Key Insights

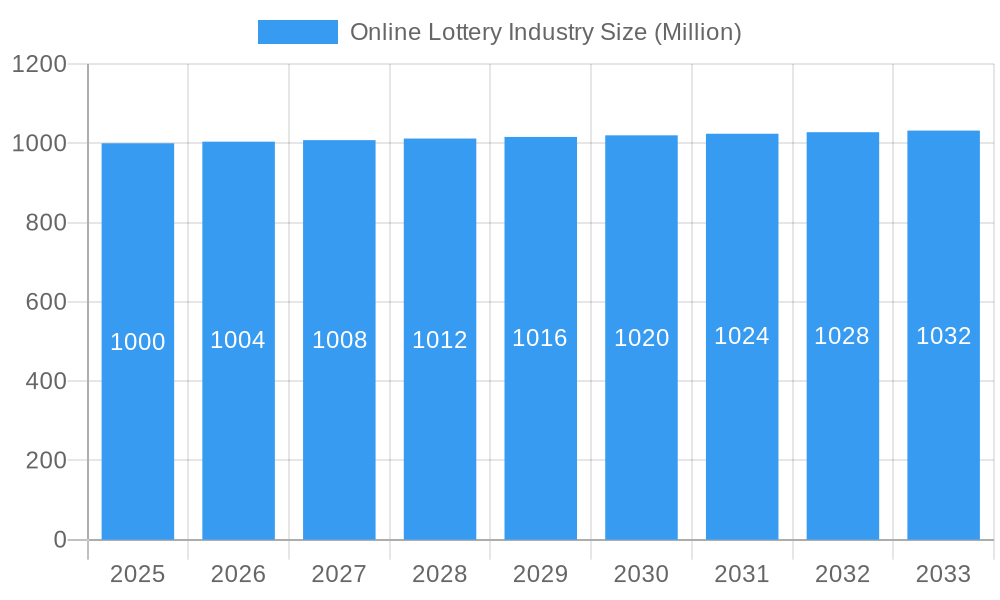

The global Online Lottery market is experiencing robust expansion, driven by increasing digital literacy, widespread smartphone adoption, and the enhanced convenience offered by online platforms. Valued at $19.43 billion in 2025, the market is poised for significant growth, projecting a compelling 9.5% CAGR from 2025 to 2033. This impressive trajectory is fueled by several key factors, including the continuous innovation in game offerings across Draw-Based Games, Instant Win Games, and Sports Games, catering to a diverse player base. The seamless accessibility via mobile platforms, coupled with the increasing preference for secure and varied payment modes such as Credit/Debit Cards, E-Wallets, Bank Transfers, and the burgeoning acceptance of Cryptocurrency, further propels market expansion. This digital transformation makes online lottery an attractive and easily accessible form of entertainment for individual players and lottery syndicates alike, pushing the industry to new heights.

Online Lottery Industry Market Size (In Billion)

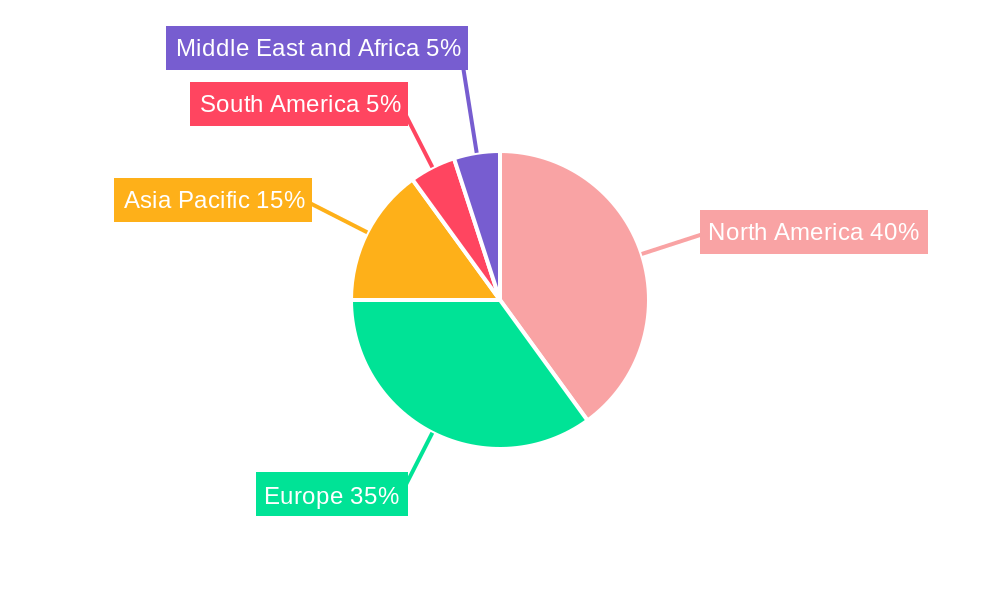

Looking ahead, the Online Lottery market is characterized by dynamic trends and a competitive landscape. Emerging trends include the integration of artificial intelligence for personalized gaming experiences, the gamification of traditional lottery formats to boost engagement, and the growing incorporation of social features allowing players to connect. While the market thrives on innovation and convenience, it also navigates certain challenges, including evolving regulatory frameworks across different regions, concerns related to responsible gaming, and the constant need for robust cybersecurity measures to protect player data and financial transactions. Leading companies such as Lotto Direct Limited, Camelot Group, Lottoland, ZEAL Network SE, and Française des Jeux are at the forefront of this evolution, continually introducing new platforms and services. Geographically, North America and Europe remain mature markets with high adoption rates, while the Asia Pacific, South America, and Middle East & Africa regions are witnessing accelerated growth, attributed to increasing internet penetration and a rising disposable income, underscoring the global appeal and promising future of the online lottery sector.

Online Lottery Industry Company Market Share

Online Lottery Industry: Unlocking Billion-Dollar Growth Opportunities and Strategic Insights (2019-2033)

Drive your strategic decisions with our comprehensive report on the dynamic Online Lottery Industry. This meticulously researched analysis provides an in-depth exploration of the global online lottery market, projected to achieve significant valuation by 2033. Discover pivotal market trends, forecast lucrative growth opportunities, and gain actionable intelligence on the competitive landscape shaping this rapidly evolving sector. From the surge in mobile gaming to the integration of cryptocurrency payments and the expansion of instant win games, our report illuminates the forces driving digital transformation in lottery, offering unparalleled insights for investors, operators, and technology providers. Navigate the complex regulatory frameworks and capitalize on emerging markets with data-backed foresight.

Online Lottery Industry Market Concentration & Dynamics

The Online Lottery Industry is characterized by a mix of established giants and agile innovators, with market concentration demonstrating a moderate to high degree. Leading players such as Lotto Direct Limited, Camelot Group, Lottoland, ZEAL Network SE, and Française des Jeux command a substantial portion of the global revenue, collectively holding an estimated xx billion market share driven by extensive brand recognition, robust digital platforms, and diversified game portfolios including popular draw-based and instant win offerings. Innovation ecosystems are vibrant, with continuous investment in mobile-first designs, augmented reality experiences, and enhanced user interfaces to attract a broader demographic and retain existing players. For instance, the integration of gamification elements and social features aims to create more engaging experiences beyond traditional lottery formats.

Regulatory frameworks play a critical role in shaping market dynamics, varying significantly across different jurisdictions. Strict licensing requirements and responsible gaming mandates can act as barriers to entry, while favorable regulations in regions like Europe and certain parts of Asia Pacific foster growth. The emergence of substitute products, particularly from the broader online gambling and sports betting sectors, presents a competitive pressure, pushing online lottery operators to innovate and offer unique value propositions. However, the allure of large jackpots and the inherent simplicity of lottery games often ensure a distinct appeal. End-user trends show a clear shift towards mobile platforms, with a significant preference for convenient, on-the-go play and diverse payment options, including e-wallets and, increasingly, cryptocurrency.

Mergers and acquisitions (M&A) activities are strategic tools for market expansion and consolidation, evidenced by several key deals in the historical period. Companies are actively pursuing acquisitions to expand geographical reach, integrate new technologies, or absorb smaller, innovative players. For example, the expansion efforts of ZEAL Network SE into new international markets reflect an inorganic growth strategy to bolster its position. Over the past few years, the industry has seen over xx billion in M&A deals, signaling a drive towards market consolidation and the strategic acquisition of technology and customer bases. This dynamic environment necessitates continuous adaptation and innovation for companies aiming to maintain or grow their market presence. The competitive intensity is further heightened by the constant development of new game types and the strategic partnerships formed between technology providers and lottery operators, creating a complex web of alliances and rivalries that define the industry's evolving landscape.

Online Lottery Industry Industry Insights & Trends

The Online Lottery Industry is undergoing a profound transformation, driven by an confluence of technological advancements, evolving consumer behaviors, and strategic market developments. The global online lottery market was valued at an estimated xx billion in the base year 2025 and is projected to exhibit a robust Compound Annual Growth Rate (CAGR) of xx% from 2025 to 2033, reaching a market size of xx billion by the end of the forecast period. This significant growth is primarily fueled by the accelerating digital transformation across industries, making online platforms the preferred channel for entertainment and transactions. The omnipresence of smartphones and improving internet penetration globally have democratized access to online lottery games, shifting traditional retail-based play to digital environments. Mobile platforms are emerging as the dominant access point, driven by convenience and the ability to play anytime, anywhere.

Technological disruptions are at the heart of the industry's evolution. Artificial Intelligence (AI) and Machine Learning (ML) are increasingly being leveraged for personalized user experiences, fraud detection, and optimized game development, enhancing player engagement and operational efficiency. Blockchain technology is also gaining traction, particularly in offering enhanced transparency, security, and the potential for new types of decentralized lottery games, attracting a niche but growing segment of players. Furthermore, the adoption of advanced data analytics allows operators to understand consumer preferences better, enabling targeted marketing campaigns and the development of highly customized game offerings that resonate with specific demographics. This data-driven approach is crucial for optimizing player acquisition and retention strategies in a competitive environment.

Evolving consumer behaviors are another critical growth driver. Younger demographics, particularly millennials and Gen Z, are digital natives who prefer online interactions and expect seamless digital experiences. Their preference for instant gratification fuels the demand for instant win games and quick play options, while social gaming elements and community features are also gaining popularity. The increased awareness and acceptance of online payment methods, including the burgeoning use of e-wallets and cryptocurrency, further facilitate online lottery participation by providing convenient and secure transaction options. Moreover, the global pandemic significantly accelerated the shift towards online entertainment, reinforcing the habit of digital engagement for many consumers and providing a long-term tailwind for the online lottery sector. The integration of online lotteries with other forms of digital entertainment, such as online casinos and sports betting platforms, is also broadening the appeal and accessibility of these games, creating a holistic digital gaming ecosystem that caters to diverse consumer preferences. This continuous innovation and responsiveness to consumer needs are essential for sustaining the industry's impressive growth trajectory.

Key Markets & Segments Leading Online Lottery Industry

Within the Online Lottery Industry, several key markets and segments demonstrate significant leadership and growth potential. Geographically, Europe remains the dominant region, commanding an estimated xx billion in market value. This dominance is driven by a combination of mature regulatory frameworks, high internet penetration, a culturally ingrained lottery tradition, and the presence of numerous established operators like Camelot Group (UK), Française des Jeux (France), and ZEAL Network SE (Germany). The region has also been at the forefront of adopting digital platforms for lottery sales, with countries like the UK, France, and Germany consistently showing high levels of online participation.

- Economic Growth: Strong economies in key European countries provide disposable income, fueling participation in leisure activities like online lotteries.

- Technological Infrastructure: Advanced digital infrastructure, including widespread high-speed internet and mobile penetration, supports seamless online gaming experiences.

- Favorable Regulatory Environments: While strict, European regulations often provide a stable and secure environment for online lottery operations, fostering consumer trust and market growth.

- High Digital Adoption: A tech-savvy population accustomed to online transactions and entertainment drives the shift from traditional to digital lottery channels.

Among the Game Type segments, Draw-Based Games continue to hold the largest market share, valued at an estimated xx billion. Traditional appeal, coupled with the allure of massive jackpots from games like Powerball and Mega Millions, translates effectively into the online sphere. These games benefit from established brand recognition and widespread marketing, attracting both seasoned players and newcomers. However, Instant Win Games are rapidly gaining traction, projected to grow at the highest CAGR of xx% during the forecast period. Their immediate gratification and diverse themes appeal to modern players seeking quick entertainment and faster results, making them a significant growth driver.

In terms of Platform, Mobile gaming has unequivocally emerged as the leading segment, capturing an estimated xx billion of the market. The convenience of playing on smartphones and tablets has revolutionized access, allowing players to engage with lottery games anytime, anywhere. This segment's growth is propelled by smartphone ubiquity, advancements in mobile app technology, and improved mobile payment integration. The Desktop platform, while still significant, is experiencing slower growth as users increasingly transition to mobile devices for their online activities.

For Payment Mode, Credit/Debit Cards remain the most widely used option, accounting for an estimated xx billion due to their universal acceptance and ease of use. However, E-Wallets are rapidly growing in popularity, expected to register a CAGR of xx%, as they offer enhanced security, faster transactions, and seamless integration with mobile platforms. The increasing acceptance of Cryptocurrency as a payment option, though currently a smaller segment (valued at xx billion), represents an exciting emerging trend, appealing to tech-savvy users and offering benefits like anonymity and reduced transaction fees, as seen with initiatives like Crypto Millions Lotto.

Lastly, the End User segment is dominated by Individual Players, who represent the vast majority of online lottery participants, contributing an estimated xx billion to the market. Their individual pursuit of jackpots forms the bedrock of the industry. Lottery Syndicates, while a smaller segment, are also growing, particularly online, as digital platforms facilitate group play and prize sharing, offering a collective approach to increasing winning odds. This blend of individual aspiration and community participation underscores the diverse engagement models within the online lottery landscape.

Online Lottery Industry Product Developments

Product innovations are a cornerstone of the Online Lottery Industry's competitive edge, focusing heavily on enhancing user experience and diversifying game offerings. Technological advancements like virtual reality (VR) integration for immersive gameplay, augmented reality (AR) for interactive lottery tickets, and advanced graphics for instant win games are shaping the future. Operators are continually launching new game types, including innovative quizzes and sports-themed games, to appeal to a broader audience. For instance, the expansion of instant win game portfolios by companies like ZEAL Network SE demonstrates a clear trend towards rapid engagement and diverse themes. These developments not only drive player acquisition and retention but also open new revenue streams, reinforcing the industry's dynamic and forward-looking approach to digital entertainment.

Challenges in the Online Lottery Industry Market

The Online Lottery Industry faces significant barriers that could impede its projected growth. Regulatory hurdles represent a primary challenge, with varying and often stringent legal frameworks across different jurisdictions leading to market fragmentation and complexity for international operators. Compliance costs, licensing fees, and advertising restrictions can be substantial, impacting profitability and market entry for new players. Supply chain issues, though less direct than in physical goods, can manifest as challenges in securing robust payment gateway integrations or reliable technology partners in certain regions. Intense competitive pressures from other online gambling sectors, such as sports betting and casino games, force lottery operators to constantly innovate to retain player attention and market share, potentially leading to increased marketing expenditures and reduced margins. For example, navigating the patchwork of global regulations can result in an estimated xx billion in compliance costs annually for major players, hindering seamless cross-border operations.

Forces Driving Online Lottery Industry Growth

The Online Lottery Industry's growth is propelled by several powerful forces. Technologically, the pervasive adoption of mobile devices and enhanced internet accessibility are primary drivers, enabling convenient play from any location. Innovations in user interface (UI) and user experience (UX) design, coupled with advanced data analytics, provide personalized gaming experiences that boost engagement. Economically, rising disposable incomes in emerging markets and the increasing digitalization of financial transactions contribute significantly to market expansion. The convenience of diverse payment modes, including e-wallets and cryptocurrency, further lowers participation barriers. Regulatory factors, particularly the legalization and regulation of online lottery in new jurisdictions, unlock previously untapped markets, providing significant growth opportunities for operators to expand their footprint globally and attract new player bases.

Challenges in the Online Lottery Industry Market

Despite facing market challenges, long-term growth catalysts in the Online Lottery Industry are robust, emphasizing innovation, strategic partnerships, and market expansions. Continuous investment in technological advancements, such as AI-driven personalization and blockchain for enhanced transparency, will redefine player experiences and build trust, fostering sustained engagement. Strategic alliances between lottery operators and technology providers, or even media companies, can unlock new distribution channels and marketing synergies, expanding reach to broader audiences. Furthermore, the ongoing legalization and regulation of online lottery services in previously untapped or underserved markets, particularly in Asia Pacific and Latin America, present significant opportunities for geographical expansion and new player acquisition, underpinning a strong trajectory for future growth.

Emerging Opportunities in Online Lottery Industry

The Online Lottery Industry is ripe with emerging opportunities that promise substantial growth. One key trend is the exploration of new geographical markets, particularly in regions where internet penetration is rapidly increasing and regulatory frameworks are evolving to permit online lottery operations. The integration of advanced technologies like virtual reality (VR) and augmented reality (AR) is creating highly immersive and engaging game experiences, attracting a new generation of tech-savvy players. Moreover, evolving consumer preferences for instant gratification and personalized content are driving demand for innovative instant win games and customizable lottery options. The increasing acceptance of cryptocurrency as a payment method also presents a nascent but significant opportunity for operators to cater to a new demographic and leverage the benefits of decentralized transactions. These opportunities underscore the industry's potential for diversification and expansion.

Leading Players in the Online Lottery Industry Sector

- Lotto Direct Limited

- Camelot Group

- Lottoland

- Lotto Agent

- LottoKings

- WinTrillions

- Lotto

- ZEAL Network SE

- Française des Jeux

- Annexio Limited

- Others

Key Milestones in Online Lottery Industry Industry

- October 2022: ZEAL Network SE expanded its games business internationally by collaborating with American online lottery provider Park Avenue Gaming. This strategic move integrated Zeal's online instant games into Park Avenue Gaming's video lottery terminal business in Argentina and its online platforms in Peru, significantly expanding Zeal's global footprint and diversifying its revenue streams in Latin American markets.

- February 2022: ZEAL Network SE forged a partnership with Lotto Hessian for instant win games. Through this collaboration, Zeal provided Lotto Hessian with 15 state lottery online games, including popular formats like crosswords, bingo, and a world cup themed game. This partnership enhanced Lotto Hessian's digital offerings and reinforced Zeal's position as a leading provider of instant win lottery content within the German market.

- December 2021: Crypto Millions Lotto announced the launch of four new lottery games on its official website. This expansion included two India-based games, India Fantasy 5 and India Million Lotto, catering to a burgeoning Asian market, alongside two US-based games, Powerball+ and Mega Millions+. These launches highlighted the growing trend of integrating cryptocurrency with popular lottery formats and expanding market reach into key geographical regions.

Strategic Outlook for Online Lottery Industry Market

The strategic outlook for the Online Lottery Industry market is exceedingly positive, driven by strong growth accelerators that promise substantial future market potential. Continuous technological innovation, including AI-driven personalization and the expanded use of blockchain, will be crucial for maintaining a competitive edge and fostering deeper player engagement. Strategic opportunities lie in targeted geographical expansion into developing markets with increasing internet penetration and evolving regulatory landscapes. Furthermore, forging strategic partnerships with payment providers, technology developers, and even media companies can unlock new distribution channels and marketing synergies, effectively broadening market reach. Investing in a diverse portfolio of game types, particularly instant win games and novel interactive experiences, will cater to evolving consumer preferences and secure long-term player loyalty, driving sustained revenue growth for the industry.

Online Lottery Industry Segmentation

-

1. Game Type

- 1.1. Draw-Based Games

- 1.2. Instant Win Games

- 1.3. Sports Games

- 1.4. Quizzes Games

- 1.5. Others

-

2. Platform

- 2.1. Desktop

- 2.2. Mobile

-

3. Payment Mode

- 3.1. Credit/Debit Cards

- 3.2. E-Wallets

- 3.3. Bank Transfers

- 3.4. Cryptocurrency

- 3.5. Others

-

4. End User

- 4.1. Individual Players

- 4.2. Lottery Syndicates

Online Lottery Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Rest of North America

-

2. Europe

- 2.1. Spain

- 2.2. United Kingdom

- 2.3. Germany

- 2.4. France

- 2.5. Italy

- 2.6. Sweden

- 2.7. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. Australia

- 3.5. Rest of Asia Pacific

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. South Africa

- 5.2. United Arab Emirates

- 5.3. Rest of Middle East and Africa

Online Lottery Industry Regional Market Share

Geographic Coverage of Online Lottery Industry

Online Lottery Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Game Type

- 5.1.1. Draw-Based Games

- 5.1.2. Instant Win Games

- 5.1.3. Sports Games

- 5.1.4. Quizzes Games

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Platform

- 5.2.1. Desktop

- 5.2.2. Mobile

- 5.3. Market Analysis, Insights and Forecast - by Payment Mode

- 5.3.1. Credit/Debit Cards

- 5.3.2. E-Wallets

- 5.3.3. Bank Transfers

- 5.3.4. Cryptocurrency

- 5.3.5. Others

- 5.4. Market Analysis, Insights and Forecast - by End User

- 5.4.1. Individual Players

- 5.4.2. Lottery Syndicates

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. Europe

- 5.5.3. Asia Pacific

- 5.5.4. South America

- 5.5.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Game Type

- 6. Global Online Lottery Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Game Type

- 6.1.1. Draw-Based Games

- 6.1.2. Instant Win Games

- 6.1.3. Sports Games

- 6.1.4. Quizzes Games

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Platform

- 6.2.1. Desktop

- 6.2.2. Mobile

- 6.3. Market Analysis, Insights and Forecast - by Payment Mode

- 6.3.1. Credit/Debit Cards

- 6.3.2. E-Wallets

- 6.3.3. Bank Transfers

- 6.3.4. Cryptocurrency

- 6.3.5. Others

- 6.4. Market Analysis, Insights and Forecast - by End User

- 6.4.1. Individual Players

- 6.4.2. Lottery Syndicates

- 6.1. Market Analysis, Insights and Forecast - by Game Type

- 7. North America Online Lottery Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Game Type

- 7.1.1. Draw-Based Games

- 7.1.2. Instant Win Games

- 7.1.3. Sports Games

- 7.1.4. Quizzes Games

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Platform

- 7.2.1. Desktop

- 7.2.2. Mobile

- 7.3. Market Analysis, Insights and Forecast - by Payment Mode

- 7.3.1. Credit/Debit Cards

- 7.3.2. E-Wallets

- 7.3.3. Bank Transfers

- 7.3.4. Cryptocurrency

- 7.3.5. Others

- 7.4. Market Analysis, Insights and Forecast - by End User

- 7.4.1. Individual Players

- 7.4.2. Lottery Syndicates

- 7.1. Market Analysis, Insights and Forecast - by Game Type

- 8. Europe Online Lottery Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Game Type

- 8.1.1. Draw-Based Games

- 8.1.2. Instant Win Games

- 8.1.3. Sports Games

- 8.1.4. Quizzes Games

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Platform

- 8.2.1. Desktop

- 8.2.2. Mobile

- 8.3. Market Analysis, Insights and Forecast - by Payment Mode

- 8.3.1. Credit/Debit Cards

- 8.3.2. E-Wallets

- 8.3.3. Bank Transfers

- 8.3.4. Cryptocurrency

- 8.3.5. Others

- 8.4. Market Analysis, Insights and Forecast - by End User

- 8.4.1. Individual Players

- 8.4.2. Lottery Syndicates

- 8.1. Market Analysis, Insights and Forecast - by Game Type

- 9. Asia Pacific Online Lottery Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Game Type

- 9.1.1. Draw-Based Games

- 9.1.2. Instant Win Games

- 9.1.3. Sports Games

- 9.1.4. Quizzes Games

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Platform

- 9.2.1. Desktop

- 9.2.2. Mobile

- 9.3. Market Analysis, Insights and Forecast - by Payment Mode

- 9.3.1. Credit/Debit Cards

- 9.3.2. E-Wallets

- 9.3.3. Bank Transfers

- 9.3.4. Cryptocurrency

- 9.3.5. Others

- 9.4. Market Analysis, Insights and Forecast - by End User

- 9.4.1. Individual Players

- 9.4.2. Lottery Syndicates

- 9.1. Market Analysis, Insights and Forecast - by Game Type

- 10. South America Online Lottery Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Game Type

- 10.1.1. Draw-Based Games

- 10.1.2. Instant Win Games

- 10.1.3. Sports Games

- 10.1.4. Quizzes Games

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Platform

- 10.2.1. Desktop

- 10.2.2. Mobile

- 10.3. Market Analysis, Insights and Forecast - by Payment Mode

- 10.3.1. Credit/Debit Cards

- 10.3.2. E-Wallets

- 10.3.3. Bank Transfers

- 10.3.4. Cryptocurrency

- 10.3.5. Others

- 10.4. Market Analysis, Insights and Forecast - by End User

- 10.4.1. Individual Players

- 10.4.2. Lottery Syndicates

- 10.1. Market Analysis, Insights and Forecast - by Game Type

- 11. Middle East and Africa Online Lottery Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Game Type

- 11.1.1. Draw-Based Games

- 11.1.2. Instant Win Games

- 11.1.3. Sports Games

- 11.1.4. Quizzes Games

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by Platform

- 11.2.1. Desktop

- 11.2.2. Mobile

- 11.3. Market Analysis, Insights and Forecast - by Payment Mode

- 11.3.1. Credit/Debit Cards

- 11.3.2. E-Wallets

- 11.3.3. Bank Transfers

- 11.3.4. Cryptocurrency

- 11.3.5. Others

- 11.4. Market Analysis, Insights and Forecast - by End User

- 11.4.1. Individual Players

- 11.4.2. Lottery Syndicates

- 11.1. Market Analysis, Insights and Forecast - by Game Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Lotto Direct Limited

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Camelot Group

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Lottoland

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Lotto Agent

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 LottoKings

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 WinTrillions

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Lotto

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 ZEAL Network SE

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Française des Jeux

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Annexio Limited

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Others

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Lotto Direct Limited

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Online Lottery Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Online Lottery Industry Revenue (billion), by Game Type 2025 & 2033

- Figure 3: North America Online Lottery Industry Revenue Share (%), by Game Type 2025 & 2033

- Figure 4: North America Online Lottery Industry Revenue (billion), by Platform 2025 & 2033

- Figure 5: North America Online Lottery Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 6: North America Online Lottery Industry Revenue (billion), by Payment Mode 2025 & 2033

- Figure 7: North America Online Lottery Industry Revenue Share (%), by Payment Mode 2025 & 2033

- Figure 8: North America Online Lottery Industry Revenue (billion), by End User 2025 & 2033

- Figure 9: North America Online Lottery Industry Revenue Share (%), by End User 2025 & 2033

- Figure 10: North America Online Lottery Industry Revenue (billion), by Country 2025 & 2033

- Figure 11: North America Online Lottery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 12: Europe Online Lottery Industry Revenue (billion), by Game Type 2025 & 2033

- Figure 13: Europe Online Lottery Industry Revenue Share (%), by Game Type 2025 & 2033

- Figure 14: Europe Online Lottery Industry Revenue (billion), by Platform 2025 & 2033

- Figure 15: Europe Online Lottery Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 16: Europe Online Lottery Industry Revenue (billion), by Payment Mode 2025 & 2033

- Figure 17: Europe Online Lottery Industry Revenue Share (%), by Payment Mode 2025 & 2033

- Figure 18: Europe Online Lottery Industry Revenue (billion), by End User 2025 & 2033

- Figure 19: Europe Online Lottery Industry Revenue Share (%), by End User 2025 & 2033

- Figure 20: Europe Online Lottery Industry Revenue (billion), by Country 2025 & 2033

- Figure 21: Europe Online Lottery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Asia Pacific Online Lottery Industry Revenue (billion), by Game Type 2025 & 2033

- Figure 23: Asia Pacific Online Lottery Industry Revenue Share (%), by Game Type 2025 & 2033

- Figure 24: Asia Pacific Online Lottery Industry Revenue (billion), by Platform 2025 & 2033

- Figure 25: Asia Pacific Online Lottery Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 26: Asia Pacific Online Lottery Industry Revenue (billion), by Payment Mode 2025 & 2033

- Figure 27: Asia Pacific Online Lottery Industry Revenue Share (%), by Payment Mode 2025 & 2033

- Figure 28: Asia Pacific Online Lottery Industry Revenue (billion), by End User 2025 & 2033

- Figure 29: Asia Pacific Online Lottery Industry Revenue Share (%), by End User 2025 & 2033

- Figure 30: Asia Pacific Online Lottery Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Online Lottery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: South America Online Lottery Industry Revenue (billion), by Game Type 2025 & 2033

- Figure 33: South America Online Lottery Industry Revenue Share (%), by Game Type 2025 & 2033

- Figure 34: South America Online Lottery Industry Revenue (billion), by Platform 2025 & 2033

- Figure 35: South America Online Lottery Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 36: South America Online Lottery Industry Revenue (billion), by Payment Mode 2025 & 2033

- Figure 37: South America Online Lottery Industry Revenue Share (%), by Payment Mode 2025 & 2033

- Figure 38: South America Online Lottery Industry Revenue (billion), by End User 2025 & 2033

- Figure 39: South America Online Lottery Industry Revenue Share (%), by End User 2025 & 2033

- Figure 40: South America Online Lottery Industry Revenue (billion), by Country 2025 & 2033

- Figure 41: South America Online Lottery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East and Africa Online Lottery Industry Revenue (billion), by Game Type 2025 & 2033

- Figure 43: Middle East and Africa Online Lottery Industry Revenue Share (%), by Game Type 2025 & 2033

- Figure 44: Middle East and Africa Online Lottery Industry Revenue (billion), by Platform 2025 & 2033

- Figure 45: Middle East and Africa Online Lottery Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 46: Middle East and Africa Online Lottery Industry Revenue (billion), by Payment Mode 2025 & 2033

- Figure 47: Middle East and Africa Online Lottery Industry Revenue Share (%), by Payment Mode 2025 & 2033

- Figure 48: Middle East and Africa Online Lottery Industry Revenue (billion), by End User 2025 & 2033

- Figure 49: Middle East and Africa Online Lottery Industry Revenue Share (%), by End User 2025 & 2033

- Figure 50: Middle East and Africa Online Lottery Industry Revenue (billion), by Country 2025 & 2033

- Figure 51: Middle East and Africa Online Lottery Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Online Lottery Industry Revenue billion Forecast, by Game Type 2020 & 2033

- Table 2: Global Online Lottery Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 3: Global Online Lottery Industry Revenue billion Forecast, by Payment Mode 2020 & 2033

- Table 4: Global Online Lottery Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 5: Global Online Lottery Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Online Lottery Industry Revenue billion Forecast, by Game Type 2020 & 2033

- Table 7: Global Online Lottery Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 8: Global Online Lottery Industry Revenue billion Forecast, by Payment Mode 2020 & 2033

- Table 9: Global Online Lottery Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 10: Global Online Lottery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 11: United States Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Canada Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Mexico Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Rest of North America Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Global Online Lottery Industry Revenue billion Forecast, by Game Type 2020 & 2033

- Table 16: Global Online Lottery Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 17: Global Online Lottery Industry Revenue billion Forecast, by Payment Mode 2020 & 2033

- Table 18: Global Online Lottery Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 19: Global Online Lottery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 20: Spain Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: United Kingdom Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Germany Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: France Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Italy Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Sweden Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Rest of Europe Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Global Online Lottery Industry Revenue billion Forecast, by Game Type 2020 & 2033

- Table 28: Global Online Lottery Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 29: Global Online Lottery Industry Revenue billion Forecast, by Payment Mode 2020 & 2033

- Table 30: Global Online Lottery Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 31: Global Online Lottery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 32: China Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: India Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Japan Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Australia Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Asia Pacific Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Online Lottery Industry Revenue billion Forecast, by Game Type 2020 & 2033

- Table 38: Global Online Lottery Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 39: Global Online Lottery Industry Revenue billion Forecast, by Payment Mode 2020 & 2033

- Table 40: Global Online Lottery Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 41: Global Online Lottery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 42: Brazil Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: Argentina Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Rest of South America Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Global Online Lottery Industry Revenue billion Forecast, by Game Type 2020 & 2033

- Table 46: Global Online Lottery Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 47: Global Online Lottery Industry Revenue billion Forecast, by Payment Mode 2020 & 2033

- Table 48: Global Online Lottery Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 49: Global Online Lottery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 50: South Africa Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 51: United Arab Emirates Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Rest of Middle East and Africa Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Online Lottery Industry?

The projected CAGR is approximately 9.5%.

2. Which companies are prominent players in the Online Lottery Industry?

Key companies in the market include Lotto Direct Limited, Camelot Group, Lottoland, Lotto Agent, LottoKings, WinTrillions, Lotto, ZEAL Network SE, Française des Jeux, Annexio Limited, Others.

3. What are the main segments of the Online Lottery Industry?

The market segments include Game Type, Platform, Payment Mode, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 19.43 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Appeal for Multi-functional and Damage Control Hair Care Products; Prevalence of Different Hair Concerns Remains the Major Driving Force.

6. What are the notable trends driving market growth?

Improved Internet Connections. Advances in Security. and Increased Number of Internet Users.

7. Are there any restraints impacting market growth?

Growing Availability of Counterfeit Products.

8. Can you provide examples of recent developments in the market?

October 2022: Zeal Network SE expanded its games business internationally. The German market leader for online lotteries collaborated with American online lottery provider Park Avenue Gaming to integrate the online instant games of Zeal into its video lottery terminal business in Argentina and its online platforms in Peru.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Online Lottery Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Online Lottery Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Online Lottery Industry?

To stay informed about further developments, trends, and reports in the Online Lottery Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence