Key Insights

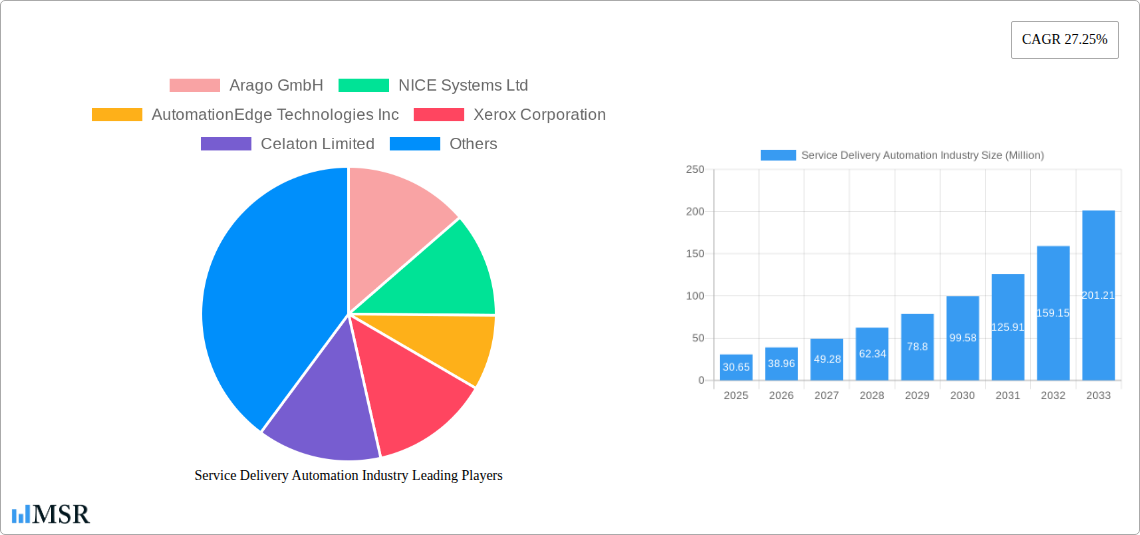

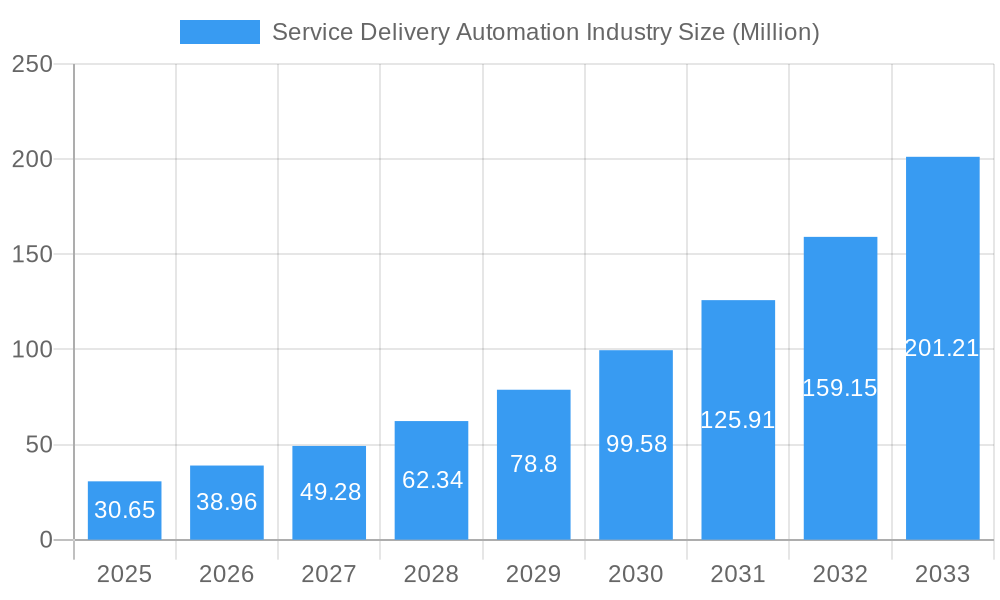

The Service Delivery Automation (SDA) market is experiencing explosive growth, projected to reach a substantial USD 30.65 million by 2025. This remarkable expansion is fueled by an impressive Compound Annual Growth Rate (CAGR) of 27.25% throughout the forecast period of 2025-2033. The primary drivers behind this surge are the increasing need for enhanced operational efficiency, significant cost reductions, and the growing demand for improved customer experiences across diverse industries. Organizations are actively adopting SDA solutions to automate repetitive, manual tasks, freeing up human capital for more strategic initiatives. This automation not only streamlines workflows but also minimizes errors, leading to higher productivity and better service delivery. The market's robust growth is further propelled by the accelerating digital transformation initiatives undertaken by businesses globally, pushing them to leverage advanced technologies for competitive advantage.

Service Delivery Automation Industry Market Size (In Million)

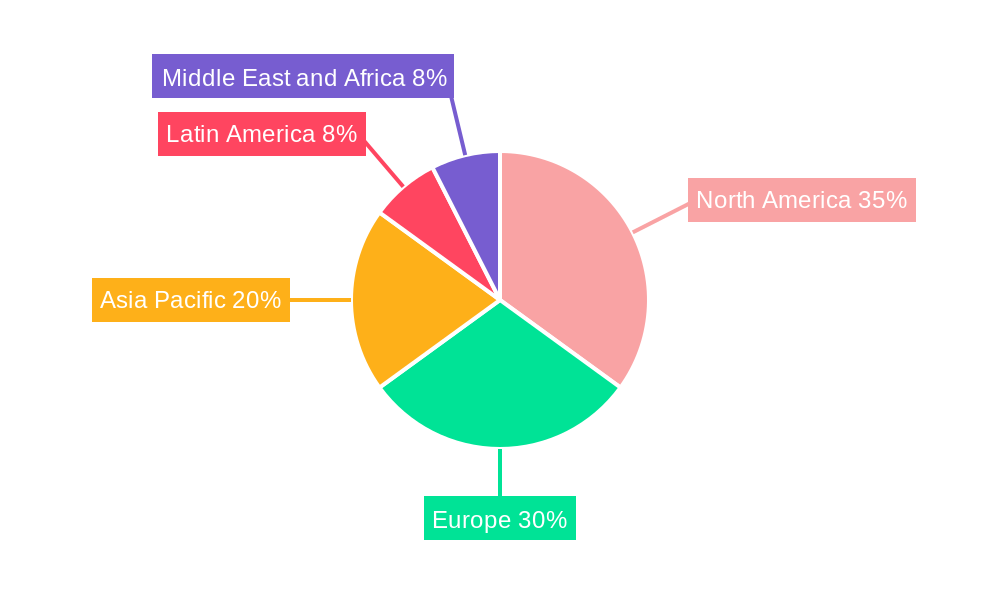

The SDA market is characterized by a dynamic segmentation, with IT Process Automation and Business Process Automation leading the charge. In terms of organization size, both Large Enterprises and Small & Medium Enterprises (SMEs) are significant adopters, indicating a broad market penetration. The adoption of SDA is widespread across critical end-user industries, including BFSI, IT, Telecommunication and Media, Hospitality and Transportation, Retail and Consumer Goods, Healthcare and Pharmaceuticals, Manufacturing and Logistics, and other emerging sectors. This broad application highlights the versatility and indispensable nature of SDA in modern business operations. The competitive landscape features prominent players such as Automation Anywhere Inc, UiPath SRL, Blue Prism, NICE Systems Ltd, and Accenture Inc, who are continuously innovating and expanding their offerings to cater to the evolving market demands. The global reach of SDA is evident, with North America and Europe currently holding significant market shares, while the Asia Pacific region is poised for substantial growth.

Service Delivery Automation Industry Company Market Share

Here is an SEO-optimized, engaging report description for the Service Delivery Automation Industry, incorporating all your specified details and adhering to the formatting and content requirements:

Unlock the future of operational efficiency with the definitive Service Delivery Automation (SDA) Industry Market Report. This comprehensive analysis delves into critical trends, market dynamics, and strategic imperatives shaping the global SDA landscape from 2019–2033. With a base year of 2025 and an extended forecast period of 2025–2033, this report provides invaluable insights for stakeholders seeking to capitalize on the accelerating adoption of automation technologies. Discover market size projections, growth drivers, technological disruptions, and emerging opportunities within IT Process Automation and Business Process Automation segments. Analyze key end-user industries including BFSI, IT, Telecommunication and Media, Hospitality and Transportation, Retail and Consumer Goods, Healthcare and Pharmaceuticals, Manufacturing and Logistics, and more.

Service Delivery Automation Industry Market Concentration & Dynamics

The Service Delivery Automation (SDA) industry is characterized by a dynamic market concentration, with a mix of established giants and agile innovators. Key players like Arago GmbH, NICE Systems Ltd, AutomationEdge Technologies Inc, Xerox Corporation, Celaton Limited, Automation Anywhere Inc, UiPath SRL, IPsoft Inc, Blue Prism, and Accenture Inc are actively shaping the competitive landscape. The innovation ecosystem is vibrant, fueled by continuous advancements in Artificial Intelligence (AI), Machine Learning (ML), and Robotic Process Automation (RPA). Regulatory frameworks, while evolving, are increasingly focused on data privacy and ethical AI implementation, influencing deployment strategies. Substitute products, such as manual processes and traditional IT service management tools, are steadily being displaced by more efficient SDA solutions. End-user trends highlight a strong demand for enhanced customer experience, cost optimization, and improved operational agility. Mergers and acquisitions (M&A) remain a significant activity, with an estimated 15 M&A deals in the historical period (2019-2024) aimed at consolidating market share and expanding technological capabilities. This activity underscores the industry's growth potential and the strategic importance of acquiring complementary technologies and customer bases.

Service Delivery Automation Industry Industry Insights & Trends

The Service Delivery Automation (SDA) industry is experiencing unprecedented growth, driven by the imperative for businesses to enhance efficiency, reduce operational costs, and elevate customer experiences. The global market size for SDA is projected to reach an estimated $75,000 Million by 2025, with a robust Compound Annual Growth Rate (CAGR) of approximately 22% during the forecast period of 2025–2033. Technological disruptions are at the forefront of this expansion. The integration of advanced AI and ML capabilities is enabling more sophisticated automation of complex tasks, moving beyond simple robotic process automation to intelligent automation. This evolution allows for predictive maintenance, proactive problem-solving, and personalized customer interactions, significantly transforming service delivery across various sectors. Evolving consumer behaviors, marked by higher expectations for instant gratification and seamless digital interactions, are compelling organizations to adopt SDA solutions to meet these demands. The shift towards hybrid and remote work models has further accelerated the need for automated processes to ensure continuity and productivity. The market is witnessing a surge in demand for cloud-based SDA solutions, offering scalability, flexibility, and cost-effectiveness, thereby democratizing access to advanced automation capabilities for Small & Medium Enterprises (SMEs) as well as Large Enterprises.

Key Markets & Segments Leading Service Delivery Automation Industry

The IT Process Automation segment is a dominant force within the Service Delivery Automation (SDA) industry, showcasing significant traction due to the inherent complexity and repetitive nature of IT operations. This dominance is propelled by the continuous need for IT departments to streamline workflows, enhance system reliability, and reduce downtime.

- IT Process Automation:

- Drivers: The escalating volume of IT infrastructure, the demand for faster incident resolution, and the imperative for enhanced cybersecurity are key drivers fueling growth in this segment.

- Dominance Analysis: IT departments across Large Enterprises are early and aggressive adopters, investing heavily in solutions that automate tasks such as server provisioning, patch management, and help desk operations. The sheer scale of IT operations in these organizations creates a strong business case for SDA.

The Business Process Automation segment, while distinct, is equally pivotal, driven by organizations' efforts to optimize core business functions beyond IT.

- Business Process Automation:

- Drivers: The pursuit of operational efficiency, cost reduction, improved compliance, and enhanced customer satisfaction are the primary accelerators for BPA adoption.

- Dominance Analysis: This segment sees significant adoption across all End-user Industries, but notably in BFSI and Retail and Consumer Goods. In BFSI, automation is crucial for fraud detection, loan processing, and customer onboarding. Retail and Consumer Goods leverage it for inventory management, order fulfillment, and personalized marketing campaigns.

Organization Size: While Large Enterprises have historically led adoption due to larger budgets and more complex needs, Small & Medium Enterprises (SMEs) are increasingly embracing SDA, driven by more accessible cloud-based solutions and the need to compete with larger players.

End-user Industry Dominance:

- BFSI: Leads due to stringent regulatory requirements, the need for robust security, and the high volume of transactional data requiring efficient processing.

- IT: As discussed, IT process automation is fundamental to the functioning of any tech-reliant organization.

- Telecommunication and Media: These sectors benefit from automation in customer service, network management, and content delivery optimization.

- Healthcare and Pharmaceuticals: Demonstrates growing adoption for administrative tasks, patient record management, and drug discovery research automation.

- Manufacturing and Logistics: Automation enhances supply chain visibility, production scheduling, and warehouse management.

Service Delivery Automation Industry Product Developments

Product developments in the Service Delivery Automation (SDA) industry are heavily focused on enhancing intelligence and seamless integration. Recent innovations emphasize the integration of advanced AI and ML capabilities to automate more complex decision-making processes. For instance, new solutions are enabling low-code/no-code environments for building sophisticated automation workflows, democratizing access for citizen developers. The market relevance is amplified by features that improve self-healing capabilities in IT systems, proactive anomaly detection, and hyper-personalization of customer interactions. This continuous stream of product innovation, driven by companies like UiPath and NICE Systems, provides businesses with a competitive edge by significantly reducing manual effort and accelerating the delivery of services.

Challenges in the Service Delivery Automation Industry Market

Despite its robust growth, the Service Delivery Automation (SDA) industry faces several challenges. One significant restraint is the complexity of integrating SDA solutions with legacy IT systems, often leading to substantial implementation costs and timelines. Another hurdle is the pervasive shortage of skilled professionals capable of designing, deploying, and managing these advanced automation platforms, estimated to create a talent gap impacting an estimated 25% of potential projects. Furthermore, concerns around data security and privacy, particularly with the increasing use of AI, require stringent adherence to evolving regulatory frameworks, potentially increasing compliance burdens. Competitive pressures also necessitate continuous innovation, demanding significant R&D investments from players in the market.

Forces Driving Service Delivery Automation Industry Growth

The Service Delivery Automation (SDA) industry is propelled by a confluence of powerful forces. The relentless pursuit of operational efficiency and cost reduction remains a primary driver, as organizations strive to do more with less. Technological advancements, particularly in Artificial Intelligence (AI), Machine Learning (ML), and Robotic Process Automation (RPA), are continuously expanding the scope and sophistication of automatable tasks. The growing demand for enhanced customer experiences, characterized by speed, personalization, and omnichannel consistency, is compelling businesses to adopt SDA for service improvement. Furthermore, the increasing adoption of cloud computing provides a scalable and accessible platform for SDA solutions, democratizing their availability for businesses of all sizes.

Challenges in the Service Delivery Automation Industry Market

Long-term growth catalysts in the Service Delivery Automation (SDA) industry are deeply rooted in continued innovation and strategic market expansion. The ongoing development of AI-powered capabilities, enabling SDA to handle more complex, cognitive tasks, will be a significant growth enabler. Partnerships and collaborations between technology providers, system integrators, and consulting firms are crucial for developing end-to-end solutions and expanding market reach. Furthermore, the growing trend of digital transformation initiatives across all industries will continue to create a sustained demand for SDA solutions. As organizations mature in their automation journey, the focus will shift towards intelligent automation and hyperautomation, unlocking new levels of efficiency and competitive advantage.

Emerging Opportunities in Service Delivery Automation Industry

Emerging opportunities in the Service Delivery Automation (SDA) industry are vast and varied. The expansion of SDA into new verticals, such as the Internet of Things (IoT) and edge computing, presents significant growth potential. The increasing focus on sustainable business practices also opens avenues for SDA to optimize resource utilization and reduce environmental impact. Moreover, the growing demand for personalized services across sectors like healthcare and education creates opportunities for highly targeted and adaptive automation solutions. The continued evolution of conversational AI and intelligent chatbots is poised to revolutionize customer service delivery, creating a more intuitive and engaging user experience.

Leading Players in the Service Delivery Automation Industry Sector

- Arago GmbH

- NICE Systems Ltd

- AutomationEdge Technologies Inc

- Xerox Corporation

- Celaton Limited

- Automation Anywhere Inc

- UiPath SRL

- IPsoft Inc

- Blue Prism

- Accenture Inc

Key Milestones in Service Delivery Automation Industry Industry

- March 2023: UiPath announced seamless integration of new machine learning models into business processes using Amazon SageMaker, eliminating intricate coding and manual labor for data science teams, thereby speeding up innovation and reducing experimentation costs.

- January 2023: NICE and Cognizant forged a partnership to unlock growth opportunities in Customer Experience (CX), Workforce Management (WFM), and digital transformation, offering a comprehensive approach to elevate customer and agent experiences through a unified CCaaS suite.

Strategic Outlook for Service Delivery Automation Industry Market

The strategic outlook for the Service Delivery Automation (SDA) industry is exceptionally positive, driven by the persistent need for digital transformation and operational excellence. Future growth accelerators will involve deeper integration of AI and ML for hyperautomation, enabling autonomous processes and intelligent decision-making. Strategic opportunities lie in expanding the application of SDA across the entire enterprise value chain, not just IT and back-office functions. The increasing adoption of industry-specific SDA solutions, tailored to the unique needs of sectors like healthcare and finance, will further propel market expansion. Furthermore, the development of more advanced analytics capabilities within SDA platforms will empower organizations with deeper insights into their operations, facilitating continuous improvement and driving long-term competitive advantage.

Service Delivery Automation Industry Segmentation

-

1. Type

- 1.1. IT Process Automation

- 1.2. Business Process Automation

-

2. Organization Size

- 2.1. Large Enterprises

- 2.2. Small & Medium Enterprises (SMEs)

-

3. End-user Industry

- 3.1. BFSI

- 3.2. IT

- 3.3. Telecommunication and Media

- 3.4. Hospitality and Transportation

- 3.5. Retail and Consumer Goods

- 3.6. Healthcare and Pharmaceuticals

- 3.7. Manufacturing and Logistics

- 3.8. Other End-User Industries

Service Delivery Automation Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Service Delivery Automation Industry Regional Market Share

Geographic Coverage of Service Delivery Automation Industry

Service Delivery Automation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 27.25% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Need for Operational Efficiency; Cost-cutting Across Industries

- 3.3. Market Restrains

- 3.3.1. Lack of Skilled Personnel

- 3.4. Market Trends

- 3.4.1. Retail and Consumer Goods to Dominate the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Service Delivery Automation Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. IT Process Automation

- 5.1.2. Business Process Automation

- 5.2. Market Analysis, Insights and Forecast - by Organization Size

- 5.2.1. Large Enterprises

- 5.2.2. Small & Medium Enterprises (SMEs)

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. BFSI

- 5.3.2. IT

- 5.3.3. Telecommunication and Media

- 5.3.4. Hospitality and Transportation

- 5.3.5. Retail and Consumer Goods

- 5.3.6. Healthcare and Pharmaceuticals

- 5.3.7. Manufacturing and Logistics

- 5.3.8. Other End-User Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Latin America

- 5.4.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Service Delivery Automation Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. IT Process Automation

- 6.1.2. Business Process Automation

- 6.2. Market Analysis, Insights and Forecast - by Organization Size

- 6.2.1. Large Enterprises

- 6.2.2. Small & Medium Enterprises (SMEs)

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. BFSI

- 6.3.2. IT

- 6.3.3. Telecommunication and Media

- 6.3.4. Hospitality and Transportation

- 6.3.5. Retail and Consumer Goods

- 6.3.6. Healthcare and Pharmaceuticals

- 6.3.7. Manufacturing and Logistics

- 6.3.8. Other End-User Industries

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Europe Service Delivery Automation Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. IT Process Automation

- 7.1.2. Business Process Automation

- 7.2. Market Analysis, Insights and Forecast - by Organization Size

- 7.2.1. Large Enterprises

- 7.2.2. Small & Medium Enterprises (SMEs)

- 7.3. Market Analysis, Insights and Forecast - by End-user Industry

- 7.3.1. BFSI

- 7.3.2. IT

- 7.3.3. Telecommunication and Media

- 7.3.4. Hospitality and Transportation

- 7.3.5. Retail and Consumer Goods

- 7.3.6. Healthcare and Pharmaceuticals

- 7.3.7. Manufacturing and Logistics

- 7.3.8. Other End-User Industries

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Asia Pacific Service Delivery Automation Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. IT Process Automation

- 8.1.2. Business Process Automation

- 8.2. Market Analysis, Insights and Forecast - by Organization Size

- 8.2.1. Large Enterprises

- 8.2.2. Small & Medium Enterprises (SMEs)

- 8.3. Market Analysis, Insights and Forecast - by End-user Industry

- 8.3.1. BFSI

- 8.3.2. IT

- 8.3.3. Telecommunication and Media

- 8.3.4. Hospitality and Transportation

- 8.3.5. Retail and Consumer Goods

- 8.3.6. Healthcare and Pharmaceuticals

- 8.3.7. Manufacturing and Logistics

- 8.3.8. Other End-User Industries

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Latin America Service Delivery Automation Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. IT Process Automation

- 9.1.2. Business Process Automation

- 9.2. Market Analysis, Insights and Forecast - by Organization Size

- 9.2.1. Large Enterprises

- 9.2.2. Small & Medium Enterprises (SMEs)

- 9.3. Market Analysis, Insights and Forecast - by End-user Industry

- 9.3.1. BFSI

- 9.3.2. IT

- 9.3.3. Telecommunication and Media

- 9.3.4. Hospitality and Transportation

- 9.3.5. Retail and Consumer Goods

- 9.3.6. Healthcare and Pharmaceuticals

- 9.3.7. Manufacturing and Logistics

- 9.3.8. Other End-User Industries

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Middle East and Africa Service Delivery Automation Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. IT Process Automation

- 10.1.2. Business Process Automation

- 10.2. Market Analysis, Insights and Forecast - by Organization Size

- 10.2.1. Large Enterprises

- 10.2.2. Small & Medium Enterprises (SMEs)

- 10.3. Market Analysis, Insights and Forecast - by End-user Industry

- 10.3.1. BFSI

- 10.3.2. IT

- 10.3.3. Telecommunication and Media

- 10.3.4. Hospitality and Transportation

- 10.3.5. Retail and Consumer Goods

- 10.3.6. Healthcare and Pharmaceuticals

- 10.3.7. Manufacturing and Logistics

- 10.3.8. Other End-User Industries

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Arago GmbH

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 NICE Systems Ltd

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 AutomationEdge Technologies Inc

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Xerox Corporation

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Celaton Limited

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Automation Anywhere Inc

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Uipath SRL

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 IPsoft Inc

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Blue Prism

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Accenture Inc

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Arago GmbH

List of Figures

- Figure 1: Global Service Delivery Automation Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Service Delivery Automation Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Service Delivery Automation Industry Revenue (Million), by Type 2025 & 2033

- Figure 4: North America Service Delivery Automation Industry Volume (K Unit), by Type 2025 & 2033

- Figure 5: North America Service Delivery Automation Industry Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Service Delivery Automation Industry Volume Share (%), by Type 2025 & 2033

- Figure 7: North America Service Delivery Automation Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 8: North America Service Delivery Automation Industry Volume (K Unit), by Organization Size 2025 & 2033

- Figure 9: North America Service Delivery Automation Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 10: North America Service Delivery Automation Industry Volume Share (%), by Organization Size 2025 & 2033

- Figure 11: North America Service Delivery Automation Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 12: North America Service Delivery Automation Industry Volume (K Unit), by End-user Industry 2025 & 2033

- Figure 13: North America Service Delivery Automation Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 14: North America Service Delivery Automation Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 15: North America Service Delivery Automation Industry Revenue (Million), by Country 2025 & 2033

- Figure 16: North America Service Delivery Automation Industry Volume (K Unit), by Country 2025 & 2033

- Figure 17: North America Service Delivery Automation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: North America Service Delivery Automation Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: Europe Service Delivery Automation Industry Revenue (Million), by Type 2025 & 2033

- Figure 20: Europe Service Delivery Automation Industry Volume (K Unit), by Type 2025 & 2033

- Figure 21: Europe Service Delivery Automation Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: Europe Service Delivery Automation Industry Volume Share (%), by Type 2025 & 2033

- Figure 23: Europe Service Delivery Automation Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 24: Europe Service Delivery Automation Industry Volume (K Unit), by Organization Size 2025 & 2033

- Figure 25: Europe Service Delivery Automation Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 26: Europe Service Delivery Automation Industry Volume Share (%), by Organization Size 2025 & 2033

- Figure 27: Europe Service Delivery Automation Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 28: Europe Service Delivery Automation Industry Volume (K Unit), by End-user Industry 2025 & 2033

- Figure 29: Europe Service Delivery Automation Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: Europe Service Delivery Automation Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 31: Europe Service Delivery Automation Industry Revenue (Million), by Country 2025 & 2033

- Figure 32: Europe Service Delivery Automation Industry Volume (K Unit), by Country 2025 & 2033

- Figure 33: Europe Service Delivery Automation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Europe Service Delivery Automation Industry Volume Share (%), by Country 2025 & 2033

- Figure 35: Asia Pacific Service Delivery Automation Industry Revenue (Million), by Type 2025 & 2033

- Figure 36: Asia Pacific Service Delivery Automation Industry Volume (K Unit), by Type 2025 & 2033

- Figure 37: Asia Pacific Service Delivery Automation Industry Revenue Share (%), by Type 2025 & 2033

- Figure 38: Asia Pacific Service Delivery Automation Industry Volume Share (%), by Type 2025 & 2033

- Figure 39: Asia Pacific Service Delivery Automation Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 40: Asia Pacific Service Delivery Automation Industry Volume (K Unit), by Organization Size 2025 & 2033

- Figure 41: Asia Pacific Service Delivery Automation Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 42: Asia Pacific Service Delivery Automation Industry Volume Share (%), by Organization Size 2025 & 2033

- Figure 43: Asia Pacific Service Delivery Automation Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 44: Asia Pacific Service Delivery Automation Industry Volume (K Unit), by End-user Industry 2025 & 2033

- Figure 45: Asia Pacific Service Delivery Automation Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 46: Asia Pacific Service Delivery Automation Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 47: Asia Pacific Service Delivery Automation Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: Asia Pacific Service Delivery Automation Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Asia Pacific Service Delivery Automation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Asia Pacific Service Delivery Automation Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Latin America Service Delivery Automation Industry Revenue (Million), by Type 2025 & 2033

- Figure 52: Latin America Service Delivery Automation Industry Volume (K Unit), by Type 2025 & 2033

- Figure 53: Latin America Service Delivery Automation Industry Revenue Share (%), by Type 2025 & 2033

- Figure 54: Latin America Service Delivery Automation Industry Volume Share (%), by Type 2025 & 2033

- Figure 55: Latin America Service Delivery Automation Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 56: Latin America Service Delivery Automation Industry Volume (K Unit), by Organization Size 2025 & 2033

- Figure 57: Latin America Service Delivery Automation Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 58: Latin America Service Delivery Automation Industry Volume Share (%), by Organization Size 2025 & 2033

- Figure 59: Latin America Service Delivery Automation Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 60: Latin America Service Delivery Automation Industry Volume (K Unit), by End-user Industry 2025 & 2033

- Figure 61: Latin America Service Delivery Automation Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 62: Latin America Service Delivery Automation Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 63: Latin America Service Delivery Automation Industry Revenue (Million), by Country 2025 & 2033

- Figure 64: Latin America Service Delivery Automation Industry Volume (K Unit), by Country 2025 & 2033

- Figure 65: Latin America Service Delivery Automation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 66: Latin America Service Delivery Automation Industry Volume Share (%), by Country 2025 & 2033

- Figure 67: Middle East and Africa Service Delivery Automation Industry Revenue (Million), by Type 2025 & 2033

- Figure 68: Middle East and Africa Service Delivery Automation Industry Volume (K Unit), by Type 2025 & 2033

- Figure 69: Middle East and Africa Service Delivery Automation Industry Revenue Share (%), by Type 2025 & 2033

- Figure 70: Middle East and Africa Service Delivery Automation Industry Volume Share (%), by Type 2025 & 2033

- Figure 71: Middle East and Africa Service Delivery Automation Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 72: Middle East and Africa Service Delivery Automation Industry Volume (K Unit), by Organization Size 2025 & 2033

- Figure 73: Middle East and Africa Service Delivery Automation Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 74: Middle East and Africa Service Delivery Automation Industry Volume Share (%), by Organization Size 2025 & 2033

- Figure 75: Middle East and Africa Service Delivery Automation Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 76: Middle East and Africa Service Delivery Automation Industry Volume (K Unit), by End-user Industry 2025 & 2033

- Figure 77: Middle East and Africa Service Delivery Automation Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 78: Middle East and Africa Service Delivery Automation Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 79: Middle East and Africa Service Delivery Automation Industry Revenue (Million), by Country 2025 & 2033

- Figure 80: Middle East and Africa Service Delivery Automation Industry Volume (K Unit), by Country 2025 & 2033

- Figure 81: Middle East and Africa Service Delivery Automation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 82: Middle East and Africa Service Delivery Automation Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Service Delivery Automation Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Global Service Delivery Automation Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 3: Global Service Delivery Automation Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 4: Global Service Delivery Automation Industry Volume K Unit Forecast, by Organization Size 2020 & 2033

- Table 5: Global Service Delivery Automation Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 6: Global Service Delivery Automation Industry Volume K Unit Forecast, by End-user Industry 2020 & 2033

- Table 7: Global Service Delivery Automation Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Global Service Delivery Automation Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: Global Service Delivery Automation Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 10: Global Service Delivery Automation Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 11: Global Service Delivery Automation Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 12: Global Service Delivery Automation Industry Volume K Unit Forecast, by Organization Size 2020 & 2033

- Table 13: Global Service Delivery Automation Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 14: Global Service Delivery Automation Industry Volume K Unit Forecast, by End-user Industry 2020 & 2033

- Table 15: Global Service Delivery Automation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Service Delivery Automation Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: Global Service Delivery Automation Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 18: Global Service Delivery Automation Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 19: Global Service Delivery Automation Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 20: Global Service Delivery Automation Industry Volume K Unit Forecast, by Organization Size 2020 & 2033

- Table 21: Global Service Delivery Automation Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 22: Global Service Delivery Automation Industry Volume K Unit Forecast, by End-user Industry 2020 & 2033

- Table 23: Global Service Delivery Automation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Global Service Delivery Automation Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: Global Service Delivery Automation Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 26: Global Service Delivery Automation Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 27: Global Service Delivery Automation Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 28: Global Service Delivery Automation Industry Volume K Unit Forecast, by Organization Size 2020 & 2033

- Table 29: Global Service Delivery Automation Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 30: Global Service Delivery Automation Industry Volume K Unit Forecast, by End-user Industry 2020 & 2033

- Table 31: Global Service Delivery Automation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 32: Global Service Delivery Automation Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 33: Global Service Delivery Automation Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 34: Global Service Delivery Automation Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 35: Global Service Delivery Automation Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 36: Global Service Delivery Automation Industry Volume K Unit Forecast, by Organization Size 2020 & 2033

- Table 37: Global Service Delivery Automation Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 38: Global Service Delivery Automation Industry Volume K Unit Forecast, by End-user Industry 2020 & 2033

- Table 39: Global Service Delivery Automation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 40: Global Service Delivery Automation Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 41: Global Service Delivery Automation Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 42: Global Service Delivery Automation Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 43: Global Service Delivery Automation Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 44: Global Service Delivery Automation Industry Volume K Unit Forecast, by Organization Size 2020 & 2033

- Table 45: Global Service Delivery Automation Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 46: Global Service Delivery Automation Industry Volume K Unit Forecast, by End-user Industry 2020 & 2033

- Table 47: Global Service Delivery Automation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 48: Global Service Delivery Automation Industry Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Service Delivery Automation Industry?

The projected CAGR is approximately 27.25%.

2. Which companies are prominent players in the Service Delivery Automation Industry?

Key companies in the market include Arago GmbH, NICE Systems Ltd, AutomationEdge Technologies Inc, Xerox Corporation, Celaton Limited, Automation Anywhere Inc, Uipath SRL, IPsoft Inc, Blue Prism, Accenture Inc.

3. What are the main segments of the Service Delivery Automation Industry?

The market segments include Type, Organization Size, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 30.65 Million as of 2022.

5. What are some drivers contributing to market growth?

Need for Operational Efficiency; Cost-cutting Across Industries.

6. What are the notable trends driving market growth?

Retail and Consumer Goods to Dominate the Market.

7. Are there any restraints impacting market growth?

Lack of Skilled Personnel.

8. Can you provide examples of recent developments in the market?

March 2023: UiPath announced that data science teams who use Amazon SageMaker, an end-to-end machine learning (ML) service, can now integrate new machine learning models into business processes seamlessly and quickly with UiPath without intricate coding or manual labor. By automating deployment pipelines, data scientists, ML engineers, and business analysts can decrease the cost of experimentation and speed up innovation.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Service Delivery Automation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Service Delivery Automation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Service Delivery Automation Industry?

To stay informed about further developments, trends, and reports in the Service Delivery Automation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence