Key Insights

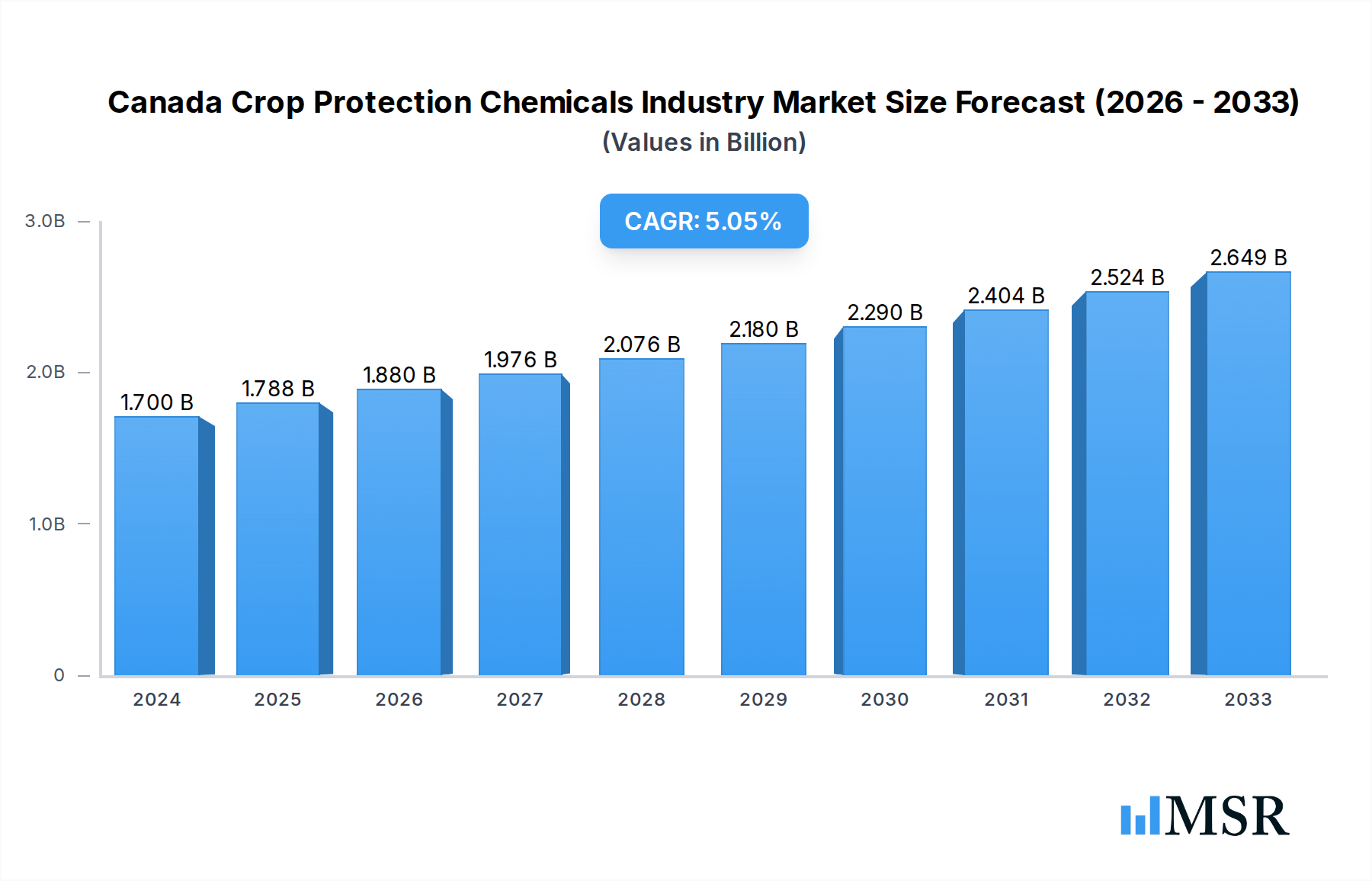

The Canadian crop protection chemicals market is projected to experience robust growth, driven by the increasing demand for food and the necessity of safeguarding crops against pests and diseases. With a current market size of approximately $1.7 billion in 2024 and an anticipated Compound Annual Growth Rate (CAGR) of 5.24%, the industry is set for significant expansion through 2033. Key drivers include the adoption of advanced agricultural practices, the need to improve crop yields to meet the demands of a growing population, and the continuous threat posed by evolving pest resistance and emerging crop diseases. Furthermore, the substantial agricultural land in Canada, coupled with government initiatives supporting modern farming techniques, further fuels market expansion.

Canada Crop Protection Chemicals Industry Market Size (In Billion)

The market encompasses a diverse range of products, including fungicides, herbicides, and insecticides, applied through various modes such as chemigation, foliar, fumigation, seed treatment, and soil treatment. These solutions are critical for a wide array of crop types, from grains and cereals to fruits, vegetables, pulses, oilseeds, and turf & ornamentals. While the market benefits from technological advancements in product formulation and application, it also faces restraints such as increasing regulatory scrutiny, growing demand for organic farming alternatives, and potential price volatility of raw materials. Key players like Bayer AG, Syngenta Group, and BASF SE are actively innovating and expanding their offerings to cater to the evolving needs of Canadian farmers and maintain their market positions.

Canada Crop Protection Chemicals Industry Company Market Share

Gain unparalleled strategic insights into the dynamic Canadian Crop Protection Chemicals market. This in-depth report, covering the period from 2019 to 2033 with a base year of 2025, provides a granular analysis of market size, growth drivers, segmentation, competitive landscape, and future opportunities. Essential for agricultural chemical companies, agribusiness stakeholders, investment firms, and policy makers, this report offers data-driven forecasts and actionable intelligence on the Canadian pesticide market, crop protection solutions, and agricultural inputs in Canada.

Canada Crop Protection Chemicals Industry Market Concentration & Dynamics

The Canadian crop protection chemicals industry exhibits a moderate to high market concentration, with a few major multinational corporations holding significant market share. Key players like FMC Corporation, Bayer AG, Syngenta Group, and Corteva Agriscience dominate, driven by extensive research and development capabilities, established distribution networks, and comprehensive product portfolios. The innovation ecosystem is robust, fueled by continuous R&D investments aimed at developing more effective, targeted, and environmentally sustainable crop protection products. Regulatory frameworks, overseen by agencies like Health Canada's Pest Management Regulatory Agency (PMRA), play a crucial role in market access and product approval, influencing the pace of innovation and market entry. Substitute products, such as biological pest control agents and integrated pest management (IPM) strategies, are gaining traction, presenting both challenges and opportunities for conventional agrochemicals. End-user trends are shifting towards sustainable agriculture, demanding solutions that minimize environmental impact while maximizing crop yields. Merger and acquisition (M&A) activities, though less frequent in recent years, have historically reshaped the competitive landscape, consolidating market power and expanding product offerings. Current M&A deal counts are low, reflecting market maturity and the high cost of acquisitions. The market share distribution is heavily skewed, with the top five companies collectively accounting for approximately 70% of the Canadian crop protection market value.

Canada Crop Protection Chemicals Industry Industry Insights & Trends

The Canadian crop protection chemicals industry is poised for significant growth, driven by an increasing global demand for food, the need to enhance agricultural productivity, and evolving farming practices. The market size is projected to reach over \$5 billion by 2033, with a Compound Annual Growth Rate (CAGR) of approximately 4.5% during the forecast period (2025–2033). Herbicides are expected to remain the largest segment by revenue, followed by fungicides and insecticides, reflecting the persistent challenges posed by weeds, fungal diseases, and insect infestations in major Canadian crops. Technological disruptions, including advancements in precision agriculture, digital farming platforms, and the development of novel active ingredients, are reshaping the industry. These innovations enable more targeted application, reduce chemical usage, and improve overall farm efficiency. The rise of biological crop protection solutions, driven by consumer preference for sustainably produced food and increasing regulatory scrutiny on synthetic pesticides, presents a transformative trend. Evolving consumer behaviors, characterized by a growing demand for organic and reduced-pesticide produce, are indirectly influencing the Canadian agricultural chemical industry by pushing for more eco-friendly formulations and integrated pest management approaches. The historical period (2019–2024) saw steady growth, with the market size growing from approximately \$3.5 billion in 2019 to an estimated \$4.2 billion in 2024. This growth was primarily fueled by the need to combat evolving pest resistance and optimize yields for major Canadian crops such as canola, wheat, and corn.

Key Markets & Segments Leading Canada Crop Protection Chemicals Industry

The Canadian crop protection chemicals market is predominantly driven by the Grains & Cereals crop type segment, which accounts for over 40% of the total market value. This dominance is attributed to the vast acreage dedicated to grains like wheat, barley, and corn across the Canadian prairies and other agricultural regions. Commercial Crops, encompassing oilseeds and other large-scale agricultural produce, also represent a substantial market segment. Within the Function segmentation, Herbicides lead the market due to the continuous battle against weed proliferation in these extensive grain and cereal fields. Fungicides and Insecticides follow closely, addressing the prevalent threats of fungal diseases and insect pests that can significantly impact crop yield and quality.

Crop Type Dominance:

- Grains & Cereals: The vast cultivation areas of wheat, barley, oats, and corn necessitate robust weed and disease management strategies, driving significant demand for herbicides and fungicides.

- Commercial Crops: This segment includes vital crops like canola, soybeans, and pulses, where effective pest and disease control is crucial for maintaining global competitiveness and meeting export demands.

Function Dominance:

- Herbicides: Essential for managing weed competition in large-scale grain and cereal cultivation, contributing the largest share to the agrochemical market in Canada.

- Fungicides: Critical for preventing and controlling a wide range of crop diseases, especially in humid regions and for susceptible crop varieties.

- Insecticides: Necessary for mitigating damage from various insect pests that affect yield and quality across multiple crop types.

The Application Mode segment, Foliar application, is the most widely used due to its direct efficacy in delivering active ingredients to the plant surface, providing immediate protection against foliar diseases and pests. Seed Treatment is also a growing application mode, offering early-season protection and improved crop establishment.

- Application Mode Dominance:

- Foliar: The most common method for widespread crop protection, delivering rapid results against prevalent threats.

- Seed Treatment: Increasingly adopted for proactive pest and disease management from the germination stage.

The Pulses & Oilseeds segment is also a significant contributor, with crops like lentils, peas, and soybeans requiring specialized crop protection solutions to combat specific pests and diseases. The Fruits & Vegetables segment, while smaller in acreage, demands high-value, specialized crop protection chemicals due to shorter crop cycles and the need for premium quality produce.

Canada Crop Protection Chemicals Industry Product Developments

Recent product developments underscore a trend towards targeted efficacy and environmental consideration within the Canadian crop protection chemicals sector. In July 2023, ADAMA introduced innovative solutions, Davai A Plus and Clearfield Broad-Spectrum Herbicide Solutions, specifically designed for imidazolinone-tolerant legumes like lentils, peas, and soybeans, addressing critical weed management challenges. January 2023 saw Gowan Canada Inc. launch Magister SC Miticide for the Canadian horticulture market, offering rapid action against specific mite species and pear psylla, crucial for protecting high-value fruits. Furthermore, also in January 2023, Bayer initiated a strategic partnership with Oerth Bio to advance crop protection technology and foster the development of more eco-friendly crop protection solutions, signaling a commitment to sustainable innovation. These advancements highlight the industry's focus on precision, efficacy, and the integration of sustainable practices to meet evolving agricultural needs and regulatory landscapes.

Challenges in the Canada Crop Protection Chemicals Industry Market

The Canadian crop protection chemicals market faces several significant challenges that can impact its growth trajectory. Regulatory hurdles, including stringent approval processes and evolving environmental standards from bodies like PMRA, can delay product launches and increase R&D costs. Supply chain disruptions, exacerbated by global events and transportation complexities, can lead to availability issues and price volatility for key agricultural chemicals. Intense competitive pressures from both established global players and emerging bio-pesticide companies necessitate continuous innovation and cost-efficiency. Furthermore, the increasing prevalence of pest resistance to existing pesticides demands the development of new active ingredients and management strategies, adding to R&D expenditure. The perception of synthetic pesticides among consumers and advocacy groups also poses a challenge, driving demand for alternatives and potentially influencing market access for certain products.

Forces Driving Canada Crop Protection Chemicals Industry Growth

Several powerful forces are propelling the growth of the Canada Crop Protection Chemicals industry. The fundamental need to ensure food security for a growing population necessitates increased agricultural productivity, making effective crop protection indispensable. Technological advancements in precision agriculture and digital farming allow for more targeted and efficient application of agrochemicals, reducing waste and environmental impact while enhancing efficacy. Government initiatives supporting agricultural innovation and sustainability can also drive market expansion. The increasing adoption of advanced farming techniques and the demand for higher crop yields to meet both domestic and international market needs are critical economic drivers. Moreover, the continuous development of novel and more efficacious crop protection agents, including next-generation fungicides, herbicides, and insecticides, directly fuels market demand.

Challenges in the Canada Crop Protection Chemicals Industry Market

Long-term growth catalysts for the Canada Crop Protection Chemicals industry lie in continued innovation and strategic market adaptation. The development of highly selective and environmentally benign crop protection solutions, including biopesticides and integrated pest management (IPM) technologies, will be crucial for addressing regulatory pressures and consumer preferences for sustainable agriculture. Strategic partnerships and collaborations between chemical manufacturers, research institutions, and agricultural technology providers can accelerate the development and adoption of novel solutions. Market expansions into niche crop segments or the development of specialized formulations for emerging agricultural practices will also contribute to sustained growth. Furthermore, leveraging digital tools for enhanced product stewardship and grower education can build trust and promote responsible use of agrochemicals, fostering long-term market viability.

Emerging Opportunities in Canada Crop Protection Chemicals Industry

Emerging opportunities within the Canada Crop Protection Chemicals industry are diverse and promising. The increasing demand for sustainable agriculture presents a significant avenue for growth in biopesticides, biological fungicides, and natural insecticides, aligning with consumer preferences and regulatory trends. Advancements in gene editing and biotechnology offer prospects for developing crops with inherent resistance to pests and diseases, potentially reducing reliance on conventional pesticides. The growth of the organic food market in Canada creates specific demand for certified organic crop protection products. Furthermore, the application of artificial intelligence (AI) and data analytics in agriculture, particularly in precision weed control and disease forecasting, opens avenues for integrated solutions that combine chemical and digital approaches. The exploration of novel application methods, such as drone-based spraying and microencapsulation technologies, also presents opportunities for improved efficiency and reduced environmental impact.

Leading Players in the Canada Crop Protection Chemicals Industry Sector

- FMC Corporation

- Sumitomo Chemical Co Ltd

- ADAMA Agricultural Solutions Ltd

- Bayer AG

- Gowan Company

- UPL Limited

- Syngenta Group

- Corteva Agriscience

- Nufarm Ltd

- BASF SE

Key Milestones in Canada Crop Protection Chemicals Industry Industry

- July 2023: ADAMA introduced new products, Davai A Plus and Clearfield Broad-Spectrum Herbicide Solutions, for imidazolinone-tolerant legumes like lentils, peas, and soybeans, addressing critical weed management needs in pulse crops.

- January 2023: For the Canadian horticulture market, Gowan Canada Inc. introduced Magister SC Miticide. The product provides rapid action against certain species of mites in both Eriophyidae and Tetranychidae families and pear psylla, enhancing protection for high-value fruit crops.

- January 2023: Bayer formed a new partnership with Oerth Bio to enhance crop protection technology and create more eco-friendly crop protection solutions, signaling a commitment to sustainable innovation and advanced research in the agrochemical sector.

Strategic Outlook for Canada Crop Protection Chemicals Industry Market

The strategic outlook for the Canada Crop Protection Chemicals industry is one of continued evolution and adaptation. Growth will be accelerated by the increasing adoption of sustainable and precision agriculture techniques, coupled with the development of innovative, environmentally responsible crop protection solutions. Key opportunities lie in leveraging digital technologies for smarter application and management of agrochemicals, alongside expanding the portfolio of biological fungicides, herbicides, and insecticides. Strategic collaborations will be vital for navigating complex regulatory landscapes and bringing novel products to market efficiently. The industry must also focus on addressing evolving consumer demands for sustainably produced food, which will drive the demand for reduced-pesticide inputs and alternative protection strategies. Investments in R&D for next-generation plant protection products and integrated pest management systems will be crucial for maintaining competitive advantage and ensuring long-term market viability.

Canada Crop Protection Chemicals Industry Segmentation

-

1. Function

- 1.1. Fungicide

- 1.2. Herbicide

- 1.3. Insecticide

- 1.4. Molluscicide

- 1.5. Nematicide

-

2. Application Mode

- 2.1. Chemigation

- 2.2. Foliar

- 2.3. Fumigation

- 2.4. Seed Treatment

- 2.5. Soil Treatment

-

3. Crop Type

- 3.1. Commercial Crops

- 3.2. Fruits & Vegetables

- 3.3. Grains & Cereals

- 3.4. Pulses & Oilseeds

- 3.5. Turf & Ornamental

-

4. Function

- 4.1. Fungicide

- 4.2. Herbicide

- 4.3. Insecticide

- 4.4. Molluscicide

- 4.5. Nematicide

-

5. Application Mode

- 5.1. Chemigation

- 5.2. Foliar

- 5.3. Fumigation

- 5.4. Seed Treatment

- 5.5. Soil Treatment

-

6. Crop Type

- 6.1. Commercial Crops

- 6.2. Fruits & Vegetables

- 6.3. Grains & Cereals

- 6.4. Pulses & Oilseeds

- 6.5. Turf & Ornamental

Canada Crop Protection Chemicals Industry Segmentation By Geography

- 1. Canada

Canada Crop Protection Chemicals Industry Regional Market Share

Geographic Coverage of Canada Crop Protection Chemicals Industry

Canada Crop Protection Chemicals Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.24% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Function

- 5.1.1. Fungicide

- 5.1.2. Herbicide

- 5.1.3. Insecticide

- 5.1.4. Molluscicide

- 5.1.5. Nematicide

- 5.2. Market Analysis, Insights and Forecast - by Application Mode

- 5.2.1. Chemigation

- 5.2.2. Foliar

- 5.2.3. Fumigation

- 5.2.4. Seed Treatment

- 5.2.5. Soil Treatment

- 5.3. Market Analysis, Insights and Forecast - by Crop Type

- 5.3.1. Commercial Crops

- 5.3.2. Fruits & Vegetables

- 5.3.3. Grains & Cereals

- 5.3.4. Pulses & Oilseeds

- 5.3.5. Turf & Ornamental

- 5.4. Market Analysis, Insights and Forecast - by Function

- 5.4.1. Fungicide

- 5.4.2. Herbicide

- 5.4.3. Insecticide

- 5.4.4. Molluscicide

- 5.4.5. Nematicide

- 5.5. Market Analysis, Insights and Forecast - by Application Mode

- 5.5.1. Chemigation

- 5.5.2. Foliar

- 5.5.3. Fumigation

- 5.5.4. Seed Treatment

- 5.5.5. Soil Treatment

- 5.6. Market Analysis, Insights and Forecast - by Crop Type

- 5.6.1. Commercial Crops

- 5.6.2. Fruits & Vegetables

- 5.6.3. Grains & Cereals

- 5.6.4. Pulses & Oilseeds

- 5.6.5. Turf & Ornamental

- 5.7. Market Analysis, Insights and Forecast - by Region

- 5.7.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by Function

- 6. Canada Crop Protection Chemicals Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Function

- 6.1.1. Fungicide

- 6.1.2. Herbicide

- 6.1.3. Insecticide

- 6.1.4. Molluscicide

- 6.1.5. Nematicide

- 6.2. Market Analysis, Insights and Forecast - by Application Mode

- 6.2.1. Chemigation

- 6.2.2. Foliar

- 6.2.3. Fumigation

- 6.2.4. Seed Treatment

- 6.2.5. Soil Treatment

- 6.3. Market Analysis, Insights and Forecast - by Crop Type

- 6.3.1. Commercial Crops

- 6.3.2. Fruits & Vegetables

- 6.3.3. Grains & Cereals

- 6.3.4. Pulses & Oilseeds

- 6.3.5. Turf & Ornamental

- 6.4. Market Analysis, Insights and Forecast - by Function

- 6.4.1. Fungicide

- 6.4.2. Herbicide

- 6.4.3. Insecticide

- 6.4.4. Molluscicide

- 6.4.5. Nematicide

- 6.5. Market Analysis, Insights and Forecast - by Application Mode

- 6.5.1. Chemigation

- 6.5.2. Foliar

- 6.5.3. Fumigation

- 6.5.4. Seed Treatment

- 6.5.5. Soil Treatment

- 6.6. Market Analysis, Insights and Forecast - by Crop Type

- 6.6.1. Commercial Crops

- 6.6.2. Fruits & Vegetables

- 6.6.3. Grains & Cereals

- 6.6.4. Pulses & Oilseeds

- 6.6.5. Turf & Ornamental

- 6.1. Market Analysis, Insights and Forecast - by Function

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 FMC Corporation

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Sumitomo Chemical Co Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 ADAMA Agricultural Solutions Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Bayer AG

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Gowan Company

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 UPL Limite

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Syngenta Group

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Corteva Agriscience

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Nufarm Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 BASF SE

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 FMC Corporation

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Canada Crop Protection Chemicals Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Canada Crop Protection Chemicals Industry Share (%) by Company 2025

List of Tables

- Table 1: Canada Crop Protection Chemicals Industry Revenue billion Forecast, by Function 2020 & 2033

- Table 2: Canada Crop Protection Chemicals Industry Revenue billion Forecast, by Application Mode 2020 & 2033

- Table 3: Canada Crop Protection Chemicals Industry Revenue billion Forecast, by Crop Type 2020 & 2033

- Table 4: Canada Crop Protection Chemicals Industry Revenue billion Forecast, by Function 2020 & 2033

- Table 5: Canada Crop Protection Chemicals Industry Revenue billion Forecast, by Application Mode 2020 & 2033

- Table 6: Canada Crop Protection Chemicals Industry Revenue billion Forecast, by Crop Type 2020 & 2033

- Table 7: Canada Crop Protection Chemicals Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 8: Canada Crop Protection Chemicals Industry Revenue billion Forecast, by Function 2020 & 2033

- Table 9: Canada Crop Protection Chemicals Industry Revenue billion Forecast, by Application Mode 2020 & 2033

- Table 10: Canada Crop Protection Chemicals Industry Revenue billion Forecast, by Crop Type 2020 & 2033

- Table 11: Canada Crop Protection Chemicals Industry Revenue billion Forecast, by Function 2020 & 2033

- Table 12: Canada Crop Protection Chemicals Industry Revenue billion Forecast, by Application Mode 2020 & 2033

- Table 13: Canada Crop Protection Chemicals Industry Revenue billion Forecast, by Crop Type 2020 & 2033

- Table 14: Canada Crop Protection Chemicals Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Crop Protection Chemicals Industry?

The projected CAGR is approximately 5.24%.

2. Which companies are prominent players in the Canada Crop Protection Chemicals Industry?

Key companies in the market include FMC Corporation, Sumitomo Chemical Co Ltd, ADAMA Agricultural Solutions Ltd, Bayer AG, Gowan Company, UPL Limite, Syngenta Group, Corteva Agriscience, Nufarm Ltd, BASF SE.

3. What are the main segments of the Canada Crop Protection Chemicals Industry?

The market segments include Function, Application Mode, Crop Type, Function, Application Mode, Crop Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.7 billion as of 2022.

5. What are some drivers contributing to market growth?

Seed Treatment As A Solution To Enhance Yield; Growing Awareness For Seed Treatment Among The Farmers; Rising Trend Of Organic Farming.

6. What are the notable trends driving market growth?

The market is driven by the growing pressure of pests and diseases.

7. Are there any restraints impacting market growth?

Limitations Across Farm-Level Seed Treatment; Rising Environmental Concerns.

8. Can you provide examples of recent developments in the market?

July 2023: ADAMA introduced new products, Davai A Plus and Clearfield Broad-Spectrum Herbicide Solutions, for imidazolinone-tolerant legumes like lentils, peas, and soybeans.January 2023: For the Canadian horticulture market, Gowan Canada Inc. introduced Magister SC Miticide. The product provides rapid action against certain species of mites in both Eriophyidae and Tetranychidae families and pear psylla.January 2023: Bayer formed a new partnership with Oerth Bio to enhance crop protection technology and create more eco-friendly crop protection solutions.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Crop Protection Chemicals Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Crop Protection Chemicals Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Crop Protection Chemicals Industry?

To stay informed about further developments, trends, and reports in the Canada Crop Protection Chemicals Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence