Key Insights

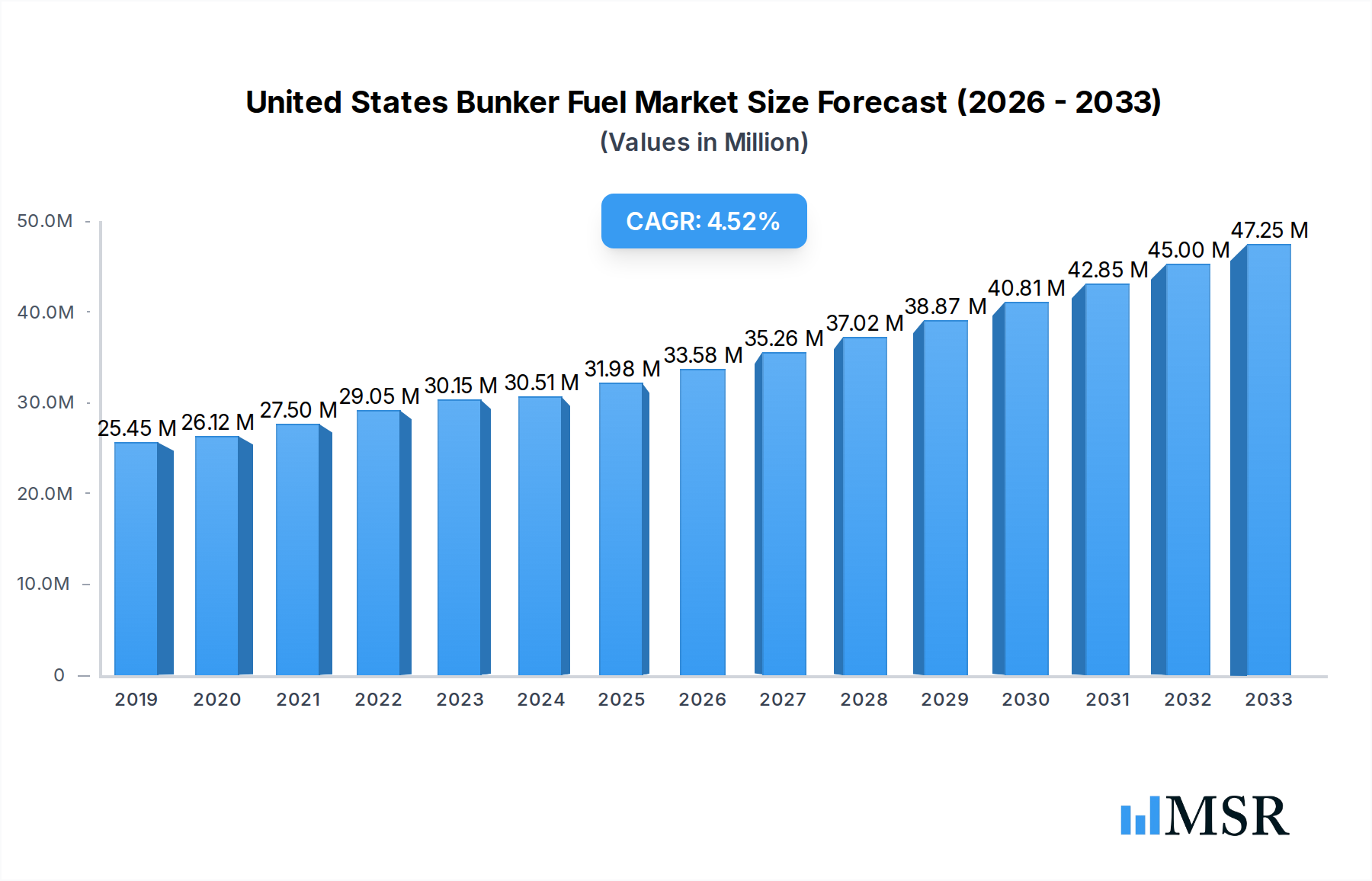

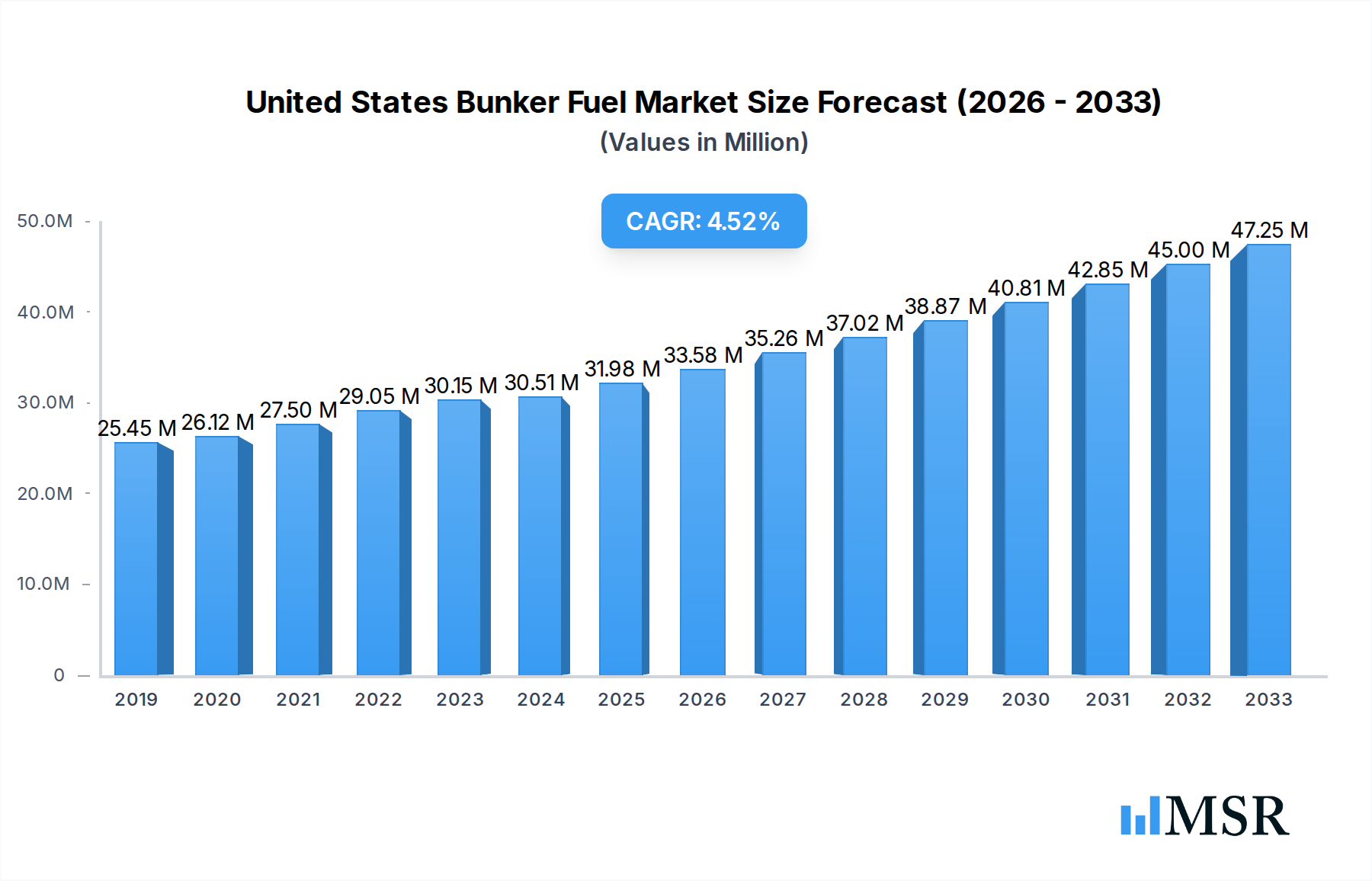

The United States bunker fuel market is poised for steady expansion, driven by robust maritime trade and evolving regulatory landscapes. With an estimated market size of $30.51 billion in 2024, the sector is projected to grow at a Compound Annual Growth Rate (CAGR) of 5% through 2033. This growth is primarily fueled by the increasing demand for cleaner marine fuels, such as Liquefied Natural Gas (LNG) and Very-low Sulfur Fuel Oil (VLSFO), in response to stringent environmental regulations like those set by the International Maritime Organization (IMO). The ongoing shift towards these lower-sulfur alternatives necessitates significant investment in infrastructure and fuel processing, creating opportunities for market players. Furthermore, the resurgence in global trade, particularly for containerized goods and bulk commodities, directly translates to higher demand for bunker fuels to power the extensive tanker and container fleets operating in and around U.S. waters.

United States Bunker Fuel Market Market Size (In Million)

Despite the positive growth trajectory, the U.S. bunker fuel market faces certain headwinds. Fluctuations in crude oil prices, a primary determinant of bunker fuel costs, can impact profitability and investment decisions. Geopolitical instability and global economic uncertainties also pose a risk to the sustained growth of maritime trade, thereby affecting bunker fuel consumption. Moreover, the substantial capital required for the transition to alternative and cleaner fuels, along with the development of LNG bunkering infrastructure, presents a significant barrier to entry for smaller players and necessitates strategic partnerships. However, the market's resilience is expected to be supported by continuous technological advancements aimed at improving fuel efficiency and the ongoing need to comply with increasingly stringent environmental standards, ensuring a dynamic and evolving market landscape.

United States Bunker Fuel Market Company Market Share

United States Bunker Fuel Market Report: Comprehensive Analysis and Future Outlook (2019–2033)

This in-depth report delivers a panoramic view of the United States bunker fuel market, a critical sector supporting maritime trade and energy logistics. Spanning the study period from 2019 to 2033, with a base year of 2025, this analysis provides actionable insights for industry stakeholders navigating this dynamic landscape. We dissect market concentration, industry trends, key segments, product developments, challenges, growth drivers, and emerging opportunities, alongside a detailed examination of leading players and pivotal milestones. Forecasted market size is estimated at USD xx billion in 2025, with a projected Compound Annual Growth Rate (CAGR) of xx% throughout the forecast period.

United States Bunker Fuel Market Market Concentration & Dynamics

The United States bunker fuel market is characterized by a moderate to high level of concentration, with a few dominant players controlling a significant portion of the market share. However, a growing number of regional suppliers and emerging fuel types are fostering a more competitive environment. The innovation ecosystem is actively evolving, driven by the demand for cleaner fuels and advancements in supply chain logistics. Regulatory frameworks, particularly those driven by environmental mandates like IMO 2020 and forthcoming US-specific regulations, are profoundly shaping market dynamics. Substitute products, such as shoreside power and alternative fuel sources for certain vessel types, are gaining traction, influencing traditional bunker fuel demand. End-user trends are increasingly focused on cost-efficiency, environmental compliance, and reliable supply chains. Mergers and acquisitions (M&A) activities are anticipated to continue as larger entities seek to consolidate their market position and expand their service offerings. M&A deal counts are predicted to rise by xx% over the forecast period. Key market share leaders are estimated to hold xx% of the market by 2025.

United States Bunker Fuel Market Industry Insights & Trends

The United States bunker fuel market is experiencing robust growth, propelled by several key factors. The U.S. maritime trade volume remains a primary driver, with increasing imports and exports necessitating substantial bunker fuel consumption for a diverse fleet. Technological disruptions are transforming the landscape, with a notable shift towards very-low sulfur fuel oil (VLSFO) and marine gas oil (MGO) due to stringent environmental regulations. The adoption of liquefied natural gas (LNG) as a marine fuel is also accelerating, particularly for new builds and retrofitted vessels, offering a cleaner alternative. Evolving consumer behaviors are evident in the demand for more sustainable and cost-effective fuel solutions, pushing suppliers to innovate. The market size for bunker fuel in the United States was estimated at USD xx billion in 2024 and is projected to reach USD xx billion by 2033. The CAGR for the historical period (2019-2024) was xx%, and it is expected to be xx% during the forecast period (2025-2033). The increasing emphasis on reducing greenhouse gas emissions and improving air quality at ports is a significant trend, leading to greater adoption of cleaner bunker fuels. The development of advanced refueling infrastructure for alternative fuels, such as LNG, is also a crucial trend shaping the market. Furthermore, digital transformation in the bunker fuel industry, including online trading platforms and real-time tracking, is enhancing operational efficiency and transparency.

Key Markets & Segments Leading United States Bunker Fuel Market

The United States East Coast is a dominant region within the U.S. bunker fuel market, driven by its extensive port infrastructure and high volume of container and tanker traffic. Key segments like Very-low Sulfur Fuel Oil (VLSFO) and Marine Gas Oil (MGO) are leading the market due to environmental regulations mandating lower sulfur content in marine fuels.

Fuel Type Dominance:

- Very-low Sulfur Fuel Oil (VLSFO): Driven by IMO 2020 regulations and ongoing environmental concerns, VLSFO has become the dominant fuel type, particularly in major U.S. ports. Its adoption is further supported by the availability of refining capacity and established distribution networks. Economic growth and increased global trade are directly contributing to higher demand for VLSFO.

- Marine Gas Oil (MGO): MGO, with its even lower sulfur content, is also experiencing significant growth, especially for vessels operating in Emission Control Areas (ECAs) and for shorter sea voyages. Its versatility and ease of use make it a preferred choice for many operators seeking compliance.

- Liquefied Natural Gas (LNG): While still a nascent segment, LNG is poised for substantial growth, driven by long-term sustainability goals and governmental incentives for cleaner fuels. The increasing number of LNG-powered vessels and the development of dedicated bunkering infrastructure are key growth enablers.

- High Sulfur Fuel Oil (HSFO): Demand for HSFO has decreased significantly due to regulatory pressures, though it continues to be used by vessels equipped with exhaust gas cleaning systems (scrubbers).

- Others: This segment may include emerging alternative fuels and specialty marine fuels.

Vessel Type Dominance:

- Container Fleet: The burgeoning e-commerce sector and global supply chain demands have fueled a consistent increase in containerized cargo, leading to robust demand for bunker fuel from this vessel type. Expansion of port facilities and greater vessel capacities further support this segment.

- Tanker Fleet: The energy sector's reliance on crude oil and refined product transportation ensures a consistent demand for bunker fuel from the tanker fleet. Fluctuations in global energy prices and geopolitical events can impact the volume of tanker traffic.

- Bulk Carrier: The movement of raw materials, agricultural products, and manufactured goods by bulk carriers contributes significantly to bunker fuel consumption. Global industrial output and commodity prices are key drivers for this segment.

- General Cargo Carriers: While less dominant than the aforementioned segments, general cargo carriers still represent a notable portion of the bunker fuel market.

- Others: This category includes specialized vessels like offshore support vessels, ferries, and tugboats, each with specific fuel requirements.

United States Bunker Fuel Market Product Developments

Product innovation in the United States bunker fuel market is primarily focused on cleaner fuel alternatives and enhanced fuel efficiency. The development of advanced VLSFO blends with improved combustion properties and reduced emissions is a key area of research. Furthermore, advancements in LNG bunkering technology, including mobile solutions and larger storage capacities, are enhancing its market viability. The relevance of these product developments lies in their ability to help vessel operators meet stringent environmental regulations, reduce operating costs through improved fuel economy, and align with growing sustainability demands from consumers and regulatory bodies.

Challenges in the United States Bunker Fuel Market Market

The United States bunker fuel market faces several significant challenges. Regulatory hurdles, including the evolving landscape of emission standards and potential carbon pricing mechanisms, can create uncertainty and necessitate costly adaptations for fuel suppliers and consumers. Supply chain disruptions, exacerbated by geopolitical events and logistical bottlenecks, can lead to price volatility and availability issues. Competitive pressures from alternative fuels and shoreside power solutions, while driving innovation, also pose a threat to traditional bunker fuel volumes. The upfront investment required for adopting cleaner fuels and associated infrastructure represents a substantial barrier for many smaller operators, impacting market penetration.

Forces Driving United States Bunker Fuel Market Growth

Key forces driving the United States bunker fuel market growth are multifaceted. Technological advancements in refining processes and the development of cleaner fuel formulations are paramount. Economic factors, such as increasing global trade volumes and robust domestic industrial activity, directly translate into higher demand for maritime transportation and, consequently, bunker fuel. Furthermore, regulatory drivers, specifically environmental mandates from organizations like the International Maritime Organization (IMO) and domestic environmental agencies, are compelling a shift towards lower-sulfur and alternative fuels. The growing emphasis on sustainability and corporate social responsibility is also accelerating the adoption of cleaner energy solutions.

Challenges in the United States Bunker Fuel Market Market

Long-term growth catalysts in the United States bunker fuel market are rooted in sustained innovation and strategic market expansions. The continued investment in research and development for next-generation marine fuels, including biofuels and synthetic fuels, presents significant future potential. Strategic partnerships between fuel suppliers, technology providers, and vessel operators will be crucial for scaling up the adoption of these novel fuels. Market expansions into new geographical areas or for niche vessel segments, coupled with the development of integrated energy solutions for the maritime sector, will also contribute to sustained growth. The ongoing commitment to reducing the carbon footprint of shipping will continue to be a powerful long-term growth accelerator.

Emerging Opportunities in United States Bunker Fuel Market

Emerging opportunities in the United States bunker fuel market are abundant, driven by a global push towards decarbonization. The increasing adoption of LNG as a marine fuel presents a significant opportunity for infrastructure development and supply chain expansion. The potential for biofuels and synthetic fuels as direct replacements for traditional bunker fuels offers a pathway to achieving net-zero emissions. Furthermore, the development of smart bunkering solutions, leveraging digital technologies for optimized fuel delivery and inventory management, represents a growing area of opportunity. Growing consumer preference for environmentally responsible shipping practices is also creating demand for green bunker fuel options.

Leading Players in the United States Bunker Fuel Market Sector

- World Fuel Services Corporation

- Exxon Mobil Corporation

- BP plc

- Chevron Corporation

- Royal Dutch Shell PLC

- Clipper Oil Company

- NuStar Energy L P

- Total S A

Key Milestones in United States Bunker Fuel Market Industry

- 2019: Implementation of IMO 2020 sulfur cap regulations, significantly impacting fuel choices and driving demand for VLSFO and MGO.

- 2020: Increased focus on scrubber installations by a growing number of vessels to continue using HSFO.

- 2021: Growing interest and initial investments in LNG bunkering infrastructure at key U.S. ports.

- 2022: Rise in price volatility of traditional bunker fuels due to global supply chain disruptions and geopolitical events.

- 2023: Significant advancements in the development of sustainable biofuels and e-fuels for maritime applications.

- 2024: Continued expansion of LNG-powered vessel fleets and the associated bunkering network.

Strategic Outlook for United States Bunker Fuel Market Market

The strategic outlook for the United States bunker fuel market is one of transformation and opportunity. The market is expected to witness a continued shift towards cleaner fuels, driven by stringent environmental regulations and growing sustainability imperatives. Investment in advanced refining technologies, the development of robust supply chains for alternative fuels like LNG, and the exploration of biofuels and synthetic fuels will be crucial growth accelerators. Strategic partnerships and collaborations across the value chain will be essential for navigating the complexities of this evolving landscape and capitalizing on future market potential, particularly in areas aligned with the decarbonization of the global shipping industry.

United States Bunker Fuel Market Segmentation

-

1. Fuel Type

- 1.1. High Sulfur Fuel Oil (HSFO)

- 1.2. Very-low Sulfur Fuel Oil (VLSFO)

- 1.3. Marine Gas Oil (MGO)

- 1.4. Liquefied Natural Gas (LNG)

- 1.5. Others

-

2. Vessel Type

- 2.1. Tanker Fleet

- 2.2. Container Fleet

- 2.3. Bulk Carrier

- 2.4. General Cargo Carriers

- 2.5. Others

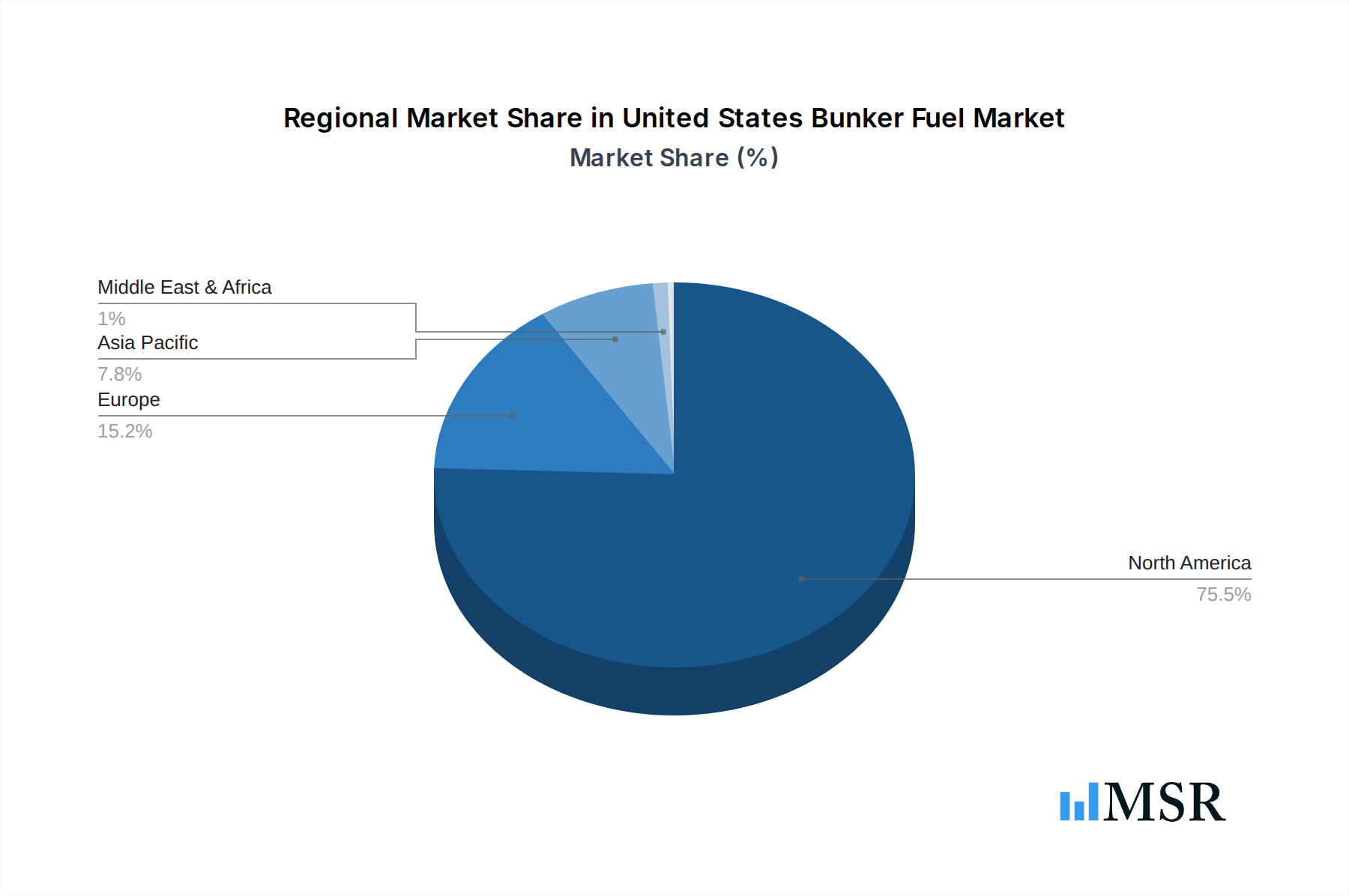

United States Bunker Fuel Market Segmentation By Geography

- 1. United States

United States Bunker Fuel Market Regional Market Share

Geographic Coverage of United States Bunker Fuel Market

United States Bunker Fuel Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Fuel Type

- 5.1.1. High Sulfur Fuel Oil (HSFO)

- 5.1.2. Very-low Sulfur Fuel Oil (VLSFO)

- 5.1.3. Marine Gas Oil (MGO)

- 5.1.4. Liquefied Natural Gas (LNG)

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Vessel Type

- 5.2.1. Tanker Fleet

- 5.2.2. Container Fleet

- 5.2.3. Bulk Carrier

- 5.2.4. General Cargo Carriers

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United States

- 5.1. Market Analysis, Insights and Forecast - by Fuel Type

- 6. United States Bunker Fuel Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Fuel Type

- 6.1.1. High Sulfur Fuel Oil (HSFO)

- 6.1.2. Very-low Sulfur Fuel Oil (VLSFO)

- 6.1.3. Marine Gas Oil (MGO)

- 6.1.4. Liquefied Natural Gas (LNG)

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Vessel Type

- 6.2.1. Tanker Fleet

- 6.2.2. Container Fleet

- 6.2.3. Bulk Carrier

- 6.2.4. General Cargo Carriers

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Fuel Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 World Fuel Services Corporation*List Not Exhaustive

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Exxon Mobil Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 BP plc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Chevron Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Royal Dutch Shell PLC

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Clipper Oil Company

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 NuStar Energy L P

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Total S A

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.1 World Fuel Services Corporation*List Not Exhaustive

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: United States Bunker Fuel Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: United States Bunker Fuel Market Share (%) by Company 2025

List of Tables

- Table 1: United States Bunker Fuel Market Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 2: United States Bunker Fuel Market Volume metric tonnes Forecast, by Fuel Type 2020 & 2033

- Table 3: United States Bunker Fuel Market Revenue billion Forecast, by Vessel Type 2020 & 2033

- Table 4: United States Bunker Fuel Market Volume metric tonnes Forecast, by Vessel Type 2020 & 2033

- Table 5: United States Bunker Fuel Market Revenue billion Forecast, by Region 2020 & 2033

- Table 6: United States Bunker Fuel Market Volume metric tonnes Forecast, by Region 2020 & 2033

- Table 7: United States Bunker Fuel Market Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 8: United States Bunker Fuel Market Volume metric tonnes Forecast, by Fuel Type 2020 & 2033

- Table 9: United States Bunker Fuel Market Revenue billion Forecast, by Vessel Type 2020 & 2033

- Table 10: United States Bunker Fuel Market Volume metric tonnes Forecast, by Vessel Type 2020 & 2033

- Table 11: United States Bunker Fuel Market Revenue billion Forecast, by Country 2020 & 2033

- Table 12: United States Bunker Fuel Market Volume metric tonnes Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United States Bunker Fuel Market?

The projected CAGR is approximately 5%.

2. Which companies are prominent players in the United States Bunker Fuel Market?

Key companies in the market include World Fuel Services Corporation*List Not Exhaustive, Exxon Mobil Corporation, BP plc, Chevron Corporation, Royal Dutch Shell PLC, Clipper Oil Company, NuStar Energy L P, Total S A.

3. What are the main segments of the United States Bunker Fuel Market?

The market segments include Fuel Type, Vessel Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 30.51 billion as of 2022.

5. What are some drivers contributing to market growth?

Government Policies for the Adoption of Energy-efficient Lighting Systems; Adoption of IoT with Lighting Systems.

6. What are the notable trends driving market growth?

Very-Low Sulfur Fuel Oil (VLSFO) Segment is Expected to Witness Significant Growth.

7. Are there any restraints impacting market growth?

The global shift toward renewable sources for electricity generation.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in metric tonnes.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United States Bunker Fuel Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United States Bunker Fuel Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United States Bunker Fuel Market?

To stay informed about further developments, trends, and reports in the United States Bunker Fuel Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence