Key Insights

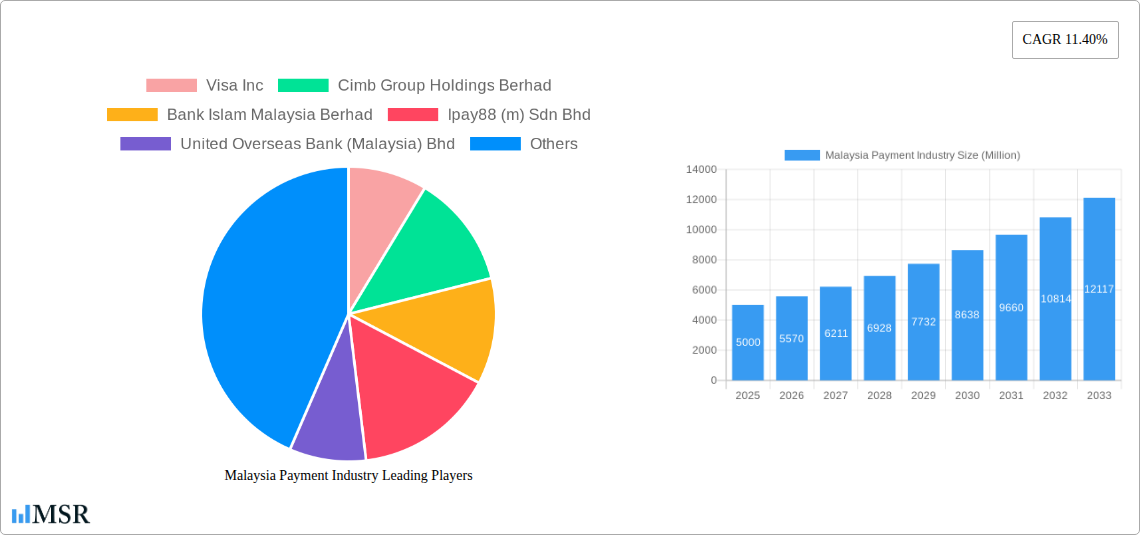

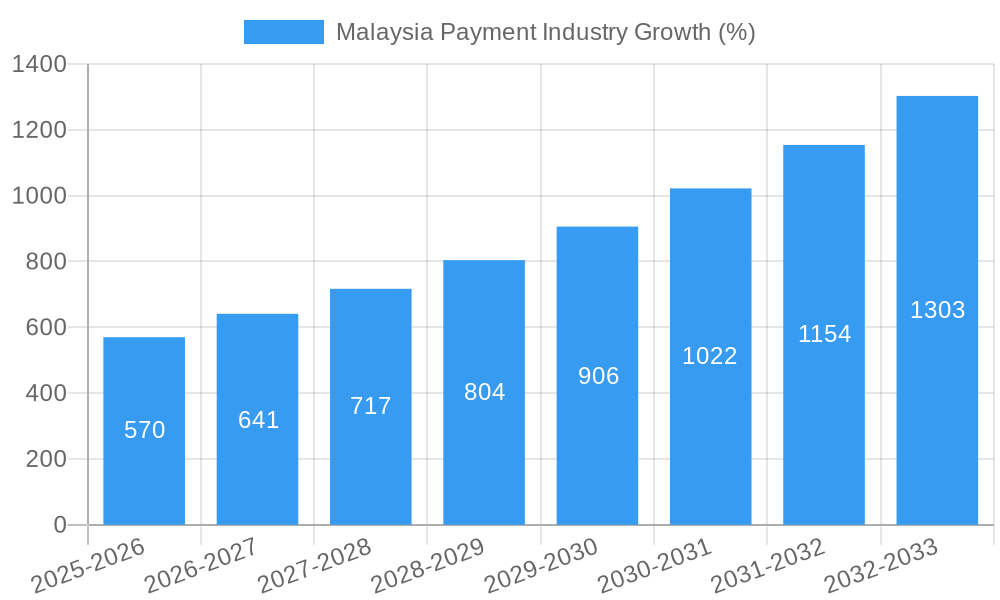

The Malaysian payment industry is experiencing robust growth, projected to reach a substantial market size by 2033. A compound annual growth rate (CAGR) of 11.40% from 2019 to 2024 suggests a dynamic market driven by increasing digital adoption, rising smartphone penetration, and a growing e-commerce sector. Key drivers include the government's push for digitalization, increasing financial inclusion initiatives, and the expanding adoption of mobile payment solutions like GrabPay and others. The increasing popularity of online shopping and digital services across retail, entertainment, healthcare, and hospitality sectors further fuels this expansion. While the exact 2025 market size is unavailable, extrapolating from the CAGR and considering the industry trends, we can estimate a significant market valuation in the hundreds of millions of ringgit. This robust growth is likely to be sustained throughout the forecast period (2025-2033), propelled by further technological advancements and evolving consumer preferences towards cashless transactions.

The segmentation reveals a strong preference for digital payment modes. Point-of-sale (POS) and online payment methods are dominating the market, reflecting a shift away from traditional cash transactions. Major players like Visa, Mastercard, GrabPay, and various Malaysian banks are aggressively competing in this space, continuously innovating their offerings and expanding their reach. However, challenges remain. These include concerns about data security, the need for improved digital literacy among certain demographics, and ensuring seamless interoperability between various payment systems. Addressing these challenges will be crucial for sustained, inclusive growth in the Malaysian payment industry. The competitive landscape necessitates ongoing innovation and strategic partnerships to maintain market share and cater to evolving consumer needs and preferences. Maintaining a balance between growth and regulatory compliance also presents an ongoing challenge for market participants.

Malaysia Payment Industry Report: 2019-2033

This comprehensive report provides a detailed analysis of the Malaysian payment industry, offering invaluable insights for stakeholders, investors, and businesses operating within this dynamic market. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report leverages historical data (2019-2024) and robust forecasting methodologies to provide a clear picture of the industry's trajectory. The Malaysian payment market, valued at xx Million in 2025, is projected to experience significant growth, reaching xx Million by 2033, achieving a CAGR of xx%. This report delves into key segments, dominant players, and emerging trends shaping the future of payments in Malaysia.

Malaysia Payment Industry Market Concentration & Dynamics

The Malaysian payment industry exhibits a moderately concentrated market structure, with key players like Maybank, CIMB Group Holdings Berhad, and several international giants holding significant market share. However, the rise of fintech companies and the increasing adoption of digital payment solutions are fostering a more competitive landscape. The innovation ecosystem is vibrant, driven by government initiatives promoting digitalization and a burgeoning startup scene. The regulatory framework, while evolving, is generally supportive of innovation but also emphasizes consumer protection and financial stability. Substitute products, such as cash, are gradually being replaced by digital alternatives, accelerating the industry's growth. End-user trends indicate a strong preference for convenient, secure, and cashless payment options. M&A activity has been moderate, with a focus on strengthening digital capabilities and expanding market reach. In the past five years, approximately xx M&A deals have been recorded within the Malaysian payments space. Key players like Visa Inc, CIMB Group Holdings Berhad, and Maybank maintain leading market share, estimated at xx%, xx%, and xx% respectively in 2025.

- Market Concentration: Moderately concentrated, with major players holding significant share.

- Innovation Ecosystem: Strong, supported by government initiatives and fintech startups.

- Regulatory Framework: Supportive of innovation, emphasizing consumer protection.

- Substitute Products: Cash is being rapidly replaced by digital payment methods.

- End-User Trends: Strong preference for convenience, security, and cashless transactions.

- M&A Activity: Moderate activity, focusing on digital expansion and market reach.

Malaysia Payment Industry Industry Insights & Trends

The Malaysian payment industry is experiencing rapid growth, driven primarily by increasing smartphone penetration, rising e-commerce adoption, and government initiatives promoting cashless transactions. Technological disruptions, such as the emergence of mobile wallets and QR code payments, are transforming the payment landscape. Consumer behavior is shifting towards digital payment methods, with a marked preference for convenience and security. The market is witnessing the rise of super-apps offering integrated payment solutions. The increasing adoption of contactless payments, fueled by the pandemic, further accelerates this shift. Furthermore, the government's push towards a digital economy is a significant catalyst, encouraging both businesses and consumers to embrace digital payment solutions. This transition is driving significant industry growth, resulting in a market size of xx Million in 2025 and is projected to reach xx Million by 2033.

Key Markets & Segments Leading Malaysia Payment Industry

The Malaysian payment industry is segmented by end-user industry (Retail, Entertainment, Healthcare, Hospitality, Other) and mode of payment (Point of Sale, Online Sale). The retail segment dominates the market, driven by robust e-commerce growth and the increasing preference for digital payments in everyday transactions. Online sales are also experiencing exponential growth, owing to the rise of e-commerce platforms and online shopping.

Dominant Segments:

- By End-user Industry: Retail (xx Million), Online Sales (xx Million)

- By Mode of Payment: Online Sale (xx Million), Point of Sale (xx Million)

Drivers:

- Retail: Strong e-commerce growth, increasing digital payment adoption.

- Online Sale: Rise of e-commerce platforms, increased online shopping.

- Point of Sale: Expanding contactless payment infrastructure.

Malaysia Payment Industry Product Developments

The Malaysian payment industry is witnessing rapid product innovation, driven by technological advancements. New payment methods, including mobile wallets, QR code payments, and biometric authentication, are gaining popularity. The integration of payment solutions within super-apps is also shaping the market. These innovations enhance convenience, security, and efficiency, fostering wider adoption of digital payments. The competitive landscape pushes companies to offer innovative features and competitive pricing, further driving product development and customer acquisition.

Challenges in the Malaysia Payment Industry Market

The Malaysian payment industry faces challenges including regulatory hurdles in keeping up with rapid technological changes, cybersecurity risks associated with digital transactions, and the need for increased financial literacy among consumers. The existing infrastructure in certain areas still lags behind in digital payments capabilities. Competition from established banks and new fintech players also intensifies pressures on profitability and market share. These challenges impact overall market growth and require proactive solutions from industry players and regulatory bodies.

Forces Driving Malaysia Payment Industry Growth

Technological advancements, including the increasing use of smartphones and the development of innovative payment solutions, are key growth drivers. The government's push towards a cashless society and supportive policies is creating a favorable environment for industry growth. The expanding e-commerce sector and the increasing adoption of digital payment methods by businesses and consumers further accelerate growth. Improved infrastructure and increased financial literacy also contribute positively to the expansion of digital payment adoption.

Challenges in the Malaysia Payment Industry Market

Long-term growth relies on continuous innovation, strategic partnerships to enhance capabilities and expand market reach, and the expansion into new markets and consumer segments. Improving cybersecurity measures and fostering consumer trust are vital for sustaining growth. Collaboration between financial institutions and fintech companies can unlock further growth potential.

Emerging Opportunities in Malaysia Payment Industry

The rise of Buy Now, Pay Later (BNPL) services and the increasing demand for cross-border payment solutions present significant opportunities. The integration of artificial intelligence and machine learning in fraud prevention and risk management also offers growth potential. The expanding adoption of open banking and the growth of the gig economy create new avenues for payment solutions providers.

Leading Players in the Malaysia Payment Industry Sector

- Visa Inc

- CIMB Group Holdings Berhad

- Bank Islam Malaysia Berhad

- Ipay88 (m) Sdn Bhd

- United Overseas Bank (Malaysia) Bhd

- Huawei Pay (Huawei Technologies Co Ltd)

- Grab Pay (Grab Holdings Limited)

- Paypal Holdings Inc

- Maybank

- Samsung Pay (Samsung Electronics Co Ltd)

Key Milestones in Malaysia Payment Industry Industry

- May 2023: Maybank launches cross-border QR payment service for Malaysia, Singapore, Indonesia, and Thailand, facilitating cashless transactions via the MAE app.

- January 2023: Xoom (PayPal) launches debit card deposit for cross-border money transfers, enhancing remittance accessibility.

Strategic Outlook for Malaysia Payment Industry Market

The Malaysian payment industry holds immense growth potential, driven by sustained digital adoption, government initiatives, and technological innovation. Strategic partnerships, investments in cybersecurity, and expansion into new market segments will be critical for success. Focus on enhancing customer experience and addressing evolving consumer preferences will be key to capturing market share and driving long-term growth.

Malaysia Payment Industry Segmentation

-

1. Mode of Payment

-

1.1. Point of Sale

- 1.1.1. Card Payments

- 1.1.2. Digital Wallets

- 1.1.3. Cash

- 1.1.4. Other Point-of-sale Payments

-

1.2. Online Sale

- 1.2.1. Other Online Sale Payments

-

1.1. Point of Sale

-

2. End-user Industry

- 2.1. Retail

- 2.2. Entertainment

- 2.3. Healthcare

- 2.4. Hospitality

- 2.5. Other End-user Industries

Malaysia Payment Industry Segmentation By Geography

- 1. Malaysia

Malaysia Payment Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 11.40% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 E-commerce Growth

- 3.2.2 Rising Basket Spend

- 3.2.3 and Rise in Digitally-aware Population; Adoption of Card-based Payments

- 3.3. Market Restrains

- 3.3.1. Challenges Faced by Small Retailers and Street Vendors while Adapting to the Cashless Payment Ecosystem

- 3.4. Market Trends

- 3.4.1. Card Payments to Witness the Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Malaysia Payment Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 5.1.1. Point of Sale

- 5.1.1.1. Card Payments

- 5.1.1.2. Digital Wallets

- 5.1.1.3. Cash

- 5.1.1.4. Other Point-of-sale Payments

- 5.1.2. Online Sale

- 5.1.2.1. Other Online Sale Payments

- 5.1.1. Point of Sale

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Retail

- 5.2.2. Entertainment

- 5.2.3. Healthcare

- 5.2.4. Hospitality

- 5.2.5. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Malaysia

- 5.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Visa Inc

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Cimb Group Holdings Berhad

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Bank Islam Malaysia Berhad

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Ipay88 (m) Sdn Bhd

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 United Overseas Bank (Malaysia) Bhd

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Huawei Pay (Huawei Technologies Co Ltd)*List Not Exhaustive

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Grab Pay (Grab Holdings Limited)

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Paypal Holdings Inc

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Maybank

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Samsung Pay (Samsung Electronics Co Ltd)

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Visa Inc

List of Figures

- Figure 1: Malaysia Payment Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Malaysia Payment Industry Share (%) by Company 2024

List of Tables

- Table 1: Malaysia Payment Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Malaysia Payment Industry Revenue Million Forecast, by Mode of Payment 2019 & 2032

- Table 3: Malaysia Payment Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 4: Malaysia Payment Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Malaysia Payment Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Malaysia Payment Industry Revenue Million Forecast, by Mode of Payment 2019 & 2032

- Table 7: Malaysia Payment Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 8: Malaysia Payment Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Malaysia Payment Industry?

The projected CAGR is approximately 11.40%.

2. Which companies are prominent players in the Malaysia Payment Industry?

Key companies in the market include Visa Inc, Cimb Group Holdings Berhad, Bank Islam Malaysia Berhad, Ipay88 (m) Sdn Bhd, United Overseas Bank (Malaysia) Bhd, Huawei Pay (Huawei Technologies Co Ltd)*List Not Exhaustive, Grab Pay (Grab Holdings Limited), Paypal Holdings Inc, Maybank, Samsung Pay (Samsung Electronics Co Ltd).

3. What are the main segments of the Malaysia Payment Industry?

The market segments include Mode of Payment, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

E-commerce Growth. Rising Basket Spend. and Rise in Digitally-aware Population; Adoption of Card-based Payments.

6. What are the notable trends driving market growth?

Card Payments to Witness the Growth.

7. Are there any restraints impacting market growth?

Challenges Faced by Small Retailers and Street Vendors while Adapting to the Cashless Payment Ecosystem.

8. Can you provide examples of recent developments in the market?

May 2023: Maybank launched its cross-border QR payment service for Maybank customers traveling to Singapore, Indonesia, and Thailand, as they can now make cashless and instant payment transactions via the MAE app. Similarly, incoming tourists from these countries can make cashless payments with Maybank QRPay merchants in Malaysia. The new offering will enable Malaysians visiting the respective countries to enjoy a cheaper, faster, and more convenient payment option through the MAE app.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Malaysia Payment Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Malaysia Payment Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Malaysia Payment Industry?

To stay informed about further developments, trends, and reports in the Malaysia Payment Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence