Key Insights

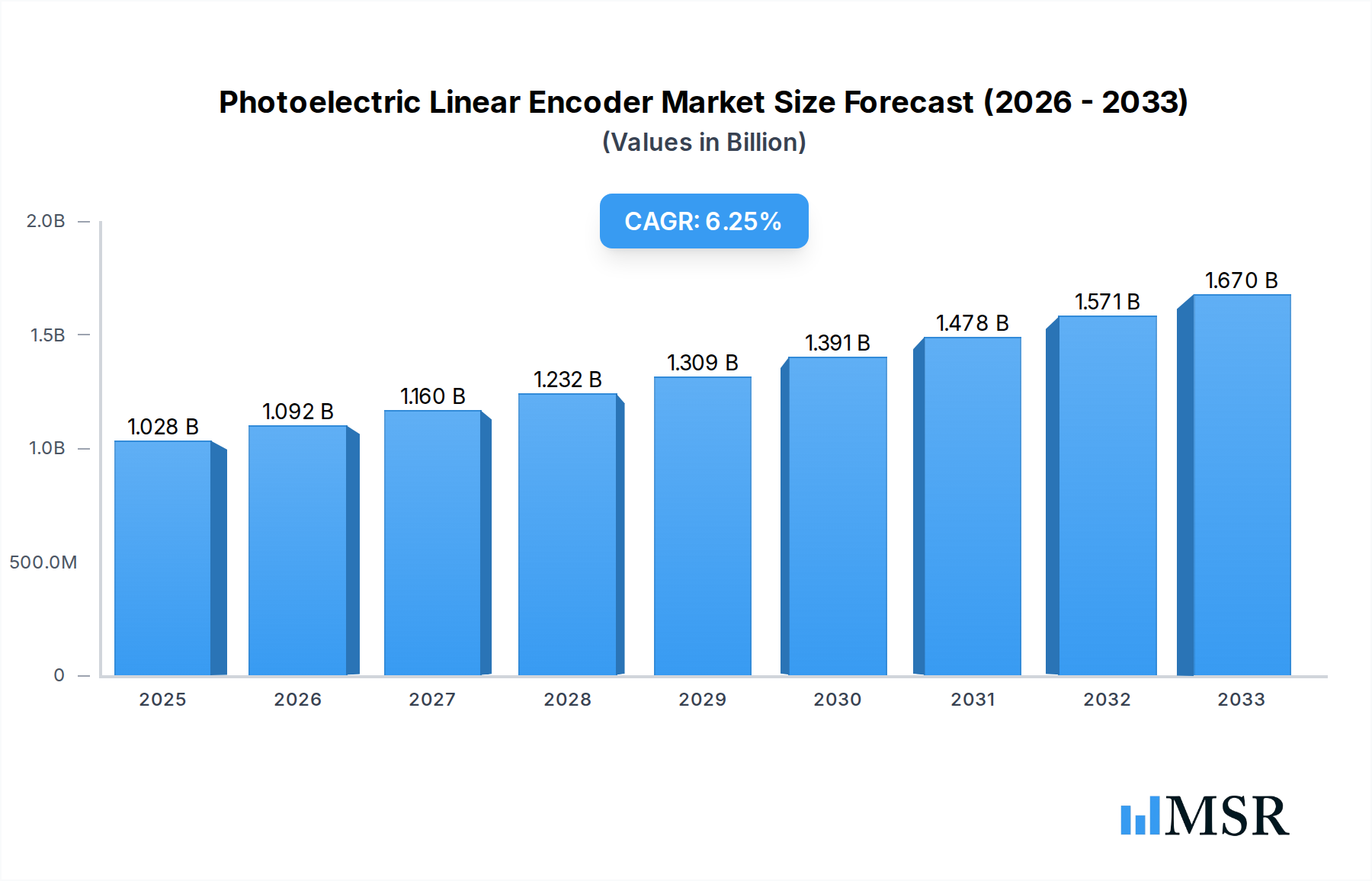

The global photoelectric linear encoder market is poised for significant expansion, with an estimated market size of USD 1028 million in 2025. This growth is fueled by the increasing adoption of industrial automation across various sectors, including manufacturing, robotics, and logistics. The demand for precise and reliable linear position feedback is paramount in these applications to enhance operational efficiency, product quality, and safety. The market is further propelled by advancements in sensor technology, leading to smaller, more accurate, and cost-effective photoelectric linear encoders. Industries like aerospace are also contributing to market growth, requiring high-performance sensing solutions for critical control systems. The competitive landscape features established players such as EPC, Dynapar, and Baumer Group, alongside emerging companies, all vying for market share through product innovation and strategic partnerships.

Photoelectric Linear Encoder Market Size (In Billion)

The market is projected to witness a healthy CAGR of 6.4% from 2025 to 2033, indicating sustained and robust growth. This upward trajectory is primarily driven by the escalating demand for precision measurement and control in advanced manufacturing processes, the growing use of robotics in assembly lines, and the need for sophisticated positioning systems in the aerospace and defense sectors. While the market benefits from these strong drivers, it also faces certain restraints, such as the initial high cost of implementation for some advanced systems and the technical expertise required for integration. However, the long-term benefits of improved automation and precision are expected to outweigh these challenges. The market is segmented into two primary types: incremental and absolute encoders, with incremental encoders holding a significant market share due to their cost-effectiveness for many applications, while absolute encoders are favored for applications requiring immediate position knowledge upon power-up. Geographically, Asia Pacific, particularly China and India, is anticipated to emerge as a key growth region, owing to its rapidly expanding manufacturing base and increasing investments in automation technologies.

Photoelectric Linear Encoder Company Market Share

Here is an SEO-optimized, engaging report description for the Photoelectric Linear Encoder market, designed to drive search visibility and attract industry stakeholders.

Report Title: Global Photoelectric Linear Encoder Market Analysis & Forecast: Industry Trends, Growth Drivers, and Competitive Landscape (2019-2033)

Report Description:

Dive deep into the rapidly evolving Photoelectric Linear Encoder Market with our comprehensive global analysis. This definitive report provides an in-depth examination of market concentration, innovation, and competitive dynamics from 2019 to 2033, with a base year of 2025. Uncover crucial industry insights, emerging trends, and key growth drivers shaping the future of linear encoder technology.

The global photoelectric linear encoder market is projected to witness robust expansion, driven by the increasing demand for precise motion control in industrial automation, aerospace, and beyond. Our report offers a detailed breakdown of market size, compound annual growth rate (CAGR), and segment-specific analysis, catering to industry stakeholders, manufacturers, and technology providers.

Explore the dominant regions and key application segments, including Industry Automation and Aerospace, alongside the pivotal encoder types: Incremental and Absolute. Gain actionable insights into product developments, prevailing challenges, and the strategic forces propelling market growth. This report features an extensive overview of leading players such as EPC, Dynapar, Baumer Group, BEI Sensors, TAMAGAWA SEIKI, Allied Motion, Broadcom, IDENCODER, and Shenzhen Bright Electronic Technology, and IDENCODER, providing a holistic view of the competitive landscape.

Key report features include:

This report is an indispensable resource for anyone seeking to understand and capitalize on the significant opportunities within the global photoelectric linear encoder market.

- Market Size & CAGR: Detailed market size estimations and CAGR projections for the forecast period.

- Segment Analysis: Comprehensive breakdown by application (Industry Automation, Aerospace) and encoder type (Incremental, Absolute).

- Regional Dominance: Identification of key geographical markets and their growth drivers.

- Competitive Intelligence: In-depth profiles of leading photoelectric linear encoder manufacturers.

- Future Outlook: Strategic insights and emerging opportunities for market participants.

Photoelectric Linear Encoder Market Concentration & Dynamics

The global photoelectric linear encoder market exhibits a moderate to high concentration, characterized by the presence of a few dominant players alongside a growing number of specialized manufacturers. Innovation ecosystems are vibrant, with significant R&D investment focused on enhancing resolution, speed, accuracy, and environmental resilience of photoelectric linear encoders. Regulatory frameworks, particularly concerning industrial safety standards and environmental compliance, are evolving, influencing product design and market entry. Substitute products, such as magnetic encoders, pose a competitive challenge, though photoelectric encoders often maintain an advantage in terms of resolution and precision for specific high-performance applications. End-user trends are increasingly driven by the demand for miniaturization, increased data output, and seamless integration into sophisticated control systems within industries like factory automation and robotics. Mergers and Acquisitions (M&A) activities, while not at an extremely high volume, are strategic, often aimed at consolidating market share, acquiring new technologies, or expanding geographical reach. For instance, M&A deal counts in the broader motion control sector have historically hovered around xx to xx annually, with targeted acquisitions in the encoder segment expected to follow suit. The market share of the top five players is estimated to be in the range of xx% to xx%, indicating a significant, yet not fully monopolistic, market structure.

Photoelectric Linear Encoder Industry Insights & Trends

The Photoelectric Linear Encoder market is poised for substantial growth, driven by an accelerating adoption of advanced automation technologies and an unyielding demand for precision in critical industrial processes. The global market size for photoelectric linear encoders is projected to reach approximately $XXX million by 2033, expanding from an estimated $XXX million in 2025. This growth trajectory is underpinned by a compelling Compound Annual Growth Rate (CAGR) of approximately XX.X% during the forecast period of 2025–2033.

A primary driver of this expansion is the escalating integration of sophisticated robotics and automated systems across diverse manufacturing sectors. As industries strive for enhanced efficiency, reduced error rates, and improved product quality, the need for high-resolution, reliable linear position feedback becomes paramount. Photoelectric linear encoders, with their inherent accuracy and speed capabilities, are indispensable components in achieving these objectives. The Industry Automation segment, in particular, is a powerhouse of demand, fueled by smart factory initiatives and the rise of Industry 4.0 principles.

Technological disruptions are continuously reshaping the landscape. Innovations such as miniaturization, enhanced environmental resistance (e.g., IP ratings for dust and water ingress), and the development of absolute encoding technologies offering multi-turn capabilities are broadening the application scope. The increasing adoption of serial communication protocols (e.g., EtherCAT, PROFINET) is facilitating seamless integration of encoders into networked control architectures, further stimulating demand.

Evolving consumer behaviors within the industrial sector are also playing a crucial role. There is a growing preference for intelligent encoders that offer advanced diagnostics, predictive maintenance capabilities, and user-friendly configuration interfaces. Manufacturers are responding by developing "smart" encoders that not only provide position data but also monitor their own health, thereby minimizing downtime and optimizing operational performance. The aerospace sector, with its stringent requirements for accuracy and reliability in flight control systems and navigation, represents another significant growth avenue. The continuous drive for lighter, more efficient aircraft necessitates advanced motion control solutions, positioning photoelectric linear encoders as key enablers.

Furthermore, the global push towards precision manufacturing in sectors like semiconductor fabrication, medical device production, and advanced metrology directly translates into a heightened demand for the sub-micron accuracy that photoelectric linear encoders provide. The ability to detect minute movements and maintain precise control over complex assembly lines makes these encoders critical for achieving the quality standards demanded by these high-value industries.

Key Markets & Segments Leading Photoelectric Linear Encoder

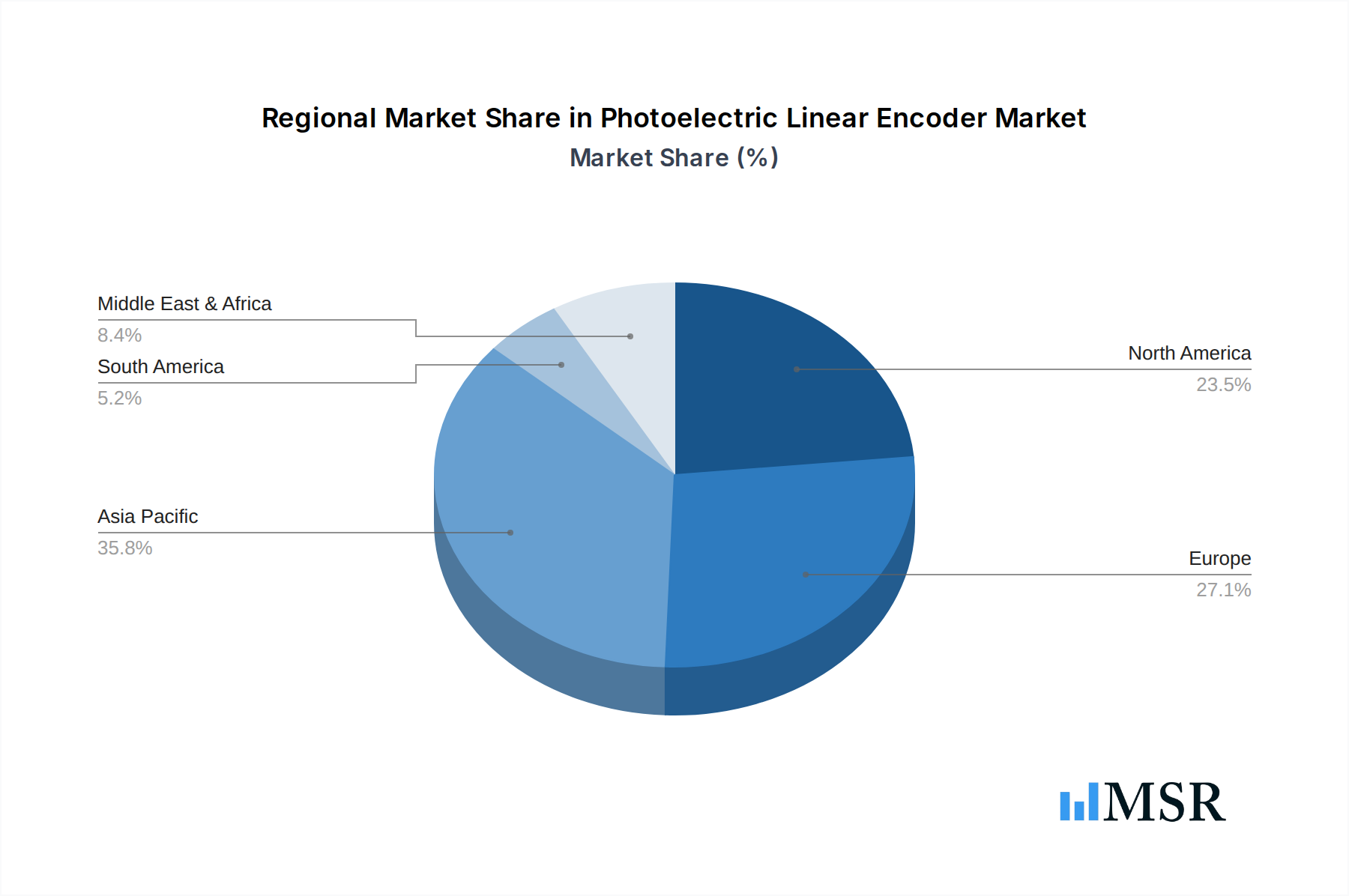

The global photoelectric linear encoder market is characterized by distinct regional strengths and segment dominance, with specific applications and encoder types driving significant growth.

Dominant Regions and Countries:

- Asia-Pacific stands out as the leading region in the photoelectric linear encoder market. This dominance is primarily attributed to the robust manufacturing base in countries like China, Japan, and South Korea, which are at the forefront of industrial automation and technological innovation.

- Drivers in Asia-Pacific:

- Massive Manufacturing Hub: The region's status as a global manufacturing powerhouse fuels demand for automation solutions, including precise positioning systems.

- Government Initiatives: Favorable government policies promoting advanced manufacturing, "Made in China 2025," and smart city development initiatives are significant catalysts.

- Growing R&D Investment: Increased spending on research and development by local and international companies within the region fosters technological advancements.

- Infrastructure Development: Continuous investment in infrastructure and smart grids further boosts the adoption of automated systems.

- Drivers in Asia-Pacific:

- North America and Europe represent other key markets, driven by advanced industrial automation adoption, stringent quality control requirements, and significant presence of aerospace and defense industries.

- Drivers in North America and Europe:

- High Adoption of Automation: Well-established industrial sectors are rapidly adopting Industry 4.0 technologies.

- Stringent Quality Standards: Industries like aerospace and medical demand the highest levels of precision and reliability offered by photoelectric linear encoders.

- Technological Advancements: Strong R&D capabilities and a focus on innovation in control systems.

- Skilled Workforce: Availability of a skilled workforce adept at implementing and maintaining advanced automation.

- Drivers in North America and Europe:

Dominant Segments:

Application: Industry Automation: This segment represents the largest and fastest-growing application for photoelectric linear encoders. The relentless pursuit of efficiency, accuracy, and productivity in manufacturing, assembly lines, robotics, and material handling systems makes photoelectric linear encoders indispensable. The increasing complexity of automated processes requires highly precise feedback for motion control, enabling seamless operation and reduced human intervention.

- Detailed Dominance Analysis: The sheer volume of manufacturing activities globally, coupled with the ongoing digital transformation of factories, places Industry Automation at the apex of demand. From large-scale automotive production to intricate semiconductor fabrication, photoelectric linear encoders are crucial for tasks such as CNC machining, pick-and-place operations, and automated inspection. The need for real-time, high-resolution positional data ensures that automated systems can perform with micron-level precision, a feat only achievable with advanced encoding technologies. The integration of collaborative robots (cobots) and autonomous mobile robots (AMRs) further amplifies this demand.

Types: Absolute Encoders: While Incremental encoders remain prevalent, Absolute encoders are gaining significant traction due to their ability to provide unambiguous position information immediately upon power-up, eliminating the need for homing routines. This is particularly critical in applications where power interruptions are frequent or where system initialization time is a key performance metric.

- Detailed Dominance Analysis: The advantages of absolute encoders, such as their intrinsic safety against position loss during power outages and their capability to provide precise position data without continuous movement, are driving their adoption, especially in safety-critical and complex automated systems. In applications like robotics, CNC machinery, and automated storage and retrieval systems, the immediate availability of accurate positional data from absolute encoders streamlines operations, improves safety, and enhances overall system efficiency. Their ability to maintain position information even after the system is powered down makes them ideal for applications requiring unattended operation or frequent restarts.

Application: Aerospace: This segment, while smaller in volume compared to Industry Automation, is characterized by very high-value applications and stringent performance requirements. Photoelectric linear encoders are critical for precision control in flight actuators, satellite positioning systems, and advanced diagnostic equipment. The demand here is driven by the need for unparalleled reliability and accuracy, where even minor deviations can have critical consequences.

Photoelectric Linear Encoder Product Developments

Recent product developments in the photoelectric linear encoder market are focused on enhancing performance, integration, and ruggedness. Innovations include encoders with higher resolutions, enabling sub-micron precision for advanced metrology and semiconductor manufacturing. Miniaturization is a key trend, allowing for integration into increasingly compact machinery. Developments in absolute encoding technology are offering multi-turn capabilities and improved error detection. Furthermore, there is a growing emphasis on encoders with built-in diagnostics and communication protocols like IO-Link for seamless integration into Industry 4.0 environments. These advancements equip photoelectric linear encoders to meet the evolving demands of sophisticated automation, robotics, and aerospace applications.

Challenges in the Photoelectric Linear Encoder Market

The photoelectric linear encoder market, despite its robust growth, faces several challenges. Intense competition from alternative encoder technologies, particularly magnetic encoders, puts pressure on pricing and market share. Supply chain disruptions, especially for specialized optical components, can lead to production delays and increased costs, impacting lead times and profitability. Furthermore, the stringent calibration and installation requirements for high-precision photoelectric encoders can be a barrier to adoption for less technically inclined users or in cost-sensitive applications. The rapid pace of technological advancement also necessitates continuous R&D investment, posing a challenge for smaller players to keep pace with innovation and maintain competitiveness.

Forces Driving Photoelectric Linear Encoder Growth

Several key forces are propelling the growth of the photoelectric linear encoder market. The overarching trend of industrial automation and the adoption of Industry 4.0 principles across global manufacturing sectors is a primary driver. The increasing demand for precision and accuracy in industries such as semiconductor manufacturing, medical device production, and advanced robotics necessitates the high-performance capabilities of photoelectric encoders. Furthermore, the aerospace and defense sectors' ongoing need for reliable and accurate motion control in critical applications provides a steady demand stream. Technological advancements, including miniaturization and improved environmental resistance, are expanding the application scope, making these encoders suitable for a wider range of demanding environments.

Challenges in the Photoelectric Linear Encoder Market

Long-term growth catalysts for the photoelectric linear encoder market stem from continued technological innovation and strategic market expansion. The development of even higher resolution encoders, capable of measuring at the nanometer scale, will open doors to ultra-precise applications in scientific instrumentation and advanced manufacturing. Innovations in material science could lead to more robust and cost-effective encoder designs, further broadening their applicability. Strategic partnerships between encoder manufacturers and automation solution providers will facilitate integrated systems and accelerate adoption. Expanding into emerging economies with rapidly industrializing sectors presents significant opportunities for market penetration and growth. The increasing demand for predictive maintenance in industrial settings also drives the development of "smart" encoders with integrated diagnostic capabilities.

Emerging Opportunities in Photoelectric Linear Encoder

Emerging opportunities in the photoelectric linear encoder market are being shaped by evolving technological landscapes and new application frontiers. The burgeoning field of cobots and collaborative robotics presents a significant avenue for growth, requiring precise and safe motion control. The increasing demand for advanced medical devices and diagnostic equipment, where sub-micron accuracy is critical, offers another lucrative segment. Furthermore, the development of augmented reality (AR) and virtual reality (VR) applications in industrial settings may create new demands for highly accurate positional tracking, where photoelectric linear encoders could play a role. The ongoing trend towards miniaturization in electronics and machinery will continue to drive demand for compact, high-performance encoder solutions. Exploration into novel optical sensing technologies could also lead to breakthroughs in encoder performance and cost-effectiveness.

Leading Players in the Photoelectric Linear Encoder Sector

- EPC

- Dynapar

- Baumer Group

- BEI Sensors

- TAMAGAWA SEIKI

- Allied Motion

- Broadcom

- IDENCODER

- Shenzhen Bright Electronic Technology

Key Milestones in Photoelectric Linear Encoder Industry

- 2019: Increased adoption of optical metrology in semiconductor fabrication, boosting demand for high-resolution photoelectric linear encoders.

- 2020: Growing impact of Industry 4.0 initiatives, driving the integration of smart encoders with advanced communication protocols.

- 2021: Advancements in miniaturization techniques leading to smaller and more robust encoder designs for diverse applications.

- 2022: Notable M&A activity in the broader motion control industry, hinting at potential consolidation in the encoder segment.

- 2023: Enhanced focus on absolute encoding technologies for improved safety and reduced system initialization times.

- 2024: Emergence of new applications in collaborative robotics and advanced medical equipment requiring high-precision linear feedback.

- 2025 (Base Year): Continued strong growth in industrial automation, solidifying the market position of photoelectric linear encoders.

- 2026-2033 (Forecast Period): Expected sustained growth driven by further technological innovations and expanding market reach into emerging economies.

Strategic Outlook for Photoelectric Linear Encoder Market

The strategic outlook for the photoelectric linear encoder market remains exceptionally positive, fueled by ongoing advancements and the insatiable demand for precision motion control across key industries. Growth accelerators include the continued digitalization of manufacturing, the rise of advanced robotics, and the expansion of aerospace and defense applications. The market will likely witness further innovation in areas such as ultra-high resolution, integrated diagnostics, and seamless connectivity to cloud-based IoT platforms. Companies that can effectively leverage these trends through strategic R&D, targeted partnerships, and expansion into high-growth geographical regions will be well-positioned to capture significant market share. The transition towards more intelligent and self-monitoring encoder systems will be a critical factor for long-term success.

Photoelectric Linear Encoder Segmentation

-

1. Application

- 1.1. Industrty Automation

- 1.2. Aerospace

-

2. Types

- 2.1. Incremental

- 2.2. Absolute

Photoelectric Linear Encoder Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Photoelectric Linear Encoder Regional Market Share

Geographic Coverage of Photoelectric Linear Encoder

Photoelectric Linear Encoder REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Photoelectric Linear Encoder Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Industrty Automation

- 5.1.2. Aerospace

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Incremental

- 5.2.2. Absolute

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Photoelectric Linear Encoder Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Industrty Automation

- 6.1.2. Aerospace

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Incremental

- 6.2.2. Absolute

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Photoelectric Linear Encoder Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Industrty Automation

- 7.1.2. Aerospace

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Incremental

- 7.2.2. Absolute

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Photoelectric Linear Encoder Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Industrty Automation

- 8.1.2. Aerospace

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Incremental

- 8.2.2. Absolute

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Photoelectric Linear Encoder Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Industrty Automation

- 9.1.2. Aerospace

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Incremental

- 9.2.2. Absolute

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Photoelectric Linear Encoder Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Industrty Automation

- 10.1.2. Aerospace

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Incremental

- 10.2.2. Absolute

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 EPC

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Dynapar

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Baumer Group

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 BEI Sensors

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 TAMAGAWA SEIKI

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Allied Motion

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Broadcom

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 IDENCODER

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Shenzhen Bright Electronic Technology

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 EPC

List of Figures

- Figure 1: Global Photoelectric Linear Encoder Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Photoelectric Linear Encoder Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Photoelectric Linear Encoder Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Photoelectric Linear Encoder Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Photoelectric Linear Encoder Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Photoelectric Linear Encoder Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Photoelectric Linear Encoder Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Photoelectric Linear Encoder Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Photoelectric Linear Encoder Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Photoelectric Linear Encoder Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Photoelectric Linear Encoder Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Photoelectric Linear Encoder Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Photoelectric Linear Encoder Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Photoelectric Linear Encoder Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Photoelectric Linear Encoder Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Photoelectric Linear Encoder Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Photoelectric Linear Encoder Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Photoelectric Linear Encoder Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Photoelectric Linear Encoder Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Photoelectric Linear Encoder Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Photoelectric Linear Encoder Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Photoelectric Linear Encoder Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Photoelectric Linear Encoder Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Photoelectric Linear Encoder Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Photoelectric Linear Encoder Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Photoelectric Linear Encoder Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Photoelectric Linear Encoder Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Photoelectric Linear Encoder Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Photoelectric Linear Encoder Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Photoelectric Linear Encoder Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Photoelectric Linear Encoder Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Photoelectric Linear Encoder Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Photoelectric Linear Encoder Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Photoelectric Linear Encoder Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Photoelectric Linear Encoder Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Photoelectric Linear Encoder Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Photoelectric Linear Encoder Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Photoelectric Linear Encoder Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Photoelectric Linear Encoder Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Photoelectric Linear Encoder Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Photoelectric Linear Encoder Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Photoelectric Linear Encoder Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Photoelectric Linear Encoder Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Photoelectric Linear Encoder Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Photoelectric Linear Encoder Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Photoelectric Linear Encoder Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Photoelectric Linear Encoder Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Photoelectric Linear Encoder Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Photoelectric Linear Encoder Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Photoelectric Linear Encoder Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Photoelectric Linear Encoder?

The projected CAGR is approximately 6.4%.

2. Which companies are prominent players in the Photoelectric Linear Encoder?

Key companies in the market include EPC, Dynapar, Baumer Group, BEI Sensors, TAMAGAWA SEIKI, Allied Motion, Broadcom, IDENCODER, Shenzhen Bright Electronic Technology.

3. What are the main segments of the Photoelectric Linear Encoder?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Photoelectric Linear Encoder," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Photoelectric Linear Encoder report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Photoelectric Linear Encoder?

To stay informed about further developments, trends, and reports in the Photoelectric Linear Encoder, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence