Key Insights

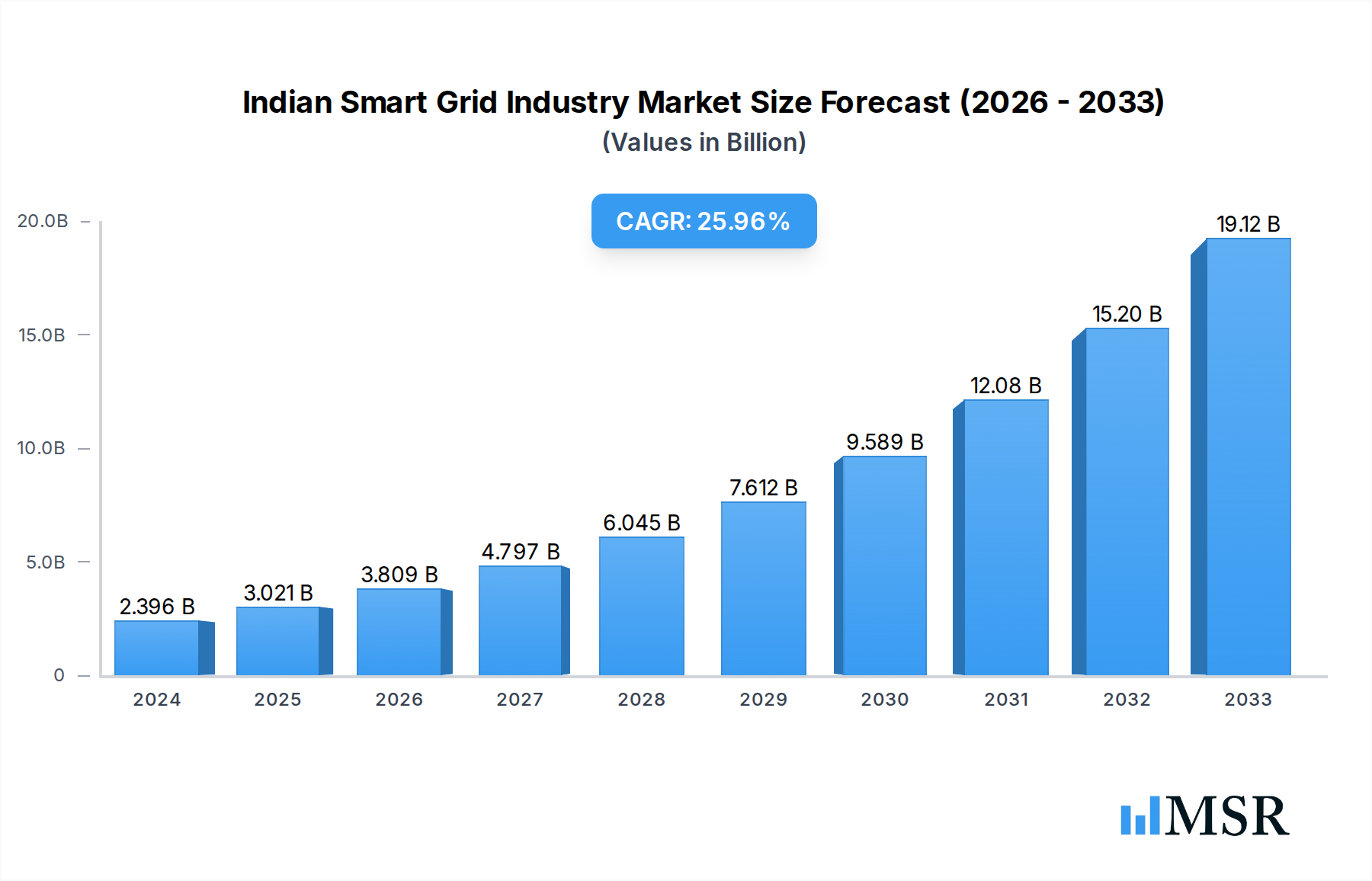

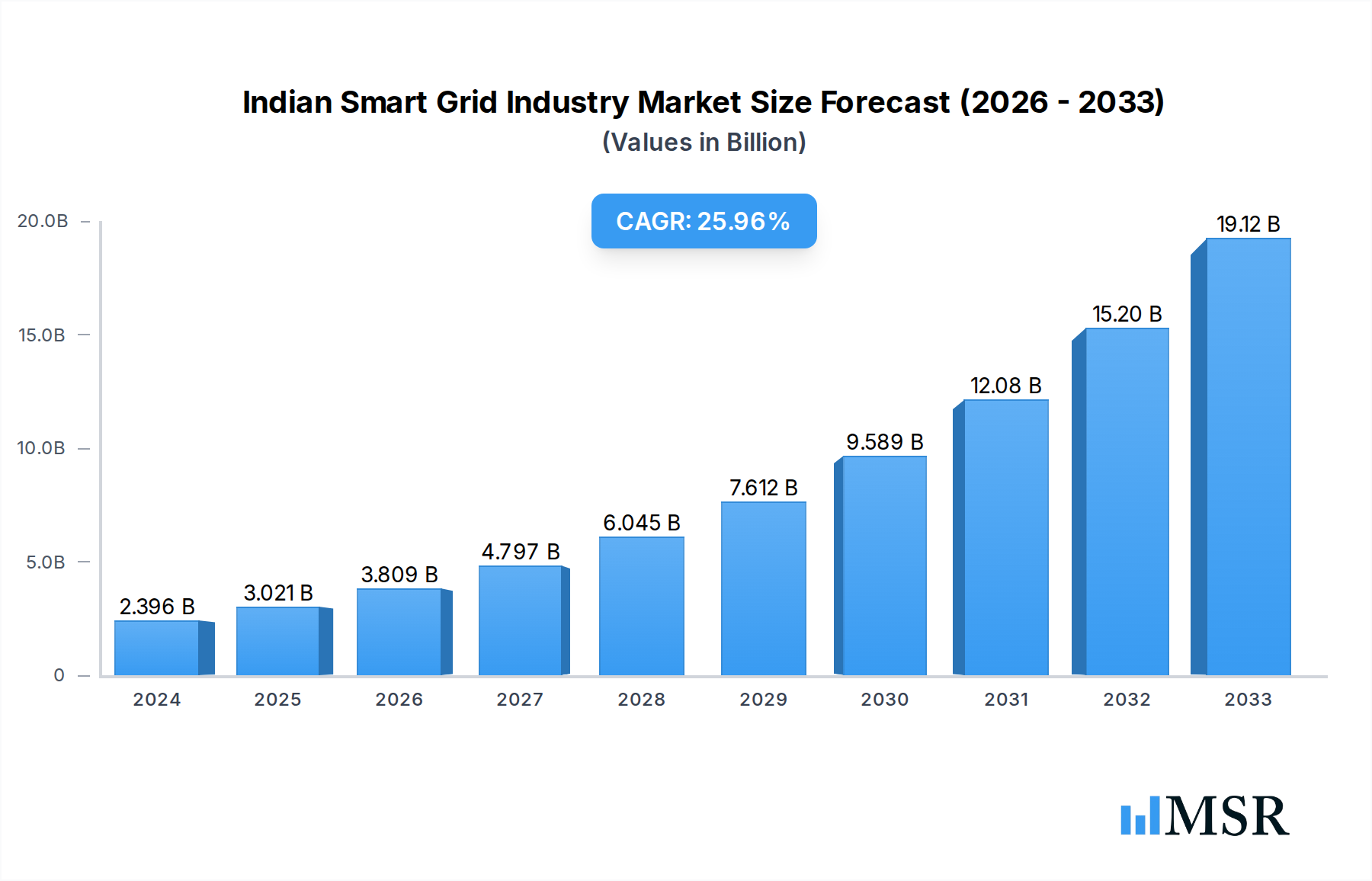

The Indian Smart Grid industry is poised for exceptional growth, projected to reach a substantial market size. With a significant market size of $2395.9 million in 2024 and a robust CAGR of 26.11%, the sector is attracting considerable investment and innovation. This remarkable expansion is fueled by a confluence of factors, including the government's strong emphasis on modernizing the power infrastructure, the escalating demand for reliable and efficient electricity supply, and the increasing adoption of digital technologies across the power value chain. Key drivers include the imperative to reduce transmission and distribution losses, enhance grid stability, and integrate renewable energy sources seamlessly. The ongoing digital transformation in India is also a major catalyst, encouraging utilities and energy companies to invest in smart grid solutions to improve operational efficiency, customer engagement, and overall grid resilience.

Indian Smart Grid Industry Market Size (In Billion)

The market is segmented across critical areas such as Transmission, Advanced Metering Infrastructure (AMI), Communication Technology, and Other Technology Application Areas. The widespread deployment of AMI is a significant growth engine, enabling real-time monitoring and management of energy consumption, leading to better demand-side management and reduced pilferage. Advancements in communication technologies, including IoT and 5G, are further bolstering the capabilities of smart grids, facilitating seamless data exchange and control. Leading global and domestic players like Honeywell International Inc., ABB Ltd, Siemens AG, and Power Grid Corporation of India Limited are actively involved in shaping the Indian smart grid landscape through strategic partnerships and technological advancements. The focus on smart grid development in India, particularly in regions like India itself, signifies a commitment to building a sustainable and technologically advanced energy future for the nation.

Indian Smart Grid Industry Company Market Share

Explore the dynamic Indian Smart Grid Industry, a critical sector poised for significant expansion driven by government initiatives, technological advancements, and the urgent need for modern, efficient, and reliable power infrastructure. This comprehensive report provides in-depth analysis, actionable insights, and strategic recommendations for stakeholders, investors, and industry leaders navigating this evolving market.

Indian Smart Grid Industry Market Concentration & Dynamics

The Indian Smart Grid Industry is characterized by a moderate to high market concentration, with a few major global and domestic players dominating key segments. Innovation ecosystems are flourishing, spurred by significant investments in research and development, particularly in areas like AI-powered grid management and advanced cybersecurity solutions for smart grids. Regulatory frameworks, such as the National Smart Grid Mission, are actively shaping the market by providing policy support and incentivizing adoption. Substitute products, primarily traditional grid technologies, are rapidly being displaced by more advanced and cost-effective smart grid solutions. End-user trends indicate a growing demand for enhanced energy efficiency, real-time monitoring, and seamless integration of renewable energy sources. Merger and acquisition (M&A) activities are on the rise as companies seek to consolidate their market position, acquire new technologies, and expand their service offerings. The estimated M&A deal count is projected to reach xx in the forecast period, indicating a consolidation trend. Market share is fragmented across segments, with Advanced Metering Infrastructure (AMI) holding a significant portion, followed by Transmission solutions.

Indian Smart Grid Industry Industry Insights & Trends

The Indian Smart Grid Industry is experiencing robust growth, projected to reach a market size of over xx billion USD by 2033, with a Compound Annual Growth Rate (CAGR) of xx% during the forecast period of 2025–2033. Key market growth drivers include the escalating demand for electricity, the need to reduce transmission and distribution (T&D) losses, and the government's ambitious vision for a digitalized power infrastructure. Technological disruptions are at the forefront, with the widespread adoption of IoT, Big Data analytics, AI, and machine learning transforming grid operations. These technologies enable predictive maintenance, optimized energy distribution, and enhanced grid resilience. Evolving consumer behaviors are also playing a crucial role, with an increasing demand for smart home integration, real-time energy consumption data, and the ability to participate in demand-response programs. The integration of renewable energy sources, such as solar and wind power, into the grid necessitates advanced smart grid solutions for seamless management and stability. The forecast period anticipates significant investments in upgrading existing grid infrastructure and deploying new smart technologies across the nation. The estimated market size for the base year 2025 is xx billion USD.

Key Markets & Segments Leading Indian Smart Grid Industry

The Indian Smart Grid Industry is witnessing significant growth across multiple segments, with Advanced Metering Infrastructure (AMI) and Transmission technologies emerging as dominant forces. The economic growth of India, coupled with massive infrastructure development projects, fuels the demand for robust and intelligent grid systems.

Transmission: This segment is crucial for modernizing India's aging power grid. Drivers include the need to reduce T&D losses, improve grid stability, and integrate power generated from remote renewable energy sources. Investments in high-voltage direct current (HVDC) technology and advanced grid monitoring systems are key. The dominance of this segment is further propelled by large-scale government initiatives aimed at upgrading the national power grid.

Advanced Metering Infrastructure (AMI): AMI is experiencing explosive growth, driven by government mandates for smart meter deployment and the benefits of real-time data for utilities and consumers.

- Drivers: Reduced billing errors, improved revenue collection, proactive identification of outages, and the enablement of smart pricing and demand-response programs.

- Dominance Analysis: The sheer scale of smart meter rollout, as evidenced by recent tenders for millions of prepaid smart meters, highlights the leadership of this segment. Companies are investing heavily in deploying smart meters with advanced communication capabilities like 4G and 5G, and pre-paid payment options are becoming a standard feature.

Communication Technology: This segment underpins the entire smart grid ecosystem.

- Drivers: The need for secure, reliable, and high-bandwidth communication networks to connect smart meters, sensors, and control systems. Technologies like fiber optics, 5G, and LoRaWAN are gaining prominence.

- Dominance Analysis: The success of other smart grid segments is directly dependent on the advancement and deployment of sophisticated communication technologies. Ensuring seamless data flow and real-time control is paramount.

Other Technology Application Areas: This broad category encompasses various innovative applications that enhance grid efficiency and reliability.

- Drivers: Integration of distributed energy resources (DERs), grid automation, renewable energy forecasting, energy storage solutions, and cybersecurity for critical infrastructure.

- Dominance Analysis: As the smart grid matures, these application areas will become increasingly critical for optimizing grid performance and meeting future energy demands.

Indian Smart Grid Industry Product Developments

Product developments in the Indian Smart Grid Industry are characterized by a strong focus on enhancing grid efficiency, reliability, and security. Innovations include AI-powered grid management software that enables predictive analytics for fault detection and load forecasting, advanced smart meters with integrated IoT capabilities for real-time data transmission, and robust communication modules supporting 5G and LoRaWAN for seamless connectivity. Furthermore, companies are developing sophisticated cybersecurity solutions to protect critical grid infrastructure from cyber threats, and advanced substation automation systems that improve operational efficiency and safety. The market relevance of these products is high, driven by the urgent need for a modernized power infrastructure that can efficiently integrate renewable energy and meet the growing energy demands of the nation.

Challenges in the Indian Smart Grid Industry Market

The Indian Smart Grid Industry faces several challenges that can impede its growth and adoption. Regulatory hurdles, including the need for standardized policies and clear tariff structures, can slow down deployment. Supply chain issues, particularly for critical components and advanced microprocessors, can lead to project delays and cost overruns. Competitive pressures from established players and the entry of new technology providers also present a challenge. Furthermore, the initial high capital investment required for smart grid infrastructure can be a deterrent for some utilities. The estimated impact of these challenges on market growth is projected to be around xx% in the short to medium term.

Forces Driving Indian Smart Grid Industry Growth

Several key forces are propelling the growth of the Indian Smart Grid Industry. Technological advancements, such as the increasing affordability and capabilities of IoT devices, AI, and Big Data analytics, are making smart grid solutions more accessible and effective. Economic factors, including the rapidly growing energy demand and the government's focus on industrial and infrastructural development, create a strong market need. Regulatory drivers, such as supportive government policies, incentives for smart meter deployment, and the push for energy efficiency, are also playing a pivotal role. The increasing integration of renewable energy sources necessitates smarter grid management to ensure stability and reliability.

Forces Driving Indian Smart Grid Industry Growth (Long-Term Catalysts)

Long-term growth catalysts for the Indian Smart Grid Industry lie in continuous innovation and strategic market expansion. The ongoing evolution of technologies like blockchain for secure energy trading and distributed ledger technology for grid management will unlock new efficiencies. Strategic partnerships between technology providers, utilities, and government bodies will accelerate the pace of deployment and foster collaborative problem-solving. Market expansions into rural electrification projects and the development of microgrids will broaden the reach of smart grid benefits. Furthermore, the increasing awareness and demand for sustainable energy solutions will continue to drive investments in smart grid infrastructure that supports decarbonization efforts.

Emerging Opportunities in Indian Smart Grid Industry

Emerging opportunities in the Indian Smart Grid Industry are vast and transformative. The rise of the electric vehicle (EV) ecosystem presents a significant opportunity for smart charging infrastructure integrated with the grid. The development of robust energy storage solutions, coupled with smart grid capabilities, will enable better management of intermittent renewable energy sources and enhance grid resilience during peak demand. New markets are opening up in smart city initiatives, where integrated smart grid solutions will be fundamental to urban development. Furthermore, the growing consumer preference for energy independence and personalized energy management solutions will drive demand for advanced smart home integrations and peer-to-peer energy trading platforms facilitated by smart grids.

Leading Players in the Indian Smart Grid Industry Sector

- Honeywell International Inc

- ABB Ltd

- Accenture PLC

- Capgemini SE

- HCL Technologies Ltd

- Siemens AG

- Cisco Systems Inc

- Schneider Electric SE

- General Electric Company

- Power Grid Corporation of India Limited

Key Milestones in Indian Smart Grid Industry Industry

- February 2023: The Brihanmumbai Electric Supply and Transport (BEST) announced its plan to install smart meters for its 10.5 lakh power consumers starting March 2023. These meters will feature 4G and 5G SIM cards and offer pre-paid payment options, marking a significant step towards consumer-centric smart metering.

- October 2022: Major Indian conglomerates like Adani Group, GMR Group, L&T, and IntelliSmart submitted bids for tenders from four Uttar Pradesh power distribution companies (discoms) to install approximately 2.85 crore prepaid smart meters, highlighting massive government push for smart metering adoption.

Strategic Outlook for Indian Smart Grid Industry Market

The strategic outlook for the Indian Smart Grid Industry is highly promising, driven by a confluence of factors including supportive government policies, rapid technological advancements, and escalating energy demands. Future market potential lies in the widespread adoption of AI-driven grid management, the integration of advanced energy storage solutions, and the expansion of smart metering across all consumer segments. Strategic opportunities include fostering public-private partnerships to accelerate infrastructure development, investing in cybersecurity to ensure grid resilience, and leveraging data analytics for optimized energy distribution and enhanced consumer services. The industry is poised for sustained growth, contributing significantly to India's energy security and sustainable development goals.

Indian Smart Grid Industry Segmentation

- 1. Transmission

- 2. Advanced Metering Infrastructure (AMI)

- 3. Communication Technology

- 4. Other Technology Application Areas

Indian Smart Grid Industry Segmentation By Geography

- 1. India

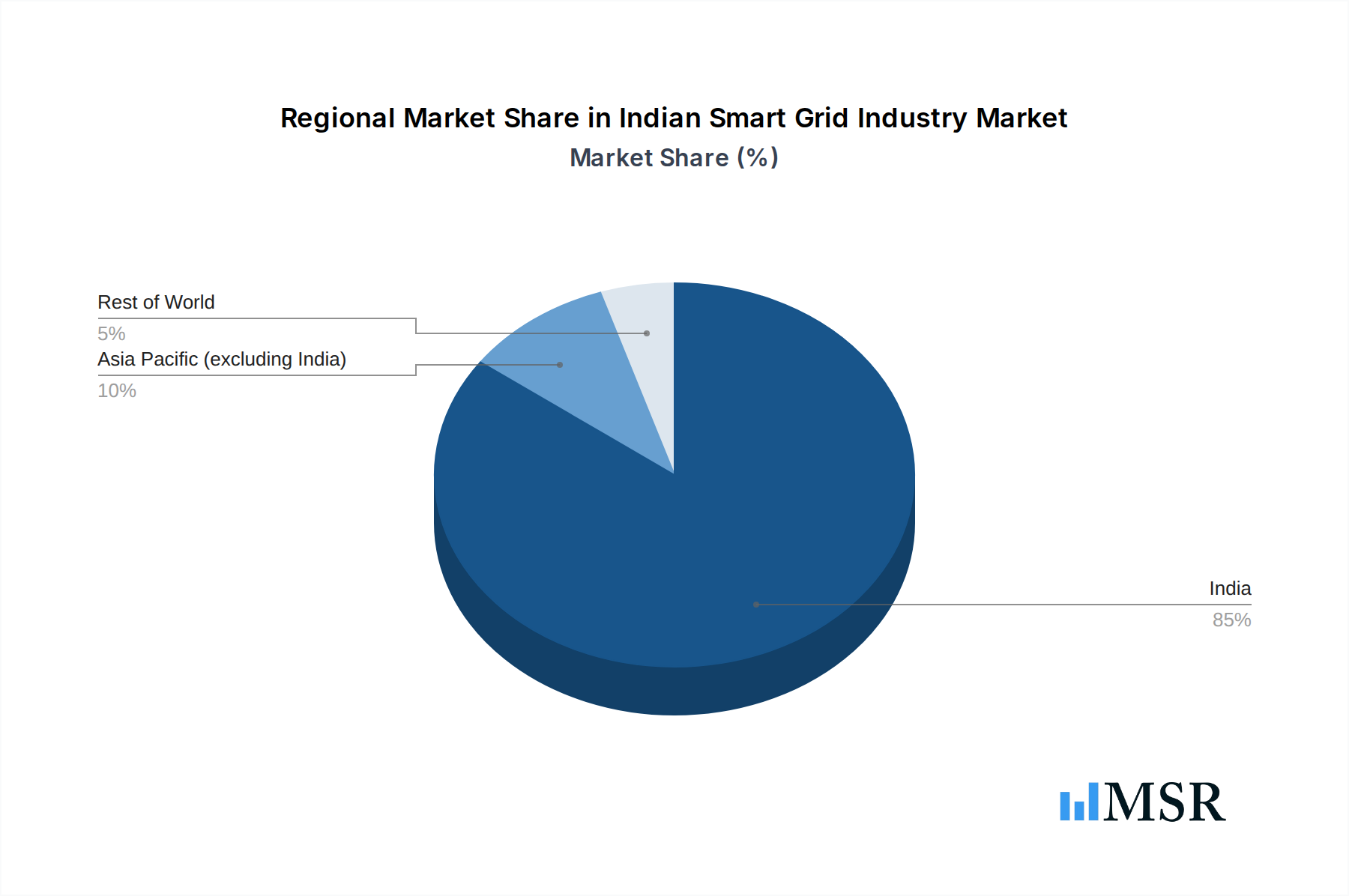

Indian Smart Grid Industry Regional Market Share

Geographic Coverage of Indian Smart Grid Industry

Indian Smart Grid Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 26.11% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Transmission

- 5.2. Market Analysis, Insights and Forecast - by Advanced Metering Infrastructure (AMI)

- 5.3. Market Analysis, Insights and Forecast - by Communication Technology

- 5.4. Market Analysis, Insights and Forecast - by Other Technology Application Areas

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. India

- 6. Indian Smart Grid Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Transmission

- 6.2. Market Analysis, Insights and Forecast - by Advanced Metering Infrastructure (AMI)

- 6.3. Market Analysis, Insights and Forecast - by Communication Technology

- 6.4. Market Analysis, Insights and Forecast - by Other Technology Application Areas

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Honeywell International Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 ABB Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Accenture PLC

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Capgemini SE

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 HCL Technologies Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Siemens AG*List Not Exhaustive

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Cisco Systems Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Schneider Electric SE

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 General Electric Company

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Power Grid Corporation of India Limited

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Honeywell International Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Indian Smart Grid Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Indian Smart Grid Industry Share (%) by Company 2025

List of Tables

- Table 1: Indian Smart Grid Industry Revenue million Forecast, by Transmission 2020 & 2033

- Table 2: Indian Smart Grid Industry Revenue million Forecast, by Advanced Metering Infrastructure (AMI) 2020 & 2033

- Table 3: Indian Smart Grid Industry Revenue million Forecast, by Communication Technology 2020 & 2033

- Table 4: Indian Smart Grid Industry Revenue million Forecast, by Other Technology Application Areas 2020 & 2033

- Table 5: Indian Smart Grid Industry Revenue million Forecast, by Region 2020 & 2033

- Table 6: Indian Smart Grid Industry Revenue million Forecast, by Transmission 2020 & 2033

- Table 7: Indian Smart Grid Industry Revenue million Forecast, by Advanced Metering Infrastructure (AMI) 2020 & 2033

- Table 8: Indian Smart Grid Industry Revenue million Forecast, by Communication Technology 2020 & 2033

- Table 9: Indian Smart Grid Industry Revenue million Forecast, by Other Technology Application Areas 2020 & 2033

- Table 10: Indian Smart Grid Industry Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Indian Smart Grid Industry?

The projected CAGR is approximately 26.11%.

2. Which companies are prominent players in the Indian Smart Grid Industry?

Key companies in the market include Honeywell International Inc, ABB Ltd, Accenture PLC, Capgemini SE, HCL Technologies Ltd, Siemens AG*List Not Exhaustive, Cisco Systems Inc, Schneider Electric SE, General Electric Company, Power Grid Corporation of India Limited.

3. What are the main segments of the Indian Smart Grid Industry?

The market segments include Transmission, Advanced Metering Infrastructure (AMI), Communication Technology, Other Technology Application Areas.

4. Can you provide details about the market size?

The market size is estimated to be USD 2395.9 million as of 2022.

5. What are some drivers contributing to market growth?

4.; Growing Power Demand from the Commercial and Industrial Sectors.

6. What are the notable trends driving market growth?

Advanced Metering Infrastructure (AMI) is Expected to Witness Significant Growth.

7. Are there any restraints impacting market growth?

4.; Stringent Environmental and Safety Regulations.

8. Can you provide examples of recent developments in the market?

February 2023: The Brihanmumbai Electric Supply and Transport (BEST) announced that the company is likely to start installing smart meters for its 10.5 lakh power consumers from March 2023 onward. These devices will be enabled with 4G and 5G SIM cards and will offer pre-paid payment options for consumers.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Indian Smart Grid Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Indian Smart Grid Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Indian Smart Grid Industry?

To stay informed about further developments, trends, and reports in the Indian Smart Grid Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence