Key Insights

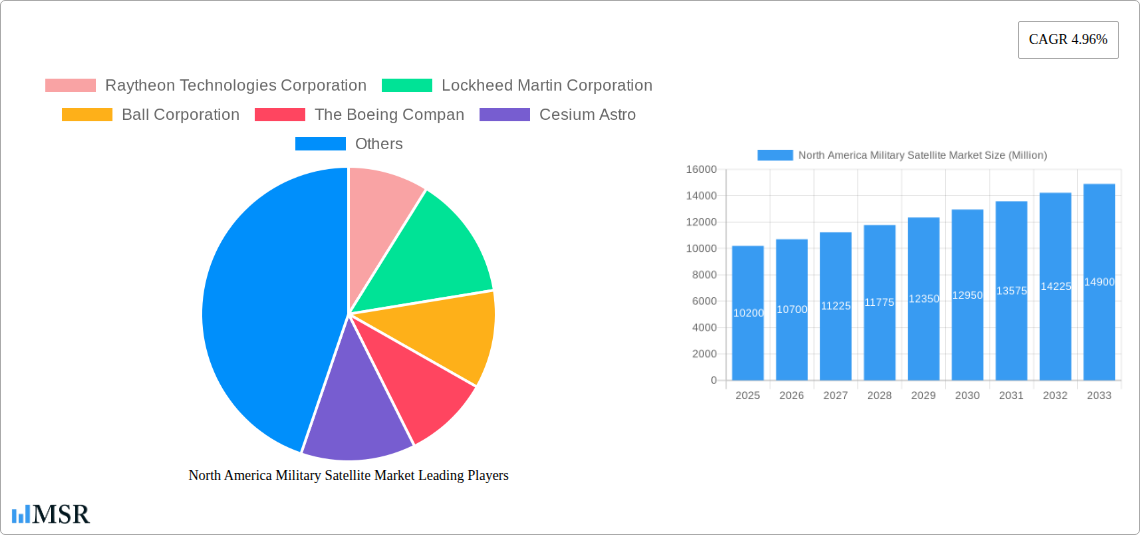

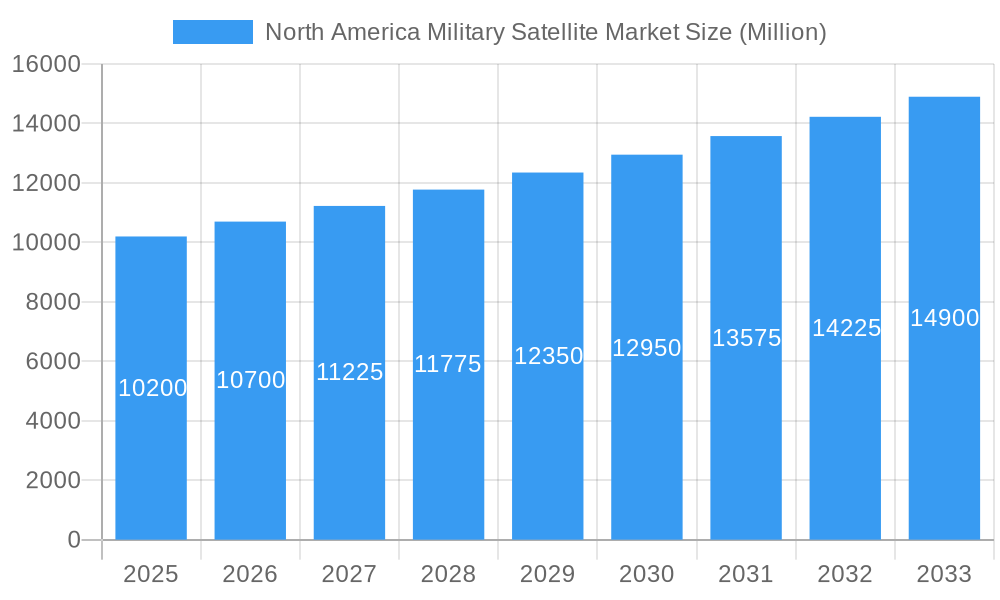

The North America Military Satellite Market is poised for robust growth, driven by increasing geopolitical tensions and the escalating need for advanced communication, navigation, and intelligence, surveillance, and reconnaissance (ISR) capabilities. With a current market size estimated around $10,200 million in 2025, the market is projected to expand at a Compound Annual Growth Rate (CAGR) of 4.96% over the forecast period of 2025-2033. This expansion is fueled by significant investments from the United States and Canada in modernizing their satellite constellations, emphasizing enhanced resilience and interoperability for joint operations. Key growth drivers include the demand for secure and reliable satellite communication systems for troop deployment, the necessity for precise navigation in complex operational environments, and the continuous evolution of earth observation technologies for battlefield awareness. The market is segmented across various satellite mass categories, with a notable inclination towards smaller, more agile satellites (Below 10 Kg and 10-100kg) that offer greater flexibility and reduced deployment costs, alongside continued investment in larger platforms for comprehensive data collection and communication relay.

North America Military Satellite Market Market Size (In Billion)

The competitive landscape features prominent defense contractors such as Raytheon Technologies Corporation, Lockheed Martin Corporation, Ball Corporation, The Boeing Company, and Northrop Grumman Corporation, alongside emerging players like Cesium Astro. These companies are actively engaged in developing and deploying next-generation military satellite systems, focusing on innovations in satellite subsystems like propulsion hardware and solar arrays to enhance mission endurance and capability. Trends in the market indicate a strong emphasis on the LEO (Low Earth Orbit) and MEO (Medium Earth Orbit) classes for their advantages in lower latency and global coverage, particularly for communication and ISR applications. While the market is driven by technological advancements and strategic imperatives, potential restraints include budget constraints within defense departments and the increasing complexity of cybersecurity threats targeting space assets. Nonetheless, the strategic importance of space-based assets for national security is expected to ensure sustained investment and innovation within the North American military satellite sector.

North America Military Satellite Market Company Market Share

This comprehensive report delves into the North America Military Satellite Market, providing an in-depth analysis of its current landscape and future projections. Covering the period from 2019 to 2033, with a base year of 2025, this study offers critical insights into market dynamics, key segments, technological advancements, and strategic opportunities. We examine the influence of major players like Raytheon Technologies Corporation, Lockheed Martin Corporation, Ball Corporation, The Boeing Company, Cesium Astro, and Northrop Grumman Corporation across various satellite mass categories (Below 10 Kg, 10-100kg, 100-500kg, 500-1000kg, above 1000kg), orbit classes (LEO, MEO, GEO), satellite subsystems (Propulsion Hardware and Propellant, Satellite Bus & Subsystems, Solar Array & Power Hardware, Structures, Harness & Mechanisms), and applications (Communication, Earth Observation, Navigation, Space Observation, Others). Understand the market concentration, innovation ecosystems, regulatory frameworks, and competitive landscape to navigate this evolving sector.

North America Military Satellite Market Market Concentration & Dynamics

The North America Military Satellite Market is characterized by a moderate to high concentration, with a few key players dominating the landscape. Innovation ecosystems are robust, fueled by significant government investment in defense and space capabilities. Regulatory frameworks, primarily driven by national security interests and international treaties, play a crucial role in shaping market entry and operational parameters. Substitute products, though limited in the military domain due to stringent requirements, primarily revolve around enhanced terrestrial or airborne communication and surveillance technologies. End-user trends are heavily influenced by the demand for real-time intelligence, secure communication, and advanced reconnaissance capabilities. Mergers and acquisitions (M&A) activities, while strategic, are less frequent due to the specialized nature of the industry and the presence of established, high-barrier-to-entry players. Market share distribution is heavily skewed towards the leading defense contractors, with smaller, agile companies like Cesium Astro carving out niches in specific sub-systems and small satellite solutions. The total number of M&A deals in the past five years is estimated to be between 5-8, primarily focused on acquiring specialized technology or expanding existing capabilities.

North America Military Satellite Market Industry Insights & Trends

The North America Military Satellite Market is experiencing significant growth, driven by an escalating geopolitical landscape and the increasing reliance of defense forces on space-based assets for mission success. The market size for North America military satellites is projected to reach approximately $35,000 Million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of around 7.5% from 2025. Key growth drivers include the continuous need for enhanced communication networks for global operations, sophisticated Earth observation capabilities for intelligence gathering and situational awareness, and precise navigation systems for military deployments. Technological disruptions are primarily centered around miniaturization of satellites (CubeSats and SmallSats), advancements in propulsion systems for greater maneuverability, improved power generation through advanced solar arrays, and the development of resilient satellite bus and subsystems capable of withstanding electronic warfare and cyber threats. Evolving consumer behaviors, within the military context, translate to a demand for more agile, cost-effective, and rapidly deployable satellite solutions. This includes a growing interest in LEO constellations for persistent surveillance and communication, as well as the integration of artificial intelligence and machine learning for faster data processing and analysis. The increasing threat landscape necessitates the development of hardened satellites and resilient communication architectures, further propelling market expansion. The market is also witnessing a trend towards enhanced cybersecurity measures for satellites, protecting them from adversarial attacks and ensuring the integrity of critical data.

Key Markets & Segments Leading North America Military Satellite Market

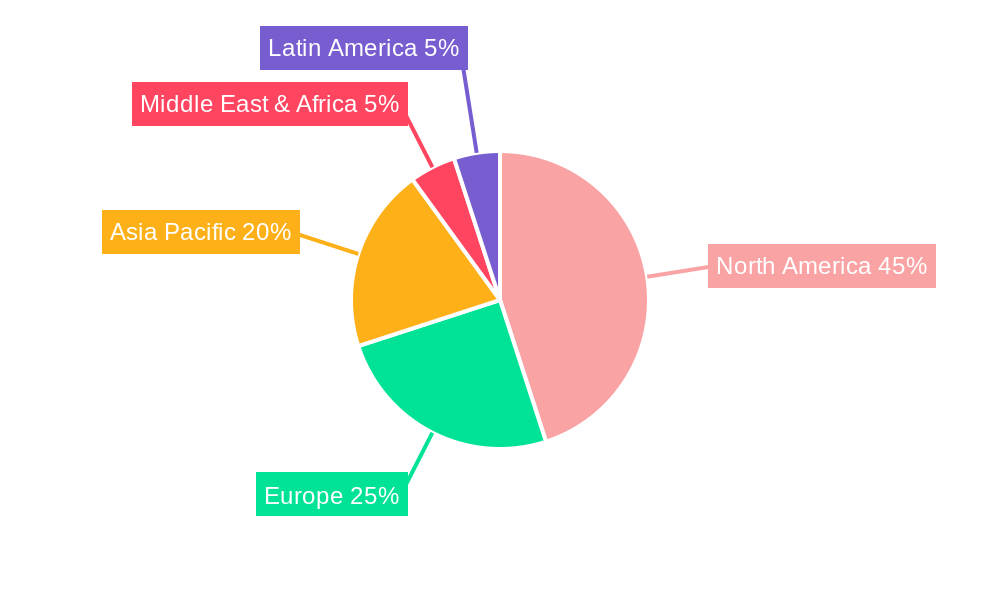

The North America Military Satellite Market is heavily dominated by the United States, which accounts for approximately 85% of the total market share. This dominance is attributed to its extensive defense budget, significant investment in space technology, and the presence of leading aerospace and defense companies.

- Satellite Mass: The 100-500kg and above 1000kg segments are currently leading due to the demand for sophisticated intelligence, surveillance, and reconnaissance (ISR) platforms and larger communication satellites. However, the Below 10 Kg segment is experiencing the fastest growth due to the increasing adoption of small satellites for specialized missions and constellations, driven by cost-effectiveness and faster deployment cycles.

- Drivers for Below 10 Kg Growth: Reduced development costs, rapid technological advancements in miniaturization, and the need for flexible, distributed satellite architectures.

- Orbit Class: The LEO (Low Earth Orbit) segment is witnessing substantial growth, driven by the deployment of large constellations for persistent surveillance and communication, offering lower latency. GEO (Geostationary Orbit) satellites remain critical for strategic communication and early warning systems, maintaining a significant market share. MEO (Medium Earth Orbit) is gaining traction for navigation systems like GPS.

- Drivers for LEO Growth: Demand for continuous coverage, reduced signal latency, and the modularity of constellation deployment.

- Satellite Subsystem: Satellite Bus & Subsystems represent the largest segment due to the comprehensive nature of these components essential for overall satellite functionality. Solar Array & Power Hardware is also a significant segment, driven by the continuous need for reliable power for extended missions. Propulsion Hardware and Propellant are critical for orbital maneuvering and station-keeping, experiencing steady growth.

- Drivers for Satellite Bus & Subsystems: Integration of advanced avionics, robust thermal control systems, and improved structural integrity for harsh space environments.

- Application: Communication and Navigation are the dominant applications, reflecting the fundamental need for secure, reliable global connectivity and precise positioning for military operations. Earth Observation is also a crucial application, providing vital intelligence and environmental monitoring capabilities, with increasing demand for higher resolution imagery and faster revisit rates.

- Drivers for Communication & Navigation Dominance: Global operational requirements, precision warfare, and secure data transmission needs.

North America Military Satellite Market Product Developments

Product development in the North America Military Satellite Market is characterized by a relentless pursuit of enhanced performance, miniaturization, and resilience. Companies are focusing on developing advanced sensor payloads for Earth observation, next-generation communication payloads for secure and high-bandwidth data transmission, and more efficient and reliable propulsion systems. The integration of AI and machine learning into satellite operations, for tasks like autonomous navigation and data analysis, is a key area of innovation. The development of smaller, more modular satellite components allows for greater flexibility in mission design and faster deployment of new capabilities. These advancements are crucial for maintaining a technological edge in a rapidly evolving defense landscape.

Challenges in the North America Military Satellite Market Market

The North America Military Satellite Market faces several challenges, including high research and development costs associated with cutting-edge technologies, long development cycles, and stringent regulatory approval processes. Supply chain vulnerabilities, particularly for specialized components, can lead to delays and cost overruns. Intense competition from both established players and emerging companies focused on disruptive technologies also presents a significant challenge. Furthermore, the ever-increasing threat of space debris and the potential for adversarial interference in space operations necessitate continuous investment in more robust and resilient satellite systems, adding to the overall cost burden.

Forces Driving North America Military Satellite Market Growth

Several key factors are propelling the growth of the North America Military Satellite Market. The escalating geopolitical tensions and the increasing importance of space-based assets for national security are primary drivers. The continuous demand for enhanced intelligence, surveillance, and reconnaissance (ISR) capabilities, coupled with the need for secure and reliable military communication systems, fuels investment. Furthermore, advancements in satellite technology, including miniaturization and improved propulsion systems, are making space-based solutions more accessible and versatile. Favorable government policies and increased defense spending in North America, particularly in the United States, provide a strong foundation for market expansion.

Challenges in the North America Military Satellite Market Market

Long-term growth catalysts for the North America Military Satellite Market are deeply rooted in ongoing technological innovation and strategic market expansion. The development of more resilient satellite architectures capable of withstanding advanced electronic warfare and cyber threats is a critical area of focus. Partnerships between government agencies and private sector entities are fostering innovation and accelerating the development of next-generation capabilities. The potential for increased international collaboration on space-based defense initiatives could also unlock new growth avenues. Moreover, the continuous evolution of space technology, such as advanced artificial intelligence for satellite autonomy and enhanced data processing, will be crucial for maintaining a strategic advantage and ensuring sustained market growth.

Emerging Opportunities in North America Military Satellite Market

Emerging opportunities in the North America Military Satellite Market lie in the development and deployment of large LEO satellite constellations for persistent ISR and communication, offering enhanced global coverage and lower latency. The growing demand for secure, encrypted communication solutions for tactical operations presents another significant opportunity. Furthermore, the increasing integration of artificial intelligence and machine learning into satellite systems for data analysis and autonomous operations is a key trend. The market also sees opportunities in providing specialized subsystems and services for the rapidly growing small satellite sector. The modernization of existing satellite infrastructure and the development of more resilient and adaptable systems for future warfare scenarios are also significant growth areas.

Leading Players in the North America Military Satellite Market Sector

- Raytheon Technologies Corporation

- Lockheed Martin Corporation

- Ball Corporation

- The Boeing Company

- Cesium Astro

- Northrop Grumman Corporation

Key Milestones in North America Military Satellite Market Industry

- November 2023: Ball Aerospace was selected by the US Air Force's Space and Missile Systems Center (SMC) to deliver the next-generation operational environmental satellite system, Weather System Follow-on - Microwave (WSF-M), for the Department of Defense (DoD).

- February 2023: Blue Canyon Technologies LLC, a subsidiary of Raytheon Technologies, provided critical hardware components for several of the smallsat missions aboard the Transporter-6 launch, which pitched 114 small payloads into polar orbit.

- February 2023: Blue Canyon Technologies LLC, a subsidiary of Raytheon Technologies, provided critical hardware components for several of the SmallSat missions aboard the Transporter-6 launch that pitched 114 small payloads into polar orbit.

Strategic Outlook for North America Military Satellite Market Market

The strategic outlook for the North America Military Satellite Market remains exceptionally strong, driven by ongoing government investment in national security and technological advancement. Future growth will be propelled by the continued development of resilient, secure, and agile satellite systems, emphasizing LEO constellations for persistent coverage and advanced ISR capabilities. Strategic partnerships between government entities and private sector innovators will accelerate the adoption of new technologies, including AI and advanced propulsion. The focus on miniaturization and modularity in satellite design will enable faster deployment and greater mission flexibility. The market is poised for sustained expansion as defense forces globally prioritize space-based assets for their operational superiority and information dominance.

North America Military Satellite Market Segmentation

-

1. Satellite Mass

- 1.1. 10-100kg

- 1.2. 100-500kg

- 1.3. 500-1000kg

- 1.4. Below 10 Kg

- 1.5. above 1000kg

-

2. Orbit Class

- 2.1. GEO

- 2.2. LEO

- 2.3. MEO

-

3. Satellite Subsystem

- 3.1. Propulsion Hardware and Propellant

- 3.2. Satellite Bus & Subsystems

- 3.3. Solar Array & Power Hardware

- 3.4. Structures, Harness & Mechanisms

-

4. Application

- 4.1. Communication

- 4.2. Earth Observation

- 4.3. Navigation

- 4.4. Space Observation

- 4.5. Others

North America Military Satellite Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Military Satellite Market Regional Market Share

Geographic Coverage of North America Military Satellite Market

North America Military Satellite Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Satellite Mass

- 5.1.1. 10-100kg

- 5.1.2. 100-500kg

- 5.1.3. 500-1000kg

- 5.1.4. Below 10 Kg

- 5.1.5. above 1000kg

- 5.2. Market Analysis, Insights and Forecast - by Orbit Class

- 5.2.1. GEO

- 5.2.2. LEO

- 5.2.3. MEO

- 5.3. Market Analysis, Insights and Forecast - by Satellite Subsystem

- 5.3.1. Propulsion Hardware and Propellant

- 5.3.2. Satellite Bus & Subsystems

- 5.3.3. Solar Array & Power Hardware

- 5.3.4. Structures, Harness & Mechanisms

- 5.4. Market Analysis, Insights and Forecast - by Application

- 5.4.1. Communication

- 5.4.2. Earth Observation

- 5.4.3. Navigation

- 5.4.4. Space Observation

- 5.4.5. Others

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Satellite Mass

- 6. North America Military Satellite Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Satellite Mass

- 6.1.1. 10-100kg

- 6.1.2. 100-500kg

- 6.1.3. 500-1000kg

- 6.1.4. Below 10 Kg

- 6.1.5. above 1000kg

- 6.2. Market Analysis, Insights and Forecast - by Orbit Class

- 6.2.1. GEO

- 6.2.2. LEO

- 6.2.3. MEO

- 6.3. Market Analysis, Insights and Forecast - by Satellite Subsystem

- 6.3.1. Propulsion Hardware and Propellant

- 6.3.2. Satellite Bus & Subsystems

- 6.3.3. Solar Array & Power Hardware

- 6.3.4. Structures, Harness & Mechanisms

- 6.4. Market Analysis, Insights and Forecast - by Application

- 6.4.1. Communication

- 6.4.2. Earth Observation

- 6.4.3. Navigation

- 6.4.4. Space Observation

- 6.4.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Satellite Mass

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Raytheon Technologies Corporation

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Lockheed Martin Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Ball Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 The Boeing Compan

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Cesium Astro

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Northrop Grumman Corporation

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.1 Raytheon Technologies Corporation

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Military Satellite Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Military Satellite Market Share (%) by Company 2025

List of Tables

- Table 1: North America Military Satellite Market Revenue billion Forecast, by Satellite Mass 2020 & 2033

- Table 2: North America Military Satellite Market Revenue billion Forecast, by Orbit Class 2020 & 2033

- Table 3: North America Military Satellite Market Revenue billion Forecast, by Satellite Subsystem 2020 & 2033

- Table 4: North America Military Satellite Market Revenue billion Forecast, by Application 2020 & 2033

- Table 5: North America Military Satellite Market Revenue billion Forecast, by Region 2020 & 2033

- Table 6: North America Military Satellite Market Revenue billion Forecast, by Satellite Mass 2020 & 2033

- Table 7: North America Military Satellite Market Revenue billion Forecast, by Orbit Class 2020 & 2033

- Table 8: North America Military Satellite Market Revenue billion Forecast, by Satellite Subsystem 2020 & 2033

- Table 9: North America Military Satellite Market Revenue billion Forecast, by Application 2020 & 2033

- Table 10: North America Military Satellite Market Revenue billion Forecast, by Country 2020 & 2033

- Table 11: United States North America Military Satellite Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Canada North America Military Satellite Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Mexico North America Military Satellite Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Military Satellite Market?

The projected CAGR is approximately 6.8%.

2. Which companies are prominent players in the North America Military Satellite Market?

Key companies in the market include Raytheon Technologies Corporation, Lockheed Martin Corporation, Ball Corporation, The Boeing Compan, Cesium Astro, Northrop Grumman Corporation.

3. What are the main segments of the North America Military Satellite Market?

The market segments include Satellite Mass, Orbit Class, Satellite Subsystem, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 15.7 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

November 2023: Ball Aerospace was selected by the US Air Force's Space and Missile Systems Center (SMC) to deliver the next-generation operational environmental satellite system, Weather System Follow-on - Microwave (WSF-M), for the Department of Defense (DoD).February 2023: Blue Canyon Technologies LLC, a subsidiary of Raytheon Technologies, provided critical hardware components for several of the smallsat missions aboard the Transporter-6 launch, which pitched 114 small payloads into polar orbit.February 2023: Blue Canyon Technologies LLC, a subsidiary of Raytheon Technologies, provided critical hardware components for several of the SmallSat missions aboard the Transporter-6 launch that pitched 114 small payloads into polar orbit.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Military Satellite Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Military Satellite Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Military Satellite Market?

To stay informed about further developments, trends, and reports in the North America Military Satellite Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence