Key Insights

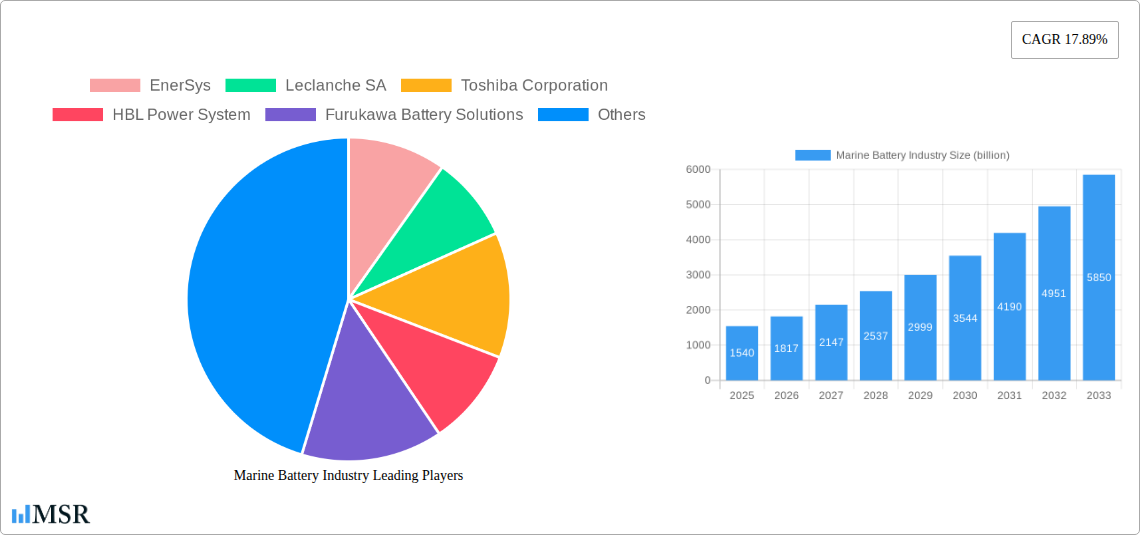

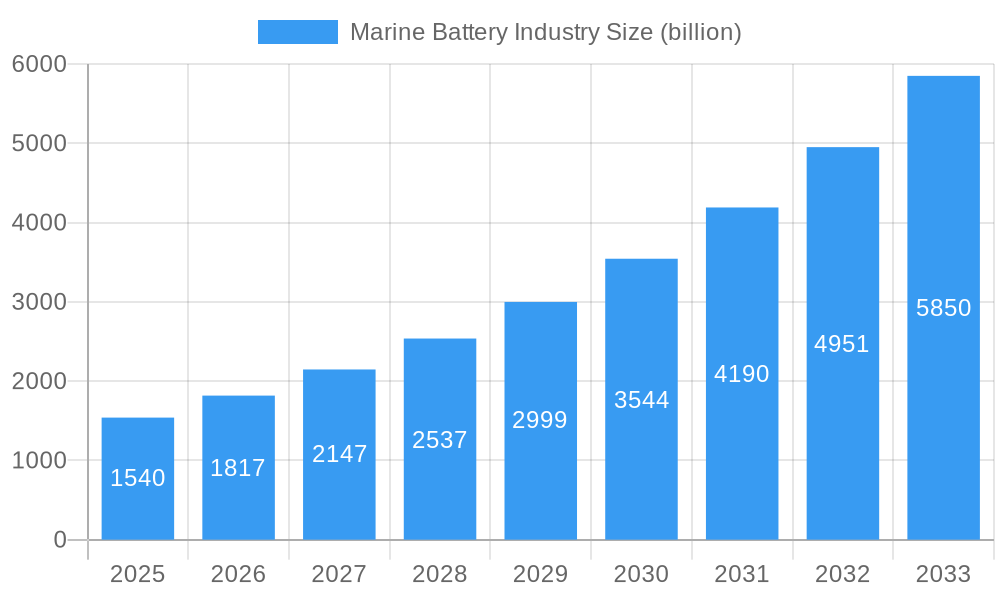

The global Marine Battery Industry is poised for significant expansion, projected to reach a market size of $1.54 billion by 2025. This growth is fueled by a remarkable Compound Annual Growth Rate (CAGR) of 17.89%, indicating robust demand and innovation within the sector. Key drivers propelling this surge include the increasing adoption of hybrid and electric propulsion systems in commercial and defense vessels, driven by stringent environmental regulations and the pursuit of operational cost efficiencies. Furthermore, advancements in battery technologies, particularly the growing prominence of Lithium-ion batteries due to their superior energy density and longer lifespan, are reshaping the market landscape. The industry is also witnessing a trend towards the integration of advanced battery management systems for enhanced safety and performance, alongside a growing interest in fuel cell technology for long-duration voyages, offering a cleaner and more sustainable power solution.

Marine Battery Industry Market Size (In Billion)

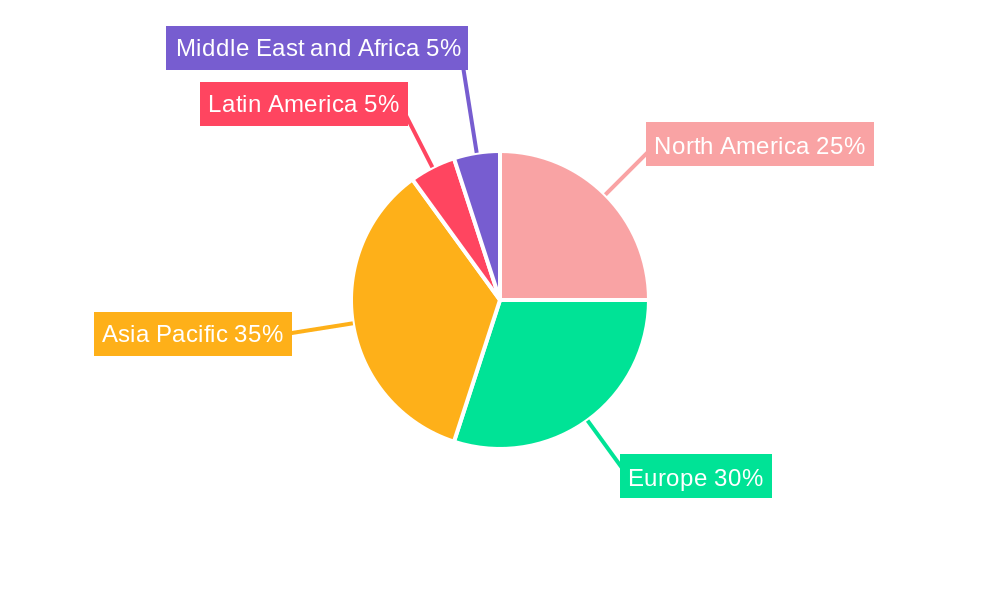

Despite the overwhelmingly positive growth trajectory, certain restraints may impact the pace of adoption. High initial investment costs for advanced battery systems and the need for robust charging infrastructure in ports present significant challenges. However, the long-term benefits, including reduced fuel consumption, lower emissions, and enhanced operational flexibility, are expected to outweigh these initial hurdles. The market is segmented by battery type, with Lithium-ion batteries dominating due to their technological advantages, and by ship type, with commercial vessels leading adoption followed closely by the defense sector. Geographically, Asia Pacific, driven by its extensive coastline and strong maritime trade, is expected to be a key growth region, alongside established markets in North America and Europe. Leading companies such as EnerSys, Leclanche SA, and Toshiba Corporation are at the forefront of innovation, developing cutting-edge solutions to meet the evolving demands of the marine sector.

Marine Battery Industry Company Market Share

Marine Battery Industry Market Report: Driving Sustainable Maritime Power Solutions (2019-2033)

This comprehensive market research report provides an in-depth analysis of the global Marine Battery Industry, focusing on lithium-ion batteries, fuel cells, and lead-acid batteries for commercial and defense ship types. With a study period spanning from 2019 to 2033, and a base year of 2025, this report offers unparalleled insights into market dynamics, key trends, and future growth trajectories. The forecast period of 2025–2033 delves into emerging technologies and strategic opportunities within the marine energy storage solutions sector. Gain actionable intelligence to navigate the evolving maritime decarbonization landscape and capitalize on the growth of electric and hybrid marine propulsion.

Marine Battery Industry Market Concentration & Dynamics

The Marine Battery Industry exhibits a moderate to high level of market concentration, with key players like EnerSys, Toshiba Corporation, and Siemens AG holding significant shares. Innovation ecosystems are flourishing, driven by increased R&D investment and a focus on enhanced energy density and faster charging capabilities for marine battery systems. Regulatory frameworks, particularly those from the International Maritime Organization (IMO) aimed at reducing greenhouse gas emissions, are a major catalyst for adoption. Substitute products, such as traditional fossil fuels, are gradually being displaced by advancements in marine battery technology. End-user trends show a strong preference for sustainable and efficient power solutions, leading to increased adoption of lithium-ion marine batteries. Merger and acquisition (M&A) activities are on the rise as larger companies seek to consolidate their market position and acquire innovative technologies. For instance, over the historical period of 2019-2024, the number of M&A deals related to marine battery manufacturers and maritime technology providers has seen a substantial increase, indicating a dynamic and consolidating market. The total market value is projected to reach $25 billion by 2033, with an estimated 100+ M&A deals expected throughout the forecast period.

Marine Battery Industry Industry Insights & Trends

The Marine Battery Industry is experiencing robust growth, driven by a confluence of technological advancements, environmental regulations, and increasing demand for cleaner maritime operations. The market size for marine batteries is projected to grow from an estimated $10 billion in 2025 to over $25 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 12%. This significant expansion is propelled by the global push for decarbonization in the shipping sector, aiming to reduce sulfur oxides (SOx) and nitrogen oxides (NOx) emissions. Technological disruptions, particularly in lithium-ion battery chemistry and fuel cell technology, are making these solutions more viable and cost-effective for a wider range of marine applications. Extended lifespan, improved safety features, and higher energy densities are key innovations that are transforming the marine propulsion systems. Evolving consumer behaviors, encompassing ship owners and operators' increasing awareness of the environmental impact of their fleets, are steering them towards adopting eco-friendly marine power. The demand for zero-emission vessels and hybrid marine solutions is accelerating this transition. Furthermore, government incentives and subsidies aimed at promoting sustainable maritime practices are playing a crucial role in driving market penetration. The development of advanced battery management systems (BMS) is also enhancing the reliability and performance of these batteries, further solidifying their position as a preferred power source for modern vessels. The integration of smart battery solutions and predictive maintenance capabilities will also be crucial in the coming years.

Key Markets & Segments Leading Marine Battery Industry

The Marine Battery Industry is witnessing significant growth across various segments, with lithium-ion batteries emerging as the dominant technology.

Battery Type Dominance:

- Lithium-ion Batteries: These are leading the market due to their high energy density, longer cycle life, and relatively lighter weight compared to traditional lead-acid batteries. They are increasingly being adopted for both new builds and retrofits in commercial and defense vessels. The growing demand for electric ferries, offshore support vessels, and naval warships utilizing zero-emission propulsion is a key driver. The market share for lithium-ion batteries is projected to exceed 65% by 2033.

- Fuel Cells: While still a nascent segment, fuel cells, particularly hydrogen fuel cells, are poised for significant growth, especially in long-haul shipping and larger vessels. Their ability to provide higher energy output and longer operational times makes them attractive for future maritime applications.

- Lead Acid Batteries: These remain relevant for smaller vessels, auxiliary power, and emergency backup systems due to their lower cost and proven reliability. However, their market share is expected to decline gradually as more advanced technologies become accessible.

- Nickel-Cadmium Batteries: Primarily used in legacy systems and specific niche applications, their market share is expected to remain relatively small and decline further.

Ship Type Dominance:

- Commercial Vessels: This segment is the largest driver of the marine battery market. The increasing pressure to comply with stringent environmental regulations and the growing operational efficiencies offered by electric and hybrid propulsion are leading to widespread adoption. This includes container ships, ferries, offshore support vessels, and inland waterway vessels. Economic growth in global trade directly correlates with the demand for efficient and sustainable commercial shipping solutions.

- Defense Vessels: The defense sector is a significant adopter, driven by the need for stealth, reduced acoustic signatures, and enhanced operational flexibility. Modern naval vessels are increasingly incorporating advanced marine battery solutions for silent running, improved power management, and as a backup power source. The ongoing modernization of naval fleets globally is a major catalyst in this segment.

Regional Dominance:

- Asia-Pacific: This region, particularly China and South Korea, is a leading market due to its strong shipbuilding industry, significant investments in green maritime technologies, and supportive government policies.

- Europe: With ambitious environmental targets and a strong focus on maritime innovation, Europe is a key market for advanced marine battery solutions.

- North America: Growing adoption in recreational boating and a developing interest in electrification of commercial fleets are contributing to market growth.

Marine Battery Industry Product Developments

Product development in the Marine Battery Industry is characterized by a relentless pursuit of higher energy density, improved safety, and extended lifespan. Leading companies are focusing on advanced lithium-ion chemistries like Nickel Manganese Cobalt (NMC) and Lithium Iron Phosphate (LFP) to meet the demanding requirements of maritime applications. Innovations in solid-state batteries are also on the horizon, promising even greater safety and energy storage capabilities. Furthermore, the integration of sophisticated Battery Management Systems (BMS) is enhancing performance and reliability, enabling precise monitoring of charge levels, temperature, and overall battery health. The development of modular and scalable battery packs allows for flexible integration into various vessel designs, from small recreational boats to large commercial and defense ships. These advancements are crucial for enabling the widespread adoption of electric and hybrid marine propulsion systems, paving the way for more sustainable and efficient maritime operations. The competitive edge lies in offering robust, safe, and cost-effective energy storage solutions tailored to specific marine environments.

Challenges in the Marine Battery Industry Market

Despite the promising growth, the Marine Battery Industry faces several significant challenges.

- High Initial Capital Investment: The upfront cost of marine battery systems, particularly for large vessels, remains a considerable barrier.

- Safety Concerns and Fire Risk Mitigation: While advancements are being made, ensuring the absolute safety of high-capacity battery installations in harsh maritime environments is paramount, requiring robust fire suppression and management systems.

- Infrastructure Development: The availability of shore-side charging infrastructure at ports is still limited, hindering the widespread adoption of fully electric vessels.

- Battery Recycling and Disposal: Establishing efficient and environmentally sound systems for recycling and disposing of end-of-life marine batteries is a growing concern.

- Supply Chain Volatility: The sourcing of raw materials, such as lithium and cobalt, can be subject to price fluctuations and geopolitical risks, impacting production costs and availability.

- Regulatory Harmonization: Divergent regulations across different maritime authorities can create complexities for global shipping operations.

Forces Driving Marine Battery Industry Growth

The Marine Battery Industry is being propelled by a powerful set of drivers.

- Stringent Environmental Regulations: International and national regulations mandating reductions in greenhouse gas emissions and pollutants are a primary catalyst, pushing ship owners towards cleaner propulsion technologies.

- Technological Advancements: Continuous innovation in battery chemistries, energy density, charging speed, and safety features is making marine battery solutions increasingly viable and competitive.

- Cost Competitiveness: The declining costs of lithium-ion batteries and the potential for lower operational expenses (fuel savings, reduced maintenance) are enhancing their economic attractiveness.

- Growing Demand for Electric and Hybrid Vessels: The increasing preference for zero-emission and low-emission maritime transport is creating a strong market pull for battery-powered solutions.

- Government Incentives and Support: Subsidies, tax credits, and R&D funding from governments worldwide are accelerating the adoption of sustainable maritime technologies.

- Energy Security and Independence: Reducing reliance on volatile fossil fuel markets is a strategic objective for many nations, driving interest in alternative energy sources like batteries.

Challenges in the Marine Battery Industry Market

The long-term growth catalysts for the Marine Battery Industry are deeply rooted in innovation and strategic market expansion. The continuous improvement in battery energy density and lifespan, driven by ongoing R&D into new materials and designs, will enable longer voyages and more demanding applications. The development of advanced thermal management systems will enhance performance and safety in diverse environmental conditions. Furthermore, the increasing integration of smart battery management systems (BMS), incorporating AI and predictive analytics, will optimize performance, extend battery life, and reduce operational risks. Strategic partnerships between battery manufacturers, shipyards, and technology providers are crucial for co-developing tailored solutions and accelerating market penetration. The expansion into emerging maritime markets and the development of standardized charging infrastructure will also play a pivotal role in sustaining long-term growth.

Emerging Opportunities in Marine Battery Industry

Emerging opportunities in the Marine Battery Industry are diverse and significant. The rapid growth of the offshore wind energy sector is creating a substantial demand for specialized vessels equipped with advanced marine battery systems for power generation and propulsion. The ongoing retrofitting of existing vessel fleets with hybrid and electric propulsion systems presents a vast untapped market. Furthermore, the development of hydrogen fuel cells as a complementary or alternative energy storage solution for long-haul shipping offers a significant growth avenue. The expansion of autonomous shipping and uncrewed vessels will also necessitate reliable and compact marine battery solutions. The increasing focus on circular economy principles presents an opportunity for developing robust battery recycling and repurposing initiatives, creating new revenue streams and enhancing sustainability.

Leading Players in the Marine Battery Industry Sector

- EnerSys

- Leclanche SA

- Toshiba Corporation

- HBL Power System

- Furukawa Battery Solutions

- Siemens AG

- BorgWarner Inc

- Wartsila

- Saft

- Exide Technologies

Key Milestones in Marine Battery Industry Industry

- October 2022: ABS signed a cooperation agreement with Contemporary Amperex Technology Co., Limited (CATL) to work together and research lithium battery propulsion for next-generation vessels. Under the agreement, the two companies would carry out research on the technical standards for battery-powered vessels, which includes key safety-related technologies such as the charging system, power battery compartment layout, propulsion system, and fire control.

- January 2022: Vision Marine Technologies entered a partnership with Octillion Power Systems, a battery supplier, to develop a custom high-voltage 35 kW battery pack exclusively for use in the recreational boating market.

Strategic Outlook for Marine Battery Industry Market

The strategic outlook for the Marine Battery Industry is exceptionally positive, driven by the undeniable global shift towards sustainable maritime transport. The increasing urgency to meet climate targets and reduce the environmental footprint of shipping operations will continue to fuel demand for advanced marine battery solutions. Key growth accelerators include strategic investments in R&D for next-generation battery technologies, such as solid-state batteries and enhanced fuel cell systems. Fostering strong collaborations between battery manufacturers, shipbuilders, and regulatory bodies will be crucial for developing standardized charging infrastructure and safety protocols. The market is also poised for expansion into new vessel segments and geographical regions. The continued decline in battery costs, coupled with government support and incentives, will further solidify the economic viability of electric and hybrid marine propulsion, positioning the Marine Battery Industry for sustained and significant growth.

Marine Battery Industry Segmentation

-

1. Battery

- 1.1. Lithium-ion

- 1.2. Nickel-Cadmium

- 1.3. Fuel Cell

- 1.4. Lead Acid

-

2. Ship Type

- 2.1. Commercial

- 2.2. Defense

Marine Battery Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Russia

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. India

- 3.2. China

- 3.3. Japan

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Latin America

- 4.1. Brazil

- 4.2. Rest of Latin America

-

5. Middle East and Africa

- 5.1. United Arab Emirates

- 5.2. Saudi Arabia

- 5.3. Israel

- 5.4. South Africa

- 5.5. Rest of Middle East and Africa

Marine Battery Industry Regional Market Share

Geographic Coverage of Marine Battery Industry

Marine Battery Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 17.89% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Battery

- 5.1.1. Lithium-ion

- 5.1.2. Nickel-Cadmium

- 5.1.3. Fuel Cell

- 5.1.4. Lead Acid

- 5.2. Market Analysis, Insights and Forecast - by Ship Type

- 5.2.1. Commercial

- 5.2.2. Defense

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Battery

- 6. Global Marine Battery Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Battery

- 6.1.1. Lithium-ion

- 6.1.2. Nickel-Cadmium

- 6.1.3. Fuel Cell

- 6.1.4. Lead Acid

- 6.2. Market Analysis, Insights and Forecast - by Ship Type

- 6.2.1. Commercial

- 6.2.2. Defense

- 6.1. Market Analysis, Insights and Forecast - by Battery

- 7. North America Marine Battery Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Battery

- 7.1.1. Lithium-ion

- 7.1.2. Nickel-Cadmium

- 7.1.3. Fuel Cell

- 7.1.4. Lead Acid

- 7.2. Market Analysis, Insights and Forecast - by Ship Type

- 7.2.1. Commercial

- 7.2.2. Defense

- 7.1. Market Analysis, Insights and Forecast - by Battery

- 8. Europe Marine Battery Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Battery

- 8.1.1. Lithium-ion

- 8.1.2. Nickel-Cadmium

- 8.1.3. Fuel Cell

- 8.1.4. Lead Acid

- 8.2. Market Analysis, Insights and Forecast - by Ship Type

- 8.2.1. Commercial

- 8.2.2. Defense

- 8.1. Market Analysis, Insights and Forecast - by Battery

- 9. Asia Pacific Marine Battery Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Battery

- 9.1.1. Lithium-ion

- 9.1.2. Nickel-Cadmium

- 9.1.3. Fuel Cell

- 9.1.4. Lead Acid

- 9.2. Market Analysis, Insights and Forecast - by Ship Type

- 9.2.1. Commercial

- 9.2.2. Defense

- 9.1. Market Analysis, Insights and Forecast - by Battery

- 10. Latin America Marine Battery Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Battery

- 10.1.1. Lithium-ion

- 10.1.2. Nickel-Cadmium

- 10.1.3. Fuel Cell

- 10.1.4. Lead Acid

- 10.2. Market Analysis, Insights and Forecast - by Ship Type

- 10.2.1. Commercial

- 10.2.2. Defense

- 10.1. Market Analysis, Insights and Forecast - by Battery

- 11. Middle East and Africa Marine Battery Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Battery

- 11.1.1. Lithium-ion

- 11.1.2. Nickel-Cadmium

- 11.1.3. Fuel Cell

- 11.1.4. Lead Acid

- 11.2. Market Analysis, Insights and Forecast - by Ship Type

- 11.2.1. Commercial

- 11.2.2. Defense

- 11.1. Market Analysis, Insights and Forecast - by Battery

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 EnerSys

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Leclanche SA

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Toshiba Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 HBL Power System

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Furukawa Battery Solutions

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Siemens AG

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 BorgWarner Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Wartsila

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Saft

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Exide Technologies

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 EnerSys

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Marine Battery Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Marine Battery Industry Revenue (billion), by Battery 2025 & 2033

- Figure 3: North America Marine Battery Industry Revenue Share (%), by Battery 2025 & 2033

- Figure 4: North America Marine Battery Industry Revenue (billion), by Ship Type 2025 & 2033

- Figure 5: North America Marine Battery Industry Revenue Share (%), by Ship Type 2025 & 2033

- Figure 6: North America Marine Battery Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Marine Battery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Marine Battery Industry Revenue (billion), by Battery 2025 & 2033

- Figure 9: Europe Marine Battery Industry Revenue Share (%), by Battery 2025 & 2033

- Figure 10: Europe Marine Battery Industry Revenue (billion), by Ship Type 2025 & 2033

- Figure 11: Europe Marine Battery Industry Revenue Share (%), by Ship Type 2025 & 2033

- Figure 12: Europe Marine Battery Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Marine Battery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Marine Battery Industry Revenue (billion), by Battery 2025 & 2033

- Figure 15: Asia Pacific Marine Battery Industry Revenue Share (%), by Battery 2025 & 2033

- Figure 16: Asia Pacific Marine Battery Industry Revenue (billion), by Ship Type 2025 & 2033

- Figure 17: Asia Pacific Marine Battery Industry Revenue Share (%), by Ship Type 2025 & 2033

- Figure 18: Asia Pacific Marine Battery Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Marine Battery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Marine Battery Industry Revenue (billion), by Battery 2025 & 2033

- Figure 21: Latin America Marine Battery Industry Revenue Share (%), by Battery 2025 & 2033

- Figure 22: Latin America Marine Battery Industry Revenue (billion), by Ship Type 2025 & 2033

- Figure 23: Latin America Marine Battery Industry Revenue Share (%), by Ship Type 2025 & 2033

- Figure 24: Latin America Marine Battery Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Latin America Marine Battery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Marine Battery Industry Revenue (billion), by Battery 2025 & 2033

- Figure 27: Middle East and Africa Marine Battery Industry Revenue Share (%), by Battery 2025 & 2033

- Figure 28: Middle East and Africa Marine Battery Industry Revenue (billion), by Ship Type 2025 & 2033

- Figure 29: Middle East and Africa Marine Battery Industry Revenue Share (%), by Ship Type 2025 & 2033

- Figure 30: Middle East and Africa Marine Battery Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East and Africa Marine Battery Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Marine Battery Industry Revenue billion Forecast, by Battery 2020 & 2033

- Table 2: Global Marine Battery Industry Revenue billion Forecast, by Ship Type 2020 & 2033

- Table 3: Global Marine Battery Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Marine Battery Industry Revenue billion Forecast, by Battery 2020 & 2033

- Table 5: Global Marine Battery Industry Revenue billion Forecast, by Ship Type 2020 & 2033

- Table 6: Global Marine Battery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Marine Battery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Marine Battery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Global Marine Battery Industry Revenue billion Forecast, by Battery 2020 & 2033

- Table 10: Global Marine Battery Industry Revenue billion Forecast, by Ship Type 2020 & 2033

- Table 11: Global Marine Battery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Germany Marine Battery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: United Kingdom Marine Battery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: France Marine Battery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Russia Marine Battery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Rest of Europe Marine Battery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Global Marine Battery Industry Revenue billion Forecast, by Battery 2020 & 2033

- Table 18: Global Marine Battery Industry Revenue billion Forecast, by Ship Type 2020 & 2033

- Table 19: Global Marine Battery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 20: India Marine Battery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: China Marine Battery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Japan Marine Battery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: South Korea Marine Battery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Rest of Asia Pacific Marine Battery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Global Marine Battery Industry Revenue billion Forecast, by Battery 2020 & 2033

- Table 26: Global Marine Battery Industry Revenue billion Forecast, by Ship Type 2020 & 2033

- Table 27: Global Marine Battery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 28: Brazil Marine Battery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: Rest of Latin America Marine Battery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Global Marine Battery Industry Revenue billion Forecast, by Battery 2020 & 2033

- Table 31: Global Marine Battery Industry Revenue billion Forecast, by Ship Type 2020 & 2033

- Table 32: Global Marine Battery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 33: United Arab Emirates Marine Battery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Saudi Arabia Marine Battery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Israel Marine Battery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: South Africa Marine Battery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Rest of Middle East and Africa Marine Battery Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Marine Battery Industry?

The projected CAGR is approximately 17.89%.

2. Which companies are prominent players in the Marine Battery Industry?

Key companies in the market include EnerSys, Leclanche SA, Toshiba Corporation, HBL Power System, Furukawa Battery Solutions, Siemens AG, BorgWarner Inc, Wartsila, Saft, Exide Technologies.

3. What are the main segments of the Marine Battery Industry?

The market segments include Battery, Ship Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.54 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Adoption of 2-wheelers across the Globe.

6. What are the notable trends driving market growth?

Lithium-ion Segment is Projected to Highest Growth During the Forecast Period.

7. Are there any restraints impacting market growth?

Rise in demand of Electric Vehicles.

8. Can you provide examples of recent developments in the market?

October 2022: ABS signed a cooperation agreement with Contemporary Amperex Technology Co., Limited (CATL) to work together and research lithium battery propulsion for next-generation vessels. Under the agreement, the two companies would carry out research on the technical standards for battery-powered vessels, which includes key safety-related technologies such as the charging system, power battery compartment layout, propulsion system, and fire control.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Marine Battery Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Marine Battery Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Marine Battery Industry?

To stay informed about further developments, trends, and reports in the Marine Battery Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence