Key Insights

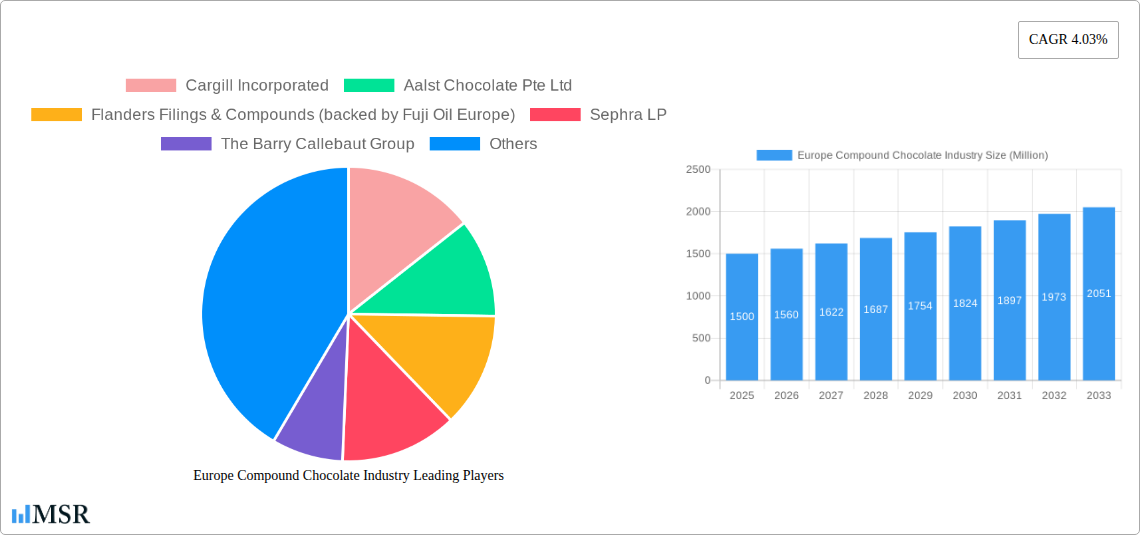

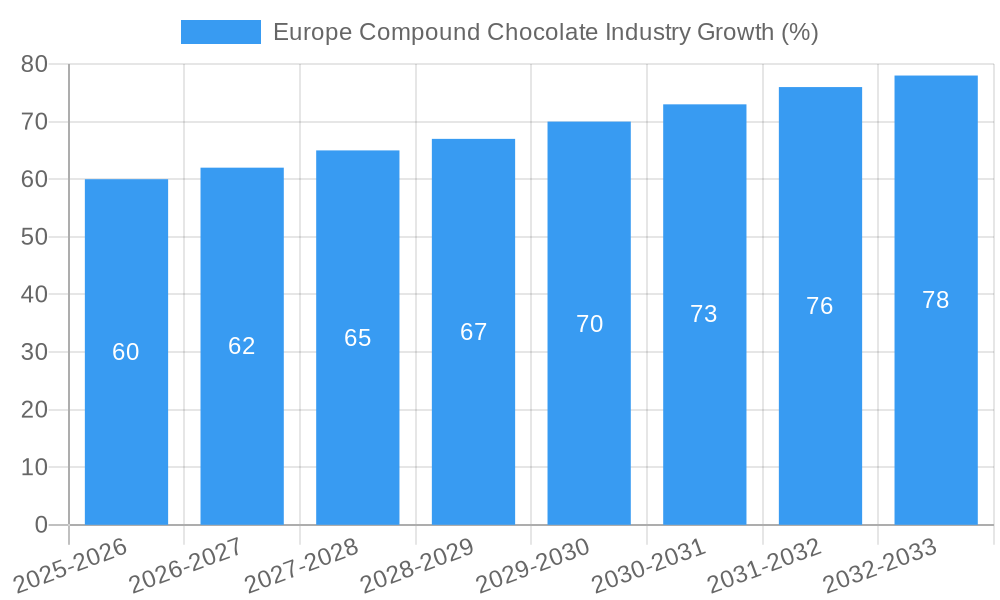

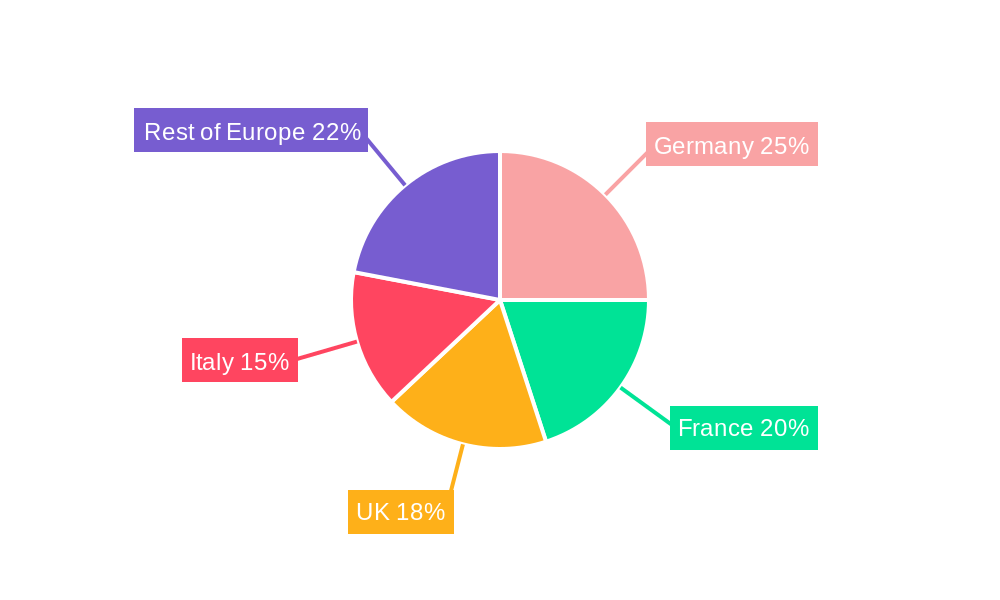

The European compound chocolate market, valued at approximately €1.5 billion in 2025, is projected to experience steady growth, exhibiting a Compound Annual Growth Rate (CAGR) of 4.03% from 2025 to 2033. This growth is driven by several key factors. The increasing demand for convenient and ready-to-use ingredients within the bakery, confectionery, and ice cream sectors fuels the market's expansion. Consumer preferences for premium chocolate experiences and innovative product development in these sectors further stimulate demand. The diverse forms of compound chocolate, including chips, chunks, slabs, and coatings, cater to a wide range of applications, enhancing versatility and driving adoption across various food and beverage categories. Germany, France, the UK, and Italy represent the major market contributors within Europe, reflecting established food manufacturing sectors and strong consumer demand. However, market growth might face some restraints, including fluctuating cocoa prices and increasing competition from other flavoring and coating options. Nonetheless, the continuous innovation in product formulations and the expansion into niche applications, such as specialty beverages and health-conscious confectionery, are expected to offset these challenges and sustain the market's positive trajectory.

The segmentation within the European compound chocolate market reveals significant opportunities. The dark chocolate segment is witnessing robust growth, fueled by health-conscious consumers seeking antioxidants and richer flavors. The milk/white chocolate segment maintains a significant market share due to its widespread appeal and use in various applications. Chocolate chips and drops remain the dominant forms, followed by chocolate slabs and coatings, catering to diverse manufacturing requirements. The bakery sector continues to be a major consumer, closely followed by confectionery and ice cream producers. Leading companies like Cargill, Barry Callebaut, and Puratos are actively investing in research and development to meet evolving consumer preferences and provide tailored solutions for specific market segments. Their global presence and established distribution networks further contribute to the market's stability and growth potential. Future growth will likely be shaped by the increasing adoption of sustainable sourcing practices, evolving consumer preferences for natural and organic ingredients, and the ongoing trend towards personalized and premium chocolate experiences.

Europe Compound Chocolate Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides a detailed analysis of the Europe compound chocolate industry, covering market size, growth drivers, key players, and future trends. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report offers invaluable insights for industry stakeholders, investors, and strategic decision-makers. The report analyzes the market across various segments, including type (dark, milk/white), form (chips/drops/chunks, slabs, coatings, others), and application (bakery, confectionery, ice cream, beverages, cereals, others). The estimated market size in 2025 is xx Million, with a projected Compound Annual Growth Rate (CAGR) of xx% during the forecast period.

Europe Compound Chocolate Industry Market Concentration & Dynamics

The Europe compound chocolate market exhibits a moderately concentrated structure, with several major players commanding significant market share. Key companies such as Cargill Incorporated, The Barry Callebaut Group, Puratos NV, and AAK hold substantial positions. However, the presence of numerous smaller, specialized manufacturers contributes to a dynamic competitive landscape. The market’s innovation ecosystem is robust, driven by continuous product development in areas like sustainable sourcing and healthier formulations. Regulatory frameworks, particularly concerning labeling and ingredient standards, significantly impact industry operations. Substitute products, such as fruit-based spreads and confectionery alternatives, exert moderate pressure. End-user trends towards premiumization and healthier options are shaping product development strategies. Mergers and acquisitions (M&A) activity has been notable, exemplified by Fuji Oil Europe's acquisition of Aalst Chocolate Pte Ltd in 2021, indicating consolidation within the sector. The total M&A deal count between 2019-2024 was xx, indicating a moderate level of consolidation. Market share data for leading players in 2024 is: Barry Callebaut (xx%), Cargill (xx%), Puratos (xx%), AAK (xx%), others (xx%).

Europe Compound Chocolate Industry Industry Insights & Trends

The Europe compound chocolate market witnessed significant growth during the historical period (2019-2024), driven by increasing consumer demand for convenient and versatile chocolate products across various food and beverage applications. The market size reached xx Million in 2024. Technological advancements in processing and formulation are enhancing product quality, shelf life, and customization options. Evolving consumer preferences towards healthier and ethically sourced chocolate are driving demand for products with reduced sugar, higher cocoa content, and sustainable sourcing certifications. The growing popularity of dark chocolate, fueled by its perceived health benefits, further contributes to market growth. The increasing prevalence of online retail channels and e-commerce platforms is transforming distribution dynamics. Emerging trends like personalization and functional chocolate are creating new market niches. The predicted market size for 2025 is xx Million, reflecting a significant increase and demonstrating the continuing expansion of the sector.

Key Markets & Segments Leading Europe Compound Chocolate Industry

The Western European region dominates the Europe compound chocolate market, driven by high chocolate consumption rates and a well-established food processing industry. Germany, France, and the UK are key national markets within this region. The strong economic conditions, robust infrastructure, and mature retail networks in these countries contribute to significant market growth.

- Dominant Segments:

- Type: Milk/white chocolate holds the largest market share, followed by dark chocolate and other types. The growing popularity of dark chocolate, fuelled by health consciousness, is driving its market segment growth.

- Form: Chocolate chips/drops/chunks are the dominant form, driven by their versatility in various applications. Chocolate slabs hold a significant share in the confectionery segment. Chocolate coatings are gaining traction due to their use in diverse applications, such as confectionery and ice cream.

- Application: The bakery and confectionery sectors are the largest consumers of compound chocolate, followed by the ice cream and frozen desserts sector. Beverages and cereals also represent growing application segments.

The dominance of these segments is linked to consumer preferences, established manufacturing infrastructure, and well-established supply chains across these regions. The sustained economic growth of the region plays a crucial role in supporting the continuous growth of this market.

Europe Compound Chocolate Industry Product Developments

Recent product innovations focus on enhancing taste, texture, and functionality. Manufacturers are introducing products with reduced sugar, added fiber, and functional ingredients such as probiotics. Technological advancements in processing techniques are resulting in more sustainable and efficient production methods. These innovations are crucial for maintaining a competitive edge in a market marked by increasing consumer demand for healthier and more ethically sourced products. The development of innovative product forms and applications is constantly evolving, providing new avenues for growth and market penetration within this increasingly dynamic sector.

Challenges in the Europe Compound Chocolate Industry Market

The Europe compound chocolate market faces several challenges, including:

- Fluctuating cocoa prices: These affect profitability and pricing strategies for manufacturers. The impact of these fluctuations is estimated to be around xx Million annually in lost profits for the industry.

- Stringent regulatory requirements: These increase compliance costs and complexity for producers.

- Intense competition: This necessitates continuous product innovation and cost optimization.

- Supply chain disruptions: These impact the availability of raw materials and increase production costs. The estimated impact of these disruptions is approximately xx Million in lost revenue per year.

Forces Driving Europe Compound Chocolate Industry Growth

Key growth drivers include:

- Rising disposable incomes: This increases consumer spending on premium and indulgent food products.

- Growing demand for convenient foods: This drives the popularity of ready-to-use chocolate products.

- Health-conscious consumers: This fuels demand for healthier chocolate options.

- Technological advancements: These improve processing efficiency and product quality.

Long-Term Growth Catalysts in the Europe Compound Chocolate Industry

Long-term growth will be fueled by strategic partnerships, collaborations, and technological advancements. Investments in sustainable cocoa sourcing initiatives, innovative product development (e.g., functional chocolates), and expansion into new market segments will be critical for maintaining long-term growth and market competitiveness. The strategic focus on the expanding health and wellness segment will also drive significant long-term growth.

Emerging Opportunities in Europe Compound Chocolate Industry

Emerging opportunities include:

- Expansion into niche markets: This includes products tailored to specific dietary needs and preferences (e.g., vegan, organic).

- Development of functional chocolates: This incorporates health-enhancing ingredients.

- Focus on sustainable and ethical sourcing: This is a key element for attracting environmentally conscious consumers.

- Growing online sales channels: These offer increased market reach and accessibility.

Leading Players in the Europe Compound Chocolate Industry Sector

- Cargill Incorporated

- Aalst Chocolate Pte Ltd

- Flanders Filings & Compounds (backed by Fuji Oil Europe)

- Sephra LP

- The Barry Callebaut Group

- Puratos NV

- Clasen Quality Chocolate

- AAK

Key Milestones in Europe Compound Chocolate Industry Industry

- 2021: Acquisition of Aalst Chocolate by Fuji Oil Europe, leading to increased market consolidation.

- 2022-2024: Launch of several new dark chocolate products with health claims by leading manufacturers, boosting market innovation and competition.

- Ongoing: Significant investments in sustainable cocoa sourcing initiatives by major industry players, demonstrating a commitment to ethical practices and environmental responsibility.

Strategic Outlook for Europe Compound Chocolate Industry Market

The Europe compound chocolate market is poised for continued growth, driven by strong consumer demand, product innovation, and a focus on sustainability. Strategic opportunities lie in expanding into niche markets, developing value-added products, and enhancing supply chain efficiency. Companies that successfully adapt to evolving consumer preferences and embrace sustainable practices will be best positioned for long-term success in this dynamic market.

Europe Compound Chocolate Industry Segmentation

-

1. Type

- 1.1. Dark

- 1.2. Milk/White

-

2. Form

- 2.1. Chocolate Chips/Drops/Chunks

- 2.2. Chocolate Slab

- 2.3. Chocolate Coatings

- 2.4. Other Forms

-

3. Application

- 3.1. Bakery

- 3.2. Confectionery

- 3.3. Ice Cream and Frozen Desserts

- 3.4. Beverages

- 3.5. Cereals

- 3.6. Other Applications

Europe Compound Chocolate Industry Segmentation By Geography

-

1. Europe

- 1.1. Germany

- 1.2. United Kingdom

- 1.3. France

- 1.4. Russia

- 1.5. Italy

- 1.6. Spain

- 1.7. Rest of Europe

Europe Compound Chocolate Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.03% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Wide Applications and Functionality; Demand For Gluten-Free Products

- 3.3. Market Restrains

- 3.3.1. Easy Availability of Economically Feasible Alternatives

- 3.4. Market Trends

- 3.4.1. Dark Compound Chocolate Becoming the Fastest Growing Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Compound Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Dark

- 5.1.2. Milk/White

- 5.2. Market Analysis, Insights and Forecast - by Form

- 5.2.1. Chocolate Chips/Drops/Chunks

- 5.2.2. Chocolate Slab

- 5.2.3. Chocolate Coatings

- 5.2.4. Other Forms

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Bakery

- 5.3.2. Confectionery

- 5.3.3. Ice Cream and Frozen Desserts

- 5.3.4. Beverages

- 5.3.5. Cereals

- 5.3.6. Other Applications

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Germany Europe Compound Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 7. France Europe Compound Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 8. Italy Europe Compound Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 9. United Kingdom Europe Compound Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 10. Netherlands Europe Compound Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 11. Sweden Europe Compound Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Europe Europe Compound Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Cargill Incorporated

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Aalst Chocolate Pte Ltd

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Flanders Filings & Compounds (backed by Fuji Oil Europe)

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Sephra LP

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 The Barry Callebaut Group

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Puratos NV

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Clasen Quality Chocolate*List Not Exhaustive

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 AAK

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.1 Cargill Incorporated

List of Figures

- Figure 1: Europe Compound Chocolate Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe Compound Chocolate Industry Share (%) by Company 2024

List of Tables

- Table 1: Europe Compound Chocolate Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe Compound Chocolate Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 3: Europe Compound Chocolate Industry Revenue Million Forecast, by Form 2019 & 2032

- Table 4: Europe Compound Chocolate Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 5: Europe Compound Chocolate Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Europe Compound Chocolate Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Germany Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: France Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Italy Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: United Kingdom Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Netherlands Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Sweden Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Rest of Europe Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Europe Compound Chocolate Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 15: Europe Compound Chocolate Industry Revenue Million Forecast, by Form 2019 & 2032

- Table 16: Europe Compound Chocolate Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 17: Europe Compound Chocolate Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: Germany Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: United Kingdom Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: France Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Russia Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Italy Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Spain Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Rest of Europe Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Compound Chocolate Industry?

The projected CAGR is approximately 4.03%.

2. Which companies are prominent players in the Europe Compound Chocolate Industry?

Key companies in the market include Cargill Incorporated, Aalst Chocolate Pte Ltd, Flanders Filings & Compounds (backed by Fuji Oil Europe), Sephra LP, The Barry Callebaut Group, Puratos NV, Clasen Quality Chocolate*List Not Exhaustive, AAK.

3. What are the main segments of the Europe Compound Chocolate Industry?

The market segments include Type, Form, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Wide Applications and Functionality; Demand For Gluten-Free Products.

6. What are the notable trends driving market growth?

Dark Compound Chocolate Becoming the Fastest Growing Market.

7. Are there any restraints impacting market growth?

Easy Availability of Economically Feasible Alternatives.

8. Can you provide examples of recent developments in the market?

1. Acquisition of Aalst Chocolate by Fuji Oil Europe in 2021 2. Launch of new dark chocolate products with health claims by leading manufacturers 3. Investment in sustainable cocoa sourcing initiatives by industry players

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Compound Chocolate Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Compound Chocolate Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Compound Chocolate Industry?

To stay informed about further developments, trends, and reports in the Europe Compound Chocolate Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence