Key Insights

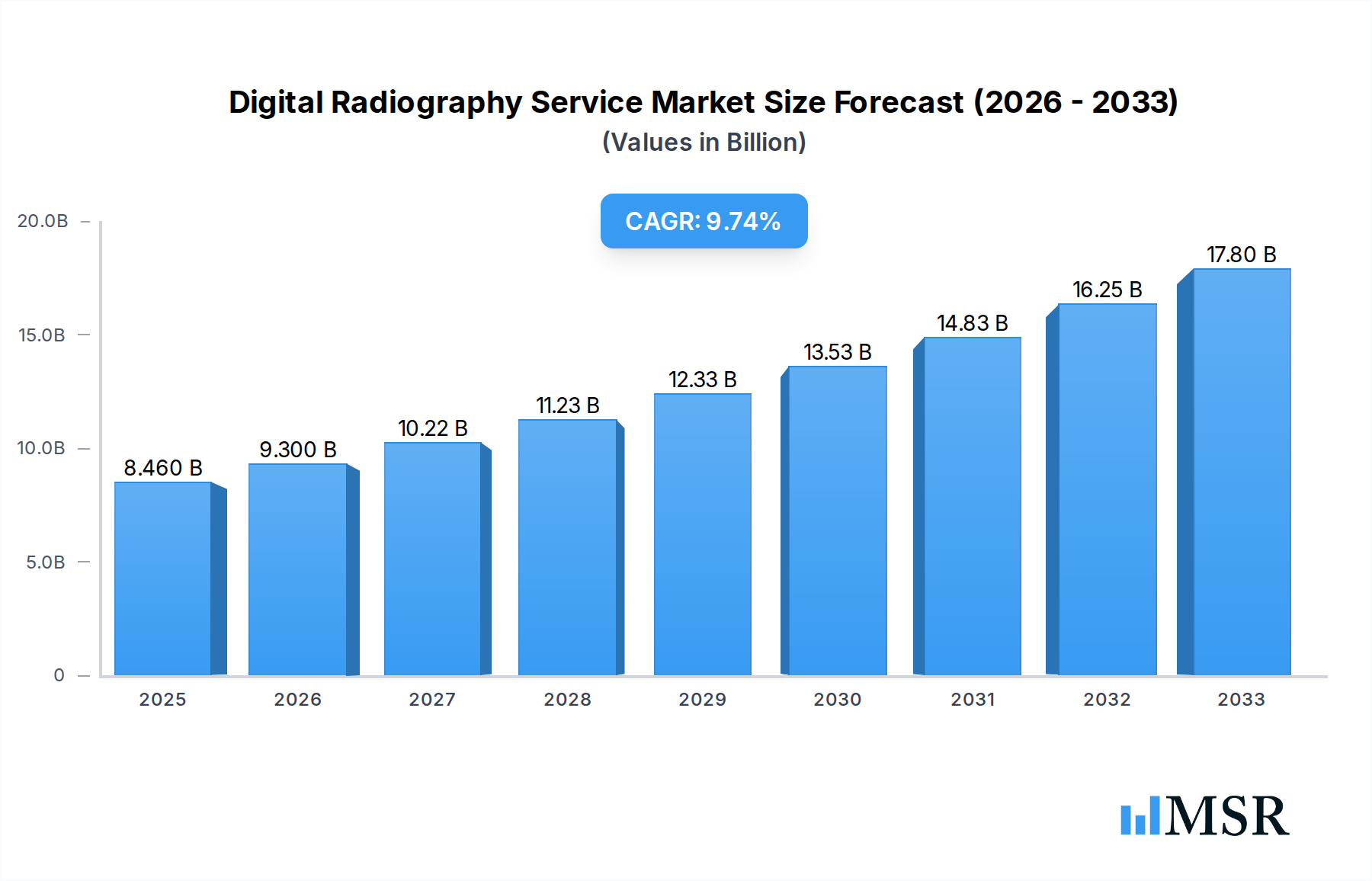

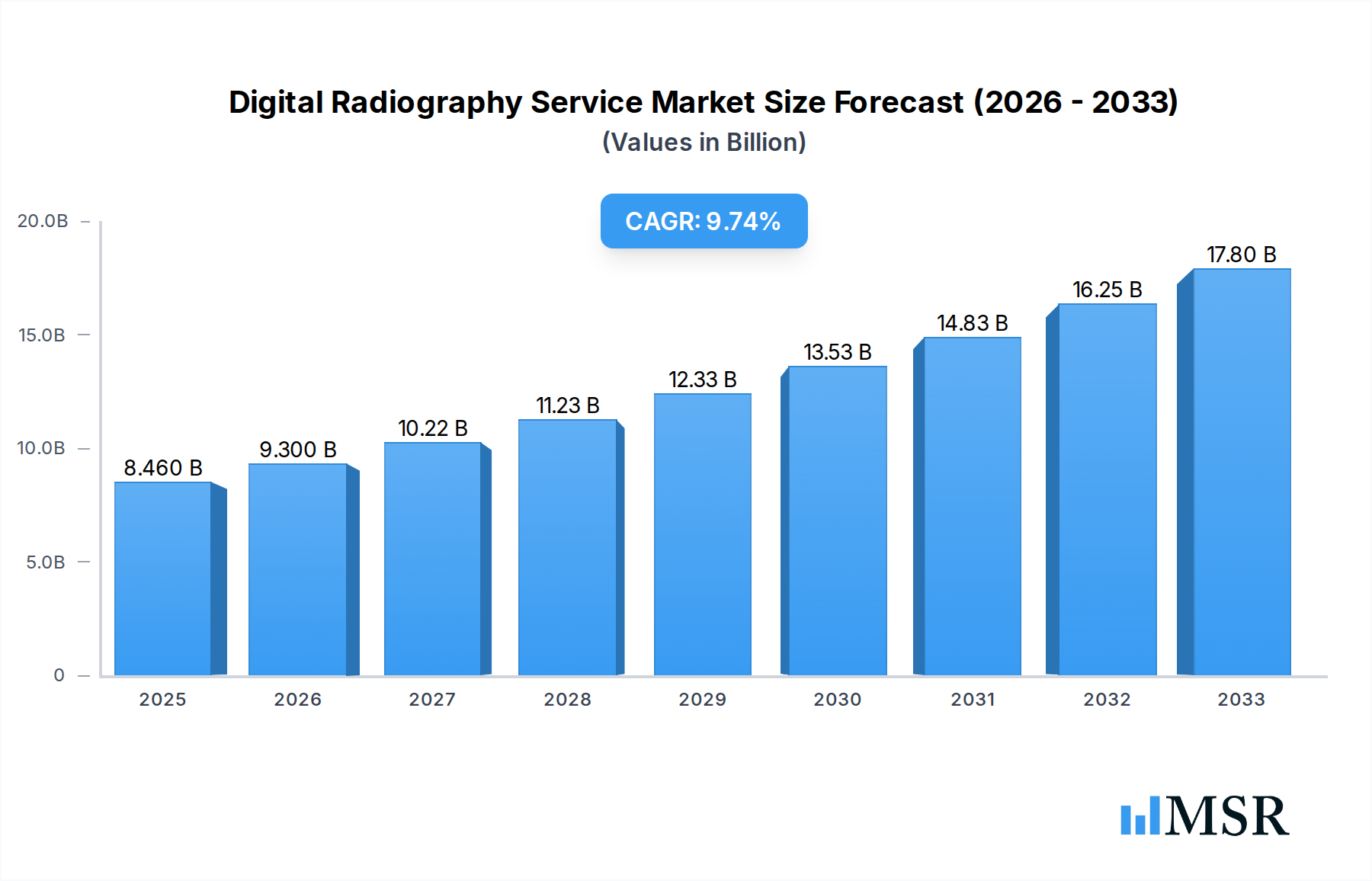

The Digital Radiography Service market is poised for significant expansion, projected to reach an estimated $8.46 billion in 2025, driven by a robust Compound Annual Growth Rate (CAGR) of 9.9% through 2033. This growth is underpinned by a confluence of factors, including the increasing demand for advanced diagnostic imaging solutions across critical sectors such as aerospace, electronics, and medical equipment. The inherent advantages of digital radiography, such as enhanced image quality, faster processing times, and reduced radiation exposure compared to traditional film-based methods, are fueling its adoption. Furthermore, the evolving regulatory landscape and a growing emphasis on preventative healthcare are compelling industries to invest in sophisticated inspection and diagnostic technologies, further accelerating market penetration. The rising sophistication of manufacturing processes also necessitates precise, non-destructive testing capabilities, a role well-fulfilled by digital radiography services.

Digital Radiography Service Market Size (In Billion)

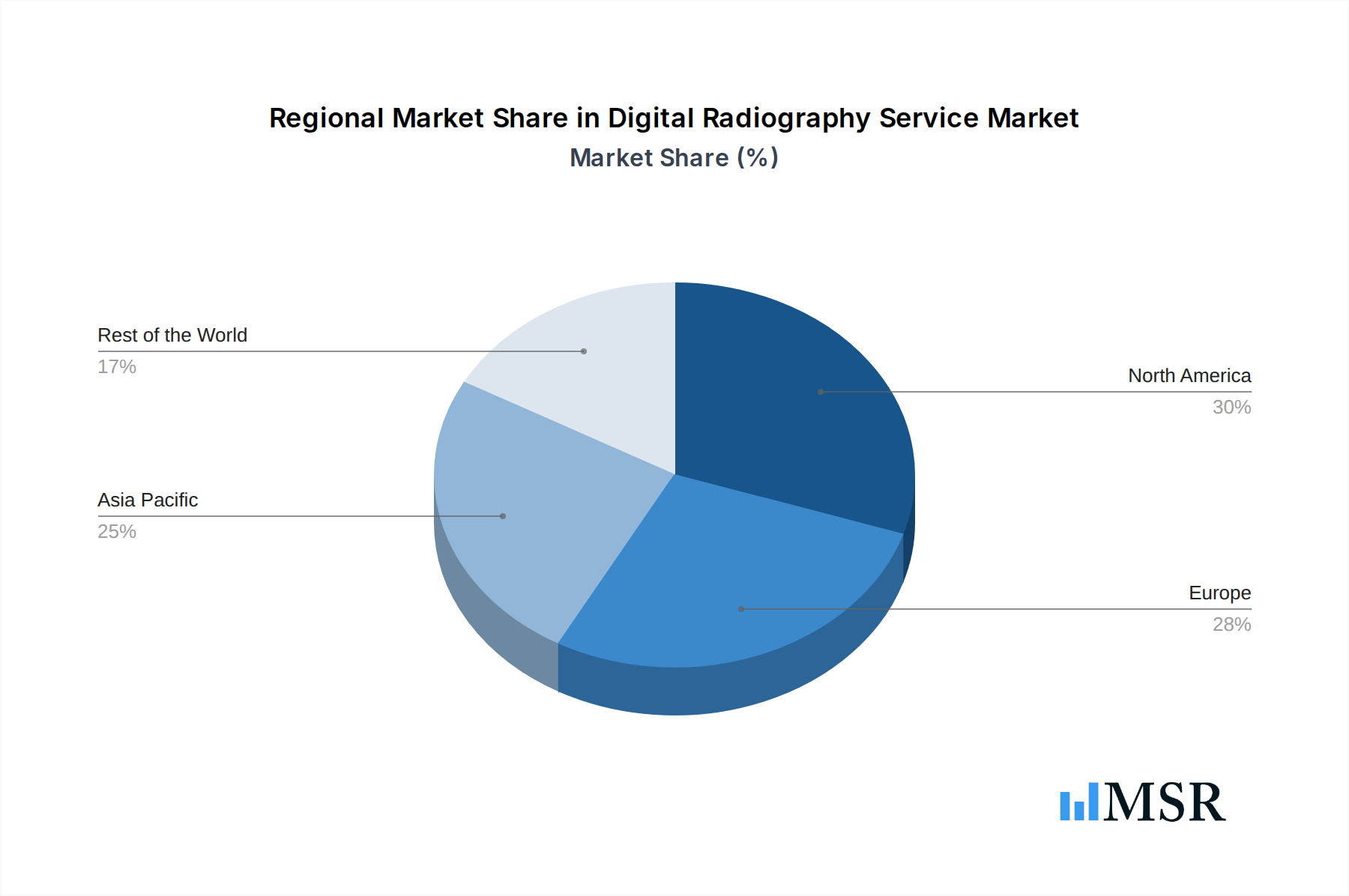

The market's expansion is further propelled by technological advancements and the expanding service offerings. Key trends include the integration of artificial intelligence (AI) and machine learning (ML) for improved image analysis and anomaly detection, as well as the increasing utilization of cloud-based platforms for data storage and accessibility. The market is bifurcated into Mechanical Internal Service and Mechanical External Service, with both segments expected to witness steady growth. Geographically, North America and Europe are anticipated to remain dominant regions, owing to their established healthcare infrastructure and strong research and development capabilities. However, the Asia Pacific region, particularly China and India, is emerging as a high-growth market due to rapid industrialization, increasing healthcare expenditure, and a burgeoning demand for advanced diagnostic tools. The competitive landscape is characterized by the presence of numerous players, including United Imaging Healthcare, MISTRAS Group, and Intertek Testing Services Inc., who are actively engaged in strategic collaborations, product innovation, and market expansion initiatives to capture a larger market share.

Digital Radiography Service Company Market Share

Digital Radiography Service Market Concentration & Dynamics

The global Digital Radiography Service market is characterized by a moderate concentration, with several key players vying for market share. Companies such as United Imaging Healthcare, Express Diagnostics, Jesse Garant Metrology Center, MISTRAS Group, and MQC Labs, Inc. are prominent. The innovation ecosystem is robust, driven by continuous advancements in detector technology, image processing software, and AI-driven analytics. Regulatory frameworks, particularly in the medical equipment and aerospace sectors, play a significant role in shaping market entry and product development. Substitute products, primarily traditional film-based radiography and other non-destructive testing (NDT) methods, present a competitive challenge, though digital radiography offers superior image quality, efficiency, and data management. End-user trends are leaning towards higher resolution, faster acquisition times, and integrated reporting solutions. Mergers and Acquisitions (M&A) are a growing trend, with an estimated xx M&A deals recorded during the historical period (2019-2024), indicating consolidation and strategic expansion. The market share distribution is dynamic, with leading companies holding a collective market share estimated at over $30 billion.

- Market Concentration: Moderate, with a few key players holding significant market share.

- Innovation Ecosystem: Strong, driven by technological advancements in detectors, software, and AI.

- Regulatory Frameworks: Influential, especially in healthcare and aerospace, impacting market access and standards.

- Substitute Products: Traditional radiography and other NDT methods.

- End-User Trends: Demand for higher resolution, faster speeds, and integrated solutions.

- M&A Activities: Increasing, with an estimated xx deals during the historical period.

- Estimated Market Share of Leading Companies: Exceeding $30 billion collectively.

Digital Radiography Service Industry Insights & Trends

The Digital Radiography Service market is poised for significant expansion, driven by increasing demand for advanced imaging solutions across diverse industrial and medical applications. The global market size for Digital Radiography Services was approximately $15 billion in 2024 and is projected to reach over $40 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 9.5% during the forecast period of 2025–2033. This robust growth is underpinned by several key factors. Technological disruptions are at the forefront, with innovations in detector technology such as flat-panel detectors (FPDs) – both amorphous silicon (a-Si) and amorphous selenium (a-Se) – offering enhanced spatial resolution, higher detective quantum efficiency (DQE), and reduced radiation dose. Furthermore, the integration of Artificial Intelligence (AI) and Machine Learning (ML) algorithms is revolutionizing image analysis, enabling faster defect detection, quantitative assessment, and predictive maintenance capabilities. This is particularly impactful in the aerospace and automotive industries, where the need for stringent quality control and inspection of complex components is paramount.

Evolving consumer behaviors, or rather end-user expectations, are also shaping the market. In the medical equipment segment, there is a growing preference for digital radiography systems that offer improved patient comfort, reduced examination times, and superior diagnostic accuracy. Radiologists are increasingly demanding PACS (Picture Archiving and Communication System) and RIS (Radiology Information System) integration for seamless workflow management. Similarly, in industrial applications, the emphasis is shifting towards portable and real-time digital radiography solutions for on-site inspections, reducing downtime and increasing operational efficiency. The development of advanced software platforms that facilitate remote collaboration, data sharing, and sophisticated image manipulation is another key trend. The increasing adoption of IoT (Internet of Things) in industrial radiography is also contributing to the market’s growth, enabling remote monitoring and diagnostics of equipment. The ongoing shift from film-based systems to digital radiography is a fundamental driver, offering significant cost savings in the long run due to the elimination of film processing chemicals and consumables, alongside improved environmental sustainability. The increasing stringency of quality and safety regulations across various sectors further necessitates the adoption of high-fidelity digital imaging techniques.

Key Markets & Segments Leading Digital Radiography Service

The Aerospace application segment is a dominant force in the Digital Radiography Service market, driven by the stringent safety and quality requirements inherent in aircraft manufacturing and maintenance. The need for precise inspection of critical components, from engine parts to structural integrity, fuels the demand for advanced digital radiography solutions. Economic growth and substantial investments in the aerospace industry, particularly in emerging economies, further bolster this segment.

- Drivers in Aerospace:

- High safety and quality regulations.

- Complex component inspection requirements.

- Technological advancements in aircraft design.

- Increased air travel and fleet expansion.

The Medical Equipment segment also commands a significant share, propelled by an aging global population, rising healthcare expenditures, and the continuous need for diagnostic imaging. The adoption of digital radiography in hospitals and clinics for a wide range of diagnostic procedures, from skeletal imaging to early disease detection, is a primary growth catalyst.

- Drivers in Medical Equipment:

- Growing and aging global population.

- Increasing healthcare spending worldwide.

- Technological advancements in medical imaging.

- Demand for improved patient outcomes and reduced radiation exposure.

The Electronics segment, while perhaps smaller in absolute terms compared to aerospace and medical, is experiencing rapid growth due to the miniaturization of electronic components and the increasing complexity of printed circuit boards (PCBs). Digital radiography is crucial for inspecting solder joints, detecting internal defects, and ensuring the reliability of electronic devices.

- Drivers in Electronics:

- Miniaturization and increasing complexity of electronic devices.

- Demand for high-reliability electronic components.

- Growth of the semiconductor industry.

- Need for quality control in manufacturing processes.

In terms of Types, Mechanical External Service and Mechanical Internal Service are both vital. Mechanical External Service is crucial for inspecting the surface integrity and external features of manufactured parts, while Mechanical Internal Service is indispensable for detecting subsurface flaws, voids, and inconsistencies within components, particularly in demanding applications like aerospace and energy. The demand for both types is driven by the need for comprehensive quality assurance and the prevention of catastrophic failures.

- Drivers for Mechanical Services:

- Need for comprehensive quality assurance.

- Prevention of structural failures.

- Extended product lifespan requirements.

- Cost reduction through early defect detection.

Geographically, North America and Europe currently lead the market due to well-established industrial infrastructure and advanced healthcare systems. However, the Asia-Pacific region is emerging as a high-growth market, fueled by rapid industrialization, increasing investments in manufacturing, and expanding healthcare sectors.

Digital Radiography Service Product Developments

Product developments in Digital Radiography Service are characterized by a relentless pursuit of enhanced image quality, speed, and automation. Innovations in detector technology, such as higher DQE and lower noise levels, are enabling clearer images with reduced radiation doses. Advancements in software, including AI-powered image analysis and defect recognition algorithms, are significantly improving the efficiency and accuracy of inspections. The market is also seeing the development of more portable and robust systems for on-site applications, catering to industries like oil & gas and construction. Furthermore, the integration of cloud-based solutions for data storage, sharing, and remote diagnostics is enhancing accessibility and collaboration, making these services more versatile and impactful across diverse applications.

Challenges in the Digital Radiography Service Market

The Digital Radiography Service market faces several challenges that impede its growth. High initial investment costs for advanced digital radiography equipment and software can be a significant barrier, particularly for small and medium-sized enterprises (SMEs). The need for skilled personnel to operate and interpret digital radiography systems also presents a challenge, requiring ongoing training and development. Furthermore, cybersecurity concerns related to the transmission and storage of sensitive imaging data, especially in the medical sector, necessitate robust security protocols. Competitive pressures from established NDT providers and the slow adoption rates in certain traditional industries also contribute to market restraints.

- High Initial Investment Costs: Requiring substantial capital outlay for equipment and software.

- Skilled Workforce Requirement: Need for trained professionals for operation and interpretation.

- Cybersecurity Concerns: Protecting sensitive imaging data from breaches.

- Slow Adoption in Traditional Industries: Resistance to change and integration of new technologies.

Forces Driving Digital Radiography Service Growth

Several key forces are propelling the growth of the Digital Radiography Service market. Technological advancements, particularly in detector technology and AI-driven image analysis, are enhancing capabilities and opening new applications. Increasing stringent regulatory compliance across industries, from aerospace to medical, necessitates high-precision inspection methods offered by digital radiography. The growing global demand for quality assurance and safety in manufactured products is a fundamental driver. Furthermore, the inherent advantages of digital radiography over traditional film-based methods, such as faster processing, improved image quality, and reduced consumables, are encouraging widespread adoption. The rising trend of digitalization and Industry 4.0 initiatives are also creating a conducive environment for the integration of digital radiography solutions.

- Technological Advancements: Innovations in detectors and AI.

- Stringent Regulatory Compliance: Driving demand for precise inspection.

- Global Quality Assurance Demand: Ensuring product reliability and safety.

- Advantages over Film-Based Methods: Efficiency, image quality, cost-effectiveness.

- Digitalization & Industry 4.0: Integration into modern industrial processes.

Challenges in the Digital Radiography Service Market

Long-term growth catalysts for the Digital Radiography Service market lie in continued innovation and strategic market expansion. The development of even more advanced AI algorithms for predictive maintenance and anomaly detection will further enhance the value proposition. Strategic partnerships between equipment manufacturers, software providers, and service companies will foster integrated solutions and broader market reach. Expansion into emerging economies, where industrialization and healthcare infrastructure are rapidly developing, presents significant untapped potential. Furthermore, focusing on niche applications and developing specialized digital radiography solutions for specific industries can unlock new revenue streams and solidify market leadership. The ongoing trend towards miniaturization and the development of highly portable digital radiography systems will also continue to drive adoption across a wider range of field applications.

Emerging Opportunities in Digital Radiography Service

Emerging opportunities in the Digital Radiography Service market are diverse and promising. The burgeoning field of additive manufacturing (3D printing) presents a significant opportunity for digital radiography to inspect internal structures and ensure the integrity of complex 3D-printed components. The increasing adoption of drone technology for inspections in hard-to-reach or hazardous environments offers a platform for integrating portable digital radiography systems. The growing demand for non-destructive testing in renewable energy sectors, such as wind turbines and solar panels, is another area of opportunity. Furthermore, the development of augmented reality (AR) and virtual reality (VR) interfaces for digital radiography image visualization and analysis can enhance user experience and diagnostic capabilities. The increasing focus on personalized medicine and advanced diagnostics in healthcare will also drive demand for higher resolution and more sophisticated digital radiography applications.

- Additive Manufacturing Inspection: Ensuring the quality of 3D-printed parts.

- Drone-Based Inspections: Expanding reach into hazardous or remote areas.

- Renewable Energy Sector: Inspection needs for wind turbines and solar panels.

- AR/VR Integration: Enhancing visualization and analysis of radiographic images.

- Personalized Medicine & Advanced Diagnostics: Driving demand for sophisticated imaging.

Leading Players in the Digital Radiography Service Sector

- United Imaging Healthcare

- Express Diagnostics

- Jesse Garant Metrology Center

- MISTRAS Group

- MQC Labs, Inc.

- Delphi Precision Imaging

- Intertek Testing Services Inc.

- Specialized NDE, Inc.

- Twin Ports Testing, Inc.

- Buffalo Inspection Services

- VJ Group

- JANX

- Micron, Inc.

- Certified Testing Systems

- WesDyne International

- XCEL NDT LLC

- NECTEC

Key Milestones in Digital Radiography Service Industry

- 2019: Increased adoption of AI in industrial radiography for automated defect detection.

- 2020: Launch of next-generation flat-panel detectors with significantly improved DQE.

- 2021: Growing integration of cloud-based PACS for remote access and collaboration.

- 2022: Major advancements in portable digital radiography systems for field applications.

- 2023: Significant investments in R&D for digital radiography solutions in additive manufacturing.

- 2024: Increased M&A activities indicating market consolidation and strategic growth.

Strategic Outlook for Digital Radiography Service Market

The strategic outlook for the Digital Radiography Service market is highly optimistic, driven by sustained technological innovation and expanding application areas. The continued integration of AI and machine learning will be a key growth accelerator, enabling advanced analytics, predictive maintenance, and autonomous inspection capabilities. Strategic collaborations between technology providers and end-users will foster tailored solutions, driving adoption across diverse industries. The increasing emphasis on regulatory compliance and safety standards worldwide will further solidify the demand for high-fidelity digital radiography. Furthermore, the expansion into emerging markets and the development of cost-effective solutions will unlock new growth avenues. The market is expected to witness further consolidation through strategic acquisitions, leading to a more streamlined and competitive landscape, with a focus on delivering comprehensive, end-to-end digital radiography solutions.

Digital Radiography Service Segmentation

-

1. Application

- 1.1. Aerospace

- 1.2. Electronics

- 1.3. Medical Equipment

- 1.4. Other

-

2. Types

- 2.1. Mechanical Internal Service

- 2.2. Mechanical External Service

Digital Radiography Service Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Digital Radiography Service Regional Market Share

Geographic Coverage of Digital Radiography Service

Digital Radiography Service REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Digital Radiography Service Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Aerospace

- 5.1.2. Electronics

- 5.1.3. Medical Equipment

- 5.1.4. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Mechanical Internal Service

- 5.2.2. Mechanical External Service

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Digital Radiography Service Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Aerospace

- 6.1.2. Electronics

- 6.1.3. Medical Equipment

- 6.1.4. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Mechanical Internal Service

- 6.2.2. Mechanical External Service

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Digital Radiography Service Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Aerospace

- 7.1.2. Electronics

- 7.1.3. Medical Equipment

- 7.1.4. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Mechanical Internal Service

- 7.2.2. Mechanical External Service

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Digital Radiography Service Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Aerospace

- 8.1.2. Electronics

- 8.1.3. Medical Equipment

- 8.1.4. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Mechanical Internal Service

- 8.2.2. Mechanical External Service

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Digital Radiography Service Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Aerospace

- 9.1.2. Electronics

- 9.1.3. Medical Equipment

- 9.1.4. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Mechanical Internal Service

- 9.2.2. Mechanical External Service

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Digital Radiography Service Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Aerospace

- 10.1.2. Electronics

- 10.1.3. Medical Equipment

- 10.1.4. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Mechanical Internal Service

- 10.2.2. Mechanical External Service

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 United Imaging Healthcare

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Express Diagnostics

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Jesse Garant Metrology Center

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 MISTRAS Group

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 MQC Labs

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Inc

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Delphi Precision Imaging

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Intertek Testing Services Inc.

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Specialized NDE

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Inc.

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Twin Ports Testing

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Inc.

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Buffalo Inspection Services

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 VJ Group

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 JANX

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Micron

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Inc.

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Certified Testing Systems

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 WesDyne International

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 XCEL NDT LLC

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 NECTEC

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.1 United Imaging Healthcare

List of Figures

- Figure 1: Global Digital Radiography Service Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Digital Radiography Service Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Digital Radiography Service Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Digital Radiography Service Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Digital Radiography Service Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Digital Radiography Service Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Digital Radiography Service Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Digital Radiography Service Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Digital Radiography Service Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Digital Radiography Service Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Digital Radiography Service Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Digital Radiography Service Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Digital Radiography Service Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Digital Radiography Service Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Digital Radiography Service Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Digital Radiography Service Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Digital Radiography Service Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Digital Radiography Service Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Digital Radiography Service Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Digital Radiography Service Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Digital Radiography Service Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Digital Radiography Service Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Digital Radiography Service Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Digital Radiography Service Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Digital Radiography Service Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Digital Radiography Service Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Digital Radiography Service Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Digital Radiography Service Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Digital Radiography Service Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Digital Radiography Service Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Digital Radiography Service Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Digital Radiography Service Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Digital Radiography Service Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Digital Radiography Service Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Digital Radiography Service Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Digital Radiography Service Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Digital Radiography Service Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Digital Radiography Service Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Digital Radiography Service Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Digital Radiography Service Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Digital Radiography Service Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Digital Radiography Service Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Digital Radiography Service Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Digital Radiography Service Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Digital Radiography Service Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Digital Radiography Service Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Digital Radiography Service Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Digital Radiography Service Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Digital Radiography Service Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Digital Radiography Service Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Digital Radiography Service?

The projected CAGR is approximately 9.9%.

2. Which companies are prominent players in the Digital Radiography Service?

Key companies in the market include United Imaging Healthcare, Express Diagnostics, Jesse Garant Metrology Center, MISTRAS Group, MQC Labs, Inc, Delphi Precision Imaging, Intertek Testing Services Inc., Specialized NDE, Inc., Twin Ports Testing, Inc., Buffalo Inspection Services, VJ Group, JANX, Micron, Inc., Certified Testing Systems, WesDyne International, XCEL NDT LLC, NECTEC.

3. What are the main segments of the Digital Radiography Service?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.46 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Digital Radiography Service," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Digital Radiography Service report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Digital Radiography Service?

To stay informed about further developments, trends, and reports in the Digital Radiography Service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence