Key Insights into the Automotive ADAS Industry

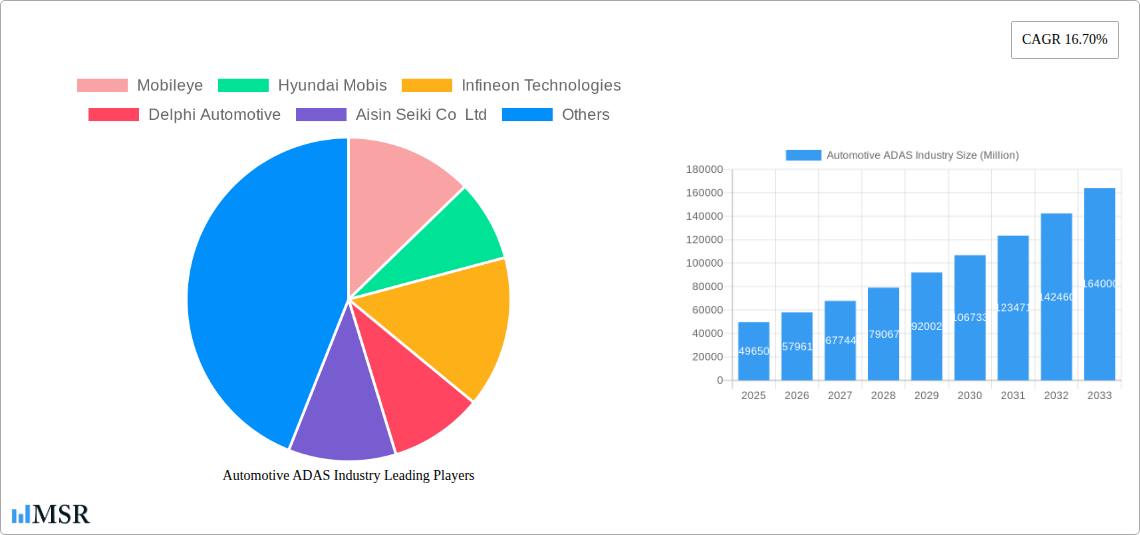

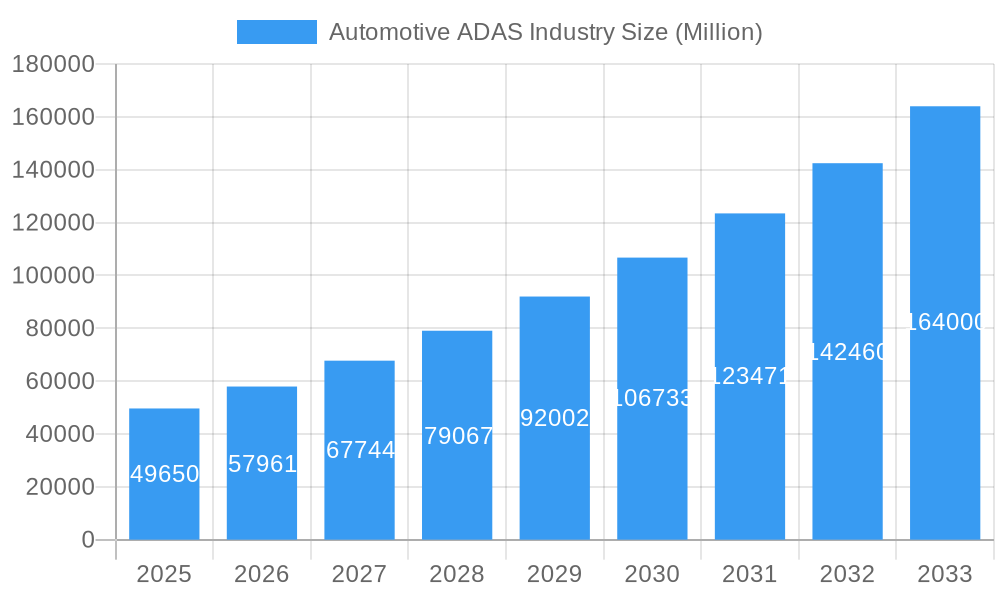

The Automotive ADAS Industry, critical for enhancing vehicle safety and paving the way for autonomous mobility, was valued at $49.65 Million in 2023. This sector is projected for substantial expansion, anticipating a robust Compound Annual Growth Rate (CAGR) of 16.70% from 2023 to 2034. By the end of this forecast period, the global Automotive ADAS Industry is expected to reach a valuation of approximately $276.41 Million. This impressive growth is fundamentally driven by the increasing sales of autonomous vehicles, a trend propelled by technological advancements and evolving regulatory landscapes. The integration of advanced sensors and sophisticated software algorithms continues to be a cornerstone of ADAS evolution, enabling features such as adaptive cruise control, lane keeping assist, and automatic emergency braking.

Automotive ADAS Industry Market Size (In Million)

The industry's trajectory is further supported by a confluence of macro tailwinds. Stricter global vehicle safety regulations, mandating the inclusion of specific ADAS features in new vehicles, are acting as a primary catalyst. Consumer demand for enhanced comfort, convenience, and safety in vehicles is also fueling adoption rates, particularly in the premium and mid-range passenger vehicle segments. Furthermore, the rapid progress in artificial intelligence, machine learning, and sensor fusion technologies is continually expanding the capabilities and reliability of ADAS systems, reducing the technological barrier to broader implementation. While the high cost of installation related to ADAS systems remains a significant restraint, particularly for entry-level and commercial vehicles, ongoing innovations in manufacturing and scaling of production are expected to mitigate this challenge over the long term. The strategic imperative for automakers to differentiate their offerings and comply with safety standards ensures continued investment and innovation within the Automotive ADAS Industry, solidifying its pivotal role in the future of transportation. The burgeoning Autonomous Driving Technology Market is directly intertwined with the growth of advanced ADAS, as the foundational elements of ADAS are prerequisites for higher levels of vehicle autonomy.

Automotive ADAS Industry Company Market Share

Passenger Car ADAS Market Dominance in the Automotive ADAS Industry

The passenger car segment currently holds the highest market share within the Automotive ADAS Industry, primarily driven by stringent safety regulations, high consumer adoption rates, and the continuous integration of advanced technologies. The widespread production volume of passenger vehicles globally provides a vast base for ADAS penetration, making the Passenger Car ADAS Market the dominant segment in terms of revenue. This dominance is attributed to several factors. Firstly, governmental bodies and safety organizations worldwide, such as Euro NCAP and NHTSA, have been instrumental in advocating and eventually mandating the inclusion of features like Automatic Emergency Braking (AEB) and Lane Departure Warning (LDW) in new passenger cars. These regulatory pressures significantly accelerate the adoption of ADAS technologies in this segment.

Secondly, consumer preferences play a crucial role. Modern car buyers increasingly prioritize safety, convenience, and technological sophistication. ADAS features, including Adaptive Cruise Control (ACC) and Blind Spot Detection (BSD), enhance the driving experience and provide a sense of security, making them highly desirable attributes in new vehicle purchases. Automakers are leveraging these features as key differentiators, packaging them into premium trims or offering them as standard across their model lineups to attract discerning customers. The trend of urbanization and the increasing number of private vehicle owners globally further amplify the demand for safer and smarter cars, directly contributing to the growth of the Passenger Car ADAS Market.

Key players in the Automotive ADAS Industry, such as Robert Bosch GmbH, Continental AG, and Mobileye, are heavily invested in developing solutions specifically tailored for passenger vehicles, ranging from basic L1 systems to more advanced L2 and L2+ functionalities. These companies focus on enhancing sensor performance, optimizing algorithms, and improving the human-machine interface to deliver seamless and reliable ADAS experiences. While the Commercial Vehicle ADAS Market is also growing due to safety and efficiency mandates, the sheer volume and consumer-driven innovation in passenger cars ensure its sustained lead. The segment is expected to continue its growth trajectory, with increasing penetration of L3 autonomous features and widespread adoption of advanced sensor suites, including radar, camera, and LiDAR Sensor Market technologies, pushing the boundaries of what is possible in conventional driving scenarios.

Key Market Drivers and Constraints in the Automotive ADAS Industry

The Automotive ADAS Industry's expansion is primarily propelled by the increasing sales of autonomous vehicles, which serves as a foundational driver for technological evolution and market penetration. As vehicle manufacturers worldwide accelerate their efforts towards higher levels of autonomous driving, the demand for sophisticated ADAS components and systems intensifies. These systems, ranging from Adaptive Cruise Control System Market offerings to advanced perception modules, form the essential building blocks for L2 to L5 autonomous capabilities. For instance, the global push for L2+ and L3 features in mass-market vehicles means that functionalities like advanced lane-keeping assist, traffic jam assist, and hands-off highway driving rely heavily on robust ADAS platforms. The projected growth in sales of vehicles equipped with at least L2 autonomy is directly correlated with the growth of the Automotive ADAS Industry, as every autonomous feature requires a complex interplay of ADAS components.

Conversely, a significant restraint on the Automotive ADAS Industry's growth is the high cost of installation related to ADAS systems. Implementing a comprehensive suite of ADAS features, including radar sensors, camera sensors, LiDAR sensors, and ultrasonic sensors, along with the necessary Electronic Control Units (ECUs) and wiring harnesses, represents a substantial addition to the vehicle’s overall manufacturing cost. This elevated cost often translates into higher retail prices for consumers, which can deter adoption, particularly in price-sensitive markets or for entry-level vehicle segments. For example, a full-featured ADAS package can add thousands of dollars to the price of a vehicle, making it less accessible to a broader consumer base. The complexity of integrating these systems, which requires extensive calibration, testing, and validation, also contributes to the overall expense. Furthermore, the specialized skills and equipment required for maintenance and repair of these advanced systems post-sale can add to the long-term cost of ownership, thereby impacting consumer perception and market penetration. Overcoming this cost barrier through economies of scale, component miniaturization, and standardized integration methodologies will be crucial for accelerating the widespread adoption of ADAS technologies.

Competitive Ecosystem of Automotive ADAS Industry

- Mobileye: A global leader in the development of computer vision and machine learning-based sensing, data analysis, localization, and mapping for ADAS and autonomous driving. Their solutions are widely adopted by major automotive manufacturers for a range of safety features.

- Hyundai Mobis: A prominent automotive supplier focusing on advanced technologies, including intelligent safety systems, infotainment, and future mobility solutions. They are actively expanding their ADAS portfolio to support L2+ and L3 autonomous driving functionalities.

- Infineon Technologies: A key provider of semiconductor solutions for automotive applications, including microcontrollers, sensors, and power semiconductors essential for ADAS functionality. Their chips power critical components in radar, camera, and ultrasonic systems.

- Delphi Automotive: A technology company now known as Aptiv, specializing in advanced safety, electrification, and connectivity solutions. They offer a comprehensive suite of ADAS technologies, including perception systems, software, and computing platforms.

- Aisin Seiki Co Ltd: A global Tier 1 supplier primarily known for drivetrain and chassis components, expanding its focus into intelligent parking assist systems, automatic emergency braking, and other ADAS technologies to enhance vehicle safety and convenience.

- Continental AG: A major automotive supplier providing advanced driver assistance systems, including radar and camera sensors, electronic control units, and software. They are a leading innovator in functional safety and system integration for autonomous driving.

- Autoliv Inc: A global leader in automotive safety systems, developing and manufacturing airbags, seatbelts, and steering wheels, with an increasing focus on active safety solutions like radar and vision systems for ADAS applications.

- Robert Bosch GmbH: A diversified technology company and a top automotive supplier, offering a vast array of ADAS components and systems, from sensors and control units to software solutions for automated driving functions.

- Hella KGAA Hueck & Co: Specializing in lighting and electronics, Hella develops sophisticated sensor technologies like radar and camera systems for ADAS, contributing to environmental perception and driver assistance functions.

- Magna International: A leading global mobility technology company providing a range of automotive components and systems, including ADAS sensors, electronic control units, and complete vehicle assembly solutions, with a strong focus on advanced driver assistance systems.

- Valeo SA: A French automotive supplier known for its innovative solutions in powertrain electrification, thermal systems, and advanced driver assistance systems. Valeo is a significant player in parking assistance, camera systems, and LiDAR technology.

- DENSO Corporation: A leading global automotive component manufacturer offering a broad portfolio of products, including ADAS components such as millimeter-wave radar, vision sensors, and ECUs for safety and driving assistance functions.

- WABCO Vehicle Control Services: Now part of ZF Friedrichshafen AG, WABCO was a global provider of electronic braking, stability, and transmission automation systems for commercial vehicles, playing a key role in ADAS for trucks and buses.

- ZF Friedrichshafen AG: A global technology company supplying systems for passenger cars, commercial vehicles, and industrial technology, with a robust portfolio in ADAS sensors, electronic control units, and integrated solutions for automated driving.

Recent Developments & Milestones in Automotive ADAS Industry

- December 2023: ECARX Holdings Inc., a global mobility technology provider, partnered with Black Sesame Technologies and BlackBerry Limited to deploy the Skyland ADAS platform in Lynk & Co’s flagship SUV, the Lynk & Co 08. This collaboration involved the integration of BlackBerry QNX Neutrino Real-Time Operating System (RTOS) and Black Sesame Technologies’ Huashan II A1000 ADAS computing chip in the ECARX Skyland Pro. This development highlights the growing trend of strategic alliances for advanced ADAS system integration, leveraging specialized expertise from various technology providers.

- December 2023: Magna, a leading global mobility technology company, enhanced its automated driving capabilities by joining NorthStar – Telia Sweden and Ericsson’s 5G innovation program for industrial enterprises. As part of the agreement, Telia and Ericsson built a dedicated, private 5G network at Magna’s test track located in Vårgårda, Sweden, where new cutting-edge advanced driver assistance system (ADAS) solutions in vehicle-to-vehicle (V2V) and vehicle-to-everything (V2X) connectivity are being trialed. This initiative underscores the critical role of next-generation connectivity, particularly 5G technology, in advancing ADAS and Autonomous Driving Technology Market functionalities.

Regional Market Breakdown for Automotive ADAS Industry

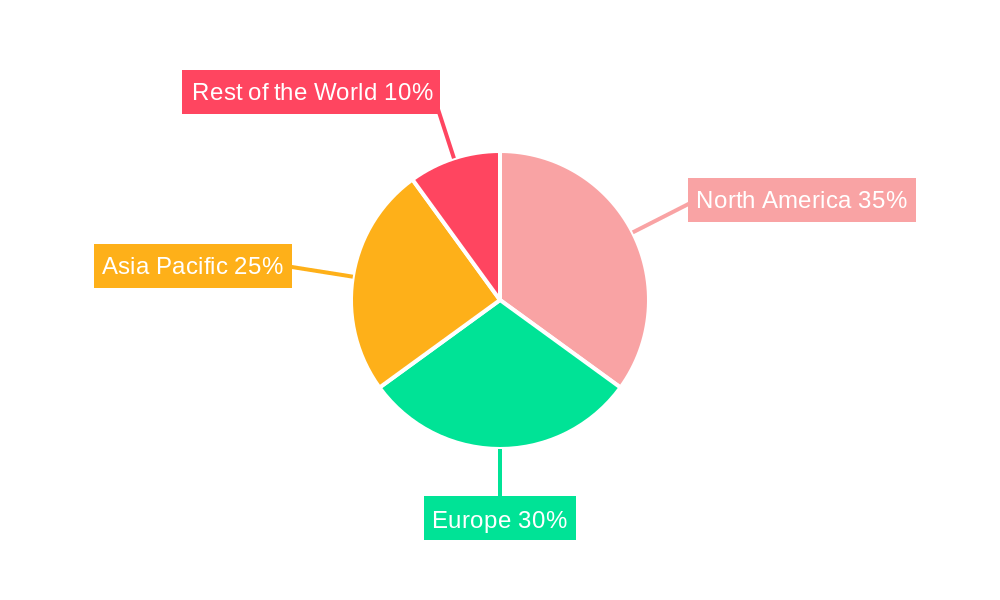

The Automotive ADAS Industry exhibits diverse growth dynamics across different global regions, influenced by varying regulatory frameworks, consumer preferences, and technological adoption rates. Asia Pacific, encompassing economic powerhouses like China, Japan, India, and South Korea, is anticipated to be the fastest-growing region. This growth is spurred by increasing vehicle production, a rapidly expanding middle class demanding safer and more technologically advanced vehicles, and strong governmental support for smart transportation initiatives. China, in particular, is a major driver, with domestic manufacturers rapidly integrating advanced ADAS features to compete with international brands. The burgeoning Passenger Car ADAS Market in these economies is a key factor.

North America, including the United States and Canada, represents a mature yet continually expanding market for the Automotive ADAS Industry. Here, growth is primarily driven by technological innovation, high consumer awareness of safety features, and a strong regulatory push from bodies like the NHTSA to reduce road fatalities. The region is a hub for R&D in autonomous driving and Vehicle Safety System Market solutions, fostering rapid adoption of new ADAS technologies. Europe also holds a substantial revenue share, characterized by stringent safety regulations from the UNECE and Euro NCAP, which mandate features such as Automatic Emergency Braking (AEB) and Lane Departure Warning (LDW). This regulatory environment accelerates the penetration of ADAS features, ensuring a steady, albeit more mature, growth trajectory.

The Rest of the World (RoW), including South America, the Middle East, and Africa, is an emerging market for the Automotive ADAS Industry. While current adoption rates may be lower due to cost sensitivities and less mature regulatory landscapes, these regions present significant long-term growth potential. Increasing urbanization, infrastructure development, and growing awareness of road safety are expected to stimulate demand for ADAS features, particularly basic L1 and L2 systems, in the coming years. Manufacturers are increasingly looking to tailor cost-effective ADAS solutions for these markets.

Automotive ADAS Industry Regional Market Share

Supply Chain & Raw Material Dynamics for Automotive ADAS Industry

Key to the functioning and evolution of the Automotive ADAS Industry is a complex and often vulnerable supply chain, heavily reliant on specialized components and raw materials. Upstream dependencies are primarily centered on the Automotive Semiconductor Market, which provides the critical microcontrollers, system-on-chips (SoCs), and application-specific integrated circuits (ASICs) necessary for processing sensor data, running AI algorithms, and controlling ADAS functions. Beyond semiconductors, the industry relies on high-quality optical components for camera systems, specialized materials for radar antennas, and precision components for LiDAR units, including lasers and photodetectors. The availability and pricing of rare earth elements, while not dominant, can also impact certain advanced sensor components.

Sourcing risks are multifaceted, ranging from geopolitical tensions affecting the global semiconductor supply to natural disasters impacting manufacturing hubs. The recent global chip shortage, exacerbated by the COVID-19 pandemic and subsequent surges in demand, starkly illustrated the fragility of this supply chain. This event led to significant production delays for automakers, directly impacting the deployment timelines of new vehicles equipped with advanced ADAS features. Price volatility for key inputs, particularly for silicon wafers and certain metals used in electronic components, adds another layer of complexity. For instance, the demand for advanced packaging materials for high-performance ADAS processors drives up costs. Manufacturers in the Automotive ADAS Industry must navigate these challenges by diversifying their supplier base, fostering stronger vertical integration, and exploring regionalized sourcing strategies to build resilience. Furthermore, the development of software-defined vehicles is shifting some dependencies, but the core hardware, including components for the LiDAR Sensor Market and Driver Monitoring System Market, remains crucial.

Regulatory & Policy Landscape Shaping Automotive ADAS Industry

The Automotive ADAS Industry operates within a rapidly evolving regulatory and policy landscape, which significantly influences product development, market adoption, and safety standards across key geographies. Major regulatory frameworks, such as those established by the United Nations Economic Commission for Europe (UNECE) and the National Highway Traffic Safety Administration (NHTSA) in the United States, play a pivotal role. UNECE regulations, particularly those concerning Automatic Emergency Braking (AEB) and Lane Departure Warning (LDW), have been instrumental in mandating these features in new vehicles across signatory countries. Similarly, consumer safety rating programs like Euro NCAP and C-NCAP in China incentivize automakers to integrate advanced ADAS features by awarding higher safety ratings, thereby accelerating market penetration and driving technological innovation.

Standardization efforts by bodies such as the International Organization for Standardization (ISO), particularly ISO 26262 for functional safety in road vehicles, provide essential guidelines for the development and validation of ADAS hardware and software. These standards ensure the reliability and safety of systems, from the basic Adaptive Cruise Control System Market offerings to complex multi-sensor fusion platforms. Recent policy changes include an increasing global trend towards making certain ADAS features standard rather than optional, reflecting a growing governmental commitment to enhancing road safety. For example, several countries are exploring or have already implemented mandates for features like Driver Monitoring System Market technologies to combat distracted and drowsy driving.

Government policies are also actively promoting the research, development, and deployment of autonomous driving technologies, which inherently build upon ADAS foundations. Initiatives such as investing in intelligent infrastructure for V2X (vehicle-to-everything) communication and creating regulatory sandboxes for testing autonomous vehicles demonstrate a concerted effort to foster the ecosystem for future mobility. The projected impact of these policies includes accelerated innovation, increased standardization, enhanced consumer trust, and ultimately, a safer and more efficient global transportation system. Compliance with diverse, and sometimes conflicting, regional regulations remains a challenge for global players in the Automotive ADAS Industry, necessitating agile product development and robust certification processes.

Automotive ADAS Industry Segmentation

-

1. System Type

- 1.1. Adaptive Cruise Control (ACC)

- 1.2. Automatic Emergency Braking (AEB)

- 1.3. Lane Departure Warning (LDW)

- 1.4. Blind Spot Detection (BSD).

- 1.5. Forward Collision Warning (FCW)

- 1.6. Driver Monitoring System (DMS)

- 1.7. Others

-

2. Sensor Type

- 2.1. Radar Sensors

- 2.2. Camera Sensors

- 2.3. LiDAR Sensors

- 2.4. Ultrasonic Sensors

- 2.5. Infrared Sensors

- 2.6. Others

-

3. LOA

- 3.1. L1

- 3.2. L2

- 3.3. L3

- 3.4. L4

- 3.5. L5

-

4. Sales Channel

- 4.1. Passenger Cars

- 4.2. Light Commercial Vehicles (LCV)

- 4.3. Heavy Commercial Vehicles (HCV)

-

5. Vehicle Type

- 5.1. OEM

- 5.2. Sales Channel

Automotive ADAS Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Russia

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. South Korea

- 3.5. Australia

- 3.6. Rest of Asia Pacific

-

4. Rest of the World

- 4.1. South America

- 4.2. Middle East and Africa

Automotive ADAS Industry Regional Market Share

Geographic Coverage of Automotive ADAS Industry

Automotive ADAS Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16.70% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by System Type

- 5.1.1. Adaptive Cruise Control (ACC)

- 5.1.2. Automatic Emergency Braking (AEB)

- 5.1.3. Lane Departure Warning (LDW)

- 5.1.4. Blind Spot Detection (BSD).

- 5.1.5. Forward Collision Warning (FCW)

- 5.1.6. Driver Monitoring System (DMS)

- 5.1.7. Others

- 5.2. Market Analysis, Insights and Forecast - by Sensor Type

- 5.2.1. Radar Sensors

- 5.2.2. Camera Sensors

- 5.2.3. LiDAR Sensors

- 5.2.4. Ultrasonic Sensors

- 5.2.5. Infrared Sensors

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by LOA

- 5.3.1. L1

- 5.3.2. L2

- 5.3.3. L3

- 5.3.4. L4

- 5.3.5. L5

- 5.4. Market Analysis, Insights and Forecast - by Sales Channel

- 5.4.1. Passenger Cars

- 5.4.2. Light Commercial Vehicles (LCV)

- 5.4.3. Heavy Commercial Vehicles (HCV)

- 5.5. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.5.1. OEM

- 5.5.2. Sales Channel

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. North America

- 5.6.2. Europe

- 5.6.3. Asia Pacific

- 5.6.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by System Type

- 6. Global Automotive ADAS Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by System Type

- 6.1.1. Adaptive Cruise Control (ACC)

- 6.1.2. Automatic Emergency Braking (AEB)

- 6.1.3. Lane Departure Warning (LDW)

- 6.1.4. Blind Spot Detection (BSD).

- 6.1.5. Forward Collision Warning (FCW)

- 6.1.6. Driver Monitoring System (DMS)

- 6.1.7. Others

- 6.2. Market Analysis, Insights and Forecast - by Sensor Type

- 6.2.1. Radar Sensors

- 6.2.2. Camera Sensors

- 6.2.3. LiDAR Sensors

- 6.2.4. Ultrasonic Sensors

- 6.2.5. Infrared Sensors

- 6.2.6. Others

- 6.3. Market Analysis, Insights and Forecast - by LOA

- 6.3.1. L1

- 6.3.2. L2

- 6.3.3. L3

- 6.3.4. L4

- 6.3.5. L5

- 6.4. Market Analysis, Insights and Forecast - by Sales Channel

- 6.4.1. Passenger Cars

- 6.4.2. Light Commercial Vehicles (LCV)

- 6.4.3. Heavy Commercial Vehicles (HCV)

- 6.5. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.5.1. OEM

- 6.5.2. Sales Channel

- 6.1. Market Analysis, Insights and Forecast - by System Type

- 7. North America Automotive ADAS Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by System Type

- 7.1.1. Adaptive Cruise Control (ACC)

- 7.1.2. Automatic Emergency Braking (AEB)

- 7.1.3. Lane Departure Warning (LDW)

- 7.1.4. Blind Spot Detection (BSD).

- 7.1.5. Forward Collision Warning (FCW)

- 7.1.6. Driver Monitoring System (DMS)

- 7.1.7. Others

- 7.2. Market Analysis, Insights and Forecast - by Sensor Type

- 7.2.1. Radar Sensors

- 7.2.2. Camera Sensors

- 7.2.3. LiDAR Sensors

- 7.2.4. Ultrasonic Sensors

- 7.2.5. Infrared Sensors

- 7.2.6. Others

- 7.3. Market Analysis, Insights and Forecast - by LOA

- 7.3.1. L1

- 7.3.2. L2

- 7.3.3. L3

- 7.3.4. L4

- 7.3.5. L5

- 7.4. Market Analysis, Insights and Forecast - by Sales Channel

- 7.4.1. Passenger Cars

- 7.4.2. Light Commercial Vehicles (LCV)

- 7.4.3. Heavy Commercial Vehicles (HCV)

- 7.5. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.5.1. OEM

- 7.5.2. Sales Channel

- 7.1. Market Analysis, Insights and Forecast - by System Type

- 8. Europe Automotive ADAS Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by System Type

- 8.1.1. Adaptive Cruise Control (ACC)

- 8.1.2. Automatic Emergency Braking (AEB)

- 8.1.3. Lane Departure Warning (LDW)

- 8.1.4. Blind Spot Detection (BSD).

- 8.1.5. Forward Collision Warning (FCW)

- 8.1.6. Driver Monitoring System (DMS)

- 8.1.7. Others

- 8.2. Market Analysis, Insights and Forecast - by Sensor Type

- 8.2.1. Radar Sensors

- 8.2.2. Camera Sensors

- 8.2.3. LiDAR Sensors

- 8.2.4. Ultrasonic Sensors

- 8.2.5. Infrared Sensors

- 8.2.6. Others

- 8.3. Market Analysis, Insights and Forecast - by LOA

- 8.3.1. L1

- 8.3.2. L2

- 8.3.3. L3

- 8.3.4. L4

- 8.3.5. L5

- 8.4. Market Analysis, Insights and Forecast - by Sales Channel

- 8.4.1. Passenger Cars

- 8.4.2. Light Commercial Vehicles (LCV)

- 8.4.3. Heavy Commercial Vehicles (HCV)

- 8.5. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.5.1. OEM

- 8.5.2. Sales Channel

- 8.1. Market Analysis, Insights and Forecast - by System Type

- 9. Asia Pacific Automotive ADAS Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by System Type

- 9.1.1. Adaptive Cruise Control (ACC)

- 9.1.2. Automatic Emergency Braking (AEB)

- 9.1.3. Lane Departure Warning (LDW)

- 9.1.4. Blind Spot Detection (BSD).

- 9.1.5. Forward Collision Warning (FCW)

- 9.1.6. Driver Monitoring System (DMS)

- 9.1.7. Others

- 9.2. Market Analysis, Insights and Forecast - by Sensor Type

- 9.2.1. Radar Sensors

- 9.2.2. Camera Sensors

- 9.2.3. LiDAR Sensors

- 9.2.4. Ultrasonic Sensors

- 9.2.5. Infrared Sensors

- 9.2.6. Others

- 9.3. Market Analysis, Insights and Forecast - by LOA

- 9.3.1. L1

- 9.3.2. L2

- 9.3.3. L3

- 9.3.4. L4

- 9.3.5. L5

- 9.4. Market Analysis, Insights and Forecast - by Sales Channel

- 9.4.1. Passenger Cars

- 9.4.2. Light Commercial Vehicles (LCV)

- 9.4.3. Heavy Commercial Vehicles (HCV)

- 9.5. Market Analysis, Insights and Forecast - by Vehicle Type

- 9.5.1. OEM

- 9.5.2. Sales Channel

- 9.1. Market Analysis, Insights and Forecast - by System Type

- 10. Rest of the World Automotive ADAS Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by System Type

- 10.1.1. Adaptive Cruise Control (ACC)

- 10.1.2. Automatic Emergency Braking (AEB)

- 10.1.3. Lane Departure Warning (LDW)

- 10.1.4. Blind Spot Detection (BSD).

- 10.1.5. Forward Collision Warning (FCW)

- 10.1.6. Driver Monitoring System (DMS)

- 10.1.7. Others

- 10.2. Market Analysis, Insights and Forecast - by Sensor Type

- 10.2.1. Radar Sensors

- 10.2.2. Camera Sensors

- 10.2.3. LiDAR Sensors

- 10.2.4. Ultrasonic Sensors

- 10.2.5. Infrared Sensors

- 10.2.6. Others

- 10.3. Market Analysis, Insights and Forecast - by LOA

- 10.3.1. L1

- 10.3.2. L2

- 10.3.3. L3

- 10.3.4. L4

- 10.3.5. L5

- 10.4. Market Analysis, Insights and Forecast - by Sales Channel

- 10.4.1. Passenger Cars

- 10.4.2. Light Commercial Vehicles (LCV)

- 10.4.3. Heavy Commercial Vehicles (HCV)

- 10.5. Market Analysis, Insights and Forecast - by Vehicle Type

- 10.5.1. OEM

- 10.5.2. Sales Channel

- 10.1. Market Analysis, Insights and Forecast - by System Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Mobileye

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Hyundai Mobis

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Infineon Technologies

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Delphi Automotive

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Aisin Seiki Co Ltd

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Continental AG

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Autoliv Inc

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Robert Bosch GmbH

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Hella KGAA Hueck & Co

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Magna International

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 Valeo SA

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 DENSO Corporation

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.13 WABCO Vehicle Control Services

- 11.1.13.1. Company Overview

- 11.1.13.2. Products

- 11.1.13.3. Company Financials

- 11.1.13.4. SWOT Analysis

- 11.1.14 ZF Friedrichshafen AG

- 11.1.14.1. Company Overview

- 11.1.14.2. Products

- 11.1.14.3. Company Financials

- 11.1.14.4. SWOT Analysis

- 11.1.1 Mobileye

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Automotive ADAS Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Automotive ADAS Industry Revenue (Million), by System Type 2025 & 2033

- Figure 3: North America Automotive ADAS Industry Revenue Share (%), by System Type 2025 & 2033

- Figure 4: North America Automotive ADAS Industry Revenue (Million), by Sensor Type 2025 & 2033

- Figure 5: North America Automotive ADAS Industry Revenue Share (%), by Sensor Type 2025 & 2033

- Figure 6: North America Automotive ADAS Industry Revenue (Million), by LOA 2025 & 2033

- Figure 7: North America Automotive ADAS Industry Revenue Share (%), by LOA 2025 & 2033

- Figure 8: North America Automotive ADAS Industry Revenue (Million), by Sales Channel 2025 & 2033

- Figure 9: North America Automotive ADAS Industry Revenue Share (%), by Sales Channel 2025 & 2033

- Figure 10: North America Automotive ADAS Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 11: North America Automotive ADAS Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 12: North America Automotive ADAS Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: North America Automotive ADAS Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive ADAS Industry Revenue (Million), by System Type 2025 & 2033

- Figure 15: Europe Automotive ADAS Industry Revenue Share (%), by System Type 2025 & 2033

- Figure 16: Europe Automotive ADAS Industry Revenue (Million), by Sensor Type 2025 & 2033

- Figure 17: Europe Automotive ADAS Industry Revenue Share (%), by Sensor Type 2025 & 2033

- Figure 18: Europe Automotive ADAS Industry Revenue (Million), by LOA 2025 & 2033

- Figure 19: Europe Automotive ADAS Industry Revenue Share (%), by LOA 2025 & 2033

- Figure 20: Europe Automotive ADAS Industry Revenue (Million), by Sales Channel 2025 & 2033

- Figure 21: Europe Automotive ADAS Industry Revenue Share (%), by Sales Channel 2025 & 2033

- Figure 22: Europe Automotive ADAS Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 23: Europe Automotive ADAS Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 24: Europe Automotive ADAS Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Europe Automotive ADAS Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive ADAS Industry Revenue (Million), by System Type 2025 & 2033

- Figure 27: Asia Pacific Automotive ADAS Industry Revenue Share (%), by System Type 2025 & 2033

- Figure 28: Asia Pacific Automotive ADAS Industry Revenue (Million), by Sensor Type 2025 & 2033

- Figure 29: Asia Pacific Automotive ADAS Industry Revenue Share (%), by Sensor Type 2025 & 2033

- Figure 30: Asia Pacific Automotive ADAS Industry Revenue (Million), by LOA 2025 & 2033

- Figure 31: Asia Pacific Automotive ADAS Industry Revenue Share (%), by LOA 2025 & 2033

- Figure 32: Asia Pacific Automotive ADAS Industry Revenue (Million), by Sales Channel 2025 & 2033

- Figure 33: Asia Pacific Automotive ADAS Industry Revenue Share (%), by Sales Channel 2025 & 2033

- Figure 34: Asia Pacific Automotive ADAS Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 35: Asia Pacific Automotive ADAS Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 36: Asia Pacific Automotive ADAS Industry Revenue (Million), by Country 2025 & 2033

- Figure 37: Asia Pacific Automotive ADAS Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Rest of the World Automotive ADAS Industry Revenue (Million), by System Type 2025 & 2033

- Figure 39: Rest of the World Automotive ADAS Industry Revenue Share (%), by System Type 2025 & 2033

- Figure 40: Rest of the World Automotive ADAS Industry Revenue (Million), by Sensor Type 2025 & 2033

- Figure 41: Rest of the World Automotive ADAS Industry Revenue Share (%), by Sensor Type 2025 & 2033

- Figure 42: Rest of the World Automotive ADAS Industry Revenue (Million), by LOA 2025 & 2033

- Figure 43: Rest of the World Automotive ADAS Industry Revenue Share (%), by LOA 2025 & 2033

- Figure 44: Rest of the World Automotive ADAS Industry Revenue (Million), by Sales Channel 2025 & 2033

- Figure 45: Rest of the World Automotive ADAS Industry Revenue Share (%), by Sales Channel 2025 & 2033

- Figure 46: Rest of the World Automotive ADAS Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 47: Rest of the World Automotive ADAS Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 48: Rest of the World Automotive ADAS Industry Revenue (Million), by Country 2025 & 2033

- Figure 49: Rest of the World Automotive ADAS Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive ADAS Industry Revenue Million Forecast, by System Type 2020 & 2033

- Table 2: Global Automotive ADAS Industry Revenue Million Forecast, by Sensor Type 2020 & 2033

- Table 3: Global Automotive ADAS Industry Revenue Million Forecast, by LOA 2020 & 2033

- Table 4: Global Automotive ADAS Industry Revenue Million Forecast, by Sales Channel 2020 & 2033

- Table 5: Global Automotive ADAS Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 6: Global Automotive ADAS Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 7: Global Automotive ADAS Industry Revenue Million Forecast, by System Type 2020 & 2033

- Table 8: Global Automotive ADAS Industry Revenue Million Forecast, by Sensor Type 2020 & 2033

- Table 9: Global Automotive ADAS Industry Revenue Million Forecast, by LOA 2020 & 2033

- Table 10: Global Automotive ADAS Industry Revenue Million Forecast, by Sales Channel 2020 & 2033

- Table 11: Global Automotive ADAS Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 12: Global Automotive ADAS Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: United States Automotive ADAS Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Canada Automotive ADAS Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Mexico Automotive ADAS Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Rest of North America Automotive ADAS Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Global Automotive ADAS Industry Revenue Million Forecast, by System Type 2020 & 2033

- Table 18: Global Automotive ADAS Industry Revenue Million Forecast, by Sensor Type 2020 & 2033

- Table 19: Global Automotive ADAS Industry Revenue Million Forecast, by LOA 2020 & 2033

- Table 20: Global Automotive ADAS Industry Revenue Million Forecast, by Sales Channel 2020 & 2033

- Table 21: Global Automotive ADAS Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 22: Global Automotive ADAS Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 23: Germany Automotive ADAS Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: United Kingdom Automotive ADAS Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: France Automotive ADAS Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Italy Automotive ADAS Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Russia Automotive ADAS Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Rest of Europe Automotive ADAS Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Global Automotive ADAS Industry Revenue Million Forecast, by System Type 2020 & 2033

- Table 30: Global Automotive ADAS Industry Revenue Million Forecast, by Sensor Type 2020 & 2033

- Table 31: Global Automotive ADAS Industry Revenue Million Forecast, by LOA 2020 & 2033

- Table 32: Global Automotive ADAS Industry Revenue Million Forecast, by Sales Channel 2020 & 2033

- Table 33: Global Automotive ADAS Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 34: Global Automotive ADAS Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 35: China Automotive ADAS Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Japan Automotive ADAS Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: India Automotive ADAS Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: South Korea Automotive ADAS Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: Australia Automotive ADAS Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Rest of Asia Pacific Automotive ADAS Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 41: Global Automotive ADAS Industry Revenue Million Forecast, by System Type 2020 & 2033

- Table 42: Global Automotive ADAS Industry Revenue Million Forecast, by Sensor Type 2020 & 2033

- Table 43: Global Automotive ADAS Industry Revenue Million Forecast, by LOA 2020 & 2033

- Table 44: Global Automotive ADAS Industry Revenue Million Forecast, by Sales Channel 2020 & 2033

- Table 45: Global Automotive ADAS Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 46: Global Automotive ADAS Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 47: South America Automotive ADAS Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 48: Middle East and Africa Automotive ADAS Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive ADAS Industry?

The projected CAGR is approximately 16.70%.

2. Which companies are prominent players in the Automotive ADAS Industry?

Key companies in the market include Mobileye, Hyundai Mobis, Infineon Technologies, Delphi Automotive, Aisin Seiki Co Ltd, Continental AG, Autoliv Inc, Robert Bosch GmbH, Hella KGAA Hueck & Co, Magna International, Valeo SA, DENSO Corporation, WABCO Vehicle Control Services, ZF Friedrichshafen AG.

3. What are the main segments of the Automotive ADAS Industry?

The market segments include System Type, Sensor Type, LOA, Sales Channel, Vehicle Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 49.65 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Sales of Autonomous Vehicles.

6. What are the notable trends driving market growth?

Passenger Cars Hold the Highest Market Share.

7. Are there any restraints impacting market growth?

High Cost of Installation Related to ADAS Systems.

8. Can you provide examples of recent developments in the market?

December 2023: ECARX Holdings Inc., a global mobility technology provider, partnered with Black Sesame Technologies and BlackBerry Limited to deploy the Skyland ADAS platform in Lynk & Co’s flagship SUV, the Lynk & Co 08. This collaboration involves the integration of BlackBerry QNX Neutrino Real-Time Operating System (RTOS) and Black Sesame Technologies’ Huashan II A1000 ADAS computing chip in the ECARX Skyland Pro.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive ADAS Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive ADAS Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive ADAS Industry?

To stay informed about further developments, trends, and reports in the Automotive ADAS Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence