Key Insights

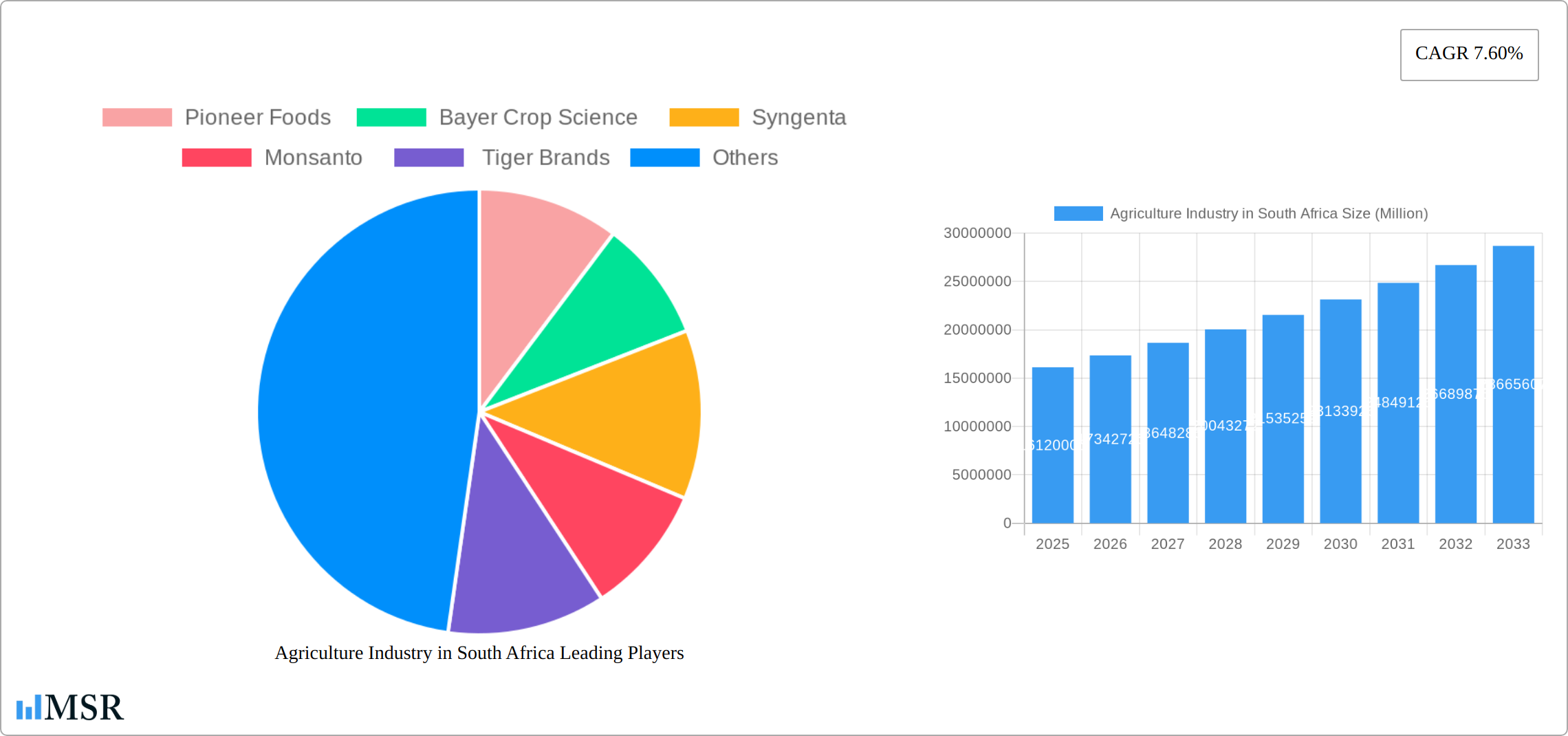

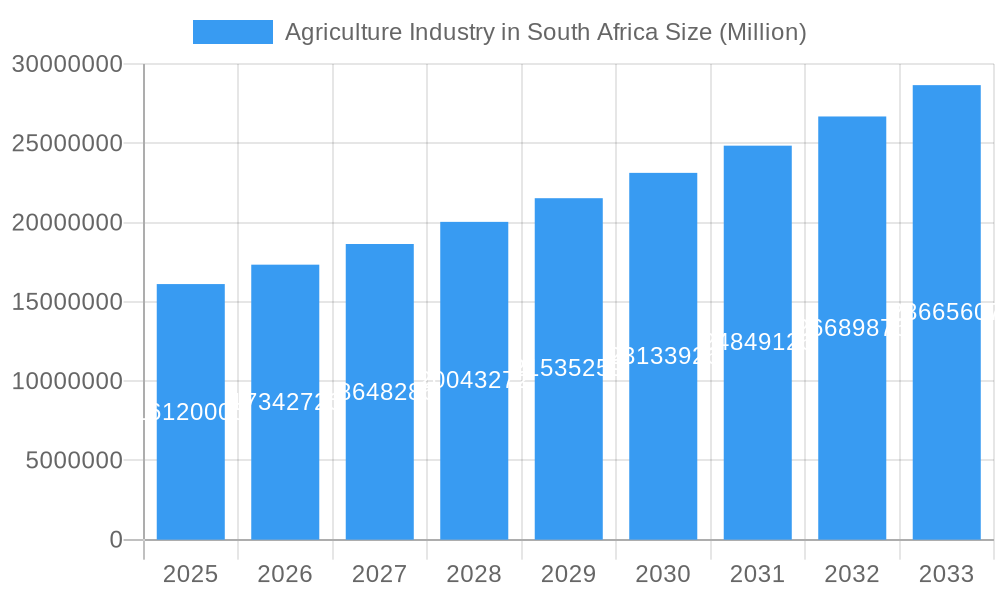

The South African agricultural industry, valued at $16.12 million in 2025, is projected to experience robust growth, driven by a Compound Annual Growth Rate (CAGR) of 7.60% from 2025 to 2033. This expansion is fueled by several key factors. Increasing global demand for food and agricultural products, coupled with South Africa's favorable climate and arable land, creates a significant opportunity for growth. Furthermore, government initiatives supporting agricultural modernization and technological advancements, such as precision farming and improved irrigation techniques, are contributing to increased productivity and efficiency. The cultivation of cereals, fruits, vegetables, and oilseeds comprises the primary segments, with cereals likely holding the largest market share due to their wide consumption and use in various food processing industries. Major players like Pioneer Foods, Bayer Crop Science, Syngenta, Monsanto, and Tiger Brands are actively shaping the market landscape through innovation and strategic investments. However, challenges remain, including water scarcity in certain regions, climate change impacts on crop yields, and infrastructure limitations that affect efficient distribution. Overcoming these restraints is crucial for sustained growth and ensuring food security within the country.

Agriculture Industry in South Africa Market Size (In Million)

The industry's future depends on the successful navigation of these challenges and the continued adoption of sustainable agricultural practices. This includes investing in research and development to develop drought-resistant crops, optimizing water management techniques, and improving access to financing for smallholder farmers. Expansion into value-added agricultural products and leveraging export opportunities in African and international markets will be key strategies for future success. The concentration of key players suggests a relatively consolidated market, yet opportunities for niche players and specialized agricultural services remain. The growth in specific crop segments will likely vary, with fruits and vegetables potentially experiencing higher growth due to evolving dietary habits and increasing health consciousness. Continued monitoring of global market trends and proactive adaptation to changing environmental conditions will be critical for sustained success within the South African agricultural sector.

Agriculture Industry in South Africa Company Market Share

South Africa Agriculture Industry Report: 2019-2033 Forecast

This comprehensive report provides a detailed analysis of the South African agriculture industry, covering the period 2019-2033, with a focus on the year 2025. It offers invaluable insights into market dynamics, key players, growth drivers, and emerging opportunities for stakeholders, investors, and industry professionals. The report leverages extensive research to provide actionable strategies for navigating this dynamic sector.

Agriculture Industry in South Africa Market Concentration & Dynamics

This section analyzes the competitive landscape of South Africa's agriculture industry, focusing on market concentration, innovation, regulations, and mergers & acquisitions (M&A). The historical period (2019-2024) showed a moderately concentrated market, with the top five players – Pioneer Foods, Bayer Crop Science, Syngenta, Monsanto, and Tiger Brands – holding an estimated xx% market share collectively in 2024. The estimated market size in 2025 is ZAR xx Million.

- Market Concentration: The Herfindahl-Hirschman Index (HHI) for 2024 is estimated at xx, suggesting a moderately concentrated market.

- Innovation Ecosystem: Investment in agricultural technology and research & development (R&D) is growing, driven by government initiatives and private sector investment.

- Regulatory Framework: The South African government's policies and regulations significantly influence the industry, including land reform and export regulations.

- Substitute Products: The availability of imported agricultural products presents competitive pressure on local producers.

- End-User Trends: Shifting consumer preferences towards healthier and sustainably produced food are shaping the demand.

- M&A Activities: The number of M&A deals in the South African agriculture sector between 2019 and 2024 totaled approximately xx, indicating moderate consolidation.

Agriculture Industry in South Africa Industry Insights & Trends

This section delves into the key trends and drivers shaping the South African agricultural landscape. The market witnessed robust growth between 2019 and 2024, with an estimated CAGR of xx%. This positive trend is projected to continue, with the market size anticipated to reach ZAR xx Million by 2025 and ZAR xx Million by 2033. Growth is primarily driven by increasing domestic demand, favorable government policies, and technological advancements in farming practices. Technological disruptions, such as precision agriculture and data analytics, are transforming farm operations and improving efficiency. Evolving consumer preferences towards organic and locally sourced products are creating new market opportunities. Climate change remains a significant challenge, impacting yields and productivity.

Key Markets & Segments Leading Agriculture Industry in South Africa

This section analyzes the dominant segments within the South African agriculture industry. Cereals remain the largest segment, followed by fruits, vegetables, and oilseeds.

- Cereals: This segment dominates, driven by high domestic consumption and export opportunities. Key drivers include increasing population, rising disposable incomes, and government support for cereal production.

- Fruits: Growth in the fruit segment is influenced by export demand, particularly for citrus fruits. Investment in infrastructure and improved farming techniques are key factors.

- Vegetables: The vegetable segment demonstrates steady growth, driven by increasing health consciousness and demand for fresh produce.

- Oilseeds: The oilseeds segment exhibits moderate growth, driven by both domestic and international demand for vegetable oils.

Dominance Analysis: The dominance of cereals is attributed to established supply chains, strong government support, and consistent demand both domestically and internationally.

Agriculture Industry in South Africa Product Developments

Technological advancements are driving product innovation, with a focus on improved crop yields, disease resistance, and reduced reliance on chemical inputs. Precision agriculture technologies, including GPS-guided machinery and sensor-based monitoring systems, are enhancing efficiency and sustainability. The development of drought-resistant and pest-resistant crop varieties is crucial in mitigating climate change impacts. These innovations provide a significant competitive advantage for South African agricultural producers.

Challenges in the Agriculture Industry in South Africa Market

The South African agricultural sector faces a complex web of interconnected challenges that significantly impact its productivity and overall contribution to the national economy. These challenges are not isolated incidents but rather systemic issues requiring multifaceted solutions.

- Water scarcity and insecurity: Erratic rainfall patterns and inefficient water management practices lead to chronic water shortages, severely impacting crop yields and livestock production. This is exacerbated by aging infrastructure and a lack of investment in water-wise agricultural technologies.

- Land reform complexities: The ongoing land reform process, while aiming for equitable land distribution, continues to present challenges related to land ownership, tenure security, and agricultural productivity. Ensuring efficient and sustainable land management within this evolving context is paramount.

- Supply chain inefficiencies and infrastructure deficits: Poor infrastructure, including inadequate transportation networks and storage facilities, leads to post-harvest losses and increased production costs. This hinders the efficient distribution of agricultural products to both domestic and international markets.

- Climate change vulnerability: South Africa's agriculture sector is highly vulnerable to the impacts of climate change, with extreme weather events such as droughts, floods, and heatwaves becoming more frequent and intense. This necessitates the adoption of climate-smart agricultural practices and resilient crop varieties.

- Input costs and market volatility: Fluctuations in the prices of fertilizers, pesticides, and fuel, combined with volatile global commodity markets, create significant uncertainty and financial risks for farmers.

These combined challenges contribute to a substantial reduction in potential agricultural output, hindering economic growth and food security. Precise quantification of this reduction requires further detailed analysis, but the impact is undeniably significant.

Forces Driving Agriculture Industry in South Africa Growth

Key growth drivers include:

- Government support: Government initiatives, including subsidies and investments in infrastructure, stimulate growth.

- Technological advancements: Precision agriculture and biotechnology are enhancing productivity.

- Growing domestic demand: A rising population and increased disposable incomes fuel demand for agricultural products.

- Export opportunities: South Africa has significant export potential for various agricultural products.

Long-Term Growth Catalysts in Agriculture Industry in South Africa

Long-term growth hinges on continued investment in research and development, fostering public-private partnerships to enhance technological capabilities, and expanding into new export markets. Focus on sustainable farming practices and climate-resilient agriculture are crucial for long-term sustainability.

Emerging Opportunities in Agriculture Industry in South Africa

Despite the challenges, the South African agricultural sector presents a range of exciting opportunities for growth and development. A strategic focus on these areas can unlock significant potential:

- Growing demand for organic and sustainably produced food: Increasing consumer awareness of health and environmental issues is driving strong demand for organic and sustainably produced agricultural products, both domestically and internationally. This presents a lucrative market niche for producers who can meet these stringent standards.

- Agri-tourism and rural development: The development of agri-tourism ventures offers significant potential for diversification and income generation, particularly in rural communities. This can create jobs, attract investment, and promote rural development.

- Value addition and processing: Moving beyond primary production and focusing on value-added products can significantly enhance profitability and create higher-value export opportunities. This includes processing, packaging, and branding of agricultural goods.

- Technological advancements: Precision agriculture, using technologies like GPS, sensors, and data analytics, can optimize resource use, improve yields, and reduce environmental impact. Investment in research and development in this area is crucial.

- Export market diversification: Exploring new export markets and strengthening existing relationships can help reduce reliance on a few key export destinations and improve market access.

Leading Players in the Agriculture Industry in South Africa Sector

Key Milestones in Agriculture Industry in South Africa Industry

- 2020: Launch of the National Agricultural Policy, a crucial step in setting a strategic direction for the sector's development and transformation. This policy aims to address many of the challenges outlined above.

- 2022: Significant investments in irrigation infrastructure represent a positive step towards improving water security and enhancing agricultural productivity in water-stressed regions. However, ongoing investment and maintenance are essential for long-term success.

- 2023: Introduction of new drought-resistant maize varieties demonstrates the ongoing efforts to develop climate-resilient crops, crucial for adapting to the changing climate.

- Ongoing initiatives: Numerous other initiatives are underway, including programs focused on farmer support, skills development, and market access, which contribute to the overall progress of the sector.

Strategic Outlook for Agriculture Industry in South Africa Market

The South African agriculture industry holds significant untapped potential for growth and economic contribution. Realizing this potential requires a concerted effort across various stakeholders, including government, the private sector, and research institutions. Strategic investments in sustainable agricultural practices, technological innovation, improved infrastructure, and effective policy implementation are crucial. A focus on value-added products, export market diversification, and building resilience to climate change will be key to ensuring the long-term competitiveness and sustainability of the South African agricultural sector. Furthermore, addressing the systemic challenges outlined above is vital for unlocking the full potential of this vital sector.

Agriculture Industry in South Africa Segmentation

-

1. Crop Type

- 1.1. Cereals

- 1.2. Fruits

- 1.3. Vegetables

- 1.4. Oilseeds

-

2. Crop Type

- 2.1. Cereals

- 2.2. Fruits

- 2.3. Vegetables

- 2.4. Oilseeds

Agriculture Industry in South Africa Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Agriculture Industry in South Africa Regional Market Share

Geographic Coverage of Agriculture Industry in South Africa

Agriculture Industry in South Africa REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.60% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Crop Type

- 5.1.1. Cereals

- 5.1.2. Fruits

- 5.1.3. Vegetables

- 5.1.4. Oilseeds

- 5.2. Market Analysis, Insights and Forecast - by Crop Type

- 5.2.1. Cereals

- 5.2.2. Fruits

- 5.2.3. Vegetables

- 5.2.4. Oilseeds

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Crop Type

- 6. Global Agriculture Industry in South Africa Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Crop Type

- 6.1.1. Cereals

- 6.1.2. Fruits

- 6.1.3. Vegetables

- 6.1.4. Oilseeds

- 6.2. Market Analysis, Insights and Forecast - by Crop Type

- 6.2.1. Cereals

- 6.2.2. Fruits

- 6.2.3. Vegetables

- 6.2.4. Oilseeds

- 6.1. Market Analysis, Insights and Forecast - by Crop Type

- 7. North America Agriculture Industry in South Africa Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Crop Type

- 7.1.1. Cereals

- 7.1.2. Fruits

- 7.1.3. Vegetables

- 7.1.4. Oilseeds

- 7.2. Market Analysis, Insights and Forecast - by Crop Type

- 7.2.1. Cereals

- 7.2.2. Fruits

- 7.2.3. Vegetables

- 7.2.4. Oilseeds

- 7.1. Market Analysis, Insights and Forecast - by Crop Type

- 8. South America Agriculture Industry in South Africa Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Crop Type

- 8.1.1. Cereals

- 8.1.2. Fruits

- 8.1.3. Vegetables

- 8.1.4. Oilseeds

- 8.2. Market Analysis, Insights and Forecast - by Crop Type

- 8.2.1. Cereals

- 8.2.2. Fruits

- 8.2.3. Vegetables

- 8.2.4. Oilseeds

- 8.1. Market Analysis, Insights and Forecast - by Crop Type

- 9. Europe Agriculture Industry in South Africa Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Crop Type

- 9.1.1. Cereals

- 9.1.2. Fruits

- 9.1.3. Vegetables

- 9.1.4. Oilseeds

- 9.2. Market Analysis, Insights and Forecast - by Crop Type

- 9.2.1. Cereals

- 9.2.2. Fruits

- 9.2.3. Vegetables

- 9.2.4. Oilseeds

- 9.1. Market Analysis, Insights and Forecast - by Crop Type

- 10. Middle East & Africa Agriculture Industry in South Africa Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Crop Type

- 10.1.1. Cereals

- 10.1.2. Fruits

- 10.1.3. Vegetables

- 10.1.4. Oilseeds

- 10.2. Market Analysis, Insights and Forecast - by Crop Type

- 10.2.1. Cereals

- 10.2.2. Fruits

- 10.2.3. Vegetables

- 10.2.4. Oilseeds

- 10.1. Market Analysis, Insights and Forecast - by Crop Type

- 11. Asia Pacific Agriculture Industry in South Africa Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Crop Type

- 11.1.1. Cereals

- 11.1.2. Fruits

- 11.1.3. Vegetables

- 11.1.4. Oilseeds

- 11.2. Market Analysis, Insights and Forecast - by Crop Type

- 11.2.1. Cereals

- 11.2.2. Fruits

- 11.2.3. Vegetables

- 11.2.4. Oilseeds

- 11.1. Market Analysis, Insights and Forecast - by Crop Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Pioneer Foods

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Bayer Crop Science

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Syngenta

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Monsanto

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Tiger Brands

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.1 Pioneer Foods

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Agriculture Industry in South Africa Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Agriculture Industry in South Africa Revenue (Million), by Crop Type 2025 & 2033

- Figure 3: North America Agriculture Industry in South Africa Revenue Share (%), by Crop Type 2025 & 2033

- Figure 4: North America Agriculture Industry in South Africa Revenue (Million), by Crop Type 2025 & 2033

- Figure 5: North America Agriculture Industry in South Africa Revenue Share (%), by Crop Type 2025 & 2033

- Figure 6: North America Agriculture Industry in South Africa Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Agriculture Industry in South Africa Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Agriculture Industry in South Africa Revenue (Million), by Crop Type 2025 & 2033

- Figure 9: South America Agriculture Industry in South Africa Revenue Share (%), by Crop Type 2025 & 2033

- Figure 10: South America Agriculture Industry in South Africa Revenue (Million), by Crop Type 2025 & 2033

- Figure 11: South America Agriculture Industry in South Africa Revenue Share (%), by Crop Type 2025 & 2033

- Figure 12: South America Agriculture Industry in South Africa Revenue (Million), by Country 2025 & 2033

- Figure 13: South America Agriculture Industry in South Africa Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Agriculture Industry in South Africa Revenue (Million), by Crop Type 2025 & 2033

- Figure 15: Europe Agriculture Industry in South Africa Revenue Share (%), by Crop Type 2025 & 2033

- Figure 16: Europe Agriculture Industry in South Africa Revenue (Million), by Crop Type 2025 & 2033

- Figure 17: Europe Agriculture Industry in South Africa Revenue Share (%), by Crop Type 2025 & 2033

- Figure 18: Europe Agriculture Industry in South Africa Revenue (Million), by Country 2025 & 2033

- Figure 19: Europe Agriculture Industry in South Africa Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Agriculture Industry in South Africa Revenue (Million), by Crop Type 2025 & 2033

- Figure 21: Middle East & Africa Agriculture Industry in South Africa Revenue Share (%), by Crop Type 2025 & 2033

- Figure 22: Middle East & Africa Agriculture Industry in South Africa Revenue (Million), by Crop Type 2025 & 2033

- Figure 23: Middle East & Africa Agriculture Industry in South Africa Revenue Share (%), by Crop Type 2025 & 2033

- Figure 24: Middle East & Africa Agriculture Industry in South Africa Revenue (Million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Agriculture Industry in South Africa Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Agriculture Industry in South Africa Revenue (Million), by Crop Type 2025 & 2033

- Figure 27: Asia Pacific Agriculture Industry in South Africa Revenue Share (%), by Crop Type 2025 & 2033

- Figure 28: Asia Pacific Agriculture Industry in South Africa Revenue (Million), by Crop Type 2025 & 2033

- Figure 29: Asia Pacific Agriculture Industry in South Africa Revenue Share (%), by Crop Type 2025 & 2033

- Figure 30: Asia Pacific Agriculture Industry in South Africa Revenue (Million), by Country 2025 & 2033

- Figure 31: Asia Pacific Agriculture Industry in South Africa Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Agriculture Industry in South Africa Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 2: Global Agriculture Industry in South Africa Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 3: Global Agriculture Industry in South Africa Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Agriculture Industry in South Africa Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 5: Global Agriculture Industry in South Africa Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 6: Global Agriculture Industry in South Africa Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Global Agriculture Industry in South Africa Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 11: Global Agriculture Industry in South Africa Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 12: Global Agriculture Industry in South Africa Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Brazil Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Global Agriculture Industry in South Africa Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 17: Global Agriculture Industry in South Africa Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 18: Global Agriculture Industry in South Africa Revenue Million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Germany Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: France Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Italy Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Spain Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Russia Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Global Agriculture Industry in South Africa Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 29: Global Agriculture Industry in South Africa Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 30: Global Agriculture Industry in South Africa Revenue Million Forecast, by Country 2020 & 2033

- Table 31: Turkey Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Israel Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: GCC Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: Global Agriculture Industry in South Africa Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 38: Global Agriculture Industry in South Africa Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 39: Global Agriculture Industry in South Africa Revenue Million Forecast, by Country 2020 & 2033

- Table 40: China Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 41: India Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Japan Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Agriculture Industry in South Africa?

The projected CAGR is approximately 7.60%.

2. Which companies are prominent players in the Agriculture Industry in South Africa?

Key companies in the market include Pioneer Foods , Bayer Crop Science , Syngenta , Monsanto , Tiger Brands.

3. What are the main segments of the Agriculture Industry in South Africa?

The market segments include Crop Type, Crop Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 16.12 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Consumption of Cashew Nuts as a Healthy Snack; Increasing Government initiatives; Growing Cashew Nut Imports in The United States.

6. What are the notable trends driving market growth?

High Demand for Food Crops with the rising population.

7. Are there any restraints impacting market growth?

Hazardous Climatic Condition Hinders Cashew Production; Stringent Regulations Related To Food Quality Standards.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Agriculture Industry in South Africa," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Agriculture Industry in South Africa report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Agriculture Industry in South Africa?

To stay informed about further developments, trends, and reports in the Agriculture Industry in South Africa, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence