Key Insights

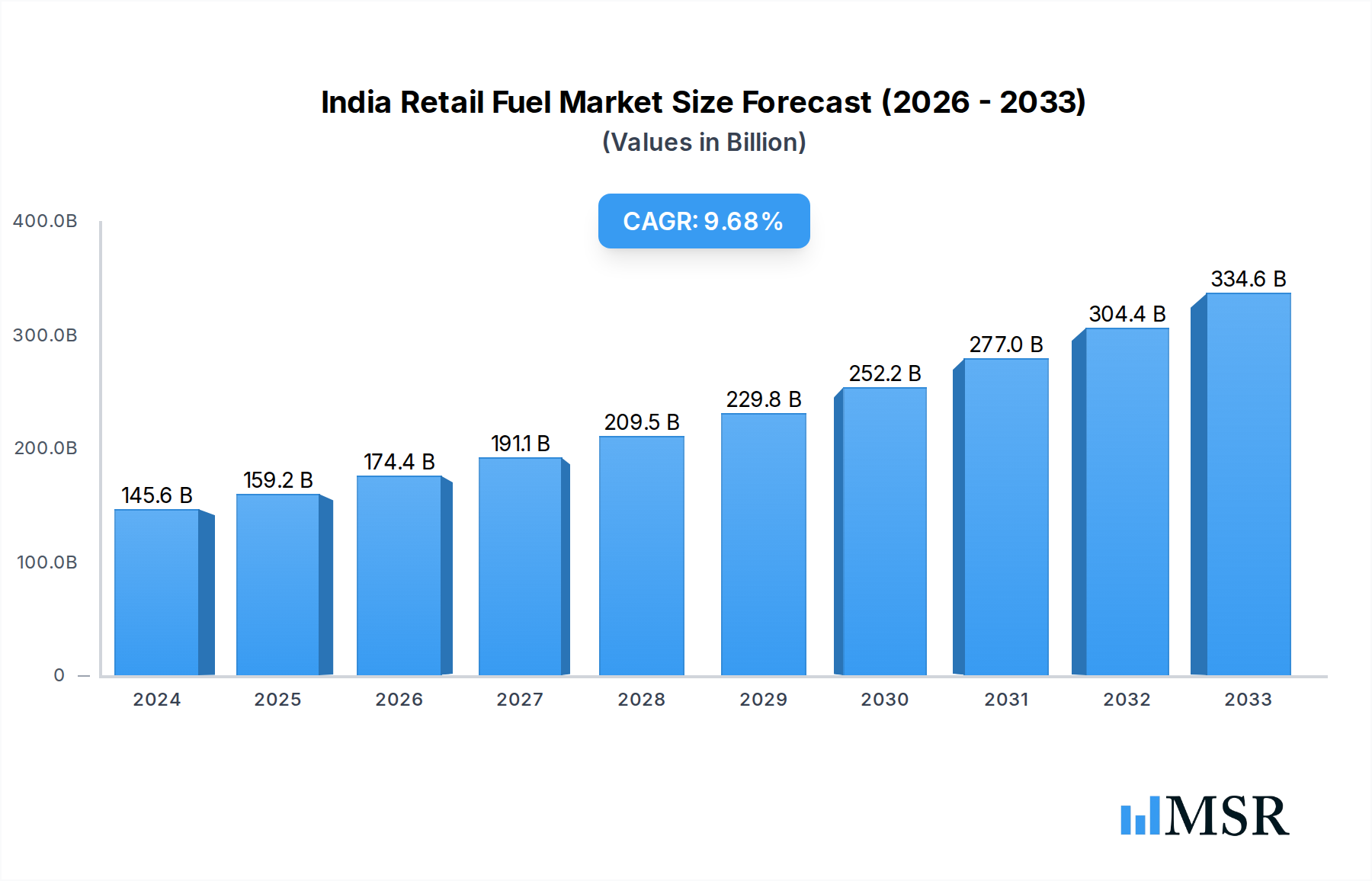

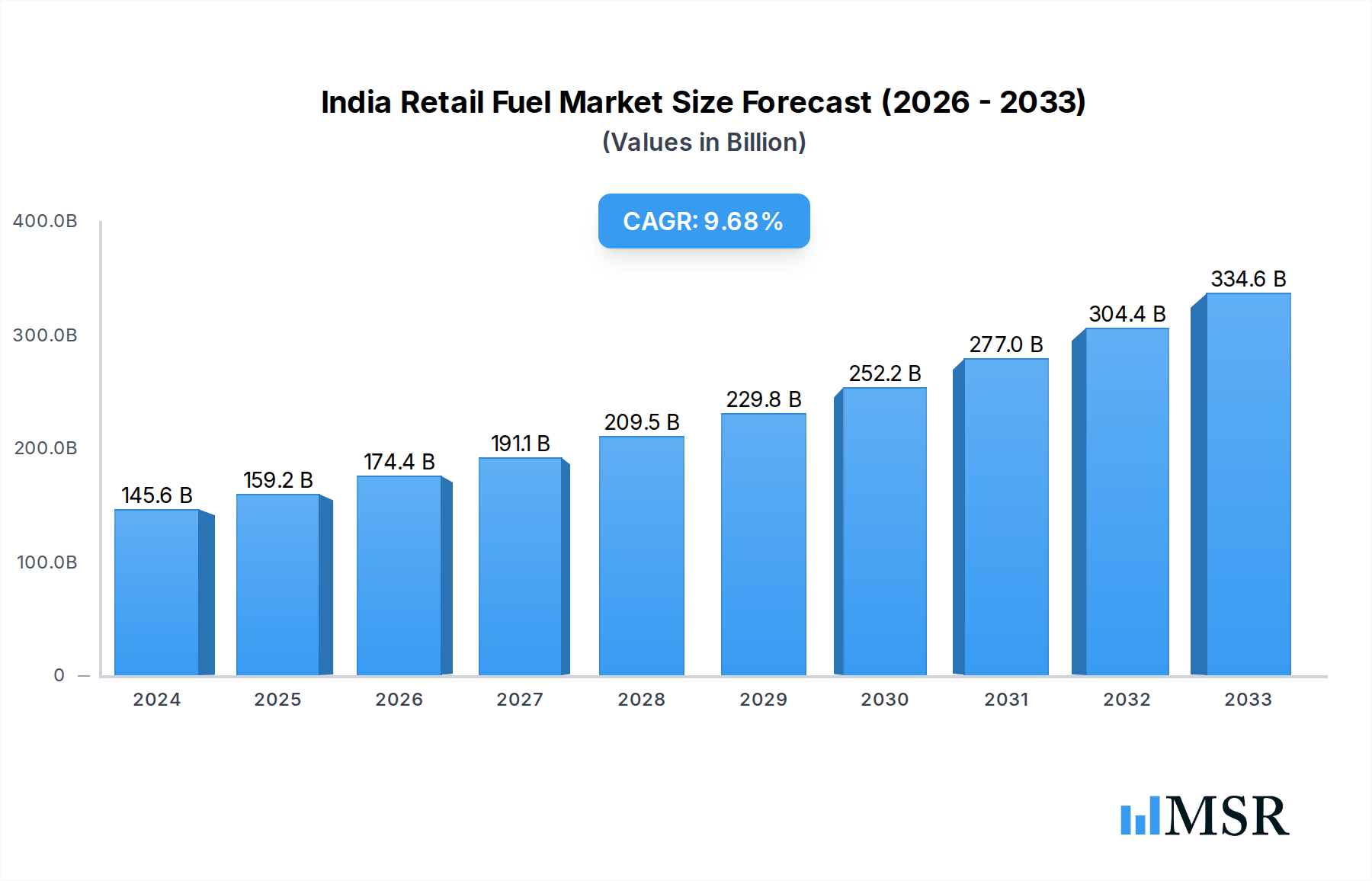

The India Retail Fuel Market is poised for substantial growth, projected to reach an estimated USD 145.63 billion in 2024, with a robust Compound Annual Growth Rate (CAGR) of 9.8% from 2025 to 2033. This expansion is primarily driven by increasing vehicle ownership, urbanization, and a burgeoning middle class with enhanced disposable income. The demand for transportation fuels, encompassing both petrol and diesel, is intrinsically linked to the nation's economic development and infrastructural advancements. Key growth catalysts include government initiatives promoting fuel efficiency, the expansion of retail fuel station networks across Tier 2 and Tier 3 cities, and the evolving consumer preference towards branded fuels offering superior quality and performance. The continuous rise in passenger vehicles, commercial fleets, and the agricultural sector's reliance on diesel engines further cements the market's upward trajectory.

India Retail Fuel Market Market Size (In Billion)

While the market demonstrates significant promise, certain restraints could influence its pace. Fluctuations in crude oil prices, geopolitical uncertainties, and the growing emphasis on electric vehicles (EVs) and alternative fuels present ongoing challenges. However, the vastness of India's existing internal combustion engine (ICE) fleet and the continued infrastructure development for conventional fuels are expected to mitigate these impacts in the medium term. The market segmentation reveals a dynamic interplay between public sector undertakings and private players, with both vying for dominance across public and private sector end-user segments. Major companies like Indian Oil Corporation Ltd., Reliance Industries Limited, and Shell PLC are actively investing in expanding their retail footprints and enhancing customer experiences to capture a larger market share amidst this competitive landscape. The transition towards cleaner fuels and improved operational efficiencies will be critical for sustained success.

India Retail Fuel Market Company Market Share

India Retail Fuel Market: In-depth Analysis and Future Outlook (2019-2033)

This comprehensive report provides an unparalleled deep dive into the India retail fuel market, a rapidly evolving sector driven by economic growth, technological innovation, and a strong push towards sustainability. Covering the historical period (2019-2024), base year (2025), estimated year (2025), and an extensive forecast period (2025-2033), this analysis offers actionable insights for oil marketing companies (OMCs), fuel retailers, investors, and policymakers. We meticulously examine market dynamics, key growth drivers, emerging trends, and the competitive landscape of the Indian petroleum market. Discover the opportunities within public sector undertakings (PSUs) and private owned entities, and understand the demand from public sector and private sector end-users.

India Retail Fuel Market Market Concentration & Dynamics

The India retail fuel market exhibits a moderate to high concentration, dominated by a few key public sector undertakings (PSUs) and burgeoning private owned players. Indian Oil Corporation Ltd (IOCL), Bharat Petroleum Corp Ltd (BPCL), and Hindustan Petroleum Corporation Limited (HPCL) collectively hold a significant market share, estimated to be over 70% of the petrol stations network. However, the entry of Reliance Industries Limited and Nayara Energy Limited, alongside international giants like Shell PLC and TotalEnergies SA, is intensifying competition and fostering innovation.

- Market Share Dynamics: While PSUs maintain dominance in the sheer number of petrol pumps and diesel sales, private players are gaining traction through strategic expansion, enhanced customer service, and diversified fuel offerings. Market share is influenced by fuel pricing, location, and the adoption of advanced technologies.

- Innovation Ecosystems: The market is witnessing innovation in fuel efficiency, biofuels, and digital integration at retail outlets. The adoption of SD-WAN technology for enhanced network connectivity at petrol stations is a testament to this.

- Regulatory Frameworks: Government policies, including fuel pricing mechanisms, environmental regulations, and mandates for ethanol blending, significantly shape market dynamics. Recent initiatives like the E20 fuel launch are direct outcomes of these frameworks.

- Substitute Products: While traditional petrol and diesel remain dominant, the rise of electric vehicles (EVs) and CNG presents long-term substitution threats, pushing the industry to explore alternative fuel solutions.

- End-User Trends: Shifting consumer preferences towards convenience, loyalty programs, and a growing awareness of environmental impact are influencing service delivery and product development at fuel stations.

- M&A Activities: While large-scale mergers are less frequent, strategic partnerships and acquisitions aimed at expanding distribution networks and acquiring technological capabilities are anticipated. The Indian fuel retail sector is ripe for consolidation and strategic alliances.

India Retail Fuel Market Industry Insights & Trends

The India retail fuel market is poised for robust growth, driven by a burgeoning economy, increasing vehicle ownership, and a strategic shift towards sustainable energy solutions. The market size is projected to expand significantly, with an estimated Compound Annual Growth Rate (CAGR) in the range of 7-9% over the forecast period. This expansion is fueled by a confluence of factors, including rising disposable incomes, urbanization, and government initiatives promoting cleaner fuels.

The government's focus on ethanol blending, aiming for E20 fuel (20% ethanol blended with petrol) by 2025, is a pivotal trend shaping the petrol market. This initiative not only addresses environmental concerns by reducing carbon emissions from conventional fuels but also supports the agricultural sector by creating demand for ethanol. Oil marketing companies (OMCs) like HPCL are actively investing in biofuel production facilities to meet this ambitious target. The widespread adoption of E20 fuel across numerous states and union territories signifies a monumental step towards a greener fuel economy.

Technological disruptions are transforming the Indian fuel retail landscape. The implementation of advanced retail automation systems, digital payment solutions, and customer loyalty programs at petrol stations is enhancing operational efficiency and customer experience. For instance, Indian Oil Corporation (IOCL) selecting Reliance Jio to connect its vast network of 7,200 IOC sites with SD-WAN technology underscores the industry's commitment to robust and secure digital infrastructure. This move ensures seamless connectivity, zero-touch provisioning, and 24/7 real-time monitoring, crucial for efficient fuel distribution and retail operations.

Evolving consumer behaviors are also playing a critical role. As the middle class expands, there's a growing demand for enhanced convenience, quality service, and a wider array of non-fuel retail offerings at fuel stations. Companies are responding by transforming petrol pumps into convenience hubs, offering services like EV charging, car washes, and food and beverage options. The proactive introduction of E20 gasoline by players like Jio-bp demonstrates an alignment with both regulatory mandates and consumer interest in more sustainable fuel options. The market is witnessing a transition from purely transactional fuel sales to a more experiential retail model.

Key Markets & Segments Leading India Retail Fuel Market

The India retail fuel market is a dynamic arena where Public Sector Undertakings (PSUs) and Private Owned entities operate across diverse segments, catering to both Public Sector and Private Sector end-users. The market's leadership is a result of strategic investments, expansive infrastructure, and an evolving regulatory landscape.

Public Sector Undertakings (PSUs) Dominance

- Extensive Network: PSU OMCs like Indian Oil Corporation Ltd (IOCL), Hindustan Petroleum Corporation Limited (HPCL), and Bharat Petroleum Corp Ltd (BPCL) dominate the petrol and diesel market due to their historical presence and vast network of over 60,000 petrol stations across India. This unparalleled reach ensures accessibility even in remote regions.

- Government Support: These entities benefit from implicit government backing, ensuring stability and access to capital for infrastructure development and expansion. Their role in national energy security is paramount.

- Retail Market Share: PSUs command a substantial share of the retail fuel sales, driven by established brand loyalty and widespread availability. They are crucial for meeting the fuel demands of both public sector organizations and the general populace.

- Infrastructure Investments: PSUs are at the forefront of investing in modernizing fuel stations, including the rollout of E20 fuel infrastructure and exploring EV charging solutions, aligning with national sustainability goals.

Private Owned Sector Growth

- Aggressive Expansion: Private players such as Reliance Industries Limited and Nayara Energy Limited, along with international entities like Shell PLC and TotalEnergies SA, are aggressively expanding their fuel retail network. They focus on strategic locations, urban centers, and high-traffic corridors.

- Customer-Centric Approach: Private companies often differentiate themselves through superior customer service, advanced loyalty programs, and non-fuel retail (NFR) offerings, attracting a segment of the private sector and discerning consumers.

- Technological Adoption: These players are quicker to adopt new technologies, from advanced forecourt automation to sophisticated data analytics for customer engagement and inventory management. The adoption of SD-WAN by IOCL, a PSU, in partnership with Reliance Jio, highlights the increasing synergy and technological advancements driven by private sector innovation.

- Niche Market Penetration: While PSUs serve the mass market, private players are increasingly focusing on specific segments, such as premium fuels, specialized industrial lubricants, and offering integrated services at their petrol pumps.

End User Segmentation

- Public Sector Demand: Government fleets, public transport, and state-owned enterprises constitute a significant portion of the fuel demand. PSUs have historically held strong relationships with these entities, ensuring a consistent off-take.

- Private Sector Consumption: The rapidly growing private sector in India, encompassing transportation, logistics, manufacturing, and individual vehicle owners, represents the largest and fastest-growing segment of fuel consumption. This segment is increasingly discerning and responsive to service quality, pricing, and innovative fuel products.

The interplay between PSUs and private players, driven by both economic growth and evolving consumer needs, is shaping a competitive yet expanding India retail fuel market. The ongoing transition towards cleaner fuels like E20 will further influence segment dominance and strategic imperatives.

India Retail Fuel Market Product Developments

The India retail fuel market is witnessing significant product developments aimed at enhancing efficiency, sustainability, and customer experience. The nationwide rollout of E20 fuel, a blend of 20% ethanol with petrol, is a prime example, driven by the government's commitment to reducing environmental emissions and promoting a greener fuel economy. Oil marketing companies (OMCs) like HPCL have invested in upgrading their facilities to produce and distribute this cleaner alternative. Furthermore, players like Jio-bp are actively marketing E20 gasoline to customers with compatible vehicles, signaling a shift towards sustainable fuel solutions at the pump. These developments are not only aligned with regulatory mandates but also cater to a growing consumer awareness of environmental impact, offering a competitive edge in the evolving petrol and diesel market.

Challenges in the India Retail Fuel Market Market

The India retail fuel market faces several significant challenges that impact its growth trajectory and operational efficiency.

- Regulatory Hurdles: Complex and evolving government regulations, particularly concerning fuel pricing, import duties, and environmental standards, can create uncertainty and impact profitability for fuel retailers.

- Supply Chain Volatility: Dependence on imported crude oil exposes the market to global price fluctuations and geopolitical risks, leading to volatility in petrol and diesel prices. Disruptions in the supply chain can impact inventory management and availability at petrol stations.

- Intensifying Competition: The growing presence of both domestic private owned companies and international players, alongside the established PSU network, intensifies competition, leading to price wars and pressure on margins for fuel distributors.

- Infrastructure Development: While significant progress has been made, the expansion and modernization of fuel infrastructure, including retail outlets and storage facilities, still lag behind the pace of demand growth in certain regions.

- Shift to Alternatives: The long-term threat from alternative energy sources like electric vehicles necessitates continuous adaptation and diversification of fuel offerings by oil marketing companies (OMCs).

Forces Driving India Retail Fuel Market Growth

The India retail fuel market is propelled by a robust set of growth drivers, indicating a promising future for fuel distribution and retail operations.

- Economic Growth & Urbanization: India's sustained economic expansion and rapid urbanization lead to increased industrial activity, commercial transportation, and a growing number of private vehicles, directly boosting the demand for petrol and diesel.

- Rising Vehicle Ownership: A burgeoning middle class with increasing disposable incomes translates into higher vehicle ownership rates, significantly driving the demand for automotive fuels at petrol stations.

- Government Initiatives: Supportive government policies, such as the push for ethanol blending (E20 fuel) and investments in infrastructure, are creating a favorable environment for fuel retailers and promoting cleaner energy solutions.

- Infrastructure Development: Continuous investment in road networks and transportation infrastructure facilitates better connectivity and accessibility, supporting the expansion of fuel retail networks.

- Technological Advancements: The adoption of digital technologies in fuel retail management, customer engagement, and supply chain optimization enhances efficiency and customer experience, contributing to market growth.

Challenges in the India Retail Fuel Market Market

The India retail fuel market is on a trajectory of significant long-term growth, driven by several key catalysts that promise sustained expansion and innovation.

- Energy Transition Opportunities: The global shift towards cleaner energy presents opportunities for oil marketing companies (OMCs) to diversify their portfolios into biofuels, hydrogen, and EV charging infrastructure at their petrol stations, creating new revenue streams and addressing environmental concerns.

- Digital Transformation: Continued investment in digital technologies, including data analytics for personalized customer experiences, smart fuel dispensers, and enhanced supply chain management, will drive operational efficiencies and foster customer loyalty in the fuel retail sector.

- Strategic Partnerships and M&A: Opportunities for strategic alliances and mergers and acquisitions (M&A) will likely emerge, allowing companies to consolidate market presence, acquire new technologies, and expand their geographical reach in the competitive petroleum market.

- Rural Market Penetration: Significant untapped potential exists in rural and semi-urban areas, offering opportunities for expansion and reaching new customer segments with essential fuel supplies.

- Focus on Non-Fuel Retail (NFR): The increasing trend of transforming petrol pumps into convenience hubs with diverse NFR offerings will continue to be a major growth accelerator, enhancing customer dwell time and increasing revenue per outlet.

Emerging Opportunities in India Retail Fuel Market

The India retail fuel market is ripe with emerging opportunities driven by evolving consumer preferences, technological advancements, and a national push towards sustainability.

- Biofuels and Alternative Fuels: The increasing focus on reducing carbon emissions presents a substantial opportunity for the wider adoption and development of biofuels, including E20 fuel, and other alternative fuels. This aligns with the government's greener fuel economy goals.

- Electric Vehicle (EV) Charging Infrastructure: As India accelerates its EV adoption, fuel retailers can capitalize on the growing demand for EV charging stations at their petrol stations, creating a synergistic business model.

- Convenience Retail and Value-Added Services: The trend of transforming fuel stations into comprehensive service hubs, offering a wide array of non-fuel retail (NFR) products, food and beverages, and other convenience services, presents a significant opportunity to enhance revenue streams and customer engagement.

- Digitalization and IoT Integration: Leveraging digital technologies, including AI-powered customer analytics, IoT for smart fuel dispensers, and seamless mobile payment solutions, can optimize operations, personalize customer experiences, and build stronger brand loyalty in the petroleum retail sector.

- Expansion into Tier 2 and Tier 3 Cities: Significant untapped market potential lies in expanding the retail fuel network and associated services into Tier 2 and Tier 3 cities, catering to the growing demand from these rapidly developing regions.

Leading Players in the India Retail Fuel Market Sector

- Shell PLC

- TotalEnergies SA

- Hindustan Petroleum Corporation Limited

- Reliance Industries Limited

- Bharat Petroleum Corp Ltd

- Nayara Energy Limited

- Indian Oil Corporation Ltd

Key Milestones in India Retail Fuel Market Industry

- February 2023: The Government of India announced the launch of E20 fuel across 11 states and union territories at 84 retail outlets in India. The Indian government aims to achieve 20% blending of ethanol with petrol by 2025 in the country. The step was taken to control the environmental emission from conventional fuels and progress towards a greener fuel economy. Oil marketing companies (OMC), including HPCL, have set up plants to accomplish the goal.

- February 2023: Jio-bp, one of India's leading retail fuel companies, began selling E20 gasoline. Customers with E20 petrol-compatible vehicles will be able to choose this fuel at select Jio-bp locations, and the service will be spread across the network shortly.

- December 2022: Indian Oil Corporation (IOCL) announced that for five years, Indian Oil Corporation (IOC) had chosen Reliance Jio to connect its 7,200 IOC sites using SD-WAN (Software Defined Wide Area Network). Jio will connect 7,200 IOC sites with an SD-WAN managed service solution, zero-touch provisioning, and real-time monitoring 24 hours a day, seven days a week.

Strategic Outlook for India Retail Fuel Market Market

The strategic outlook for the India retail fuel market is characterized by a transition towards greater sustainability, enhanced customer experience, and digital integration. Oil marketing companies (OMCs) and private owned players will increasingly focus on expanding their EV charging infrastructure, developing and promoting biofuels like E20 fuel, and leveraging digital technologies to optimize operations and personalize customer interactions. Strategic partnerships and potential mergers will play a crucial role in consolidating market presence and acquiring new capabilities. The expansion of non-fuel retail (NFR) offerings at petrol stations will be a key growth accelerator, transforming them into convenience hubs. Embracing these evolving trends will be critical for sustained success and market leadership in the dynamic Indian petroleum market.

India Retail Fuel Market Segmentation

-

1. Ownership

- 1.1. Public Sector Undertakings

- 1.2. Private Owned

-

2. End User

- 2.1. Public Sector

- 2.2. Private Sector

India Retail Fuel Market Segmentation By Geography

- 1. India

India Retail Fuel Market Regional Market Share

Geographic Coverage of India Retail Fuel Market

India Retail Fuel Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.62% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Ownership

- 5.1.1. Public Sector Undertakings

- 5.1.2. Private Owned

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Public Sector

- 5.2.2. Private Sector

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. India

- 5.1. Market Analysis, Insights and Forecast - by Ownership

- 6. India Retail Fuel Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Ownership

- 6.1.1. Public Sector Undertakings

- 6.1.2. Private Owned

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Public Sector

- 6.2.2. Private Sector

- 6.1. Market Analysis, Insights and Forecast - by Ownership

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Shell PLC

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 TotalEnergies SA

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Hindustan Petroleum Corporation Limited

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Reliance Industries Limited

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Bharat Petroleum Corp Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Nayara Energy Limited

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Indian Oil Corporation Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.1 Shell PLC

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: India Retail Fuel Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: India Retail Fuel Market Share (%) by Company 2025

List of Tables

- Table 1: India Retail Fuel Market Revenue billion Forecast, by Ownership 2020 & 2033

- Table 2: India Retail Fuel Market Volume Metric Tonns Forecast, by Ownership 2020 & 2033

- Table 3: India Retail Fuel Market Revenue billion Forecast, by End User 2020 & 2033

- Table 4: India Retail Fuel Market Volume Metric Tonns Forecast, by End User 2020 & 2033

- Table 5: India Retail Fuel Market Revenue billion Forecast, by Region 2020 & 2033

- Table 6: India Retail Fuel Market Volume Metric Tonns Forecast, by Region 2020 & 2033

- Table 7: India Retail Fuel Market Revenue billion Forecast, by Ownership 2020 & 2033

- Table 8: India Retail Fuel Market Volume Metric Tonns Forecast, by Ownership 2020 & 2033

- Table 9: India Retail Fuel Market Revenue billion Forecast, by End User 2020 & 2033

- Table 10: India Retail Fuel Market Volume Metric Tonns Forecast, by End User 2020 & 2033

- Table 11: India Retail Fuel Market Revenue billion Forecast, by Country 2020 & 2033

- Table 12: India Retail Fuel Market Volume Metric Tonns Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Retail Fuel Market?

The projected CAGR is approximately 2.62%.

2. Which companies are prominent players in the India Retail Fuel Market?

Key companies in the market include Shell PLC, TotalEnergies SA, Hindustan Petroleum Corporation Limited, Reliance Industries Limited, Bharat Petroleum Corp Ltd, Nayara Energy Limited, Indian Oil Corporation Ltd.

3. What are the main segments of the India Retail Fuel Market?

The market segments include Ownership, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 54.8 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Growing Vehicle Ownership4.; Government Initiatives.

6. What are the notable trends driving market growth?

The Public Sector Undertakings Segment is Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Volatile Crude Oil Prices.

8. Can you provide examples of recent developments in the market?

February 2023: The Government of India announced the launch of E20 fuel across 11 states and union territories at 84 retail outlets in India. The Indian government aims to achieve 20% blending of ethanol with petrol by 2025 in the country. The step was taken to control the environmental emission from conventional fuels and progress towards a greener fuel economy. Oil marketing companies (OMC), including HPCL, have set up plants to accomplish the goal.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in Metric Tonns.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Retail Fuel Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Retail Fuel Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Retail Fuel Market?

To stay informed about further developments, trends, and reports in the India Retail Fuel Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence