Key Insights

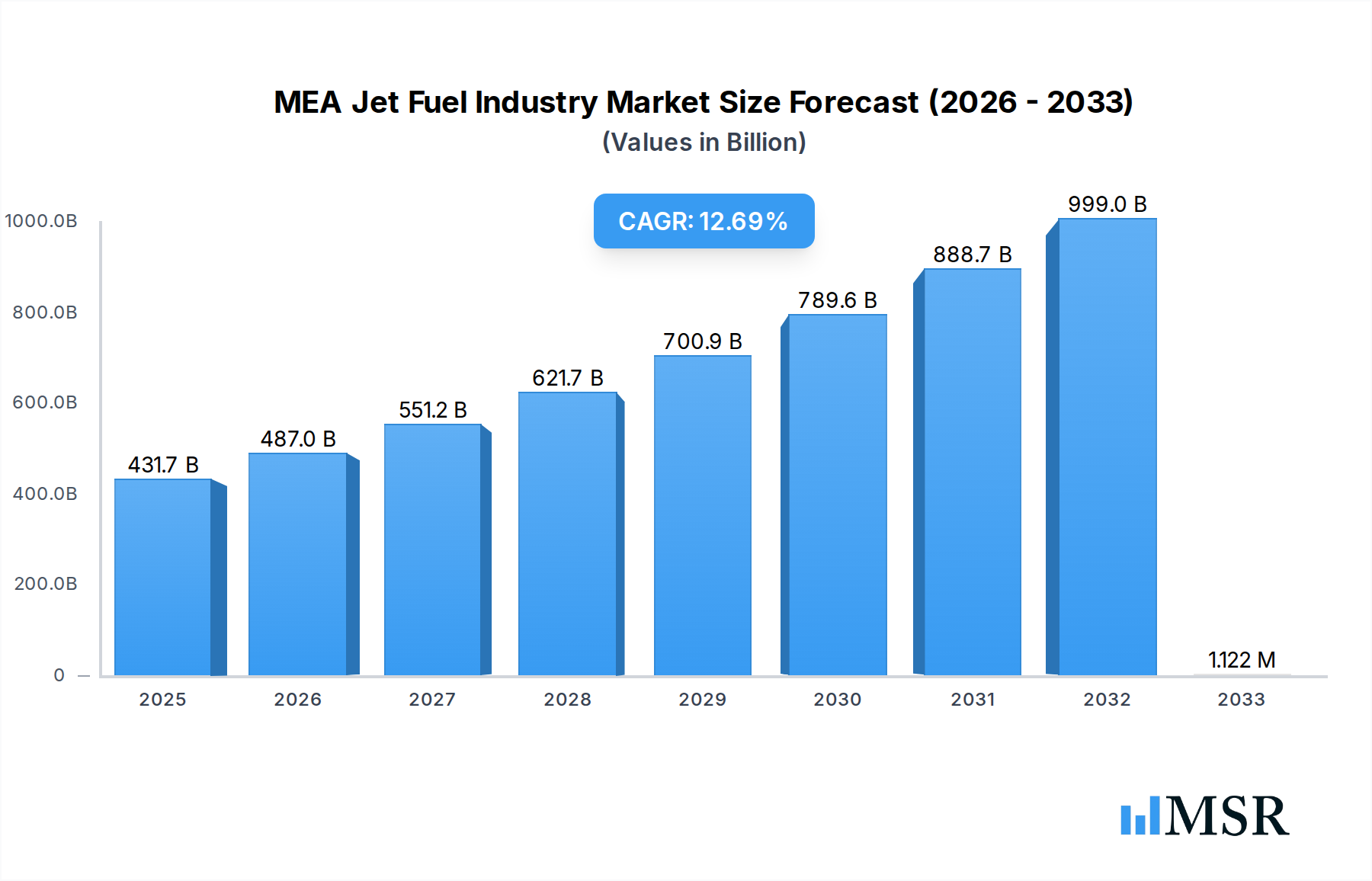

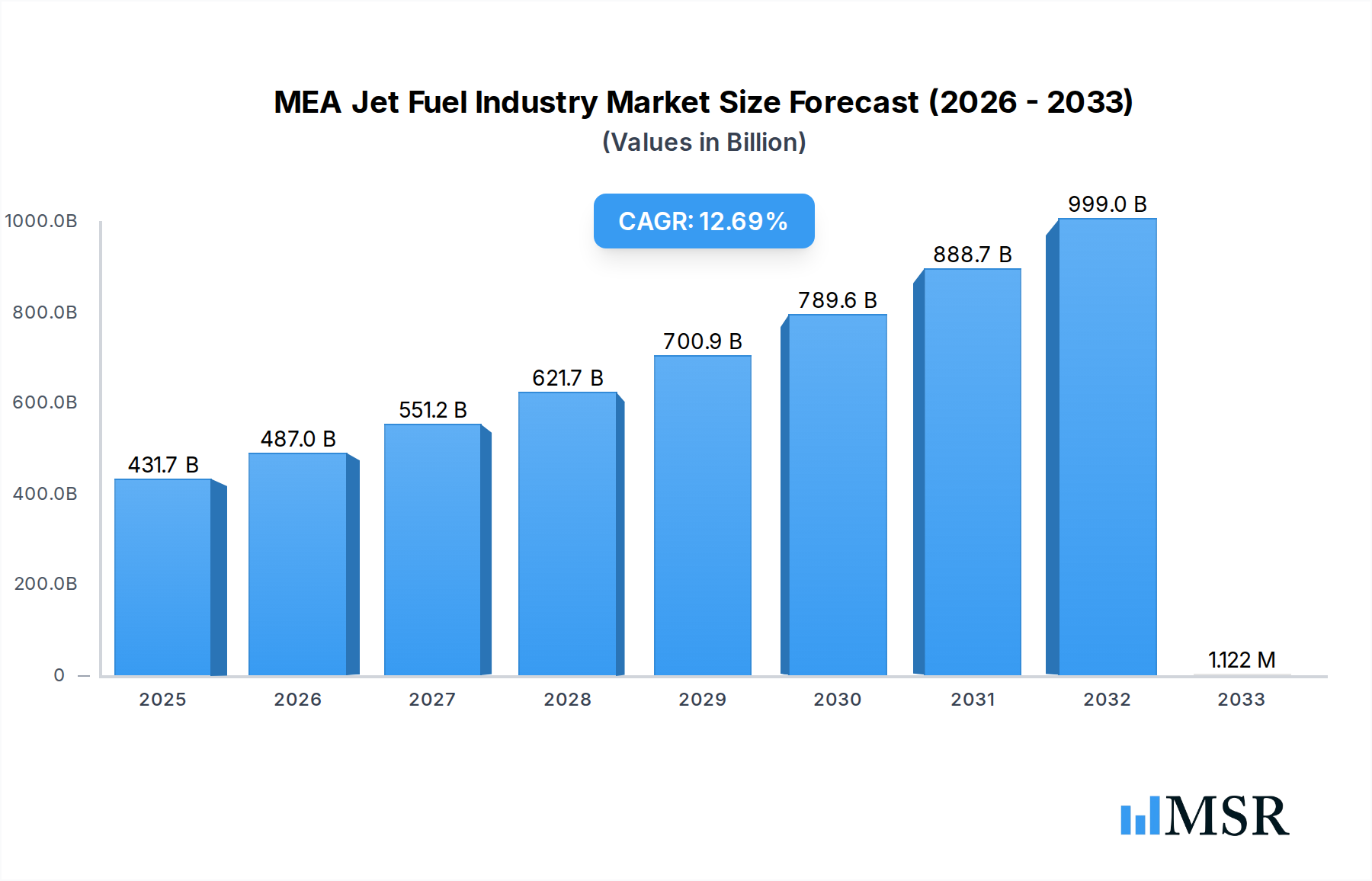

The Middle East and Africa (MEA) Jet Fuel Industry is poised for robust expansion, with a projected market size of USD 431.7 billion in 2025, driven by an impressive Compound Annual Growth Rate (CAGR) of 12.8% through 2033. This significant growth is underpinned by several key factors. The burgeoning aviation sector across the MEA region, fueled by increasing tourism, trade, and economic diversification initiatives, is a primary demand driver. Countries like the United Arab Emirates and Saudi Arabia are heavily investing in expanding their airline fleets and developing world-class airport infrastructure, directly translating to higher jet fuel consumption. Furthermore, the growing emphasis on sustainable aviation practices is propelling the adoption of aviation biofuels, representing a significant trend that will shape market dynamics. The defense sector also contributes to demand, with increased military activities and modernization efforts across various MEA nations.

MEA Jet Fuel Industry Market Size (In Billion)

While the market exhibits strong upward momentum, certain restraints need to be addressed. Fluctuations in crude oil prices, a fundamental component of jet fuel production, can impact profitability and pricing stability. Geopolitical instability in some parts of the MEA region could also pose challenges to consistent market growth and investment. However, the dominant growth trajectory is expected to be sustained by advancements in fuel efficiency technologies and the strategic expansion of commercial aviation networks. The market segmentation reveals a diverse landscape, with Air Turbine Fuel (ATF) dominating due to its widespread use in commercial aviation, followed by Aviation Biofuel's increasing prominence. Commercial aviation applications are the largest segment, followed by Defense and General Aviation. Geographically, the United Arab Emirates and Saudi Arabia are expected to lead the market, with other nations like Qatar, Egypt, and South Africa also demonstrating substantial growth potential. Major players like Shell PLC, Abu Dhabi National Oil Company, and Exxon Mobil Corporation are strategically positioned to capitalize on these market opportunities.

MEA Jet Fuel Industry Company Market Share

MEA Jet Fuel Industry Market Analysis: Fueling Growth in a Dynamic Aerospace Hub (2019-2033)

Explore the burgeoning Middle East and Africa (MEA) Jet Fuel Market, a critical sector poised for significant expansion. This comprehensive report offers deep insights into the Middle Eastern aviation fuel market and African jet fuel market dynamics, driven by robust growth in commercial aviation, defense aviation, and general aviation. Uncover the latest sustainable aviation fuel (SAF) initiatives, aviation biofuel advancements, and the dominance of Air Turbine Fuel (ATF). With a detailed analysis covering United Arab Emirates (UAE) jet fuel market, Saudi Arabia jet fuel market, Qatar jet fuel market, Egypt jet fuel market, and South Africa jet fuel market, this report is indispensable for stakeholders seeking to capitalize on opportunities within this multi-billion dollar industry. Our study period spans 2019–2033, with the base year and estimated year at 2025, and the forecast period from 2025–2033, built upon historical data from 2019–2024.

MEA Jet Fuel Industry Market Concentration & Dynamics

The MEA Jet Fuel Industry exhibits a moderate to high market concentration, with a few key players holding significant market share. The market share of dominant companies is estimated to be over xx billion USD. Innovation ecosystems are rapidly evolving, driven by the increasing demand for sustainable solutions. Regulatory frameworks are becoming more stringent, particularly concerning environmental impact and emissions reduction, incentivizing the adoption of sustainable aviation fuel (SAF). Substitute products, such as electric propulsion, are in their nascent stages but are being closely monitored. End-user trends are heavily influenced by the growth in air travel, the expansion of airline fleets, and a growing emphasis on fuel efficiency and reduced carbon footprints. Merger and acquisition (M&A) activities are anticipated to increase as companies seek to consolidate market positions, secure supply chains for novel fuels, and invest in next-generation aviation technologies. M&A deal counts are projected to rise by xx% within the forecast period.

- Market Concentration: Dominated by a mix of established energy giants and national oil companies.

- Innovation Ecosystems: Flourishing with investments in green hydrogen production for SAF and advanced biofuel research.

- Regulatory Frameworks: Increasingly focused on decarbonization targets and mandates for SAF usage.

- Substitute Products: Emerging electric and hydrogen propulsion technologies are long-term considerations.

- End-User Trends: Demand for cost-efficiency, environmental compliance, and enhanced travel experiences.

- M&A Activities: Expected to rise for strategic partnerships and acquisitions to strengthen market presence and access new technologies.

MEA Jet Fuel Industry Industry Insights & Trends

The MEA Jet Fuel Industry is poised for substantial growth, with the global market size estimated to reach over xx billion by 2025 and projected to expand at a Compound Annual Growth Rate (CAGR) of xx% during the forecast period. This expansion is primarily fueled by a resurgence in air travel post-pandemic, coupled with significant investments in aviation infrastructure across the region. Key market growth drivers include the expanding middle class in emerging economies, leading to increased demand for air travel, and the strategic development of aviation hubs in countries like the UAE and Saudi Arabia. Technological disruptions are at the forefront, with a strong push towards sustainable aviation fuel (SAF) and the exploration of green hydrogen as a feedstock for its production. Companies are actively investing in research and development to enhance the efficiency and scalability of aviation biofuel production methods. Evolving consumer behaviors are also playing a crucial role, with an increasing preference for airlines and travel options that demonstrate a commitment to environmental sustainability. This heightened awareness is prompting fuel providers and airlines to prioritize the development and adoption of lower-emission fuels. The geopolitical landscape and government initiatives aimed at diversifying economies and promoting tourism are further accelerating the demand for reliable and efficient jet fuel supply. The continuous expansion of cargo operations, driven by e-commerce growth, also contributes significantly to the overall jet fuel consumption.

Key Markets & Segments Leading MEA Jet Fuel Industry

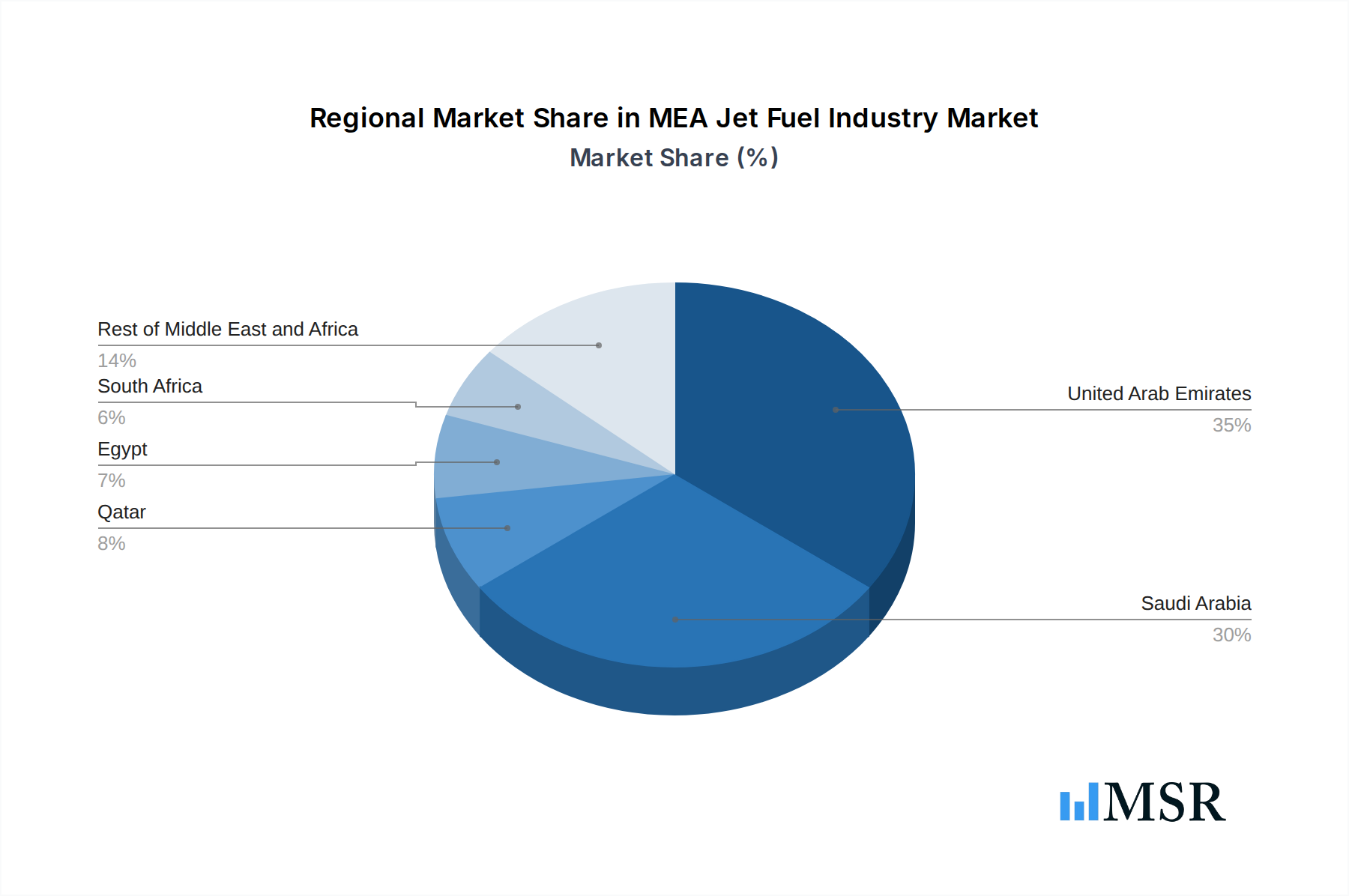

The United Arab Emirates (UAE) is currently the dominant market within the MEA Jet Fuel Industry, driven by its status as a global aviation hub with major airlines and significant cargo operations. Following closely are Saudi Arabia and Qatar, both actively investing in expanding their aviation infrastructure and tourism sectors. The Rest of Middle-East and Africa region presents considerable untapped potential for growth.

Dominant Geography:

- United Arab Emirates: Home to major airlines, extensive airport infrastructure, and a strong focus on tourism and trade, leading to consistent high demand for ATF and growing interest in SAF.

- Saudi Arabia: Undergoing massive economic diversification and tourism development initiatives, projecting substantial growth in commercial and defense aviation fuel consumption.

- Qatar: Continues to be a key transit hub with significant investments in its national carrier and airport expansion.

- Egypt: Benefiting from a growing tourism sector and increasing domestic air travel.

- South Africa: A mature aviation market with established infrastructure, but facing economic challenges that influence growth rates.

Dominant Fuel Type:

- Air Turbine Fuel (ATF): Currently the most dominant fuel type, catering to the vast majority of commercial and military aircraft. Its market share is estimated to be over xx billion.

- Aviation Biofuel: Experiencing rapid growth and investment due to sustainability mandates and corporate environmental goals. The market is projected to reach over xx billion by 2033.

- AVGAS: Primarily used in general aviation, its market share is smaller but stable, with niche growth opportunities.

Dominant Application:

- Commercial: The largest segment, driven by passenger and cargo air traffic. Expected to account for over xx% of the total market by 2033.

- Defense: A significant and consistent consumer of jet fuel, particularly in countries with strong national defense programs.

- General Aviation: While a smaller segment, it is crucial for business travel, training, and specialized services, showing steady growth.

MEA Jet Fuel Industry Product Developments

The MEA Jet Fuel Industry is witnessing significant product development focused on sustainability and enhanced performance. Innovations in Aviation Biofuel production, utilizing feedstocks like used cooking oil and agricultural waste, are gaining traction. Investments in green hydrogen technology are paving the way for advanced Sustainable Aviation Fuel (SAF) synthesis, promising reduced carbon emissions and improved fuel efficiency. The development of novel fuel blends and additives aims to optimize engine performance and extend aircraft range. These advancements are crucial for meeting evolving environmental regulations and airline demands for greener aviation solutions.

Challenges in the MEA Jet Fuel Industry Market

The MEA Jet Fuel Industry faces several challenges that could impact its growth trajectory. Regulatory hurdles, particularly in standardizing sustainable aviation fuel (SAF) certifications and mandates across diverse nations, can slow adoption. Supply chain complexities for new fuel types, including aviation biofuel and its production feedstocks, pose logistical and cost-related issues. Intense competition among established fuel suppliers and emerging SAF producers creates pricing pressures. Infrastructure limitations in certain regions for SAF distribution and blending facilities also present a significant barrier.

- Regulatory Standardization: Inconsistent SAF mandates and certification processes across MEA nations.

- Supply Chain Volatility: Ensuring consistent and scalable supply of sustainable feedstocks for biofuels.

- Infrastructure Gaps: Limited blending and distribution facilities for SAF in many parts of the region.

- Cost Competitiveness: SAF often commands a premium price compared to conventional jet fuel.

Forces Driving MEA Jet Fuel Industry Growth

Several powerful forces are driving the growth of the MEA Jet Fuel Industry. The rapid expansion of commercial aviation, fueled by increasing air passenger traffic and the growth of low-cost carriers, is a primary driver. Significant government investments in aviation infrastructure, including new airports and the expansion of existing ones, are creating greater demand. The strong push for sustainable aviation fuel (SAF), driven by global climate initiatives and airline commitments to reduce their carbon footprint, is a major growth catalyst. Furthermore, economic diversification strategies in many MEA nations, emphasizing tourism and trade, are directly boosting air travel and, consequently, jet fuel demand.

Challenges in the MEA Jet Fuel Industry Market

Long-term growth in the MEA Jet Fuel Industry is contingent upon overcoming significant challenges. The capital-intensive nature of establishing large-scale Sustainable Aviation Fuel (SAF) production facilities requires substantial investment and supportive financial frameworks. Geopolitical instability in certain sub-regions can disrupt supply chains and impact investor confidence. The high cost of Aviation Biofuel production, relative to conventional jet fuel, remains a barrier to widespread adoption without further technological advancements and economies of scale. The pace of regulatory evolution globally and within the MEA region will also significantly influence the transition to cleaner aviation fuels.

Emerging Opportunities in MEA Jet Fuel Industry

Emerging opportunities in the MEA Jet Fuel Industry are abundant, particularly in the realm of Sustainable Aviation Fuel (SAF). The region's commitment to renewable energy sources, such as solar and wind power, provides a strong foundation for green hydrogen production, a key component for advanced SAF. Developing localized aviation biofuel production capabilities using abundant agricultural and waste resources presents a significant opportunity to reduce import dependence and create local employment. Partnerships between national oil companies, technology providers, and airlines are fostering innovation in SAF development and deployment. The growth of smaller airports and the increasing demand for charter flights also create niche markets for specialized fuel solutions.

Leading Players in the MEA Jet Fuel Industry Sector

- Shell PLC

- Abu Dhabi National Oil Company

- Exxon Mobil Corporation

- Emirates National Oil Company

- Chevron Corporation

- TotalENergies SE

- BP PLC

- Repsol SA

Key Milestones in MEA Jet Fuel Industry Industry

- January 2022: Masdar, Siemens Energy, and TotalEnergies signed a partnership agreement focused on green hydrogen to produce sustainable aviation fuel (SAF), marking a significant step towards low-carbon aviation fuel production in the region.

- January 2023: AviLease and the Saudi Investment Recycling Company (SIRC) signed a Memorandum of Understanding (MoU) to launch the production and distribution of sustainable aviation fuel (SAF) to AviLease's network, indicating a growing commitment to SAF within the Saudi Arabian aviation ecosystem.

Strategic Outlook for MEA Jet Fuel Industry Market

The strategic outlook for the MEA Jet Fuel Industry is exceptionally positive, driven by a confluence of factors. The ongoing global push for decarbonization, coupled with the MEA region's proactive stance on renewable energy and economic diversification, creates a fertile ground for growth in Sustainable Aviation Fuel (SAF). Strategic investments in advanced Aviation Biofuel production technologies and the exploration of novel feedstocks will be crucial. Collaborations between industry stakeholders, governments, and research institutions will accelerate innovation and market penetration. Furthermore, the continuous expansion of aviation infrastructure and the projected increase in air traffic will sustain the demand for conventional Air Turbine Fuel (ATF) while paving the way for the gradual integration of cleaner alternatives. The MEA region is well-positioned to become a leader in the global transition to sustainable aviation.

MEA Jet Fuel Industry Segmentation

-

1. Fuel Type

- 1.1. Air Turbine Fuel (ATF)

- 1.2. Aviation Biofuel

- 1.3. AVGAS

-

2. Application

- 2.1. Commercial

- 2.2. Defense

- 2.3. General Aviation

-

3. Geography

- 3.1. United Arab Emirates

- 3.2. Saudi Arabia

- 3.3. Qatar

- 3.4. Egypt

- 3.5. South Africa

- 3.6. Rest of Middle-East and Africa

MEA Jet Fuel Industry Segmentation By Geography

- 1. United Arab Emirates

- 2. Saudi Arabia

- 3. Qatar

- 4. Egypt

- 5. South Africa

- 6. Rest of Middle East and Africa

MEA Jet Fuel Industry Regional Market Share

Geographic Coverage of MEA Jet Fuel Industry

MEA Jet Fuel Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Fuel Type

- 5.1.1. Air Turbine Fuel (ATF)

- 5.1.2. Aviation Biofuel

- 5.1.3. AVGAS

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Commercial

- 5.2.2. Defense

- 5.2.3. General Aviation

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United Arab Emirates

- 5.3.2. Saudi Arabia

- 5.3.3. Qatar

- 5.3.4. Egypt

- 5.3.5. South Africa

- 5.3.6. Rest of Middle-East and Africa

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United Arab Emirates

- 5.4.2. Saudi Arabia

- 5.4.3. Qatar

- 5.4.4. Egypt

- 5.4.5. South Africa

- 5.4.6. Rest of Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Fuel Type

- 6. Global MEA Jet Fuel Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Fuel Type

- 6.1.1. Air Turbine Fuel (ATF)

- 6.1.2. Aviation Biofuel

- 6.1.3. AVGAS

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Commercial

- 6.2.2. Defense

- 6.2.3. General Aviation

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United Arab Emirates

- 6.3.2. Saudi Arabia

- 6.3.3. Qatar

- 6.3.4. Egypt

- 6.3.5. South Africa

- 6.3.6. Rest of Middle-East and Africa

- 6.1. Market Analysis, Insights and Forecast - by Fuel Type

- 7. United Arab Emirates MEA Jet Fuel Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Fuel Type

- 7.1.1. Air Turbine Fuel (ATF)

- 7.1.2. Aviation Biofuel

- 7.1.3. AVGAS

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Commercial

- 7.2.2. Defense

- 7.2.3. General Aviation

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United Arab Emirates

- 7.3.2. Saudi Arabia

- 7.3.3. Qatar

- 7.3.4. Egypt

- 7.3.5. South Africa

- 7.3.6. Rest of Middle-East and Africa

- 7.1. Market Analysis, Insights and Forecast - by Fuel Type

- 8. Saudi Arabia MEA Jet Fuel Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Fuel Type

- 8.1.1. Air Turbine Fuel (ATF)

- 8.1.2. Aviation Biofuel

- 8.1.3. AVGAS

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Commercial

- 8.2.2. Defense

- 8.2.3. General Aviation

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. United Arab Emirates

- 8.3.2. Saudi Arabia

- 8.3.3. Qatar

- 8.3.4. Egypt

- 8.3.5. South Africa

- 8.3.6. Rest of Middle-East and Africa

- 8.1. Market Analysis, Insights and Forecast - by Fuel Type

- 9. Qatar MEA Jet Fuel Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Fuel Type

- 9.1.1. Air Turbine Fuel (ATF)

- 9.1.2. Aviation Biofuel

- 9.1.3. AVGAS

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Commercial

- 9.2.2. Defense

- 9.2.3. General Aviation

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. United Arab Emirates

- 9.3.2. Saudi Arabia

- 9.3.3. Qatar

- 9.3.4. Egypt

- 9.3.5. South Africa

- 9.3.6. Rest of Middle-East and Africa

- 9.1. Market Analysis, Insights and Forecast - by Fuel Type

- 10. Egypt MEA Jet Fuel Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Fuel Type

- 10.1.1. Air Turbine Fuel (ATF)

- 10.1.2. Aviation Biofuel

- 10.1.3. AVGAS

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Commercial

- 10.2.2. Defense

- 10.2.3. General Aviation

- 10.3. Market Analysis, Insights and Forecast - by Geography

- 10.3.1. United Arab Emirates

- 10.3.2. Saudi Arabia

- 10.3.3. Qatar

- 10.3.4. Egypt

- 10.3.5. South Africa

- 10.3.6. Rest of Middle-East and Africa

- 10.1. Market Analysis, Insights and Forecast - by Fuel Type

- 11. South Africa MEA Jet Fuel Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Fuel Type

- 11.1.1. Air Turbine Fuel (ATF)

- 11.1.2. Aviation Biofuel

- 11.1.3. AVGAS

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Commercial

- 11.2.2. Defense

- 11.2.3. General Aviation

- 11.3. Market Analysis, Insights and Forecast - by Geography

- 11.3.1. United Arab Emirates

- 11.3.2. Saudi Arabia

- 11.3.3. Qatar

- 11.3.4. Egypt

- 11.3.5. South Africa

- 11.3.6. Rest of Middle-East and Africa

- 11.1. Market Analysis, Insights and Forecast - by Fuel Type

- 12. Rest of Middle East and Africa MEA Jet Fuel Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Fuel Type

- 12.1.1. Air Turbine Fuel (ATF)

- 12.1.2. Aviation Biofuel

- 12.1.3. AVGAS

- 12.2. Market Analysis, Insights and Forecast - by Application

- 12.2.1. Commercial

- 12.2.2. Defense

- 12.2.3. General Aviation

- 12.3. Market Analysis, Insights and Forecast - by Geography

- 12.3.1. United Arab Emirates

- 12.3.2. Saudi Arabia

- 12.3.3. Qatar

- 12.3.4. Egypt

- 12.3.5. South Africa

- 12.3.6. Rest of Middle-East and Africa

- 12.1. Market Analysis, Insights and Forecast - by Fuel Type

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Shell PLC

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Abu Dhabi National Oil Company*List Not Exhaustive

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Exxon Mobil Corporation

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Emirates National Oil Company

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Chevron Corporation

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 TotalENergies SE

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 BP PLC

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Repsol SA

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.1 Shell PLC

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global MEA Jet Fuel Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global MEA Jet Fuel Industry Volume Breakdown (Litre, %) by Region 2025 & 2033

- Figure 3: United Arab Emirates MEA Jet Fuel Industry Revenue (billion), by Fuel Type 2025 & 2033

- Figure 4: United Arab Emirates MEA Jet Fuel Industry Volume (Litre), by Fuel Type 2025 & 2033

- Figure 5: United Arab Emirates MEA Jet Fuel Industry Revenue Share (%), by Fuel Type 2025 & 2033

- Figure 6: United Arab Emirates MEA Jet Fuel Industry Volume Share (%), by Fuel Type 2025 & 2033

- Figure 7: United Arab Emirates MEA Jet Fuel Industry Revenue (billion), by Application 2025 & 2033

- Figure 8: United Arab Emirates MEA Jet Fuel Industry Volume (Litre), by Application 2025 & 2033

- Figure 9: United Arab Emirates MEA Jet Fuel Industry Revenue Share (%), by Application 2025 & 2033

- Figure 10: United Arab Emirates MEA Jet Fuel Industry Volume Share (%), by Application 2025 & 2033

- Figure 11: United Arab Emirates MEA Jet Fuel Industry Revenue (billion), by Geography 2025 & 2033

- Figure 12: United Arab Emirates MEA Jet Fuel Industry Volume (Litre), by Geography 2025 & 2033

- Figure 13: United Arab Emirates MEA Jet Fuel Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 14: United Arab Emirates MEA Jet Fuel Industry Volume Share (%), by Geography 2025 & 2033

- Figure 15: United Arab Emirates MEA Jet Fuel Industry Revenue (billion), by Country 2025 & 2033

- Figure 16: United Arab Emirates MEA Jet Fuel Industry Volume (Litre), by Country 2025 & 2033

- Figure 17: United Arab Emirates MEA Jet Fuel Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: United Arab Emirates MEA Jet Fuel Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: Saudi Arabia MEA Jet Fuel Industry Revenue (billion), by Fuel Type 2025 & 2033

- Figure 20: Saudi Arabia MEA Jet Fuel Industry Volume (Litre), by Fuel Type 2025 & 2033

- Figure 21: Saudi Arabia MEA Jet Fuel Industry Revenue Share (%), by Fuel Type 2025 & 2033

- Figure 22: Saudi Arabia MEA Jet Fuel Industry Volume Share (%), by Fuel Type 2025 & 2033

- Figure 23: Saudi Arabia MEA Jet Fuel Industry Revenue (billion), by Application 2025 & 2033

- Figure 24: Saudi Arabia MEA Jet Fuel Industry Volume (Litre), by Application 2025 & 2033

- Figure 25: Saudi Arabia MEA Jet Fuel Industry Revenue Share (%), by Application 2025 & 2033

- Figure 26: Saudi Arabia MEA Jet Fuel Industry Volume Share (%), by Application 2025 & 2033

- Figure 27: Saudi Arabia MEA Jet Fuel Industry Revenue (billion), by Geography 2025 & 2033

- Figure 28: Saudi Arabia MEA Jet Fuel Industry Volume (Litre), by Geography 2025 & 2033

- Figure 29: Saudi Arabia MEA Jet Fuel Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 30: Saudi Arabia MEA Jet Fuel Industry Volume Share (%), by Geography 2025 & 2033

- Figure 31: Saudi Arabia MEA Jet Fuel Industry Revenue (billion), by Country 2025 & 2033

- Figure 32: Saudi Arabia MEA Jet Fuel Industry Volume (Litre), by Country 2025 & 2033

- Figure 33: Saudi Arabia MEA Jet Fuel Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Saudi Arabia MEA Jet Fuel Industry Volume Share (%), by Country 2025 & 2033

- Figure 35: Qatar MEA Jet Fuel Industry Revenue (billion), by Fuel Type 2025 & 2033

- Figure 36: Qatar MEA Jet Fuel Industry Volume (Litre), by Fuel Type 2025 & 2033

- Figure 37: Qatar MEA Jet Fuel Industry Revenue Share (%), by Fuel Type 2025 & 2033

- Figure 38: Qatar MEA Jet Fuel Industry Volume Share (%), by Fuel Type 2025 & 2033

- Figure 39: Qatar MEA Jet Fuel Industry Revenue (billion), by Application 2025 & 2033

- Figure 40: Qatar MEA Jet Fuel Industry Volume (Litre), by Application 2025 & 2033

- Figure 41: Qatar MEA Jet Fuel Industry Revenue Share (%), by Application 2025 & 2033

- Figure 42: Qatar MEA Jet Fuel Industry Volume Share (%), by Application 2025 & 2033

- Figure 43: Qatar MEA Jet Fuel Industry Revenue (billion), by Geography 2025 & 2033

- Figure 44: Qatar MEA Jet Fuel Industry Volume (Litre), by Geography 2025 & 2033

- Figure 45: Qatar MEA Jet Fuel Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 46: Qatar MEA Jet Fuel Industry Volume Share (%), by Geography 2025 & 2033

- Figure 47: Qatar MEA Jet Fuel Industry Revenue (billion), by Country 2025 & 2033

- Figure 48: Qatar MEA Jet Fuel Industry Volume (Litre), by Country 2025 & 2033

- Figure 49: Qatar MEA Jet Fuel Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Qatar MEA Jet Fuel Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Egypt MEA Jet Fuel Industry Revenue (billion), by Fuel Type 2025 & 2033

- Figure 52: Egypt MEA Jet Fuel Industry Volume (Litre), by Fuel Type 2025 & 2033

- Figure 53: Egypt MEA Jet Fuel Industry Revenue Share (%), by Fuel Type 2025 & 2033

- Figure 54: Egypt MEA Jet Fuel Industry Volume Share (%), by Fuel Type 2025 & 2033

- Figure 55: Egypt MEA Jet Fuel Industry Revenue (billion), by Application 2025 & 2033

- Figure 56: Egypt MEA Jet Fuel Industry Volume (Litre), by Application 2025 & 2033

- Figure 57: Egypt MEA Jet Fuel Industry Revenue Share (%), by Application 2025 & 2033

- Figure 58: Egypt MEA Jet Fuel Industry Volume Share (%), by Application 2025 & 2033

- Figure 59: Egypt MEA Jet Fuel Industry Revenue (billion), by Geography 2025 & 2033

- Figure 60: Egypt MEA Jet Fuel Industry Volume (Litre), by Geography 2025 & 2033

- Figure 61: Egypt MEA Jet Fuel Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 62: Egypt MEA Jet Fuel Industry Volume Share (%), by Geography 2025 & 2033

- Figure 63: Egypt MEA Jet Fuel Industry Revenue (billion), by Country 2025 & 2033

- Figure 64: Egypt MEA Jet Fuel Industry Volume (Litre), by Country 2025 & 2033

- Figure 65: Egypt MEA Jet Fuel Industry Revenue Share (%), by Country 2025 & 2033

- Figure 66: Egypt MEA Jet Fuel Industry Volume Share (%), by Country 2025 & 2033

- Figure 67: South Africa MEA Jet Fuel Industry Revenue (billion), by Fuel Type 2025 & 2033

- Figure 68: South Africa MEA Jet Fuel Industry Volume (Litre), by Fuel Type 2025 & 2033

- Figure 69: South Africa MEA Jet Fuel Industry Revenue Share (%), by Fuel Type 2025 & 2033

- Figure 70: South Africa MEA Jet Fuel Industry Volume Share (%), by Fuel Type 2025 & 2033

- Figure 71: South Africa MEA Jet Fuel Industry Revenue (billion), by Application 2025 & 2033

- Figure 72: South Africa MEA Jet Fuel Industry Volume (Litre), by Application 2025 & 2033

- Figure 73: South Africa MEA Jet Fuel Industry Revenue Share (%), by Application 2025 & 2033

- Figure 74: South Africa MEA Jet Fuel Industry Volume Share (%), by Application 2025 & 2033

- Figure 75: South Africa MEA Jet Fuel Industry Revenue (billion), by Geography 2025 & 2033

- Figure 76: South Africa MEA Jet Fuel Industry Volume (Litre), by Geography 2025 & 2033

- Figure 77: South Africa MEA Jet Fuel Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 78: South Africa MEA Jet Fuel Industry Volume Share (%), by Geography 2025 & 2033

- Figure 79: South Africa MEA Jet Fuel Industry Revenue (billion), by Country 2025 & 2033

- Figure 80: South Africa MEA Jet Fuel Industry Volume (Litre), by Country 2025 & 2033

- Figure 81: South Africa MEA Jet Fuel Industry Revenue Share (%), by Country 2025 & 2033

- Figure 82: South Africa MEA Jet Fuel Industry Volume Share (%), by Country 2025 & 2033

- Figure 83: Rest of Middle East and Africa MEA Jet Fuel Industry Revenue (billion), by Fuel Type 2025 & 2033

- Figure 84: Rest of Middle East and Africa MEA Jet Fuel Industry Volume (Litre), by Fuel Type 2025 & 2033

- Figure 85: Rest of Middle East and Africa MEA Jet Fuel Industry Revenue Share (%), by Fuel Type 2025 & 2033

- Figure 86: Rest of Middle East and Africa MEA Jet Fuel Industry Volume Share (%), by Fuel Type 2025 & 2033

- Figure 87: Rest of Middle East and Africa MEA Jet Fuel Industry Revenue (billion), by Application 2025 & 2033

- Figure 88: Rest of Middle East and Africa MEA Jet Fuel Industry Volume (Litre), by Application 2025 & 2033

- Figure 89: Rest of Middle East and Africa MEA Jet Fuel Industry Revenue Share (%), by Application 2025 & 2033

- Figure 90: Rest of Middle East and Africa MEA Jet Fuel Industry Volume Share (%), by Application 2025 & 2033

- Figure 91: Rest of Middle East and Africa MEA Jet Fuel Industry Revenue (billion), by Geography 2025 & 2033

- Figure 92: Rest of Middle East and Africa MEA Jet Fuel Industry Volume (Litre), by Geography 2025 & 2033

- Figure 93: Rest of Middle East and Africa MEA Jet Fuel Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 94: Rest of Middle East and Africa MEA Jet Fuel Industry Volume Share (%), by Geography 2025 & 2033

- Figure 95: Rest of Middle East and Africa MEA Jet Fuel Industry Revenue (billion), by Country 2025 & 2033

- Figure 96: Rest of Middle East and Africa MEA Jet Fuel Industry Volume (Litre), by Country 2025 & 2033

- Figure 97: Rest of Middle East and Africa MEA Jet Fuel Industry Revenue Share (%), by Country 2025 & 2033

- Figure 98: Rest of Middle East and Africa MEA Jet Fuel Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global MEA Jet Fuel Industry Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 2: Global MEA Jet Fuel Industry Volume Litre Forecast, by Fuel Type 2020 & 2033

- Table 3: Global MEA Jet Fuel Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 4: Global MEA Jet Fuel Industry Volume Litre Forecast, by Application 2020 & 2033

- Table 5: Global MEA Jet Fuel Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 6: Global MEA Jet Fuel Industry Volume Litre Forecast, by Geography 2020 & 2033

- Table 7: Global MEA Jet Fuel Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 8: Global MEA Jet Fuel Industry Volume Litre Forecast, by Region 2020 & 2033

- Table 9: Global MEA Jet Fuel Industry Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 10: Global MEA Jet Fuel Industry Volume Litre Forecast, by Fuel Type 2020 & 2033

- Table 11: Global MEA Jet Fuel Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 12: Global MEA Jet Fuel Industry Volume Litre Forecast, by Application 2020 & 2033

- Table 13: Global MEA Jet Fuel Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 14: Global MEA Jet Fuel Industry Volume Litre Forecast, by Geography 2020 & 2033

- Table 15: Global MEA Jet Fuel Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global MEA Jet Fuel Industry Volume Litre Forecast, by Country 2020 & 2033

- Table 17: Global MEA Jet Fuel Industry Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 18: Global MEA Jet Fuel Industry Volume Litre Forecast, by Fuel Type 2020 & 2033

- Table 19: Global MEA Jet Fuel Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global MEA Jet Fuel Industry Volume Litre Forecast, by Application 2020 & 2033

- Table 21: Global MEA Jet Fuel Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 22: Global MEA Jet Fuel Industry Volume Litre Forecast, by Geography 2020 & 2033

- Table 23: Global MEA Jet Fuel Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global MEA Jet Fuel Industry Volume Litre Forecast, by Country 2020 & 2033

- Table 25: Global MEA Jet Fuel Industry Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 26: Global MEA Jet Fuel Industry Volume Litre Forecast, by Fuel Type 2020 & 2033

- Table 27: Global MEA Jet Fuel Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 28: Global MEA Jet Fuel Industry Volume Litre Forecast, by Application 2020 & 2033

- Table 29: Global MEA Jet Fuel Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 30: Global MEA Jet Fuel Industry Volume Litre Forecast, by Geography 2020 & 2033

- Table 31: Global MEA Jet Fuel Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 32: Global MEA Jet Fuel Industry Volume Litre Forecast, by Country 2020 & 2033

- Table 33: Global MEA Jet Fuel Industry Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 34: Global MEA Jet Fuel Industry Volume Litre Forecast, by Fuel Type 2020 & 2033

- Table 35: Global MEA Jet Fuel Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 36: Global MEA Jet Fuel Industry Volume Litre Forecast, by Application 2020 & 2033

- Table 37: Global MEA Jet Fuel Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 38: Global MEA Jet Fuel Industry Volume Litre Forecast, by Geography 2020 & 2033

- Table 39: Global MEA Jet Fuel Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 40: Global MEA Jet Fuel Industry Volume Litre Forecast, by Country 2020 & 2033

- Table 41: Global MEA Jet Fuel Industry Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 42: Global MEA Jet Fuel Industry Volume Litre Forecast, by Fuel Type 2020 & 2033

- Table 43: Global MEA Jet Fuel Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 44: Global MEA Jet Fuel Industry Volume Litre Forecast, by Application 2020 & 2033

- Table 45: Global MEA Jet Fuel Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 46: Global MEA Jet Fuel Industry Volume Litre Forecast, by Geography 2020 & 2033

- Table 47: Global MEA Jet Fuel Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 48: Global MEA Jet Fuel Industry Volume Litre Forecast, by Country 2020 & 2033

- Table 49: Global MEA Jet Fuel Industry Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 50: Global MEA Jet Fuel Industry Volume Litre Forecast, by Fuel Type 2020 & 2033

- Table 51: Global MEA Jet Fuel Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 52: Global MEA Jet Fuel Industry Volume Litre Forecast, by Application 2020 & 2033

- Table 53: Global MEA Jet Fuel Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 54: Global MEA Jet Fuel Industry Volume Litre Forecast, by Geography 2020 & 2033

- Table 55: Global MEA Jet Fuel Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 56: Global MEA Jet Fuel Industry Volume Litre Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the MEA Jet Fuel Industry?

The projected CAGR is approximately 12.8%.

2. Which companies are prominent players in the MEA Jet Fuel Industry?

Key companies in the market include Shell PLC, Abu Dhabi National Oil Company*List Not Exhaustive, Exxon Mobil Corporation, Emirates National Oil Company, Chevron Corporation, TotalENergies SE, BP PLC, Repsol SA.

3. What are the main segments of the MEA Jet Fuel Industry?

The market segments include Fuel Type, Application, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 431.7 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Renewables Capacity in Thailand4.; Rising Modernization of Existing Transmission and Distribution Infrastructure.

6. What are the notable trends driving market growth?

Commercial Sector to Dominate the Market.

7. Are there any restraints impacting market growth?

Huge Capital Expenditure Required for Carrying out Modernization of Existing Facilities.

8. Can you provide examples of recent developments in the market?

January 2022: Masdar, Siemens Energy, and TotalEnergies signed a partnership agreement focused on green hydrogen to produce sustainable aviation fuel (SAF).

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in Litre.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "MEA Jet Fuel Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the MEA Jet Fuel Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the MEA Jet Fuel Industry?

To stay informed about further developments, trends, and reports in the MEA Jet Fuel Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence