Key Insights

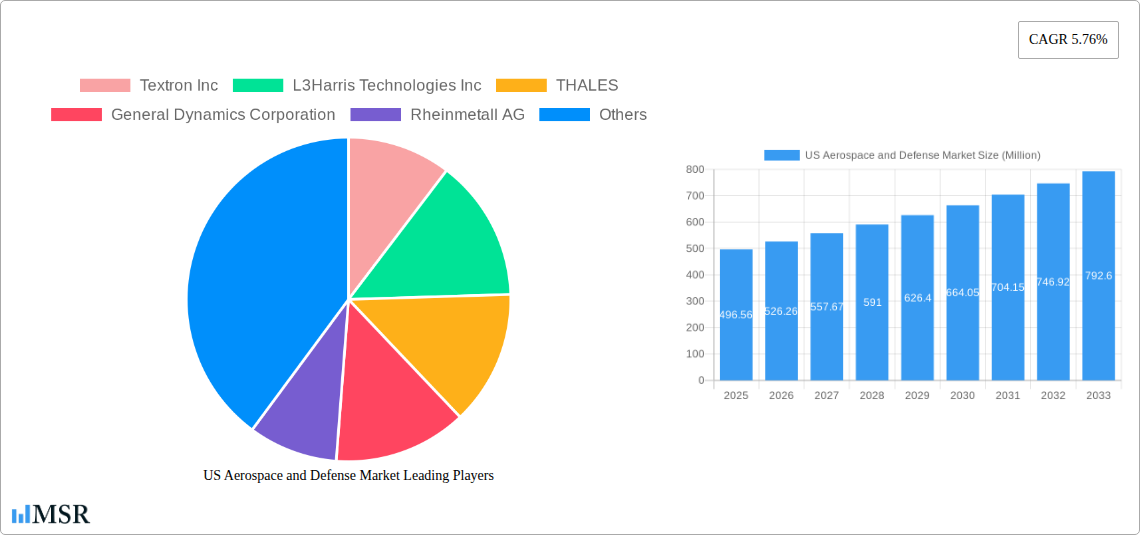

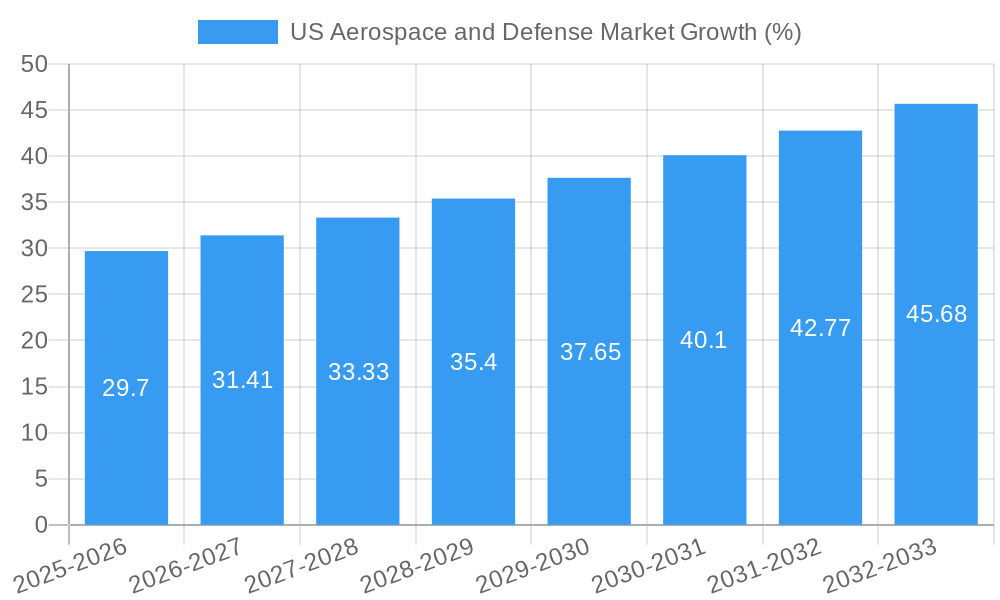

The US Aerospace and Defense market, valued at $496.56 billion in 2025, is projected to experience robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 5.76% from 2025 to 2033. This expansion is fueled by several key factors. Increased defense spending, driven by geopolitical instability and modernization efforts across various military branches, significantly contributes to market growth. Technological advancements in areas such as unmanned aerial systems (UAS), advanced avionics, and hypersonic weapons are creating new market opportunities and driving demand for sophisticated technologies. Furthermore, the growing commercial aviation sector, particularly in areas like business jets and airliners, is a significant contributor, demanding modern aircraft, maintenance, repair, and overhaul (MRO) services, and advanced technological integrations. The market's segmentation across military and commercial applications offers diverse growth avenues, with notable segments including avionics, missiles and weapons, space systems, and aircraft structures. Competition among established players like Boeing, Lockheed Martin, and Raytheon Technologies, alongside emerging companies, is fostering innovation and driving efficiency improvements. However, potential challenges include fluctuating government budgets, supply chain disruptions, and evolving regulatory landscapes, which necessitate careful market monitoring and strategic adaptation.

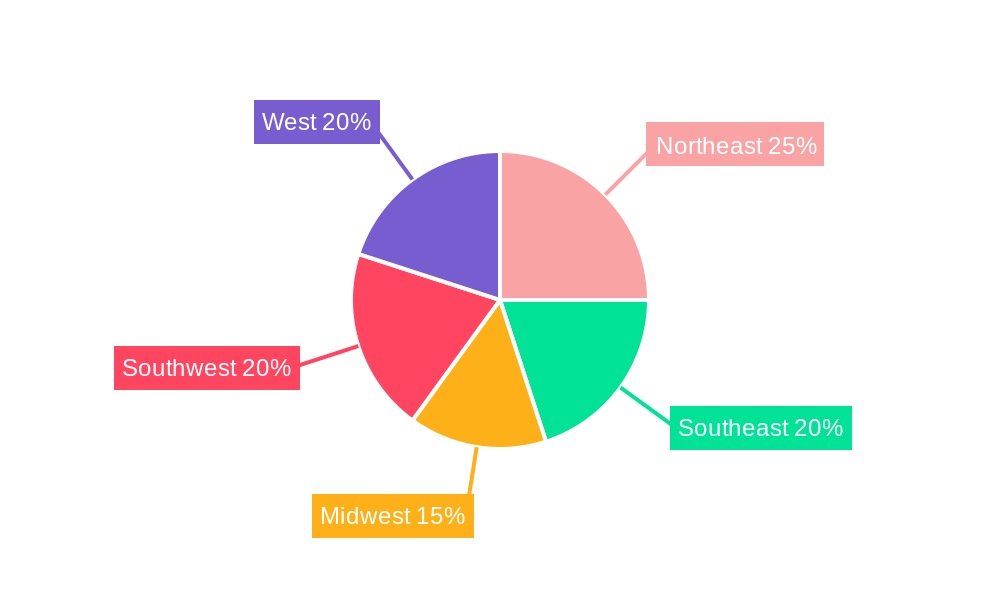

The market's regional distribution within the US shows significant concentration, with variations across Northeast, Southeast, Midwest, Southwest, and West regions likely reflecting different concentrations of manufacturing facilities, military bases, and aerospace hubs. The robust R&D efforts across various segments – from avionics and control systems to space systems and aircraft structures – indicates a strong focus on innovation and technological advancement. This commitment to R&D, coupled with the continuing need for MRO services across the lifespan of military and commercial aircraft, ensures a sustained demand for aerospace and defense products and services within the forecast period. Understanding the interplay between technological advancements, government policies, and industry competition is crucial for success in this dynamic market.

US Aerospace and Defense Market: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the US Aerospace and Defense market, offering actionable insights for industry stakeholders. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report examines market dynamics, key segments, leading players, and emerging opportunities. The report analyzes a market valued at $xx Million in 2025, projected to reach $xx Million by 2033, exhibiting a CAGR of xx%.

US Aerospace and Defense Market Market Concentration & Dynamics

The US Aerospace and Defense market is characterized by a concentrated landscape dominated by a few major players, including Boeing, Lockheed Martin, and Northrop Grumman, holding a combined market share of approximately xx%. However, a vibrant ecosystem of smaller companies and specialized firms contributes significantly to innovation and niche market development. The market's high capital intensity and stringent regulatory frameworks create significant barriers to entry, limiting the number of new participants.

Innovation is driven by continuous advancements in areas such as autonomous systems, artificial intelligence, hypersonic technologies, and advanced materials. The regulatory environment, characterized by strict safety and security standards enforced by agencies like the FAA and DoD, influences technological development and market access.

Substitute products are limited, primarily due to the specialized nature of aerospace and defense technologies. However, increasing reliance on commercial off-the-shelf (COTS) components presents a form of indirect substitution.

End-user trends are shifting toward greater demand for unmanned systems, advanced sensors, and cybersecurity solutions, reflecting evolving defense strategies and technological advancements.

Mergers and acquisitions (M&A) activity in the sector has been significant, with xx major deals recorded between 2019 and 2024, mainly driven by efforts to consolidate market share, expand technological capabilities, and enhance supply chain resilience. These M&A activities further contribute to market concentration.

US Aerospace and Defense Market Industry Insights & Trends

The US Aerospace and Defense market is experiencing robust growth, fueled by several factors. Increasing defense budgets, particularly in response to geopolitical uncertainties, are a major driver. Technological advancements, particularly in areas such as AI, hypersonic technologies, and directed energy weapons, are creating new market opportunities and driving innovation.

The market is also influenced by evolving consumer behavior, with increasing demand for customized solutions and greater emphasis on cost-effectiveness. The shift towards autonomous and unmanned systems, alongside the rising importance of cybersecurity, presents significant growth avenues.

The market size for the US Aerospace and Defense sector was estimated at $xx Million in 2024 and is projected to reach $xx Million by 2033, reflecting the influence of these factors. The overall market growth is expected to be driven by increased demand for military aircraft, missiles, and space systems, alongside ongoing research and development activities.

Key Markets & Segments Leading US Aerospace and Defense Market

Military Aircraft and Systems: This segment dominates the market, driven by continuous modernization and procurement programs by the US Air Force, Army, and Navy. The segment comprises combat aircraft (fighter jets, bombers), transport aircraft, and associated systems like weapons, avionics, and support equipment. Boeing, Lockheed Martin, and Northrop Grumman are key players. The market for combat aircraft is projected to experience significant growth, fueled by technological advancements and replacement of aging fleets. Research and development in hypersonic technology is creating new opportunities.

Space Systems and Equipment: The space sector is experiencing remarkable growth, driven by increasing demand for satellite-based services and space-based assets. The market includes spacecraft, launch vehicles, ground systems, and satellite communications. Major players include SpaceX, Boeing, and Lockheed Martin. The growing commercial space sector, coupled with government initiatives, drives substantial investment in research and development, creating significant opportunities.

Unmanned Aerial Systems (UAS): The UAS market is expanding rapidly, driven by technological advancements and a growing need for surveillance, reconnaissance, and strike capabilities. Market dynamics are shaped by technological innovations, government regulations, and defense modernization efforts. Key players include companies specializing in drone technology and integrated systems.

Avionics and Control Systems: This segment is witnessing consistent growth driven by the increasing need for advanced avionics in military and commercial aircraft. Technological advancements in areas such as AI-powered flight control systems are further driving market expansion. The integration of sophisticated sensors, communication systems, and display systems is a key trend shaping this market.

The Southeastern region of the US holds a significant share of the market due to its concentration of aerospace and defense companies and associated infrastructure.

US Aerospace and Defense Market Product Developments

Recent product developments include advancements in hypersonic weapons, improved stealth technologies, AI-powered autonomous systems, and the integration of advanced sensors into both military and commercial aircraft. These developments offer significant competitive advantages, enhancing operational capabilities, and improving the efficiency of platforms. The focus on reducing reliance on foreign suppliers is also driving innovation in domestic production.

Challenges in the US Aerospace and Defense Market Market

Significant challenges include stringent regulatory compliance requirements, supply chain vulnerabilities, particularly regarding rare earth minerals, and intense competition from both domestic and international players. These challenges impact costs, timelines, and overall market dynamics. Supply chain disruptions caused by geopolitical events can delay projects and increase costs significantly, impacting the profitability of firms.

Forces Driving US Aerospace and Defense Market Growth

Key drivers include increased government spending on defense modernization, technological advancements creating higher-performing weapons systems, and ongoing geopolitical instability leading to heightened demand for defense capabilities. These factors are mutually reinforcing, creating a positive feedback loop that accelerates market growth.

Long-Term Growth Catalysts in the US Aerospace and Defense Market

Long-term growth will be fueled by continued investment in research and development, strategic partnerships between companies to share risk and expertise, and expansion into new markets driven by increasing global demand for advanced defense technologies.

Emerging Opportunities in US Aerospace and Defense Market

Emerging opportunities include the development and adoption of hypersonic weapons, the growth of the space-based defense sector, and the increasing demand for cybersecurity solutions to protect critical infrastructure and data. These trends are expected to unlock new growth trajectories.

Leading Players in the US Aerospace and Defense Market Sector

- Textron Inc

- L3Harris Technologies Inc

- THALES

- General Dynamics Corporation

- Rheinmetall AG

- Lockheed Martin Corporation

- Airbus SE

- QinetiQ Group PLC

- Naval Group

- Fincantieri S p A

- Safran SA

- RTX Corporation

- Embraer SA

- Leonardo S p A

- Rolls-Royce plc

- BAE Systems plc

- Northrop Grumman Corporation

- The Boeing Company

- GKN Aerospace

Key Milestones in US Aerospace and Defense Market Industry

- 2020: Increased defense spending in response to geopolitical events.

- 2021: Launch of several new advanced military aircraft programs.

- 2022: Significant M&A activity amongst aerospace and defense companies.

- 2023: Acceleration of investments in hypersonic weapons development.

- 2024: Increased focus on space-based defense systems and capabilities.

Strategic Outlook for US Aerospace and Defense Market Market

The US Aerospace and Defense market is poised for sustained growth, driven by technological innovation, government investments, and evolving geopolitical landscape. Strategic opportunities lie in developing and deploying advanced technologies, fostering collaborative partnerships, and expanding into emerging markets. Companies that effectively navigate regulatory complexities and adapt to shifting demand will secure a competitive edge in this dynamic market.

US Aerospace and Defense Market Segmentation

-

1. Commercial and General Aviation

- 1.1. Market Overview

-

1.2. Market Dynamics

- 1.2.1. Drivers

- 1.2.2. Restraints

- 1.2.3. Opportunities

- 1.3. Market Trends

-

1.4. Segmentation: Commercial Aircraft

- 1.4.1. Air Traffic

- 1.4.2. Training and Flight Simulators

- 1.4.3. Airport

-

1.4.4. Structures

-

1.4.4.1. Airframe

- 1.4.4.1.1. Material

- 1.4.4.1.2. Adhesives and Coatings

- 1.4.4.2. Engine and Engine Systems

- 1.4.4.3. Cabin Interiors

- 1.4.4.4. Landing Gear

-

1.4.4.5. Avionics and Control Systems

- 1.4.4.5.1. Communication System

- 1.4.4.5.2. Navigation System

- 1.4.4.5.3. Flight Control System

- 1.4.4.5.4. Health Monitoring System

- 1.4.4.6. Electrical Systems

- 1.4.4.7. Environmental Control Systems

- 1.4.4.8. Fuel and Fuel Systems

- 1.4.4.9. MRO

- 1.4.4.10. Research and Development

- 1.4.4.11. Supply C

- 1.4.4.12. Competitor Analysis

-

1.4.4.1. Airframe

- 1.5. Segmenta

-

2. Military Aircraft and Systems

- 2.1. Market Overview

-

2.2. Defense Spending and Budget Allocation Details

- 2.2.1. Army

- 2.2.2. Navy and Marine Corps

- 2.2.3. Air Force

-

2.3. Market Dynamics

- 2.3.1. Drivers

- 2.3.2. Restraints

- 2.3.3. Opportunities

- 2.4. Market Trends

- 2.5. MRO

- 2.6. Research and Development

- 2.7. Training and Flight Simulators

- 2.8. Competitor Analysis

- 2.9. Supply Chain Analysis

- 2.10. Customer/Distributor Information

-

2.11. Segmentation: Combat Aircraft

-

2.11.1. Structures

-

2.11.1.1. Airframe

- 2.11.1.1.1. Material

- 2.11.1.1.2. Adhesives and Coatings

- 2.11.1.2. Engine and Engine Systems

- 2.11.1.3. Landing Gear

-

2.11.1.1. Airframe

-

2.11.2. Avionics and Control Systems

- 2.11.2.1. General Avionics

- 2.11.2.2. Mission Specific Avionics

- 2.11.3. Missiles and Weapons

-

2.11.1. Structures

- 2.12. Segmentation: Non-Combat Aircraft

-

3. Unmanned Aerial Systems

- 3.1. Market Overview

-

3.2. Market Dynamics

- 3.2.1. Drivers

- 3.2.2. Restraints

- 3.2.3. Opportunities

- 3.3. Market Trends

- 3.4. Research and Development

- 3.5. Competitor Analysis

- 3.6. Regulatory Landscape and Future Policy Changes

-

3.7. Segmentation

- 3.7.1. Commercial

- 3.7.2. Military

-

4. Space Systems and Equipment

- 4.1. Market Overview

-

4.2. Market Dynamics

- 4.2.1. Drivers

- 4.2.2. Restraints

- 4.2.3. Opportunities

- 4.3. Market Trends

- 4.4. Research and Development

- 4.5. Competitor Analysis

- 4.6. Regulatory Landscape and Future Policy Changes

- 4.7. Customer Information

- 4.8. Segmenta

-

4.9. Segmentation: Satellites

-

4.9.1. By Subsystem

- 4.9.1.1. Command and Control System

- 4.9.1.2. Telemetr

- 4.9.1.3. Antenna System

- 4.9.1.4. Transponders

- 4.9.1.5. Power System

-

4.9.2. By Application

- 4.9.2.1. Military

- 4.9.2.2. Commercial

-

4.9.1. By Subsystem

US Aerospace and Defense Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

US Aerospace and Defense Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 5.76% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 3.4.1. The Space Sector is Expected to Witness the Highest Growth During the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global US Aerospace and Defense Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Commercial and General Aviation

- 5.1.1. Market Overview

- 5.1.2. Market Dynamics

- 5.1.2.1. Drivers

- 5.1.2.2. Restraints

- 5.1.2.3. Opportunities

- 5.1.3. Market Trends

- 5.1.4. Segmentation: Commercial Aircraft

- 5.1.4.1. Air Traffic

- 5.1.4.2. Training and Flight Simulators

- 5.1.4.3. Airport

- 5.1.4.4. Structures

- 5.1.4.4.1. Airframe

- 5.1.4.4.1.1. Material

- 5.1.4.4.1.2. Adhesives and Coatings

- 5.1.4.4.2. Engine and Engine Systems

- 5.1.4.4.3. Cabin Interiors

- 5.1.4.4.4. Landing Gear

- 5.1.4.4.5. Avionics and Control Systems

- 5.1.4.4.5.1. Communication System

- 5.1.4.4.5.2. Navigation System

- 5.1.4.4.5.3. Flight Control System

- 5.1.4.4.5.4. Health Monitoring System

- 5.1.4.4.6. Electrical Systems

- 5.1.4.4.7. Environmental Control Systems

- 5.1.4.4.8. Fuel and Fuel Systems

- 5.1.4.4.9. MRO

- 5.1.4.4.10. Research and Development

- 5.1.4.4.11. Supply C

- 5.1.4.4.12. Competitor Analysis

- 5.1.4.4.1. Airframe

- 5.1.5. Segmenta

- 5.2. Market Analysis, Insights and Forecast - by Military Aircraft and Systems

- 5.2.1. Market Overview

- 5.2.2. Defense Spending and Budget Allocation Details

- 5.2.2.1. Army

- 5.2.2.2. Navy and Marine Corps

- 5.2.2.3. Air Force

- 5.2.3. Market Dynamics

- 5.2.3.1. Drivers

- 5.2.3.2. Restraints

- 5.2.3.3. Opportunities

- 5.2.4. Market Trends

- 5.2.5. MRO

- 5.2.6. Research and Development

- 5.2.7. Training and Flight Simulators

- 5.2.8. Competitor Analysis

- 5.2.9. Supply Chain Analysis

- 5.2.10. Customer/Distributor Information

- 5.2.11. Segmentation: Combat Aircraft

- 5.2.11.1. Structures

- 5.2.11.1.1. Airframe

- 5.2.11.1.1.1. Material

- 5.2.11.1.1.2. Adhesives and Coatings

- 5.2.11.1.2. Engine and Engine Systems

- 5.2.11.1.3. Landing Gear

- 5.2.11.1.1. Airframe

- 5.2.11.2. Avionics and Control Systems

- 5.2.11.2.1. General Avionics

- 5.2.11.2.2. Mission Specific Avionics

- 5.2.11.3. Missiles and Weapons

- 5.2.11.1. Structures

- 5.2.12. Segmentation: Non-Combat Aircraft

- 5.3. Market Analysis, Insights and Forecast - by Unmanned Aerial Systems

- 5.3.1. Market Overview

- 5.3.2. Market Dynamics

- 5.3.2.1. Drivers

- 5.3.2.2. Restraints

- 5.3.2.3. Opportunities

- 5.3.3. Market Trends

- 5.3.4. Research and Development

- 5.3.5. Competitor Analysis

- 5.3.6. Regulatory Landscape and Future Policy Changes

- 5.3.7. Segmentation

- 5.3.7.1. Commercial

- 5.3.7.2. Military

- 5.4. Market Analysis, Insights and Forecast - by Space Systems and Equipment

- 5.4.1. Market Overview

- 5.4.2. Market Dynamics

- 5.4.2.1. Drivers

- 5.4.2.2. Restraints

- 5.4.2.3. Opportunities

- 5.4.3. Market Trends

- 5.4.4. Research and Development

- 5.4.5. Competitor Analysis

- 5.4.6. Regulatory Landscape and Future Policy Changes

- 5.4.7. Customer Information

- 5.4.8. Segmenta

- 5.4.9. Segmentation: Satellites

- 5.4.9.1. By Subsystem

- 5.4.9.1.1. Command and Control System

- 5.4.9.1.2. Telemetr

- 5.4.9.1.3. Antenna System

- 5.4.9.1.4. Transponders

- 5.4.9.1.5. Power System

- 5.4.9.2. By Application

- 5.4.9.2.1. Military

- 5.4.9.2.2. Commercial

- 5.4.9.1. By Subsystem

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. South America

- 5.5.3. Europe

- 5.5.4. Middle East & Africa

- 5.5.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Commercial and General Aviation

- 6. North America US Aerospace and Defense Market Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Commercial and General Aviation

- 6.1.1. Market Overview

- 6.1.2. Market Dynamics

- 6.1.2.1. Drivers

- 6.1.2.2. Restraints

- 6.1.2.3. Opportunities

- 6.1.3. Market Trends

- 6.1.4. Segmentation: Commercial Aircraft

- 6.1.4.1. Air Traffic

- 6.1.4.2. Training and Flight Simulators

- 6.1.4.3. Airport

- 6.1.4.4. Structures

- 6.1.4.4.1. Airframe

- 6.1.4.4.1.1. Material

- 6.1.4.4.1.2. Adhesives and Coatings

- 6.1.4.4.2. Engine and Engine Systems

- 6.1.4.4.3. Cabin Interiors

- 6.1.4.4.4. Landing Gear

- 6.1.4.4.5. Avionics and Control Systems

- 6.1.4.4.5.1. Communication System

- 6.1.4.4.5.2. Navigation System

- 6.1.4.4.5.3. Flight Control System

- 6.1.4.4.5.4. Health Monitoring System

- 6.1.4.4.6. Electrical Systems

- 6.1.4.4.7. Environmental Control Systems

- 6.1.4.4.8. Fuel and Fuel Systems

- 6.1.4.4.9. MRO

- 6.1.4.4.10. Research and Development

- 6.1.4.4.11. Supply C

- 6.1.4.4.12. Competitor Analysis

- 6.1.4.4.1. Airframe

- 6.1.5. Segmenta

- 6.2. Market Analysis, Insights and Forecast - by Military Aircraft and Systems

- 6.2.1. Market Overview

- 6.2.2. Defense Spending and Budget Allocation Details

- 6.2.2.1. Army

- 6.2.2.2. Navy and Marine Corps

- 6.2.2.3. Air Force

- 6.2.3. Market Dynamics

- 6.2.3.1. Drivers

- 6.2.3.2. Restraints

- 6.2.3.3. Opportunities

- 6.2.4. Market Trends

- 6.2.5. MRO

- 6.2.6. Research and Development

- 6.2.7. Training and Flight Simulators

- 6.2.8. Competitor Analysis

- 6.2.9. Supply Chain Analysis

- 6.2.10. Customer/Distributor Information

- 6.2.11. Segmentation: Combat Aircraft

- 6.2.11.1. Structures

- 6.2.11.1.1. Airframe

- 6.2.11.1.1.1. Material

- 6.2.11.1.1.2. Adhesives and Coatings

- 6.2.11.1.2. Engine and Engine Systems

- 6.2.11.1.3. Landing Gear

- 6.2.11.1.1. Airframe

- 6.2.11.2. Avionics and Control Systems

- 6.2.11.2.1. General Avionics

- 6.2.11.2.2. Mission Specific Avionics

- 6.2.11.3. Missiles and Weapons

- 6.2.11.1. Structures

- 6.2.12. Segmentation: Non-Combat Aircraft

- 6.3. Market Analysis, Insights and Forecast - by Unmanned Aerial Systems

- 6.3.1. Market Overview

- 6.3.2. Market Dynamics

- 6.3.2.1. Drivers

- 6.3.2.2. Restraints

- 6.3.2.3. Opportunities

- 6.3.3. Market Trends

- 6.3.4. Research and Development

- 6.3.5. Competitor Analysis

- 6.3.6. Regulatory Landscape and Future Policy Changes

- 6.3.7. Segmentation

- 6.3.7.1. Commercial

- 6.3.7.2. Military

- 6.4. Market Analysis, Insights and Forecast - by Space Systems and Equipment

- 6.4.1. Market Overview

- 6.4.2. Market Dynamics

- 6.4.2.1. Drivers

- 6.4.2.2. Restraints

- 6.4.2.3. Opportunities

- 6.4.3. Market Trends

- 6.4.4. Research and Development

- 6.4.5. Competitor Analysis

- 6.4.6. Regulatory Landscape and Future Policy Changes

- 6.4.7. Customer Information

- 6.4.8. Segmenta

- 6.4.9. Segmentation: Satellites

- 6.4.9.1. By Subsystem

- 6.4.9.1.1. Command and Control System

- 6.4.9.1.2. Telemetr

- 6.4.9.1.3. Antenna System

- 6.4.9.1.4. Transponders

- 6.4.9.1.5. Power System

- 6.4.9.2. By Application

- 6.4.9.2.1. Military

- 6.4.9.2.2. Commercial

- 6.4.9.1. By Subsystem

- 6.1. Market Analysis, Insights and Forecast - by Commercial and General Aviation

- 7. South America US Aerospace and Defense Market Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Commercial and General Aviation

- 7.1.1. Market Overview

- 7.1.2. Market Dynamics

- 7.1.2.1. Drivers

- 7.1.2.2. Restraints

- 7.1.2.3. Opportunities

- 7.1.3. Market Trends

- 7.1.4. Segmentation: Commercial Aircraft

- 7.1.4.1. Air Traffic

- 7.1.4.2. Training and Flight Simulators

- 7.1.4.3. Airport

- 7.1.4.4. Structures

- 7.1.4.4.1. Airframe

- 7.1.4.4.1.1. Material

- 7.1.4.4.1.2. Adhesives and Coatings

- 7.1.4.4.2. Engine and Engine Systems

- 7.1.4.4.3. Cabin Interiors

- 7.1.4.4.4. Landing Gear

- 7.1.4.4.5. Avionics and Control Systems

- 7.1.4.4.5.1. Communication System

- 7.1.4.4.5.2. Navigation System

- 7.1.4.4.5.3. Flight Control System

- 7.1.4.4.5.4. Health Monitoring System

- 7.1.4.4.6. Electrical Systems

- 7.1.4.4.7. Environmental Control Systems

- 7.1.4.4.8. Fuel and Fuel Systems

- 7.1.4.4.9. MRO

- 7.1.4.4.10. Research and Development

- 7.1.4.4.11. Supply C

- 7.1.4.4.12. Competitor Analysis

- 7.1.4.4.1. Airframe

- 7.1.5. Segmenta

- 7.2. Market Analysis, Insights and Forecast - by Military Aircraft and Systems

- 7.2.1. Market Overview

- 7.2.2. Defense Spending and Budget Allocation Details

- 7.2.2.1. Army

- 7.2.2.2. Navy and Marine Corps

- 7.2.2.3. Air Force

- 7.2.3. Market Dynamics

- 7.2.3.1. Drivers

- 7.2.3.2. Restraints

- 7.2.3.3. Opportunities

- 7.2.4. Market Trends

- 7.2.5. MRO

- 7.2.6. Research and Development

- 7.2.7. Training and Flight Simulators

- 7.2.8. Competitor Analysis

- 7.2.9. Supply Chain Analysis

- 7.2.10. Customer/Distributor Information

- 7.2.11. Segmentation: Combat Aircraft

- 7.2.11.1. Structures

- 7.2.11.1.1. Airframe

- 7.2.11.1.1.1. Material

- 7.2.11.1.1.2. Adhesives and Coatings

- 7.2.11.1.2. Engine and Engine Systems

- 7.2.11.1.3. Landing Gear

- 7.2.11.1.1. Airframe

- 7.2.11.2. Avionics and Control Systems

- 7.2.11.2.1. General Avionics

- 7.2.11.2.2. Mission Specific Avionics

- 7.2.11.3. Missiles and Weapons

- 7.2.11.1. Structures

- 7.2.12. Segmentation: Non-Combat Aircraft

- 7.3. Market Analysis, Insights and Forecast - by Unmanned Aerial Systems

- 7.3.1. Market Overview

- 7.3.2. Market Dynamics

- 7.3.2.1. Drivers

- 7.3.2.2. Restraints

- 7.3.2.3. Opportunities

- 7.3.3. Market Trends

- 7.3.4. Research and Development

- 7.3.5. Competitor Analysis

- 7.3.6. Regulatory Landscape and Future Policy Changes

- 7.3.7. Segmentation

- 7.3.7.1. Commercial

- 7.3.7.2. Military

- 7.4. Market Analysis, Insights and Forecast - by Space Systems and Equipment

- 7.4.1. Market Overview

- 7.4.2. Market Dynamics

- 7.4.2.1. Drivers

- 7.4.2.2. Restraints

- 7.4.2.3. Opportunities

- 7.4.3. Market Trends

- 7.4.4. Research and Development

- 7.4.5. Competitor Analysis

- 7.4.6. Regulatory Landscape and Future Policy Changes

- 7.4.7. Customer Information

- 7.4.8. Segmenta

- 7.4.9. Segmentation: Satellites

- 7.4.9.1. By Subsystem

- 7.4.9.1.1. Command and Control System

- 7.4.9.1.2. Telemetr

- 7.4.9.1.3. Antenna System

- 7.4.9.1.4. Transponders

- 7.4.9.1.5. Power System

- 7.4.9.2. By Application

- 7.4.9.2.1. Military

- 7.4.9.2.2. Commercial

- 7.4.9.1. By Subsystem

- 7.1. Market Analysis, Insights and Forecast - by Commercial and General Aviation

- 8. Europe US Aerospace and Defense Market Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Commercial and General Aviation

- 8.1.1. Market Overview

- 8.1.2. Market Dynamics

- 8.1.2.1. Drivers

- 8.1.2.2. Restraints

- 8.1.2.3. Opportunities

- 8.1.3. Market Trends

- 8.1.4. Segmentation: Commercial Aircraft

- 8.1.4.1. Air Traffic

- 8.1.4.2. Training and Flight Simulators

- 8.1.4.3. Airport

- 8.1.4.4. Structures

- 8.1.4.4.1. Airframe

- 8.1.4.4.1.1. Material

- 8.1.4.4.1.2. Adhesives and Coatings

- 8.1.4.4.2. Engine and Engine Systems

- 8.1.4.4.3. Cabin Interiors

- 8.1.4.4.4. Landing Gear

- 8.1.4.4.5. Avionics and Control Systems

- 8.1.4.4.5.1. Communication System

- 8.1.4.4.5.2. Navigation System

- 8.1.4.4.5.3. Flight Control System

- 8.1.4.4.5.4. Health Monitoring System

- 8.1.4.4.6. Electrical Systems

- 8.1.4.4.7. Environmental Control Systems

- 8.1.4.4.8. Fuel and Fuel Systems

- 8.1.4.4.9. MRO

- 8.1.4.4.10. Research and Development

- 8.1.4.4.11. Supply C

- 8.1.4.4.12. Competitor Analysis

- 8.1.4.4.1. Airframe

- 8.1.5. Segmenta

- 8.2. Market Analysis, Insights and Forecast - by Military Aircraft and Systems

- 8.2.1. Market Overview

- 8.2.2. Defense Spending and Budget Allocation Details

- 8.2.2.1. Army

- 8.2.2.2. Navy and Marine Corps

- 8.2.2.3. Air Force

- 8.2.3. Market Dynamics

- 8.2.3.1. Drivers

- 8.2.3.2. Restraints

- 8.2.3.3. Opportunities

- 8.2.4. Market Trends

- 8.2.5. MRO

- 8.2.6. Research and Development

- 8.2.7. Training and Flight Simulators

- 8.2.8. Competitor Analysis

- 8.2.9. Supply Chain Analysis

- 8.2.10. Customer/Distributor Information

- 8.2.11. Segmentation: Combat Aircraft

- 8.2.11.1. Structures

- 8.2.11.1.1. Airframe

- 8.2.11.1.1.1. Material

- 8.2.11.1.1.2. Adhesives and Coatings

- 8.2.11.1.2. Engine and Engine Systems

- 8.2.11.1.3. Landing Gear

- 8.2.11.1.1. Airframe

- 8.2.11.2. Avionics and Control Systems

- 8.2.11.2.1. General Avionics

- 8.2.11.2.2. Mission Specific Avionics

- 8.2.11.3. Missiles and Weapons

- 8.2.11.1. Structures

- 8.2.12. Segmentation: Non-Combat Aircraft

- 8.3. Market Analysis, Insights and Forecast - by Unmanned Aerial Systems

- 8.3.1. Market Overview

- 8.3.2. Market Dynamics

- 8.3.2.1. Drivers

- 8.3.2.2. Restraints

- 8.3.2.3. Opportunities

- 8.3.3. Market Trends

- 8.3.4. Research and Development

- 8.3.5. Competitor Analysis

- 8.3.6. Regulatory Landscape and Future Policy Changes

- 8.3.7. Segmentation

- 8.3.7.1. Commercial

- 8.3.7.2. Military

- 8.4. Market Analysis, Insights and Forecast - by Space Systems and Equipment

- 8.4.1. Market Overview

- 8.4.2. Market Dynamics

- 8.4.2.1. Drivers

- 8.4.2.2. Restraints

- 8.4.2.3. Opportunities

- 8.4.3. Market Trends

- 8.4.4. Research and Development

- 8.4.5. Competitor Analysis

- 8.4.6. Regulatory Landscape and Future Policy Changes

- 8.4.7. Customer Information

- 8.4.8. Segmenta

- 8.4.9. Segmentation: Satellites

- 8.4.9.1. By Subsystem

- 8.4.9.1.1. Command and Control System

- 8.4.9.1.2. Telemetr

- 8.4.9.1.3. Antenna System

- 8.4.9.1.4. Transponders

- 8.4.9.1.5. Power System

- 8.4.9.2. By Application

- 8.4.9.2.1. Military

- 8.4.9.2.2. Commercial

- 8.4.9.1. By Subsystem

- 8.1. Market Analysis, Insights and Forecast - by Commercial and General Aviation

- 9. Middle East & Africa US Aerospace and Defense Market Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Commercial and General Aviation

- 9.1.1. Market Overview

- 9.1.2. Market Dynamics

- 9.1.2.1. Drivers

- 9.1.2.2. Restraints

- 9.1.2.3. Opportunities

- 9.1.3. Market Trends

- 9.1.4. Segmentation: Commercial Aircraft

- 9.1.4.1. Air Traffic

- 9.1.4.2. Training and Flight Simulators

- 9.1.4.3. Airport

- 9.1.4.4. Structures

- 9.1.4.4.1. Airframe

- 9.1.4.4.1.1. Material

- 9.1.4.4.1.2. Adhesives and Coatings

- 9.1.4.4.2. Engine and Engine Systems

- 9.1.4.4.3. Cabin Interiors

- 9.1.4.4.4. Landing Gear

- 9.1.4.4.5. Avionics and Control Systems

- 9.1.4.4.5.1. Communication System

- 9.1.4.4.5.2. Navigation System

- 9.1.4.4.5.3. Flight Control System

- 9.1.4.4.5.4. Health Monitoring System

- 9.1.4.4.6. Electrical Systems

- 9.1.4.4.7. Environmental Control Systems

- 9.1.4.4.8. Fuel and Fuel Systems

- 9.1.4.4.9. MRO

- 9.1.4.4.10. Research and Development

- 9.1.4.4.11. Supply C

- 9.1.4.4.12. Competitor Analysis

- 9.1.4.4.1. Airframe

- 9.1.5. Segmenta

- 9.2. Market Analysis, Insights and Forecast - by Military Aircraft and Systems

- 9.2.1. Market Overview

- 9.2.2. Defense Spending and Budget Allocation Details

- 9.2.2.1. Army

- 9.2.2.2. Navy and Marine Corps

- 9.2.2.3. Air Force

- 9.2.3. Market Dynamics

- 9.2.3.1. Drivers

- 9.2.3.2. Restraints

- 9.2.3.3. Opportunities

- 9.2.4. Market Trends

- 9.2.5. MRO

- 9.2.6. Research and Development

- 9.2.7. Training and Flight Simulators

- 9.2.8. Competitor Analysis

- 9.2.9. Supply Chain Analysis

- 9.2.10. Customer/Distributor Information

- 9.2.11. Segmentation: Combat Aircraft

- 9.2.11.1. Structures

- 9.2.11.1.1. Airframe

- 9.2.11.1.1.1. Material

- 9.2.11.1.1.2. Adhesives and Coatings

- 9.2.11.1.2. Engine and Engine Systems

- 9.2.11.1.3. Landing Gear

- 9.2.11.1.1. Airframe

- 9.2.11.2. Avionics and Control Systems

- 9.2.11.2.1. General Avionics

- 9.2.11.2.2. Mission Specific Avionics

- 9.2.11.3. Missiles and Weapons

- 9.2.11.1. Structures

- 9.2.12. Segmentation: Non-Combat Aircraft

- 9.3. Market Analysis, Insights and Forecast - by Unmanned Aerial Systems

- 9.3.1. Market Overview

- 9.3.2. Market Dynamics

- 9.3.2.1. Drivers

- 9.3.2.2. Restraints

- 9.3.2.3. Opportunities

- 9.3.3. Market Trends

- 9.3.4. Research and Development

- 9.3.5. Competitor Analysis

- 9.3.6. Regulatory Landscape and Future Policy Changes

- 9.3.7. Segmentation

- 9.3.7.1. Commercial

- 9.3.7.2. Military

- 9.4. Market Analysis, Insights and Forecast - by Space Systems and Equipment

- 9.4.1. Market Overview

- 9.4.2. Market Dynamics

- 9.4.2.1. Drivers

- 9.4.2.2. Restraints

- 9.4.2.3. Opportunities

- 9.4.3. Market Trends

- 9.4.4. Research and Development

- 9.4.5. Competitor Analysis

- 9.4.6. Regulatory Landscape and Future Policy Changes

- 9.4.7. Customer Information

- 9.4.8. Segmenta

- 9.4.9. Segmentation: Satellites

- 9.4.9.1. By Subsystem

- 9.4.9.1.1. Command and Control System

- 9.4.9.1.2. Telemetr

- 9.4.9.1.3. Antenna System

- 9.4.9.1.4. Transponders

- 9.4.9.1.5. Power System

- 9.4.9.2. By Application

- 9.4.9.2.1. Military

- 9.4.9.2.2. Commercial

- 9.4.9.1. By Subsystem

- 9.1. Market Analysis, Insights and Forecast - by Commercial and General Aviation

- 10. Asia Pacific US Aerospace and Defense Market Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Commercial and General Aviation

- 10.1.1. Market Overview

- 10.1.2. Market Dynamics

- 10.1.2.1. Drivers

- 10.1.2.2. Restraints

- 10.1.2.3. Opportunities

- 10.1.3. Market Trends

- 10.1.4. Segmentation: Commercial Aircraft

- 10.1.4.1. Air Traffic

- 10.1.4.2. Training and Flight Simulators

- 10.1.4.3. Airport

- 10.1.4.4. Structures

- 10.1.4.4.1. Airframe

- 10.1.4.4.1.1. Material

- 10.1.4.4.1.2. Adhesives and Coatings

- 10.1.4.4.2. Engine and Engine Systems

- 10.1.4.4.3. Cabin Interiors

- 10.1.4.4.4. Landing Gear

- 10.1.4.4.5. Avionics and Control Systems

- 10.1.4.4.5.1. Communication System

- 10.1.4.4.5.2. Navigation System

- 10.1.4.4.5.3. Flight Control System

- 10.1.4.4.5.4. Health Monitoring System

- 10.1.4.4.6. Electrical Systems

- 10.1.4.4.7. Environmental Control Systems

- 10.1.4.4.8. Fuel and Fuel Systems

- 10.1.4.4.9. MRO

- 10.1.4.4.10. Research and Development

- 10.1.4.4.11. Supply C

- 10.1.4.4.12. Competitor Analysis

- 10.1.4.4.1. Airframe

- 10.1.5. Segmenta

- 10.2. Market Analysis, Insights and Forecast - by Military Aircraft and Systems

- 10.2.1. Market Overview

- 10.2.2. Defense Spending and Budget Allocation Details

- 10.2.2.1. Army

- 10.2.2.2. Navy and Marine Corps

- 10.2.2.3. Air Force

- 10.2.3. Market Dynamics

- 10.2.3.1. Drivers

- 10.2.3.2. Restraints

- 10.2.3.3. Opportunities

- 10.2.4. Market Trends

- 10.2.5. MRO

- 10.2.6. Research and Development

- 10.2.7. Training and Flight Simulators

- 10.2.8. Competitor Analysis

- 10.2.9. Supply Chain Analysis

- 10.2.10. Customer/Distributor Information

- 10.2.11. Segmentation: Combat Aircraft

- 10.2.11.1. Structures

- 10.2.11.1.1. Airframe

- 10.2.11.1.1.1. Material

- 10.2.11.1.1.2. Adhesives and Coatings

- 10.2.11.1.2. Engine and Engine Systems

- 10.2.11.1.3. Landing Gear

- 10.2.11.1.1. Airframe

- 10.2.11.2. Avionics and Control Systems

- 10.2.11.2.1. General Avionics

- 10.2.11.2.2. Mission Specific Avionics

- 10.2.11.3. Missiles and Weapons

- 10.2.11.1. Structures

- 10.2.12. Segmentation: Non-Combat Aircraft

- 10.3. Market Analysis, Insights and Forecast - by Unmanned Aerial Systems

- 10.3.1. Market Overview

- 10.3.2. Market Dynamics

- 10.3.2.1. Drivers

- 10.3.2.2. Restraints

- 10.3.2.3. Opportunities

- 10.3.3. Market Trends

- 10.3.4. Research and Development

- 10.3.5. Competitor Analysis

- 10.3.6. Regulatory Landscape and Future Policy Changes

- 10.3.7. Segmentation

- 10.3.7.1. Commercial

- 10.3.7.2. Military

- 10.4. Market Analysis, Insights and Forecast - by Space Systems and Equipment

- 10.4.1. Market Overview

- 10.4.2. Market Dynamics

- 10.4.2.1. Drivers

- 10.4.2.2. Restraints

- 10.4.2.3. Opportunities

- 10.4.3. Market Trends

- 10.4.4. Research and Development

- 10.4.5. Competitor Analysis

- 10.4.6. Regulatory Landscape and Future Policy Changes

- 10.4.7. Customer Information

- 10.4.8. Segmenta

- 10.4.9. Segmentation: Satellites

- 10.4.9.1. By Subsystem

- 10.4.9.1.1. Command and Control System

- 10.4.9.1.2. Telemetr

- 10.4.9.1.3. Antenna System

- 10.4.9.1.4. Transponders

- 10.4.9.1.5. Power System

- 10.4.9.2. By Application

- 10.4.9.2.1. Military

- 10.4.9.2.2. Commercial

- 10.4.9.1. By Subsystem

- 10.1. Market Analysis, Insights and Forecast - by Commercial and General Aviation

- 11. Northeast US Aerospace and Defense Market Analysis, Insights and Forecast, 2019-2031

- 12. Southeast US Aerospace and Defense Market Analysis, Insights and Forecast, 2019-2031

- 13. Midwest US Aerospace and Defense Market Analysis, Insights and Forecast, 2019-2031

- 14. Southwest US Aerospace and Defense Market Analysis, Insights and Forecast, 2019-2031

- 15. West US Aerospace and Defense Market Analysis, Insights and Forecast, 2019-2031

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 Textron Inc

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 L3Harris Technologies Inc

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 THALES

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 General Dynamics Corporation

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 Rheinmetall AG

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Lockheed Martin Corporation

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 Airbus SE

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 QinetiQ Group PLC

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 Naval Group

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 Fincantieri S p A

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.11 Safran SA

- 16.2.11.1. Overview

- 16.2.11.2. Products

- 16.2.11.3. SWOT Analysis

- 16.2.11.4. Recent Developments

- 16.2.11.5. Financials (Based on Availability)

- 16.2.12 RTX Corporation

- 16.2.12.1. Overview

- 16.2.12.2. Products

- 16.2.12.3. SWOT Analysis

- 16.2.12.4. Recent Developments

- 16.2.12.5. Financials (Based on Availability)

- 16.2.13 Embraer SA

- 16.2.13.1. Overview

- 16.2.13.2. Products

- 16.2.13.3. SWOT Analysis

- 16.2.13.4. Recent Developments

- 16.2.13.5. Financials (Based on Availability)

- 16.2.14 Leonardo S p A

- 16.2.14.1. Overview

- 16.2.14.2. Products

- 16.2.14.3. SWOT Analysis

- 16.2.14.4. Recent Developments

- 16.2.14.5. Financials (Based on Availability)

- 16.2.15 Rolls-Royce plc

- 16.2.15.1. Overview

- 16.2.15.2. Products

- 16.2.15.3. SWOT Analysis

- 16.2.15.4. Recent Developments

- 16.2.15.5. Financials (Based on Availability)

- 16.2.16 BAE Systems plc

- 16.2.16.1. Overview

- 16.2.16.2. Products

- 16.2.16.3. SWOT Analysis

- 16.2.16.4. Recent Developments

- 16.2.16.5. Financials (Based on Availability)

- 16.2.17 Northrop Grumman Corporation

- 16.2.17.1. Overview

- 16.2.17.2. Products

- 16.2.17.3. SWOT Analysis

- 16.2.17.4. Recent Developments

- 16.2.17.5. Financials (Based on Availability)

- 16.2.18 The Boeing Company

- 16.2.18.1. Overview

- 16.2.18.2. Products

- 16.2.18.3. SWOT Analysis

- 16.2.18.4. Recent Developments

- 16.2.18.5. Financials (Based on Availability)

- 16.2.19 GKN Aerospace

- 16.2.19.1. Overview

- 16.2.19.2. Products

- 16.2.19.3. SWOT Analysis

- 16.2.19.4. Recent Developments

- 16.2.19.5. Financials (Based on Availability)

- 16.2.1 Textron Inc

List of Figures

- Figure 1: Global US Aerospace and Defense Market Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: United states US Aerospace and Defense Market Revenue (Million), by Country 2024 & 2032

- Figure 3: United states US Aerospace and Defense Market Revenue Share (%), by Country 2024 & 2032

- Figure 4: North America US Aerospace and Defense Market Revenue (Million), by Commercial and General Aviation 2024 & 2032

- Figure 5: North America US Aerospace and Defense Market Revenue Share (%), by Commercial and General Aviation 2024 & 2032

- Figure 6: North America US Aerospace and Defense Market Revenue (Million), by Military Aircraft and Systems 2024 & 2032

- Figure 7: North America US Aerospace and Defense Market Revenue Share (%), by Military Aircraft and Systems 2024 & 2032

- Figure 8: North America US Aerospace and Defense Market Revenue (Million), by Unmanned Aerial Systems 2024 & 2032

- Figure 9: North America US Aerospace and Defense Market Revenue Share (%), by Unmanned Aerial Systems 2024 & 2032

- Figure 10: North America US Aerospace and Defense Market Revenue (Million), by Space Systems and Equipment 2024 & 2032

- Figure 11: North America US Aerospace and Defense Market Revenue Share (%), by Space Systems and Equipment 2024 & 2032

- Figure 12: North America US Aerospace and Defense Market Revenue (Million), by Country 2024 & 2032

- Figure 13: North America US Aerospace and Defense Market Revenue Share (%), by Country 2024 & 2032

- Figure 14: South America US Aerospace and Defense Market Revenue (Million), by Commercial and General Aviation 2024 & 2032

- Figure 15: South America US Aerospace and Defense Market Revenue Share (%), by Commercial and General Aviation 2024 & 2032

- Figure 16: South America US Aerospace and Defense Market Revenue (Million), by Military Aircraft and Systems 2024 & 2032

- Figure 17: South America US Aerospace and Defense Market Revenue Share (%), by Military Aircraft and Systems 2024 & 2032

- Figure 18: South America US Aerospace and Defense Market Revenue (Million), by Unmanned Aerial Systems 2024 & 2032

- Figure 19: South America US Aerospace and Defense Market Revenue Share (%), by Unmanned Aerial Systems 2024 & 2032

- Figure 20: South America US Aerospace and Defense Market Revenue (Million), by Space Systems and Equipment 2024 & 2032

- Figure 21: South America US Aerospace and Defense Market Revenue Share (%), by Space Systems and Equipment 2024 & 2032

- Figure 22: South America US Aerospace and Defense Market Revenue (Million), by Country 2024 & 2032

- Figure 23: South America US Aerospace and Defense Market Revenue Share (%), by Country 2024 & 2032

- Figure 24: Europe US Aerospace and Defense Market Revenue (Million), by Commercial and General Aviation 2024 & 2032

- Figure 25: Europe US Aerospace and Defense Market Revenue Share (%), by Commercial and General Aviation 2024 & 2032

- Figure 26: Europe US Aerospace and Defense Market Revenue (Million), by Military Aircraft and Systems 2024 & 2032

- Figure 27: Europe US Aerospace and Defense Market Revenue Share (%), by Military Aircraft and Systems 2024 & 2032

- Figure 28: Europe US Aerospace and Defense Market Revenue (Million), by Unmanned Aerial Systems 2024 & 2032

- Figure 29: Europe US Aerospace and Defense Market Revenue Share (%), by Unmanned Aerial Systems 2024 & 2032

- Figure 30: Europe US Aerospace and Defense Market Revenue (Million), by Space Systems and Equipment 2024 & 2032

- Figure 31: Europe US Aerospace and Defense Market Revenue Share (%), by Space Systems and Equipment 2024 & 2032

- Figure 32: Europe US Aerospace and Defense Market Revenue (Million), by Country 2024 & 2032

- Figure 33: Europe US Aerospace and Defense Market Revenue Share (%), by Country 2024 & 2032

- Figure 34: Middle East & Africa US Aerospace and Defense Market Revenue (Million), by Commercial and General Aviation 2024 & 2032

- Figure 35: Middle East & Africa US Aerospace and Defense Market Revenue Share (%), by Commercial and General Aviation 2024 & 2032

- Figure 36: Middle East & Africa US Aerospace and Defense Market Revenue (Million), by Military Aircraft and Systems 2024 & 2032

- Figure 37: Middle East & Africa US Aerospace and Defense Market Revenue Share (%), by Military Aircraft and Systems 2024 & 2032

- Figure 38: Middle East & Africa US Aerospace and Defense Market Revenue (Million), by Unmanned Aerial Systems 2024 & 2032

- Figure 39: Middle East & Africa US Aerospace and Defense Market Revenue Share (%), by Unmanned Aerial Systems 2024 & 2032

- Figure 40: Middle East & Africa US Aerospace and Defense Market Revenue (Million), by Space Systems and Equipment 2024 & 2032

- Figure 41: Middle East & Africa US Aerospace and Defense Market Revenue Share (%), by Space Systems and Equipment 2024 & 2032

- Figure 42: Middle East & Africa US Aerospace and Defense Market Revenue (Million), by Country 2024 & 2032

- Figure 43: Middle East & Africa US Aerospace and Defense Market Revenue Share (%), by Country 2024 & 2032

- Figure 44: Asia Pacific US Aerospace and Defense Market Revenue (Million), by Commercial and General Aviation 2024 & 2032

- Figure 45: Asia Pacific US Aerospace and Defense Market Revenue Share (%), by Commercial and General Aviation 2024 & 2032

- Figure 46: Asia Pacific US Aerospace and Defense Market Revenue (Million), by Military Aircraft and Systems 2024 & 2032

- Figure 47: Asia Pacific US Aerospace and Defense Market Revenue Share (%), by Military Aircraft and Systems 2024 & 2032

- Figure 48: Asia Pacific US Aerospace and Defense Market Revenue (Million), by Unmanned Aerial Systems 2024 & 2032

- Figure 49: Asia Pacific US Aerospace and Defense Market Revenue Share (%), by Unmanned Aerial Systems 2024 & 2032

- Figure 50: Asia Pacific US Aerospace and Defense Market Revenue (Million), by Space Systems and Equipment 2024 & 2032

- Figure 51: Asia Pacific US Aerospace and Defense Market Revenue Share (%), by Space Systems and Equipment 2024 & 2032

- Figure 52: Asia Pacific US Aerospace and Defense Market Revenue (Million), by Country 2024 & 2032

- Figure 53: Asia Pacific US Aerospace and Defense Market Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global US Aerospace and Defense Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global US Aerospace and Defense Market Revenue Million Forecast, by Commercial and General Aviation 2019 & 2032

- Table 3: Global US Aerospace and Defense Market Revenue Million Forecast, by Military Aircraft and Systems 2019 & 2032

- Table 4: Global US Aerospace and Defense Market Revenue Million Forecast, by Unmanned Aerial Systems 2019 & 2032

- Table 5: Global US Aerospace and Defense Market Revenue Million Forecast, by Space Systems and Equipment 2019 & 2032

- Table 6: Global US Aerospace and Defense Market Revenue Million Forecast, by Region 2019 & 2032

- Table 7: Global US Aerospace and Defense Market Revenue Million Forecast, by Country 2019 & 2032

- Table 8: Northeast US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Southeast US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Midwest US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Southwest US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: West US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Global US Aerospace and Defense Market Revenue Million Forecast, by Commercial and General Aviation 2019 & 2032

- Table 14: Global US Aerospace and Defense Market Revenue Million Forecast, by Military Aircraft and Systems 2019 & 2032

- Table 15: Global US Aerospace and Defense Market Revenue Million Forecast, by Unmanned Aerial Systems 2019 & 2032

- Table 16: Global US Aerospace and Defense Market Revenue Million Forecast, by Space Systems and Equipment 2019 & 2032

- Table 17: Global US Aerospace and Defense Market Revenue Million Forecast, by Country 2019 & 2032

- Table 18: United States US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Canada US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Mexico US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Global US Aerospace and Defense Market Revenue Million Forecast, by Commercial and General Aviation 2019 & 2032

- Table 22: Global US Aerospace and Defense Market Revenue Million Forecast, by Military Aircraft and Systems 2019 & 2032

- Table 23: Global US Aerospace and Defense Market Revenue Million Forecast, by Unmanned Aerial Systems 2019 & 2032

- Table 24: Global US Aerospace and Defense Market Revenue Million Forecast, by Space Systems and Equipment 2019 & 2032

- Table 25: Global US Aerospace and Defense Market Revenue Million Forecast, by Country 2019 & 2032

- Table 26: Brazil US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Argentina US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Rest of South America US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: Global US Aerospace and Defense Market Revenue Million Forecast, by Commercial and General Aviation 2019 & 2032

- Table 30: Global US Aerospace and Defense Market Revenue Million Forecast, by Military Aircraft and Systems 2019 & 2032

- Table 31: Global US Aerospace and Defense Market Revenue Million Forecast, by Unmanned Aerial Systems 2019 & 2032

- Table 32: Global US Aerospace and Defense Market Revenue Million Forecast, by Space Systems and Equipment 2019 & 2032

- Table 33: Global US Aerospace and Defense Market Revenue Million Forecast, by Country 2019 & 2032

- Table 34: United Kingdom US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 35: Germany US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: France US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 37: Italy US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: Spain US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 39: Russia US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 40: Benelux US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 41: Nordics US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: Rest of Europe US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 43: Global US Aerospace and Defense Market Revenue Million Forecast, by Commercial and General Aviation 2019 & 2032

- Table 44: Global US Aerospace and Defense Market Revenue Million Forecast, by Military Aircraft and Systems 2019 & 2032

- Table 45: Global US Aerospace and Defense Market Revenue Million Forecast, by Unmanned Aerial Systems 2019 & 2032

- Table 46: Global US Aerospace and Defense Market Revenue Million Forecast, by Space Systems and Equipment 2019 & 2032

- Table 47: Global US Aerospace and Defense Market Revenue Million Forecast, by Country 2019 & 2032

- Table 48: Turkey US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 49: Israel US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 50: GCC US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 51: North Africa US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 52: South Africa US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 53: Rest of Middle East & Africa US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 54: Global US Aerospace and Defense Market Revenue Million Forecast, by Commercial and General Aviation 2019 & 2032

- Table 55: Global US Aerospace and Defense Market Revenue Million Forecast, by Military Aircraft and Systems 2019 & 2032

- Table 56: Global US Aerospace and Defense Market Revenue Million Forecast, by Unmanned Aerial Systems 2019 & 2032

- Table 57: Global US Aerospace and Defense Market Revenue Million Forecast, by Space Systems and Equipment 2019 & 2032

- Table 58: Global US Aerospace and Defense Market Revenue Million Forecast, by Country 2019 & 2032

- Table 59: China US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 60: India US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 61: Japan US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 62: South Korea US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 63: ASEAN US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 64: Oceania US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 65: Rest of Asia Pacific US Aerospace and Defense Market Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the US Aerospace and Defense Market?

The projected CAGR is approximately 5.76%.

2. Which companies are prominent players in the US Aerospace and Defense Market?

Key companies in the market include Textron Inc, L3Harris Technologies Inc, THALES, General Dynamics Corporation, Rheinmetall AG, Lockheed Martin Corporation, Airbus SE, QinetiQ Group PLC, Naval Group, Fincantieri S p A, Safran SA, RTX Corporation, Embraer SA, Leonardo S p A, Rolls-Royce plc, BAE Systems plc, Northrop Grumman Corporation, The Boeing Company, GKN Aerospace.

3. What are the main segments of the US Aerospace and Defense Market?

The market segments include Commercial and General Aviation, Military Aircraft and Systems, Unmanned Aerial Systems, Space Systems and Equipment.

4. Can you provide details about the market size?

The market size is estimated to be USD 496.56 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

The Space Sector is Expected to Witness the Highest Growth During the Forecast Period.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "US Aerospace and Defense Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the US Aerospace and Defense Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the US Aerospace and Defense Market?

To stay informed about further developments, trends, and reports in the US Aerospace and Defense Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence