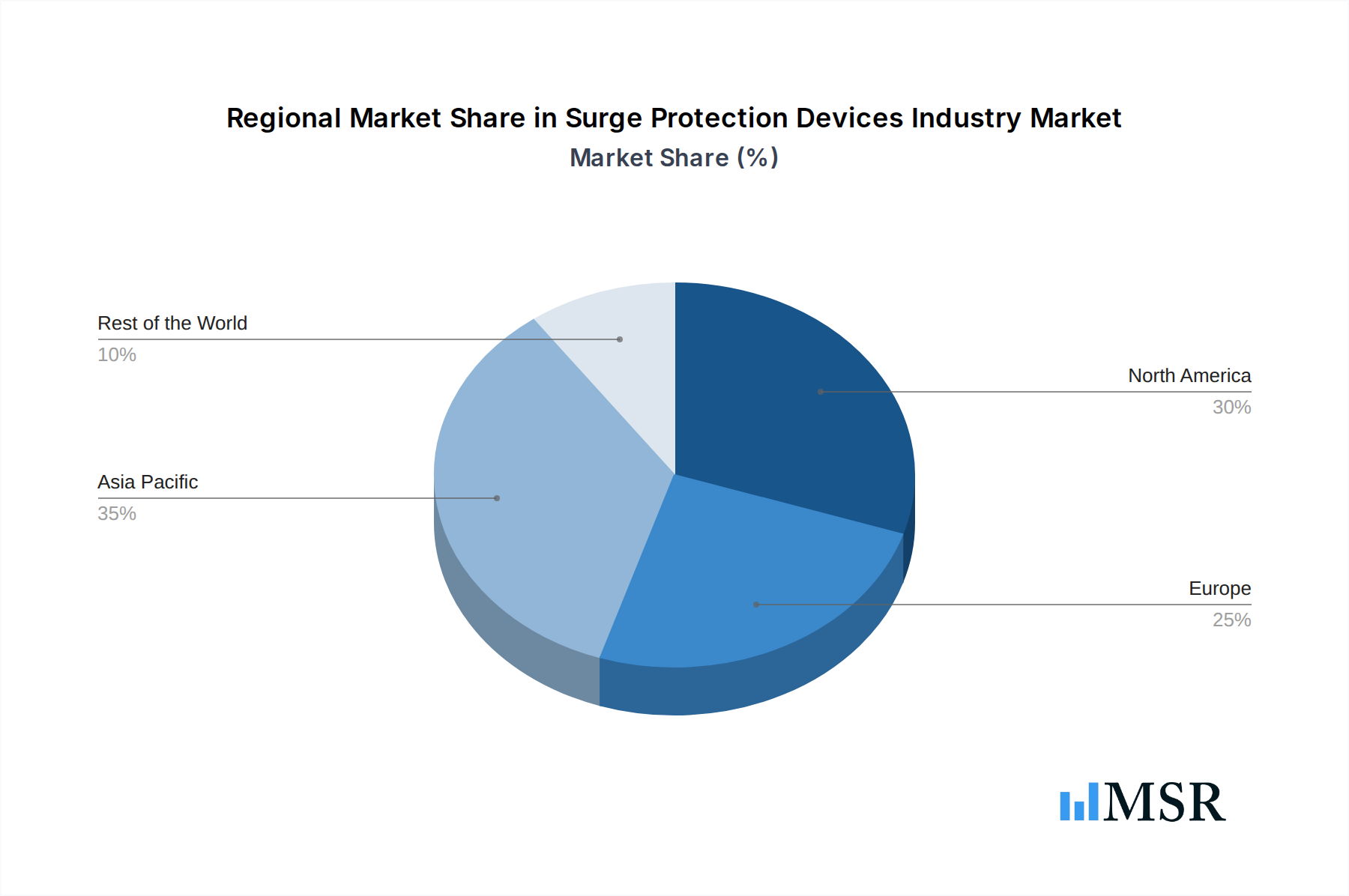

Surge Protection Devices Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Rest of the World

Surge Protection Devices Industry Regional Market Share

Geographic Coverage of Surge Protection Devices Industry

Surge Protection Devices Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Hard-Wired

- 5.1.2. Plug-In

- 5.1.3. Line Cord

- 5.2. Market Analysis, Insights and Forecast - by Discharge Current

- 5.2.1. Upto 10KA

- 5.2.2. 10KA-25KA

- 5.2.3. Above 25KA

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Industrial

- 5.3.2. Commercial

- 5.3.3. Residential

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Surge Protection Devices Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Hard-Wired

- 6.1.2. Plug-In

- 6.1.3. Line Cord

- 6.2. Market Analysis, Insights and Forecast - by Discharge Current

- 6.2.1. Upto 10KA

- 6.2.2. 10KA-25KA

- 6.2.3. Above 25KA

- 6.3. Market Analysis, Insights and Forecast - by End User

- 6.3.1. Industrial

- 6.3.2. Commercial

- 6.3.3. Residential

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Surge Protection Devices Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Hard-Wired

- 7.1.2. Plug-In

- 7.1.3. Line Cord

- 7.2. Market Analysis, Insights and Forecast - by Discharge Current

- 7.2.1. Upto 10KA

- 7.2.2. 10KA-25KA

- 7.2.3. Above 25KA

- 7.3. Market Analysis, Insights and Forecast - by End User

- 7.3.1. Industrial

- 7.3.2. Commercial

- 7.3.3. Residential

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Surge Protection Devices Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Hard-Wired

- 8.1.2. Plug-In

- 8.1.3. Line Cord

- 8.2. Market Analysis, Insights and Forecast - by Discharge Current

- 8.2.1. Upto 10KA

- 8.2.2. 10KA-25KA

- 8.2.3. Above 25KA

- 8.3. Market Analysis, Insights and Forecast - by End User

- 8.3.1. Industrial

- 8.3.2. Commercial

- 8.3.3. Residential

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Surge Protection Devices Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Hard-Wired

- 9.1.2. Plug-In

- 9.1.3. Line Cord

- 9.2. Market Analysis, Insights and Forecast - by Discharge Current

- 9.2.1. Upto 10KA

- 9.2.2. 10KA-25KA

- 9.2.3. Above 25KA

- 9.3. Market Analysis, Insights and Forecast - by End User

- 9.3.1. Industrial

- 9.3.2. Commercial

- 9.3.3. Residential

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Rest of the World Surge Protection Devices Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Hard-Wired

- 10.1.2. Plug-In

- 10.1.3. Line Cord

- 10.2. Market Analysis, Insights and Forecast - by Discharge Current

- 10.2.1. Upto 10KA

- 10.2.2. 10KA-25KA

- 10.2.3. Above 25KA

- 10.3. Market Analysis, Insights and Forecast - by End User

- 10.3.1. Industrial

- 10.3.2. Commercial

- 10.3.3. Residential

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 ABB Ltd

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Tripp Lite

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Leviton Manufacturing Company Inc

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Schneider Electric Se

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Littelfuse Inc

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Belkin International

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Hubbell Incorporated

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Emersen Electric Co

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Legrand

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Eaton Corporation Plc

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.1 ABB Ltd

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Surge Protection Devices Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Surge Protection Devices Industry Volume Breakdown (K Units, %) by Region 2025 & 2033

- Figure 3: North America Surge Protection Devices Industry Revenue (billion), by Type 2025 & 2033

- Figure 4: North America Surge Protection Devices Industry Volume (K Units), by Type 2025 & 2033

- Figure 5: North America Surge Protection Devices Industry Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Surge Protection Devices Industry Volume Share (%), by Type 2025 & 2033

- Figure 7: North America Surge Protection Devices Industry Revenue (billion), by Discharge Current 2025 & 2033

- Figure 8: North America Surge Protection Devices Industry Volume (K Units), by Discharge Current 2025 & 2033

- Figure 9: North America Surge Protection Devices Industry Revenue Share (%), by Discharge Current 2025 & 2033

- Figure 10: North America Surge Protection Devices Industry Volume Share (%), by Discharge Current 2025 & 2033

- Figure 11: North America Surge Protection Devices Industry Revenue (billion), by End User 2025 & 2033

- Figure 12: North America Surge Protection Devices Industry Volume (K Units), by End User 2025 & 2033

- Figure 13: North America Surge Protection Devices Industry Revenue Share (%), by End User 2025 & 2033

- Figure 14: North America Surge Protection Devices Industry Volume Share (%), by End User 2025 & 2033

- Figure 15: North America Surge Protection Devices Industry Revenue (billion), by Country 2025 & 2033

- Figure 16: North America Surge Protection Devices Industry Volume (K Units), by Country 2025 & 2033

- Figure 17: North America Surge Protection Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: North America Surge Protection Devices Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: Europe Surge Protection Devices Industry Revenue (billion), by Type 2025 & 2033

- Figure 20: Europe Surge Protection Devices Industry Volume (K Units), by Type 2025 & 2033

- Figure 21: Europe Surge Protection Devices Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: Europe Surge Protection Devices Industry Volume Share (%), by Type 2025 & 2033

- Figure 23: Europe Surge Protection Devices Industry Revenue (billion), by Discharge Current 2025 & 2033

- Figure 24: Europe Surge Protection Devices Industry Volume (K Units), by Discharge Current 2025 & 2033

- Figure 25: Europe Surge Protection Devices Industry Revenue Share (%), by Discharge Current 2025 & 2033

- Figure 26: Europe Surge Protection Devices Industry Volume Share (%), by Discharge Current 2025 & 2033

- Figure 27: Europe Surge Protection Devices Industry Revenue (billion), by End User 2025 & 2033

- Figure 28: Europe Surge Protection Devices Industry Volume (K Units), by End User 2025 & 2033

- Figure 29: Europe Surge Protection Devices Industry Revenue Share (%), by End User 2025 & 2033

- Figure 30: Europe Surge Protection Devices Industry Volume Share (%), by End User 2025 & 2033

- Figure 31: Europe Surge Protection Devices Industry Revenue (billion), by Country 2025 & 2033

- Figure 32: Europe Surge Protection Devices Industry Volume (K Units), by Country 2025 & 2033

- Figure 33: Europe Surge Protection Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Europe Surge Protection Devices Industry Volume Share (%), by Country 2025 & 2033

- Figure 35: Asia Pacific Surge Protection Devices Industry Revenue (billion), by Type 2025 & 2033

- Figure 36: Asia Pacific Surge Protection Devices Industry Volume (K Units), by Type 2025 & 2033

- Figure 37: Asia Pacific Surge Protection Devices Industry Revenue Share (%), by Type 2025 & 2033

- Figure 38: Asia Pacific Surge Protection Devices Industry Volume Share (%), by Type 2025 & 2033

- Figure 39: Asia Pacific Surge Protection Devices Industry Revenue (billion), by Discharge Current 2025 & 2033

- Figure 40: Asia Pacific Surge Protection Devices Industry Volume (K Units), by Discharge Current 2025 & 2033

- Figure 41: Asia Pacific Surge Protection Devices Industry Revenue Share (%), by Discharge Current 2025 & 2033

- Figure 42: Asia Pacific Surge Protection Devices Industry Volume Share (%), by Discharge Current 2025 & 2033

- Figure 43: Asia Pacific Surge Protection Devices Industry Revenue (billion), by End User 2025 & 2033

- Figure 44: Asia Pacific Surge Protection Devices Industry Volume (K Units), by End User 2025 & 2033

- Figure 45: Asia Pacific Surge Protection Devices Industry Revenue Share (%), by End User 2025 & 2033

- Figure 46: Asia Pacific Surge Protection Devices Industry Volume Share (%), by End User 2025 & 2033

- Figure 47: Asia Pacific Surge Protection Devices Industry Revenue (billion), by Country 2025 & 2033

- Figure 48: Asia Pacific Surge Protection Devices Industry Volume (K Units), by Country 2025 & 2033

- Figure 49: Asia Pacific Surge Protection Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Asia Pacific Surge Protection Devices Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Rest of the World Surge Protection Devices Industry Revenue (billion), by Type 2025 & 2033

- Figure 52: Rest of the World Surge Protection Devices Industry Volume (K Units), by Type 2025 & 2033

- Figure 53: Rest of the World Surge Protection Devices Industry Revenue Share (%), by Type 2025 & 2033

- Figure 54: Rest of the World Surge Protection Devices Industry Volume Share (%), by Type 2025 & 2033

- Figure 55: Rest of the World Surge Protection Devices Industry Revenue (billion), by Discharge Current 2025 & 2033

- Figure 56: Rest of the World Surge Protection Devices Industry Volume (K Units), by Discharge Current 2025 & 2033

- Figure 57: Rest of the World Surge Protection Devices Industry Revenue Share (%), by Discharge Current 2025 & 2033

- Figure 58: Rest of the World Surge Protection Devices Industry Volume Share (%), by Discharge Current 2025 & 2033

- Figure 59: Rest of the World Surge Protection Devices Industry Revenue (billion), by End User 2025 & 2033

- Figure 60: Rest of the World Surge Protection Devices Industry Volume (K Units), by End User 2025 & 2033

- Figure 61: Rest of the World Surge Protection Devices Industry Revenue Share (%), by End User 2025 & 2033

- Figure 62: Rest of the World Surge Protection Devices Industry Volume Share (%), by End User 2025 & 2033

- Figure 63: Rest of the World Surge Protection Devices Industry Revenue (billion), by Country 2025 & 2033

- Figure 64: Rest of the World Surge Protection Devices Industry Volume (K Units), by Country 2025 & 2033

- Figure 65: Rest of the World Surge Protection Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 66: Rest of the World Surge Protection Devices Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Surge Protection Devices Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Surge Protection Devices Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 3: Global Surge Protection Devices Industry Revenue billion Forecast, by Discharge Current 2020 & 2033

- Table 4: Global Surge Protection Devices Industry Volume K Units Forecast, by Discharge Current 2020 & 2033

- Table 5: Global Surge Protection Devices Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 6: Global Surge Protection Devices Industry Volume K Units Forecast, by End User 2020 & 2033

- Table 7: Global Surge Protection Devices Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 8: Global Surge Protection Devices Industry Volume K Units Forecast, by Region 2020 & 2033

- Table 9: Global Surge Protection Devices Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 10: Global Surge Protection Devices Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 11: Global Surge Protection Devices Industry Revenue billion Forecast, by Discharge Current 2020 & 2033

- Table 12: Global Surge Protection Devices Industry Volume K Units Forecast, by Discharge Current 2020 & 2033

- Table 13: Global Surge Protection Devices Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 14: Global Surge Protection Devices Industry Volume K Units Forecast, by End User 2020 & 2033

- Table 15: Global Surge Protection Devices Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global Surge Protection Devices Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 17: Global Surge Protection Devices Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Surge Protection Devices Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 19: Global Surge Protection Devices Industry Revenue billion Forecast, by Discharge Current 2020 & 2033

- Table 20: Global Surge Protection Devices Industry Volume K Units Forecast, by Discharge Current 2020 & 2033

- Table 21: Global Surge Protection Devices Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 22: Global Surge Protection Devices Industry Volume K Units Forecast, by End User 2020 & 2033

- Table 23: Global Surge Protection Devices Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global Surge Protection Devices Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 25: Global Surge Protection Devices Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 26: Global Surge Protection Devices Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 27: Global Surge Protection Devices Industry Revenue billion Forecast, by Discharge Current 2020 & 2033

- Table 28: Global Surge Protection Devices Industry Volume K Units Forecast, by Discharge Current 2020 & 2033

- Table 29: Global Surge Protection Devices Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 30: Global Surge Protection Devices Industry Volume K Units Forecast, by End User 2020 & 2033

- Table 31: Global Surge Protection Devices Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 32: Global Surge Protection Devices Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 33: Global Surge Protection Devices Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 34: Global Surge Protection Devices Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 35: Global Surge Protection Devices Industry Revenue billion Forecast, by Discharge Current 2020 & 2033

- Table 36: Global Surge Protection Devices Industry Volume K Units Forecast, by Discharge Current 2020 & 2033

- Table 37: Global Surge Protection Devices Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 38: Global Surge Protection Devices Industry Volume K Units Forecast, by End User 2020 & 2033

- Table 39: Global Surge Protection Devices Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 40: Global Surge Protection Devices Industry Volume K Units Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Surge Protection Devices Industry?

The projected CAGR is approximately 8.1%.

2. Which companies are prominent players in the Surge Protection Devices Industry?

Key companies in the market include ABB Ltd, Tripp Lite, Leviton Manufacturing Company Inc, Schneider Electric Se, Littelfuse Inc, Belkin International, Hubbell Incorporated, Emersen Electric Co, Legrand, Eaton Corporation Plc.

3. What are the main segments of the Surge Protection Devices Industry?

The market segments include Type, Discharge Current, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.8 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Electronic Device Protection Systems; Consistent Power Quality Problems.

6. What are the notable trends driving market growth?

Residential Segment is one of the Factor Driving the Market.

7. Are there any restraints impacting market growth?

Additional Cost for Installation.

8. Can you provide examples of recent developments in the market?

April 2022 - The most recent advancements in surge protection for PV systems, battery energy storage, and e-car charging stations will be displayed by Raycap, an international manufacturer of electronic components for surge protection, communication, and monitoring, at booth 350 in hall A5. For years, the Raycap systems have offered trustworthy defense against surge and lightning-related damage. In addition to showcasing its tried-and-true photovoltaic and inverter solutions at The smarter E Europe, the company will also showcase the most recent parts for battery energy storage systems and e-charging station protection.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Units.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Surge Protection Devices Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Surge Protection Devices Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Surge Protection Devices Industry?

To stay informed about further developments, trends, and reports in the Surge Protection Devices Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence