Key Insights

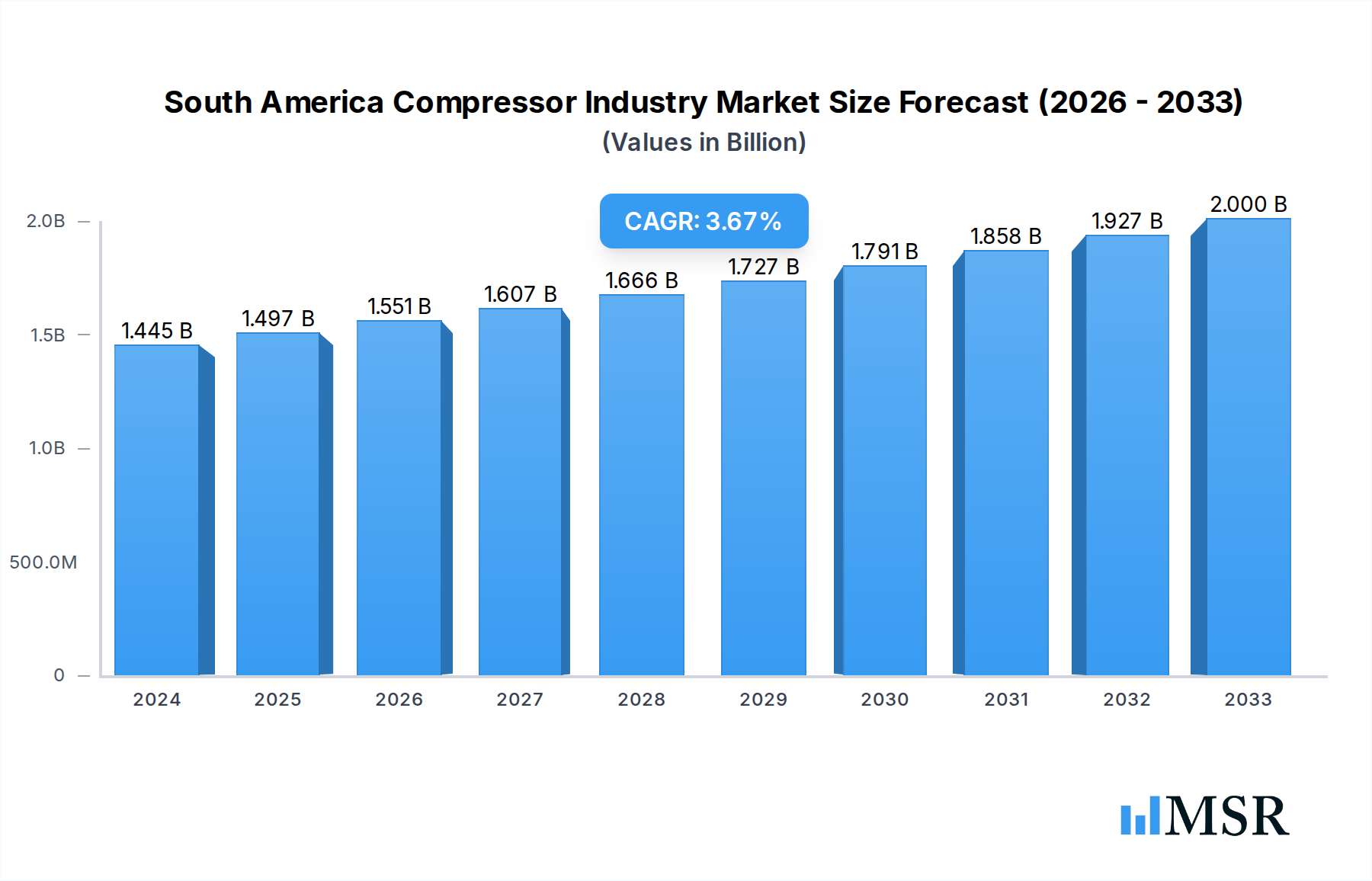

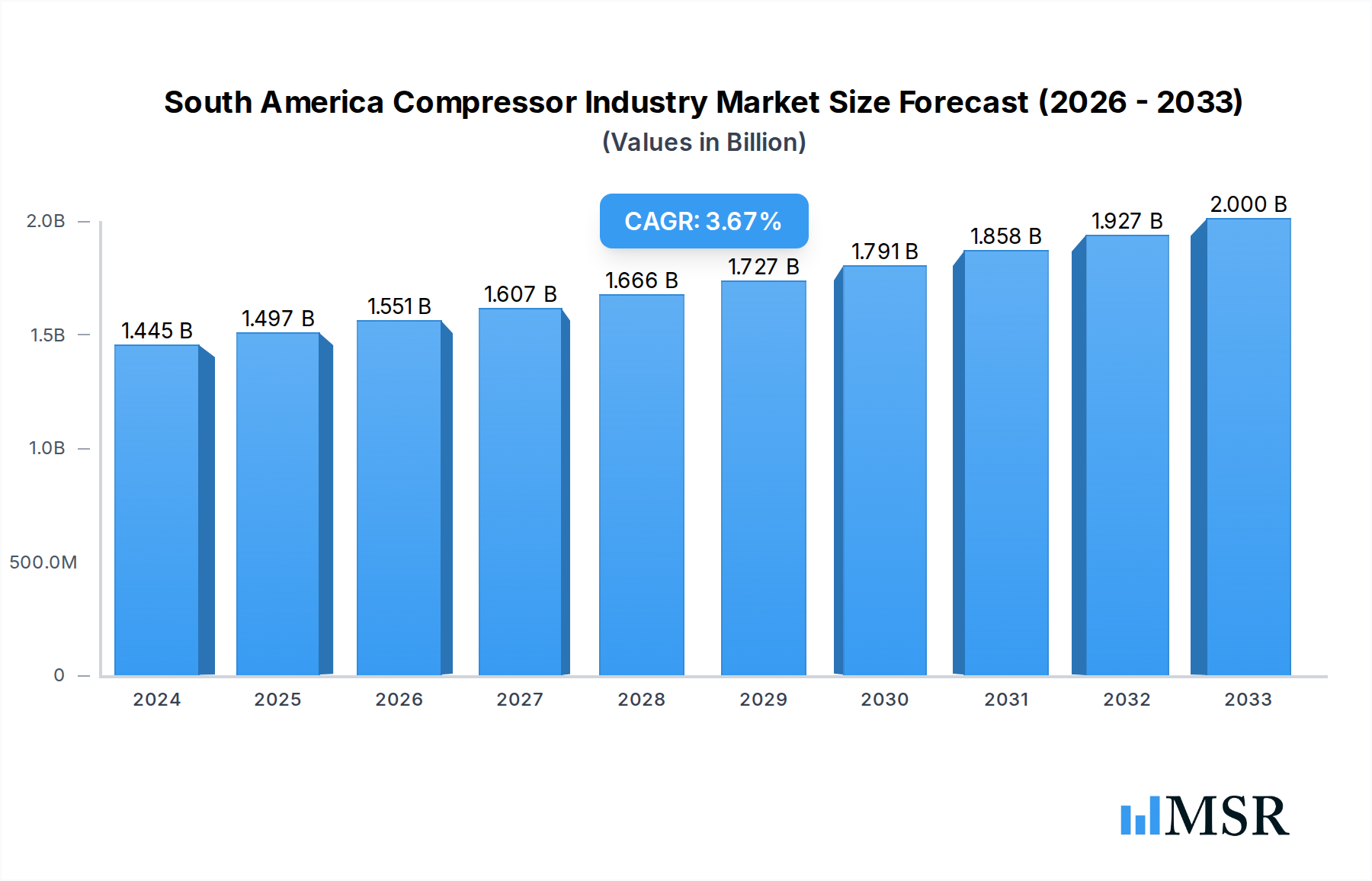

The South America compressor industry is poised for steady growth, with an estimated market size of USD 1445.4 million in 2024 and a projected Compound Annual Growth Rate (CAGR) of 4% from 2025 to 2033. This expansion is primarily fueled by robust demand from key end-user sectors, including the oil and gas industry, the power sector, manufacturing, and the chemicals and petrochemical industry. The oil and gas sector, in particular, continues to be a significant driver due to ongoing exploration and production activities, as well as the need for efficient compression in refining processes. Similarly, the burgeoning power generation initiatives across South America, coupled with increased industrialization and manufacturing output, are contributing to a sustained demand for various types of compressors, including positive displacement and dynamic compressors. Technological advancements, such as the development of energy-efficient and smart compressors, are also playing a crucial role in driving market adoption and meeting stringent environmental regulations.

South America Compressor Industry Market Size (In Billion)

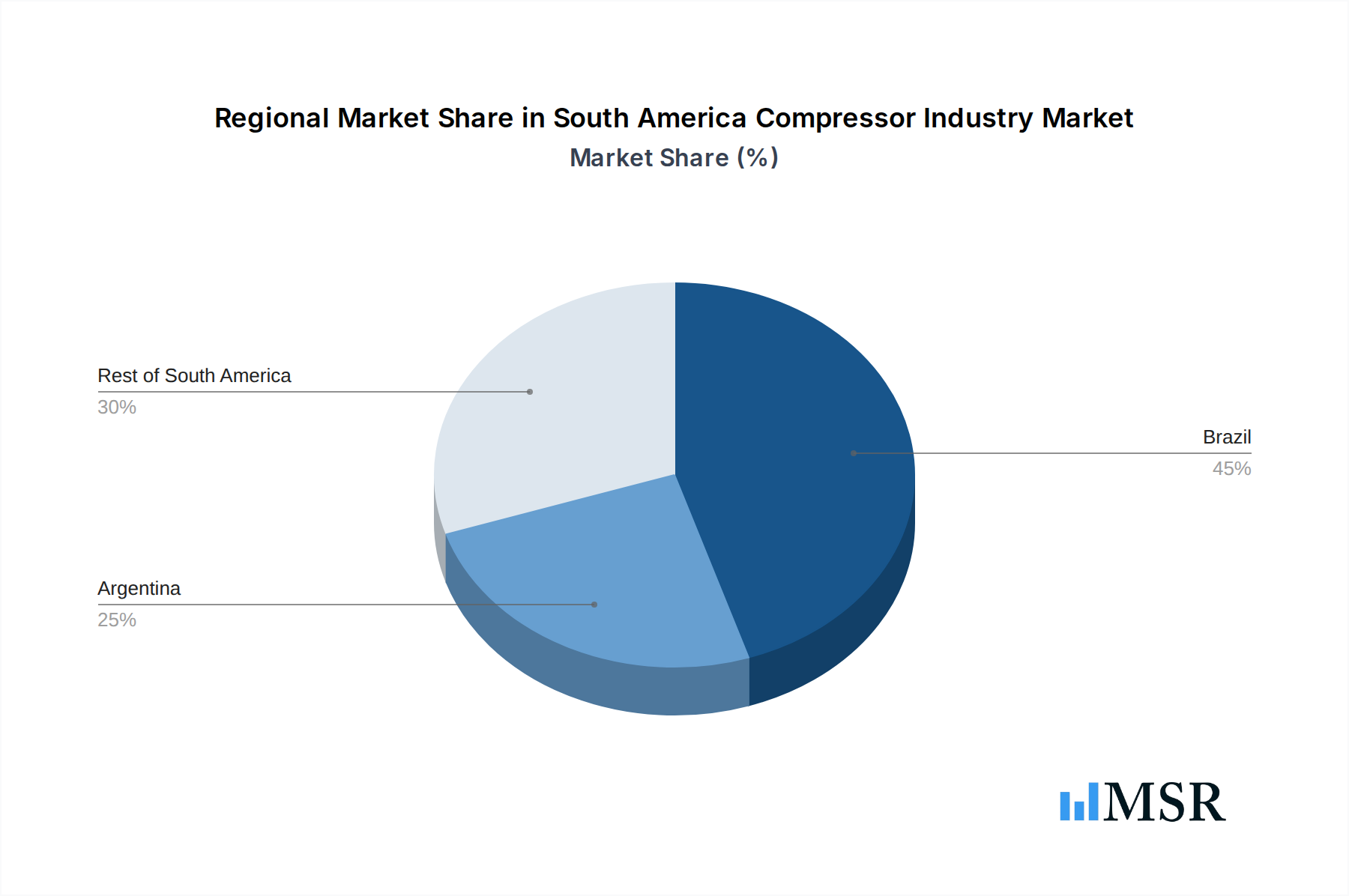

The market is characterized by a dynamic competitive landscape with major global players and regional manufacturers vying for market share. Key companies like Trane Technologies PLC, Ebara Corporation, Atlas Copco AB, and Baker Hughes Co are actively involved in the South American market, offering a wide range of compressor solutions. The geographical segmentation highlights Brazil as a significant contributor to the market's revenue, followed by Argentina and the rest of South America. Investments in infrastructure development, particularly in countries with substantial natural resource reserves, will continue to bolster the demand for compressors. While the market exhibits strong growth potential, factors such as fluctuating raw material prices for compressor manufacturing and the initial high capital investment required for advanced compressor technologies might present some challenges. However, the increasing focus on operational efficiency and emission reduction across industries is expected to outweigh these restraints, ensuring continued positive momentum for the South American compressor market.

South America Compressor Industry Company Market Share

Here is the SEO-optimized report description for the South America Compressor Industry:

Unlock Critical Insights: South America Compressor Industry Market Analysis (2019-2033)

Gain a comprehensive understanding of the burgeoning South America compressor market with this in-depth report, covering the study period of 2019–2033, with a base year of 2025. This detailed analysis delves into the intricate dynamics, key growth drivers, emerging opportunities, and strategic outlook for compressor manufacturers and end-users across the continent. Our report provides actionable intelligence for stakeholders looking to capitalize on the USD 10 billion+ LNG expansion in Argentina and the USD 140 million+ LNG regasification terminal in Brazil.

With a focus on Positive Displacement compressors and Dynamic compressors, and detailed segmentation by end-users including the Oil and Gas Industry, Power Sector, Manufacturing Sector, and Chemicals and Petrochemical Industry, this report offers unparalleled market visibility. Explore the competitive landscape featuring global leaders like Trane Technologies PLC, Ebara Corporation, Atlas Copco AB, Baker Hughes Co, Siemens AG, and General Electric Company.

South America Compressor Industry Market Concentration & Dynamics

The South America compressor industry exhibits a moderately concentrated market, driven by the significant investments from major global players and a growing number of regional manufacturers. Innovation ecosystems are flourishing, particularly in Brazil and Argentina, fueled by advancements in energy efficiency and digitalization, impacting the demand for both Positive Displacement and Dynamic compressor technologies. Regulatory frameworks are evolving to promote sustainable industrial practices, influencing compressor specifications and operational standards, especially within the Oil and Gas Industry and the Chemicals and Petrochemical Industry. The threat of substitute products, while present in some smaller applications, remains limited in large-scale industrial processes where the reliability and performance of compressors are paramount. End-user trends are heavily influenced by the expanding energy sector, particularly liquefied natural gas (LNG) projects, and the ongoing industrialization across various sectors. Mergers and acquisitions (M&A) activities are anticipated to increase as companies seek to consolidate market share and expand their technological capabilities. The report analyzes key M&A deal counts and their impact on market share within the historical period (2019-2024) and the forecast period (2025-2033).

South America Compressor Industry Industry Insights & Trends

The South America compressor industry is poised for significant expansion, projected to achieve a market size exceeding USD 5,000 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of approximately 6.5% during the forecast period (2025-2033). This growth is primarily propelled by escalating demand from the Oil and Gas Industry, driven by substantial investments in exploration, production, and downstream processing, particularly in regions like Brazil and Argentina. The burgeoning Power Sector also contributes significantly, with increasing energy demands necessitating efficient power generation infrastructure that relies heavily on industrial compressors. Furthermore, the expanding Manufacturing Sector, encompassing automotive, food and beverage, and general manufacturing, is adopting advanced compressor technologies for process optimization and automation. The Chemicals and Petrochemical Industry remains a cornerstone of demand, with continuous growth in production facilities and the expansion of petrochemical complexes across the continent.

Technological disruptions are playing a pivotal role, with a clear shift towards energy-efficient and smart compressors. The integration of IoT (Internet of Things) and AI-powered predictive maintenance solutions is becoming a standard expectation, reducing operational downtime and enhancing overall efficiency. Manufacturers are investing heavily in research and development to offer variable speed drives (VSDs) and advanced control systems that optimize energy consumption, aligning with sustainability goals. Evolving consumer behaviors, from an industrial perspective, are characterized by a demand for reliable, cost-effective, and environmentally friendly compressor solutions. This includes a preference for compact designs, lower noise levels, and extended service life. The ongoing infrastructure development and urbanization across South America also contribute to the demand for compressors in various construction and industrial applications. The report provides detailed analysis of market size evolution and CAGR projections for each segment and geography.

Key Markets & Segments Leading South America Compressor Industry

Brazil stands as the dominant market within the South America compressor industry, driven by its robust industrial base and significant investments in the Oil and Gas Industry and the Power Sector. The country's vast energy reserves and ongoing development of offshore oil fields, coupled with a growing demand for electricity, create a perpetual need for high-capacity compressors.

- Dominant Region/Country: Brazil is the primary market, followed by Argentina, with the Rest of South America showing steady growth.

- Leading Segments by Type:

- Dynamic Compressors: Essential for large-scale operations in oil and gas processing, power generation, and petrochemical plants, experiencing strong demand due to the scale of projects in Brazil and Argentina.

- Positive Displacement Compressors: Vital for various industrial applications, including manufacturing, chemicals, and smaller-scale oil and gas operations, demonstrating consistent growth driven by industrial diversification.

- Leading Segments by End User:

- Oil and Gas Industry: The largest segment, fueled by exploration, production, and LNG initiatives in Brazil and Argentina, with projects like the YPF and Petronas LNG plant significantly boosting demand.

- Power Sector: Driven by the need for efficient power generation, including thermal power plants and renewable energy integration, requiring reliable compressor solutions.

- Manufacturing Sector: Benefiting from economic growth and increased industrial activity, leading to demand for compressors in automotive, food and beverage, and general manufacturing.

- Chemicals and Petrochemical Industry: A consistent and substantial driver of compressor demand, with ongoing expansions and new plant constructions across the region.

The dominance of Brazil is further reinforced by government initiatives promoting industrial growth and infrastructure development. Argentina's burgeoning LNG projects, such as the USD 10 billion YPF and Petronas deal, are rapidly increasing its significance in the compressor market, particularly for Dynamic Compressors. The "Rest of South America," encompassing countries like Colombia, Peru, and Chile, contributes a steady demand from mining, manufacturing, and its respective oil and gas sectors, showcasing diversified growth patterns. The integration of advanced compressor technologies and energy-efficient solutions is a key trend across all leading segments, responding to both economic pressures and environmental regulations.

South America Compressor Industry Product Developments

The South America compressor industry is witnessing a surge in product innovations focused on enhanced energy efficiency, reduced emissions, and smart functionalities. Manufacturers are introducing advanced Positive Displacement and Dynamic compressor models equipped with variable speed drives (VSDs) and integrated intelligent control systems. These advancements not only optimize energy consumption but also provide predictive maintenance capabilities, minimizing downtime and operational costs. The development of modular and compact compressor units is also a notable trend, catering to the space constraints in various industrial and urban settings. Emphasis is placed on materials science to improve durability and resistance to harsh operating environments prevalent in sectors like oil and gas.

Challenges in the South America Compressor Industry Market

The South America compressor industry faces several hurdles, including:

- Economic Volatility: Fluctuations in regional economies and currency depreciation can impact investment decisions for capital-intensive compressor purchases.

- Regulatory Complexity: Navigating diverse and evolving environmental and safety regulations across different countries can be challenging for manufacturers and end-users.

- Supply Chain Disruptions: Global and local supply chain issues can lead to extended lead times and increased costs for critical components.

- Skilled Workforce Shortage: A lack of trained technicians for installation, maintenance, and repair of advanced compressor systems can hinder efficient operations.

- Infrastructure Gaps: In certain regions, underdeveloped infrastructure can pose challenges for the logistics and deployment of large-scale compressor systems.

Forces Driving South America Compressor Industry Growth

Several key factors are propelling the growth of the South America compressor industry:

- Expanding Oil and Gas Sector: Significant investments in exploration, production, and LNG projects, particularly in Brazil and Argentina, are creating substantial demand.

- Industrialization and Manufacturing Growth: The increasing diversification and expansion of the manufacturing base across various sectors are driving the need for efficient compression solutions.

- Infrastructure Development: Ongoing public and private infrastructure projects, including power plants and industrial facilities, require robust compressor technology.

- Focus on Energy Efficiency: Growing environmental consciousness and the pursuit of operational cost savings are pushing demand for advanced, energy-efficient compressors.

- Technological Advancements: Innovations in compressor design, including smart features and digitalization, are enhancing performance and reliability, encouraging adoption.

Challenges in the South America Compressor Industry Market

Long-term growth catalysts for the South America compressor industry are rooted in sustained economic development and technological innovation. Continued investment in the Oil and Gas Industry, especially in the expansion of LNG capabilities, presents a significant long-term opportunity. The transition towards cleaner energy sources and the increasing demand for renewable energy integration will necessitate advanced compressor technologies for various applications, including hydrogen production and storage. Furthermore, the ongoing push for industrial automation and smart manufacturing across the Manufacturing Sector and Chemicals and Petrochemical Industry will drive demand for sophisticated, data-driven compressor systems. Strategic partnerships between technology providers and industrial end-users will foster the development and adoption of tailored solutions, ensuring sustained market expansion.

Emerging Opportunities in South America Compressor Industry

Emerging opportunities in the South America compressor industry are diverse and promising:

- Green Hydrogen Production: The growing global interest in hydrogen as a clean energy source presents a significant opportunity for compressors used in hydrogen liquefaction, compression, and storage.

- Carbon Capture, Utilization, and Storage (CCUS): As environmental regulations tighten, CCUS technologies will require specialized compressors, offering a new avenue for growth.

- Digitalization and IIoT Integration: The demand for smart compressors with advanced analytics, remote monitoring, and predictive maintenance capabilities is escalating, offering value-added services.

- Renewable Energy Infrastructure: Compressors are essential for various aspects of renewable energy infrastructure, including compressed air energy storage (CAES) systems.

- Expansion in Emerging Economies: Growth in countries within the "Rest of South America" beyond the major players, driven by nascent industrialization and resource development, offers untapped market potential.

Leading Players in the South America Compressor Industry Sector

- Trane Technologies PLC

- Ebara Corporation

- ELGI Equipments Ltd

- Atlas Copco AB

- Baker Hughes Co

- Aerzener Maschinenfabrik GmbH

- Siemens AG

- Schulz S A

- General Electric Company

Key Milestones in South America Compressor Industry Industry

- September 2022: YPF and Petronas signed a deal to build a liquefied natural gas (LNG) plant and a pipeline to transport the fuel in Argentina. The project's initial investment is estimated at around USD 10 billion. It is expected to have a capacity of a power output of 5 million tonnes of LNG during the first year of operation, significantly boosting demand for large-scale industrial compressors.

- January 2023: Compass Gás e Energia announced that the company plans to start operations at its liquefied natural gas (LNG) regasification terminal in São Paulo state in late June 2023. The regasification terminal was built at the cost of USD 140 million and will have the capacity to regasify 14Mm3/d, signaling substantial investment in Brazil's energy infrastructure and increasing the need for gas handling compressors.

Strategic Outlook for South America Compressor Industry Market

The strategic outlook for the South America compressor industry is overwhelmingly positive, characterized by sustained growth fueled by strategic investments and technological advancements. The ongoing energy transition and the continental focus on expanding LNG production and infrastructure in countries like Brazil and Argentina will remain primary growth accelerators, driving demand for high-performance Dynamic compressors. Furthermore, the increasing adoption of Industry 4.0 principles will push the market towards smart, connected, and energy-efficient Positive Displacement and Dynamic compressor solutions, offering predictive maintenance and optimized operational efficiency. Companies that can offer integrated solutions, including advanced services and digital capabilities, are best positioned to capture market share. Exploring opportunities in emerging sectors like green hydrogen and CCUS will be crucial for long-term sustainability and market leadership.

South America Compressor Industry Segmentation

-

1. Type

- 1.1. Positive Diplacement

- 1.2. Dynamic

-

2. End User

- 2.1. Oil and Gas Industry

- 2.2. Power Sector

- 2.3. Manufacturing Sector

- 2.4. Chemicals and Petrochemical Industry

- 2.5. Other End Users

-

3. Geography

- 3.1. Brazil

- 3.2. Argentina

- 3.3. Rest of South America

South America Compressor Industry Segmentation By Geography

- 1. Brazil

- 2. Argentina

- 3. Rest of South America

South America Compressor Industry Regional Market Share

Geographic Coverage of South America Compressor Industry

South America Compressor Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Positive Diplacement

- 5.1.2. Dynamic

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Oil and Gas Industry

- 5.2.2. Power Sector

- 5.2.3. Manufacturing Sector

- 5.2.4. Chemicals and Petrochemical Industry

- 5.2.5. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. Brazil

- 5.3.2. Argentina

- 5.3.3. Rest of South America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Brazil

- 5.4.2. Argentina

- 5.4.3. Rest of South America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. South America Compressor Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Positive Diplacement

- 6.1.2. Dynamic

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Oil and Gas Industry

- 6.2.2. Power Sector

- 6.2.3. Manufacturing Sector

- 6.2.4. Chemicals and Petrochemical Industry

- 6.2.5. Other End Users

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. Brazil

- 6.3.2. Argentina

- 6.3.3. Rest of South America

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Brazil South America Compressor Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Positive Diplacement

- 7.1.2. Dynamic

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Oil and Gas Industry

- 7.2.2. Power Sector

- 7.2.3. Manufacturing Sector

- 7.2.4. Chemicals and Petrochemical Industry

- 7.2.5. Other End Users

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. Brazil

- 7.3.2. Argentina

- 7.3.3. Rest of South America

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Argentina South America Compressor Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Positive Diplacement

- 8.1.2. Dynamic

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Oil and Gas Industry

- 8.2.2. Power Sector

- 8.2.3. Manufacturing Sector

- 8.2.4. Chemicals and Petrochemical Industry

- 8.2.5. Other End Users

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. Brazil

- 8.3.2. Argentina

- 8.3.3. Rest of South America

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Rest of South America South America Compressor Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Positive Diplacement

- 9.1.2. Dynamic

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Oil and Gas Industry

- 9.2.2. Power Sector

- 9.2.3. Manufacturing Sector

- 9.2.4. Chemicals and Petrochemical Industry

- 9.2.5. Other End Users

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. Brazil

- 9.3.2. Argentina

- 9.3.3. Rest of South America

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Trane Technologies PLC

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Ebara Corporation

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 ELGI Equipments Ltd*List Not Exhaustive

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 Atlas Copco AB

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 Baker Hughes Co

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 Aerzener Maschinenfabrik GmbH

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 Siemens AG

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Schulz S A

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 General Electric Company

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.1 Trane Technologies PLC

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: South America Compressor Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: South America Compressor Industry Share (%) by Company 2025

List of Tables

- Table 1: South America Compressor Industry Revenue million Forecast, by Type 2020 & 2033

- Table 2: South America Compressor Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 3: South America Compressor Industry Revenue million Forecast, by End User 2020 & 2033

- Table 4: South America Compressor Industry Volume K Units Forecast, by End User 2020 & 2033

- Table 5: South America Compressor Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 6: South America Compressor Industry Volume K Units Forecast, by Geography 2020 & 2033

- Table 7: South America Compressor Industry Revenue million Forecast, by Region 2020 & 2033

- Table 8: South America Compressor Industry Volume K Units Forecast, by Region 2020 & 2033

- Table 9: South America Compressor Industry Revenue million Forecast, by Type 2020 & 2033

- Table 10: South America Compressor Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 11: South America Compressor Industry Revenue million Forecast, by End User 2020 & 2033

- Table 12: South America Compressor Industry Volume K Units Forecast, by End User 2020 & 2033

- Table 13: South America Compressor Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 14: South America Compressor Industry Volume K Units Forecast, by Geography 2020 & 2033

- Table 15: South America Compressor Industry Revenue million Forecast, by Country 2020 & 2033

- Table 16: South America Compressor Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 17: South America Compressor Industry Revenue million Forecast, by Type 2020 & 2033

- Table 18: South America Compressor Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 19: South America Compressor Industry Revenue million Forecast, by End User 2020 & 2033

- Table 20: South America Compressor Industry Volume K Units Forecast, by End User 2020 & 2033

- Table 21: South America Compressor Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 22: South America Compressor Industry Volume K Units Forecast, by Geography 2020 & 2033

- Table 23: South America Compressor Industry Revenue million Forecast, by Country 2020 & 2033

- Table 24: South America Compressor Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 25: South America Compressor Industry Revenue million Forecast, by Type 2020 & 2033

- Table 26: South America Compressor Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 27: South America Compressor Industry Revenue million Forecast, by End User 2020 & 2033

- Table 28: South America Compressor Industry Volume K Units Forecast, by End User 2020 & 2033

- Table 29: South America Compressor Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 30: South America Compressor Industry Volume K Units Forecast, by Geography 2020 & 2033

- Table 31: South America Compressor Industry Revenue million Forecast, by Country 2020 & 2033

- Table 32: South America Compressor Industry Volume K Units Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South America Compressor Industry?

The projected CAGR is approximately 4%.

2. Which companies are prominent players in the South America Compressor Industry?

Key companies in the market include Trane Technologies PLC, Ebara Corporation, ELGI Equipments Ltd*List Not Exhaustive, Atlas Copco AB, Baker Hughes Co, Aerzener Maschinenfabrik GmbH, Siemens AG, Schulz S A, General Electric Company.

3. What are the main segments of the South America Compressor Industry?

The market segments include Type, End User, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 1445.4 million as of 2022.

5. What are some drivers contributing to market growth?

4.; Growing Oil and Gas Industry4.; Rapid Growth in the Industrial Sector.

6. What are the notable trends driving market growth?

Oil and Gas Industry Segment Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Fluctuation in Oil and Gas Prices.

8. Can you provide examples of recent developments in the market?

September 2022: YPF and Petronas signed a deal to build a liquefied natural gas (LNG) plant and a pipeline to transport the fuel. The project's initial investment is estimated at around USD 10 billion. It is expected to have a capacity of a power output of 5 million tonnes of LNG during the first year of operation.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K Units.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South America Compressor Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South America Compressor Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South America Compressor Industry?

To stay informed about further developments, trends, and reports in the South America Compressor Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence