Key Insights

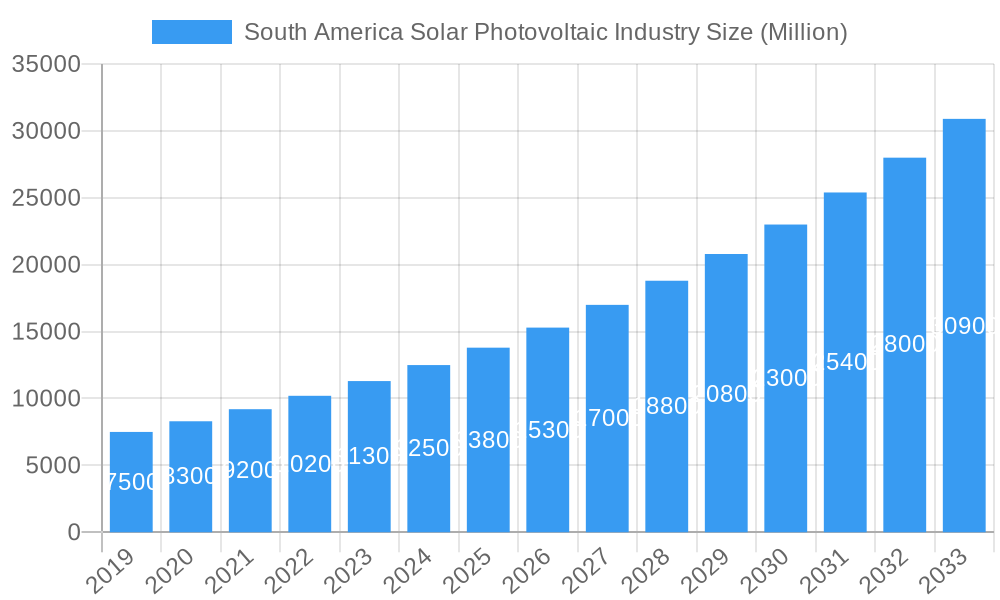

The South America Solar Photovoltaic (PV) Industry is projected for substantial growth, with an estimated market size of $6.6 billion by 2024, driven by a strong Compound Annual Growth Rate (CAGR) of 11.2%. This expansion is fueled by the region's commitment to renewable energy, supported by favorable government policies, decreasing solar technology costs, and heightened climate change awareness. Key growth factors include national energy transition initiatives, significant investments in large-scale solar farms, and increasing demand for sustainable energy solutions from commercial, industrial, and residential consumers. The region's abundant solar resources further bolster this upward trend. Emerging trends such as the integration of solar with energy storage, the growth of distributed solar generation, and innovative financing models are expected to accelerate market adoption.

South America Solar Photovoltaic Industry Market Size (In Billion)

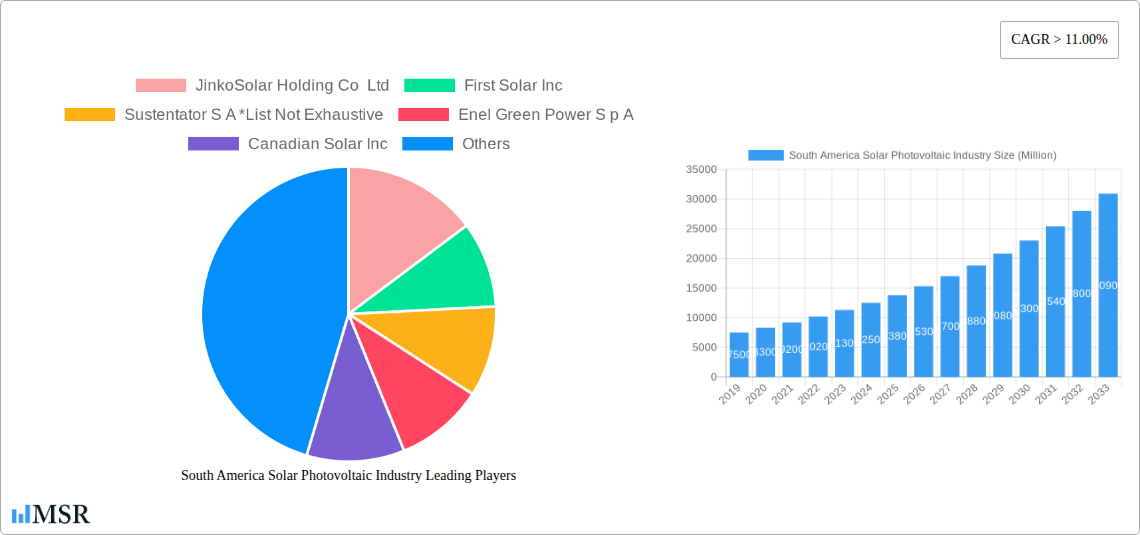

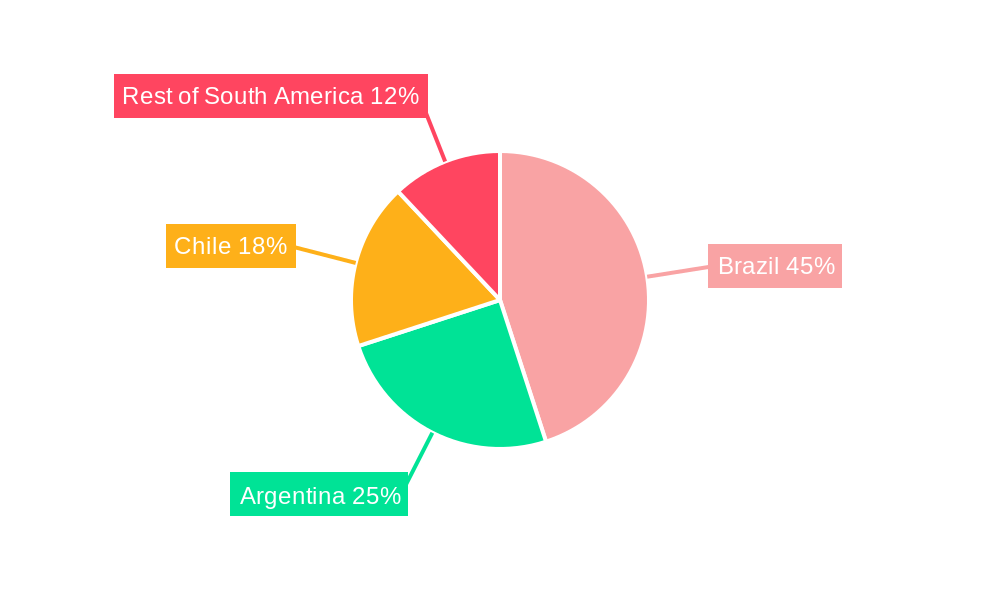

While the sector presents considerable opportunities, potential challenges include supply chain volatility, the need for robust grid infrastructure upgrades to manage intermittent solar power, and the demand for skilled labor. Nevertheless, strategic investments and policy reforms are actively addressing these obstacles. The market is segmented by deployment type into ground-mounted and rooftop systems, with commercial and industrial sectors anticipated to lead adoption, followed by the residential segment. Brazil is the dominant market, with Argentina and Chile also showing significant growth. The "Rest of South America" is expected to gain momentum as awareness and investment increase. Leading companies, including JinkoSolar Holding Co. Ltd, First Solar Inc., and Canadian Solar Inc., are actively investing in manufacturing, project development, and technological innovation to capitalize on this dynamic market.

South America Solar Photovoltaic Industry Company Market Share

Gain comprehensive insights into South America's rapidly expanding solar PV market. This detailed report covers market dynamics, growth drivers, key segments, product innovations, and strategic opportunities within this vital renewable energy sector. Essential for industry leaders, investors, policymakers, and stakeholders, this analysis provides actionable intelligence for navigating and profiting from the South American solar PV landscape. The report spans the period from 2019 to 2033, with a base year of 2024 and a forecast period of 2024-2033, offering unparalleled market foresight.

South America Solar Photovoltaic Industry Market Concentration & Dynamics

The South America Solar Photovoltaic Industry is experiencing a dynamic shift, characterized by increasing market concentration driven by large-scale project development and consolidation. Innovation ecosystems are flourishing, fueled by advancements in solar panel efficiency and energy storage solutions. Regulatory frameworks across key geographies like Brazil and Argentina are becoming more supportive, incentivizing investment in utility-scale solar farms and distributed solar generation. Substitute products, such as fossil fuels, are facing increasing competition from the declining costs of solar PV technology. End-user trends reveal a growing demand for renewable energy solutions in both residential solar and commercial and industrial (C&I) solar segments, driven by cost savings and sustainability goals. Mergers and acquisitions (M&A) activities are on the rise, with major players acquiring smaller developers and integratting their operations to capture greater market share. For instance, recent M&A activities have seen a notable increase in deal counts, indicating a strong appetite for expansion and consolidation. Market share is increasingly dominated by a few key players, though the "Rest of South America" region presents opportunities for emerging companies.

South America Solar Photovoltaic Industry Industry Insights & Trends

The South America Solar Photovoltaic Industry is poised for substantial growth, projected to reach an estimated market size of $XX Billion in 2025, with a robust Compound Annual Growth Rate (CAGR) of XX% anticipated during the forecast period (2025-2033). This surge is primarily propelled by a confluence of economic, technological, and environmental factors. Favorable government policies, including tax incentives, feed-in tariffs, and renewable energy targets, are actively stimulating investment in solar power projects. The declining cost of photovoltaic modules and inverters, coupled with advancements in solar technology, have made solar energy increasingly competitive with traditional energy sources. Furthermore, a growing global and regional emphasis on decarbonization and combating climate change is driving the adoption of clean energy, with solar PV at the forefront. Technological disruptions, such as the integration of artificial intelligence (AI) in solar farm management and the development of more efficient bifacial solar panels, are further enhancing the performance and appeal of solar solutions. Evolving consumer behaviors, including a heightened awareness of environmental issues and a desire for energy independence, are fueling the demand for rooftop solar installations in the residential solar segment. The commercial and industrial (C&I) solar segment is also experiencing significant traction as businesses seek to reduce operational costs and enhance their corporate social responsibility profiles through on-site solar power generation. The expansion of energy storage systems alongside solar PV is also a critical trend, addressing the intermittency of solar power and increasing grid reliability. The historical period (2019-2024) has laid a strong foundation for this projected growth, witnessing consistent increases in installed capacity and market penetration.

Key Markets & Segments Leading South America Solar Photovoltaic Industry

The South America Solar Photovoltaic Industry's dominance is undeniably centered in Brazil, which consistently leads the market in installed solar capacity and investment. Its vast land area, abundant solar irradiance, and supportive regulatory environment make it a prime destination for utility-scale solar farms.

Brazil:

- Drivers: Strong government support through auctions and tax incentives, a large and growing energy demand, and significant advancements in grid infrastructure to accommodate renewable energy.

- Dominance Analysis: Brazil's sheer scale of energy consumption and its proactive approach to renewable energy deployment have positioned it as the undisputed leader. The country's commitment to diversifying its energy matrix, moving away from hydro dependence, has significantly accelerated the adoption of solar photovoltaic technology.

Argentina:

- Drivers: A growing portfolio of renewable energy projects, including substantial solar power plant development, and a rising interest in distributed generation.

- Dominance Analysis: Argentina is rapidly emerging as a key player, driven by its "Renewable Distributed Generation Law" and ambitious targets for renewable energy integration. The country is actively attracting foreign investment for large-scale photovoltaic projects.

Chile:

- Drivers: Exceptional solar irradiance in the Atacama Desert, a well-established regulatory framework for renewables, and significant interest in behind-the-meter solar solutions.

- Dominance Analysis: Chile has been a pioneer in Latin America for solar energy development, particularly for concentrated solar power (CSP) and large-scale PV installations. Its focus on exportable renewable energy potential also plays a crucial role.

Rest of South America:

- Drivers: Emerging markets like Colombia, Peru, and Uruguay are showing increasing interest and commitment to solar PV adoption, driven by energy security concerns and environmental mandates.

- Dominance Analysis: While not yet matching the scale of the leading nations, these regions represent significant future growth potential, with nascent policy development and pilot projects paving the way for wider adoption of solar solutions.

Within the deployment segments, Ground Mounted solar installations continue to dominate due to their suitability for large-scale solar power generation projects. However, the Rooftop segment, encompassing both Residential Solar and Commercial and Industrial (C&I) Solar, is experiencing rapid growth, fueled by declining costs and increasing interest in energy independence and cost savings. The Commercial and Industrial (C&I) Solar segment, in particular, is a key driver for market expansion as businesses invest in on-site solar power to reduce operational expenditures and meet sustainability targets.

South America Solar Photovoltaic Industry Product Developments

Product developments in the South America Solar Photovoltaic Industry are characterized by a relentless pursuit of efficiency and cost-effectiveness. Innovations in solar panel technology, such as the widespread adoption of PERC (Passivated Emitter and Rear Cell) and TOPCon (Tunnel Oxide Passivated Contact) solar cells, are leading to higher energy yields per square meter. The integration of bifacial solar panels is gaining traction, allowing for greater energy capture from both the front and rear surfaces, particularly beneficial in ground-mounted installations. Furthermore, advancements in solar inverter technology, including smart inverters with enhanced grid-support functions and improved energy management capabilities, are crucial for optimizing performance and grid integration. The development of more robust and efficient energy storage systems, including advanced battery technologies, is also a significant product innovation, addressing the intermittency of solar power and enhancing grid stability. These technological advancements are directly contributing to the growing market relevance and competitive edge of solar PV solutions across the region.

Challenges in the South America Solar Photovoltaic Industry Market

The South America Solar Photovoltaic Industry, while experiencing robust growth, faces several challenges. Regulatory hurdles and inconsistencies across different countries can create uncertainty for investors and developers. Grid integration limitations in some areas can hinder the efficient deployment of large-scale solar projects. Supply chain disruptions, particularly for key components like solar modules and inverters, can lead to project delays and cost overruns. Furthermore, intense competitive pressures from both established global players and emerging local companies can impact profit margins. Financing challenges, especially for smaller-scale projects and in regions with less developed financial markets, also present a barrier. The estimated impact of these challenges can lead to project delays of up to 15% and cost increases of 5-10% for some developments.

Forces Driving South America Solar Photovoltaic Industry Growth

Several key forces are propelling the South America Solar Photovoltaic Industry forward. Technological advancements, leading to higher efficiency and lower costs of solar PV equipment, are making solar energy increasingly competitive. Economic drivers, such as the demand for affordable and reliable energy, are fueling investment in renewable sources. Government initiatives and supportive policies, including renewable energy targets and financial incentives, are creating a favorable investment climate. The growing global and regional emphasis on sustainability and decarbonization is a significant ethical and environmental driver, pushing for the adoption of cleaner energy solutions. For example, Brazil's commitment to reducing its carbon footprint through renewable energy expansion is a prime illustration of this driver.

Challenges in the South America Solar Photovoltaic Industry Market

While rapid growth is anticipated, the South America Solar Photovoltaic Industry must navigate several long-term growth catalysts and potential hindrances. The continuous improvement in solar panel efficiency and the development of next-generation photovoltaic technologies will remain crucial for maintaining cost-competitiveness. Strategic partnerships and collaborations between technology providers, developers, and financial institutions are essential for scaling up projects and accessing capital. Market expansions into less developed but high-potential countries within the region will unlock new revenue streams. However, ongoing challenges related to grid modernization, skilled workforce development, and land acquisition complexities need to be proactively addressed to ensure sustained and widespread growth.

Emerging Opportunities in South America Solar Photovoltaic Industry

The South America Solar Photovoltaic Industry is ripe with emerging opportunities. The expansion of off-grid solar solutions in remote areas offers significant potential for energy access and development. The integration of solar PV with other renewable energy sources, such as wind power, can create more stable and reliable energy systems. The increasing demand for green hydrogen production powered by solar energy presents a novel and substantial opportunity for the sector. Furthermore, the growing interest in corporate power purchase agreements (PPAs) for solar energy by large corporations seeking to meet their sustainability goals is a rapidly expanding market segment. The development of smart grids and energy management systems will also create new avenues for innovation and service provision.

Leading Players in the South America Solar Photovoltaic Industry Sector

- JinkoSolar Holding Co Ltd

- First Solar Inc

- Sustentator S A

- Enel Green Power S p A

- Canadian Solar Inc

- Atlas Renewable Energy

- JA Solar Holdings Co Ltd

- Acciona SA

- Sonnedix Power Holdings Ltd

- Trina Solar Limited

Key Milestones in South America Solar Photovoltaic Industry Industry

- 2019: Launch of significant government-backed renewable energy auctions in Brazil, driving large-scale solar project development.

- 2020: Argentina implements its "Renewable Distributed Generation Law," spurring growth in rooftop solar.

- 2021: Chile achieves significant milestones in solar energy penetration, with renewables forming a substantial portion of its energy mix.

- 2022: Increased investment in utility-scale solar farms across Brazil and Argentina, with several multi-hundred-megawatt projects coming online.

- 2023: Growing interest in energy storage solutions for solar PV projects to enhance grid stability and reliability.

- 2024 (Estimated): Continued expansion of C&I solar installations driven by cost savings and corporate sustainability targets.

Strategic Outlook for South America Solar Photovoltaic Industry Market

The strategic outlook for the South America Solar Photovoltaic Industry remains exceptionally positive, with continued strong growth anticipated. Key accelerators for future market potential include the ongoing decline in solar PV module costs, advancements in energy storage technologies, and increasingly robust supportive government policies across the region. Opportunities lie in expanding market reach into emerging economies, fostering innovation in integrated renewable energy systems, and capitalizing on the growing demand for sustainable energy solutions. Strategic initiatives focused on grid modernization, simplifying regulatory processes, and promoting local manufacturing of solar components will be crucial for sustained success and unlocking the full potential of this dynamic market.

South America Solar Photovoltaic Industry Segmentation

-

1. Deployment

- 1.1. Ground Mounted

- 1.2. Rooftop

-

2. End-User

- 2.1. Residential

- 2.2. Commercial and Industrial

-

3. Geography

- 3.1. Brazil

- 3.2. Argentina

- 3.3. Chile

- 3.4. Rest of South America

South America Solar Photovoltaic Industry Segmentation By Geography

- 1. Brazil

- 2. Argentina

- 3. Chile

- 4. Rest of South America

South America Solar Photovoltaic Industry Regional Market Share

Geographic Coverage of South America Solar Photovoltaic Industry

South America Solar Photovoltaic Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 5.1.1. Ground Mounted

- 5.1.2. Rooftop

- 5.2. Market Analysis, Insights and Forecast - by End-User

- 5.2.1. Residential

- 5.2.2. Commercial and Industrial

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. Brazil

- 5.3.2. Argentina

- 5.3.3. Chile

- 5.3.4. Rest of South America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Brazil

- 5.4.2. Argentina

- 5.4.3. Chile

- 5.4.4. Rest of South America

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 6. South America Solar Photovoltaic Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 6.1.1. Ground Mounted

- 6.1.2. Rooftop

- 6.2. Market Analysis, Insights and Forecast - by End-User

- 6.2.1. Residential

- 6.2.2. Commercial and Industrial

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. Brazil

- 6.3.2. Argentina

- 6.3.3. Chile

- 6.3.4. Rest of South America

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 7. Brazil South America Solar Photovoltaic Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Deployment

- 7.1.1. Ground Mounted

- 7.1.2. Rooftop

- 7.2. Market Analysis, Insights and Forecast - by End-User

- 7.2.1. Residential

- 7.2.2. Commercial and Industrial

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. Brazil

- 7.3.2. Argentina

- 7.3.3. Chile

- 7.3.4. Rest of South America

- 7.1. Market Analysis, Insights and Forecast - by Deployment

- 8. Argentina South America Solar Photovoltaic Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Deployment

- 8.1.1. Ground Mounted

- 8.1.2. Rooftop

- 8.2. Market Analysis, Insights and Forecast - by End-User

- 8.2.1. Residential

- 8.2.2. Commercial and Industrial

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. Brazil

- 8.3.2. Argentina

- 8.3.3. Chile

- 8.3.4. Rest of South America

- 8.1. Market Analysis, Insights and Forecast - by Deployment

- 9. Chile South America Solar Photovoltaic Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Deployment

- 9.1.1. Ground Mounted

- 9.1.2. Rooftop

- 9.2. Market Analysis, Insights and Forecast - by End-User

- 9.2.1. Residential

- 9.2.2. Commercial and Industrial

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. Brazil

- 9.3.2. Argentina

- 9.3.3. Chile

- 9.3.4. Rest of South America

- 9.1. Market Analysis, Insights and Forecast - by Deployment

- 10. Rest of South America South America Solar Photovoltaic Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Deployment

- 10.1.1. Ground Mounted

- 10.1.2. Rooftop

- 10.2. Market Analysis, Insights and Forecast - by End-User

- 10.2.1. Residential

- 10.2.2. Commercial and Industrial

- 10.3. Market Analysis, Insights and Forecast - by Geography

- 10.3.1. Brazil

- 10.3.2. Argentina

- 10.3.3. Chile

- 10.3.4. Rest of South America

- 10.1. Market Analysis, Insights and Forecast - by Deployment

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 JinkoSolar Holding Co Ltd

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 First Solar Inc

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Sustentator S A *List Not Exhaustive

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Enel Green Power S p A

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Canadian Solar Inc

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Atlas Renewable Energy

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 JA Solar Holdings Co Ltd

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Acciona SA

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Sonnedix Power Holdings Ltd

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Trina Solar Limited

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.1 JinkoSolar Holding Co Ltd

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: South America Solar Photovoltaic Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: South America Solar Photovoltaic Industry Share (%) by Company 2025

List of Tables

- Table 1: South America Solar Photovoltaic Industry Revenue billion Forecast, by Deployment 2020 & 2033

- Table 2: South America Solar Photovoltaic Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 3: South America Solar Photovoltaic Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 4: South America Solar Photovoltaic Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: South America Solar Photovoltaic Industry Revenue billion Forecast, by Deployment 2020 & 2033

- Table 6: South America Solar Photovoltaic Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 7: South America Solar Photovoltaic Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 8: South America Solar Photovoltaic Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: South America Solar Photovoltaic Industry Revenue billion Forecast, by Deployment 2020 & 2033

- Table 10: South America Solar Photovoltaic Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 11: South America Solar Photovoltaic Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 12: South America Solar Photovoltaic Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: South America Solar Photovoltaic Industry Revenue billion Forecast, by Deployment 2020 & 2033

- Table 14: South America Solar Photovoltaic Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 15: South America Solar Photovoltaic Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 16: South America Solar Photovoltaic Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 17: South America Solar Photovoltaic Industry Revenue billion Forecast, by Deployment 2020 & 2033

- Table 18: South America Solar Photovoltaic Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 19: South America Solar Photovoltaic Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 20: South America Solar Photovoltaic Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South America Solar Photovoltaic Industry?

The projected CAGR is approximately 11.2%.

2. Which companies are prominent players in the South America Solar Photovoltaic Industry?

Key companies in the market include JinkoSolar Holding Co Ltd, First Solar Inc, Sustentator S A *List Not Exhaustive, Enel Green Power S p A, Canadian Solar Inc, Atlas Renewable Energy, JA Solar Holdings Co Ltd, Acciona SA, Sonnedix Power Holdings Ltd, Trina Solar Limited.

3. What are the main segments of the South America Solar Photovoltaic Industry?

The market segments include Deployment, End-User, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.6 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Integration of Renewable Energy4.; Supportive Government Policies.

6. What are the notable trends driving market growth?

Ground Mounted Solar PV to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; High infrastructure costs.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South America Solar Photovoltaic Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South America Solar Photovoltaic Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South America Solar Photovoltaic Industry?

To stay informed about further developments, trends, and reports in the South America Solar Photovoltaic Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence