Key Insights

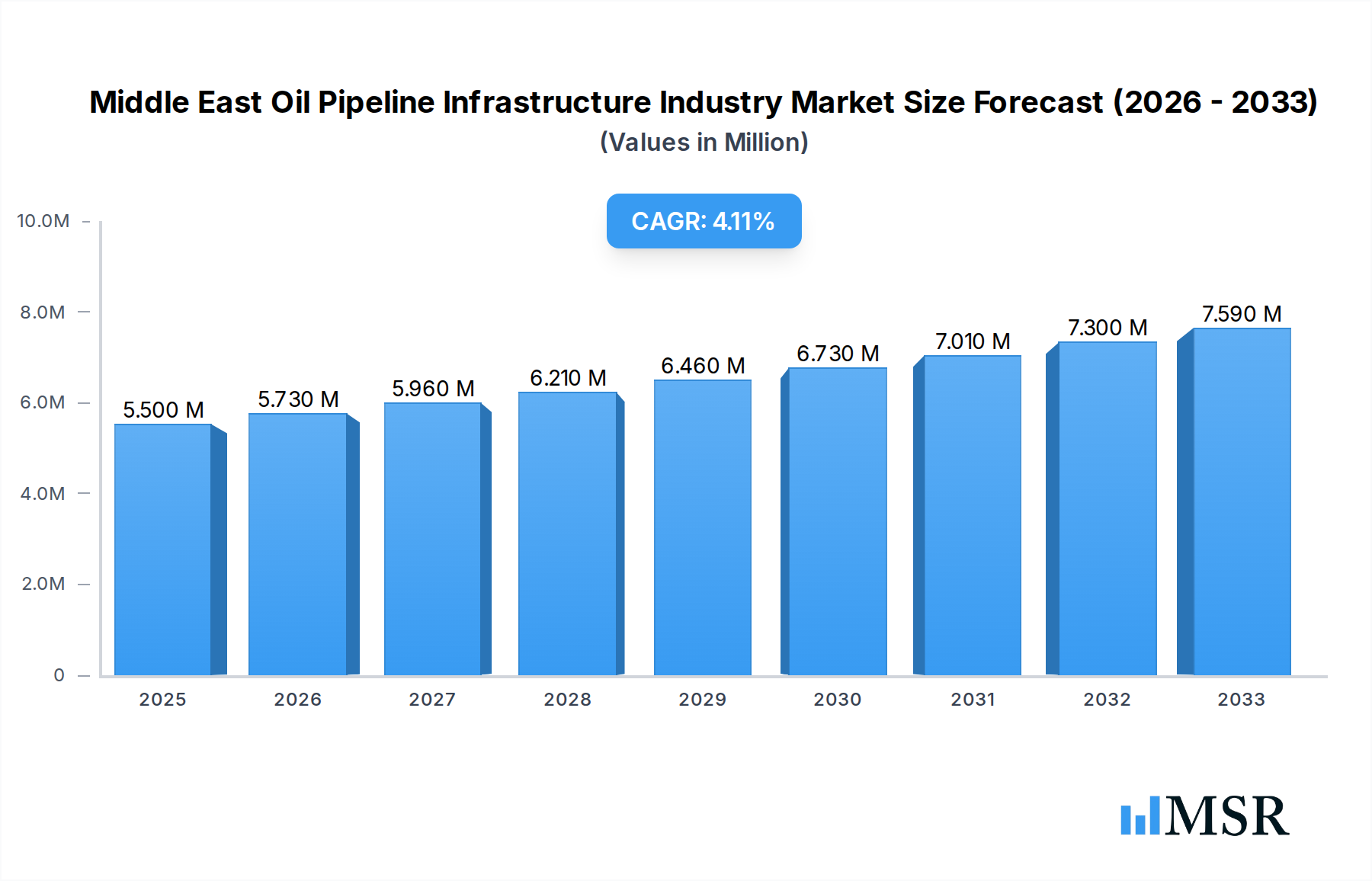

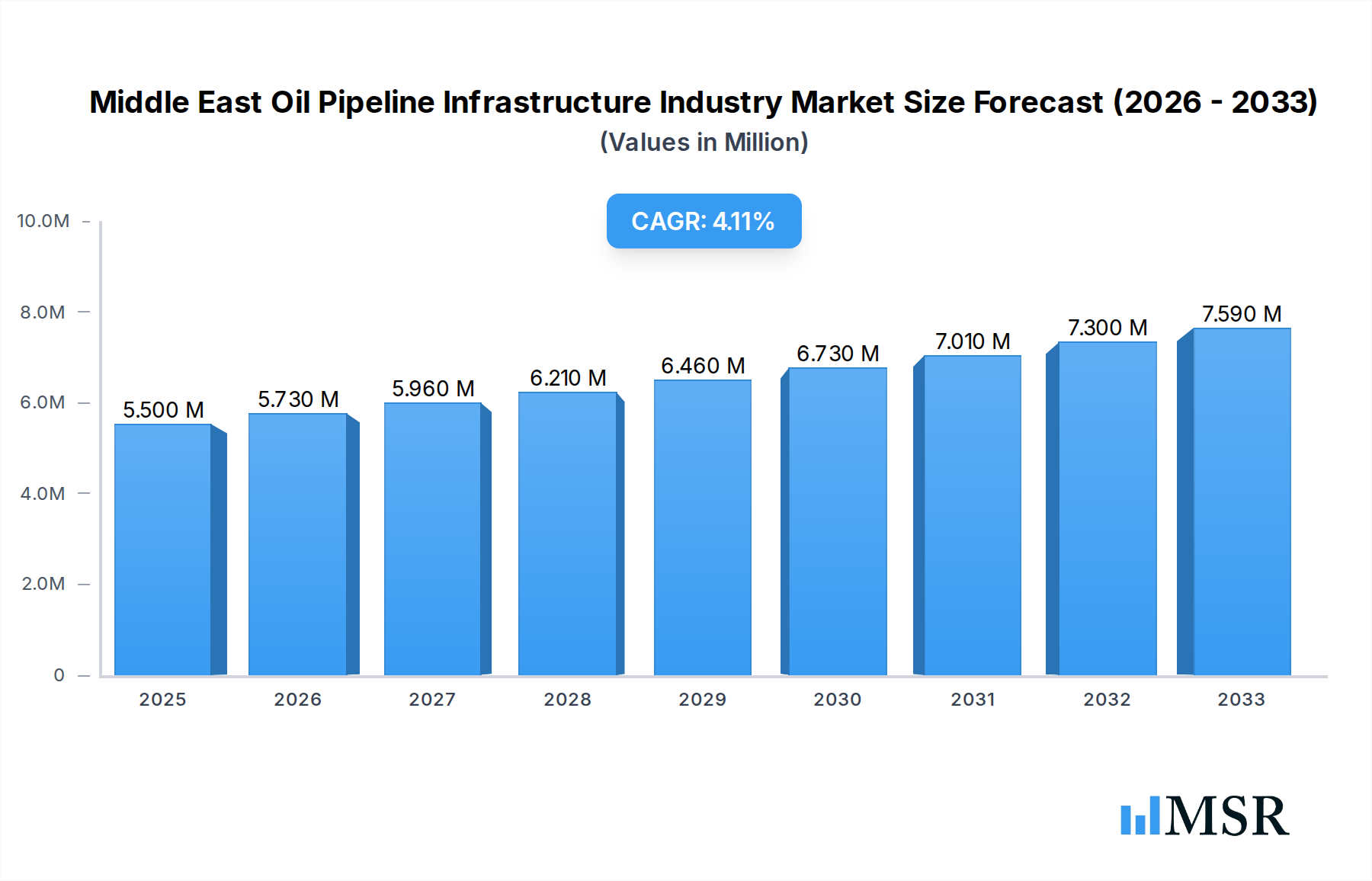

The Middle East Oil Pipeline Infrastructure Industry is poised for significant expansion, with the market size currently estimated at $5.50 million in 2025. This growth is fueled by a robust Compound Annual Growth Rate (CAGR) of 4.12%, projecting a healthy trajectory through to 2033. The region's strategic importance as a global energy hub, coupled with ongoing investments in expanding oil and gas production capacity and downstream refining operations, are the primary drivers. Initiatives aimed at enhancing energy security, diversifying export routes, and modernizing existing infrastructure to meet growing global demand are further stimulating market activity. Technological advancements in pipeline construction, leak detection, and monitoring systems are also playing a crucial role in driving efficiency and safety, underpinning the sector's growth.

Middle East Oil Pipeline Infrastructure Industry Market Size (In Million)

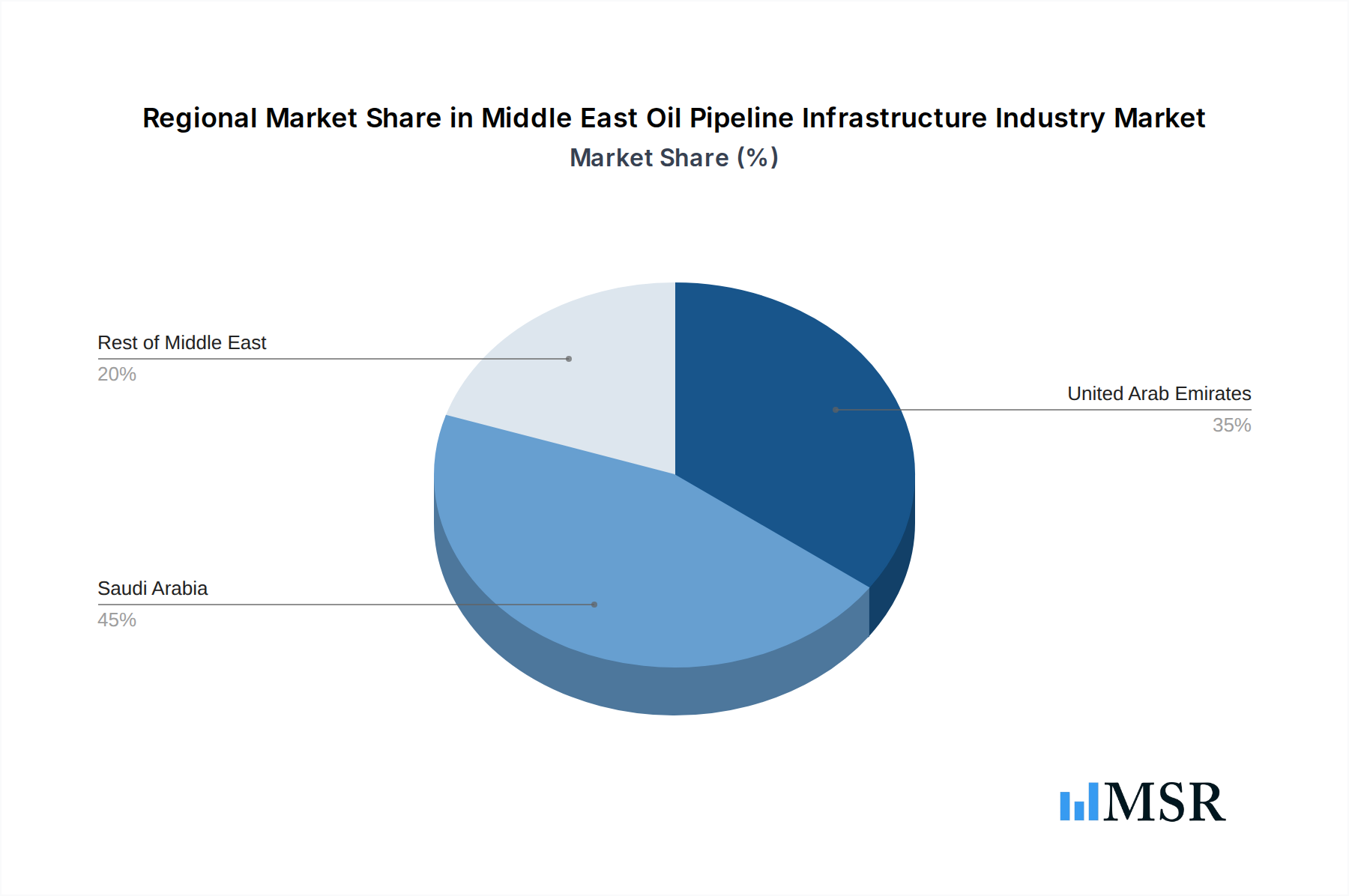

The market is segmented into two primary types: Seamless and Welded pipelines, with both experiencing increased demand due to varied application requirements in the oil and gas sector. Geographically, Saudi Arabia and the United Arab Emirates are leading the charge in market development, driven by substantial government investments in oil and gas infrastructure and ambitious national visions focused on economic diversification. The "Rest of the Middle East" region also presents considerable growth potential as these nations seek to leverage their hydrocarbon resources. Key players such as Vallourec SA, Sumitomo Corporation, and Jindal SAW Ltd are actively participating in this dynamic market, contributing to innovation and infrastructure development. Despite the strong growth outlook, potential restraints such as fluctuating crude oil prices and geopolitical complexities in the region could influence the pace of investment and project execution. However, the fundamental demand for reliable oil transportation infrastructure ensures continued market resilience.

Middle East Oil Pipeline Infrastructure Industry Company Market Share

Here's the SEO-optimized and engaging report description for the Middle East Oil Pipeline Infrastructure Industry, ready for immediate use:

Middle East Oil Pipeline Infrastructure Industry: Market Analysis, Trends, and Future Outlook (2019–2033)

This comprehensive report offers an in-depth analysis of the Middle East Oil Pipeline Infrastructure Industry, a critical sector powering the region's global energy significance. Spanning from the historical period of 2019–2024 through to a forecast period of 2025–2033, with a base year of 2025, this study provides unparalleled insights into market dynamics, growth drivers, and future opportunities. We delve into the intricacies of pipeline construction, maintenance, and operational advancements, catering to stakeholders including oil and gas companies, pipeline manufacturers, EPC contractors, investors, and government bodies. Understand the evolving landscape shaped by technological innovations, geopolitical shifts, and increasing demand for efficient energy transportation across the United Arab Emirates, Saudi Arabia, and the Rest of Middle East.

Middle East Oil Pipeline Infrastructure Industry Market Concentration & Dynamics

The Middle East Oil Pipeline Infrastructure Industry exhibits a moderate to high market concentration, with a few dominant players accounting for a significant portion of project execution and material supply. Innovation is a key differentiator, focusing on advanced materials for enhanced durability, leak detection technologies, and smart pipeline management systems. Regulatory frameworks are robust, emphasizing stringent safety standards, environmental protection, and national content policies. Substitute products, primarily alternative transportation methods like shipping, are continuously evaluated against the cost-effectiveness and reliability of pipeline networks. End-user trends are increasingly geared towards optimizing existing infrastructure, expanding capacity for both crude oil and natural gas, and embracing digital transformation for operational efficiency. Mergers and acquisitions (M&A) activities are sporadic but strategic, often aimed at consolidating market share, acquiring specialized technological expertise, or expanding geographical reach. For instance, a recent trend involves joint ventures for mega-projects to share risks and capital investment. Market share analysis reveals that companies specializing in large-diameter welded pipes and complex project management hold a leading position. The M&A deal count for the historical period (2019-2024) is estimated at XX deals, indicating consolidation in certain niches.

Middle East Oil Pipeline Infrastructure Industry Industry Insights & Trends

The Middle East Oil Pipeline Infrastructure Industry is poised for substantial growth, driven by the region's pivotal role in global energy supply and ongoing investments in its hydrocarbon sector. The market size for oil pipeline infrastructure in the Middle East is estimated to reach approximately USD $XX Billion in the base year of 2025, with a projected Compound Annual Growth Rate (CAGR) of XX% during the forecast period of 2025–2033. This expansion is underpinned by several key factors. Firstly, the increasing global demand for oil and gas necessitates the expansion and upgrade of existing pipeline networks to ensure secure and efficient transportation. Saudi Arabia and the United Arab Emirates, as major oil producers, are at the forefront of these investments, with ambitious projects aimed at enhancing export capabilities and domestic distribution. Technological disruptions are playing a crucial role, with advancements in smart pipeline technology, including real-time monitoring, predictive maintenance using AI and IoT sensors, and the development of novel materials that offer superior resistance to corrosion and extreme temperatures. These innovations are not only improving operational efficiency and safety but also reducing the environmental footprint of pipeline operations. Evolving consumer behaviors, while less directly impactful on infrastructure, are influencing the demand for cleaner energy sources and efficient delivery, prompting investments in gas pipeline infrastructure alongside oil pipelines. Furthermore, geopolitical considerations and the need for diversified export routes are stimulating new pipeline development projects, aiming to reduce reliance on certain chokepoints. The shift towards digitalization and automation in pipeline operations is also a significant trend, promising to enhance asset integrity management and operational resilience. The market also sees a growing emphasis on seamless pipes for high-pressure applications and specialized coatings for enhanced longevity. The overall industry trend points towards a robust and technologically advanced future for oil and gas transportation in the Middle East.

Key Markets & Segments Leading Middle East Oil Pipeline Infrastructure Industry

The Middle East Oil Pipeline Infrastructure Industry is dominated by specific geographies and product segments that are driving overall market expansion and technological adoption.

Dominant Geography: Saudi Arabia

- Economic Growth: Saudi Arabia's sustained economic diversification efforts and its position as the world's largest oil exporter create a continuous demand for robust and expanding pipeline infrastructure to support its vast production capabilities. The Vision 2030 initiative, with its focus on industrial development and energy sector investment, is a significant catalyst.

- Infrastructure Development: The Kingdom is undertaking massive infrastructure projects, including the development of new oil fields, refineries, and export terminals, all of which rely heavily on extensive pipeline networks for efficient crude oil and refined product transportation.

- Strategic Importance: Saudi Arabia's strategic position in global energy markets necessitates a resilient and advanced pipeline system capable of handling large volumes and ensuring reliable supply chains.

Dominant Geography: United Arab Emirates

- Production Capacity: The UAE, with its significant oil reserves and production capacity, is a major driver for pipeline infrastructure development, particularly for connecting offshore fields to onshore processing facilities and export terminals.

- Expansion Projects: Continuous investment in expanding oil and gas production and refining capacity directly translates into a sustained demand for new pipeline construction and upgrades.

- Technological Adoption: The UAE is a frontrunner in adopting advanced technologies in its infrastructure projects, including smart pipeline solutions and high-performance materials.

Dominant Segment: Welded Pipes

- Scale of Projects: The large-scale nature of oil and gas transportation projects in the Middle East, including the construction of major trunk lines and export pipelines, predominantly utilizes welded pipes due to their cost-effectiveness and suitability for large diameters.

- Versatility: Welded pipes, including both Electric Resistance Welded (ERW) and Longitudinal Submerged Arc Welded (LSAW) variants, offer versatility in terms of diameter and wall thickness, catering to a wide range of pressure and flow requirements.

- Cost Efficiency: For high-volume, long-distance transportation of crude oil and natural gas, welded pipes generally offer a more economical solution compared to seamless pipes, making them the preferred choice for major infrastructure developments.

Segment: Seamless Pipes

- High-Pressure Applications: Seamless pipes are crucial for specific applications requiring exceptional structural integrity and resistance to high internal pressures, such as in certain sections of gas transmission networks or for transporting specialized hydrocarbon products.

- Corrosion Resistance: Seamless construction can offer inherent advantages in corrosion resistance for certain challenging environments, although advancements in coatings for welded pipes are narrowing this gap.

- Specialized Needs: While not as prevalent as welded pipes for bulk transportation, seamless pipes remain vital for niche applications and specialized segments within the broader oil and gas infrastructure.

The dominance of Saudi Arabia and the United Arab Emirates is directly linked to their substantial hydrocarbon reserves and their strategic roles in the global energy market. The preference for welded pipes in the region is a clear reflection of the scale and economic considerations of the massive pipeline projects undertaken.

Middle East Oil Pipeline Infrastructure Industry Product Developments

Product innovation in the Middle East Oil Pipeline Infrastructure Industry is significantly focused on enhancing durability, safety, and operational efficiency. Companies are developing advanced steel alloys for pipes that offer superior resistance to corrosion, sour gas environments, and extreme temperatures, thereby extending pipeline lifespans and reducing maintenance costs. Furthermore, the integration of smart technologies, such as embedded sensors for real-time integrity monitoring and leak detection, is transforming pipeline management. Innovations in coating technologies, including multi-layer epoxy and polyethylene coatings, are providing enhanced protection against external damage and environmental degradation. These advancements are critical for ensuring the reliable and safe transportation of oil and gas across challenging terrains and long distances in the region, offering competitive advantages and meeting increasingly stringent regulatory requirements.

Challenges in the Middle East Oil Pipeline Infrastructure Industry Market

The Middle East Oil Pipeline Infrastructure Industry faces several significant challenges that can impact growth and operational efficiency. These include:

- Geopolitical Instability: Regional conflicts and political tensions can disrupt supply chains, increase project risks, and deter foreign investment, leading to project delays and cost overruns.

- Regulatory Hurdles: Navigating complex and evolving regulatory landscapes, particularly concerning environmental impact assessments and safety standards across different nations, can be time-consuming and costly.

- Supply Chain Volatility: The availability and cost of raw materials, such as high-grade steel, can fluctuate significantly due to global demand and geopolitical factors, impacting project timelines and budgets. The global steel market experienced price volatility of approximately XX% in the historical period.

- Skilled Labor Shortages: A shortage of skilled engineers, technicians, and construction workers can lead to project delays and impact the quality of execution.

- Environmental Concerns: Growing awareness and stricter regulations regarding the environmental impact of infrastructure projects, including potential leaks and habitat disruption, necessitate significant investment in sustainable practices and technologies.

Forces Driving Middle East Oil Pipeline Infrastructure Industry Growth

Several key forces are propelling the growth of the Middle East Oil Pipeline Infrastructure Industry. Economically, the region's vast oil and gas reserves and its central role in global energy markets necessitate continuous investment in expanding and modernizing transportation networks. Technologically, advancements in materials science have led to the development of more durable and corrosion-resistant pipes, while innovations in smart pipeline monitoring and leak detection systems enhance safety and operational efficiency. Regulatory factors, including government initiatives to boost energy production and export capacity, and policies encouraging local manufacturing and job creation, also play a crucial role. For instance, the push for domestic production of pipeline materials in countries like Saudi Arabia is driving significant investment in manufacturing facilities, creating a multiplier effect on the industry. The ongoing demand for reliable energy supply from major consuming nations further solidifies the need for robust pipeline infrastructure in the Middle East.

Challenges in the Middle East Oil Pipeline Infrastructure Industry Market

Long-term growth catalysts for the Middle East Oil Pipeline Infrastructure Industry are multifaceted. The increasing global energy demand, particularly from developing economies in Asia, ensures a sustained need for efficient and large-scale transportation solutions, positioning the Middle East as a critical supply hub. Technological innovation continues to be a major driver, with ongoing research and development in areas like pipeline integrity management, digital twins for predictive maintenance, and advanced welding techniques promising to enhance operational reliability and reduce lifecycle costs. Strategic partnerships and joint ventures between international and regional players are fostering knowledge transfer and capital infusion, enabling the execution of mega-projects. Furthermore, the region's commitment to expanding its refining capacity and petrochemical production necessitates the development of associated pipeline networks for feedstock and product distribution, creating further avenues for growth. Market expansion into emerging energy transportation needs, such as hydrogen or CO2 pipelines, also presents a long-term growth opportunity.

Emerging Opportunities in Middle East Oil Pipeline Infrastructure Industry

Emerging opportunities within the Middle East Oil Pipeline Infrastructure Industry are driven by evolving energy landscapes and technological advancements. The increasing focus on natural gas as a cleaner transitional fuel is creating significant demand for new gas pipeline construction and the expansion of existing networks. Furthermore, the development of liquefied natural gas (LNG) export facilities, such as those in Qatar and the UAE, requires extensive pipeline connections. The potential for cross-border pipeline projects to diversify export routes and enhance regional energy security presents a substantial opportunity. Innovations in trenchless technology for pipeline installation are opening up possibilities for projects in challenging terrains, minimizing environmental impact and reducing construction time. The growing interest in carbon capture, utilization, and storage (CCUS) technologies also presents an emerging market for CO2 pipeline infrastructure. Opportunities also lie in the retrofitting and upgrading of older pipelines with advanced monitoring and automation systems to meet modern safety and efficiency standards.

Leading Players in the Middle East Oil Pipeline Infrastructure Industry Sector

- Vallourec SA

- Sumitomo Corporation

- Jindal SAW Ltd

- EEW Group

- Rezayat Group

- Arabian Pipes Company

- ArcelorMittal SA

Key Milestones in Middle East Oil Pipeline Infrastructure Industry Industry

- August 2022: Kazakhstan is expected to sell its crude oil through Azerbaijan's main oil pipeline, as the country seeks alternatives to a route threatened by Russia. Another 3.5 million metric tons of Kazakh crude per year could begin flowing through another Azeri pipeline to Georgia's Black Sea port of Supsa in 2023. This development highlights a strategic shift in energy transit routes and underscores the importance of diverse pipeline corridors.

- March 2023: Gas Arabian Services Company has been granted a USD 13.58 million engineering, procurement, and construction (EPC) contract for a gas pipeline by Advanced Petrochemical Company (Advanced). The pipeline will connect Advanced's Propane Dehydrogenation (PDH) unit to Jubail United's cracking unit for upgrading the by-product gas stream to high-value chemicals. This signifies ongoing investment in gas infrastructure and the integration of petrochemical processing, showcasing advancements in gas pipeline applications.

Strategic Outlook for Middle East Oil Pipeline Infrastructure Industry Market

The strategic outlook for the Middle East Oil Pipeline Infrastructure Industry remains highly positive, driven by robust demand fundamentals and continuous technological evolution. Future growth will be shaped by the region's commitment to expanding its oil and gas production, coupled with a growing emphasis on natural gas and potentially hydrogen transportation. Investments in smart pipeline technologies and advanced materials will continue to be critical for enhancing operational efficiency, safety, and environmental sustainability. The industry is expected to witness further strategic alliances and consolidations as companies seek to enhance their competitive edge and secure market share in large-scale projects. Emerging opportunities in CO2 transportation for CCUS initiatives and the potential development of new international export routes will also contribute to the sector's long-term expansion. Adapting to evolving energy transition pathways while capitalizing on existing hydrocarbon strengths will be key to sustained success.

Middle East Oil Pipeline Infrastructure Industry Segmentation

-

1. Type

- 1.1. Seamless

- 1.2. Welded

-

2. Geography

- 2.1. United Arab Emirates

- 2.2. Saudi Arabia

- 2.3. Rest of Middle East

Middle East Oil Pipeline Infrastructure Industry Segmentation By Geography

- 1. United Arab Emirates

- 2. Saudi Arabia

- 3. Rest of Middle East

Middle East Oil Pipeline Infrastructure Industry Regional Market Share

Geographic Coverage of Middle East Oil Pipeline Infrastructure Industry

Middle East Oil Pipeline Infrastructure Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.12% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Seamless

- 5.1.2. Welded

- 5.2. Market Analysis, Insights and Forecast - by Geography

- 5.2.1. United Arab Emirates

- 5.2.2. Saudi Arabia

- 5.2.3. Rest of Middle East

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United Arab Emirates

- 5.3.2. Saudi Arabia

- 5.3.3. Rest of Middle East

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Seamless

- 6.1.2. Welded

- 6.2. Market Analysis, Insights and Forecast - by Geography

- 6.2.1. United Arab Emirates

- 6.2.2. Saudi Arabia

- 6.2.3. Rest of Middle East

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. United Arab Emirates Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Seamless

- 7.1.2. Welded

- 7.2. Market Analysis, Insights and Forecast - by Geography

- 7.2.1. United Arab Emirates

- 7.2.2. Saudi Arabia

- 7.2.3. Rest of Middle East

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Saudi Arabia Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Seamless

- 8.1.2. Welded

- 8.2. Market Analysis, Insights and Forecast - by Geography

- 8.2.1. United Arab Emirates

- 8.2.2. Saudi Arabia

- 8.2.3. Rest of Middle East

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Rest of Middle East Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Seamless

- 9.1.2. Welded

- 9.2. Market Analysis, Insights and Forecast - by Geography

- 9.2.1. United Arab Emirates

- 9.2.2. Saudi Arabia

- 9.2.3. Rest of Middle East

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Vallourec SA

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Sumitomo Corporation

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Jindal SAW Ltd

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 EEW Group

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 Rezayat Group

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 Arabian Pipes Company

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 ArcelorMittal SA*List Not Exhaustive

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.1 Vallourec SA

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: Middle East Oil Pipeline Infrastructure Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Middle East Oil Pipeline Infrastructure Industry Share (%) by Company 2025

List of Tables

- Table 1: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 3: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 6: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 8: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 9: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 11: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 12: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Middle East Oil Pipeline Infrastructure Industry?

The projected CAGR is approximately 4.12%.

2. Which companies are prominent players in the Middle East Oil Pipeline Infrastructure Industry?

Key companies in the market include Vallourec SA, Sumitomo Corporation, Jindal SAW Ltd, EEW Group, Rezayat Group, Arabian Pipes Company, ArcelorMittal SA*List Not Exhaustive.

3. What are the main segments of the Middle East Oil Pipeline Infrastructure Industry?

The market segments include Type, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.50 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Proven Shale Gas Reserves 4.; Technological Advancement in Horizontal Drilling and Hydraulic Fracturing.

6. What are the notable trends driving market growth?

Seamless Type Segment to Witness a Significant Growth.

7. Are there any restraints impacting market growth?

4.; High Exploration Cost.

8. Can you provide examples of recent developments in the market?

August 2022: Kazakhstan is expected to sell its crude oil through Azerbaijan's main oil pipeline, as the country seeks alternatives to a route threatened by Russia. Another 3.5 million metric tons of Kazakh crude per year could begin flowing through another Azeri pipeline to Georgia's Black Sea port of Supsa in 2023.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Middle East Oil Pipeline Infrastructure Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Middle East Oil Pipeline Infrastructure Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Middle East Oil Pipeline Infrastructure Industry?

To stay informed about further developments, trends, and reports in the Middle East Oil Pipeline Infrastructure Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence