Key Insights

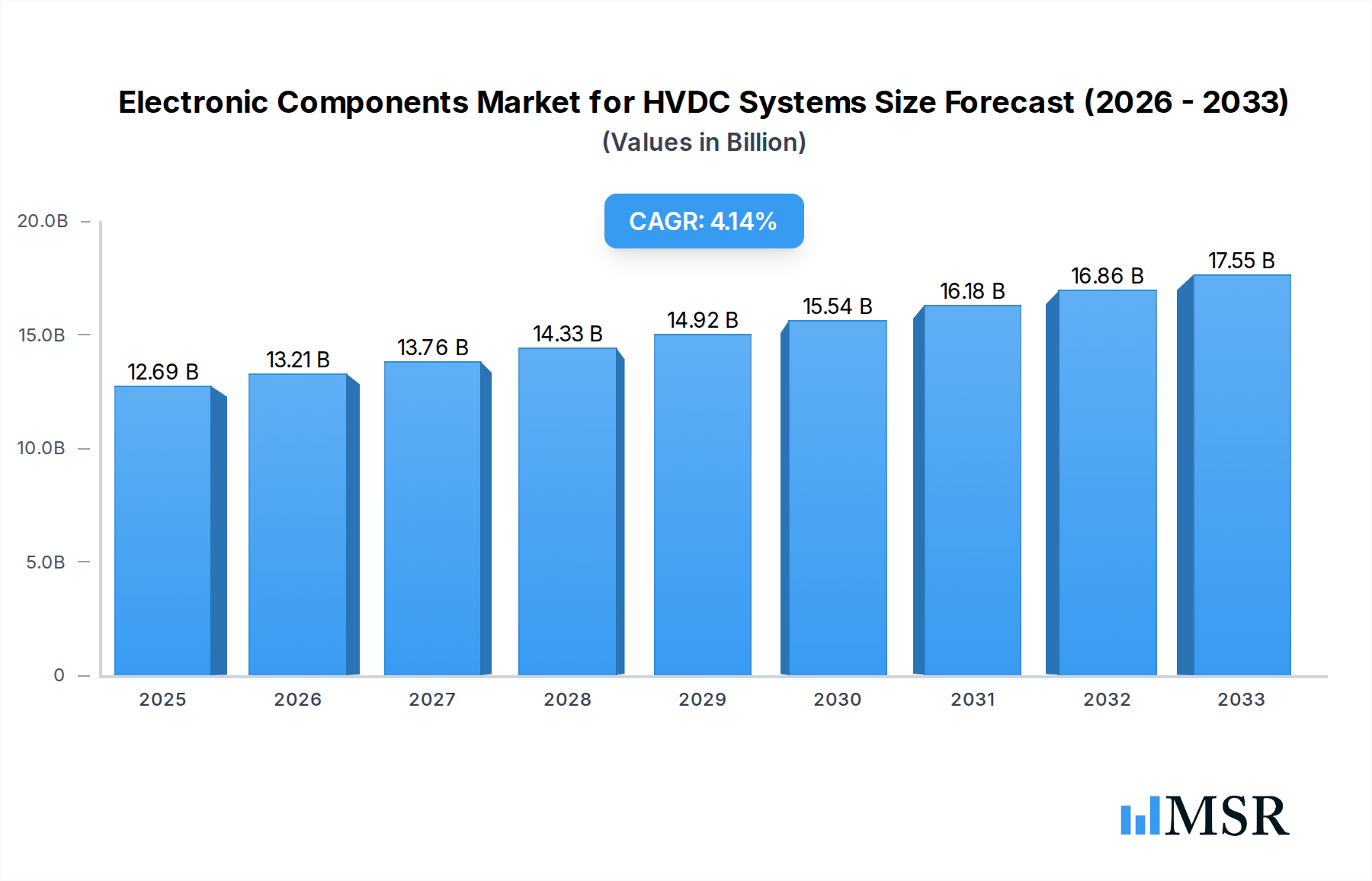

The global Electronic Components Market for HVDC Systems is poised for significant expansion, projected to reach an estimated USD 12.69 billion in 2025. This robust growth is fueled by an increasing global demand for efficient and sustainable energy transmission solutions, directly benefiting the HVDC market. The market is expected to witness a Compound Annual Growth Rate (CAGR) of 4.2% from 2019 to 2033, indicating a sustained upward trajectory. Key drivers for this expansion include the growing need for long-distance power transmission, the integration of renewable energy sources like wind and solar which often require HVDC for efficient integration into the grid, and the ongoing modernization of existing power grids worldwide. The market's segmentation into Active Components (such as IGBTs and Thyristors) and Passive Components (including Capacitors and Resistors) highlights the critical role of these individual elements in ensuring the reliability and performance of HVDC systems. Leading companies like Infineon Technologies AG, Siemens Energy, and Hitachi Energy AG are heavily investing in research and development to innovate and cater to the evolving demands of this crucial sector.

Electronic Components Market for HVDC Systems Market Size (In Billion)

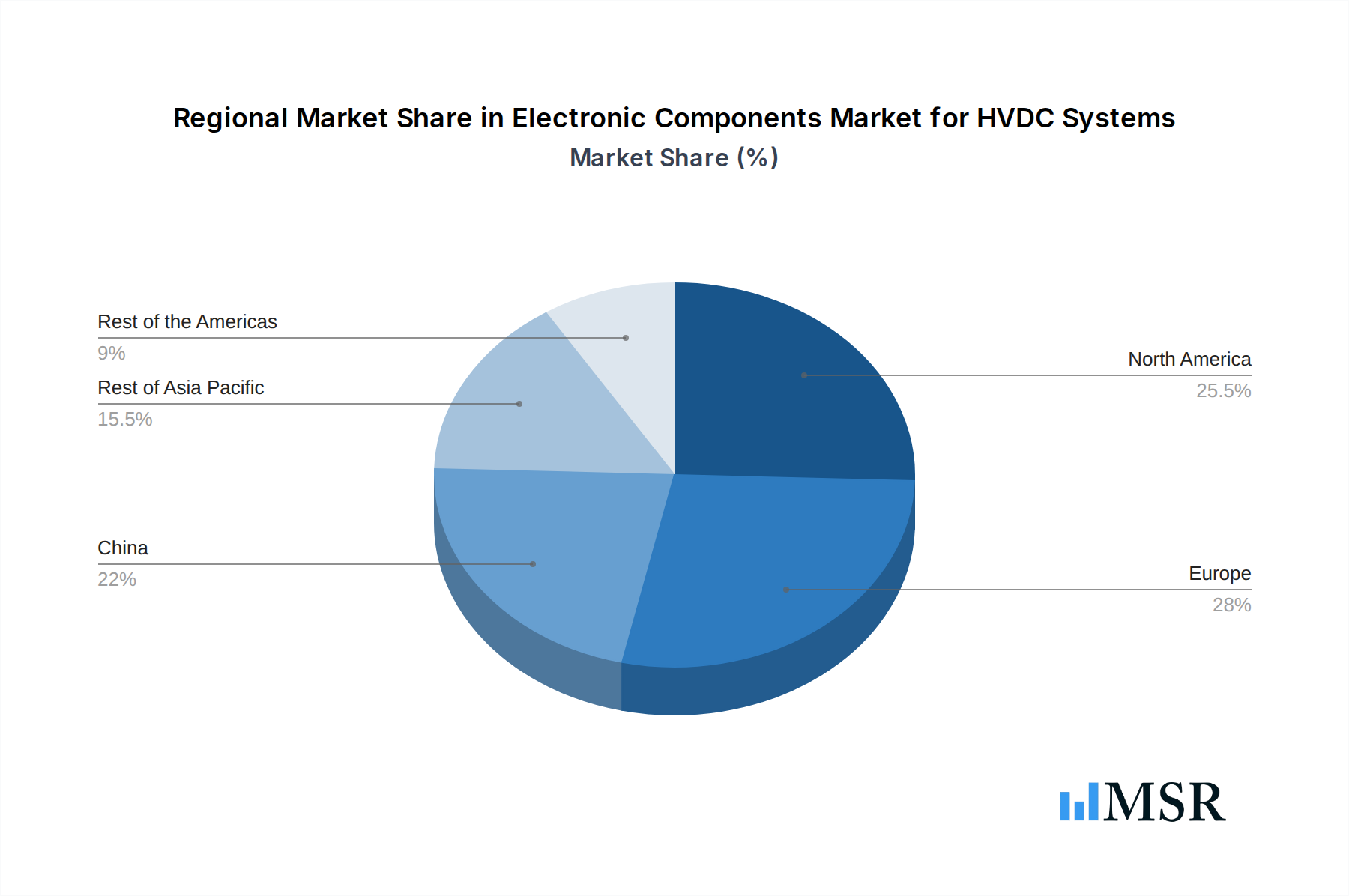

The market is characterized by a dynamic interplay of trends and restraints. A primary trend is the increasing adoption of advanced semiconductor technologies for power electronics, leading to more efficient and compact HVDC converter stations. Furthermore, the growing focus on grid stability and resilience, especially in the face of fluctuating renewable energy generation, is driving the demand for sophisticated electronic components. However, the market also faces restraints such as the high initial cost of HVDC infrastructure and the stringent regulatory requirements that can slow down project approvals. Geographically, North America and Europe are expected to remain key markets, driven by their commitment to renewable energy targets and grid upgrades. The Rest of Asia Pacific, particularly China, is also anticipated to witness substantial growth due to its rapidly expanding industrial base and increasing investments in power transmission infrastructure. Understanding these market dynamics, including the strategic focus of major players and the evolving technological landscape, is crucial for stakeholders aiming to capitalize on the opportunities within the Electronic Components Market for HVDC Systems.

Electronic Components Market for HVDC Systems Company Market Share

Here's the SEO-optimized report description for the Electronic Components Market for HVDC Systems, incorporating your specific requirements.

Unlock critical insights into the burgeoning Electronic Components Market for HVDC Systems. This comprehensive report delves into the intricate dynamics, key players, and transformative trends shaping the future of High-Voltage Direct Current (HVDC) infrastructure. With a projected market size exceeding $XX billion by 2033, driven by the accelerating global energy transition and the demand for efficient power transmission, understanding the role of advanced electronic components is paramount. Explore detailed analyses of IGBTs, Thyristors, Capacitors, and Resistors, crucial for enabling the next generation of HVDC technology.

Electronic Components Market for HVDC Systems Market Concentration & Dynamics

The Electronic Components Market for HVDC Systems exhibits a moderately concentrated landscape, with a significant presence of established global players alongside emerging innovators. The innovation ecosystem is robust, fueled by substantial R&D investments aimed at enhancing component efficiency, reliability, and power handling capabilities. Regulatory frameworks, particularly those related to grid modernization, renewable energy integration, and grid stability, play a pivotal role in shaping market entry and product development strategies. Substitute products, such as advancements in Flexible AC Transmission Systems (FACTS) and other grid enhancement technologies, pose a competitive challenge, though HVDC's inherent advantages in long-distance transmission and grid interconnectivity maintain its dominance. End-user trends, driven by the increasing adoption of renewable energy sources like offshore wind and solar farms, and the growing demand for intercontinental power exchange, are profoundly influencing component requirements. Mergers & Acquisitions (M&A) activities, while not overwhelmingly frequent, are strategically focused on acquiring niche technologies or expanding market reach, with approximately X significant M&A deals recorded within the historical period. Key market share leaders in specific component categories exert considerable influence, but the market remains dynamic due to continuous technological advancements.

Electronic Components Market for HVDC Systems Industry Insights & Trends

The Electronic Components Market for HVDC Systems is poised for significant expansion, projected to reach a market size of over $XX billion by the base year 2025, with a remarkable Compound Annual Growth Rate (CAGR) of approximately X.X% during the forecast period of 2025–2033. This robust growth is intrinsically linked to the global imperative for a more efficient and sustainable energy infrastructure. The increasing demand for renewable energy integration, the necessity for long-distance and high-capacity power transmission, and the ongoing modernization of aging power grids worldwide are primary growth drivers. Technological disruptions are at the forefront, with continuous advancements in semiconductor materials, such as Silicon Carbide (SiC) and Gallium Nitride (GaN), enabling the development of more compact, efficient, and higher-performing components like IGBTs and Thyristors. These advancements are crucial for improving the efficiency of power conversion and reducing transmission losses in HVDC systems. Evolving consumer behaviors, or rather, societal and governmental mandates for decarbonization and grid resilience, are further propelling the adoption of HVDC technology. The electrification of transportation and industries, coupled with the need to connect remote renewable energy sources to demand centers, underscores the indispensable role of HVDC. Furthermore, the increasing deployment of offshore wind farms, which require long-distance underwater transmission, presents a substantial market opportunity for specialized HVDC components. The development of smart grids and the integration of distributed energy resources necessitate advanced power electronics for effective management and control, directly benefiting the electronic components sector for HVDC applications. The focus on upgrading existing AC networks to HVDC for greater efficiency and capacity is another significant trend. The increasing complexity of power grids and the need for grid stability in the face of intermittent renewable generation further amplify the demand for sophisticated control and conversion systems, which are built upon these essential electronic components. The market is also witnessing a trend towards higher voltage and higher power ratings for components to meet the ever-growing transmission demands.

Key Markets & Segments Leading Electronic Components Market for HVDC Systems

The Active Components segment, particularly IGBTs (Insulated Gate Bipolar Transistors) and Thyristors, is currently leading the Electronic Components Market for HVDC Systems. This dominance stems from their critical role in power conversion and switching applications within HVDC converter stations.

- Dominant Drivers for Active Components:

- High Power Handling Capabilities: IGBTs and Thyristors are essential for efficiently handling the high voltages and currents characteristic of HVDC transmission.

- Switching Efficiency: These components offer superior switching speeds and lower conduction losses compared to older technologies, leading to improved overall system efficiency.

- Rapid Renewable Energy Integration: The surge in offshore wind farms and large-scale solar projects necessitates robust power conversion, driving demand for advanced IGBTs and Thyristors.

- Grid Modernization & Expansion: Upgrading existing grids and building new HVDC lines for long-distance transmission directly translates to increased demand for these active components.

- Technological Advancements: Continuous innovation in materials like SiC and GaN is leading to the development of higher-performance, more reliable, and more compact active components, further solidifying their market position.

The Passive Components segment, encompassing Capacitors and Resistors, also plays a vital role, albeit with a different demand profile. While active components are central to power conversion, passive components are indispensable for filtering, smoothing, energy storage, and surge protection within HVDC systems. Regions with significant investments in large-scale infrastructure projects, particularly in Asia-Pacific (e.g., China, India) and Europe, are the primary drivers of demand. North America is also experiencing growth due to grid modernization initiatives. The dominance of active components is fueled by the direct correlation between the expansion of HVDC transmission capacity and the need for sophisticated power converters. The technological advancements in semiconductors have enabled the creation of more powerful and efficient IGBTs and Thyristors, making them the bedrock of modern HVDC technology. The growing complexity of grid management, including the integration of variable renewable energy sources, further emphasizes the need for precise control and conversion capabilities provided by these components.

Electronic Components Market for HVDC Systems Product Developments

Product innovations in the Electronic Components Market for HVDC Systems are centered on enhancing performance, reliability, and sustainability. Manufacturers are increasingly focusing on developing components with higher power density, improved thermal management, and extended operational lifespans to meet the demanding requirements of HVDC applications. For instance, advancements in materials like Silicon Carbide (SiC) are enabling the creation of more efficient and compact IGBTs and Thyristors, reducing system losses and footprint. Similarly, the development of high-performance capacitors with enhanced surge capability and reduced Equivalent Series Resistance (ESR) is crucial for filtering and energy storage. These technological advancements not only improve the efficiency and cost-effectiveness of HVDC systems but also contribute to grid stability and the seamless integration of renewable energy sources.

Challenges in the Electronic Components Market for HVDC Systems Market

The Electronic Components Market for HVDC Systems faces several significant challenges. Supply chain disruptions, exacerbated by geopolitical factors and raw material availability, can lead to production delays and increased costs. High development and manufacturing costs associated with advanced power electronics, coupled with stringent quality control requirements for high-voltage applications, present a barrier to entry for smaller players. Stringent regulatory approvals and long qualification cycles for components used in critical infrastructure can slow down the adoption of new technologies. Furthermore, intense competition and price pressures from established players necessitate continuous innovation and cost optimization. Skilled workforce shortages in specialized areas of power electronics also pose a challenge to market expansion.

Forces Driving Electronic Components Market for HVDC Systems Growth

The primary forces driving the Electronic Components Market for HVDC Systems are the global surge in demand for renewable energy, necessitating efficient long-distance transmission solutions. The ongoing modernization and expansion of electrical grids worldwide, including the development of supergrids and intercontinental connections, are significant catalysts. Furthermore, the increasing demand for energy security and grid stability, particularly in the face of climate change and growing energy consumption, fuels the adoption of HVDC technology. Government initiatives and policies promoting clean energy and infrastructure development also play a crucial role. The inherent efficiency and capacity advantages of HVDC over traditional AC transmission for long distances make it a preferred choice for large-scale power projects.

Challenges in the Electronic Components Market for HVDC Systems Market

Long-term growth catalysts for the Electronic Components Market for HVDC Systems are deeply rooted in the sustained global push towards decarbonization and the electrification of various sectors. Innovations in material science, leading to even more efficient and robust semiconductor materials like advanced SiC and GaN, will unlock new performance benchmarks for components. The increasing complexity of grid management, driven by the proliferation of distributed energy resources and smart grid technologies, will necessitate highly sophisticated and reliable electronic components for seamless integration and control. Furthermore, the growing need for grid interconnections between countries and continents for energy trading and resilience will continue to drive the demand for high-capacity HVDC systems.

Emerging Opportunities in Electronic Components Market for HVDC Systems

Emerging opportunities within the Electronic Components Market for HVDC Systems are vast and varied. The rapid expansion of offshore wind farms, requiring extensive subsea HVDC cables, presents a substantial growth avenue for specialized components. The integration of HVDC technology into urban power distribution networks for enhanced reliability and efficiency is another promising area. The development of floating offshore wind platforms and their associated HVDC transmission infrastructure will open new markets. Furthermore, the increasing adoption of electric vehicles and the need for robust charging infrastructure could indirectly benefit the HVDC market by driving overall grid capacity enhancements. The potential for integrating HVDC with energy storage solutions to further stabilize grids is also a significant emerging trend.

Leading Players in the Electronic Components Market for HVDC Systems Sector

- Vishay Intertechnology Inc.

- Infineon Technologies AG

- Microchip Technology Inc.

- Hitachi Energy AG (Hitachi Ltd)

- Fuji Electric Co., Ltd.

- Toshiba Corporation

- Mitsubishi Electric Corporation

- Broadcom Inc.

- STMicroelectronics NV

- Renesas Electronics Corporation

- Texas Instruments Incorporated

- TDK Corporation

- Siemens Energy

- Eaton Corporation

Key Milestones in Electronic Components Market for HVDC Systems Industry

- February 2023: Hitachi Energy India Ltd expanded its regional facility by launching a new assembly and testing factory near Chennai, India. This facility will manufacture advanced power electronics for HVDC Light, HVDC Classic, and STATCOM, along with the MACH control and protection system, enhancing production capacity and accelerating the energy transition.

- December 2022: Vishay Intertechnology Inc. announced the release of a new series of screw terminal aluminum electrolytic capacitors (202 PML-ST), ideal for pulsed power filtering, buffering, and energy storage applications requiring extended lifetimes of 10 to 15 years.

Strategic Outlook for Electronic Components Market for HVDC Systems Market

The strategic outlook for the Electronic Components Market for HVDC Systems is overwhelmingly positive, driven by the indispensable role of HVDC technology in achieving global decarbonization goals and modernizing energy infrastructure. Growth accelerators include continued advancements in semiconductor technology, leading to more efficient and cost-effective components. Strategic partnerships between component manufacturers and HVDC system integrators will be crucial for co-developing solutions tailored to evolving grid demands. The increasing focus on grid resilience and the integration of diverse renewable energy sources will solidify HVDC's position, creating sustained demand for its enabling electronic components. Furthermore, the expansion of HVDC interconnections across continents will unlock new market potential and drive further innovation in the sector.

Electronic Components Market for HVDC Systems Segmentation

-

1. Type

-

1.1. Active Components

- 1.1.1. IGBT

- 1.1.2. Thyristor

-

1.2. Passive Components

- 1.2.1. Capacitors

- 1.2.2. Resistors

-

1.1. Active Components

Electronic Components Market for HVDC Systems Segmentation By Geography

- 1. North America

- 2. Rest of the Americas

- 3. Europe

- 4. China

- 5. Rest of Asia Pacific

Electronic Components Market for HVDC Systems Regional Market Share

Geographic Coverage of Electronic Components Market for HVDC Systems

Electronic Components Market for HVDC Systems REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Active Components

- 5.1.1.1. IGBT

- 5.1.1.2. Thyristor

- 5.1.2. Passive Components

- 5.1.2.1. Capacitors

- 5.1.2.2. Resistors

- 5.1.1. Active Components

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Rest of the Americas

- 5.2.3. Europe

- 5.2.4. China

- 5.2.5. Rest of Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Electronic Components Market for HVDC Systems Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Active Components

- 6.1.1.1. IGBT

- 6.1.1.2. Thyristor

- 6.1.2. Passive Components

- 6.1.2.1. Capacitors

- 6.1.2.2. Resistors

- 6.1.1. Active Components

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Electronic Components Market for HVDC Systems Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Active Components

- 7.1.1.1. IGBT

- 7.1.1.2. Thyristor

- 7.1.2. Passive Components

- 7.1.2.1. Capacitors

- 7.1.2.2. Resistors

- 7.1.1. Active Components

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Rest of the Americas Electronic Components Market for HVDC Systems Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Active Components

- 8.1.1.1. IGBT

- 8.1.1.2. Thyristor

- 8.1.2. Passive Components

- 8.1.2.1. Capacitors

- 8.1.2.2. Resistors

- 8.1.1. Active Components

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Europe Electronic Components Market for HVDC Systems Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Active Components

- 9.1.1.1. IGBT

- 9.1.1.2. Thyristor

- 9.1.2. Passive Components

- 9.1.2.1. Capacitors

- 9.1.2.2. Resistors

- 9.1.1. Active Components

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. China Electronic Components Market for HVDC Systems Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Active Components

- 10.1.1.1. IGBT

- 10.1.1.2. Thyristor

- 10.1.2. Passive Components

- 10.1.2.1. Capacitors

- 10.1.2.2. Resistors

- 10.1.1. Active Components

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Rest of Asia Pacific Electronic Components Market for HVDC Systems Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Active Components

- 11.1.1.1. IGBT

- 11.1.1.2. Thyristor

- 11.1.2. Passive Components

- 11.1.2.1. Capacitors

- 11.1.2.2. Resistors

- 11.1.1. Active Components

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Vishay Intertechnology Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Infineon Technologies AG

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Microchip Technology Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Hitachi Energy AG (Hitachi Ltd)

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Fuji Electri

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Toshiba Corporation

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Mitsubishi Electric Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Broadcom Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 STMicroelectronics NV

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Renesas Electronics Corporation

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Texas Instruments Incorporated

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 TDK Corporation

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Siemens Energy

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Eaton Corporation

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 Vishay Intertechnology Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Electronic Components Market for HVDC Systems Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Electronic Components Market for HVDC Systems Revenue (billion), by Type 2025 & 2033

- Figure 3: North America Electronic Components Market for HVDC Systems Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Electronic Components Market for HVDC Systems Revenue (billion), by Country 2025 & 2033

- Figure 5: North America Electronic Components Market for HVDC Systems Revenue Share (%), by Country 2025 & 2033

- Figure 6: Rest of the Americas Electronic Components Market for HVDC Systems Revenue (billion), by Type 2025 & 2033

- Figure 7: Rest of the Americas Electronic Components Market for HVDC Systems Revenue Share (%), by Type 2025 & 2033

- Figure 8: Rest of the Americas Electronic Components Market for HVDC Systems Revenue (billion), by Country 2025 & 2033

- Figure 9: Rest of the Americas Electronic Components Market for HVDC Systems Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Electronic Components Market for HVDC Systems Revenue (billion), by Type 2025 & 2033

- Figure 11: Europe Electronic Components Market for HVDC Systems Revenue Share (%), by Type 2025 & 2033

- Figure 12: Europe Electronic Components Market for HVDC Systems Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Electronic Components Market for HVDC Systems Revenue Share (%), by Country 2025 & 2033

- Figure 14: China Electronic Components Market for HVDC Systems Revenue (billion), by Type 2025 & 2033

- Figure 15: China Electronic Components Market for HVDC Systems Revenue Share (%), by Type 2025 & 2033

- Figure 16: China Electronic Components Market for HVDC Systems Revenue (billion), by Country 2025 & 2033

- Figure 17: China Electronic Components Market for HVDC Systems Revenue Share (%), by Country 2025 & 2033

- Figure 18: Rest of Asia Pacific Electronic Components Market for HVDC Systems Revenue (billion), by Type 2025 & 2033

- Figure 19: Rest of Asia Pacific Electronic Components Market for HVDC Systems Revenue Share (%), by Type 2025 & 2033

- Figure 20: Rest of Asia Pacific Electronic Components Market for HVDC Systems Revenue (billion), by Country 2025 & 2033

- Figure 21: Rest of Asia Pacific Electronic Components Market for HVDC Systems Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Electronic Components Market for HVDC Systems Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Electronic Components Market for HVDC Systems Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Global Electronic Components Market for HVDC Systems Revenue billion Forecast, by Type 2020 & 2033

- Table 4: Global Electronic Components Market for HVDC Systems Revenue billion Forecast, by Country 2020 & 2033

- Table 5: Global Electronic Components Market for HVDC Systems Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Electronic Components Market for HVDC Systems Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Electronic Components Market for HVDC Systems Revenue billion Forecast, by Type 2020 & 2033

- Table 8: Global Electronic Components Market for HVDC Systems Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Global Electronic Components Market for HVDC Systems Revenue billion Forecast, by Type 2020 & 2033

- Table 10: Global Electronic Components Market for HVDC Systems Revenue billion Forecast, by Country 2020 & 2033

- Table 11: Global Electronic Components Market for HVDC Systems Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Electronic Components Market for HVDC Systems Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Electronic Components Market for HVDC Systems?

The projected CAGR is approximately 4.2%.

2. Which companies are prominent players in the Electronic Components Market for HVDC Systems?

Key companies in the market include Vishay Intertechnology Inc, Infineon Technologies AG, Microchip Technology Inc, Hitachi Energy AG (Hitachi Ltd), Fuji Electri, Toshiba Corporation, Mitsubishi Electric Corporation, Broadcom Inc, STMicroelectronics NV, Renesas Electronics Corporation, Texas Instruments Incorporated, TDK Corporation, Siemens Energy, Eaton Corporation.

3. What are the main segments of the Electronic Components Market for HVDC Systems?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.69 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Adoption of Renewable Energy; Increasing Investments in Submarine Power Transmission.

6. What are the notable trends driving market growth?

Capacitors to be the Fastest Growing Passive Component.

7. Are there any restraints impacting market growth?

Rising Metal Prices Impacting Component Production Costs.

8. Can you provide examples of recent developments in the market?

February 2023 - Hitachi Energy India Ltd (formerly ABB Power Products and Systems India) expanded its regional facility by launching a new assembly and testing factory near Chennai, India. The new factory would manufacture advanced power electronics for HVDC Light, HVDC Classic, and STATCOM, together with a MACH control and protection system. It would deliver cutting-edge solutions to accelerate the energy transition, enabling Hitachi Energy to increase its production capacity.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Electronic Components Market for HVDC Systems," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Electronic Components Market for HVDC Systems report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Electronic Components Market for HVDC Systems?

To stay informed about further developments, trends, and reports in the Electronic Components Market for HVDC Systems, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence