Key Insights

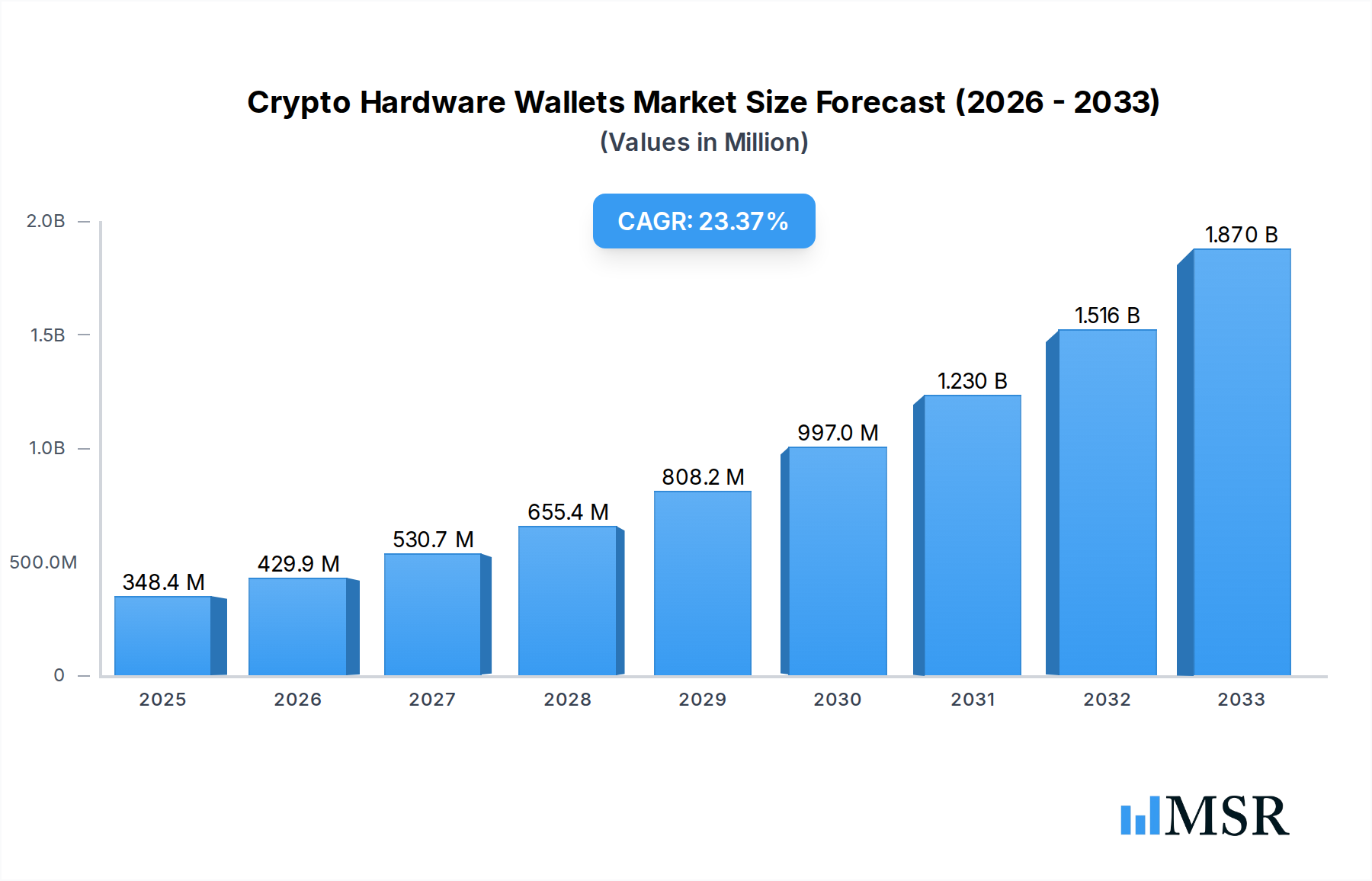

The global Crypto Hardware Wallets market is poised for exceptional growth, projected to reach an estimated $348.4 million in 2025 with a robust CAGR of 23.5% over the forecast period. This significant expansion is fueled by a confluence of factors, primarily the increasing adoption of cryptocurrencies by both individual investors and businesses seeking secure storage solutions. As digital asset portfolios grow, the need for advanced security features offered by hardware wallets becomes paramount. The inherent security advantages, such as offline storage of private keys and protection against online threats like malware and phishing, are driving demand. Furthermore, the growing regulatory clarity and institutional interest in the crypto space are contributing to a more stable and trusted environment, encouraging wider adoption and consequently, a higher demand for specialized hardware wallet solutions. The market's trajectory is also influenced by ongoing innovation in connectivity options, with USB and Bluetooth interfaces becoming standard, and emerging technologies like NFC offering enhanced user convenience and accessibility.

Crypto Hardware Wallets Market Size (In Million)

The market's expansion is further propelled by a growing awareness of the risks associated with storing digital assets on exchanges or software wallets. Users are increasingly prioritizing the self-custody of their cryptocurrencies, leading to a surge in demand for hardware wallets that offer superior protection. Key drivers include the rising number of cryptocurrency users globally, the increasing complexity and value of crypto holdings, and the continuous development of new and improved hardware wallet models with user-friendly interfaces and enhanced security protocols. While the market demonstrates a strong upward trend, potential restraints such as the initial cost of hardware wallets for some consumers and the learning curve associated with setting up and managing them could present minor headwinds. However, the overwhelming benefit of enhanced security and peace of mind for crypto asset holders is expected to largely outweigh these concerns, ensuring a dynamic and thriving market for crypto hardware wallets throughout the forecast period.

Crypto Hardware Wallets Company Market Share

Unlock Unprecedented Security: The Comprehensive Crypto Hardware Wallets Market Report 2024-2033

This definitive industry report offers an in-depth analysis of the global crypto hardware wallets market, covering historical performance, current dynamics, and future projections. With an estimated market size projected to reach 15,000 million by 2033, and a robust CAGR of 20% during the forecast period (2025-2033), this report is an indispensable resource for investors, developers, security professionals, and policymakers seeking to navigate this rapidly evolving sector. We delve into key players, technological advancements, market segmentation, and emerging trends to provide actionable insights for strategic decision-making. The study period spans from 2019 to 2033, with a base year of 2025, offering a comprehensive historical and forward-looking perspective.

Crypto Hardware Wallets Market Concentration & Dynamics

The crypto hardware wallets market, while experiencing rapid growth, exhibits a moderate level of concentration, with a few dominant players like Ledger and Trezor holding substantial market share, estimated at over 60% combined in 2024. The innovation ecosystem is robust, driven by continuous advancements in security features and user experience. Regulatory frameworks are evolving, with increased scrutiny on digital asset security, impacting product development and market entry strategies. Substitute products, such as software wallets and exchange-held assets, pose a challenge but are increasingly viewed as less secure alternatives for significant holdings. End-user trends indicate a growing demand for user-friendly yet highly secure solutions, particularly among institutional investors and cryptocurrency enthusiasts. Mergers and acquisitions (M&A) activities are on the rise, with an estimated 15 M&A deals in the historical period (2019-2024), indicating consolidation and strategic expansion by key companies. The market is characterized by fierce competition, a focus on intellectual property, and strategic partnerships to enhance distribution and technological capabilities.

Crypto Hardware Wallets Industry Insights & Trends

The global crypto hardware wallets market is on a trajectory of significant expansion, driven by the escalating adoption of cryptocurrencies and the paramount need for robust digital asset security. The market size, valued at approximately 8,000 million in 2024, is projected to ascend to 15,000 million by 2033, exhibiting a compound annual growth rate (CAGR) of 20% during the forecast period (2025-2033). This growth is underpinned by several key factors, including the increasing institutionalization of cryptocurrencies, where large corporations and financial institutions are allocating significant capital to digital assets, necessitating enterprise-grade security solutions. Furthermore, the retail segment is witnessing sustained growth as more individuals enter the crypto space, becoming increasingly aware of the risks associated with online storage and seeking secure offline solutions.

Technological disruptions are continuously shaping the industry. Innovations in multi-signature capabilities, advanced encryption algorithms, and secure element technology are enhancing the protection against sophisticated cyber threats. The integration of biometric authentication, such as fingerprint scanners and facial recognition, is improving user accessibility without compromising on security. The proliferation of decentralized finance (DeFi) applications also fuels the demand for hardware wallets that can seamlessly and securely interact with these protocols, allowing users to manage their assets across various platforms.

Evolving consumer behaviors underscore a paradigm shift towards self-custody. As users gain more experience with digital assets, there's a growing preference for maintaining control over private keys, a core tenet of cryptocurrency ownership, which hardware wallets facilitate. This trend is amplified by a series of high-profile exchange hacks and security breaches, which have underscored the vulnerabilities of centralized platforms. Consequently, consumers are actively seeking to mitigate these risks by investing in dedicated hardware solutions. The development of more intuitive user interfaces and mobile app integrations is also broadening the appeal of hardware wallets to a wider demographic, including those less technically inclined. The market is also observing a trend towards greater interoperability, with manufacturers striving to ensure their devices support a wider range of cryptocurrencies and blockchain networks.

Key Markets & Segments Leading Crypto Hardware Wallets

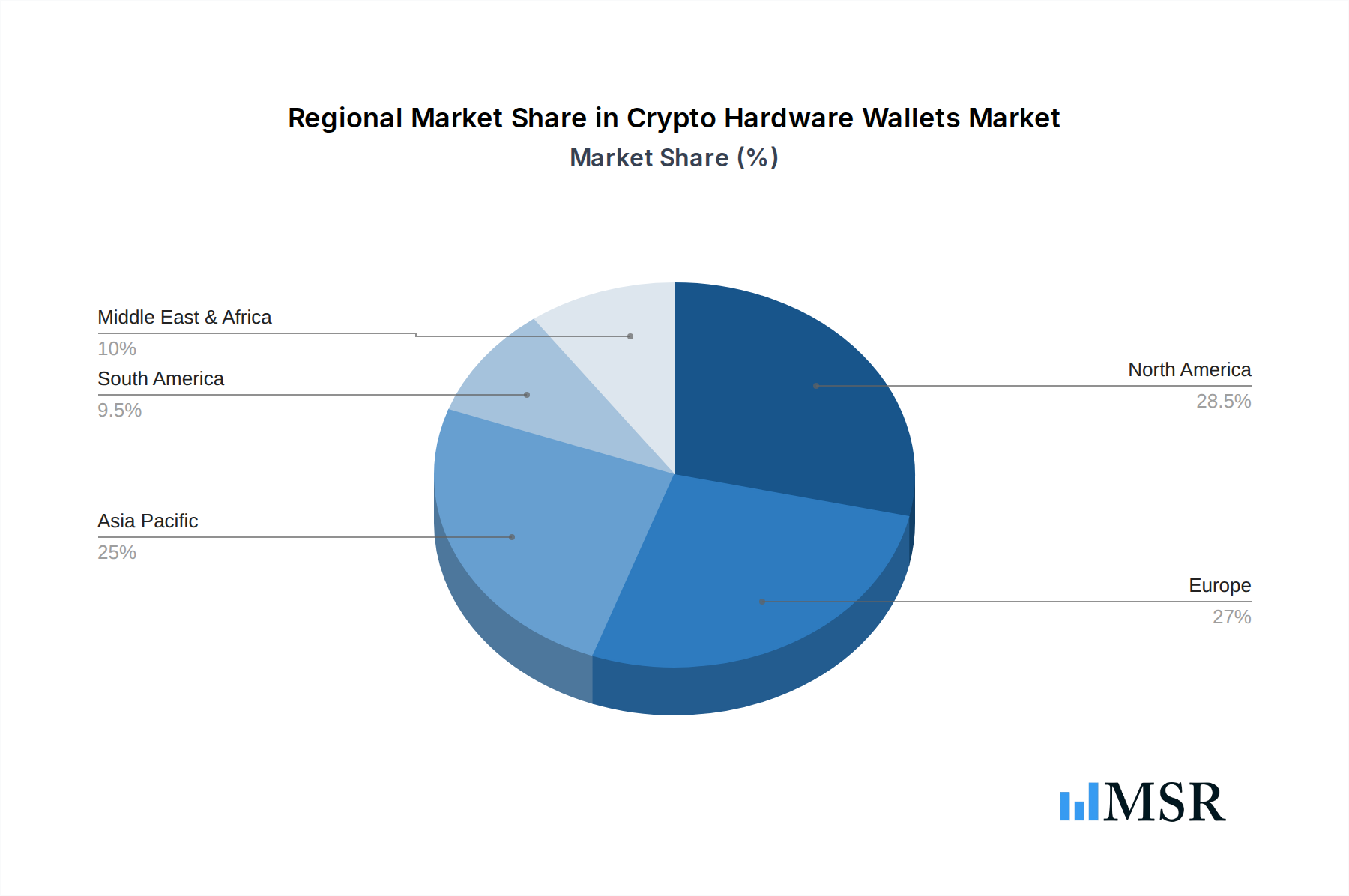

The global crypto hardware wallets market is experiencing robust growth across various regions and segments, driven by a confluence of economic development, technological infrastructure, and regulatory landscapes. North America, particularly the United States, stands as a dominant region, contributing an estimated 35% of the global market share in 2025. This dominance is fueled by a mature cryptocurrency ecosystem, a high concentration of institutional investors, and a significant retail investor base. Favorable regulatory environments, albeit evolving, and strong venture capital funding for blockchain and crypto startups further bolster this leadership.

Within application segments, the Individual user base currently constitutes the largest market share, estimated at 65% in 2025, reflecting the widespread adoption of cryptocurrencies for personal investment and trading. However, the Professionals/Business segment is witnessing accelerated growth, projected to capture 35% of the market by 2033, as more businesses integrate digital assets into their treasury management and investment strategies. This segment demands advanced security features, multi-user access, and enhanced compliance capabilities.

By connectivity type, USB Connectivity Type remains the most prevalent, accounting for an estimated 70% of the market in 2025, owing to its established reliability and widespread compatibility. This is driven by the need for secure and direct interaction with computers for transaction signing. However, Bluetooth Connectivity Type is emerging as a significant growth driver, projected to increase its market share to 20% by 2033. This surge is attributed to the growing demand for mobile-first solutions and enhanced user convenience, enabling seamless integration with smartphones for managing digital assets on the go. NFC Connectivity, while currently holding a smaller market share of approximately 10%, is expected to witness steady growth, driven by its potential for quick, contactless transactions and integration into payment systems.

Drivers for regional and segment dominance include:

- Economic Growth & Disposable Income: Higher economic development in regions like North America and Western Europe correlates with increased disposable income, allowing for investment in cryptocurrencies and their associated security hardware.

- Technological Adoption & Infrastructure: Countries with advanced internet penetration, smartphone adoption, and a burgeoning tech-savvy population tend to exhibit higher demand for crypto hardware wallets.

- Regulatory Clarity & Support: Jurisdictions offering clearer regulatory frameworks and supportive policies for cryptocurrency innovation tend to attract more businesses and investors, thereby boosting the market for hardware wallets.

- Institutional Investor Influx: The increasing allocation of capital by institutional investors into cryptocurrencies necessitates robust, enterprise-grade security solutions, driving demand in the Professionals/Business segment.

- Retail Investor Education & Awareness: Growing public awareness of cryptocurrency security risks, amplified by media coverage and educational initiatives, is a key driver for individual adoption of hardware wallets.

- Rise of Mobile-First & DeFi: The proliferation of mobile-based cryptocurrency services and the rapid expansion of Decentralized Finance (DeFi) are fueling the demand for convenient connectivity options like Bluetooth and potential for NFC integration.

Crypto Hardware Wallets Product Developments

Product development in the crypto hardware wallets sector is characterized by a relentless pursuit of enhanced security, improved user experience, and broader cryptocurrency support. Innovations include the integration of advanced secure element chips, multi-signature capabilities for institutional use, and firmware updates enabling compatibility with a wider array of digital assets and blockchain networks. Companies are also focusing on sleeker form factors, intuitive interfaces, and enhanced physical security features to mitigate risks of tampering and loss. The market relevance is driven by the direct correlation between these advancements and the growing need for secure self-custody solutions in the face of increasing cyber threats.

Challenges in the Crypto Hardware Wallets Market

Despite robust growth, the crypto hardware wallets market faces several challenges. Regulatory uncertainty in various jurisdictions can hinder adoption and investment. Supply chain disruptions, as seen globally, can impact manufacturing and product availability, leading to price volatility. Intense competitive pressures from established players and emerging startups necessitate continuous innovation and competitive pricing strategies. Furthermore, the learning curve for some users, particularly those new to cryptocurrency, can act as a barrier to entry, requiring manufacturers to invest in user education and simplified interfaces. The perceived risk of physical loss or damage to the device also remains a concern for a segment of users.

Forces Driving Crypto Hardware Wallets Growth

The crypto hardware wallets market is propelled by a powerful combination of technological advancements, economic shifts, and evolving regulatory landscapes. The increasing mainstream adoption of cryptocurrencies, driven by institutional interest and growing retail participation, is a primary catalyst. This surge in adoption necessitates robust security measures to protect digital assets from the growing threat of cyberattacks. Furthermore, the maturation of blockchain technology and the expansion of decentralized finance (DeFi) ecosystems create a greater need for secure and user-friendly hardware solutions that can seamlessly interact with these platforms. Regulatory clarity in some key markets also provides a more conducive environment for growth.

Challenges in the Crypto Hardware Wallets Market

The long-term growth catalysts for the crypto hardware wallets market lie in continuous innovation and strategic market expansion. The development of next-generation security protocols, potentially incorporating quantum-resistant cryptography, will be crucial to address future threats. Partnerships with cryptocurrency exchanges, DeFi platforms, and financial institutions can expand distribution channels and enhance product integration. Market expansion into emerging economies with rapidly growing cryptocurrency adoption will unlock significant new user bases. Furthermore, the development of specialized hardware wallets tailored for specific use cases, such as enterprise-level solutions or integrated payment devices, will foster sustained demand.

Emerging Opportunities in Crypto Hardware Wallets

Emerging opportunities in the crypto hardware wallets market are abundant, driven by technological innovation and evolving consumer preferences. The integration of hardware wallets with Web3 applications and the metaverse presents a significant growth avenue, enabling secure access and management of digital assets within these immersive environments. The development of specialized hardware for institutional investors, offering enhanced compliance features and multi-custodian solutions, represents a high-value market. Furthermore, the potential for hardware wallets to serve as secure identity management tools beyond just cryptocurrencies, and their integration into broader digital security ecosystems, offers substantial long-term growth prospects. The growing demand for eco-friendly and sustainable hardware wallet designs also presents an untapped niche.

Leading Players in the Crypto Hardware Wallets Sector

- Ledger

- Trezor

- KeepKey

- Digital BitBox

- Coinkite

- BitLox

- CoolWallet

- CryoBit

- ELLIPAL

- Keystone

- OneKey

- imkey

- SafePal

Key Milestones in Crypto Hardware Wallets Industry

- 2019: Increased awareness of hardware wallet benefits following major exchange hacks.

- 2020: Trezor Model T gains significant traction for its touchscreen interface and broader coin support.

- 2021: Ledger Nano S Plus launch, offering enhanced security and improved usability for a wider range of cryptocurrencies.

- 2022: Emergence of multi-signature hardware wallets for institutional investors.

- 2023: Increased focus on Bluetooth connectivity and mobile app integration for enhanced user convenience.

- 2024: Growing adoption of advanced security features like secure element chips and passphrases becoming standard.

- 2025 (Estimated): Further integration with DeFi protocols and Web3 applications becomes a key feature.

- 2026 (Projected): Introduction of more eco-friendly and sustainable hardware wallet designs.

- 2027 (Projected): Potential for early adoption of quantum-resistant cryptographic solutions.

- 2028-2033 (Projected): Maturation of the market with specialized wallets for niche applications and wider integration into digital identity solutions.

Strategic Outlook for Crypto Hardware Wallets Market

The strategic outlook for the crypto hardware wallets market is exceptionally bright, poised for sustained expansion fueled by technological innovation and increasing cryptocurrency adoption. Growth accelerators include the ongoing mainstreaming of digital assets, the burgeoning DeFi and NFT markets, and the rising demand for robust self-custody solutions among both retail and institutional users. Companies that focus on enhancing user experience, expanding multi-currency support, and investing in cutting-edge security features will be best positioned for success. Strategic partnerships with exchanges, payment processors, and emerging Web3 platforms will be critical for market penetration and growth. The market also presents opportunities for diversification into related security services and digital identity management solutions.

Crypto Hardware Wallets Segmentation

-

1. Application

- 1.1. Individual

- 1.2. Professionals/Business

-

2. Types

- 2.1. USB Connectivity Type

- 2.2. Bluetooth Connectivity Type

- 2.3. NFC Connectivity

Crypto Hardware Wallets Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Crypto Hardware Wallets Regional Market Share

Geographic Coverage of Crypto Hardware Wallets

Crypto Hardware Wallets REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Individual

- 5.1.2. Professionals/Business

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. USB Connectivity Type

- 5.2.2. Bluetooth Connectivity Type

- 5.2.3. NFC Connectivity

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Crypto Hardware Wallets Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Individual

- 6.1.2. Professionals/Business

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. USB Connectivity Type

- 6.2.2. Bluetooth Connectivity Type

- 6.2.3. NFC Connectivity

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Crypto Hardware Wallets Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Individual

- 7.1.2. Professionals/Business

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. USB Connectivity Type

- 7.2.2. Bluetooth Connectivity Type

- 7.2.3. NFC Connectivity

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Crypto Hardware Wallets Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Individual

- 8.1.2. Professionals/Business

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. USB Connectivity Type

- 8.2.2. Bluetooth Connectivity Type

- 8.2.3. NFC Connectivity

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Crypto Hardware Wallets Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Individual

- 9.1.2. Professionals/Business

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. USB Connectivity Type

- 9.2.2. Bluetooth Connectivity Type

- 9.2.3. NFC Connectivity

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Crypto Hardware Wallets Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Individual

- 10.1.2. Professionals/Business

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. USB Connectivity Type

- 10.2.2. Bluetooth Connectivity Type

- 10.2.3. NFC Connectivity

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Crypto Hardware Wallets Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Individual

- 11.1.2. Professionals/Business

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. USB Connectivity Type

- 11.2.2. Bluetooth Connectivity Type

- 11.2.3. NFC Connectivity

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Ledger

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Trezor

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 KeepKey

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Digital BitBox

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Coinkite

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 BitLox

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 CoolWallet

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 CryoBit

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 ELLIPAL

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Keystone

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 OneKey

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 imkey

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 SafePal

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.1 Ledger

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Crypto Hardware Wallets Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global Crypto Hardware Wallets Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Crypto Hardware Wallets Revenue (undefined), by Application 2025 & 2033

- Figure 4: North America Crypto Hardware Wallets Volume (K), by Application 2025 & 2033

- Figure 5: North America Crypto Hardware Wallets Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Crypto Hardware Wallets Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Crypto Hardware Wallets Revenue (undefined), by Types 2025 & 2033

- Figure 8: North America Crypto Hardware Wallets Volume (K), by Types 2025 & 2033

- Figure 9: North America Crypto Hardware Wallets Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Crypto Hardware Wallets Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Crypto Hardware Wallets Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America Crypto Hardware Wallets Volume (K), by Country 2025 & 2033

- Figure 13: North America Crypto Hardware Wallets Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Crypto Hardware Wallets Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Crypto Hardware Wallets Revenue (undefined), by Application 2025 & 2033

- Figure 16: South America Crypto Hardware Wallets Volume (K), by Application 2025 & 2033

- Figure 17: South America Crypto Hardware Wallets Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Crypto Hardware Wallets Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Crypto Hardware Wallets Revenue (undefined), by Types 2025 & 2033

- Figure 20: South America Crypto Hardware Wallets Volume (K), by Types 2025 & 2033

- Figure 21: South America Crypto Hardware Wallets Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Crypto Hardware Wallets Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Crypto Hardware Wallets Revenue (undefined), by Country 2025 & 2033

- Figure 24: South America Crypto Hardware Wallets Volume (K), by Country 2025 & 2033

- Figure 25: South America Crypto Hardware Wallets Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Crypto Hardware Wallets Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Crypto Hardware Wallets Revenue (undefined), by Application 2025 & 2033

- Figure 28: Europe Crypto Hardware Wallets Volume (K), by Application 2025 & 2033

- Figure 29: Europe Crypto Hardware Wallets Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Crypto Hardware Wallets Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Crypto Hardware Wallets Revenue (undefined), by Types 2025 & 2033

- Figure 32: Europe Crypto Hardware Wallets Volume (K), by Types 2025 & 2033

- Figure 33: Europe Crypto Hardware Wallets Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Crypto Hardware Wallets Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Crypto Hardware Wallets Revenue (undefined), by Country 2025 & 2033

- Figure 36: Europe Crypto Hardware Wallets Volume (K), by Country 2025 & 2033

- Figure 37: Europe Crypto Hardware Wallets Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Crypto Hardware Wallets Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Crypto Hardware Wallets Revenue (undefined), by Application 2025 & 2033

- Figure 40: Middle East & Africa Crypto Hardware Wallets Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Crypto Hardware Wallets Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Crypto Hardware Wallets Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Crypto Hardware Wallets Revenue (undefined), by Types 2025 & 2033

- Figure 44: Middle East & Africa Crypto Hardware Wallets Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Crypto Hardware Wallets Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Crypto Hardware Wallets Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Crypto Hardware Wallets Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East & Africa Crypto Hardware Wallets Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Crypto Hardware Wallets Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Crypto Hardware Wallets Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Crypto Hardware Wallets Revenue (undefined), by Application 2025 & 2033

- Figure 52: Asia Pacific Crypto Hardware Wallets Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Crypto Hardware Wallets Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Crypto Hardware Wallets Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Crypto Hardware Wallets Revenue (undefined), by Types 2025 & 2033

- Figure 56: Asia Pacific Crypto Hardware Wallets Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Crypto Hardware Wallets Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Crypto Hardware Wallets Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Crypto Hardware Wallets Revenue (undefined), by Country 2025 & 2033

- Figure 60: Asia Pacific Crypto Hardware Wallets Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Crypto Hardware Wallets Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Crypto Hardware Wallets Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Crypto Hardware Wallets Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Crypto Hardware Wallets Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Crypto Hardware Wallets Revenue undefined Forecast, by Types 2020 & 2033

- Table 4: Global Crypto Hardware Wallets Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Crypto Hardware Wallets Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Global Crypto Hardware Wallets Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Crypto Hardware Wallets Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: Global Crypto Hardware Wallets Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Crypto Hardware Wallets Revenue undefined Forecast, by Types 2020 & 2033

- Table 10: Global Crypto Hardware Wallets Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Crypto Hardware Wallets Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Global Crypto Hardware Wallets Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United States Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Mexico Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Crypto Hardware Wallets Revenue undefined Forecast, by Application 2020 & 2033

- Table 20: Global Crypto Hardware Wallets Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Crypto Hardware Wallets Revenue undefined Forecast, by Types 2020 & 2033

- Table 22: Global Crypto Hardware Wallets Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Crypto Hardware Wallets Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: Global Crypto Hardware Wallets Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Brazil Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Argentina Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Crypto Hardware Wallets Revenue undefined Forecast, by Application 2020 & 2033

- Table 32: Global Crypto Hardware Wallets Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Crypto Hardware Wallets Revenue undefined Forecast, by Types 2020 & 2033

- Table 34: Global Crypto Hardware Wallets Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Crypto Hardware Wallets Revenue undefined Forecast, by Country 2020 & 2033

- Table 36: Global Crypto Hardware Wallets Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 40: Germany Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: France Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: Italy Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Spain Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: Russia Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Benelux Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: Nordics Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Crypto Hardware Wallets Revenue undefined Forecast, by Application 2020 & 2033

- Table 56: Global Crypto Hardware Wallets Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Crypto Hardware Wallets Revenue undefined Forecast, by Types 2020 & 2033

- Table 58: Global Crypto Hardware Wallets Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Crypto Hardware Wallets Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: Global Crypto Hardware Wallets Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 62: Turkey Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 64: Israel Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 66: GCC Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 68: North Africa Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 70: South Africa Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Crypto Hardware Wallets Revenue undefined Forecast, by Application 2020 & 2033

- Table 74: Global Crypto Hardware Wallets Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Crypto Hardware Wallets Revenue undefined Forecast, by Types 2020 & 2033

- Table 76: Global Crypto Hardware Wallets Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Crypto Hardware Wallets Revenue undefined Forecast, by Country 2020 & 2033

- Table 78: Global Crypto Hardware Wallets Volume K Forecast, by Country 2020 & 2033

- Table 79: China Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 80: China Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 82: India Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 84: Japan Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 86: South Korea Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 90: Oceania Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Crypto Hardware Wallets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Crypto Hardware Wallets Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Crypto Hardware Wallets?

The projected CAGR is approximately 9.3%.

2. Which companies are prominent players in the Crypto Hardware Wallets?

Key companies in the market include Ledger, Trezor, KeepKey, Digital BitBox, Coinkite, BitLox, CoolWallet, CryoBit, ELLIPAL, Keystone, OneKey, imkey, SafePal.

3. What are the main segments of the Crypto Hardware Wallets?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Crypto Hardware Wallets," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Crypto Hardware Wallets report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Crypto Hardware Wallets?

To stay informed about further developments, trends, and reports in the Crypto Hardware Wallets, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence