Key Insights

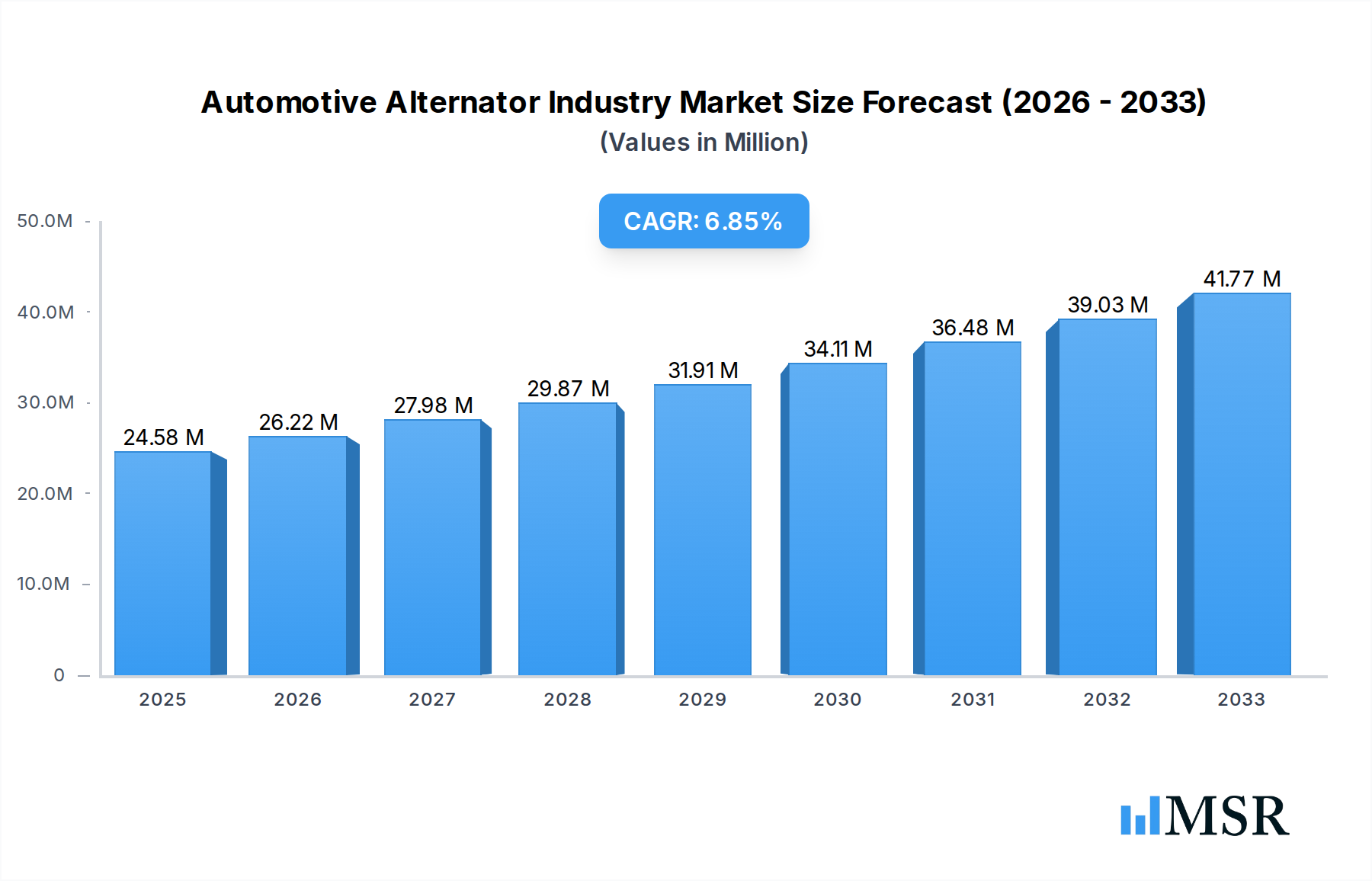

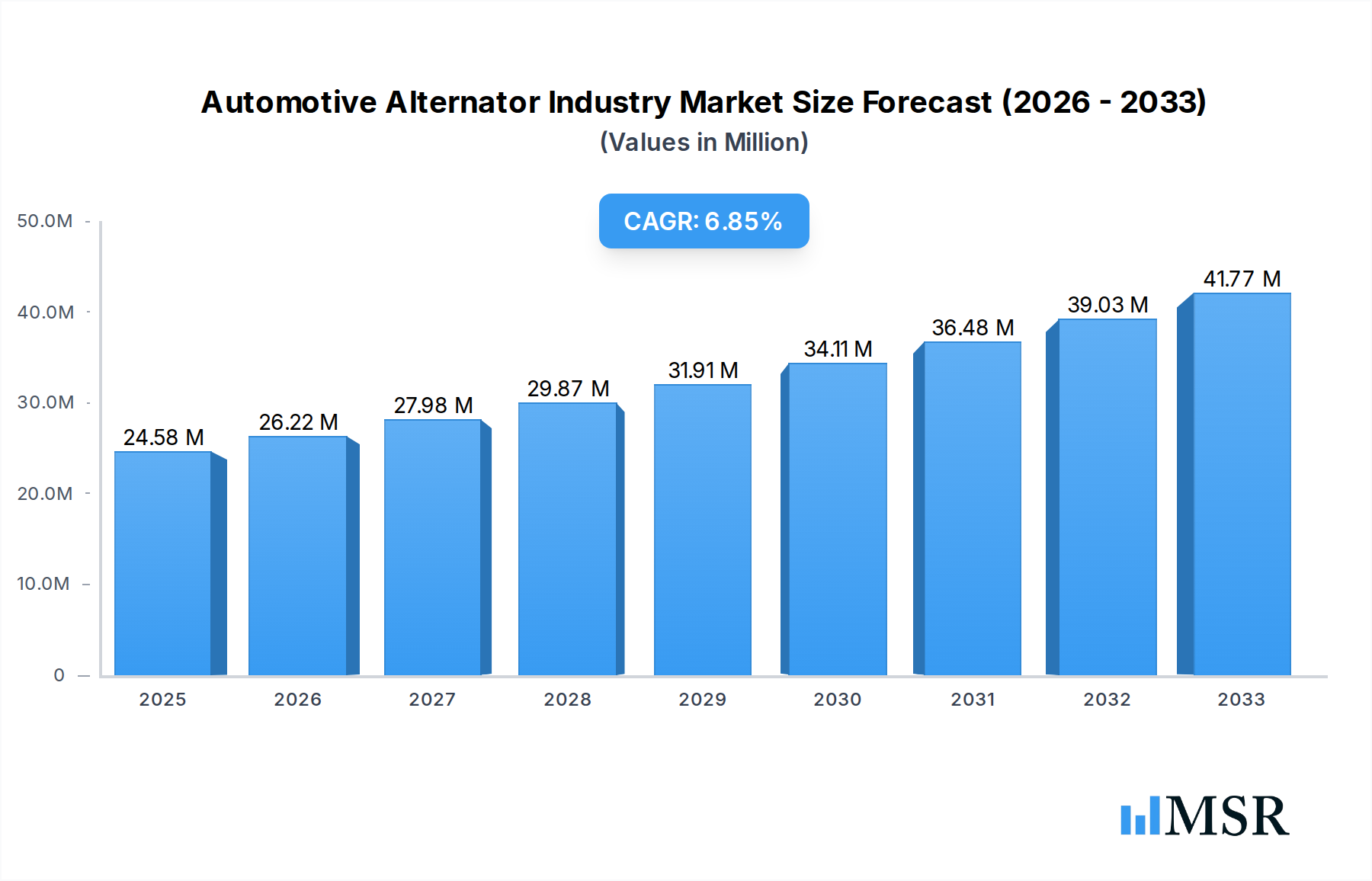

The global Automotive Alternator Industry is poised for robust expansion, projected to reach a significant market size of 24.58 million by 2025. This growth is underpinned by a compound annual growth rate (CAGR) of 6.70% throughout the forecast period (2025-2033). A primary driver for this upward trajectory is the increasing global vehicle parc, coupled with a sustained demand for new vehicle sales, especially in emerging economies. The ongoing shift in automotive technology, while leaning towards electrification, still necessitates robust alternator systems for internal combustion engine (ICE) vehicles and, critically, for hybrid powertrains which are seeing substantial adoption. These hybrid systems rely on alternators for battery charging and power management, thus ensuring continued relevance. Furthermore, advancements in alternator technology, focusing on improved efficiency, reduced weight, and enhanced durability, are contributing to market growth as manufacturers seek to optimize fuel economy and reduce emissions. The expanding automotive aftermarket, driven by the need for replacement parts and upgrades, also represents a significant contributing factor to the industry's healthy growth.

Automotive Alternator Industry Market Size (In Million)

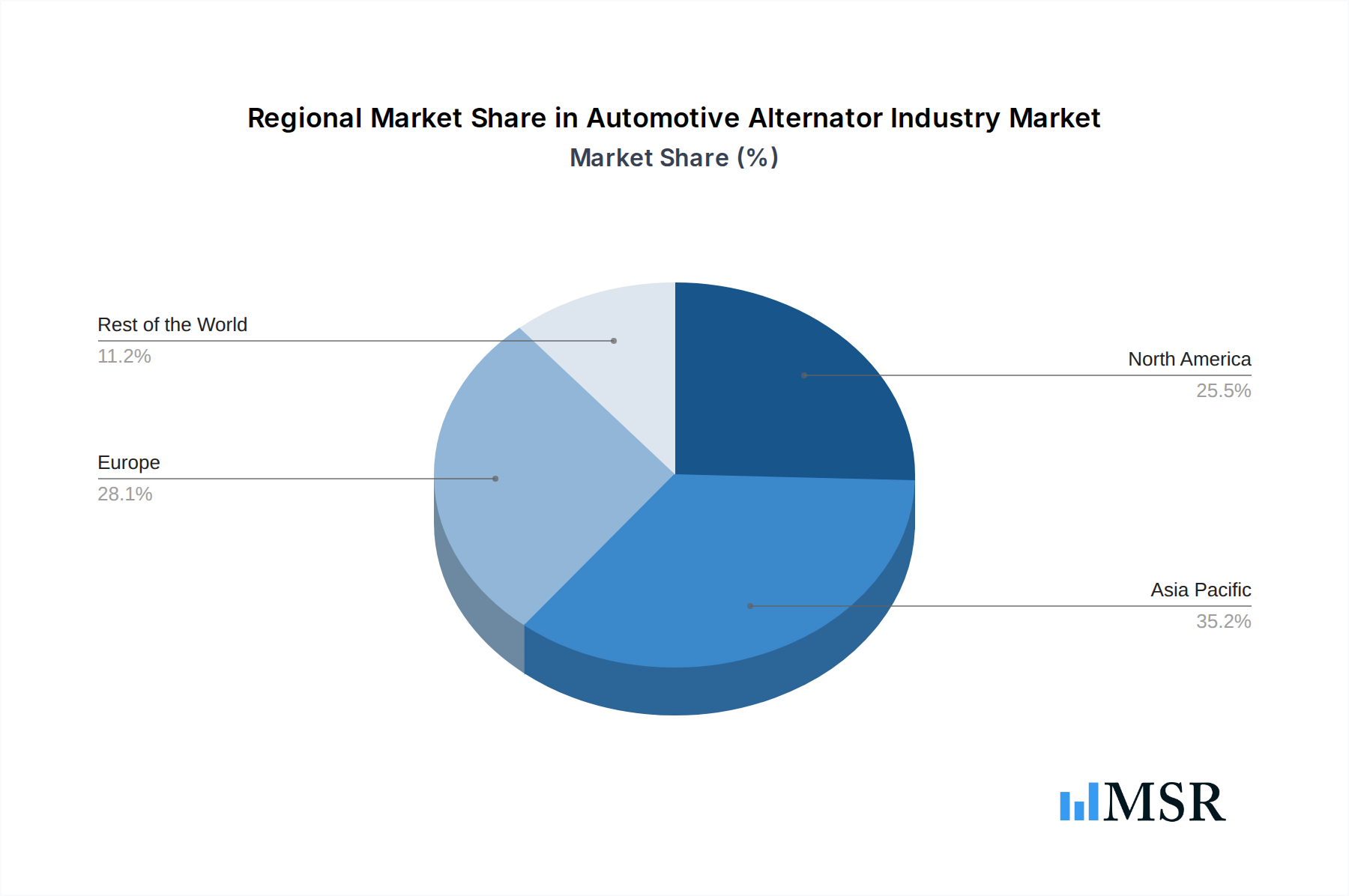

The market is segmented across various key areas, reflecting the diverse automotive landscape. Powertrain types include traditional IC engine vehicles and the rapidly growing segment of hybrid and electric vehicles. Vehicle types are broadly categorized into passenger cars and commercial vehicles, both of which are experiencing consistent demand. In terms of electrical configuration, single-phase and three-phase alternators cater to different vehicle requirements. Key players such as Robert Bosch GmbH, DENSO Corporation, and Hitachi Automotive Systems Ltd. are at the forefront, investing in research and development to innovate and meet evolving market needs. Geographically, Asia Pacific, led by China and India, is expected to be a dominant region due to its massive manufacturing base and burgeoning automotive market. North America and Europe, with their advanced automotive technologies and strong aftermarket presence, also represent substantial markets. The ongoing evolution of vehicle powertrains, including the increasing adoption of mild-hybrid systems and the sophisticated power demands of modern vehicles, ensures a sustained and evolving role for advanced alternator solutions within the automotive ecosystem.

Automotive Alternator Industry Company Market Share

This in-depth report provides a comprehensive analysis of the global automotive alternator market, a critical component in vehicle electrical systems. Covering the study period of 2019–2033, with a base year of 2025 and a forecast period from 2025–2033, this report offers invaluable insights for stakeholders seeking to understand market dynamics, growth drivers, and emerging opportunities. We delve into the automotive alternator industry across various powertrain types including IC engine vehicles and hybrid and electric vehicles, and across vehicle types such as passenger cars and commercial vehicles. The analysis extends to alternator types including single phase and three phase.

Automotive Alternator Industry Market Concentration & Dynamics

The global automotive alternator market exhibits a moderate to high concentration, with a few key players dominating significant market share. Robert Bosch GmbH, DENSO Corporation, and Hitachi Automotive Systems Ltd are recognized leaders, collectively holding a substantial portion of the market. The historical period (2019–2024) saw increased investment in advanced alternator technologies, driven by stringent emission regulations and the growing demand for fuel-efficient vehicles. Innovation ecosystems are thriving, with significant R&D expenditure focused on lightweight designs, improved efficiency, and the integration of smart functionalities. Regulatory frameworks, particularly around emissions and energy consumption, continue to shape product development and market access. Substitute products, while emerging in the form of advanced power electronics in electric vehicles, are not yet direct replacements for the core function of alternators in most automotive applications. End-user trends indicate a rising preference for vehicles equipped with advanced safety and infotainment systems, all reliant on robust electrical power generation, thus bolstering alternator demand. Mergers and acquisitions (M&A) activities, though not exceptionally high in volume during the historical period, have been strategic, aimed at consolidating market presence and acquiring technological expertise. For instance, a key M&A deal in 2022 involved the acquisition of a specialized alternator component manufacturer by a major Tier-1 supplier, aiming to enhance its vertical integration. Current market share estimates for 2025 place Bosch at approximately 18%, DENSO at 15%, and Hitachi at 12%, with other significant players like Valeo, BorgWarner Inc, and Tenneco Inc collectively accounting for another 30%. The remaining market share is distributed among several smaller and regional manufacturers. The forecast period (2025–2033) is expected to witness continued consolidation and strategic alliances to navigate the evolving automotive landscape.

Automotive Alternator Industry Industry Insights & Trends

The automotive alternator industry is poised for sustained growth, driven by a confluence of technological advancements, evolving consumer preferences, and stringent environmental mandates. The global automotive alternator market size was valued at approximately 15 Billion in 2024 and is projected to reach 22 Billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 4.5% during the forecast period (2025–2033). A primary growth driver is the continuous evolution of internal combustion engine (ICE) vehicles, which, despite the rise of EVs, will remain a significant part of the global fleet for years to come. Modern ICE vehicles are equipped with increasingly sophisticated electronic systems, demanding more powerful and efficient alternators. This includes advanced driver-assistance systems (ADAS), complex infotainment units, and enhanced climate control systems, all of which place a higher electrical load on the vehicle. Simultaneously, the burgeoning hybrid and electric vehicle (HEV) segment presents a unique dynamic. While fully electric vehicles do not rely on traditional alternators, hybrid vehicles utilize them to charge the battery pack and power onboard systems. This creates a dual demand: for advanced, high-output alternators in HEVs and for increasingly sophisticated alternator solutions in the ever-evolving ICE vehicle sector. Technological disruptions are a key theme, with manufacturers investing heavily in developing lighter, more compact, and more energy-efficient alternators. Innovations such as variable voltage alternators, integrated starter-generators (ISGs), and advanced thermal management systems are becoming more prevalent. These advancements not only improve fuel economy and reduce emissions in ICE vehicles but also contribute to the overall efficiency and range of hybrid powertrains. Evolving consumer behaviors are also playing a crucial role. There is a growing awareness and demand for vehicles that offer a superior in-car experience, which translates to more electronic features. Furthermore, global sustainability initiatives and government incentives are pushing consumers towards more environmentally friendly vehicles, including hybrids, which indirectly fuels the demand for advanced alternator technologies. The increasing average age of vehicle fleets in developed markets also necessitates a steady replacement demand for alternators. The report anticipates a strong emphasis on miniaturization and improved power density to accommodate the space constraints in modern vehicle architectures.

Key Markets & Segments Leading Automotive Alternator Industry

The automotive alternator industry is significantly influenced by regional economic conditions, regulatory landscapes, and consumer adoption rates for different vehicle technologies.

Dominant Region: Asia-Pacific, particularly China, India, and Southeast Asian nations, is emerging as the dominant region in the automotive alternator market.

- Drivers for Asia-Pacific Dominance:

- Economic Growth & Rising Disposable Incomes: Leading to increased vehicle ownership and sales of both passenger cars and commercial vehicles.

- Robust Manufacturing Hubs: Presence of major automotive manufacturers and a strong supply chain for automotive components.

- Government Initiatives: Favorable policies promoting automotive production and sales, including incentives for adopting cleaner technologies.

- Rapid Urbanization: Increased demand for transportation solutions, driving the sale of both personal and commercial vehicles.

- High Production Volumes of ICE Vehicles: While EV adoption is growing, the sheer volume of ICE vehicle production continues to fuel demand for traditional alternators.

- Drivers for Asia-Pacific Dominance:

Leading Powertrain Type: IC Engine Vehicles continue to represent the largest segment for automotive alternators.

- Dominance Analysis: Despite the accelerating transition towards electrification, internal combustion engines will remain a significant part of the global automotive landscape throughout the forecast period (2025–2033). The sheer volume of passenger cars and commercial vehicles equipped with ICE powertrains worldwide ensures a sustained demand for their associated alternator systems. Modern ICE vehicles are increasingly equipped with more complex electrical architectures, requiring higher output and more efficient alternators to power advanced features such as infotainment systems, ADAS, and sophisticated climate control. The technological advancements in ICE efficiency and emission reduction, though slowing down compared to EVs, still necessitate robust and reliable electrical power generation.

Leading Vehicle Type: Passenger Cars constitute the largest vehicle type segment for automotive alternators.

- Dominance Analysis: The global passenger car market consistently outpaces the commercial vehicle segment in terms of unit sales. This higher volume directly translates to a greater demand for alternators. Modern passenger cars are replete with electronic features, from sophisticated infotainment systems and navigation to advanced safety features like multiple airbags, parking sensors, and sophisticated lighting systems. The increasing integration of these technologies, driven by consumer demand for comfort, convenience, and safety, necessitates more powerful and reliable electrical systems, thus driving the demand for advanced alternators. The growth in emerging economies, where vehicle ownership is rising rapidly, further fuels the passenger car segment, consequently boosting the demand for alternators.

Dominant Alternator Type: Three Phase alternators are increasingly dominating the market.

- Dominance Analysis: While Single Phase alternators are still prevalent in older or lower-spec vehicles, the trend towards more powerful and efficient electrical systems in modern vehicles is driving the adoption of Three Phase alternators. Three-phase alternators offer higher power output, better voltage regulation, and improved efficiency compared to their single-phase counterparts. This makes them ideal for meeting the growing electrical demands of advanced automotive electronics, including those found in hybrid vehicles. As vehicles become more electrified and incorporate more power-hungry components, the advantages of three-phase systems become increasingly apparent, leading to their widespread adoption across the industry.

Automotive Alternator Industry Product Developments

Recent product developments in the automotive alternator industry are characterized by a focus on enhancing efficiency, reducing weight, and integrating intelligent features. Manufacturers are actively developing advanced alternator technologies such as higher power density units, integrated starter-generators (ISGs), and alternators with improved thermal management. These innovations aim to meet the increasing electrical demands of modern vehicles while contributing to fuel efficiency and reduced emissions. For example, the introduction of 12V/48V mild-hybrid systems has spurred the development of specialized alternators capable of higher voltage output and greater energy regeneration. These advanced products offer a competitive edge by enabling manufacturers to comply with stringent environmental regulations and cater to consumer demand for fuel-efficient and feature-rich vehicles. The market relevance of these developments is high, as they directly address the evolving needs of the automotive sector, paving the way for more sustainable and technologically advanced transportation.

Challenges in the Automotive Alternator Industry Market

The automotive alternator industry faces several significant challenges that could impede growth. The escalating transition towards fully electric vehicles (EVs) presents a long-term threat, as EVs do not utilize traditional alternators, leading to a potential decline in demand from this segment. Supply chain disruptions, exacerbated by geopolitical events and raw material price volatility, continue to pose a risk to production schedules and cost management. Furthermore, intense competition among established players and new entrants, particularly from lower-cost manufacturing regions, puts pressure on profit margins. Regulatory hurdles, such as evolving emission standards and the push for lighter vehicle components, necessitate continuous and costly R&D investments. The estimated impact of these challenges on market growth in the forecast period (2025–2033) could be a reduction in the overall projected CAGR by up to 0.5% if not effectively mitigated.

Forces Driving Automotive Alternator Industry Growth

Several key forces are propelling the growth of the automotive alternator industry. The persistent demand for IC engine vehicles globally, particularly in emerging economies, ensures a robust market for traditional alternators. The increasing sophistication of hybrid and electric vehicles necessitates advanced alternator systems for battery charging and auxiliary power. Technological advancements, such as the development of variable voltage alternators and integrated starter-generators (ISGs), are enhancing efficiency and performance. Stringent global emission regulations continue to drive innovation in alternator technology to improve fuel economy. Furthermore, the growing adoption of advanced driver-assistance systems (ADAS) and other in-car electronic features amplifies the electrical load on vehicles, creating a demand for higher-output alternators. For instance, the rise of 48V mild-hybrid systems, expected to grow at a CAGR of 15% from 2025-2033, is a significant driver.

Challenges in the Automotive Alternator Industry Market

While the industry faces challenges, long-term growth catalysts are evident. The continued evolution and adoption of mild-hybrid vehicle (MHV) technology present a substantial opportunity, as these vehicles rely on advanced alternator systems. Investments in research and development for lightweight and highly efficient alternators will be crucial for maintaining competitiveness. Strategic partnerships and joint ventures among manufacturers can help to share R&D costs and expand market reach. Furthermore, the increasing integration of alternator functionalities into larger power management systems within vehicles presents opportunities for value-added solutions. The expansion into aftermarket services and the development of remanufactured alternator solutions can also provide sustained revenue streams. The projected growth in the commercial vehicle segment, driven by logistics and e-commerce, will also contribute to long-term demand.

Emerging Opportunities in Automotive Alternator Industry

The automotive alternator industry is ripe with emerging opportunities driven by technological innovation and shifting consumer preferences. The increasing penetration of 48V mild-hybrid systems across various vehicle segments presents a significant growth avenue. Manufacturers can capitalize on developing specialized high-performance alternators tailored for these applications. The growing demand for advanced automotive electronics, including sophisticated infotainment systems, connectivity features, and autonomous driving capabilities, is creating a need for more powerful and efficient electrical power generation. Opportunities also lie in developing smart alternators with integrated diagnostic capabilities and improved power management functionalities. Furthermore, the expansion of the aftermarket sector for replacement alternators, particularly in regions with an aging vehicle fleet, offers a steady revenue stream. The development of more energy-efficient alternator designs can also open doors to new markets and applications beyond traditional automotive use.

Leading Players in the Automotive Alternator Industry Sector

- Mitsubishi Corporation

- Hitachi Automotive Systems Ltd

- BorgWarner Inc

- Tenneco Inc

- Valeo

- Robert Bosch GmbH

- Hella KGaA Hueck & Co

- Mecc Alt

- DENSO Corporation

- Lucas Industries PLC

Key Milestones in Automotive Alternator Industry Industry

- 2019: Launch of advanced 48V mild-hybrid alternator systems by several key players, responding to growing demand for fuel efficiency.

- 2020: Increased investment in R&D for lightweight alternator materials, driven by stricter emission standards and vehicle weight reduction targets.

- 2021: Several strategic partnerships formed between alternator manufacturers and EV component suppliers to explore integration opportunities in electrified powertrains.

- 2022: Introduction of alternators with enhanced thermal management systems to improve performance and longevity in demanding operating conditions.

- 2023: Significant focus on developing integrated starter-generators (ISGs) for a wider range of vehicle platforms, enhancing electrification capabilities.

- 2024: Growing interest in smart alternators with embedded diagnostics and predictive maintenance capabilities, signaling a move towards connected vehicle ecosystems.

Strategic Outlook for Automotive Alternator Industry Market

The strategic outlook for the automotive alternator industry is characterized by a dual focus on optimizing existing ICE technologies while embracing the evolving needs of electrified powertrains. Growth accelerators will be driven by continued innovation in alternator efficiency, power output, and integration capabilities. Companies that can successfully develop and market advanced alternators for mild-hybrid vehicles and those that can adapt their technologies to complement the electrical architectures of hybrid and electric vehicles will be best positioned. Strategic investments in R&D for lightweight materials and intelligent power management solutions will be critical. Furthermore, expanding global manufacturing footprints and strengthening supply chain resilience will be paramount to meeting the diverse demands of the automotive market. The report anticipates a shift towards more modular and adaptable alternator designs that can serve multiple vehicle platforms, optimizing production and reducing costs.

Automotive Alternator Industry Segmentation

-

1. Powertrain Type

- 1.1. IC Engine Vehicles

- 1.2. Hybrid and Electric Vehicles

-

2. Vehicle Type

- 2.1. Passenger Cars

- 2.2. Commercial Vehicles

-

3. Type

- 3.1. Single Phase

- 3.2. Three Phase

Automotive Alternator Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Rest of North America

-

2. Asia Pacific

- 2.1. China

- 2.2. Japan

- 2.3. India

- 2.4. South Korea

- 2.5. Rest of Asia Pacific

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Rest of Europe

-

4. Rest of the World

- 4.1. Brazil

- 4.2. Saudi Arabia

- 4.3. Other Countries

Automotive Alternator Industry Regional Market Share

Geographic Coverage of Automotive Alternator Industry

Automotive Alternator Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.70% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Powertrain Type

- 5.1.1. IC Engine Vehicles

- 5.1.2. Hybrid and Electric Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.2.1. Passenger Cars

- 5.2.2. Commercial Vehicles

- 5.3. Market Analysis, Insights and Forecast - by Type

- 5.3.1. Single Phase

- 5.3.2. Three Phase

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Asia Pacific

- 5.4.3. Europe

- 5.4.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Powertrain Type

- 6. Global Automotive Alternator Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Powertrain Type

- 6.1.1. IC Engine Vehicles

- 6.1.2. Hybrid and Electric Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.2.1. Passenger Cars

- 6.2.2. Commercial Vehicles

- 6.3. Market Analysis, Insights and Forecast - by Type

- 6.3.1. Single Phase

- 6.3.2. Three Phase

- 6.1. Market Analysis, Insights and Forecast - by Powertrain Type

- 7. North America Automotive Alternator Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Powertrain Type

- 7.1.1. IC Engine Vehicles

- 7.1.2. Hybrid and Electric Vehicles

- 7.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.2.1. Passenger Cars

- 7.2.2. Commercial Vehicles

- 7.3. Market Analysis, Insights and Forecast - by Type

- 7.3.1. Single Phase

- 7.3.2. Three Phase

- 7.1. Market Analysis, Insights and Forecast - by Powertrain Type

- 8. Asia Pacific Automotive Alternator Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Powertrain Type

- 8.1.1. IC Engine Vehicles

- 8.1.2. Hybrid and Electric Vehicles

- 8.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.2.1. Passenger Cars

- 8.2.2. Commercial Vehicles

- 8.3. Market Analysis, Insights and Forecast - by Type

- 8.3.1. Single Phase

- 8.3.2. Three Phase

- 8.1. Market Analysis, Insights and Forecast - by Powertrain Type

- 9. Europe Automotive Alternator Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Powertrain Type

- 9.1.1. IC Engine Vehicles

- 9.1.2. Hybrid and Electric Vehicles

- 9.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 9.2.1. Passenger Cars

- 9.2.2. Commercial Vehicles

- 9.3. Market Analysis, Insights and Forecast - by Type

- 9.3.1. Single Phase

- 9.3.2. Three Phase

- 9.1. Market Analysis, Insights and Forecast - by Powertrain Type

- 10. Rest of the World Automotive Alternator Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Powertrain Type

- 10.1.1. IC Engine Vehicles

- 10.1.2. Hybrid and Electric Vehicles

- 10.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 10.2.1. Passenger Cars

- 10.2.2. Commercial Vehicles

- 10.3. Market Analysis, Insights and Forecast - by Type

- 10.3.1. Single Phase

- 10.3.2. Three Phase

- 10.1. Market Analysis, Insights and Forecast - by Powertrain Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Mitsubishi Corporation

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Hitachi Automotive Systems Ltd

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 BorgWarner Inc

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Tenneco Inc

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Valeo

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Robert Bosch GmbH

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Hella KGaA Hueck & Co

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Mecc Alt

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 DENSO Corporation

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Lucas Industries PLC

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.1 Mitsubishi Corporation

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Automotive Alternator Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Automotive Alternator Industry Revenue (Million), by Powertrain Type 2025 & 2033

- Figure 3: North America Automotive Alternator Industry Revenue Share (%), by Powertrain Type 2025 & 2033

- Figure 4: North America Automotive Alternator Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 5: North America Automotive Alternator Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 6: North America Automotive Alternator Industry Revenue (Million), by Type 2025 & 2033

- Figure 7: North America Automotive Alternator Industry Revenue Share (%), by Type 2025 & 2033

- Figure 8: North America Automotive Alternator Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Automotive Alternator Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Automotive Alternator Industry Revenue (Million), by Powertrain Type 2025 & 2033

- Figure 11: Asia Pacific Automotive Alternator Industry Revenue Share (%), by Powertrain Type 2025 & 2033

- Figure 12: Asia Pacific Automotive Alternator Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 13: Asia Pacific Automotive Alternator Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 14: Asia Pacific Automotive Alternator Industry Revenue (Million), by Type 2025 & 2033

- Figure 15: Asia Pacific Automotive Alternator Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Asia Pacific Automotive Alternator Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Asia Pacific Automotive Alternator Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Europe Automotive Alternator Industry Revenue (Million), by Powertrain Type 2025 & 2033

- Figure 19: Europe Automotive Alternator Industry Revenue Share (%), by Powertrain Type 2025 & 2033

- Figure 20: Europe Automotive Alternator Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 21: Europe Automotive Alternator Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 22: Europe Automotive Alternator Industry Revenue (Million), by Type 2025 & 2033

- Figure 23: Europe Automotive Alternator Industry Revenue Share (%), by Type 2025 & 2033

- Figure 24: Europe Automotive Alternator Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Europe Automotive Alternator Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Rest of the World Automotive Alternator Industry Revenue (Million), by Powertrain Type 2025 & 2033

- Figure 27: Rest of the World Automotive Alternator Industry Revenue Share (%), by Powertrain Type 2025 & 2033

- Figure 28: Rest of the World Automotive Alternator Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 29: Rest of the World Automotive Alternator Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 30: Rest of the World Automotive Alternator Industry Revenue (Million), by Type 2025 & 2033

- Figure 31: Rest of the World Automotive Alternator Industry Revenue Share (%), by Type 2025 & 2033

- Figure 32: Rest of the World Automotive Alternator Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: Rest of the World Automotive Alternator Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Alternator Industry Revenue Million Forecast, by Powertrain Type 2020 & 2033

- Table 2: Global Automotive Alternator Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 3: Global Automotive Alternator Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 4: Global Automotive Alternator Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Automotive Alternator Industry Revenue Million Forecast, by Powertrain Type 2020 & 2033

- Table 6: Global Automotive Alternator Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 7: Global Automotive Alternator Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 8: Global Automotive Alternator Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United States Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Canada Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Mexico Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Rest of North America Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Global Automotive Alternator Industry Revenue Million Forecast, by Powertrain Type 2020 & 2033

- Table 14: Global Automotive Alternator Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 15: Global Automotive Alternator Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 16: Global Automotive Alternator Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 17: China Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Japan Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: India Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: South Korea Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Rest of Asia Pacific Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Global Automotive Alternator Industry Revenue Million Forecast, by Powertrain Type 2020 & 2033

- Table 23: Global Automotive Alternator Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 24: Global Automotive Alternator Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 25: Global Automotive Alternator Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 26: Germany Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: United Kingdom Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: France Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Italy Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Rest of Europe Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Global Automotive Alternator Industry Revenue Million Forecast, by Powertrain Type 2020 & 2033

- Table 32: Global Automotive Alternator Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 33: Global Automotive Alternator Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 34: Global Automotive Alternator Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 35: Brazil Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Saudi Arabia Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: Other Countries Automotive Alternator Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Alternator Industry?

The projected CAGR is approximately 6.70%.

2. Which companies are prominent players in the Automotive Alternator Industry?

Key companies in the market include Mitsubishi Corporation, Hitachi Automotive Systems Ltd, BorgWarner Inc, Tenneco Inc, Valeo, Robert Bosch GmbH, Hella KGaA Hueck & Co, Mecc Alt, DENSO Corporation, Lucas Industries PLC.

3. What are the main segments of the Automotive Alternator Industry?

The market segments include Powertrain Type, Vehicle Type, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 24.58 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Vehicle Production.

6. What are the notable trends driving market growth?

Passenger Car Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

Shift Towards Electric powertrain.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Alternator Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Alternator Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Alternator Industry?

To stay informed about further developments, trends, and reports in the Automotive Alternator Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence