Key Insights

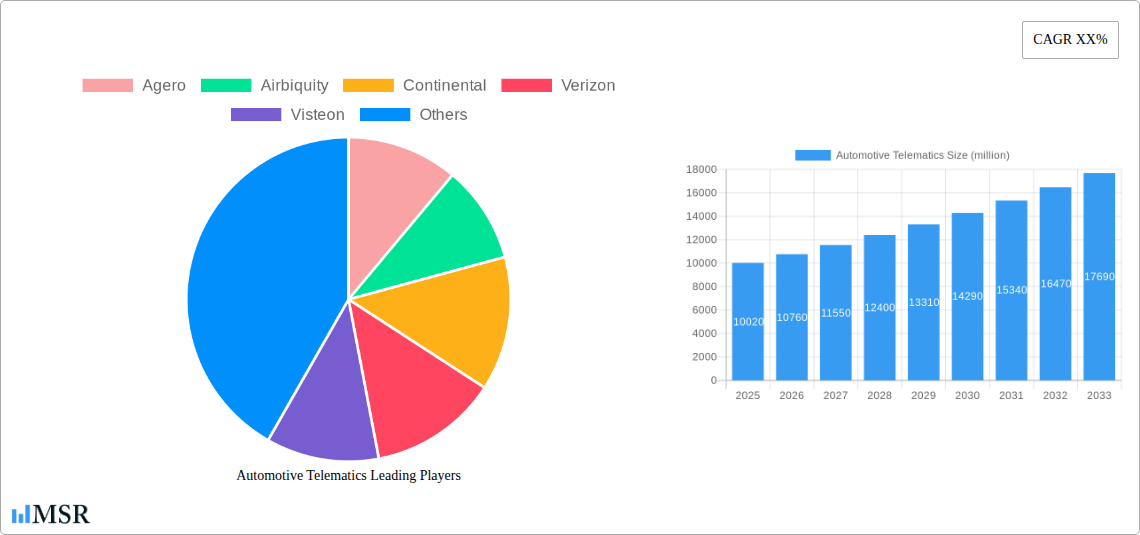

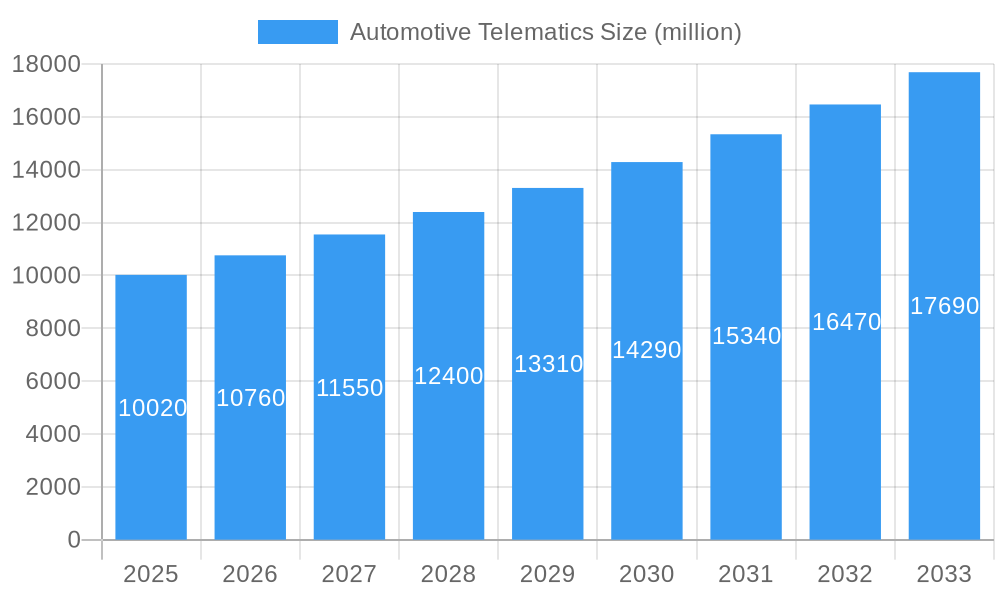

The global Automotive Telematics market is poised for significant expansion, projected to reach $10.02 billion in 2025. This robust growth is fueled by a projected compound annual growth rate (CAGR) of 7.6% over the forecast period of 2025-2033. Key drivers propelling this market include the increasing adoption of connected vehicle technologies, the growing demand for advanced safety and security features, and the rising integration of IoT solutions within the automotive sector. Furthermore, the burgeoning popularity of subscription-based services for navigation, entertainment, and real-time diagnostics is creating new revenue streams and enhancing consumer value. The market's evolution is also shaped by stringent government regulations mandating the inclusion of eCall systems and other safety telematics in new vehicles, further bolstering its trajectory.

Automotive Telematics Market Size (In Billion)

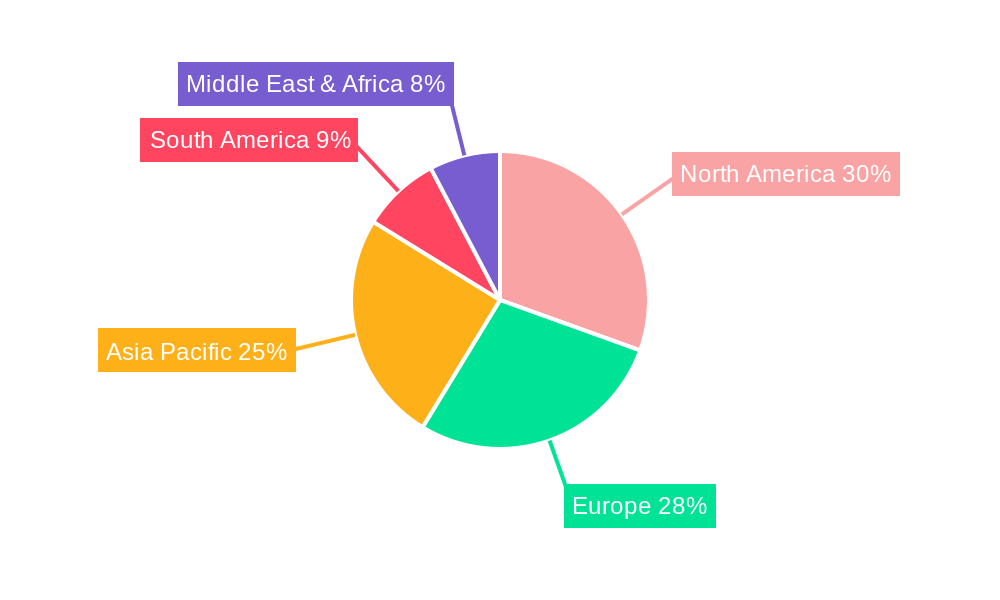

The Automotive Telematics market is segmented across various applications, with Passenger Cars dominating due to their widespread adoption and the rapid integration of advanced features. Light Commercial Vehicles (LCVs) and Heavy Commercial Vehicles (HCVs) are also significant segments, driven by fleet management solutions, route optimization, and the need for enhanced operational efficiency. On the technology front, Plug and Play Telematics are gaining traction for their ease of installation and adaptability, while Hardwired Install Telematics offer greater reliability and comprehensive data capture for commercial fleets. Geographically, North America and Europe are expected to lead the market in the initial years, driven by early adoption of advanced technologies and supportive regulatory frameworks. However, the Asia Pacific region, particularly China and India, is anticipated to witness the fastest growth due to its rapidly expanding automotive industry and increasing consumer disposable income. Restraints, such as data privacy concerns and the initial cost of implementation, are being addressed through technological advancements and evolving business models.

Automotive Telematics Company Market Share

This comprehensive Automotive Telematics Market Report delves deep into the intricate dynamics, burgeoning trends, and future trajectory of the global automotive telematics industry. Covering a study period from 2019 to 2033, with a base and estimated year of 2025, this report offers invaluable insights for industry stakeholders, including vehicle manufacturers, telematics solution providers, fleet operators, and investors. We dissect market concentration, analyze technological disruptions, identify key market segments, and outline strategic growth opportunities. With an estimated market size projected to exceed XX billion by 2033, this report is your definitive guide to navigating the evolving automotive landscape.

Automotive Telematics Market Concentration & Dynamics

The global automotive telematics market exhibits a dynamic landscape characterized by moderate concentration. Leading players like Agero, Airbiquity, Continental, Verizon, Visteon, Trimble, Masternaut, TomTom International, and Telogis are actively shaping the industry through strategic collaborations and product innovations. The market's innovation ecosystem thrives on the integration of Artificial Intelligence (AI), Internet of Things (IoT), and 5G technologies, driving the development of advanced safety, navigation, and fleet management solutions. Regulatory frameworks, particularly those pertaining to data privacy and vehicle security, are increasingly influencing market development. The presence of substitute products, such as standalone GPS devices, is diminishing as integrated telematics solutions offer superior functionality and connectivity. End-user trends are heavily skewed towards enhanced safety features, real-time vehicle diagnostics, and efficient fleet management, particularly within the commercial vehicle segment. Mergers and Acquisition (M&A) activities, with an estimated XX count of significant deals in the historical period (2019-2024), indicate a consolidation phase aimed at expanding market reach and technological capabilities.

Automotive Telematics Industry Insights & Trends

The automotive telematics industry is poised for substantial growth, driven by a confluence of technological advancements, evolving consumer expectations, and increasing adoption of connected vehicle technologies. The global market size is projected to reach an impressive XX billion by 2033, growing at a Compound Annual Growth Rate (CAGR) of approximately XX% during the forecast period (2025-2033). Key market growth drivers include the burgeoning demand for advanced driver-assistance systems (ADAS), the imperative for enhanced vehicle safety and security, and the growing need for efficient fleet management solutions across commercial sectors. Technological disruptions, such as the widespread deployment of 5G networks, are enabling faster data transmission and more sophisticated real-time services, including predictive maintenance and over-the-air (OTA) updates. Evolving consumer behaviors are also playing a pivotal role, with drivers increasingly expecting seamless integration of their digital lives into their vehicles, demanding personalized infotainment, proactive vehicle health monitoring, and on-demand services. The rise of electric vehicles (EVs) further amplifies the need for telematics for battery management, charging optimization, and range prediction. Furthermore, the increasing focus on data-driven insights for insurance telematics and usage-based insurance (UBI) models is creating new revenue streams and driving innovation. The integration of AI and machine learning is enhancing predictive capabilities, enabling more accurate diagnostics and proactive safety interventions. The expansion of the shared mobility sector, including car-sharing and ride-hailing services, also necessitates robust telematics solutions for fleet tracking, management, and user experience enhancement. The growing emphasis on sustainability and environmental compliance is also pushing the demand for telematics solutions that can monitor fuel efficiency and emissions.

Key Markets & Segments Leading Automotive Telematics

The Passenger Car segment is a dominant force in the automotive telematics market, driven by escalating consumer demand for safety, convenience, and connected services. In this segment, Plug and Play Telematics solutions are gaining significant traction due to their ease of installation and immediate functionality, appealing to a broad consumer base. The economic growth in developed and developing nations, coupled with rising disposable incomes, directly fuels the demand for new passenger vehicles equipped with advanced telematics features. Infrastructure development, including better road networks and widespread mobile connectivity, further supports the seamless operation of telematics systems. The growing awareness among consumers about the safety benefits offered by telematics, such as real-time accident detection and emergency assistance, is a key driver. Additionally, the integration of telematics with infotainment systems and mobile applications is enhancing the user experience, making connected car features a must-have rather than a luxury.

Within the commercial vehicle sector, the LCV-Light Commercial Vehicle segment is experiencing robust growth, fueled by the expansion of e-commerce and last-mile delivery services. For LCVs, both Plug and Play Telematics and Hardwired Install Telematics find application, with the choice often depending on the specific fleet management needs and operational complexity. The increasing need for efficient route optimization, real-time fleet tracking, and driver behavior monitoring to reduce operational costs and improve delivery times are paramount. Government initiatives promoting efficient logistics and reducing carbon emissions also indirectly boost the adoption of telematics in LCVs.

The HCV-Heavy Commercial Vehicle segment is a critical area for Hardwired Install Telematics, owing to its requirement for robust, integrated, and tamper-proof solutions for long-haul operations. Drivers in this segment include stringent regulatory compliance for driver hours, fuel efficiency mandates, and the critical need for enhanced safety and security of high-value cargo. The telematics solutions in HCVs enable sophisticated fleet management, including predictive maintenance, real-time diagnostics, and advanced driver monitoring systems (e.g., fatigue detection). The expansion of global trade and supply chains necessitates efficient and reliable transportation, making telematics indispensable for optimizing fleet performance and minimizing downtime. The economic viability of telematics in HCVs is further underscored by significant cost savings achieved through fuel optimization, reduced maintenance, and improved driver safety.

Automotive Telematics Product Developments

Product innovation in automotive telematics is rapidly advancing, focusing on seamless integration and enhanced functionality. Key developments include the rollout of AI-powered predictive maintenance systems that anticipate vehicle failures, reducing downtime and repair costs. Advanced driver monitoring systems (ADMS) are incorporating sophisticated sensors and algorithms to detect driver fatigue and distraction, significantly improving road safety. The increasing integration of telematics with in-vehicle infotainment systems provides drivers with enhanced navigation, personalized content, and seamless connectivity. Over-the-air (OTA) software updates are becoming standard, allowing manufacturers to remotely improve vehicle performance, fix bugs, and introduce new features without requiring physical dealership visits. The development of specialized telematics solutions for electric vehicles (EVs), focusing on battery health monitoring, charging management, and range optimization, is a significant trend. These product advancements are driven by the need for safer, more efficient, and more connected vehicles, providing a competitive edge to companies that can deliver these cutting-edge solutions.

Challenges in the Automotive Telematics Market

The automotive telematics market faces several significant challenges that temper its growth. Data security and privacy concerns remain a paramount hurdle, with consumers and regulators alike demanding robust safeguards for sensitive vehicle and personal data. The high cost of implementation for advanced telematics solutions, particularly for smaller fleet operators and individual consumers, can be a deterrent. Interoperability issues between different telematics platforms and vehicle manufacturers' proprietary systems can create fragmentation and hinder seamless integration. Furthermore, the evolving regulatory landscape, with differing data privacy laws across various regions, adds complexity to global deployment. Supply chain disruptions, particularly in the semiconductor industry, can impact the availability of essential components for telematics hardware. Competitive pressures from a crowded market also necessitate continuous innovation and cost optimization.

Forces Driving Automotive Telematics Growth

Several powerful forces are propelling the growth of the automotive telematics market. The increasing demand for enhanced vehicle safety and security is a primary driver, with features like real-time accident detection, emergency calling (eCall), and vehicle tracking becoming standard expectations. The growing adoption of connected car technologies and the rise of the Internet of Things (IoT) ecosystem are creating new opportunities for telematics integration. Stringent government regulations mandating safety features and promoting efficient transportation further fuel market expansion. The economic benefits of fleet management optimization, including fuel savings, reduced downtime, and improved driver productivity, are compelling for commercial vehicle operators. The advancements in telecommunication technologies, such as 5G, are enabling faster data transfer and more sophisticated real-time services, making telematics more powerful and accessible.

Challenges in the Automotive Telematics Market

Long-term growth catalysts in the automotive telematics market are deeply intertwined with continuous technological innovation and strategic market expansion. The evolution of AI and machine learning will unlock advanced capabilities in areas like predictive diagnostics, personalized driver behavior coaching, and autonomous driving support. Strategic partnerships between telematics providers, automakers, and third-party service providers will foster richer ecosystems of connected services. Market expansions into emerging economies, driven by increasing vehicle ownership and the need for advanced mobility solutions, represent a significant growth avenue. Furthermore, the development of standardized telematics architectures and data protocols will facilitate broader adoption and reduce integration complexities, paving the way for a more unified and efficient connected vehicle landscape. The increasing focus on sustainability and green mobility will also drive demand for telematics solutions that optimize EV performance and reduce emissions.

Emerging Opportunities in Automotive Telematics

Emerging opportunities in the automotive telematics sector are vast and transformative. The burgeoning usage-based insurance (UBI) market presents a significant avenue for growth, leveraging telematics data to offer personalized insurance premiums. The expansion of the mobility-as-a-service (MaaS) landscape, including ride-sharing and car-sharing platforms, necessitates robust telematics for fleet management, tracking, and user experience enhancement. The integration of telematics with smart city initiatives, enabling V2X (Vehicle-to-Everything) communication, promises to revolutionize traffic management, safety, and urban planning. The development of advanced driver-assistance systems (ADAS) and the gradual progression towards autonomous driving will rely heavily on sophisticated telematics for data processing, communication, and real-time decision-making. The growing demand for personalized in-car experiences, including tailored content delivery and proactive vehicle diagnostics, also opens new service-based opportunities.

Leading Players in the Automotive Telematics Sector

- Agero

- Airbiquity

- Continental

- Verizon

- Visteon

- Trimble

- Masternaut

- TomTom International

- Telogis

Key Milestones in Automotive Telematics Industry

- 2019: Increased adoption of eCall systems in new vehicle models across Europe, mandating emergency assistance.

- 2020: Significant growth in fleet management telematics solutions driven by e-commerce and last-mile delivery demands.

- 2021: Advancements in 5G technology paving the way for faster data transmission and real-time vehicle-to-infrastructure (V2I) communication.

- 2022: Expansion of usage-based insurance (UBI) programs, leveraging telematics for personalized policy offerings.

- 2023: Increased focus on cybersecurity for connected vehicles and telematics data protection.

- 2024: Growing integration of AI and machine learning for predictive maintenance and advanced driver assistance.

- 2025 (Estimated): Widespread adoption of advanced telematics features in electric vehicles (EVs) for battery management and charging optimization.

- 2026-2030: Potential for increased V2X communication implementation and integration with smart city infrastructure.

- 2031-2033: Maturation of autonomous driving technology heavily reliant on advanced telematics for real-time data and decision-making.

Strategic Outlook for Automotive Telematics Market

The strategic outlook for the automotive telematics market is exceptionally positive, driven by an unwavering demand for safer, more efficient, and intelligently connected vehicles. Growth accelerators include the continued integration of AI and IoT, enabling sophisticated predictive analytics and personalized user experiences. Strategic partnerships between telematics providers, automakers, and technology companies will be crucial for developing comprehensive ecosystems of connected services. Furthermore, expansion into emerging markets and the development of tailored solutions for specific vehicle segments, such as electric and autonomous vehicles, will unlock significant new revenue streams. The focus on data-driven insights for insurance, fleet management, and enhanced driver safety will continue to be a cornerstone of market growth. The industry's ability to address evolving regulatory landscapes and cybersecurity concerns will be paramount for sustained success.

Automotive Telematics Segmentation

-

1. Application

- 1.1. Passenger Car

- 1.2. LCV-Light Commercial Vehicle

- 1.3. HCV-Heavy Commercial Vehicle

-

2. Types

- 2.1. Plug and Play Telematics

- 2.2. Hardwired Install Telematics

Automotive Telematics Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Telematics Regional Market Share

Geographic Coverage of Automotive Telematics

Automotive Telematics REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Car

- 5.1.2. LCV-Light Commercial Vehicle

- 5.1.3. HCV-Heavy Commercial Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Plug and Play Telematics

- 5.2.2. Hardwired Install Telematics

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Automotive Telematics Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Car

- 6.1.2. LCV-Light Commercial Vehicle

- 6.1.3. HCV-Heavy Commercial Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Plug and Play Telematics

- 6.2.2. Hardwired Install Telematics

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Automotive Telematics Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Car

- 7.1.2. LCV-Light Commercial Vehicle

- 7.1.3. HCV-Heavy Commercial Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Plug and Play Telematics

- 7.2.2. Hardwired Install Telematics

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Automotive Telematics Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Car

- 8.1.2. LCV-Light Commercial Vehicle

- 8.1.3. HCV-Heavy Commercial Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Plug and Play Telematics

- 8.2.2. Hardwired Install Telematics

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Automotive Telematics Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Car

- 9.1.2. LCV-Light Commercial Vehicle

- 9.1.3. HCV-Heavy Commercial Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Plug and Play Telematics

- 9.2.2. Hardwired Install Telematics

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Automotive Telematics Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Car

- 10.1.2. LCV-Light Commercial Vehicle

- 10.1.3. HCV-Heavy Commercial Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Plug and Play Telematics

- 10.2.2. Hardwired Install Telematics

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Automotive Telematics Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Passenger Car

- 11.1.2. LCV-Light Commercial Vehicle

- 11.1.3. HCV-Heavy Commercial Vehicle

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Plug and Play Telematics

- 11.2.2. Hardwired Install Telematics

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Agero

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Airbiquity

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Continental

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Verizon

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Visteon

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Trimble

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Masternaut

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 TomTom International

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Telogis

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.1 Agero

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Automotive Telematics Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Automotive Telematics Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Automotive Telematics Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive Telematics Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Automotive Telematics Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Automotive Telematics Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Automotive Telematics Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive Telematics Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Automotive Telematics Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive Telematics Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Automotive Telematics Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Automotive Telematics Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Automotive Telematics Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive Telematics Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Automotive Telematics Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive Telematics Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Automotive Telematics Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Automotive Telematics Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Automotive Telematics Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive Telematics Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive Telematics Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive Telematics Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Automotive Telematics Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Automotive Telematics Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive Telematics Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive Telematics Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive Telematics Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive Telematics Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Automotive Telematics Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Automotive Telematics Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive Telematics Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Telematics Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Telematics Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Automotive Telematics Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Automotive Telematics Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Automotive Telematics Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Automotive Telematics Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive Telematics Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Automotive Telematics Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Automotive Telematics Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Telematics Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Automotive Telematics Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Automotive Telematics Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive Telematics Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Automotive Telematics Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Automotive Telematics Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive Telematics Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Automotive Telematics Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Automotive Telematics Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive Telematics Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Telematics?

The projected CAGR is approximately 7.6%.

2. Which companies are prominent players in the Automotive Telematics?

Key companies in the market include Agero, Airbiquity, Continental, Verizon, Visteon, Trimble, Masternaut, TomTom International, Telogis.

3. What are the main segments of the Automotive Telematics?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 10.02 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Telematics," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Telematics report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Telematics?

To stay informed about further developments, trends, and reports in the Automotive Telematics, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence