Key Insights

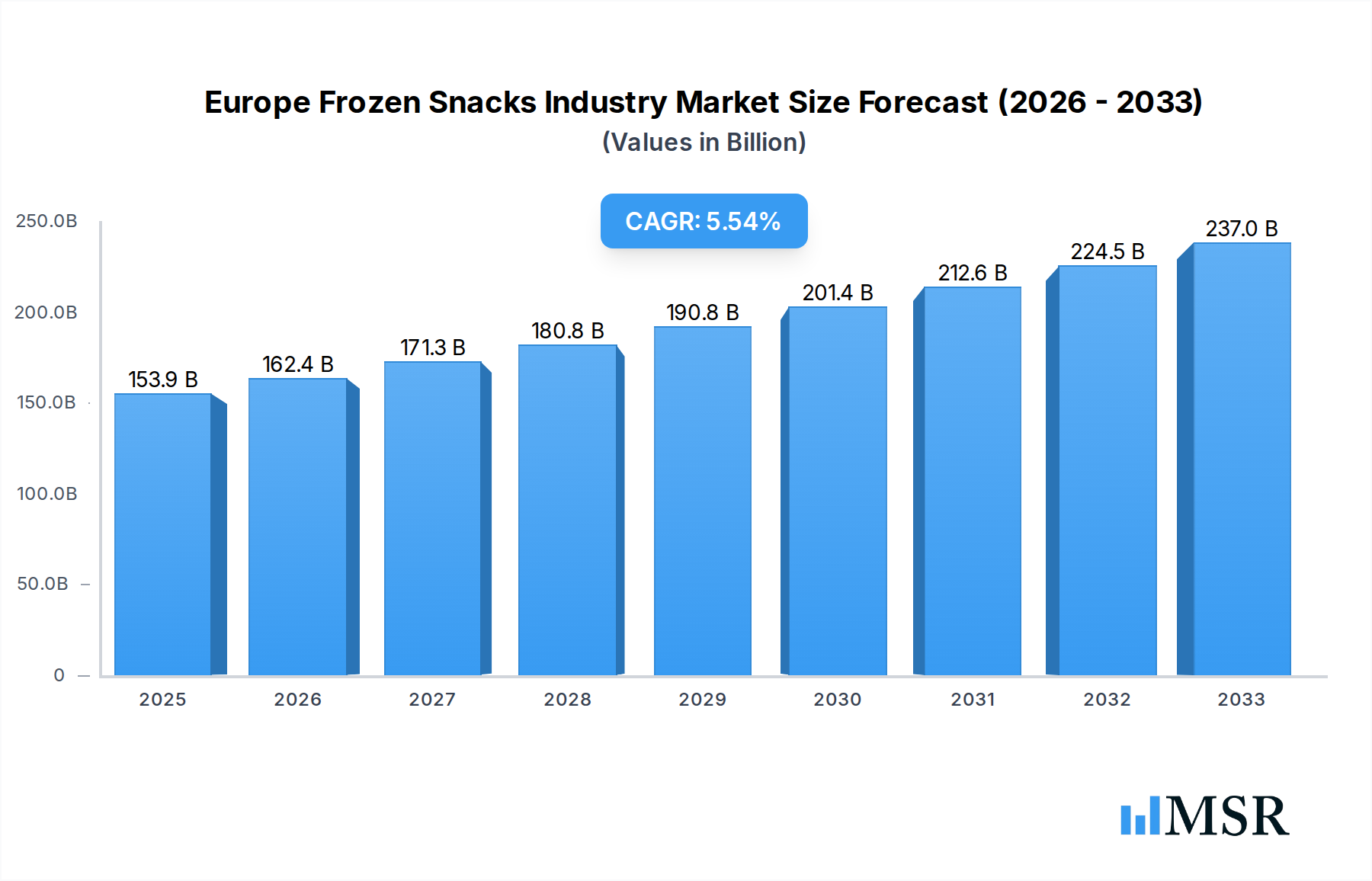

The European Frozen Snacks market is poised for significant expansion, with an estimated market size of $153.91 billion in 2025. This growth is propelled by a robust CAGR of 5.5%, indicating a sustained upward trajectory throughout the forecast period of 2025-2033. Key drivers fueling this expansion include evolving consumer lifestyles, a greater demand for convenient and quick meal solutions, and increasing disposable incomes across the region. The rising popularity of home entertainment and snacking occasions further bolsters the demand for readily available frozen snack options. Manufacturers are increasingly innovating with diverse product offerings, incorporating healthier ingredients and catering to specific dietary preferences, which are also contributing to market vitality.

Europe Frozen Snacks Industry Market Size (In Billion)

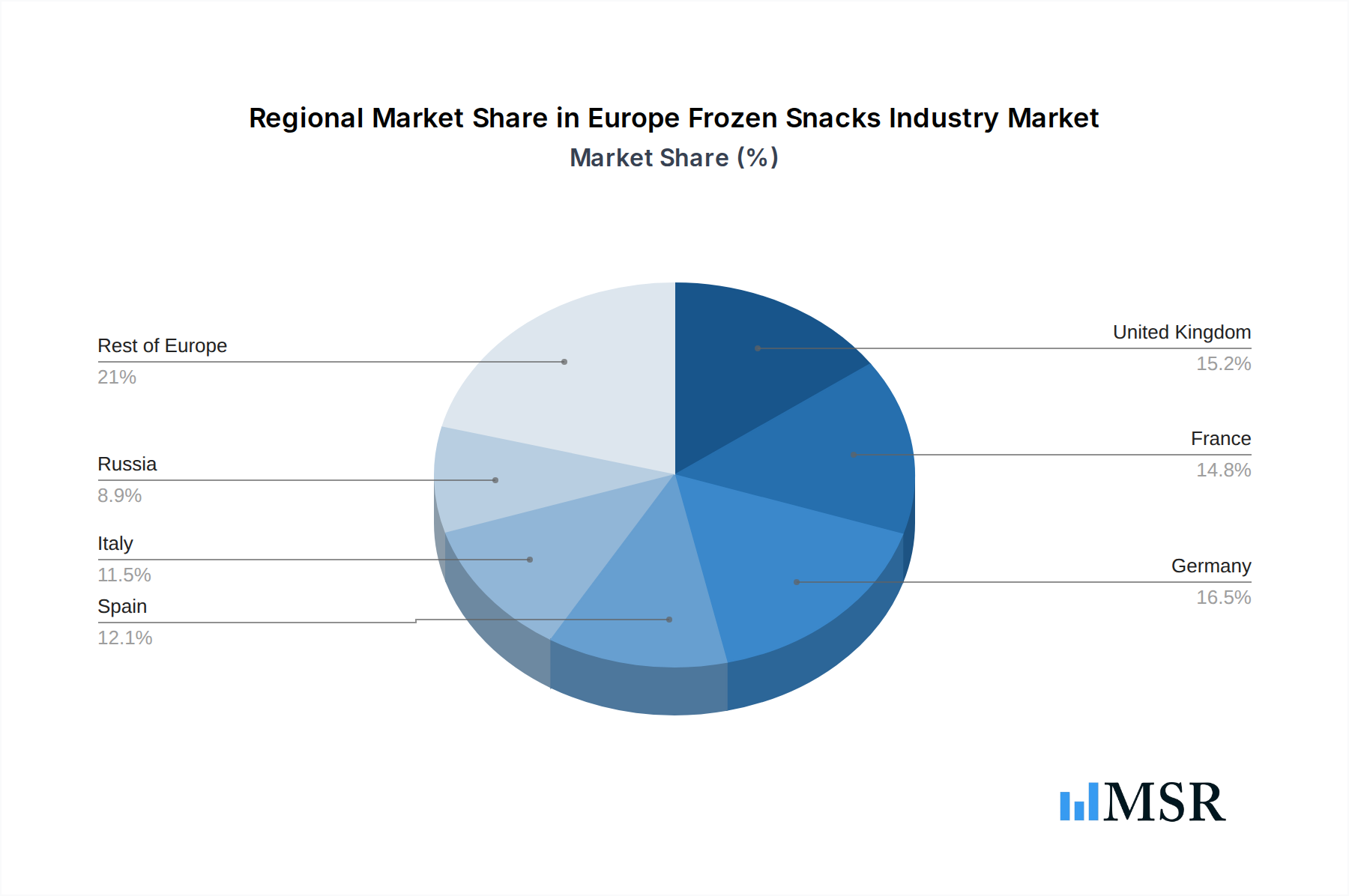

The market's segmentation reveals a dynamic landscape. Fruit-based snacks and potato-based snacks are anticipated to lead the charge, reflecting a growing consumer preference for both indulgent and healthier frozen options. The distribution channel analysis highlights the dominance of hypermarkets and supermarkets, underscoring the importance of widespread retail availability. However, online retail stores are emerging as a critical growth avenue, driven by the convenience of e-commerce and a younger demographic's purchasing habits. While the market benefits from strong demand, potential restraints could emerge from fluctuating raw material costs and increasing competition. Geographically, all European regions, including the United Kingdom, France, Germany, Spain, Italy, and Russia, are expected to contribute to this growth, albeit at varying paces, with "Rest of Europe" also presenting substantial opportunities.

Europe Frozen Snacks Industry Company Market Share

Europe Frozen Snacks Industry: Navigating a Billion-Dollar Market (2019-2033)

This comprehensive report delves into the dynamic Europe Frozen Snacks Industry, forecasting its trajectory from 2019 to 2033. With a base year of 2025 and a forecast period extending to 2033, this study provides unparalleled insights into market dynamics, key trends, and strategic opportunities within this burgeoning sector. Discover the driving forces, emerging challenges, and leading players shaping the multi-billion dollar frozen snacks landscape.

Europe Frozen Snacks Industry Market Concentration & Dynamics

The Europe Frozen Snacks Industry is characterized by a moderate to high level of market concentration, with a few dominant players holding significant market share. Key stakeholders are actively engaged in innovation ecosystems, driven by evolving consumer preferences for convenience and healthier options. Regulatory frameworks, while generally supportive, are increasingly focusing on product labeling, ingredient transparency, and sustainability, impacting product development and market entry strategies. The threat of substitute products, including fresh and chilled snacks, remains a consideration, but the inherent advantages of frozen snacks – longer shelf life, convenience, and consistent quality – continue to drive demand. End-user trends highlight a growing appetite for plant-based, gluten-free, and artisanal frozen snacks, pushing companies to diversify their product portfolios. Mergers and acquisitions (M&A) activities are on the rise as established players seek to expand their market reach, acquire innovative technologies, and consolidate their positions. The M&A deal count is projected to increase by xx% in the forecast period, indicating a strategic consolidation phase within the industry.

Europe Frozen Snacks Industry Industry Insights & Trends

The Europe Frozen Snacks Industry is poised for significant growth, driven by a confluence of factors. The market size is estimated to reach €XX billion by 2025, with a projected Compound Annual Growth Rate (CAGR) of XX% from 2019 to 2033. This robust expansion is fueled by the increasing demand for convenient food solutions among busy European consumers, particularly millennials and Gen Z who prioritize speed and ease in meal preparation. Technological disruptions are playing a pivotal role, with advancements in freezing technologies extending product shelf life and preserving nutritional value, thereby enhancing consumer appeal. Innovations in packaging are also contributing to this growth, with a focus on sustainable and portion-controlled options that align with health-conscious trends. Evolving consumer behaviors are at the forefront of market evolution. There's a discernible shift towards healthier frozen snack options, with a growing preference for products made with natural ingredients, reduced sodium, and lower sugar content. The demand for plant-based and vegan frozen snacks has surged, reflecting a broader dietary shift across Europe. Furthermore, the rise of online retail stores and direct-to-consumer (DTC) models has opened new avenues for market penetration, offering consumers greater accessibility and a wider selection of frozen snack products. The impact of economic factors, such as disposable income and consumer confidence, will continue to influence purchasing decisions, with a sustained demand for affordable yet high-quality frozen snacks.

Key Markets & Segments Leading Europe Frozen Snacks Industry

Dominant Region and Country: Western Europe, particularly Germany, the United Kingdom, and France, continues to be the dominant region for the Europe Frozen Snacks Industry, largely due to higher disposable incomes, established retail infrastructures, and a strong consumer culture embracing convenience foods.

- Economic Growth: Robust economic growth in these key markets translates to increased consumer spending power, directly benefiting the frozen snacks sector.

- Developed Retail Infrastructure: The widespread presence of hypermarkets, supermarkets, and specialized convenience stores ensures easy accessibility for consumers.

- Urbanization: High population density in urban centers drives demand for quick and convenient food options.

Dominant Segment - Type: Potato-based Snacks are currently the leading segment by volume and value, owing to their widespread popularity and versatility. However, Meat- and Seafood-based Snacks and Fruit-based Snacks are exhibiting strong growth potential, driven by health trends and demand for premium offerings.

- Potato-based Snacks:

- Consumer Preference: Long-standing consumer familiarity and preference for products like frozen fries, potato wedges, and hash browns.

- Versatility: Ability to be prepared quickly and served as a side or a standalone snack.

- Innovation: Continuous product development with new flavors, seasonings, and healthier preparation methods.

- Meat- and Seafood-based Snacks:

- Premiumization: Growing demand for premium, protein-rich options like frozen chicken bites, fish sticks, and shrimp snacks.

- Convenience: Offer a quick and easy way to consume protein.

- Health-Conscious Options: Development of baked and air-fried variants to cater to health-conscious consumers.

- Fruit-based Snacks:

- Health and Wellness Trend: Increasing consumer interest in healthier, natural snack alternatives.

- Natural Sweetness: Appeals to consumers seeking to reduce refined sugar intake.

- Versatility in Usage: Used as standalone snacks, smoothie ingredients, or dessert components.

Dominant Segment - Distribution Channel: Hypermarket/Supermarket remains the primary distribution channel, offering a wide selection and competitive pricing. However, Online Retail Stores are rapidly gaining traction, with a projected CAGR of XX% during the forecast period, driven by e-commerce penetration and consumer convenience.

- Hypermarket/Supermarket:

- Extensive Reach: Dominant in terms of store count and geographical coverage across Europe.

- Consumer Habits: Established shopping habits favor these large format stores for grocery purchases.

- Promotional Activities: Frequent in-store promotions and discounts drive sales volume.

- Online Retail Stores:

- Convenience and Accessibility: Facilitates doorstep delivery, appealing to busy lifestyles.

- Wider Product Selection: Online platforms often offer a broader range of niche and specialized frozen snacks.

- Personalized Offers: Data analytics enable targeted promotions and personalized recommendations.

- Convenience Stores:

- Impulse Purchases: Strategically located for quick and impulse buys, particularly for immediate consumption.

- On-the-Go Solutions: Cater to consumers seeking immediate snack solutions.

Europe Frozen Snacks Industry Product Developments

Product development in the Europe Frozen Snacks Industry is witnessing a significant shift towards health, convenience, and sustainability. Companies are heavily investing in creating plant-based alternatives to traditional meat and dairy snacks, catering to the growing vegan and vegetarian populations. Innovations include the introduction of gluten-free frozen snacks, allergen-free options, and products fortified with essential nutrients like protein and fiber. Advanced freezing technologies are being employed to preserve the texture, taste, and nutritional integrity of a wider range of ingredients, including fruits, vegetables, and even more delicate seafood. Packaging solutions are also evolving, with an emphasis on eco-friendly materials, recyclable options, and smart packaging technologies that extend shelf life and provide better product information. The market relevance of these developments is high, as they directly address evolving consumer demands and regulatory pressures, enabling companies to gain a competitive edge and capture new market segments.

Challenges in the Europe Frozen Snacks Industry Market

The Europe Frozen Snacks Industry faces several challenges that could impede growth. High energy costs associated with refrigeration and transportation represent a significant operational expense, impacting profit margins. Complex and varied regulatory landscapes across different European countries concerning food safety, labeling, and ingredient sourcing can create compliance hurdles for manufacturers. Intense competition from both established frozen snack brands and emerging players, as well as the constant threat of substitute fresh and chilled snack alternatives, necessitates continuous innovation and competitive pricing strategies. Furthermore, consumer perception regarding the healthiness of frozen foods remains a persistent challenge, requiring ongoing marketing efforts to highlight nutritional benefits and healthier preparation methods. Supply chain disruptions, exacerbated by geopolitical events and climate change, can also impact the availability and cost of raw materials, further straining the industry.

Forces Driving Europe Frozen Snacks Industry Growth

Several key forces are propelling the growth of the Europe Frozen Snacks Industry. The increasing demand for convenience driven by busy lifestyles and smaller household sizes is a primary catalyst. Technological advancements in freezing, packaging, and logistics are enhancing product quality, extending shelf life, and improving distribution efficiency. Evolving consumer preferences, particularly the growing interest in healthier options, plant-based diets, and artisanal products, are creating new market opportunities. Economic stability and rising disposable incomes in key European markets enable consumers to spend more on premium and convenient food items. Additionally, supportive government initiatives and evolving retail landscapes, including the proliferation of online grocery platforms, are further bolstering market expansion.

Challenges in the Europe Frozen Snacks Industry Market

Long-term growth catalysts in the Europe Frozen Snacks Industry are deeply intertwined with its ability to adapt to evolving consumer demands and technological advancements. Continuous innovation in product development, focusing on healthier formulations, novel ingredients, and diverse flavor profiles, will be crucial. The expansion into emerging markets within Europe that are currently underserved by frozen snack offerings presents significant untapped potential. Strategic partnerships and collaborations between manufacturers, retailers, and technology providers can streamline supply chains, optimize distribution, and foster co-innovation. Embracing sustainability throughout the value chain, from sourcing to packaging, will not only meet consumer expectations but also potentially unlock cost efficiencies. Furthermore, leveraging data analytics to understand consumer behavior and predict market trends will enable companies to proactively tailor their offerings and marketing strategies for sustained growth.

Emerging Opportunities in Europe Frozen Snacks Industry

Emerging opportunities within the Europe Frozen Snacks Industry are abundant and diverse. The burgeoning demand for plant-based frozen snacks presents a substantial growth avenue, with significant potential for innovation in meat and dairy alternatives. The rising popularity of "free-from" products (gluten-free, dairy-free, etc.) caters to a growing segment of health-conscious consumers. The integration of smart technologies in packaging, such as QR codes for product information or temperature indicators, can enhance consumer trust and experience. Expansion into niche markets and specialized retail channels, including health food stores and gourmet delis, offers avenues for premium product differentiation. Furthermore, the increasing adoption of subscription-based models and direct-to-consumer (DTC) sales for frozen snacks provides a direct channel to engage with consumers and build brand loyalty.

Leading Players in the Europe Frozen Snacks Industry Sector

- Young's Seafood Limited

- Dr August Oetker KG

- Sudzucker AG

- Glendale Foods Limited

- Del Monte Foods Inc

- Nomad Foods Limited

- Cooperatie Koninklijke Cosun U A

- McCain Foods Limited

- Hain Celestial Group

Key Milestones in Europe Frozen Snacks Industry Industry

- 2019: Increased consumer adoption of plant-based diets leads to a surge in demand for vegan frozen snacks.

- 2020: The COVID-19 pandemic drives a significant increase in at-home consumption, boosting sales of frozen convenience foods.

- 2021: Growing awareness of sustainability prompts manufacturers to explore eco-friendly packaging solutions.

- 2022: Technological advancements in blast freezing improve the texture and quality of frozen fruits and vegetables.

- 2023: The rise of online grocery platforms accelerates the growth of e-commerce for frozen snack sales.

- 2024: Increased focus on health and wellness leads to the introduction of more low-sodium and high-protein frozen snack options.

- 2025 (Estimated): Continued innovation in personalized nutrition and functional frozen snacks is expected.

- 2026-2033 (Forecast): Anticipated consolidation through M&A activities as larger players seek to expand their portfolios and market share.

Strategic Outlook for Europe Frozen Snacks Industry Market

The strategic outlook for the Europe Frozen Snacks Industry is overwhelmingly positive, driven by continued demand for convenience and evolving consumer preferences. Growth accelerators will center on product innovation, particularly in healthier and plant-based offerings, and expanding distribution channels, with a strong emphasis on online retail. Companies that prioritize sustainability in their sourcing and packaging will gain a competitive advantage. Strategic opportunities lie in exploring new product categories, investing in advanced freezing technologies to maintain quality and extend shelf life, and leveraging data analytics to personalize consumer offerings and marketing efforts. Future success will hinge on the industry's ability to adapt to regulatory changes, mitigate supply chain risks, and effectively communicate the health benefits and convenience of frozen snacks to a discerning European consumer base.

Europe Frozen Snacks Industry Segmentation

-

1. Type

- 1.1. Fruit-based Snacks

- 1.2. Potato-based Snacks

- 1.3. Meat- and Seafood-based Snacks

- 1.4. Others

-

2. Distribution Channel

- 2.1. Hypermarket/Supermarket

- 2.2. Convenience Stores

- 2.3. Online Retail Stores

- 2.4. Other Distribution Channels

Europe Frozen Snacks Industry Segmentation By Geography

- 1. United Kingdom

- 2. France

- 3. Germany

- 4. Spain

- 5. Italy

- 6. Russia

- 7. Rest of Europe

Europe Frozen Snacks Industry Regional Market Share

Geographic Coverage of Europe Frozen Snacks Industry

Europe Frozen Snacks Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Fruit-based Snacks

- 5.1.2. Potato-based Snacks

- 5.1.3. Meat- and Seafood-based Snacks

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Hypermarket/Supermarket

- 5.2.2. Convenience Stores

- 5.2.3. Online Retail Stores

- 5.2.4. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United Kingdom

- 5.3.2. France

- 5.3.3. Germany

- 5.3.4. Spain

- 5.3.5. Italy

- 5.3.6. Russia

- 5.3.7. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Europe Frozen Snacks Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Fruit-based Snacks

- 6.1.2. Potato-based Snacks

- 6.1.3. Meat- and Seafood-based Snacks

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Hypermarket/Supermarket

- 6.2.2. Convenience Stores

- 6.2.3. Online Retail Stores

- 6.2.4. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. United Kingdom Europe Frozen Snacks Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Fruit-based Snacks

- 7.1.2. Potato-based Snacks

- 7.1.3. Meat- and Seafood-based Snacks

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Hypermarket/Supermarket

- 7.2.2. Convenience Stores

- 7.2.3. Online Retail Stores

- 7.2.4. Other Distribution Channels

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. France Europe Frozen Snacks Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Fruit-based Snacks

- 8.1.2. Potato-based Snacks

- 8.1.3. Meat- and Seafood-based Snacks

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Hypermarket/Supermarket

- 8.2.2. Convenience Stores

- 8.2.3. Online Retail Stores

- 8.2.4. Other Distribution Channels

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Germany Europe Frozen Snacks Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Fruit-based Snacks

- 9.1.2. Potato-based Snacks

- 9.1.3. Meat- and Seafood-based Snacks

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Hypermarket/Supermarket

- 9.2.2. Convenience Stores

- 9.2.3. Online Retail Stores

- 9.2.4. Other Distribution Channels

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Spain Europe Frozen Snacks Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Fruit-based Snacks

- 10.1.2. Potato-based Snacks

- 10.1.3. Meat- and Seafood-based Snacks

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. Hypermarket/Supermarket

- 10.2.2. Convenience Stores

- 10.2.3. Online Retail Stores

- 10.2.4. Other Distribution Channels

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Italy Europe Frozen Snacks Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Fruit-based Snacks

- 11.1.2. Potato-based Snacks

- 11.1.3. Meat- and Seafood-based Snacks

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.2.1. Hypermarket/Supermarket

- 11.2.2. Convenience Stores

- 11.2.3. Online Retail Stores

- 11.2.4. Other Distribution Channels

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Russia Europe Frozen Snacks Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Type

- 12.1.1. Fruit-based Snacks

- 12.1.2. Potato-based Snacks

- 12.1.3. Meat- and Seafood-based Snacks

- 12.1.4. Others

- 12.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 12.2.1. Hypermarket/Supermarket

- 12.2.2. Convenience Stores

- 12.2.3. Online Retail Stores

- 12.2.4. Other Distribution Channels

- 12.1. Market Analysis, Insights and Forecast - by Type

- 13. Rest of Europe Europe Frozen Snacks Industry Analysis, Insights and Forecast, 2020-2032

- 13.1. Market Analysis, Insights and Forecast - by Type

- 13.1.1. Fruit-based Snacks

- 13.1.2. Potato-based Snacks

- 13.1.3. Meat- and Seafood-based Snacks

- 13.1.4. Others

- 13.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 13.2.1. Hypermarket/Supermarket

- 13.2.2. Convenience Stores

- 13.2.3. Online Retail Stores

- 13.2.4. Other Distribution Channels

- 13.1. Market Analysis, Insights and Forecast - by Type

- 14. Competitive Analysis

- 14.1. Company Profiles

- 14.1.1 Young's Seafood Limited

- 14.1.1.1. Company Overview

- 14.1.1.2. Products

- 14.1.1.3. Company Financials

- 14.1.1.4. SWOT Analysis

- 14.1.2 Dr August Oetker KG

- 14.1.2.1. Company Overview

- 14.1.2.2. Products

- 14.1.2.3. Company Financials

- 14.1.2.4. SWOT Analysis

- 14.1.3 Sudzucker AG

- 14.1.3.1. Company Overview

- 14.1.3.2. Products

- 14.1.3.3. Company Financials

- 14.1.3.4. SWOT Analysis

- 14.1.4 Glendale Foods Limited

- 14.1.4.1. Company Overview

- 14.1.4.2. Products

- 14.1.4.3. Company Financials

- 14.1.4.4. SWOT Analysis

- 14.1.5 Del Monte Foods Inc*List Not Exhaustive

- 14.1.5.1. Company Overview

- 14.1.5.2. Products

- 14.1.5.3. Company Financials

- 14.1.5.4. SWOT Analysis

- 14.1.6 Nomad Foods Limited

- 14.1.6.1. Company Overview

- 14.1.6.2. Products

- 14.1.6.3. Company Financials

- 14.1.6.4. SWOT Analysis

- 14.1.7 Cooperatie Koninklijke Cosun U A

- 14.1.7.1. Company Overview

- 14.1.7.2. Products

- 14.1.7.3. Company Financials

- 14.1.7.4. SWOT Analysis

- 14.1.8 McCain Foods Limited

- 14.1.8.1. Company Overview

- 14.1.8.2. Products

- 14.1.8.3. Company Financials

- 14.1.8.4. SWOT Analysis

- 14.1.9 Hain Celestial Group

- 14.1.9.1. Company Overview

- 14.1.9.2. Products

- 14.1.9.3. Company Financials

- 14.1.9.4. SWOT Analysis

- 14.1.1 Young's Seafood Limited

- 14.2. Market Entropy

- 14.2.1 Company's Key Areas Served

- 14.2.2 Recent Developments

- 14.3. Company Market Share Analysis 2025

- 14.3.1 Top 5 Companies Market Share Analysis

- 14.3.2 Top 3 Companies Market Share Analysis

- 14.4. List of Potential Customers

- 15. Research Methodology

List of Figures

- Figure 1: Europe Frozen Snacks Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Frozen Snacks Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Frozen Snacks Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Europe Frozen Snacks Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 3: Europe Frozen Snacks Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Europe Frozen Snacks Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Europe Frozen Snacks Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 6: Europe Frozen Snacks Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Europe Frozen Snacks Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 8: Europe Frozen Snacks Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 9: Europe Frozen Snacks Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Europe Frozen Snacks Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 11: Europe Frozen Snacks Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 12: Europe Frozen Snacks Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Europe Frozen Snacks Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 14: Europe Frozen Snacks Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 15: Europe Frozen Snacks Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Europe Frozen Snacks Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 17: Europe Frozen Snacks Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 18: Europe Frozen Snacks Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: Europe Frozen Snacks Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 20: Europe Frozen Snacks Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 21: Europe Frozen Snacks Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 22: Europe Frozen Snacks Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 23: Europe Frozen Snacks Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 24: Europe Frozen Snacks Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Frozen Snacks Industry?

The projected CAGR is approximately 5.5%.

2. Which companies are prominent players in the Europe Frozen Snacks Industry?

Key companies in the market include Young's Seafood Limited, Dr August Oetker KG, Sudzucker AG, Glendale Foods Limited, Del Monte Foods Inc*List Not Exhaustive, Nomad Foods Limited, Cooperatie Koninklijke Cosun U A, McCain Foods Limited, Hain Celestial Group.

3. What are the main segments of the Europe Frozen Snacks Industry?

The market segments include Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 153.91 billion as of 2022.

5. What are some drivers contributing to market growth?

The numerous benefits offered by collagen in the food and beverage industry.

6. What are the notable trends driving market growth?

Potato Snacks Emerged as a Prominent Segment.

7. Are there any restraints impacting market growth?

Increasing vegan population in the region.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Frozen Snacks Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Frozen Snacks Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Frozen Snacks Industry?

To stay informed about further developments, trends, and reports in the Europe Frozen Snacks Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence