Key Insights

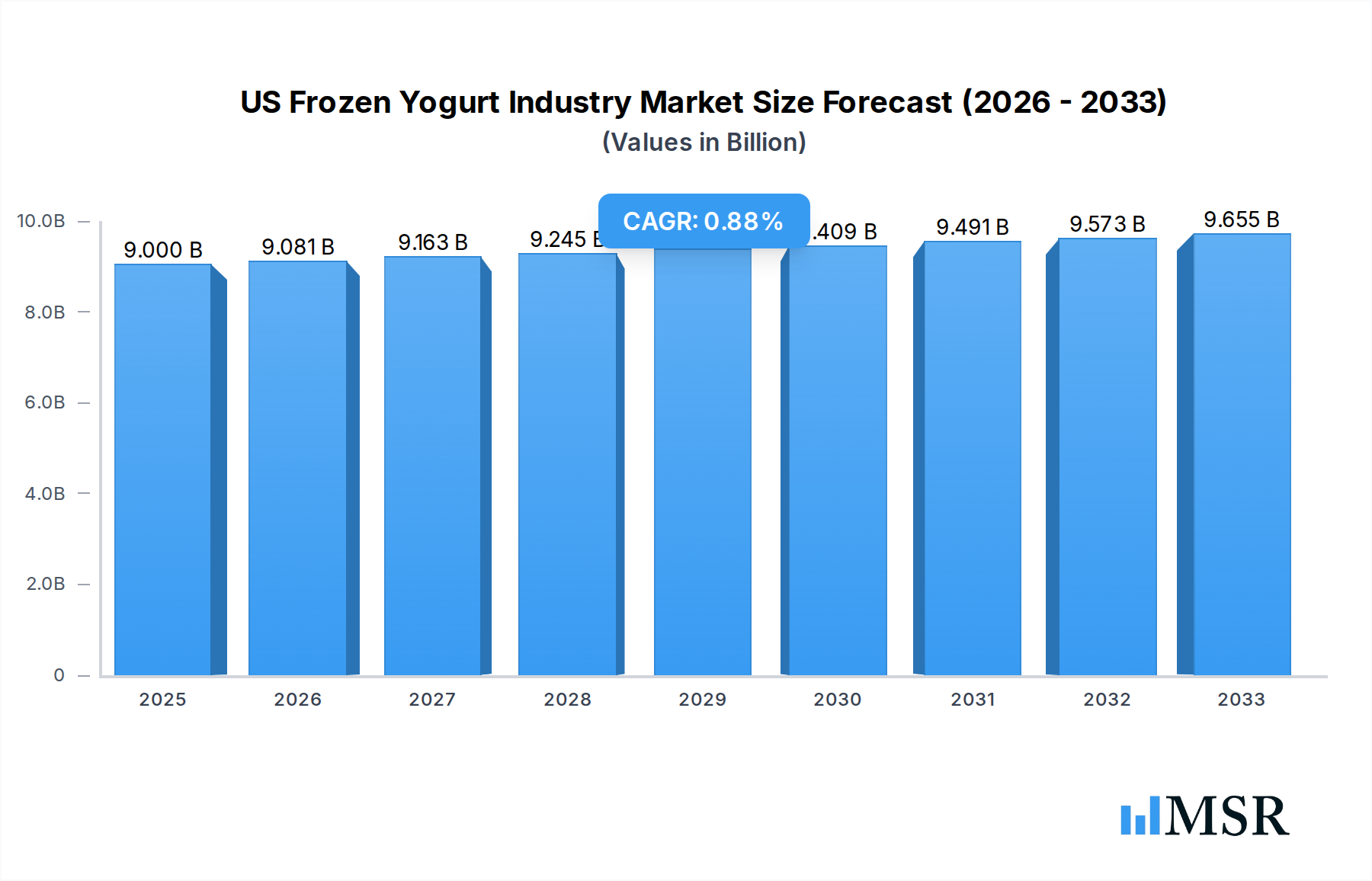

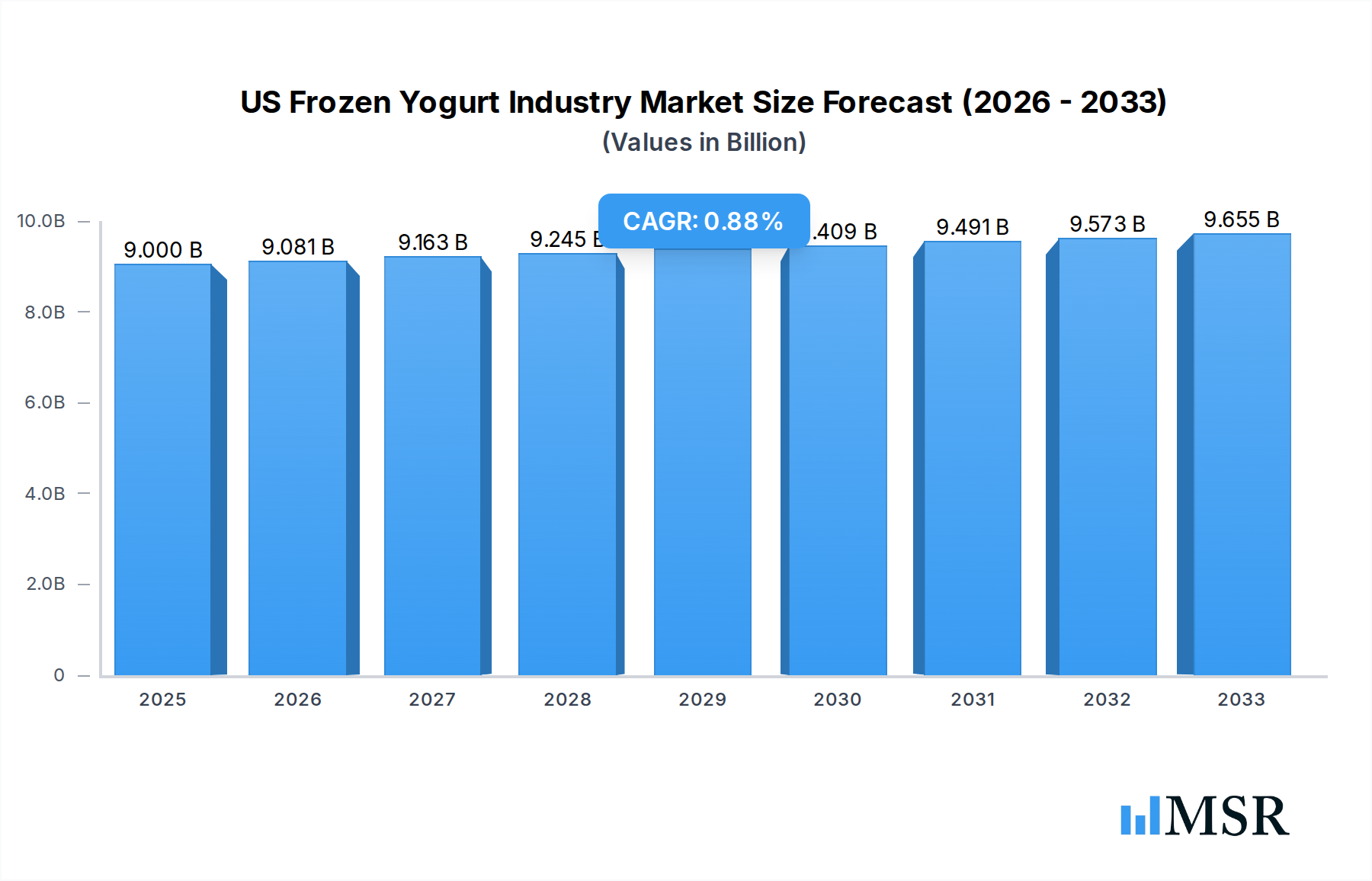

The US Frozen Yogurt industry is poised for steady, albeit modest, growth in the coming years, reflecting a mature market landscape. The market size in 2025 is estimated at $9 billion, with a projected Compound Annual Growth Rate (CAGR) of 0.9% through 2033. This indicates a stable demand driven by established consumer preferences and ongoing innovation within the frozen dessert sector. The primary drivers for this market include the sustained popularity of frozen yogurt as a perceived healthier alternative to traditional ice cream, coupled with continuous product development that introduces new flavors, textures, and dairy-free options. The increasing availability through diverse retail channels, from large supermarkets and hypermarkets to specialized frozen yogurt shops and convenience stores, ensures accessibility for a broad consumer base. Furthermore, the growing trend towards customizable dessert experiences and the incorporation of premium ingredients contribute to sustained consumer interest and spending within this segment.

US Frozen Yogurt Industry Market Size (In Billion)

While the overall growth is moderate, specific segments within the US frozen yogurt market demonstrate stronger potential. The non-dairy frozen yogurt segment, in particular, is experiencing a significant uplift due to the rising health consciousness and the expanding vegan and lactose-intolerant consumer base. This trend is expected to offset some of the slower growth in traditional dairy-based offerings. However, the market faces certain restraints, including intense competition from other frozen dessert categories like premium ice cream and gelato, as well as the increasing popularity of other chilled treats. Price sensitivity among consumers and the operational costs associated with maintaining frozen product freshness throughout the supply chain also pose challenges. Despite these factors, strategic marketing efforts, product differentiation, and an emphasis on health and wellness benefits are likely to sustain the US frozen yogurt market through the forecast period.

US Frozen Yogurt Industry Company Market Share

Unlock the insights into the burgeoning US Frozen Yogurt Industry with this comprehensive report. Spanning a detailed study period from 2019 to 2033, with a base year of 2025, this analysis offers unparalleled depth into market dynamics, consumer behavior, and future growth trajectories. Whether you're a stakeholder, investor, or industry professional, this report provides actionable intelligence to navigate and capitalize on the evolving frozen yogurt landscape.

US Frozen Yogurt Industry Market Concentration & Dynamics

The US Frozen Yogurt Industry is characterized by a moderately concentrated market structure, with a few key players holding significant market share, estimated to be over 70% of the total market value. Major companies like Lactalis, Unilever, General Mills Inc, HP Hood LLC, Danone SA, Dairy Farmers of America Inc, Wells Enterprises, and Prairie Farms Dairy Inc are at the forefront of innovation and distribution. The innovation ecosystem is driven by a continuous demand for healthier alternatives and novel flavor profiles. Regulatory frameworks, primarily focusing on food safety and labeling standards, are well-established, influencing product development and market entry. Substitute products, such as ice cream, gelato, and sorbet, exert competitive pressure, but the perceived health benefits of frozen yogurt offer a distinct advantage. End-user trends showcase a growing preference for plant-based and low-sugar options, directly impacting product formulations and marketing strategies. Mergers and acquisitions (M&A) activity, with an estimated 15-20 significant deals within the historical period, has been a crucial driver of consolidation and market expansion, particularly among smaller, innovative brands seeking to scale.

US Frozen Yogurt Industry Industry Insights & Trends

The US Frozen Yogurt Industry is poised for substantial growth, projected to reach an estimated market size of over $4.5 billion by the forecast year 2025, with a Compound Annual Growth Rate (CAGR) of approximately 6.8% during the forecast period of 2025–2033. This robust expansion is fueled by a confluence of factors, chief among them being the escalating consumer demand for healthier indulgence options. The persistent health and wellness trend has positioned frozen yogurt as a favorable alternative to traditional ice cream, attributed to its lower fat content and perceived probiotic benefits. Technological disruptions are playing an increasingly vital role, with advancements in processing techniques enabling the creation of smoother textures and richer flavors, even in non-dairy formulations. Furthermore, the integration of innovative ingredients, such as natural sweeteners and functional additives like prebiotics and probiotics, is enhancing the appeal of frozen yogurt to health-conscious consumers. Evolving consumer behaviors are also significant drivers. There's a discernible shift towards personalized consumption experiences, leading to a rise in customizable frozen yogurt options, both in retail settings and through at-home consumption kits. The increasing adoption of e-commerce and direct-to-consumer (DTC) models is further expanding market reach and accessibility. The demand for convenience, coupled with the growing popularity of plant-based diets, is propelling the growth of non-dairy frozen yogurt segments. This includes a wider array of bases like almond, oat, coconut, and soy, catering to a broader consumer base with dietary restrictions and ethical considerations. The influence of social media and influencer marketing is also paramount, shaping consumer preferences and driving trial of new products and brands.

Key Markets & Segments Leading US Frozen Yogurt Industry

The US Frozen Yogurt Industry is dominated by the Dairy-based Frozen Yogurt segment, which holds an estimated market share of over 75% in the base year of 2025. This dominance is underpinned by established consumer familiarity and a wide range of existing product formulations and flavor profiles. However, the Non-dairy Frozen Yogurt segment is exhibiting the most rapid growth, driven by the burgeoning plant-based movement and increasing consumer awareness of lactose intolerance and dairy allergies.

Within the application segments, Supermarkets/Hypermarkets represent the largest distribution channel, accounting for an estimated 60% of sales in 2025. This is due to their extensive reach, accessibility, and the ability to offer a wide variety of brands and flavors.

- Drivers for Supermarket/Hypermarket Dominance:

- Convenience: One-stop shopping for groceries and frozen treats.

- Variety: Wide selection catering to diverse consumer preferences.

- Promotional Activities: Frequent discounts and loyalty programs incentivize purchases.

- Brand Visibility: Prime shelf placement for established and new products.

Convenience Stores are the second-largest application segment, capturing approximately 20% of the market share in 2025. Their growth is fueled by impulse purchases and the demand for readily available, single-serving options.

- Drivers for Convenience Store Growth:

- Accessibility: Ubiquitous presence in urban and suburban areas.

- Impulse Purchases: On-the-go consumption occasions.

- Snack Appeal: Convenient and refreshing treat options.

- Expanding Product Offerings: Diversification beyond basic snacks and beverages.

Specialty Stores and Other Distribution Channels, including food service, direct-to-consumer (DTC) online platforms, and specialized dessert parlors, collectively make up the remaining 20% of the market share in 2025. While smaller individually, these channels are crucial for catering to niche markets and fostering brand loyalty through unique experiences and premium offerings. The rise of DTC platforms, in particular, is enabling brands to connect directly with consumers, offering personalized experiences and building stronger brand communities.

US Frozen Yogurt Industry Product Developments

Product innovations in the US Frozen Yogurt Industry are increasingly focused on health-conscious and premium offerings. Developments include the introduction of novel flavor combinations, such as turmeric-ginger or lavender-honey, alongside a surge in plant-based alternatives utilizing ingredients like oat, cashew, and coconut milk. Sugar reduction and the use of natural sweeteners remain key areas of innovation. Furthermore, functional ingredients like probiotics, prebiotics, and added vitamins are being incorporated to enhance the perceived health benefits. The market relevance of these innovations is high, as they directly address evolving consumer preferences for healthier, more diverse, and ingredient-conscious frozen desserts, providing a competitive edge in a dynamic market.

Challenges in the US Frozen Yogurt Industry Market

The US Frozen Yogurt Industry faces several challenges that could impede its growth trajectory. Regulatory hurdles, particularly concerning evolving labeling requirements and potential ingredient restrictions, can increase operational costs and necessitate product reformulation. Supply chain disruptions, including raw material availability and fluctuating commodity prices for dairy and alternative bases, can impact production efficiency and profitability. Intense competitive pressures from established ice cream brands, premium frozen desserts, and rapidly growing non-dairy alternatives also pose a significant restraint. The cost sensitivity of some consumer segments can limit the adoption of premium or niche frozen yogurt products, especially when faced with lower-priced alternatives.

Forces Driving US Frozen Yogurt Industry Growth

Several forces are propelling the growth of the US Frozen Yogurt Industry. The overarching health and wellness trend is a primary driver, with consumers actively seeking perceived healthier alternatives to traditional desserts. Technological advancements in production and ingredient formulation allow for enhanced taste, texture, and nutritional profiles, catering to sophisticated consumer demands. The growing popularity of plant-based diets and the increasing prevalence of lactose intolerance and dairy allergies are significantly boosting the demand for non-dairy frozen yogurt options. Furthermore, evolving consumer preferences for unique flavors, customizable options, and ethically sourced ingredients are creating new market opportunities and driving product innovation.

Challenges in the US Frozen Yogurt Industry Market

Long-term growth catalysts in the US Frozen Yogurt Industry are rooted in continuous innovation and strategic market expansion. The development of novel, high-protein, and low-sugar frozen yogurt varieties will continue to attract health-conscious consumers. Strategic partnerships with food service providers and grocery retailers can expand distribution networks and brand visibility. Furthermore, investments in research and development for sustainable sourcing of ingredients and eco-friendly packaging will resonate with environmentally conscious consumers, fostering long-term brand loyalty and market resilience. Exploring international markets for potential expansion can also contribute to sustained global growth.

Emerging Opportunities in US Frozen Yogurt Industry

Emerging opportunities in the US Frozen Yogurt Industry lie in several key areas. The continued expansion of the non-dairy segment, with innovative bases and allergen-free formulations, presents a substantial growth avenue. The demand for premium and gourmet frozen yogurt, featuring unique flavor profiles and high-quality ingredients, caters to a discerning consumer base willing to pay a premium. Direct-to-consumer (DTC) models and subscription box services offer innovative ways to reach consumers directly and foster brand loyalty. Furthermore, the integration of functional ingredients, such as adaptogens and cognitive enhancers, could tap into the growing wellness and functional food markets.

Leading Players in the US Frozen Yogurt Industry Sector

- Lactalis

- Unilever

- General Mills Inc

- HP Hood LLC

- Danone SA

- Dairy Farmers of America Inc

- Wells Enterprises

- Prairie Farms Dairy Inc

Key Milestones in US Frozen Yogurt Industry Industry

- 2019: Increased focus on probiotic-enriched frozen yogurt products.

- 2020: Significant surge in demand for at-home frozen yogurt consumption kits.

- 2021: Expansion of non-dairy frozen yogurt options across major retailers.

- 2022: Introduction of innovative, low-sugar and natural sweetener-based products.

- 2023: Growth in M&A activity with smaller, specialized frozen yogurt brands being acquired.

- 2024: Enhanced focus on sustainable sourcing and eco-friendly packaging.

Strategic Outlook for US Frozen Yogurt Industry Market

The strategic outlook for the US Frozen Yogurt Industry is exceptionally positive, driven by sustained consumer demand for healthier indulgence and a dynamic innovation landscape. Growth accelerators will include the continued development and marketing of plant-based and functional frozen yogurt options, catering to evolving dietary trends and wellness preferences. Expanding distribution channels, particularly through e-commerce and DTC platforms, will enhance accessibility and customer engagement. Strategic collaborations with lifestyle influencers and health experts can further bolster brand credibility and market penetration. The industry's ability to adapt to evolving consumer tastes and regulatory environments, while focusing on product quality and sustainability, will be paramount for long-term success.

US Frozen Yogurt Industry Segmentation

-

1. Category

- 1.1. Dairy-based Frozen Yogurt

- 1.2. Non-dairy Frozen Yogurt

-

2. Application

- 2.1. Supermarket/Hypermarkets

- 2.2. Convenience Stores

- 2.3. Specialty Stores

- 2.4. Other Distribution Channels

US Frozen Yogurt Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

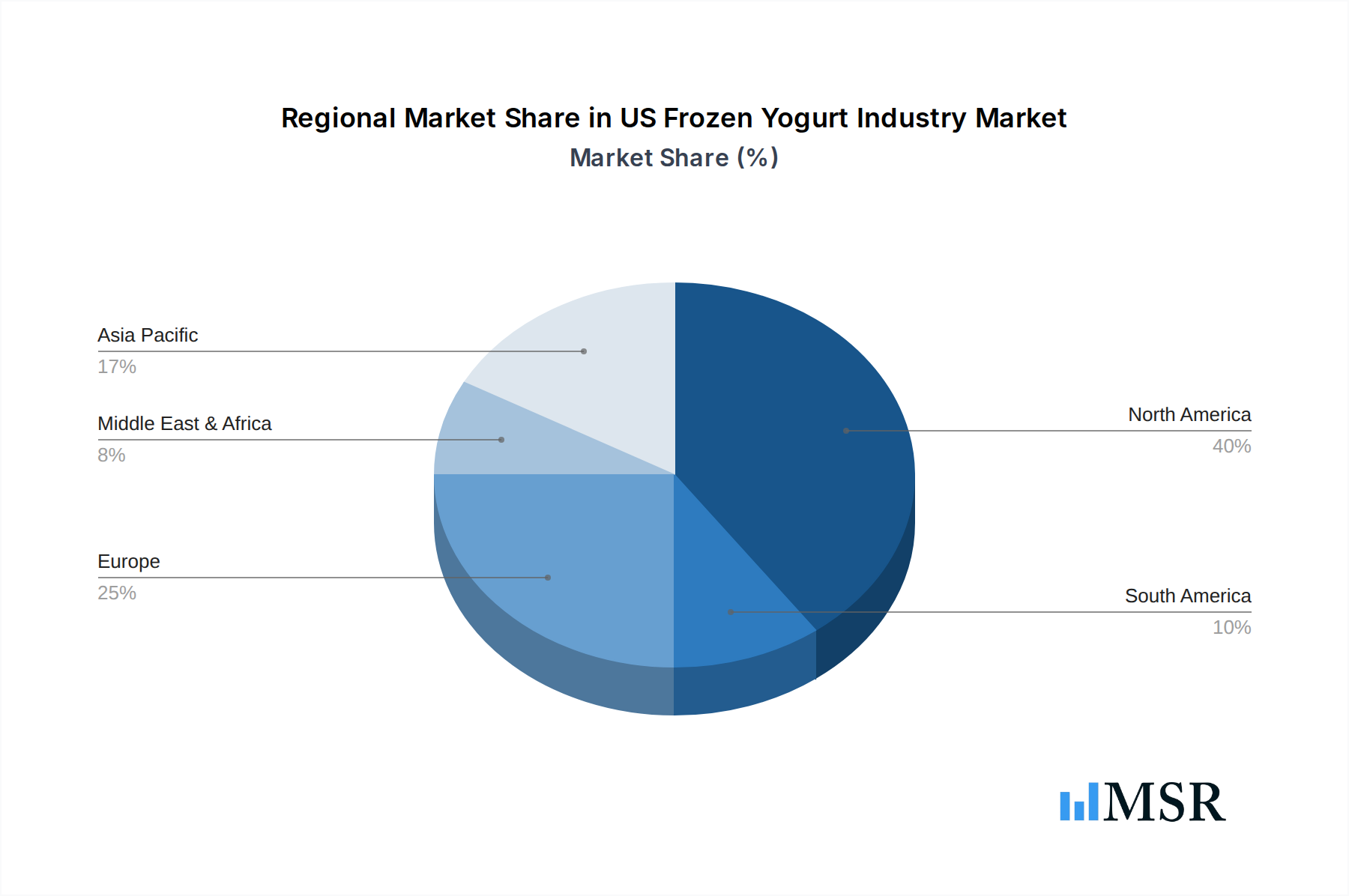

US Frozen Yogurt Industry Regional Market Share

Geographic Coverage of US Frozen Yogurt Industry

US Frozen Yogurt Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 0.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Category

- 5.1.1. Dairy-based Frozen Yogurt

- 5.1.2. Non-dairy Frozen Yogurt

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Supermarket/Hypermarkets

- 5.2.2. Convenience Stores

- 5.2.3. Specialty Stores

- 5.2.4. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Category

- 6. Global US Frozen Yogurt Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Category

- 6.1.1. Dairy-based Frozen Yogurt

- 6.1.2. Non-dairy Frozen Yogurt

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Supermarket/Hypermarkets

- 6.2.2. Convenience Stores

- 6.2.3. Specialty Stores

- 6.2.4. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Category

- 7. North America US Frozen Yogurt Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Category

- 7.1.1. Dairy-based Frozen Yogurt

- 7.1.2. Non-dairy Frozen Yogurt

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Supermarket/Hypermarkets

- 7.2.2. Convenience Stores

- 7.2.3. Specialty Stores

- 7.2.4. Other Distribution Channels

- 7.1. Market Analysis, Insights and Forecast - by Category

- 8. South America US Frozen Yogurt Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Category

- 8.1.1. Dairy-based Frozen Yogurt

- 8.1.2. Non-dairy Frozen Yogurt

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Supermarket/Hypermarkets

- 8.2.2. Convenience Stores

- 8.2.3. Specialty Stores

- 8.2.4. Other Distribution Channels

- 8.1. Market Analysis, Insights and Forecast - by Category

- 9. Europe US Frozen Yogurt Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Category

- 9.1.1. Dairy-based Frozen Yogurt

- 9.1.2. Non-dairy Frozen Yogurt

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Supermarket/Hypermarkets

- 9.2.2. Convenience Stores

- 9.2.3. Specialty Stores

- 9.2.4. Other Distribution Channels

- 9.1. Market Analysis, Insights and Forecast - by Category

- 10. Middle East & Africa US Frozen Yogurt Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Category

- 10.1.1. Dairy-based Frozen Yogurt

- 10.1.2. Non-dairy Frozen Yogurt

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Supermarket/Hypermarkets

- 10.2.2. Convenience Stores

- 10.2.3. Specialty Stores

- 10.2.4. Other Distribution Channels

- 10.1. Market Analysis, Insights and Forecast - by Category

- 11. Asia Pacific US Frozen Yogurt Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Category

- 11.1.1. Dairy-based Frozen Yogurt

- 11.1.2. Non-dairy Frozen Yogurt

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Supermarket/Hypermarkets

- 11.2.2. Convenience Stores

- 11.2.3. Specialty Stores

- 11.2.4. Other Distribution Channels

- 11.1. Market Analysis, Insights and Forecast - by Category

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Lactalis

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Unilever

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 General Mills Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 HP Hood LLC

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Danone SA

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Dairy Farmers of America Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Wells Enterpris

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Prairie Farms Dairy Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.1 Lactalis

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global US Frozen Yogurt Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America US Frozen Yogurt Industry Revenue (billion), by Category 2025 & 2033

- Figure 3: North America US Frozen Yogurt Industry Revenue Share (%), by Category 2025 & 2033

- Figure 4: North America US Frozen Yogurt Industry Revenue (billion), by Application 2025 & 2033

- Figure 5: North America US Frozen Yogurt Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America US Frozen Yogurt Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America US Frozen Yogurt Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America US Frozen Yogurt Industry Revenue (billion), by Category 2025 & 2033

- Figure 9: South America US Frozen Yogurt Industry Revenue Share (%), by Category 2025 & 2033

- Figure 10: South America US Frozen Yogurt Industry Revenue (billion), by Application 2025 & 2033

- Figure 11: South America US Frozen Yogurt Industry Revenue Share (%), by Application 2025 & 2033

- Figure 12: South America US Frozen Yogurt Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: South America US Frozen Yogurt Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe US Frozen Yogurt Industry Revenue (billion), by Category 2025 & 2033

- Figure 15: Europe US Frozen Yogurt Industry Revenue Share (%), by Category 2025 & 2033

- Figure 16: Europe US Frozen Yogurt Industry Revenue (billion), by Application 2025 & 2033

- Figure 17: Europe US Frozen Yogurt Industry Revenue Share (%), by Application 2025 & 2033

- Figure 18: Europe US Frozen Yogurt Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe US Frozen Yogurt Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa US Frozen Yogurt Industry Revenue (billion), by Category 2025 & 2033

- Figure 21: Middle East & Africa US Frozen Yogurt Industry Revenue Share (%), by Category 2025 & 2033

- Figure 22: Middle East & Africa US Frozen Yogurt Industry Revenue (billion), by Application 2025 & 2033

- Figure 23: Middle East & Africa US Frozen Yogurt Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: Middle East & Africa US Frozen Yogurt Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa US Frozen Yogurt Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific US Frozen Yogurt Industry Revenue (billion), by Category 2025 & 2033

- Figure 27: Asia Pacific US Frozen Yogurt Industry Revenue Share (%), by Category 2025 & 2033

- Figure 28: Asia Pacific US Frozen Yogurt Industry Revenue (billion), by Application 2025 & 2033

- Figure 29: Asia Pacific US Frozen Yogurt Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Asia Pacific US Frozen Yogurt Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific US Frozen Yogurt Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global US Frozen Yogurt Industry Revenue billion Forecast, by Category 2020 & 2033

- Table 2: Global US Frozen Yogurt Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Global US Frozen Yogurt Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global US Frozen Yogurt Industry Revenue billion Forecast, by Category 2020 & 2033

- Table 5: Global US Frozen Yogurt Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 6: Global US Frozen Yogurt Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global US Frozen Yogurt Industry Revenue billion Forecast, by Category 2020 & 2033

- Table 11: Global US Frozen Yogurt Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 12: Global US Frozen Yogurt Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global US Frozen Yogurt Industry Revenue billion Forecast, by Category 2020 & 2033

- Table 17: Global US Frozen Yogurt Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 18: Global US Frozen Yogurt Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global US Frozen Yogurt Industry Revenue billion Forecast, by Category 2020 & 2033

- Table 29: Global US Frozen Yogurt Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 30: Global US Frozen Yogurt Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global US Frozen Yogurt Industry Revenue billion Forecast, by Category 2020 & 2033

- Table 38: Global US Frozen Yogurt Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 39: Global US Frozen Yogurt Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific US Frozen Yogurt Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the US Frozen Yogurt Industry?

The projected CAGR is approximately 0.9%.

2. Which companies are prominent players in the US Frozen Yogurt Industry?

Key companies in the market include Lactalis, Unilever, General Mills Inc, HP Hood LLC, Danone SA, Dairy Farmers of America Inc, Wells Enterpris, Prairie Farms Dairy Inc.

3. What are the main segments of the US Frozen Yogurt Industry?

The market segments include Category, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 9 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Health Concerns are Supporting the Market's Growth; Growing Consumer Preference for Convenience Seafood.

6. What are the notable trends driving market growth?

Growing Demand for Non-Dairy Frozen Yogurt.

7. Are there any restraints impacting market growth?

Rising Concern About Quality and Safety Standards of Canned Tuna.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "US Frozen Yogurt Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the US Frozen Yogurt Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the US Frozen Yogurt Industry?

To stay informed about further developments, trends, and reports in the US Frozen Yogurt Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence