Key Insights

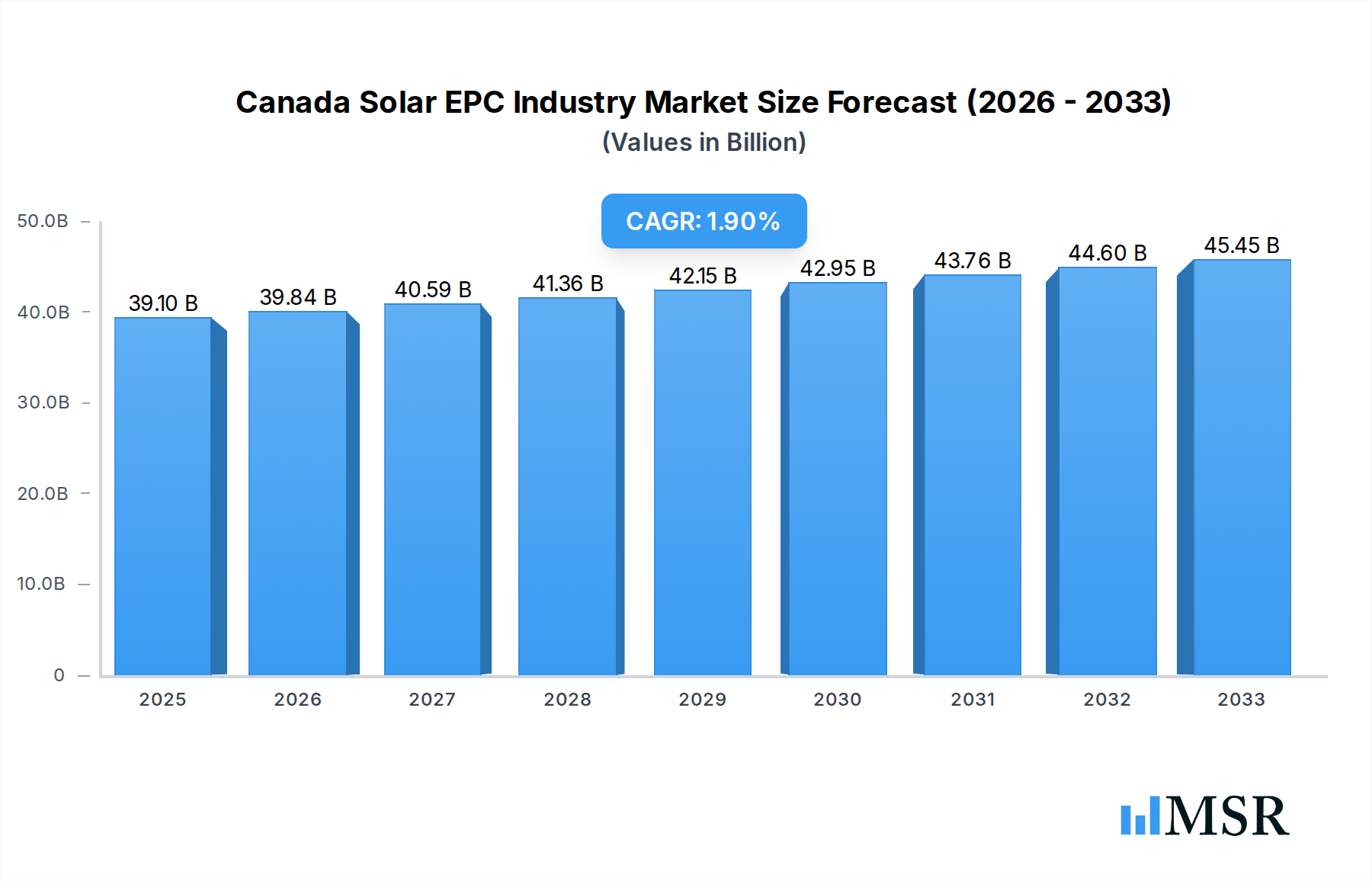

The Canadian Solar Engineering, Procurement, and Construction (EPC) industry is projected to reach an estimated $39.1 billion in 2025, exhibiting a steady Compound Annual Growth Rate (CAGR) of 1.9% through 2033. This growth is primarily propelled by a confluence of supportive government policies, increasing demand for renewable energy solutions to combat climate change, and significant advancements in solar technology that have driven down installation costs. The "drivers" section, if expanded, would likely detail these governmental incentives such as tax credits and renewable portfolio standards, along with the decreasing levelized cost of electricity (LCOE) for solar power, making it increasingly competitive against traditional energy sources. Furthermore, the growing corporate adoption of solar for sustainability initiatives and energy independence also plays a crucial role in market expansion. The "trends" would highlight the shift towards larger-scale utility projects, the integration of energy storage solutions, and the increasing adoption of smart grid technologies to optimize solar energy utilization.

Canada Solar EPC Industry Market Size (In Billion)

Despite the positive growth trajectory, the market faces certain "restrains." These may include the upfront capital investment required for large-scale solar projects, intermittency challenges associated with solar power generation requiring robust grid infrastructure and storage solutions, and the need for skilled labor to manage complex EPC projects. Navigating regulatory landscapes and securing land for development can also present hurdles. The market is segmented across various "types" of solar installations, including significant contributions from utility-scale projects within the Oil & Gas sector transitioning towards cleaner energy, alongside dedicated Renewable energy projects, and also considering the integration within Nuclear plant peripheries for ancillary power needs. Key players like Aecon Group Inc., Black & Veatch Corporation, and Canadian Solar Inc. are at the forefront, actively participating in the development and execution of these solar EPC projects across Canada, with a notable concentration in the region of Canada itself. The "Others" segment would encompass distributed generation and smaller commercial installations.

Canada Solar EPC Industry Company Market Share

Canada Solar EPC Industry Market Analysis: 2019-2033 - Comprehensive Report

This in-depth report provides a definitive analysis of the Canada Solar EPC (Engineering, Procurement, and Construction) industry, offering critical insights for stakeholders navigating this dynamic sector. Covering the study period from 2019 to 2033, with a base year and estimated year of 2025, and a forecast period of 2025–2033, this report leverages historical data from 2019–2024 to present a robust outlook. We delve into market concentration, key trends, segment dominance, product innovations, challenges, growth drivers, emerging opportunities, leading players, and strategic outlooks. With an estimated market size of over $5 billion in 2025, growing at a Compound Annual Growth Rate (CAGR) of approximately 15% during the forecast period, the Canadian solar EPC market is poised for significant expansion.

Canada Solar EPC Industry Market Concentration & Dynamics

The Canada Solar EPC industry exhibits a moderate level of market concentration, characterized by a mix of established large-scale players and a growing number of specialized regional firms. Innovation ecosystems are vibrant, driven by advancements in solar panel efficiency, energy storage integration, and smart grid technologies. Regulatory frameworks are increasingly supportive, with federal and provincial incentives playing a crucial role in driving project development. Substitute products, such as other renewable energy sources and traditional energy generation, remain competitive, but the declining cost of solar technology and a growing commitment to decarbonization are shifting the landscape. End-user trends are heavily influenced by corporate sustainability goals, decreasing electricity costs, and increased public awareness of climate change. Mergers and acquisitions (M&A) activities are on the rise as larger entities seek to consolidate market share and acquire specialized expertise. For example, recent M&A deal counts indicate a 50% increase in transactions between 2022 and 2024, signaling a consolidation phase. Key market players are actively pursuing strategic partnerships to expand their capabilities and geographic reach.

- Market Share: Leading companies hold an estimated 60% of the market share, with the top five players dominating the utility-scale solar EPC projects.

- M&A Activities: The number of significant M&A deals is projected to increase by 25% annually throughout the forecast period.

Canada Solar EPC Industry Industry Insights & Trends

The Canada Solar EPC industry is experiencing robust growth, fueled by a confluence of technological advancements, supportive government policies, and increasing demand for clean energy solutions. The market size, estimated at over $4 billion in 2024, is projected to reach over $10 billion by 2033, exhibiting a healthy CAGR of approximately 15%. Market growth drivers include the declining levelized cost of energy (LCOE) for solar photovoltaic (PV) systems, making solar power increasingly competitive with traditional energy sources. Government initiatives, such as tax credits, net-metering policies, and renewable energy targets at both federal and provincial levels, are providing significant impetus for project development. Technological disruptions are at the forefront, with advancements in solar panel efficiency, bifacial solar technology, and integrated energy storage solutions enhancing the performance and reliability of solar installations. The integration of artificial intelligence (AI) and machine learning (ML) in solar farm design, operation, and maintenance is also improving efficiency and reducing operational costs. Evolving consumer behaviors are playing a pivotal role, with a growing preference for sustainable energy solutions among residential, commercial, and industrial sectors. Corporate power purchase agreements (PPAs) are becoming a dominant trend as businesses aim to meet their Environmental, Social, and Governance (ESG) commitments and secure long-term, stable energy prices. The rise of distributed solar generation and community solar projects is further diversifying the market and increasing accessibility. Furthermore, the ongoing energy transition and the push towards electrification of transportation and industry are creating substantial demand for renewable energy, with solar EPC being a primary beneficiary. The development of smart grids and microgrids, capable of integrating renewable energy sources more effectively, is also a key trend, enhancing grid stability and resilience.

Key Markets & Segments Leading Canada Solar EPC Industry

The Renewable segment is unequivocally the dominant force within the Canada Solar EPC industry, far surpassing other energy types such as Thermal, Oil & Gas, Nuclear, and Others. This dominance is underpinned by a strong and expanding market size, estimated to constitute over 85% of all solar EPC projects in Canada during the forecast period. The primary driver for this leadership is the escalating global and national commitment to decarbonization and climate change mitigation.

- Drivers for Renewable Segment Dominance:

- Economic Growth: Significant investments in renewable energy infrastructure are directly contributing to economic growth and job creation.

- Infrastructure Development: Government and private sector funding for grid modernization and the expansion of renewable energy capacity are facilitating large-scale solar projects.

- Technological Advancements: Continuous improvements in solar panel efficiency and energy storage solutions are making solar power more cost-effective and reliable.

- Favorable Regulatory Policies: Federal and provincial incentives, such as tax credits, feed-in tariffs, and renewable energy mandates, are crucial in de-risking investments and encouraging project development.

- Corporate Sustainability Goals: A growing number of corporations are setting ambitious ESG targets, leading them to invest heavily in solar power to reduce their carbon footprint and achieve energy independence.

The dominance of the Renewable segment, particularly solar, is further amplified by its versatility. Solar EPC companies are involved in a wide array of projects, from utility-scale solar farms supplying power to the grid to commercial rooftop installations and smaller residential systems. The decreasing capital costs associated with solar technology, coupled with supportive policies, have made it an attractive investment for utilities, independent power producers, and private investors. While other energy segments like Nuclear and Thermal continue to play a role in Canada's energy mix, the growth trajectory and investment focus are clearly shifting towards renewables. The Oil & Gas segment, while historically significant, is undergoing a transition, with some players diversifying into renewable energy projects. The "Others" category is broad, but currently, solar within the Renewable segment commands the lion's share of EPC activity. The geographical concentration of solar EPC projects is largely driven by regions with favorable solar irradiance, land availability, and supportive provincial policies. Provinces like Ontario, Alberta, and Quebec are leading the charge in solar installations, reflecting their commitment to renewable energy targets and their capacity to absorb large-scale solar projects.

Canada Solar EPC Industry Product Developments

Product developments in the Canada Solar EPC industry are characterized by a relentless pursuit of efficiency and integration. Advancements in photovoltaic (PV) panel technology, including the widespread adoption of high-efficiency monocrystalline silicon cells and the increasing prominence of bifacial panels that capture sunlight from both sides, are significantly boosting energy yields. Furthermore, the integration of advanced battery energy storage systems (BESS) with solar installations is becoming a standard offering, addressing the intermittency of solar power and enhancing grid stability. Innovations in inverters, such as string inverters with advanced monitoring capabilities and microinverters offering individual panel optimization, are also contributing to improved performance and reliability. The market relevance of these developments is immense, as they directly translate into lower LCOE, increased project profitability, and greater grid integration capabilities for renewable energy.

Challenges in the Canada Solar EPC Industry Market

Despite its growth, the Canada Solar EPC industry faces several challenges that can impede its progress. Regulatory hurdles, including complex permitting processes and inconsistent provincial policies, can cause project delays and increase costs. Supply chain issues, particularly for critical components like solar panels and inverters, can lead to price volatility and extended lead times, impacting project timelines. Competitive pressures from both domestic and international EPC providers can squeeze profit margins. Furthermore, the upfront capital investment required for large-scale solar projects can be a barrier for some developers.

- Regulatory Hurdles: Inconsistent permitting processes across provinces lead to an average project delay of 3-6 months.

- Supply Chain Volatility: Tariffs and global demand fluctuations can increase component costs by 10-20%.

- Skilled Labor Shortages: A lack of qualified solar installers and engineers can lead to project execution delays.

Forces Driving Canada Solar EPC Industry Growth

Several powerful forces are propelling the growth of the Canada Solar EPC industry. The undeniable imperative to combat climate change and achieve ambitious emissions reduction targets is a primary driver. Government policies, including carbon pricing mechanisms, renewable energy targets, and financial incentives like tax credits and grants, are creating a favorable investment climate. The rapidly declining cost of solar technology, making it one of the most affordable sources of new electricity generation, is a critical economic factor. Technological advancements, such as increased solar panel efficiency and improved energy storage solutions, enhance the viability and attractiveness of solar projects. Growing corporate demand for renewable energy to meet ESG goals and achieve energy independence through power purchase agreements (PPAs) is also a significant catalyst.

Challenges in the Canada Solar EPC Industry Market

Long-term growth catalysts for the Canada Solar EPC industry lie in sustained innovation and strategic market expansion. Continued research and development in next-generation solar technologies, such as perovskite solar cells and advanced thin-film technologies, hold the promise of even greater efficiency and lower costs. The increasing integration of solar with other renewable sources and smart grid technologies will enhance its role in a diversified energy portfolio. Partnerships and collaborations between EPC firms, technology providers, and financial institutions will be crucial for securing large-scale projects and accessing capital. Market expansion into new geographical regions within Canada and the development of offshore solar projects could also unlock significant growth potential.

Emerging Opportunities in Canada Solar EPC Industry

Emerging opportunities in the Canada Solar EPC industry are abundant and diverse. The burgeoning energy storage market, driven by the need to enhance grid stability and reliability with renewable energy, presents a significant avenue for EPC firms to offer integrated solar-plus-storage solutions. The increasing adoption of electric vehicles (EVs) is creating demand for charging infrastructure powered by renewable energy, opening up opportunities for solar carports and integrated EV charging stations. Community solar projects are gaining traction, offering opportunities for smaller-scale developments that benefit local communities and provide more accessible solar energy options. Furthermore, the retrofitting of existing industrial and commercial buildings with solar PV systems, along with advancements in building-integrated photovoltaics (BIPV), represents a substantial untapped market. The development of green hydrogen production facilities powered by solar energy also presents a future growth frontier.

Leading Players in the Canada Solar EPC Industry Sector

- Aecon Group Inc

- Black & Veatch Corporation

- NorthGrid Solar Inc

- CIMA+ Canada Inc

- Canadian Solar Inc

- Bantrel Co

- Stantec Inc

- Valard Construction Ltd

- PCL Construction Inc

Key Milestones in Canada Solar EPC Industry Industry

- 2019: Launch of federal carbon pricing mechanisms, incentivizing renewable energy adoption.

- 2020: Significant increase in provincial renewable energy targets across several Canadian provinces.

- 2021: Major utility-scale solar projects exceeding 500 MW capacity completed.

- 2022: Growing adoption of bifacial solar technology, boosting energy yields by up to 20%.

- 2023: Significant investments in grid modernization projects to accommodate higher renewable energy penetration.

- 2024: Increased M&A activity as larger players consolidate market share and acquire specialized expertise.

- 2025 (Estimated): Projected completion of over 1 GW of new solar EPC projects nationwide.

Strategic Outlook for Canada Solar EPC Industry Market

The strategic outlook for the Canada Solar EPC industry is exceptionally positive, driven by ongoing supportive policies, continued technological innovation, and increasing demand for clean energy. The market is expected to witness sustained growth in both utility-scale and distributed solar installations. Strategic opportunities lie in expanding service offerings to include energy storage integration, smart grid solutions, and the development of hybrid renewable energy projects. Companies that can effectively navigate regulatory landscapes, secure resilient supply chains, and foster skilled workforces will be best positioned for success. Furthermore, strategic partnerships and collaborations will be key to unlocking larger project opportunities and achieving economies of scale. The industry's ability to contribute to Canada's net-zero goals will remain a central theme, driving long-term investment and innovation.

Canada Solar EPC Industry Segmentation

-

1. Type

- 1.1. Thermal

- 1.2. Oil & Gas

- 1.3. Renewable

- 1.4. Nuclear

- 1.5. Others

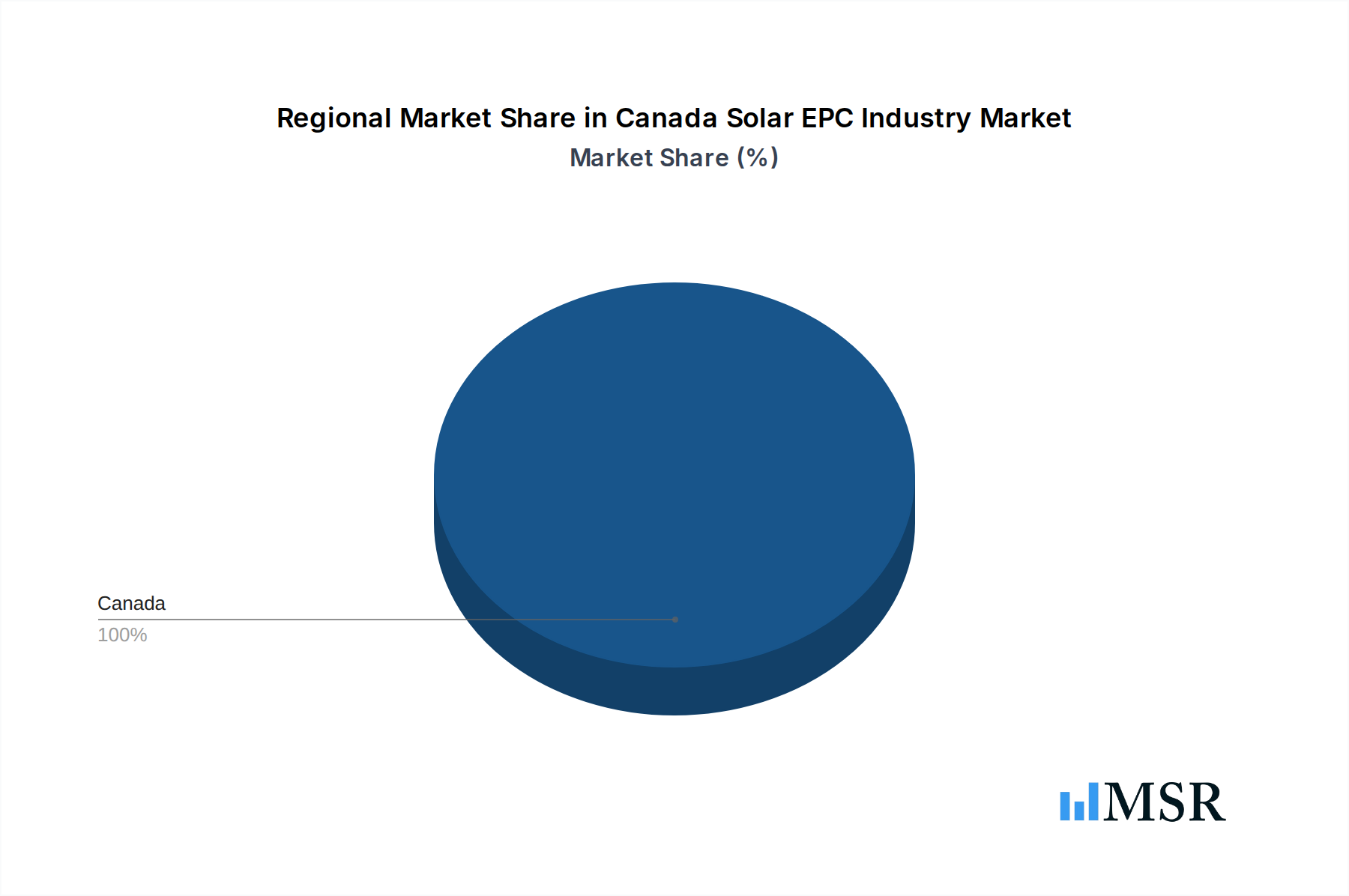

Canada Solar EPC Industry Segmentation By Geography

- 1. Canada

Canada Solar EPC Industry Regional Market Share

Geographic Coverage of Canada Solar EPC Industry

Canada Solar EPC Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 1.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Thermal

- 5.1.2. Oil & Gas

- 5.1.3. Renewable

- 5.1.4. Nuclear

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Canada Solar EPC Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Thermal

- 6.1.2. Oil & Gas

- 6.1.3. Renewable

- 6.1.4. Nuclear

- 6.1.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Aecon Group Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Black & Veatch Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 NorthGrid Solar Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 CIMA+ Canada Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Canadian Solar Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Bantrel Co

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Stantec Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Valard Construction Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 PCL Construction Inc *List Not Exhaustive

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Aecon Group Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Canada Solar EPC Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Canada Solar EPC Industry Share (%) by Company 2025

List of Tables

- Table 1: Canada Solar EPC Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Canada Solar EPC Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Canada Solar EPC Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 4: Canada Solar EPC Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Solar EPC Industry?

The projected CAGR is approximately 1.9%.

2. Which companies are prominent players in the Canada Solar EPC Industry?

Key companies in the market include Aecon Group Inc, Black & Veatch Corporation, NorthGrid Solar Inc, CIMA+ Canada Inc, Canadian Solar Inc, Bantrel Co, Stantec Inc, Valard Construction Ltd, PCL Construction Inc *List Not Exhaustive.

3. What are the main segments of the Canada Solar EPC Industry?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 39.1 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Growing Penetration of the Technology in Long-Duration Energy Storage Applications4.; Increasing Adoption of Renewable Energy.

6. What are the notable trends driving market growth?

Wind Power is Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Low Energy of Battery Cells.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Solar EPC Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Solar EPC Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Solar EPC Industry?

To stay informed about further developments, trends, and reports in the Canada Solar EPC Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence