Key Insights

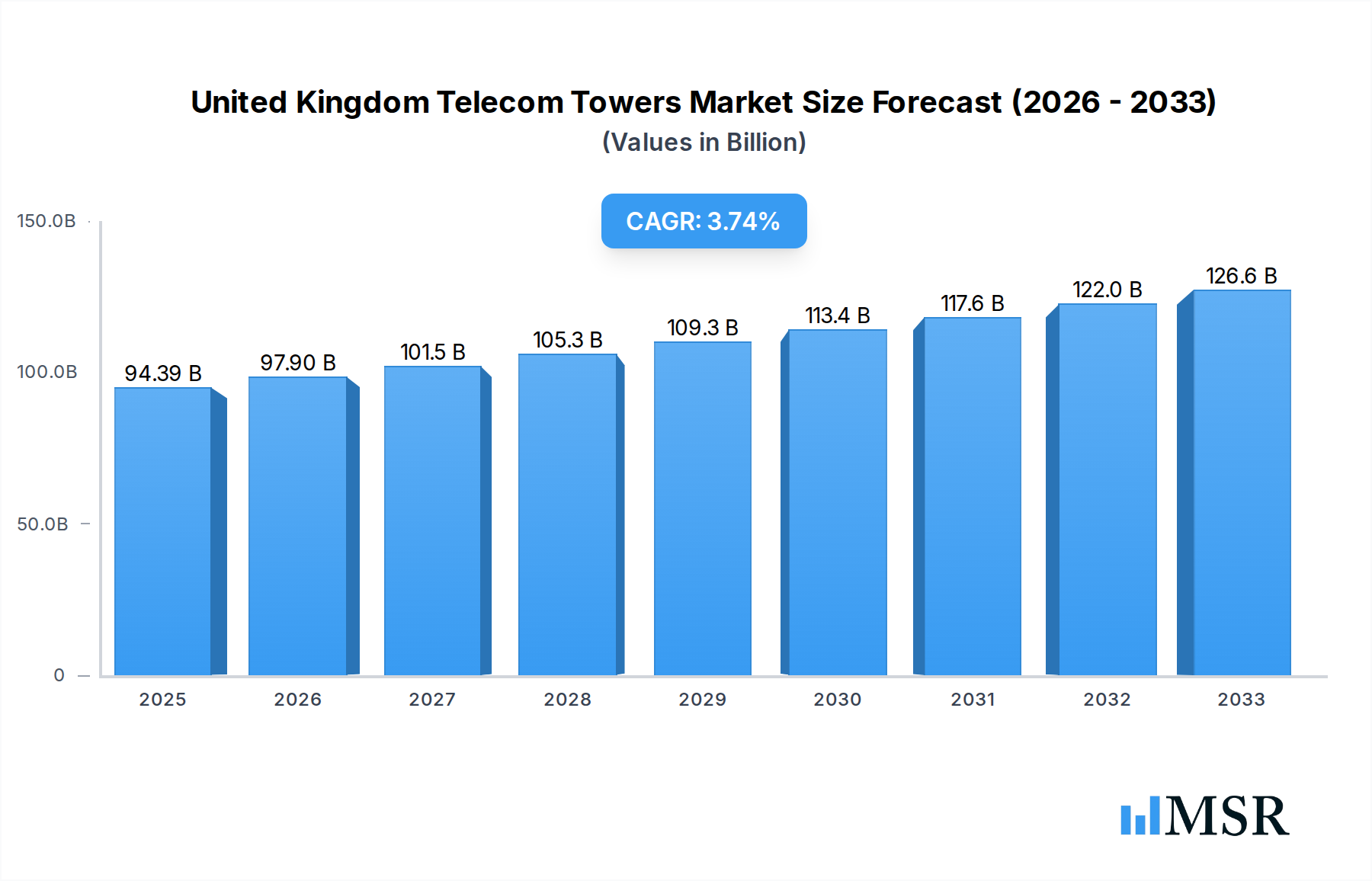

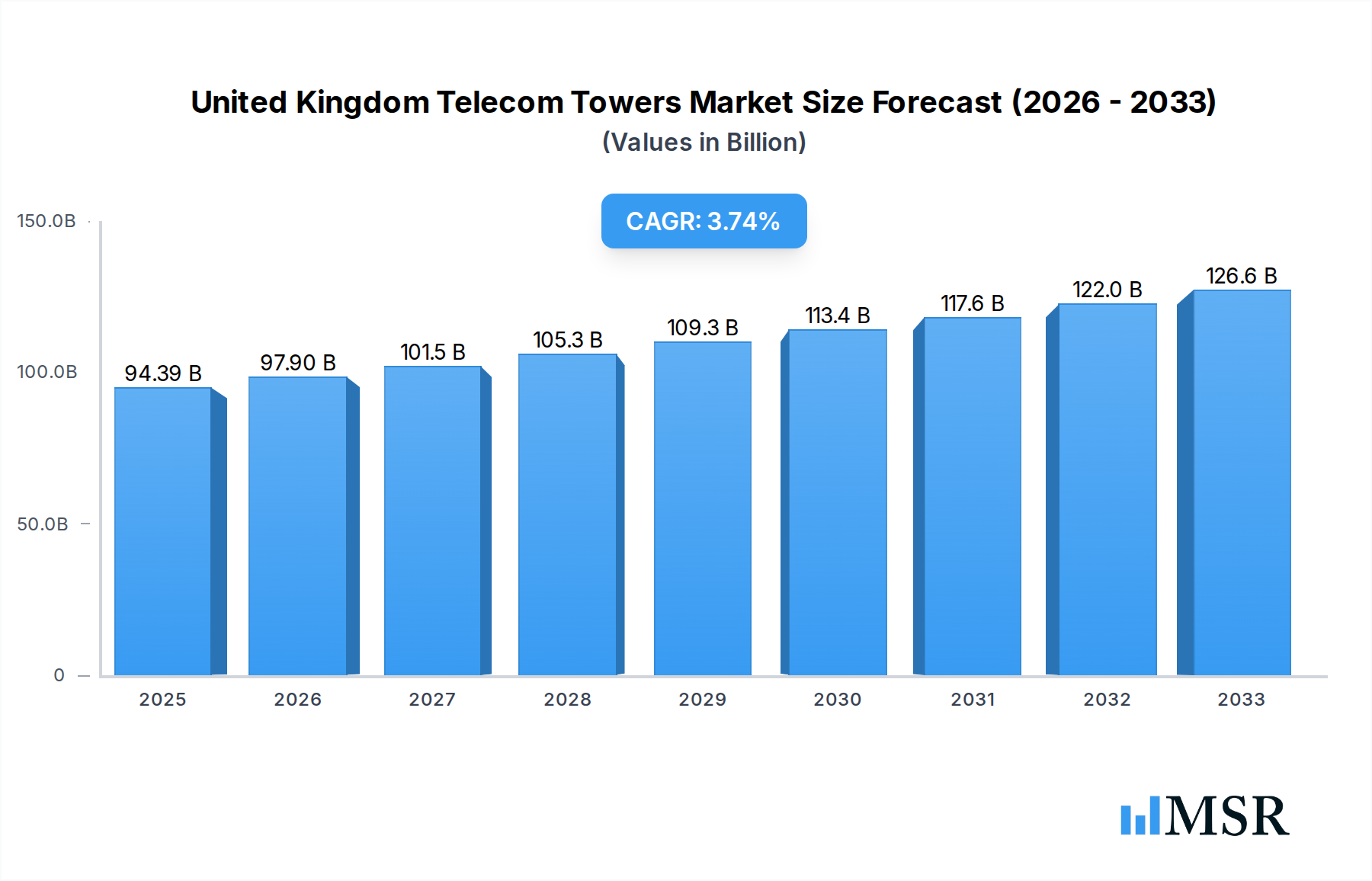

The United Kingdom telecom towers market is poised for significant expansion, projected to reach an estimated USD 94.39 billion by 2025, with a robust Compound Annual Growth Rate (CAGR) of 3.7% anticipated between 2025 and 2033. This growth is primarily fueled by the relentless demand for enhanced mobile broadband, the ongoing rollout of 5G networks, and the increasing densification of infrastructure to support data-intensive applications. Key drivers include the need for expanded network coverage, improved data speeds, and the growing adoption of IoT devices, all of which necessitate a greater number of strategically located and advanced telecom towers. Furthermore, the ongoing investment in upgrading existing infrastructure and the development of new sites to accommodate evolving technologies like 5G standalone and future wireless generations will continue to underpin market expansion. The market's dynamic nature is further shaped by evolving ownership models and diverse installation methods, reflecting the industry's adaptability to technological advancements and evolving deployment strategies.

United Kingdom Telecom Towers Market Market Size (In Billion)

The market's trajectory is also influenced by a dynamic interplay of trends and restraints. Major trends include the rise of shared infrastructure models, which promote cost-efficiency and faster deployment, and the increasing adoption of renewable energy sources for powering tower sites, aligning with sustainability goals. Innovations in tower design and construction, along with the integration of small cells and edge computing capabilities directly at tower locations, are also shaping the future landscape. However, challenges such as high capital expenditure for new deployments, complex regulatory frameworks, and potential site acquisition difficulties can act as restraints. Despite these hurdles, the United Kingdom's commitment to digital transformation and its position as a leading market for telecommunications innovation suggest a strong and sustained growth path for its telecom towers sector. The segmentation analysis reveals a significant market share within operator-owned and private-owned structures, with a growing emphasis on rooftop and ground-based installations, increasingly powered by renewable energy.

United Kingdom Telecom Towers Market Company Market Share

Unlock the future of UK connectivity with our comprehensive analysis of the United Kingdom Telecom Towers Market. This in-depth report offers critical insights into the evolving landscape of mobile infrastructure, driven by 5G deployment, private network expansion, and strategic M&A activities. Essential for MNOs, tower companies, investors, and technology providers seeking to capitalize on this dynamic sector.

Study Period: 2019–2033 | Base Year: 2025 | Estimated Year: 2025 | Forecast Period: 2025–2033 | Historical Period: 2019–2024

United Kingdom Telecom Towers Market Market Concentration & Dynamics

The United Kingdom telecom towers market is characterized by moderate to high concentration, with a few dominant players controlling a significant share of the infrastructure. Key companies like BT Group, Vodafone UK, Cellnex UK Ltd, and Crown Castle UK Limited are actively shaping the competitive landscape through strategic investments and infrastructure sharing agreements. The innovation ecosystem is robust, fueled by the relentless drive towards 5G and emerging technologies like private networks. Regulatory frameworks, overseen by Ofcom, play a crucial role in ensuring fair competition and facilitating infrastructure deployment, though evolving policies can present both opportunities and challenges. Substitute products are limited, with fiber optic backhaul and small cells offering complementary solutions rather than direct replacements for macro tower infrastructure. End-user trends indicate a growing demand for higher bandwidth, lower latency, and ubiquitous connectivity, primarily driven by consumers, enterprises, and the public sector. Mergers and acquisitions (M&A) activity has been a significant theme, with tower companies consolidating their portfolios and MNOs divesting non-core assets to focus on network operations and service provision. For instance, the ongoing expansion of networks by operators and the increasing demand for colocation services contribute to an estimated XX billion in M&A deal values over the historical period.

- Market Share Dynamics: Dominated by a handful of key players, with significant activity in infrastructure acquisition and divestiture.

- Innovation Focus: 5G rollout, edge computing integration, and development of private mobile networks.

- Regulatory Environment: Ofcom's oversight aims to promote competition and infrastructure sharing.

- Substitute Solutions: Primarily fiber backhaul and small cell deployments for specific use cases.

- End-User Demand: High demand for enhanced mobile broadband, IoT, and enterprise connectivity.

- M&A Trends: Consolidation among tower companies and strategic partnerships between operators and infrastructure providers.

United Kingdom Telecom Towers Market Industry Insights & Trends

The United Kingdom telecom towers market is poised for substantial growth, projected to reach an estimated value of GBP XX billion by 2033. This expansion is primarily fueled by the ongoing and accelerated deployment of 5G networks across the nation. The demand for enhanced mobile broadband (eMBB), ultra-reliable low-latency communications (URLLC), and massive machine-type communications (mMTC) necessitates a denser and more robust tower infrastructure. Operators are investing heavily in upgrading existing sites and building new towers to accommodate the increasing number of antennas and radio equipment required for 5G. The compound annual growth rate (CAGR) is estimated at XX% during the forecast period (2025–2033), reflecting this sustained investment.

Technological disruptions are at the forefront of market evolution. The integration of edge computing capabilities directly at tower sites is becoming increasingly critical to reduce latency and enable real-time data processing for applications such as autonomous vehicles, smart cities, and industrial automation. Furthermore, the burgeoning market for private mobile networks, particularly 5G private networks for enterprises, presents a significant growth avenue. Companies are recognizing the benefits of dedicated, high-performance wireless networks for their operations, leading to increased demand for custom-built tower solutions and colocation services. This trend is exemplified by the partnership between Virgin Media O2 and Accenture, aimed at capitalizing on the projected GBP 528 million (USD 673.41 million) market for UK mobile private networks by 2030, further driving the need for localized tower infrastructure.

Evolving consumer behaviors are also playing a pivotal role. The proliferation of data-intensive applications, mobile gaming, augmented reality (AR), and virtual reality (VR) experiences is placing unprecedented demand on mobile networks. This surge in data consumption necessitates a densification of infrastructure, with more tower sites required to provide seamless coverage and capacity. The shift towards remote and hybrid working models further amplifies the need for reliable and high-speed mobile connectivity, extending beyond traditional urban centers. The increasing adoption of IoT devices across various sectors, from smart homes to industrial IoT, also contributes to this demand, as each device requires a connection point, often facilitated by tower-based infrastructure. The strategic focus on expanding and fortifying partnerships, such as the July 2024 agreement between Cellnex UK and Vodafone and Virgin Media O2 for tower infrastructure, underscores the industry's commitment to meeting these evolving connectivity demands and ensuring network stability.

Key Markets & Segments Leading United Kingdom Telecom Towers Market

The United Kingdom telecom towers market is segmented across various ownership models, installation types, and fuel sources, each exhibiting distinct growth trajectories and contributing to the overall market expansion.

Ownership Segments

- Operator-owned: Historically dominant, these towers are owned and operated by mobile network operators (MNOs) themselves. While still significant, the trend is shifting towards divestment and colocation to unlock capital and focus on core services.

- Private-owned: Tower companies that own and lease tower space to multiple MNOs are increasingly becoming the dominant force. This model promotes efficient infrastructure utilization and facilitates faster deployment of new technologies like 5G.

- MNO Captive Sites: These are sites owned by MNOs but specifically dedicated to their own network needs. They represent a crucial part of the existing infrastructure and are often prime candidates for future colocation or divestment.

Dominance Analysis: The Private-owned segment is projected to lead the market growth in the coming years. This is driven by the significant investment by independent tower companies and the increasing preference of MNOs to utilize shared infrastructure to reduce capital expenditure and accelerate deployment timelines. The economic growth in the UK, coupled with the continuous demand for enhanced mobile connectivity, further fuels the expansion of private tower portfolios.

Installation Segments

- Rooftop: Installation of antennas and equipment on existing building rooftops. This is a cost-effective solution, particularly in dense urban areas where land acquisition is challenging and expensive.

- Ground-based: Traditional tower structures erected on land. These offer greater flexibility in terms of height, capacity, and accessibility, making them essential for widespread rural and urban coverage.

Dominance Analysis: Ground-based towers are expected to remain the predominant installation type, forming the backbone of national mobile networks. Their ability to support higher antenna configurations and accommodate multiple tenants makes them indispensable for robust 5G coverage and future network upgrades. However, rooftop installations will continue to play a vital role in urban densification strategies.

Fuel Type Segments

- Renewable: Powering telecom towers using solar, wind, or other sustainable energy sources. This segment is gaining traction due to increasing environmental consciousness and the potential for long-term cost savings.

- Non-renewable: Traditional reliance on grid power or diesel generators. While currently the most common, this segment is facing pressure from sustainability initiatives and the need for more reliable and resilient power solutions.

Dominance Analysis: While Non-renewable fuel types currently dominate due to established infrastructure, the Renewable segment is set to witness the highest growth rate. This surge is propelled by government initiatives promoting green energy, increasing electricity costs, and the operational resilience benefits offered by renewable power sources, especially in remote locations. The integration of battery storage solutions further enhances the attractiveness of renewable power for telecom towers.

United Kingdom Telecom Towers Market Product Developments

Recent product developments in the United Kingdom telecom towers market are heavily influenced by the advancements in 5G technology and the growing demand for sophisticated connectivity solutions. Tower companies are innovating by integrating advanced features such as integrated power systems, advanced cooling solutions for increased equipment density, and modular designs for rapid deployment and scalability. The development of hybrid power solutions, combining renewable energy sources with efficient battery storage, is a key trend, enhancing operational resilience and reducing carbon footprints. Furthermore, there's a growing emphasis on "smart towers" equipped with sensors and analytics capabilities to monitor performance, predict maintenance needs, and optimize energy consumption, thereby providing significant competitive advantages and enhanced service delivery.

Challenges in the United Kingdom Telecom Towers Market Market

The United Kingdom telecom towers market faces several significant challenges that could impede its growth trajectory. These include:

- Regulatory Hurdles: Complex planning permission processes and local authority regulations can lead to significant delays in new tower deployments and site upgrades, impacting the speed of 5G rollout.

- Supply Chain Constraints: Global supply chain disruptions can affect the availability of critical components and equipment, leading to increased lead times and project cost escalations.

- High Infrastructure Costs: The capital expenditure required for acquiring land, constructing new towers, and upgrading existing sites remains substantial, posing a barrier to entry for smaller players and impacting investment decisions for larger ones.

- Community Opposition: Public perception and potential concerns regarding the aesthetic impact and health implications of telecom towers can lead to local opposition, further complicating deployment efforts.

Forces Driving United Kingdom Telecom Towers Market Growth

Several powerful forces are driving the growth of the United Kingdom telecom towers market. The primary catalyst is the widespread and accelerated deployment of 5G networks, which necessitates a denser and more advanced tower infrastructure to support higher frequencies and greater data capacity. The burgeoning demand for mobile private networks (MPNs), especially among enterprises seeking dedicated and secure wireless solutions for industries like manufacturing, logistics, and healthcare, is another significant growth driver. Government initiatives and targets focused on digital connectivity and bridging the digital divide are also instrumental, encouraging investment in infrastructure expansion, particularly in underserved rural areas. Furthermore, the continuous evolution of digital services, including IoT, AR/VR, and cloud-based applications, is creating an insatiable demand for ubiquitous, high-speed, and low-latency mobile connectivity, directly translating into increased demand for telecom tower services.

Challenges in the United Kingdom Telecom Towers Market Market

Long-term growth in the United Kingdom telecom towers market is being propelled by several key factors. The ongoing evolution towards next-generation mobile technologies, beyond 5G, such as 6G, will require continuous investment in and upgrading of existing tower infrastructure, ensuring a sustained demand for tower services. Strategic partnerships between tower companies, MNOs, and technology providers are fostering innovation and creating new revenue streams, particularly in areas like edge computing integration and specialized enterprise solutions. The increasing focus on sustainability and the adoption of renewable energy sources for powering towers not only addresses environmental concerns but also offers operational cost efficiencies, making them attractive long-term solutions. Moreover, the expanding use cases for IoT devices and the development of smart city initiatives will continue to drive the need for pervasive network coverage, thus stimulating further growth in the telecom tower sector.

Emerging Opportunities in United Kingdom Telecom Towers Market

Emerging opportunities in the United Kingdom telecom towers market are diverse and promising. The rapid growth of the 5G private network market presents a significant avenue for tower companies to offer customized infrastructure solutions to enterprises across various sectors, from industrial automation to smart logistics. The increasing adoption of edge computing at tower sites offers new service possibilities, enabling low-latency applications for smart cities, autonomous vehicles, and real-time data analytics. The continuous demand for enhanced rural connectivity provides opportunities for infrastructure expansion in underserved areas, often supported by government subsidies and digital inclusion initiatives. Furthermore, the development of open RAN (Radio Access Network) architectures could lead to increased vendor diversity and innovation, potentially creating new colocation opportunities and demand for specialized infrastructure. The integration of AI and machine learning for network management and predictive maintenance on tower sites also represents a burgeoning area for value-added services.

Leading Players in the United Kingdom Telecom Towers Market Sector

- Vodafone UK

- BT Group

- Atlas Tower Group

- Cellnex UK Ltd

- Telefonica UK Limited

- Crown Castle UK Limited

- Virgin Media O2

- Wireless Infrastructure Group

- Helios Towers

- Freshwav

Key Milestones in United Kingdom Telecom Towers Market Industry

- July 2024: Cellnex UK signed a long-term agreement with Vodafone and Virgin Media O2, supplying the two MNOs with tower infrastructure and related services. This agreement fortifies and expands the existing partnership, ensuring stability for all parties involved and driving demand for colocation services.

- May 2024: Virgin Media O2 and Accenture partnered to capitalize on the growing mobile private network market in the United Kingdom, projected to hit GBP 528 million (USD 673.41 million) by 2030. Accenture may enhance Virgin Media O2's 5G private network capabilities for UK businesses. Accenture specializes in helping enterprises harness the potential of 5G across various applications, indicating a strong future for enterprise-focused tower infrastructure.

Strategic Outlook for United Kingdom Telecom Towers Market Market

The strategic outlook for the United Kingdom telecom towers market is one of sustained growth and evolution. Key growth accelerators include the continued build-out of 5G networks, with a focus on expanding capacity and coverage to meet increasing data demands. The significant potential in the mobile private network sector, driven by enterprise adoption of dedicated wireless solutions, will present substantial opportunities for tower companies. Furthermore, the integration of edge computing capabilities at tower sites will unlock new revenue streams and cater to the demand for low-latency applications. Strategic investments in renewable energy solutions and enhanced network resilience will be crucial for operational efficiency and sustainability. Partnerships and M&A activities are expected to continue, shaping the competitive landscape and driving infrastructure consolidation. The market is poised to benefit from ongoing technological advancements and the relentless demand for seamless and high-performance connectivity across all sectors of the UK economy.

United Kingdom Telecom Towers Market Segmentation

-

1. Ownership

- 1.1. Operator-owned

- 1.2. Private-owned

- 1.3. MNO Captive Sites

-

2. Installation

- 2.1. Rooftop

- 2.2. Ground-based

-

3. Fuel Type

- 3.1. Renewable

- 3.2. Non-renewable

United Kingdom Telecom Towers Market Segmentation By Geography

- 1. United Kingdom

United Kingdom Telecom Towers Market Regional Market Share

Geographic Coverage of United Kingdom Telecom Towers Market

United Kingdom Telecom Towers Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Ownership

- 5.1.1. Operator-owned

- 5.1.2. Private-owned

- 5.1.3. MNO Captive Sites

- 5.2. Market Analysis, Insights and Forecast - by Installation

- 5.2.1. Rooftop

- 5.2.2. Ground-based

- 5.3. Market Analysis, Insights and Forecast - by Fuel Type

- 5.3.1. Renewable

- 5.3.2. Non-renewable

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United Kingdom

- 5.1. Market Analysis, Insights and Forecast - by Ownership

- 6. United Kingdom Telecom Towers Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Ownership

- 6.1.1. Operator-owned

- 6.1.2. Private-owned

- 6.1.3. MNO Captive Sites

- 6.2. Market Analysis, Insights and Forecast - by Installation

- 6.2.1. Rooftop

- 6.2.2. Ground-based

- 6.3. Market Analysis, Insights and Forecast - by Fuel Type

- 6.3.1. Renewable

- 6.3.2. Non-renewable

- 6.1. Market Analysis, Insights and Forecast - by Ownership

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Vodafone UK

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 BT Group

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Atlas Tower Group

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Cellnex UK Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Telefonica UK Limited

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Crown Castle UK Limited

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Virgin Media O2

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Wireless Infrastructure Group

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Helios Towers

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Freshwav

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Vodafone UK

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: United Kingdom Telecom Towers Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: United Kingdom Telecom Towers Market Share (%) by Company 2025

List of Tables

- Table 1: United Kingdom Telecom Towers Market Revenue billion Forecast, by Ownership 2020 & 2033

- Table 2: United Kingdom Telecom Towers Market Revenue billion Forecast, by Installation 2020 & 2033

- Table 3: United Kingdom Telecom Towers Market Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 4: United Kingdom Telecom Towers Market Revenue billion Forecast, by Region 2020 & 2033

- Table 5: United Kingdom Telecom Towers Market Revenue billion Forecast, by Ownership 2020 & 2033

- Table 6: United Kingdom Telecom Towers Market Revenue billion Forecast, by Installation 2020 & 2033

- Table 7: United Kingdom Telecom Towers Market Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 8: United Kingdom Telecom Towers Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United Kingdom Telecom Towers Market?

The projected CAGR is approximately 3.7%.

2. Which companies are prominent players in the United Kingdom Telecom Towers Market?

Key companies in the market include Vodafone UK, BT Group, Atlas Tower Group, Cellnex UK Ltd, Telefonica UK Limited, Crown Castle UK Limited, Virgin Media O2, Wireless Infrastructure Group, Helios Towers, Freshwav.

3. What are the main segments of the United Kingdom Telecom Towers Market?

The market segments include Ownership, Installation, Fuel Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 94.389 billion as of 2022.

5. What are some drivers contributing to market growth?

Connecting/Improving Connectivity to Rural Areas5.1.2 5G Deployment Acts as a Major Catalyst for Growth in the Cell-tower Leasing Environment.

6. What are the notable trends driving market growth?

5G Deployment Acts as a Major Catalyst for Growth in the Cell-tower Leasing Environment.

7. Are there any restraints impacting market growth?

Connecting/Improving Connectivity to Rural Areas5.1.2 5G Deployment Acts as a Major Catalyst for Growth in the Cell-tower Leasing Environment.

8. Can you provide examples of recent developments in the market?

July 2024: Cellnex UK signed a long-term agreement with Vodafone and Virgin Media O2, supplying the two MNOs with tower infrastructure and related services. This agreement fortifies and expands the existing partnership, ensuring stability for all parties involved.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United Kingdom Telecom Towers Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United Kingdom Telecom Towers Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United Kingdom Telecom Towers Market?

To stay informed about further developments, trends, and reports in the United Kingdom Telecom Towers Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence