Key Insights

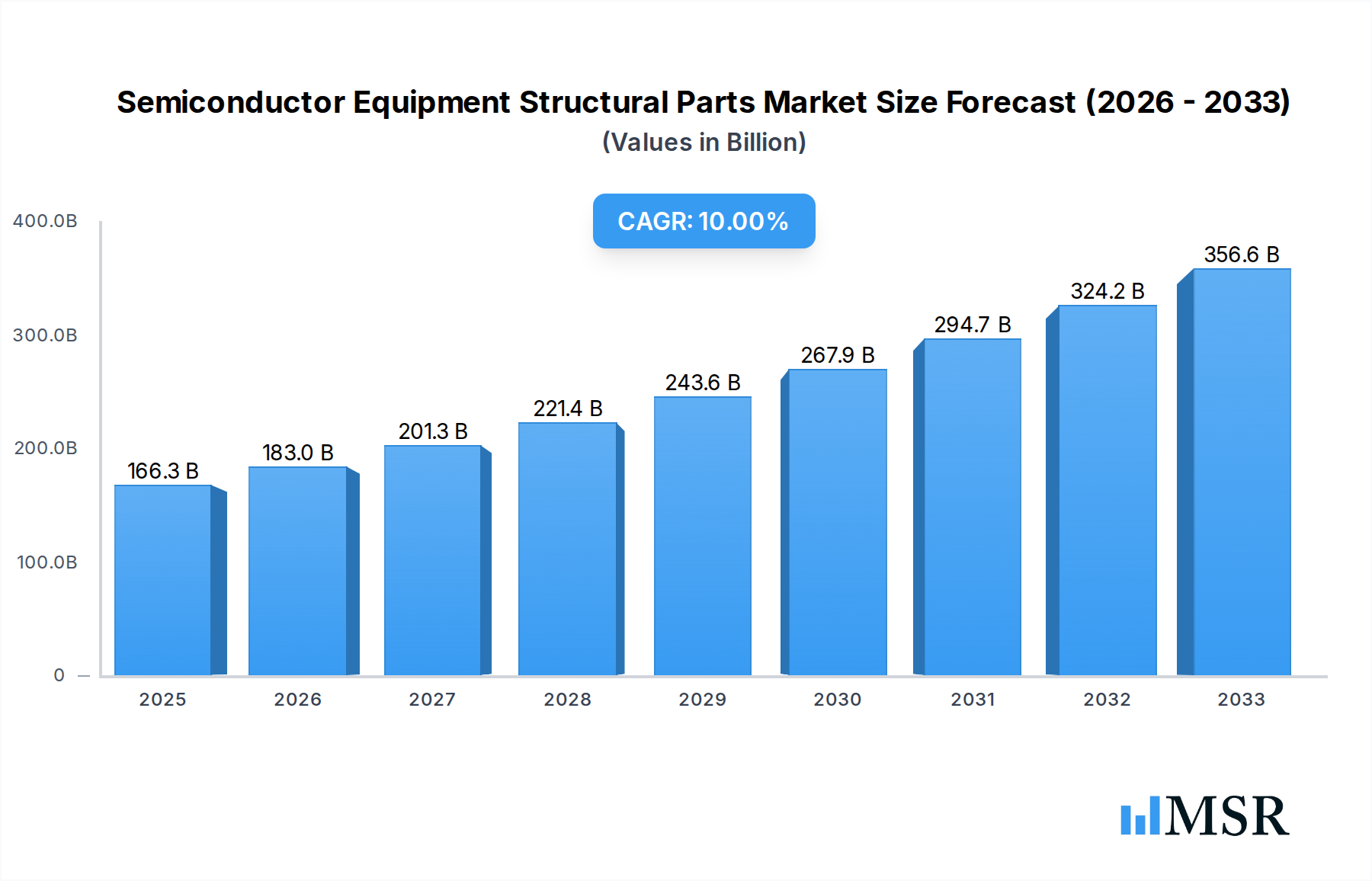

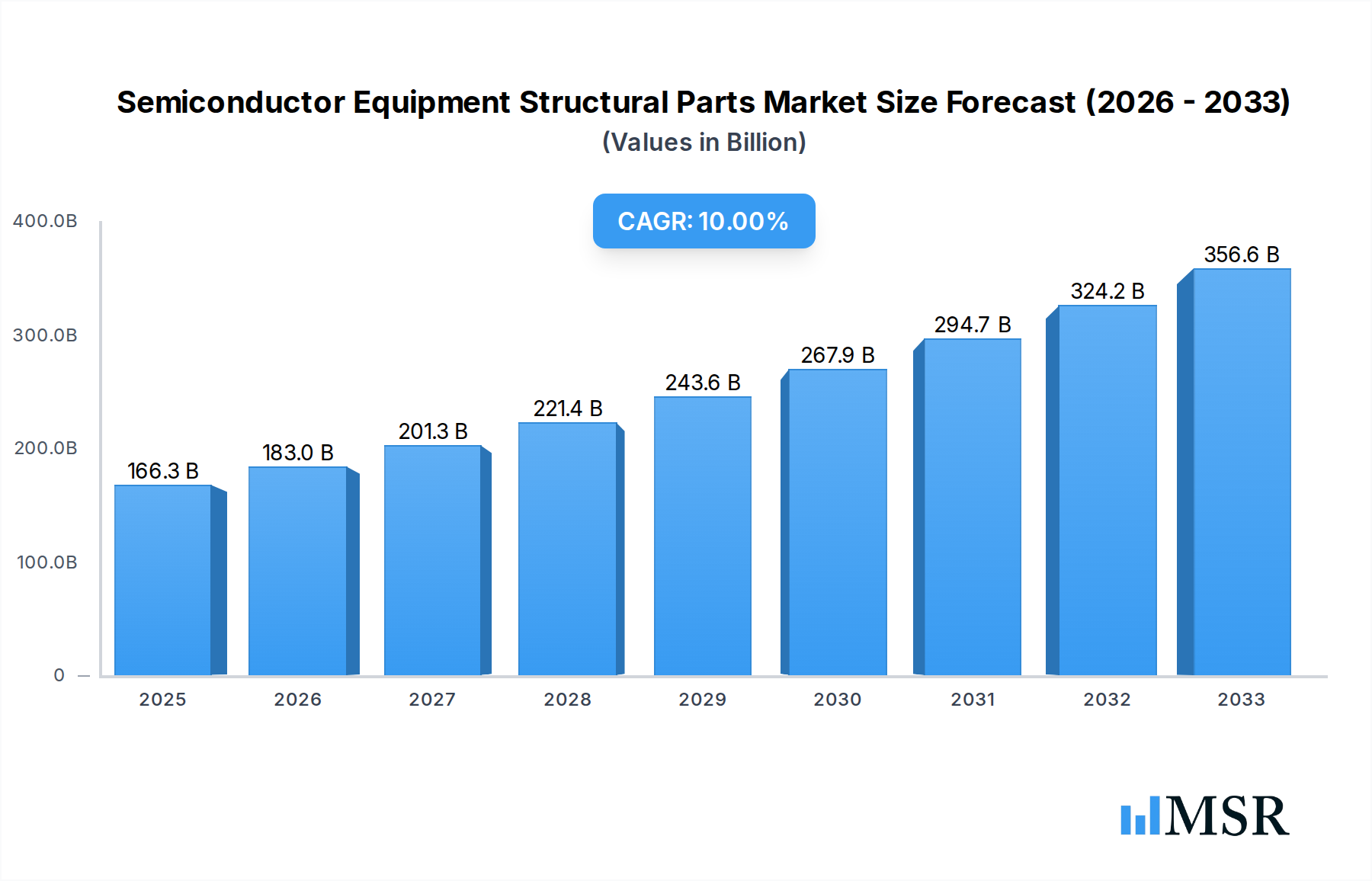

The global market for Semiconductor Equipment Structural Parts is poised for significant expansion, projected to reach an estimated $166.35 billion in 2025. This robust growth is underpinned by a compelling Compound Annual Growth Rate (CAGR) of 11%, indicating a sustained upward trajectory through 2033. This surge is primarily driven by the insatiable global demand for advanced semiconductors, fueled by the proliferation of 5G technology, artificial intelligence, the Internet of Things (IoT), and high-performance computing. As semiconductor manufacturers continually strive to enhance wafer fabrication processes and testing accuracy, the need for highly precise, durable, and specialized structural components for their equipment escalates. This includes critical parts for both wafer manufacturing equipment, ensuring the integrity and precision of chip production, and wafer testing equipment, guaranteeing the quality and functionality of finished semiconductors. The continuous innovation in semiconductor technology necessitates equally advanced structural solutions to support next-generation manufacturing and testing infrastructure.

Semiconductor Equipment Structural Parts Market Size (In Billion)

The market's expansion is further bolstered by ongoing technological advancements in material science and manufacturing techniques, enabling the production of lighter, stronger, and more resilient structural parts. Key trends include the increasing adoption of advanced alloys and composite materials, as well as sophisticated manufacturing processes like additive manufacturing (3D printing) for highly complex geometries. While the market demonstrates strong growth potential, certain factors could influence its pace. These might include geopolitical tensions impacting global supply chains, the high capital expenditure required for advanced semiconductor manufacturing facilities, and the stringent quality control demands inherent in the semiconductor industry. However, the overarching demand for semiconductors across virtually all modern industries, coupled with the strategic importance of semiconductor manufacturing, suggests a resilient and growing market for its essential structural components, with significant opportunities for established and emerging players alike, particularly in key regions like Asia Pacific.

Semiconductor Equipment Structural Parts Company Market Share

This in-depth report provides a panoramic view of the global Semiconductor Equipment Structural Parts market, a critical enabler of the advanced electronics industry. Spanning a study period from 2019 to 2033, with a base year of 2025, this analysis meticulously examines market dynamics, key players, technological advancements, and future growth trajectories. The market is projected to reach an estimated value of $50 billion by 2025, with a robust Compound Annual Growth Rate (CAGR) of 15% during the forecast period of 2025–2033. This report is essential for semiconductor manufacturers, equipment providers, material suppliers, investors, and industry strategists seeking to navigate this complex and rapidly evolving landscape.

Semiconductor Equipment Structural Parts Market Concentration & Dynamics

The semiconductor equipment structural parts market exhibits a moderate concentration, characterized by the presence of both large, established players and agile, specialized manufacturers. Innovation ecosystems are thriving, driven by intense R&D investment from leading companies aiming to meet the stringent demands of wafer manufacturing equipment and wafer testing equipment. Regulatory frameworks, particularly those focusing on supply chain security and export controls for advanced technologies, are increasingly influential. Substitute products are limited due to the highly specialized nature of these components; however, advancements in material science could offer future alternatives. End-user trends highlight a strong demand for high-precision, durable, and cost-effective structural parts that can withstand extreme conditions and contribute to increased manufacturing yields. Merger and acquisition (M&A) activities have been on an upward trend, with an estimated 15 major M&A deals recorded between 2019 and 2024, indicating consolidation and strategic expansion by key players like Dana Precision and Precision Components. Market share is fragmented, with the top 5 players holding approximately 40% of the market.

Semiconductor Equipment Structural Parts Industry Insights & Trends

The semiconductor equipment structural parts industry is poised for exceptional growth, fueled by an insatiable global demand for semiconductors. The estimated market size for semiconductor equipment structural parts reached $45 billion in 2024 and is projected to expand significantly, driven by the relentless advancement of integrated circuits and the increasing complexity of semiconductor manufacturing processes. A key growth driver is the burgeoning demand for advanced microprocessors and memory chips powering artificial intelligence (AI), 5G technology, and the Internet of Things (IoT). Technological disruptions are primarily centered around material science innovations, leading to the development of lighter, stronger, and more resistant aluminum structural parts and steel structural parts. Advanced manufacturing techniques like additive manufacturing (3D printing) are also gaining traction for producing intricate and customized components. Evolving consumer behaviors, characterized by a preference for more powerful and energy-efficient electronic devices, directly translate into increased demand for sophisticated semiconductor manufacturing equipment, and consequently, its structural components. The continuous push for miniaturization and higher performance in semiconductors necessitates structural parts with tighter tolerances, superior thermal management capabilities, and enhanced vibration damping. The global semiconductor capital expenditure is expected to surge past $100 billion annually, directly impacting the demand for these essential parts.

Key Markets & Segments Leading Semiconductor Equipment Structural Parts

The Wafer Manufacturing Equipment segment is the dominant force in the semiconductor equipment structural parts market, accounting for an estimated 70% of the total market value. This dominance is driven by the sheer scale and complexity of wafer fabrication processes, which require an extensive array of high-precision structural components. Within this segment, the demand for Aluminum Structural Parts is substantial, estimated at $25 billion in 2025, owing to their excellent strength-to-weight ratio, corrosion resistance, and machinability, crucial for maintaining cleanroom environments and minimizing particle generation.

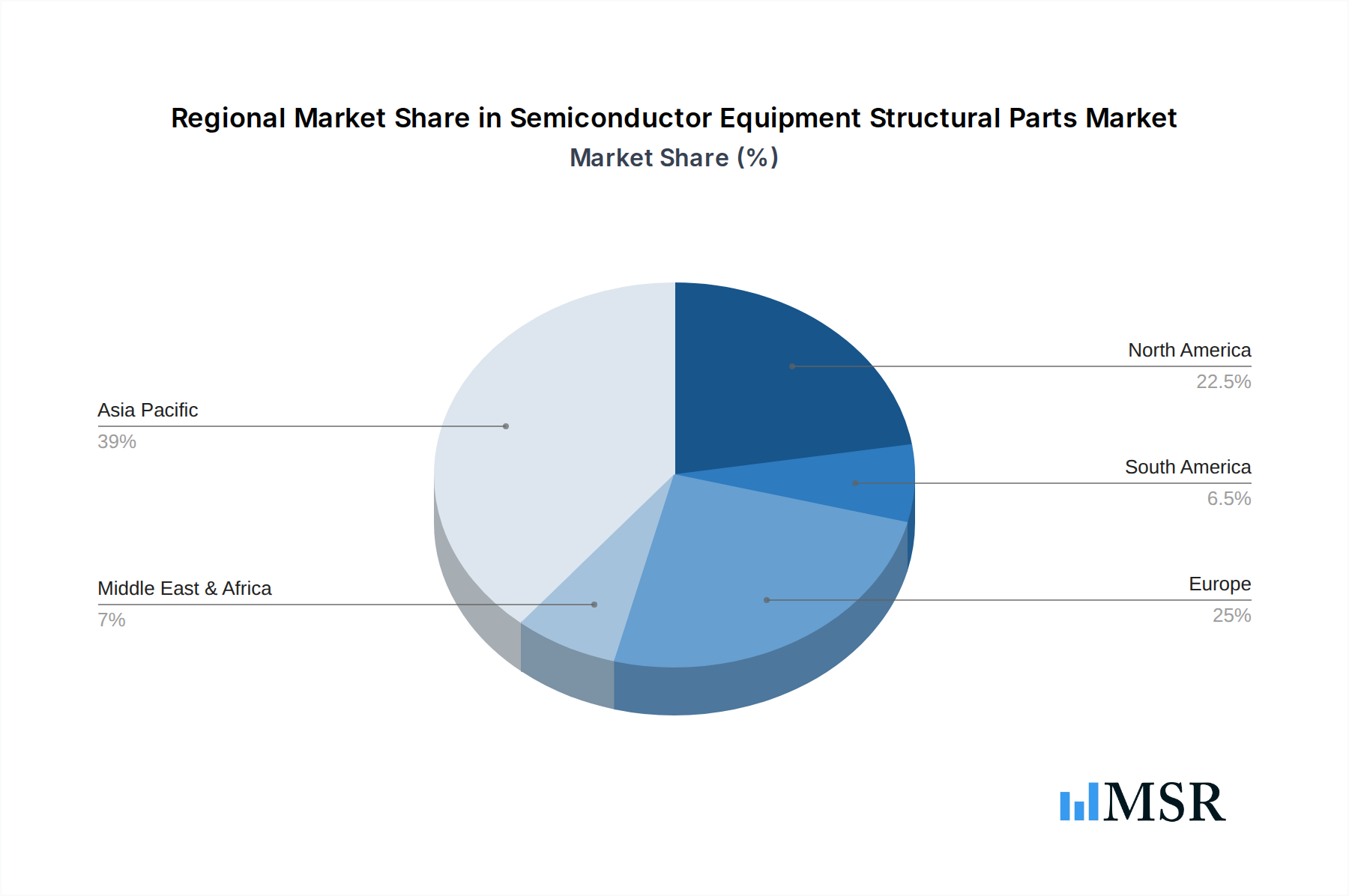

Dominant Region: Asia Pacific

- Economic Growth: Rapid industrialization and significant government investments in domestic semiconductor production capabilities.

- Infrastructure Development: Extensive expansion of semiconductor manufacturing facilities and R&D centers.

- Key Markets: China, South Korea, Taiwan, and Japan are major hubs for semiconductor manufacturing.

Dominant Application: Wafer Manufacturing Equipment

- Drivers: The continuous need for advanced lithography, etching, deposition, and cleaning systems. The ongoing global semiconductor shortage has accelerated investment in new wafer fabrication plants, directly boosting demand for the structural components of these complex machines. The increasing complexity of chip designs, requiring more intricate fabrication steps, further amplifies the need for specialized and robust structural parts.

- Detailed Dominance Analysis: Wafer manufacturing is the foundational stage of semiconductor production. The structural components for this equipment must meet exceptionally high standards of precision, rigidity, and stability to ensure sub-micron tolerances. Equipment like steppers, etchers, and chemical mechanical planarizers (CMPs) rely heavily on meticulously engineered structural elements. The demand for these parts is directly correlated with the output capacity and technological sophistication of semiconductor foundries worldwide.

Dominant Type: Aluminum Structural Parts

- Drivers: Lightweight properties are crucial for reducing inertia and enabling faster, more precise movements in wafer processing equipment. Excellent thermal conductivity aids in heat dissipation, a critical factor in maintaining stable operating conditions. High purity and non-reactivity are essential for preventing contamination in ultra-clean manufacturing environments.

- Detailed Dominance Analysis: Aluminum alloys, particularly those with high purity and excellent machinability, are indispensable for constructing the frames, gantries, and precision stages of wafer manufacturing and testing equipment. Their ability to be precisely machined into complex geometries without compromising structural integrity makes them a preferred choice. Companies like Suzhou Huaya Intelligence Technology are key suppliers of these critical aluminum components.

The Wafer Testing Equipment segment, while smaller, is also experiencing significant growth, valued at approximately $15 billion in 2025, as the need for rigorous quality control at every stage of production intensifies. Steel Structural Parts also play a vital role, especially in heavier machinery and applications requiring extreme rigidity and shock absorption, with an estimated market value of $10 billion in 2025.

Semiconductor Equipment Structural Parts Product Developments

Recent product developments in semiconductor equipment structural parts are heavily influenced by the pursuit of enhanced precision, thermal stability, and reduced vibration. Innovations include the use of advanced aluminum alloys and specialized steel grades engineered for superior mechanical properties and reduced thermal expansion. Furthermore, manufacturers are focusing on the integration of damping technologies and sophisticated surface treatments to minimize particle generation and improve longevity. The increasing adoption of additive manufacturing for creating complex, lightweight, and optimized structural components for wafer handling systems and robotic arms is also a significant trend, offering customization and faster prototyping capabilities.

Challenges in the Semiconductor Equipment Structural Parts Market

The semiconductor equipment structural parts market faces several significant challenges. Supply chain disruptions, exacerbated by geopolitical tensions and material scarcity, can lead to significant lead time extensions and cost overruns, impacting the $50 billion market. Stringent quality control requirements and the need for ultra-high purity materials add complexity and expense to manufacturing processes. Intense competitive pressures from both established and emerging players can squeeze profit margins. Furthermore, the high capital investment required for specialized manufacturing equipment and R&D presents a substantial barrier to entry for new participants. The increasing complexity of semiconductor nodes, requiring ever-higher precision, also poses a challenge for maintaining existing infrastructure and developing new solutions within budget constraints.

Forces Driving Semiconductor Equipment Structural Parts Growth

Several powerful forces are driving the growth of the semiconductor equipment structural parts market. The relentless demand for advanced electronics across consumer, automotive, and industrial sectors necessitates continuous expansion and upgrading of semiconductor manufacturing capacity. The rapid evolution of technologies like AI, 5G, and autonomous driving creates a compounding demand for more powerful and specialized chips, directly translating into increased orders for sophisticated manufacturing equipment and its critical structural components. Government initiatives worldwide aimed at bolstering domestic semiconductor production and reducing reliance on foreign supply chains also act as significant catalysts. Furthermore, ongoing advancements in material science and manufacturing technologies are enabling the development of more efficient and cost-effective structural parts, further fueling market expansion.

Challenges in the Semiconductor Equipment Structural Parts Market

Long-term growth catalysts for the semiconductor equipment structural parts market lie in continued technological innovation and strategic market expansion. The ongoing miniaturization trend in semiconductor technology demands increasingly complex and precise structural components, pushing the boundaries of material science and manufacturing precision. Partnerships and collaborations between equipment manufacturers and structural parts suppliers are crucial for co-developing next-generation solutions. Emerging markets in Southeast Asia and India, with their growing ambitions in semiconductor manufacturing, present significant long-term growth opportunities. The development of modular and adaptable structural designs can also cater to evolving equipment needs and reduce time-to-market for new fabrication technologies.

Emerging Opportunities in Semiconductor Equipment Structural Parts

Emerging opportunities in the semiconductor equipment structural parts market are abundant. The growing adoption of heterogeneous integration and advanced packaging technologies presents new demands for specialized structural components in assembly and testing equipment. The increasing focus on sustainability and energy efficiency in semiconductor manufacturing is driving demand for lightweight and advanced material solutions that minimize energy consumption during operation. Furthermore, the expansion of the industrial IoT and smart manufacturing initiatives creates opportunities for intelligent structural components with integrated sensing capabilities for real-time performance monitoring and predictive maintenance. The potential for localized manufacturing of critical structural parts in key semiconductor-producing regions to enhance supply chain resilience is also a significant emerging trend.

Leading Players in the Semiconductor Equipment Structural Parts Sector

- Suzhou Huaya Intelligence Technology

- Dana Precision

- Precision Components

- Summit Steel & Manufacturing, Inc.

- Zhejiang Jiafeng Electrical & Mechanical

- Shenyang Fortune Precision Equipment

- Falcontech

Key Milestones in Semiconductor Equipment Structural Parts Industry

- 2019: Increased investment in advanced materials research for high-precision structural components.

- 2020: Emergence of additive manufacturing as a viable solution for complex structural parts, impacting prototyping and niche applications.

- 2021: Global chip shortage intensifies focus on supply chain resilience and domestic manufacturing of critical components.

- 2022: Significant R&D breakthroughs in aluminum alloys and specialized steels for enhanced thermal stability and rigidity.

- 2023: Growing demand for structural components that support next-generation lithography and advanced packaging technologies.

- 2024: Increased M&A activity as larger players aim to consolidate market share and expand technological capabilities.

Strategic Outlook for Semiconductor Equipment Structural Parts Market

The strategic outlook for the semiconductor equipment structural parts market is exceptionally positive, driven by sustained global demand for semiconductors and ongoing technological advancements. Key growth accelerators include the continued investment in advanced semiconductor manufacturing capacity by both established and emerging players, the increasing complexity of chip architectures requiring more sophisticated equipment, and the strong governmental support for semiconductor self-sufficiency globally. Future opportunities lie in developing innovative material solutions, embracing digital manufacturing technologies, and forging strategic partnerships to meet the evolving needs of the semiconductor industry. The market is expected to witness substantial growth as it underpins the very foundation of the digital economy.

Semiconductor Equipment Structural Parts Segmentation

-

1. Application

- 1.1. Wafer Manufacturing Equipment

- 1.2. Wafer Testing Equipment

-

2. Types

- 2.1. Aluminum Structural Parts

- 2.2. Steel Structural Parts

Semiconductor Equipment Structural Parts Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Semiconductor Equipment Structural Parts Regional Market Share

Geographic Coverage of Semiconductor Equipment Structural Parts

Semiconductor Equipment Structural Parts REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Semiconductor Equipment Structural Parts Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Wafer Manufacturing Equipment

- 5.1.2. Wafer Testing Equipment

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Aluminum Structural Parts

- 5.2.2. Steel Structural Parts

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Semiconductor Equipment Structural Parts Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Wafer Manufacturing Equipment

- 6.1.2. Wafer Testing Equipment

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Aluminum Structural Parts

- 6.2.2. Steel Structural Parts

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Semiconductor Equipment Structural Parts Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Wafer Manufacturing Equipment

- 7.1.2. Wafer Testing Equipment

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Aluminum Structural Parts

- 7.2.2. Steel Structural Parts

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Semiconductor Equipment Structural Parts Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Wafer Manufacturing Equipment

- 8.1.2. Wafer Testing Equipment

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Aluminum Structural Parts

- 8.2.2. Steel Structural Parts

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Semiconductor Equipment Structural Parts Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Wafer Manufacturing Equipment

- 9.1.2. Wafer Testing Equipment

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Aluminum Structural Parts

- 9.2.2. Steel Structural Parts

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Semiconductor Equipment Structural Parts Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Wafer Manufacturing Equipment

- 10.1.2. Wafer Testing Equipment

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Aluminum Structural Parts

- 10.2.2. Steel Structural Parts

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Suzhou Huaya Intelligence Technology

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Dana Precision

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Precision Components

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Summit Steel & Manufacturing

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Inc.

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Zhejiang Jiafeng Electrical & Mechanical

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Shenyang Fortune Precision Equipment

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Falcontech

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.1 Suzhou Huaya Intelligence Technology

List of Figures

- Figure 1: Global Semiconductor Equipment Structural Parts Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Semiconductor Equipment Structural Parts Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Semiconductor Equipment Structural Parts Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Semiconductor Equipment Structural Parts Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Semiconductor Equipment Structural Parts Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Semiconductor Equipment Structural Parts Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Semiconductor Equipment Structural Parts Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Semiconductor Equipment Structural Parts Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Semiconductor Equipment Structural Parts Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Semiconductor Equipment Structural Parts Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Semiconductor Equipment Structural Parts Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Semiconductor Equipment Structural Parts Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Semiconductor Equipment Structural Parts Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Semiconductor Equipment Structural Parts Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Semiconductor Equipment Structural Parts Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Semiconductor Equipment Structural Parts Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Semiconductor Equipment Structural Parts Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Semiconductor Equipment Structural Parts Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Semiconductor Equipment Structural Parts Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Semiconductor Equipment Structural Parts Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Semiconductor Equipment Structural Parts Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Semiconductor Equipment Structural Parts Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Semiconductor Equipment Structural Parts Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Semiconductor Equipment Structural Parts Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Semiconductor Equipment Structural Parts Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Semiconductor Equipment Structural Parts Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Semiconductor Equipment Structural Parts Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Semiconductor Equipment Structural Parts Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Semiconductor Equipment Structural Parts Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Semiconductor Equipment Structural Parts Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Semiconductor Equipment Structural Parts Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Semiconductor Equipment Structural Parts Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Semiconductor Equipment Structural Parts Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Semiconductor Equipment Structural Parts Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Semiconductor Equipment Structural Parts Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Semiconductor Equipment Structural Parts Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Semiconductor Equipment Structural Parts Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Semiconductor Equipment Structural Parts Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Semiconductor Equipment Structural Parts Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Semiconductor Equipment Structural Parts Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Semiconductor Equipment Structural Parts Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Semiconductor Equipment Structural Parts Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Semiconductor Equipment Structural Parts Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Semiconductor Equipment Structural Parts Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Semiconductor Equipment Structural Parts Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Semiconductor Equipment Structural Parts Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Semiconductor Equipment Structural Parts Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Semiconductor Equipment Structural Parts Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Semiconductor Equipment Structural Parts Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Semiconductor Equipment Structural Parts Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Equipment Structural Parts?

The projected CAGR is approximately 11%.

2. Which companies are prominent players in the Semiconductor Equipment Structural Parts?

Key companies in the market include Suzhou Huaya Intelligence Technology, Dana Precision, Precision Components, Summit Steel & Manufacturing, Inc., Zhejiang Jiafeng Electrical & Mechanical, Shenyang Fortune Precision Equipment, Falcontech.

3. What are the main segments of the Semiconductor Equipment Structural Parts?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 166.35 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Semiconductor Equipment Structural Parts," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Semiconductor Equipment Structural Parts report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Semiconductor Equipment Structural Parts?

To stay informed about further developments, trends, and reports in the Semiconductor Equipment Structural Parts, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence