Key Insights

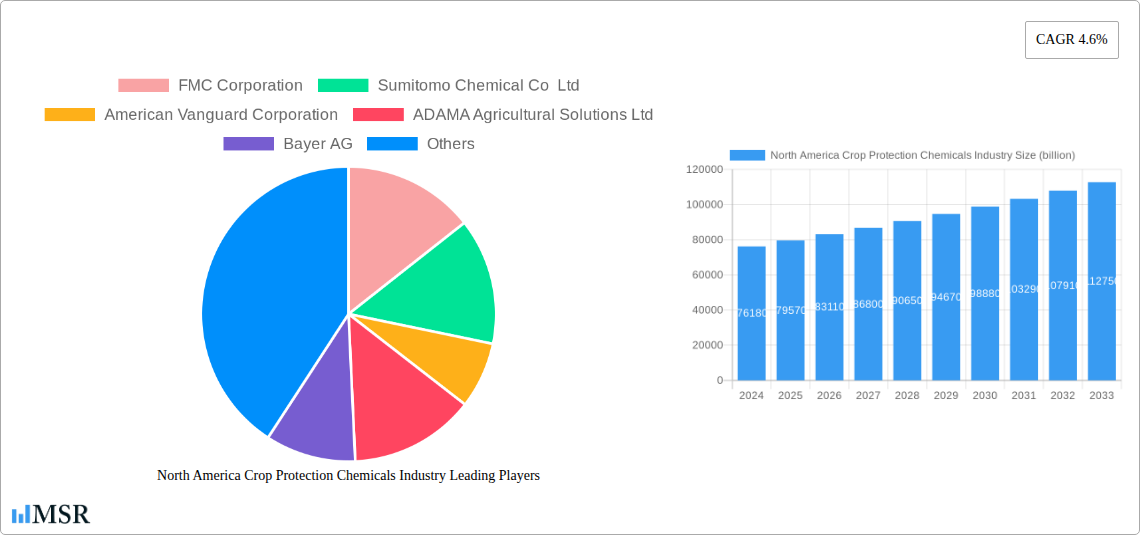

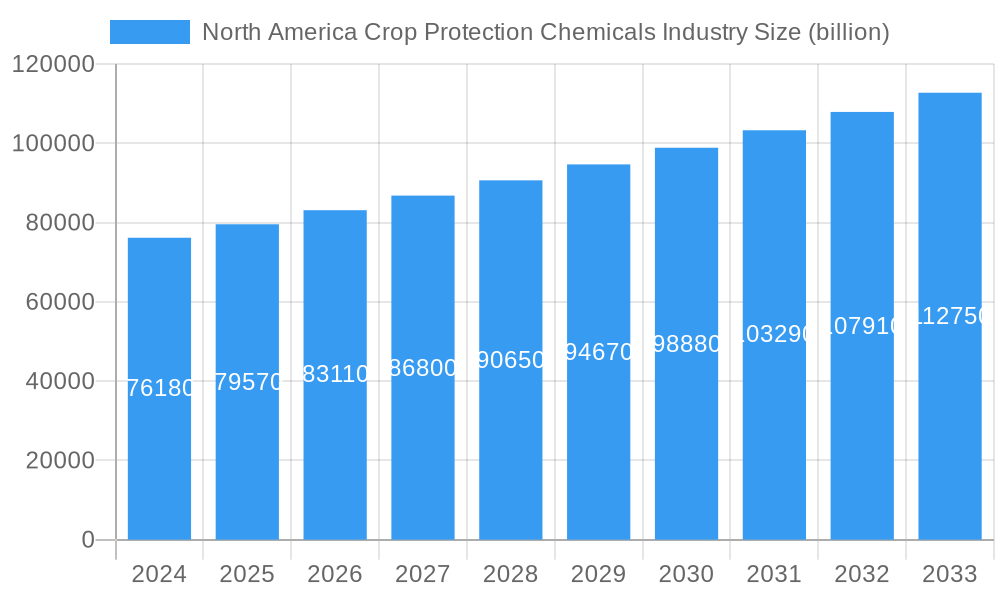

The North American crop protection chemicals market is experiencing robust growth, projected to reach a substantial USD 76.18 billion in 2024. This expansion is fueled by an increasing demand for higher agricultural yields to meet the growing global population's food requirements and the persistent need to mitigate crop losses caused by pests, diseases, and weeds. The market is characterized by a CAGR of 4.6%, indicating a healthy and sustained upward trajectory over the forecast period of 2025-2033. This growth is further underpinned by advancements in chemical formulations, leading to more effective and environmentally conscious crop protection solutions. Key market drivers include the rising adoption of integrated pest management (IPM) strategies that incorporate chemical interventions, government initiatives promoting sustainable agriculture, and the continuous development of new and innovative agrochemical products by leading companies.

North America Crop Protection Chemicals Industry Market Size (In Billion)

Within North America, the crop protection chemicals industry is segmented across various functions, with fungicides, herbicides, and insecticides dominating the market share. These segments are crucial for safeguarding a wide array of crops, from essential grains and cereals to high-value fruits and vegetables, as well as commercial crops. Application modes such as foliar application and seed treatment are widely adopted due to their efficiency and effectiveness. While the market benefits from strong demand and technological innovation, certain restraints, such as increasing regulatory scrutiny regarding environmental impact and the development of pest resistance to existing chemicals, necessitate ongoing research and development for sustainable solutions. Nonetheless, the outlook for the North American crop protection chemicals market remains highly positive, driven by the imperative to ensure food security and enhance agricultural productivity.

North America Crop Protection Chemicals Industry Company Market Share

North America Crop Protection Chemicals Industry: Market Insights, Trends, and Future Outlook (2019-2033)

Dive deep into the dynamic North America crop protection chemicals market with our comprehensive report. Covering the historical period of 2019–2024 and projecting growth through 2033, this analysis provides actionable insights for stakeholders seeking to capitalize on opportunities in this multi-billion dollar industry. With a base year of 2025, the report forecasts a robust CAGR of xx%, driven by increasing demand for high-yield agriculture and sustainable farming practices. Explore market concentration, key segments, product innovations, challenges, and future strategies within the North American agriculture sector. This report is your definitive guide to understanding the crop protection solutions market, including fungicides, herbicides, insecticides, molluscicides, and nematicides, applied through chemigation, foliar, fumigation, seed treatment, and soil treatment methods across commercial crops, fruits & vegetables, grains & cereals, pulses & oilseeds, and turf & ornamental sectors.

North America Crop Protection Chemicals Industry Market Concentration & Dynamics

The North America crop protection chemicals industry exhibits a moderate to high market concentration, with a few key players dominating a significant share of the multi-billion dollar market. Innovation ecosystems are actively driven by substantial R&D investments, focusing on developing environmentally-friendly crop protection solutions and addressing pest resistance. Regulatory frameworks, particularly in the United States and Canada, play a pivotal role, influencing product approvals and market access. The constant evolution of these regulations necessitates proactive adaptation from industry players. Substitute products, such as biological pest control agents and precision agriculture technologies, are gaining traction, though chemical crop protection remains essential for large-scale agricultural operations. End-user trends are increasingly leaning towards integrated pest management (IPM) strategies and demand for sustainable agricultural inputs. Merger and acquisition (M&A) activities are a recurring theme, driven by the pursuit of market expansion, enhanced product portfolios, and synergistic capabilities. For instance, numerous M&A deals were recorded during the historical period, contributing to the evolving competitive landscape. Key market share figures and M&A deal counts are detailed within the full report.

North America Crop Protection Chemicals Industry Industry Insights & Trends

The North America crop protection chemicals market is poised for substantial growth, driven by several interconnected factors. The increasing global population and the consequent demand for enhanced food security are primary market growth drivers. This necessitates optimizing crop yields, making effective crop protection chemicals indispensable. Technological disruptions, including the development of more targeted and lower-dose active ingredients, alongside advancements in application technologies like drone spraying and smart irrigation, are revolutionizing the sector. Evolving consumer behaviors are also playing a crucial role; there's a growing preference for food produced with minimal chemical residue, pushing manufacturers towards developing safer and more sustainable crop protection products. The market size in 2025 is estimated at US$ xx billion, with a projected CAGR of xx% during the forecast period (2025–2033). Factors such as the rising adoption of advanced farming techniques, increasing prevalence of crop diseases and pest infestations exacerbated by climate change, and supportive government initiatives promoting agricultural productivity further fuel market expansion. The demand for specialized solutions for high-value crops and the growing awareness regarding the economic impact of crop losses are also significant contributors to the industry's upward trajectory. The integration of digital tools for crop monitoring and predictive analytics is also a key trend, enabling more precise and efficient application of crop protection agents.

Key Markets & Segments Leading North America Crop Protection Chemicals Industry

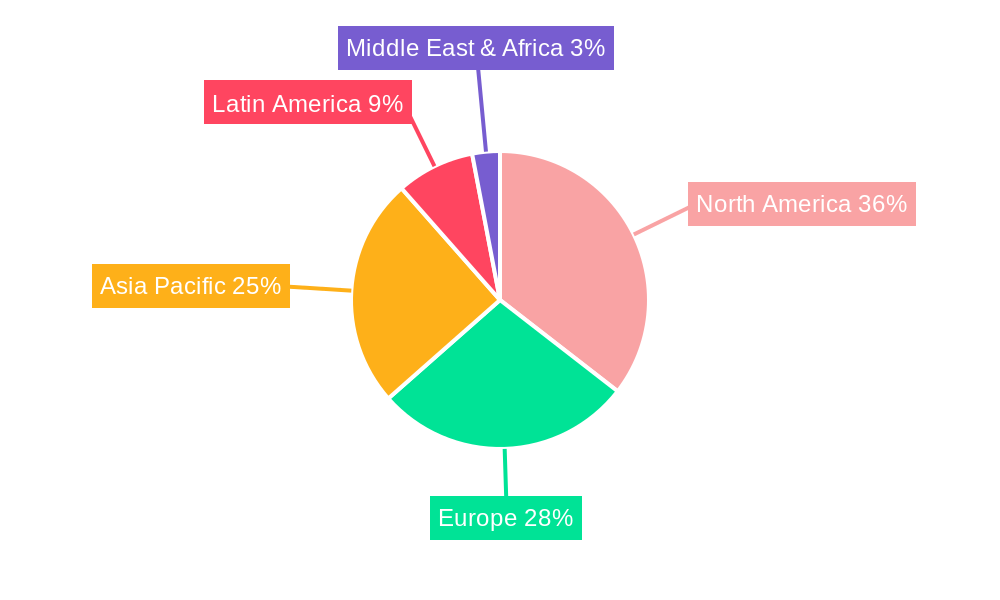

The North America crop protection chemicals industry is a multifaceted landscape where specific regions and product segments demonstrate significant dominance. The United States, with its vast agricultural landmass and advanced farming practices, stands as the leading market. Canada also contributes significantly to the overall market value. Within the Function segment, Herbicides command the largest market share, driven by the persistent challenge of weed management across major grain crops and commercial farming operations. Insecticides follow closely, essential for controlling a wide array of insect pests that threaten crop health and yield. Fungicides are also critical, particularly in regions with humid climates or for crops prone to fungal diseases.

The Application Mode segment sees Foliar application as the most prevalent method, offering direct and efficient delivery of active ingredients. Seed Treatment is a rapidly growing application mode, providing early-stage protection to crops and reducing the need for later, more intensive spraying. Soil Treatment and Chemigation also hold considerable importance for specific crop types and pest challenges.

In terms of Crop Type, Grains & Cereals represent the largest segment due to the extensive cultivation of corn, wheat, and soybeans across North America. Commercial Crops, encompassing a broad range of agricultural produce for industrial use, also contribute substantially. Fruits & Vegetables and Pulses & Oilseeds are vital segments where specialized crop protection is crucial for quality and yield. The Turf & Ornamental segment, while smaller, is characterized by higher-value, specialized products driven by demand from landscaping, golf courses, and public spaces. Economic growth, infrastructure development supporting agricultural logistics, and the increasing need for food production to meet rising domestic and international demand are key drivers of dominance in these segments.

North America Crop Protection Chemicals Industry Product Developments

Product innovation is a cornerstone of the North America crop protection chemicals market, with companies continuously introducing advanced solutions to meet evolving agricultural needs and regulatory demands. Recent developments highlight a focus on targeted efficacy and improved environmental profiles. For instance, ADAMA's introduction of Davai A Plus and Clearfield Broad-Spectrum Herbicide Solutions in July 2023 caters to specific legume crops, addressing the critical need for effective weed control in these economically important commodities. Nufarm's launch of Tourney EZ in April 2023, a specialized liquid formulation fungicide for turf and ornamental crops, demonstrates a commitment to addressing niche market demands and reinforcing its position in this sector. Furthermore, AMVAC's release of herbicides like Impact Core and Sinate in March 2023 underscores the industry's proactive approach to combating herbicide resistance, a growing concern for maize cultivation. These developments signify a trend towards precision agriculture and customized solutions that enhance crop health, boost yields, and minimize environmental impact, thereby maintaining a competitive edge.

Challenges in the North America Crop Protection Chemicals Industry Market

The North America crop protection chemicals market faces several significant challenges that can impede growth and profitability. Stringent regulatory frameworks and lengthy approval processes for new active ingredients and formulations represent a substantial barrier, increasing R&D costs and time-to-market. The growing prevalence of pest and weed resistance to existing chemistries necessitates continuous innovation and the development of new modes of action, which is an expensive undertaking. Supply chain disruptions, exacerbated by geopolitical events and global economic volatility, can lead to increased raw material costs and product availability issues, impacting market stability. Furthermore, increasing public scrutiny and consumer demand for residue-free produce pressure manufacturers to develop more sustainable and biologically-derived alternatives, creating competitive pressure on traditional chemical solutions.

Forces Driving North America Crop Protection Chemicals Industry Growth

Several powerful forces are propelling the growth of the North America crop protection chemicals industry. The ever-increasing global population and the resultant demand for food security remain a fundamental driver, necessitating optimized agricultural output. Technological advancements in agricultural practices, including precision farming and the adoption of advanced irrigation systems, create a demand for sophisticated crop protection solutions that integrate with these technologies. Supportive government policies and subsidies aimed at boosting agricultural productivity and promoting sustainable farming methods further incentivize the use of effective crop protection products. Additionally, the rising incidence of crop diseases and pest infestations, often intensified by changing climate patterns, creates an ongoing need for robust pest management strategies.

Challenges in the North America Crop Protection Chemicals Industry Market

Long-term growth catalysts for the North America crop protection chemicals industry are rooted in continuous innovation, strategic partnerships, and expanding market reach. The development of next-generation crop protection chemicals with improved environmental profiles and novel modes of action will be crucial for sustained market relevance. Strategic collaborations between chemical manufacturers, seed companies, and technology providers are essential for offering integrated solutions that address the complex challenges faced by farmers. Expanding into emerging crop segments and addressing niche pest challenges will also unlock new avenues for growth. Furthermore, the increasing focus on biopesticides and integrated pest management (IPM) presents an opportunity for companies to diversify their portfolios and cater to a broader range of farmer preferences and regulatory requirements, ensuring long-term market resilience and expansion.

Emerging Opportunities in North America Crop Protection Chemicals Industry

Emerging opportunities within the North America crop protection chemicals industry are shaped by evolving agricultural practices and consumer demands. The growing adoption of biological crop protection agents, including bio-pesticides and bio-stimulants, presents a significant growth avenue as farmers seek more sustainable alternatives. The increasing use of digital agriculture platforms and AI-driven decision-making tools creates opportunities for companies to develop integrated crop protection solutions that leverage data analytics for precise application and targeted pest management. Furthermore, the demand for specialized crop protection for specialty crops and organic farming is on the rise, offering niche market potential. The development of seed treatment technologies that provide enhanced protection and nutrient delivery also represents a promising area. Consumer preference for traceable and sustainably produced food is also driving opportunities for products that can demonstrate clear environmental benefits.

Leading Players in the North America Crop Protection Chemicals Industry Sector

- FMC Corporation

- Sumitomo Chemical Co Ltd

- American Vanguard Corporation

- ADAMA Agricultural Solutions Ltd

- Bayer AG

- UPL Limited

- Syngenta Group

- Corteva Agriscience

- Nufarm Ltd

- BASF SE

Key Milestones in North America Crop Protection Chemicals Industry Industry

- July 2023: ADAMA introduced new products, Davai A Plus and Clearfield Broad-Spectrum Herbicide Solutions, for imidazolinone-tolerant legumes like lentils, peas, and soybeans, strengthening its offering for pulse crops.

- April 2023: Nufarm launched a new liquid formulation fungicide, Tourney EZ, exclusively for turf and ornamental crops based on customer demand, further solidifying its position in the turf and ornamental sector.

- March 2023: AMVAC launched a portfolio of herbicides, including Impact Core and Sinate, to combat weed resistance in maize, addressing a critical agricultural challenge.

Strategic Outlook for North America Crop Protection Chemicals Industry Market

The strategic outlook for the North America crop protection chemicals market is characterized by a dual focus on innovation and sustainability. Companies will likely continue to invest heavily in the research and development of novel active ingredients that offer enhanced efficacy, reduced environmental impact, and address increasing pest resistance. The integration of digital technologies, such as precision agriculture tools and data analytics, will be crucial for providing farmers with more efficient and targeted crop protection solutions. Furthermore, strategic partnerships and acquisitions will remain a key strategy for consolidating market share, expanding product portfolios, and accessing new technologies. The growing demand for biological solutions and integrated pest management approaches presents a significant opportunity for diversification and market penetration, ensuring long-term growth and relevance in an evolving agricultural landscape.

North America Crop Protection Chemicals Industry Segmentation

-

1. Function

- 1.1. Fungicide

- 1.2. Herbicide

- 1.3. Insecticide

- 1.4. Molluscicide

- 1.5. Nematicide

-

2. Application Mode

- 2.1. Chemigation

- 2.2. Foliar

- 2.3. Fumigation

- 2.4. Seed Treatment

- 2.5. Soil Treatment

-

3. Crop Type

- 3.1. Commercial Crops

- 3.2. Fruits & Vegetables

- 3.3. Grains & Cereals

- 3.4. Pulses & Oilseeds

- 3.5. Turf & Ornamental

-

4. Function

- 4.1. Fungicide

- 4.2. Herbicide

- 4.3. Insecticide

- 4.4. Molluscicide

- 4.5. Nematicide

-

5. Application Mode

- 5.1. Chemigation

- 5.2. Foliar

- 5.3. Fumigation

- 5.4. Seed Treatment

- 5.5. Soil Treatment

-

6. Crop Type

- 6.1. Commercial Crops

- 6.2. Fruits & Vegetables

- 6.3. Grains & Cereals

- 6.4. Pulses & Oilseeds

- 6.5. Turf & Ornamental

North America Crop Protection Chemicals Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Crop Protection Chemicals Industry Regional Market Share

Geographic Coverage of North America Crop Protection Chemicals Industry

North America Crop Protection Chemicals Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Function

- 5.1.1. Fungicide

- 5.1.2. Herbicide

- 5.1.3. Insecticide

- 5.1.4. Molluscicide

- 5.1.5. Nematicide

- 5.2. Market Analysis, Insights and Forecast - by Application Mode

- 5.2.1. Chemigation

- 5.2.2. Foliar

- 5.2.3. Fumigation

- 5.2.4. Seed Treatment

- 5.2.5. Soil Treatment

- 5.3. Market Analysis, Insights and Forecast - by Crop Type

- 5.3.1. Commercial Crops

- 5.3.2. Fruits & Vegetables

- 5.3.3. Grains & Cereals

- 5.3.4. Pulses & Oilseeds

- 5.3.5. Turf & Ornamental

- 5.4. Market Analysis, Insights and Forecast - by Function

- 5.4.1. Fungicide

- 5.4.2. Herbicide

- 5.4.3. Insecticide

- 5.4.4. Molluscicide

- 5.4.5. Nematicide

- 5.5. Market Analysis, Insights and Forecast - by Application Mode

- 5.5.1. Chemigation

- 5.5.2. Foliar

- 5.5.3. Fumigation

- 5.5.4. Seed Treatment

- 5.5.5. Soil Treatment

- 5.6. Market Analysis, Insights and Forecast - by Crop Type

- 5.6.1. Commercial Crops

- 5.6.2. Fruits & Vegetables

- 5.6.3. Grains & Cereals

- 5.6.4. Pulses & Oilseeds

- 5.6.5. Turf & Ornamental

- 5.7. Market Analysis, Insights and Forecast - by Region

- 5.7.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Function

- 6. North America Crop Protection Chemicals Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Function

- 6.1.1. Fungicide

- 6.1.2. Herbicide

- 6.1.3. Insecticide

- 6.1.4. Molluscicide

- 6.1.5. Nematicide

- 6.2. Market Analysis, Insights and Forecast - by Application Mode

- 6.2.1. Chemigation

- 6.2.2. Foliar

- 6.2.3. Fumigation

- 6.2.4. Seed Treatment

- 6.2.5. Soil Treatment

- 6.3. Market Analysis, Insights and Forecast - by Crop Type

- 6.3.1. Commercial Crops

- 6.3.2. Fruits & Vegetables

- 6.3.3. Grains & Cereals

- 6.3.4. Pulses & Oilseeds

- 6.3.5. Turf & Ornamental

- 6.4. Market Analysis, Insights and Forecast - by Function

- 6.4.1. Fungicide

- 6.4.2. Herbicide

- 6.4.3. Insecticide

- 6.4.4. Molluscicide

- 6.4.5. Nematicide

- 6.5. Market Analysis, Insights and Forecast - by Application Mode

- 6.5.1. Chemigation

- 6.5.2. Foliar

- 6.5.3. Fumigation

- 6.5.4. Seed Treatment

- 6.5.5. Soil Treatment

- 6.6. Market Analysis, Insights and Forecast - by Crop Type

- 6.6.1. Commercial Crops

- 6.6.2. Fruits & Vegetables

- 6.6.3. Grains & Cereals

- 6.6.4. Pulses & Oilseeds

- 6.6.5. Turf & Ornamental

- 6.1. Market Analysis, Insights and Forecast - by Function

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 FMC Corporation

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Sumitomo Chemical Co Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 American Vanguard Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 ADAMA Agricultural Solutions Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Bayer AG

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 UPL Limite

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Syngenta Group

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Corteva Agriscience

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Nufarm Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 BASF SE

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 FMC Corporation

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Crop Protection Chemicals Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Crop Protection Chemicals Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Crop Protection Chemicals Industry Revenue billion Forecast, by Function 2020 & 2033

- Table 2: North America Crop Protection Chemicals Industry Volume Kiloton Forecast, by Function 2020 & 2033

- Table 3: North America Crop Protection Chemicals Industry Revenue billion Forecast, by Application Mode 2020 & 2033

- Table 4: North America Crop Protection Chemicals Industry Volume Kiloton Forecast, by Application Mode 2020 & 2033

- Table 5: North America Crop Protection Chemicals Industry Revenue billion Forecast, by Crop Type 2020 & 2033

- Table 6: North America Crop Protection Chemicals Industry Volume Kiloton Forecast, by Crop Type 2020 & 2033

- Table 7: North America Crop Protection Chemicals Industry Revenue billion Forecast, by Function 2020 & 2033

- Table 8: North America Crop Protection Chemicals Industry Volume Kiloton Forecast, by Function 2020 & 2033

- Table 9: North America Crop Protection Chemicals Industry Revenue billion Forecast, by Application Mode 2020 & 2033

- Table 10: North America Crop Protection Chemicals Industry Volume Kiloton Forecast, by Application Mode 2020 & 2033

- Table 11: North America Crop Protection Chemicals Industry Revenue billion Forecast, by Crop Type 2020 & 2033

- Table 12: North America Crop Protection Chemicals Industry Volume Kiloton Forecast, by Crop Type 2020 & 2033

- Table 13: North America Crop Protection Chemicals Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 14: North America Crop Protection Chemicals Industry Volume Kiloton Forecast, by Region 2020 & 2033

- Table 15: North America Crop Protection Chemicals Industry Revenue billion Forecast, by Function 2020 & 2033

- Table 16: North America Crop Protection Chemicals Industry Volume Kiloton Forecast, by Function 2020 & 2033

- Table 17: North America Crop Protection Chemicals Industry Revenue billion Forecast, by Application Mode 2020 & 2033

- Table 18: North America Crop Protection Chemicals Industry Volume Kiloton Forecast, by Application Mode 2020 & 2033

- Table 19: North America Crop Protection Chemicals Industry Revenue billion Forecast, by Crop Type 2020 & 2033

- Table 20: North America Crop Protection Chemicals Industry Volume Kiloton Forecast, by Crop Type 2020 & 2033

- Table 21: North America Crop Protection Chemicals Industry Revenue billion Forecast, by Function 2020 & 2033

- Table 22: North America Crop Protection Chemicals Industry Volume Kiloton Forecast, by Function 2020 & 2033

- Table 23: North America Crop Protection Chemicals Industry Revenue billion Forecast, by Application Mode 2020 & 2033

- Table 24: North America Crop Protection Chemicals Industry Volume Kiloton Forecast, by Application Mode 2020 & 2033

- Table 25: North America Crop Protection Chemicals Industry Revenue billion Forecast, by Crop Type 2020 & 2033

- Table 26: North America Crop Protection Chemicals Industry Volume Kiloton Forecast, by Crop Type 2020 & 2033

- Table 27: North America Crop Protection Chemicals Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 28: North America Crop Protection Chemicals Industry Volume Kiloton Forecast, by Country 2020 & 2033

- Table 29: United States North America Crop Protection Chemicals Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: United States North America Crop Protection Chemicals Industry Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 31: Canada North America Crop Protection Chemicals Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Canada North America Crop Protection Chemicals Industry Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 33: Mexico North America Crop Protection Chemicals Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Mexico North America Crop Protection Chemicals Industry Volume (Kiloton) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Crop Protection Chemicals Industry?

The projected CAGR is approximately 4.6%.

2. Which companies are prominent players in the North America Crop Protection Chemicals Industry?

Key companies in the market include FMC Corporation, Sumitomo Chemical Co Ltd, American Vanguard Corporation, ADAMA Agricultural Solutions Ltd, Bayer AG, UPL Limite, Syngenta Group, Corteva Agriscience, Nufarm Ltd, BASF SE.

3. What are the main segments of the North America Crop Protection Chemicals Industry?

The market segments include Function, Application Mode, Crop Type, Function, Application Mode, Crop Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 76.18 billion as of 2022.

5. What are some drivers contributing to market growth?

Seed Treatment As A Solution To Enhance Yield; Growing Awareness For Seed Treatment Among The Farmers; Rising Trend Of Organic Farming.

6. What are the notable trends driving market growth?

The United States dominated the market due to the increased demand to protect crops from pests and diseases.

7. Are there any restraints impacting market growth?

Limitations Across Farm-Level Seed Treatment; Rising Environmental Concerns.

8. Can you provide examples of recent developments in the market?

July 2023: ADAMA introduced new products, Davai A Plus and Clearfield Broad-Spectrum Herbicide Solutions, for imidazolinone-tolerant legumes like lentils, peas, and soybeans.April 2023: Nufarm launched a new liquid formulation fungicide, Tourney EZ, exclusively for turf and ornamental crops based on customer demand, which further strengthens the company's role in turf and ornamental crop protection.March 2023: AMVAC launched a portfolio of herbicides, including Impact Core and Sinate, to combat weed resistance in maize.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in Kiloton.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Crop Protection Chemicals Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Crop Protection Chemicals Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Crop Protection Chemicals Industry?

To stay informed about further developments, trends, and reports in the North America Crop Protection Chemicals Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence